Period: 30 January – 5 February 2021

Top news story: The main news this week naturally continues the news of last week – the stock market scandal. In January, the USA Mint sold 220,500 gold coins «American Eagle», which is 290% more than the year before. Physical gold is clearly in short supply, and this is causing the dollar system serious difficulties. In fact, we have a gradual return of gold to the position of the General-Purpose Equivalent (GPE).

Let us note that this process was described already in 2003 in the book A.Kobyakov and M.Khazin «Sunset dollar empire and the end of the «Pax Americana», however it proceeded rather slowly, sometimes interrupted by long rolls. Gold prices have, however, increased very significantly since 2003, and there is every reason to believe that this process will continue as the GPE changes and the United States dollar moves away from these positions.

Macroeconomics

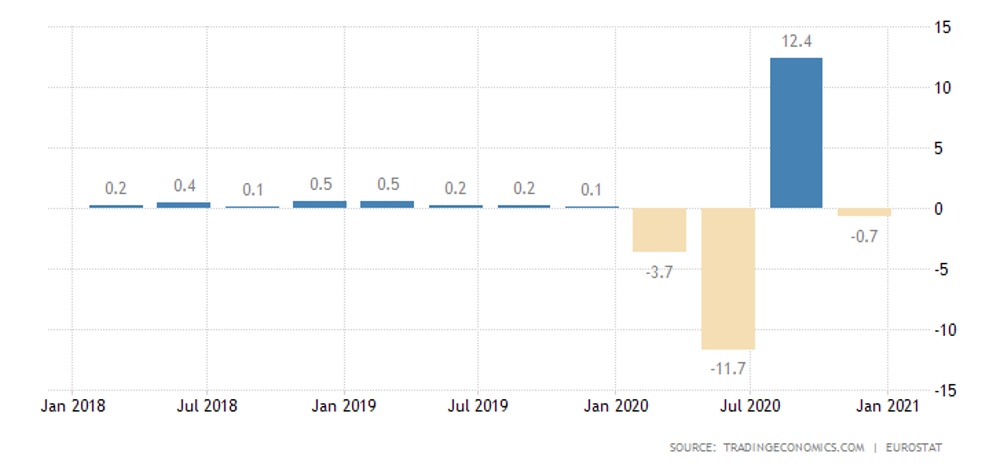

The Euro Area GDP in the fourth quarter went into quarterly losses:

As a result, the annual decline increased from -4,3% to -5,1%.

Indonesia’s GDP as a whole slumped by 2,1% in 2020.

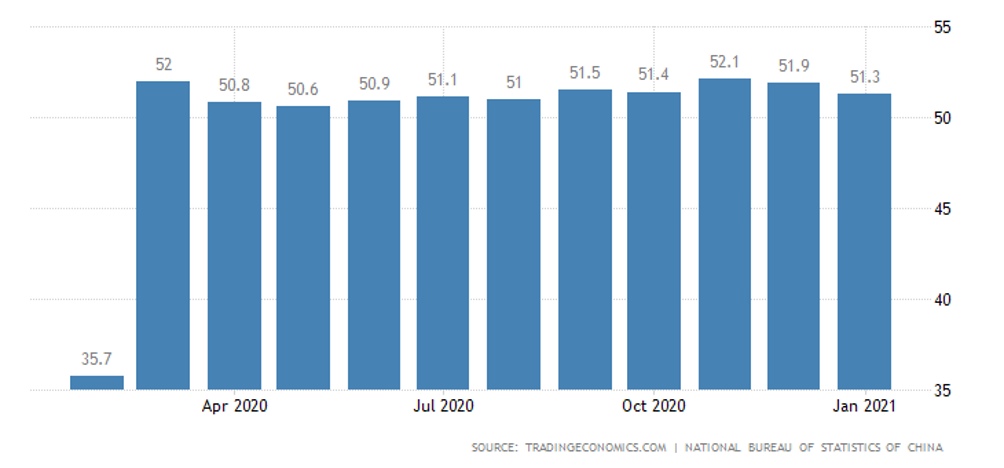

China NBS Manufacturing PMI is the worst since August 2020:

Let’s remind that PMI is the industry’s assessment coefficient. Its value above 50 means growth, below 50 means decline.

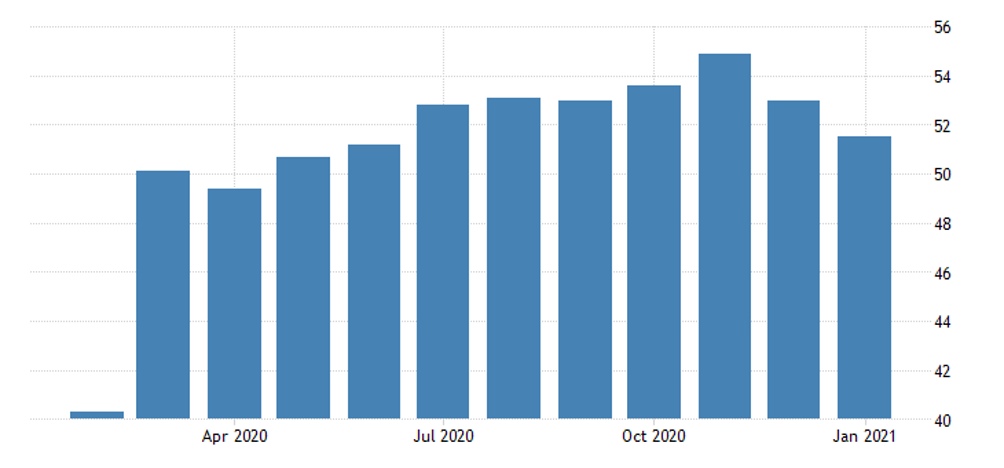

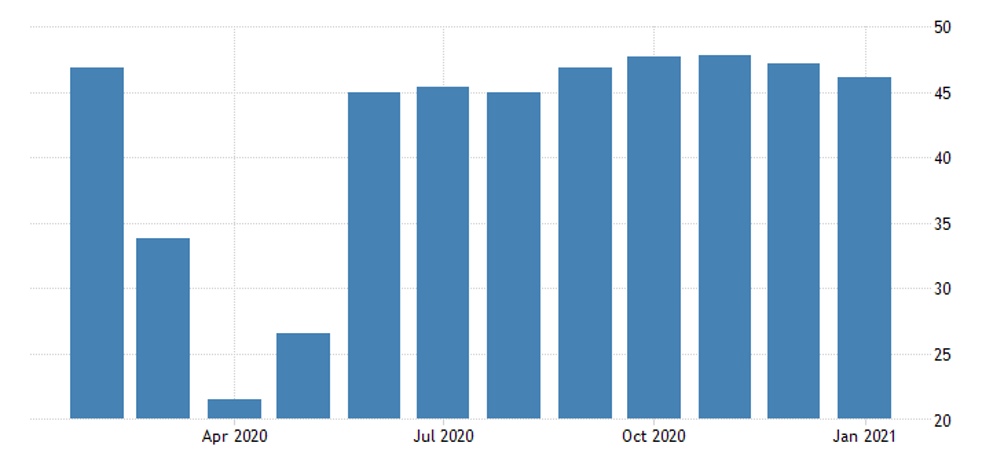

In the service sector, the situation is worse, at least since March, rather than taking into account the February failure of 2020 – even since 2009:

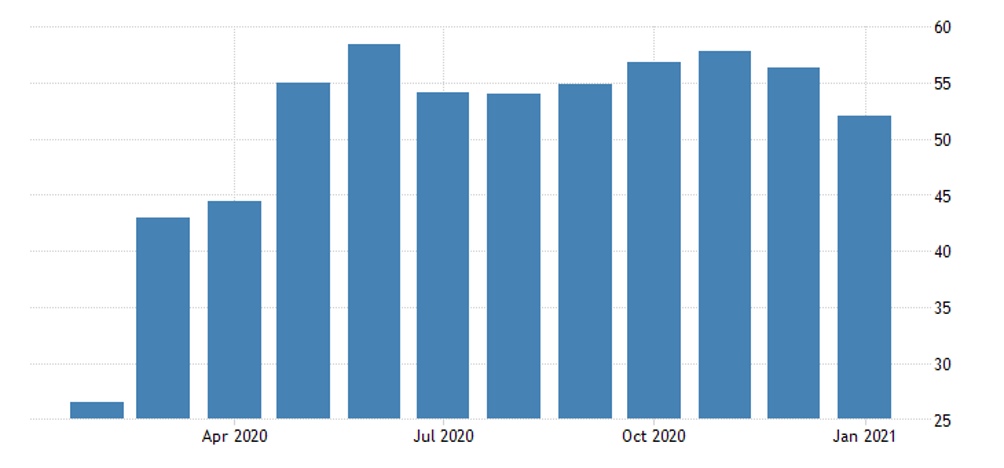

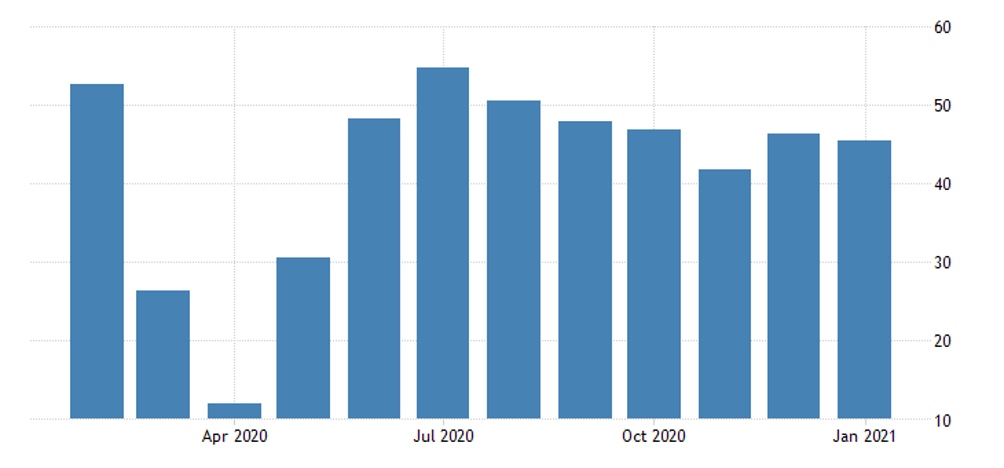

A private study confirms the weakness of both industry and services:

Japan, too, is experiencing a slowdown:

And in the Euro Area:

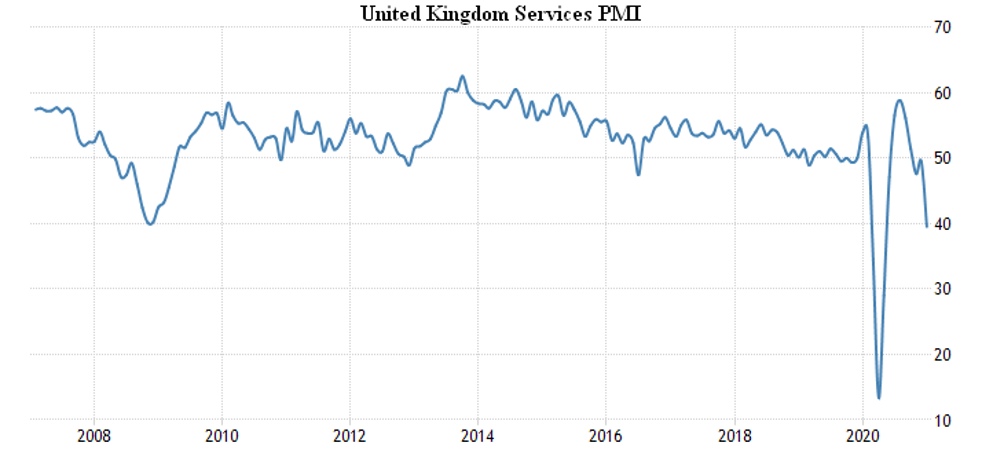

This is most evident in Britain:

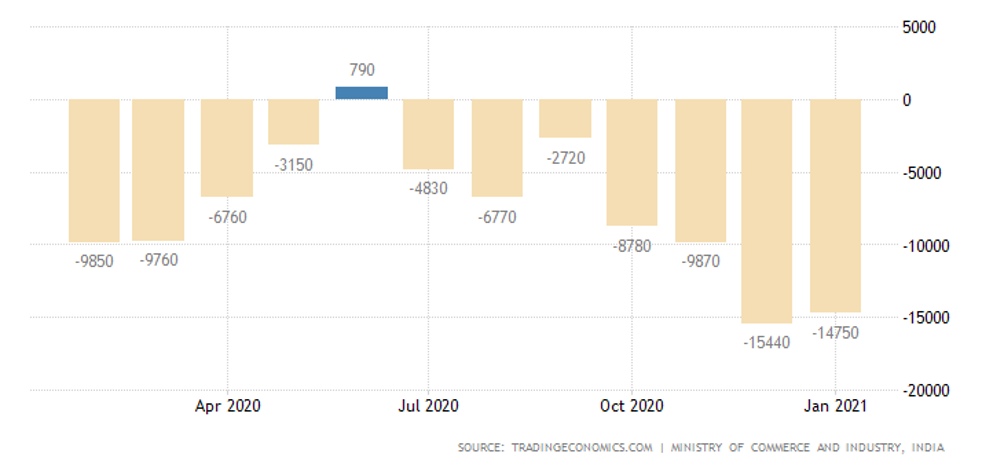

India’s trade deficit remains close to record peaks:

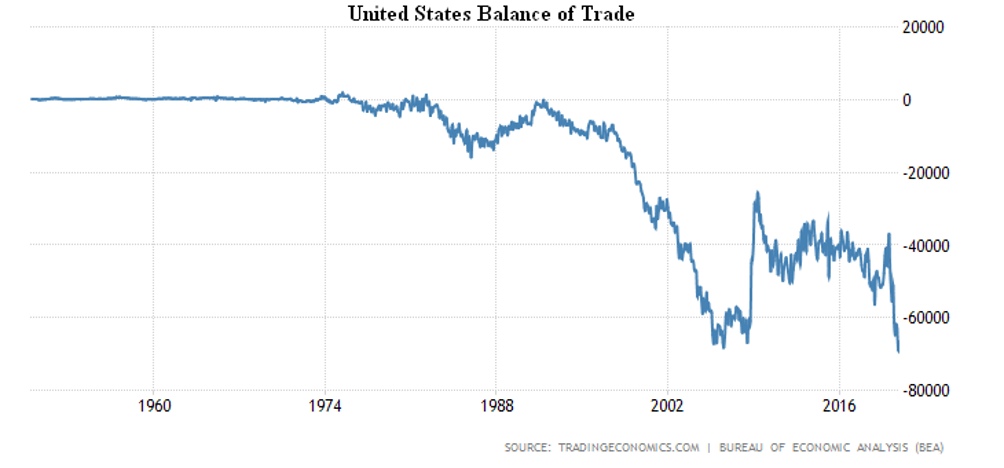

Just like in the U.S.:

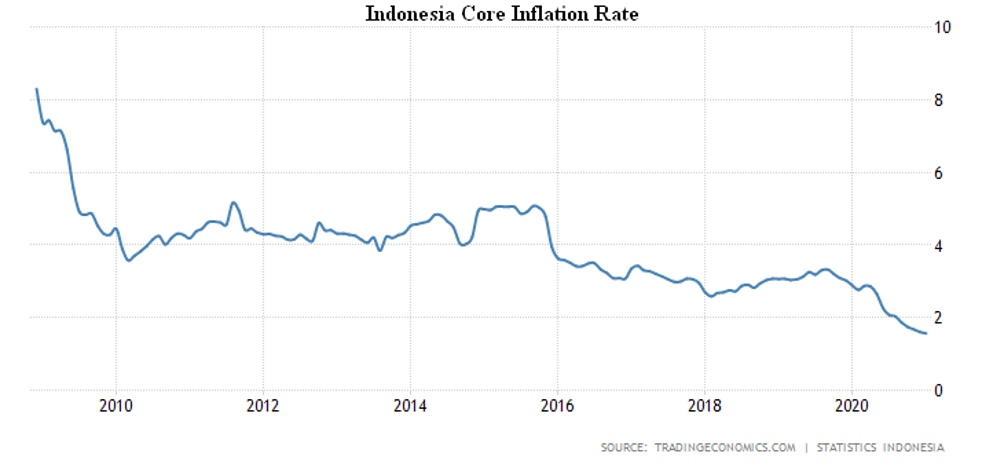

Core inflation in Indonesia is minimal for the entire history of the survey (+1,56%):

In Turkey, the CPI continues to gain speed, as does the PPI:

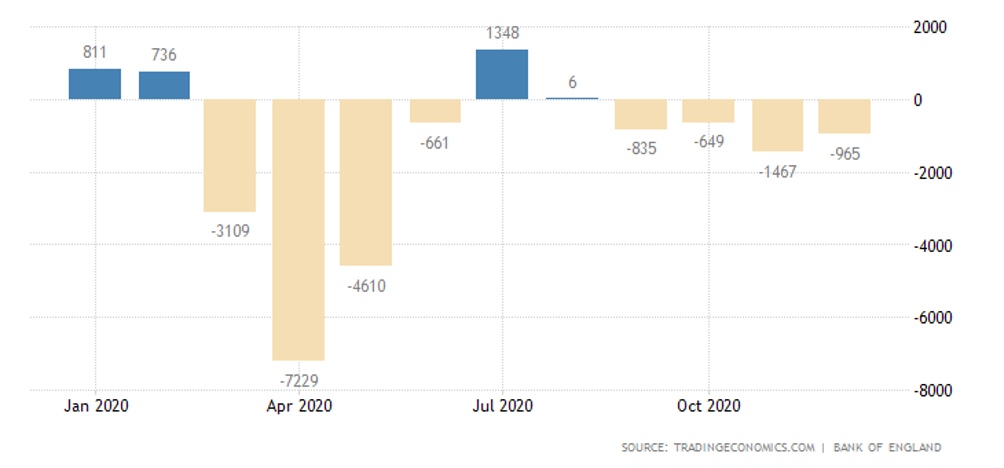

In Britain, consumer credit continues to decline:

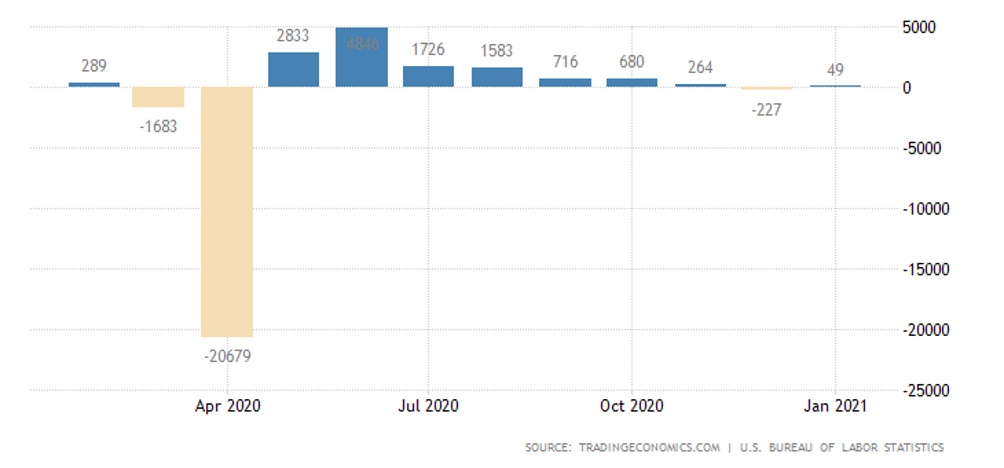

The number of jobs in the US rose slightly in January, but made up only one fifth of the losses in December; employment remains at 10 million below the peak of February 2020, the proportion of job seekers seeking work longer than six months is the highest since 2012 (39,5%):

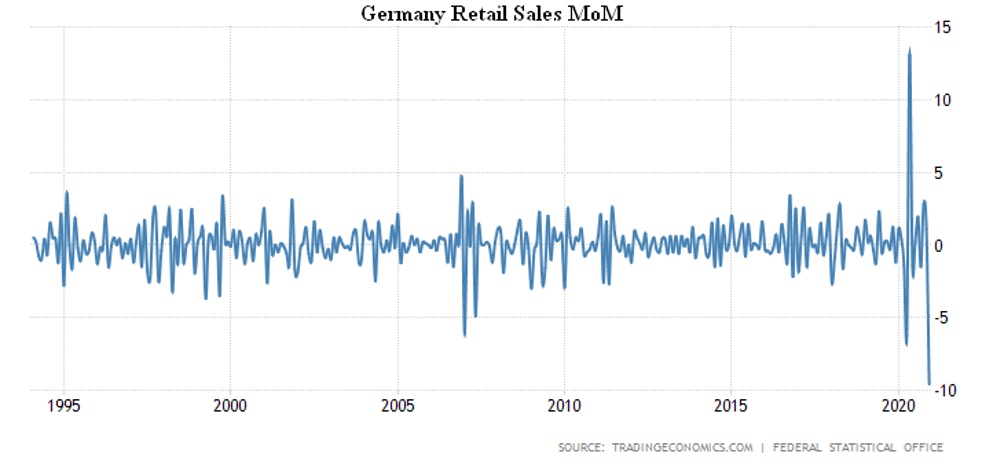

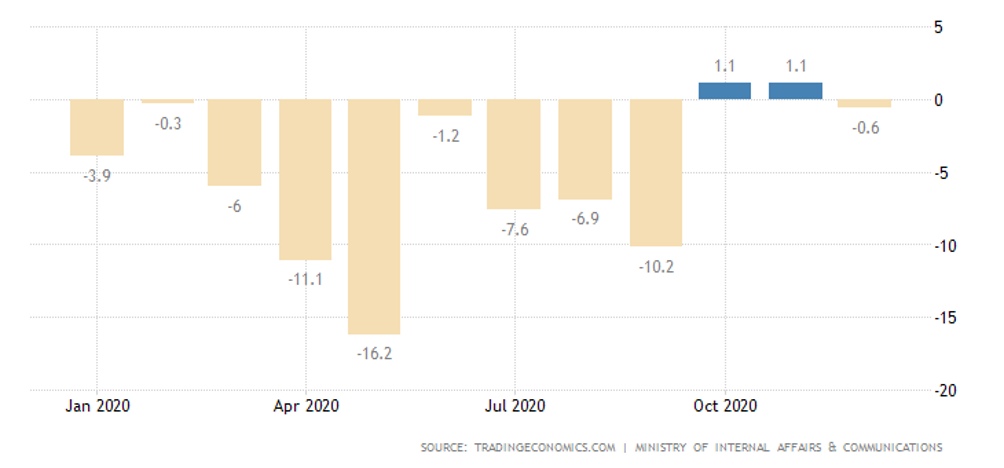

In Germany, the second lock was worse than the first for retail sales – they have a record -9,6% per month:

Worst annual performance since May (+1,5%).

Consumer spending in Japan returned to annual negative values in December after two months of positive:

The Central Bank of Australia left the rates close to zero, announcing that they would remain there at least until 2024, and expanded the asset buy program.

The Central Bank of England left everything unchanged, but began preparing a negative key rate (six months later).

The Central Bank of India did not change anything.

Summary: According to data from the fourth quarter, the situation is negative, which became clear at the end of last year. And in this context, the tightening of quarantine measures finds an explanation: the authorities of some countries again intend to justify themselves by blaming «objective» circumstances beyond their control. This is not at all new, but such obvious cynicism, in such generally very difficult circumstances, looks rather unsightly.

It may be noted that some countries are deflationary because of falling demand, while others are inflationary. Given that both are involved in promoting their economies’ emissions. This is due to one circumstance: the existence of a mechanism for sterilization excess money. China does so by converting the renminbi into a currency derived from foreign trade surpluses, the US by transferring money to financial markets. Whereas Turkey does not have such a mechanism.

What is better is cause for debate. In both cases, the real standard of living of the majority of the population is steadily declining. Balancing the fine line, that is, printing exactly the amount that citizens get money, but not too much, is almost impossible, because the rate at which money moves across sectors of the economy varies and depends, among other things, on the amount of money. There may be, in theory, a cash-flow management that does not lend itself to inflation or deflation, but no one in history has ever been able to do so.

We note that while President Trump was in office, he escalated China’s trade relations by tightening the regime, and thus prolonged the situation in the US by bringing China’s monetary problems closer. Biden did the opposite, giving China an additional resource, taking it from the US. This means that the probability of a stock market crash in the US before China collapses has soared.

Also note that the increase in the number of jobs in the United States is also Trump’s merit. With Biden’s policies, there is a strong possibility of a job collapse in February, but we will be monitoring the situation.