Period: 18 – 24 July 2020

Top news story: Two headlines this week. The first was this week’s EU summit.

- The exercise revealed that the leadership of the entity did not have any model for recovery from the crisis. This means that no one has this model because it cannot be kept secret and the summit would discuss a variety of options. It is only about the distribution of money (by origin) which always causes conflicts and problems.

- Second, gold prices continue to rise despite the summer and the crisis (the current price is approximately $1,900 per ounce). This suggests that market participants’ confidence in economic recovery is weak. It should be noted that market participants are a rather narrow group and cannot be drawn conclusions about market sentiment in general.

Macroeconomics

South Korea’s GDP slumped by 3,3% per quarter and 2,9% per year in April-June – both its worst since 1998, and its export slowdown (-16,6% and -13,6%) record since 1963.

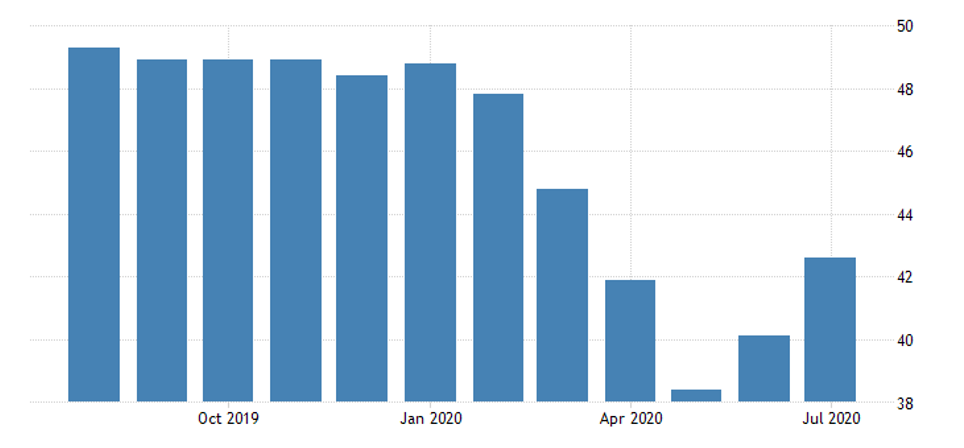

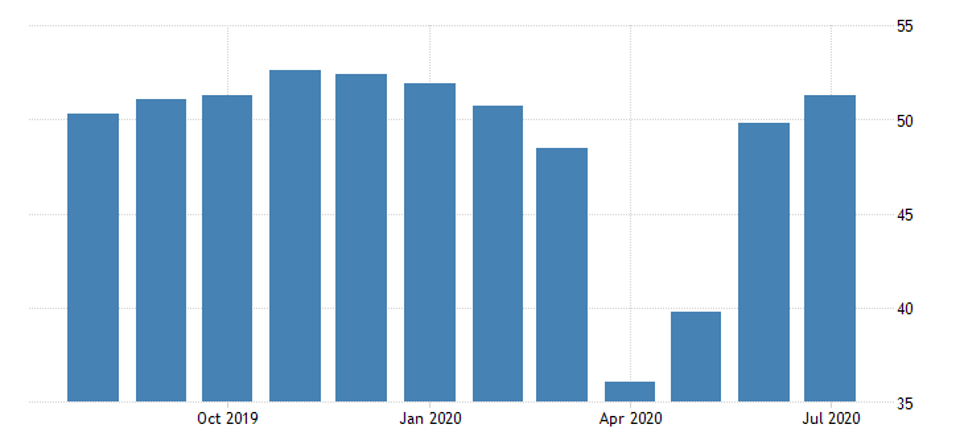

Japan’s Manufacturing PMI improvement in July was modest, still deep in the recession:

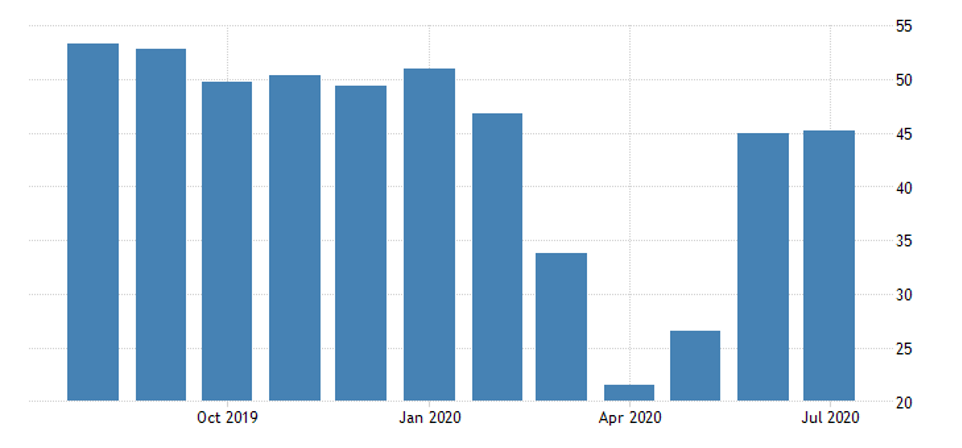

In the service sector, improvements have come to a halt:

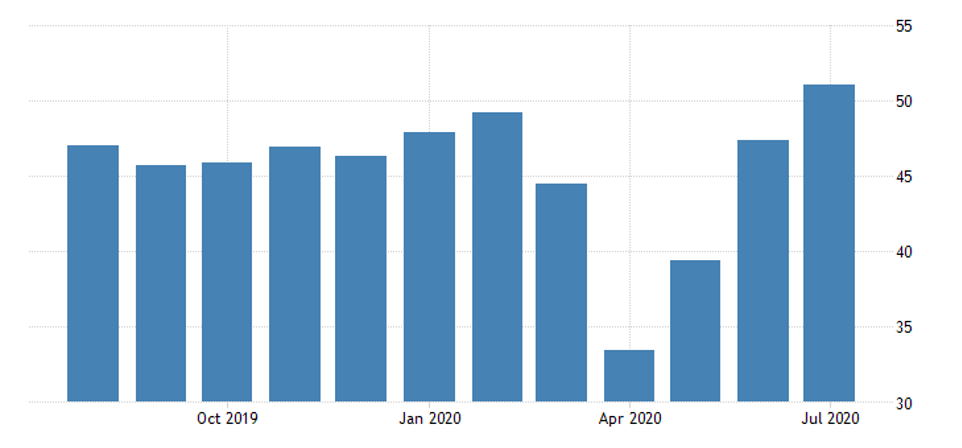

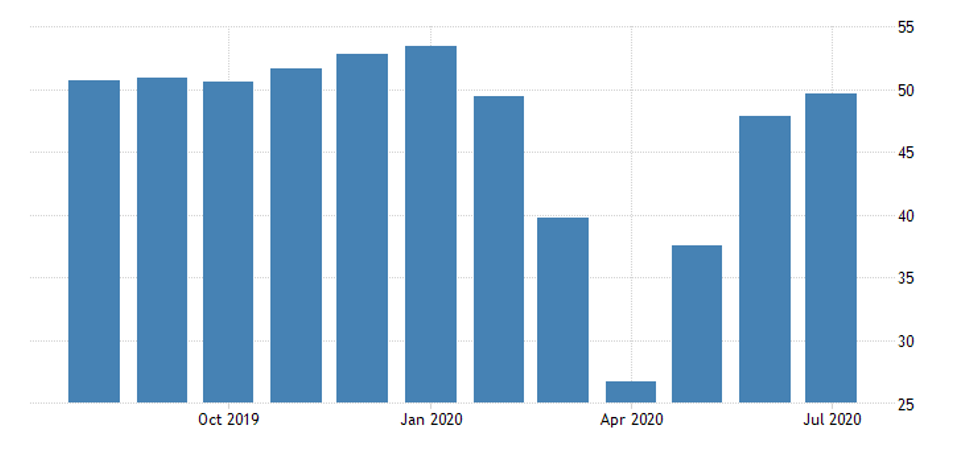

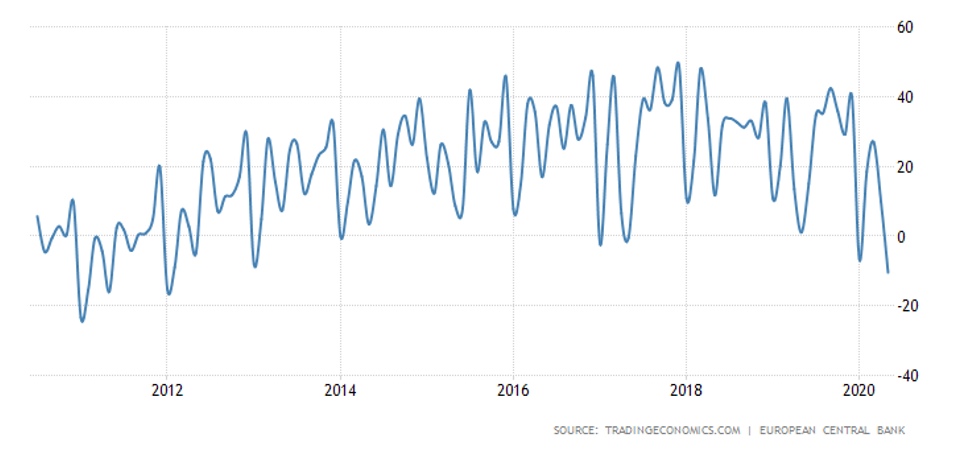

Europe has a better picture:

The US is better than Japan, but worse than Europe:

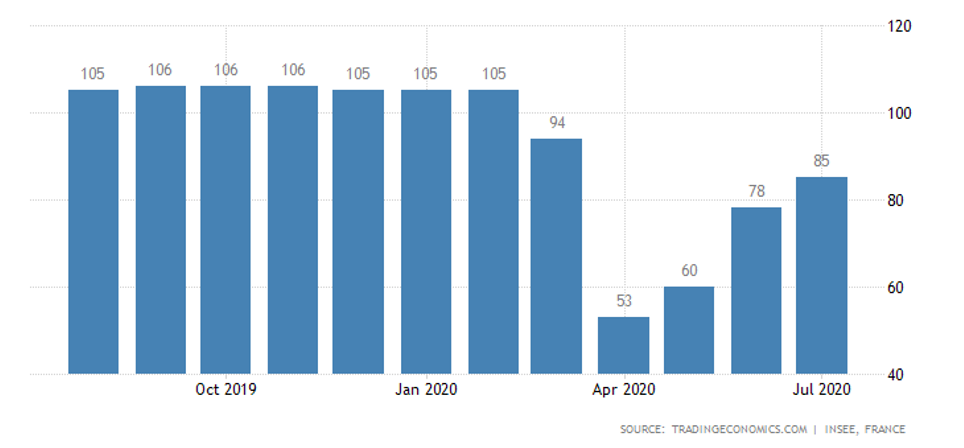

France’s business confidence and business climate are improving very slowly:

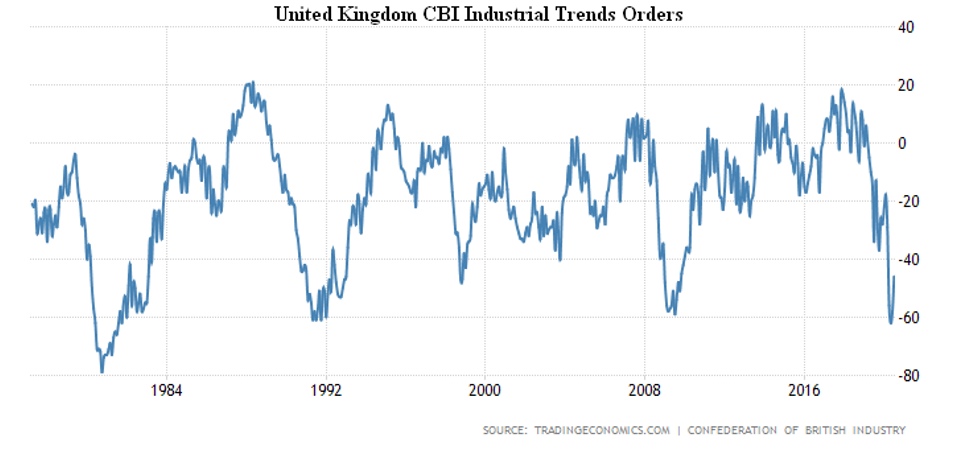

The balance of industrial orders in Britain is also struggling to improve:

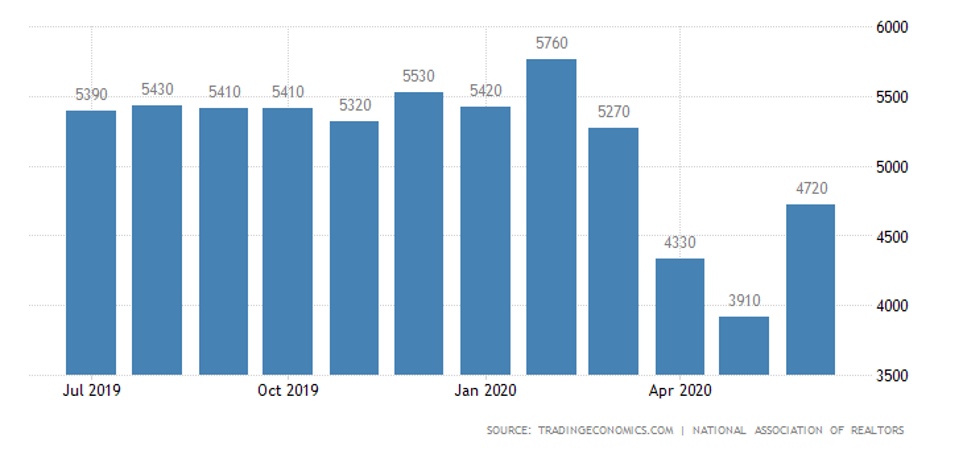

Existing home sales in the US were weaker than expected, and prices rose to record highs:

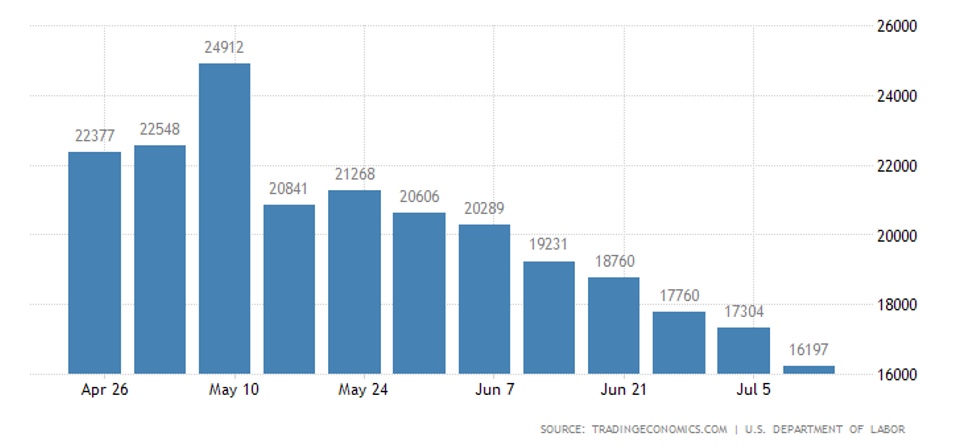

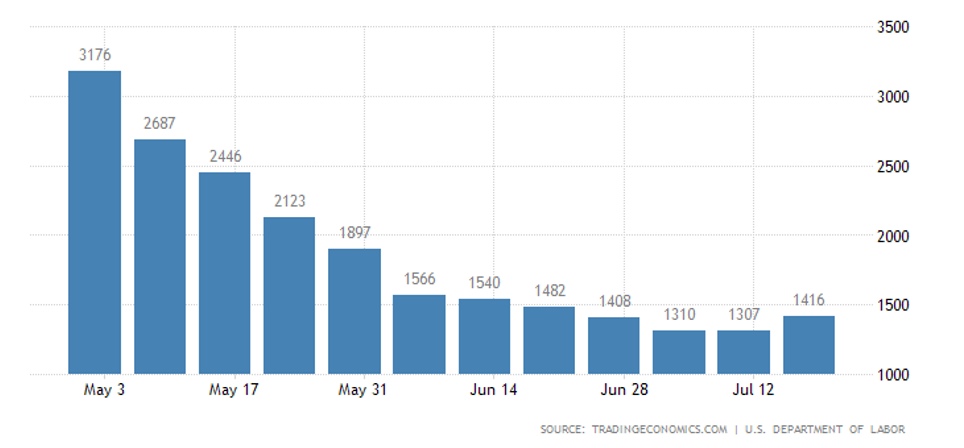

In the United States, the number of recipients of unemployment benefits in the week prior to 18 July decreased:

However, by the following week, more people had suddenly applied for benefits than the previous week:

According to the Ministry of Labor’s report, the total number of beneficiaries remains huge, about 32 million.

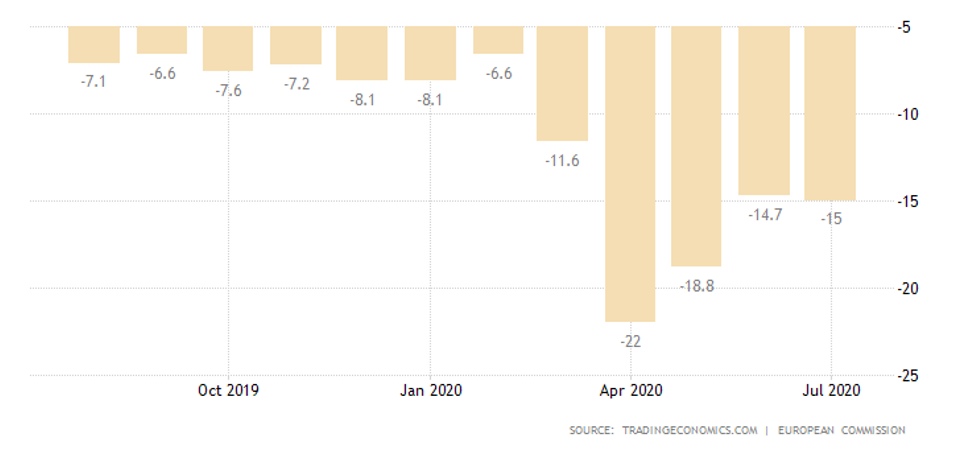

Eurozone residents’ market sentiments unexpectedly worsened in July:

Market sentiment in Britain improved, but only slightly.

The Eurozone’s current account is in deficit, the worst in eight years:

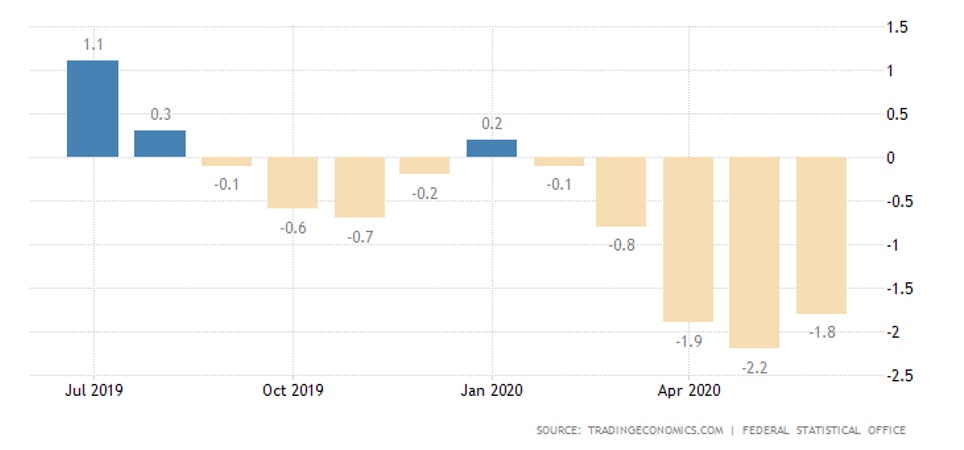

Germany’s PPI recovery is significantly slower than expected:

Japan’s CPI has remained at the trough since 2016.

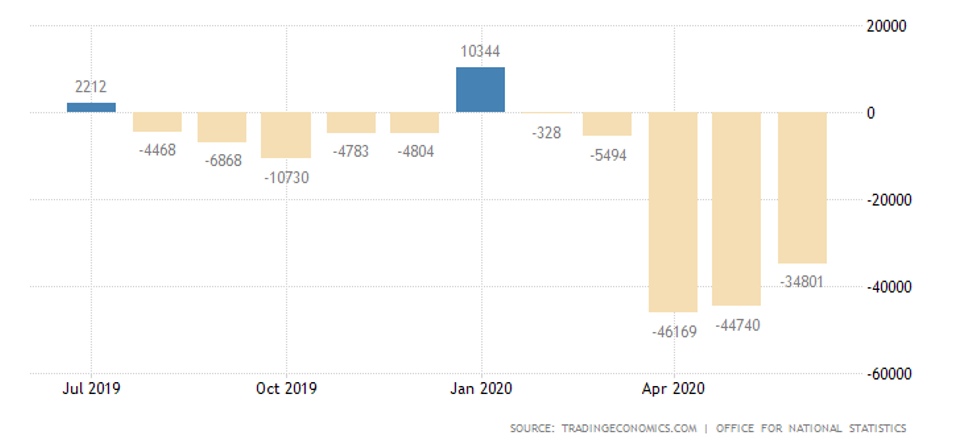

Britain’s budget deficit remains huge, with public debt reaching 99,6% of GDP:

The Central Bank of China, like the Central Bank of Turkey, has left monetary policy unchanged. But the Central Bank of South Africa lowered the rate by another 0,25% to 3,50%, and the GDP estimate for 2020 is down to -7,3%.

The Central Bank of Russia also cut the rate by 0,25% to 4,25%.

Summary. Our forecast has been met – recovery rates have slowed. However, in view of the increase in the price of gold, some economic agents assume a negative scenario. They expect a new recession before the economy recovers from quarantine problems. We are certain of this, because in fact the quarantine accelerated the structural crisis but did not exhaust it.

At the same time, authorities around the world do not understand the structural causes of the crisis and consequently do not see how it can be developed. This means that the right measures will not be taken, and those that are being implemented (mainly the distribution of emission money) cannot stop the crisis and cannot reduce its scale. These measures can only slow down the pace of the crisis. Thus, these actions by entrepreneurs must be developed and implemented on their own.