Period: November 28 – December 4, 2020

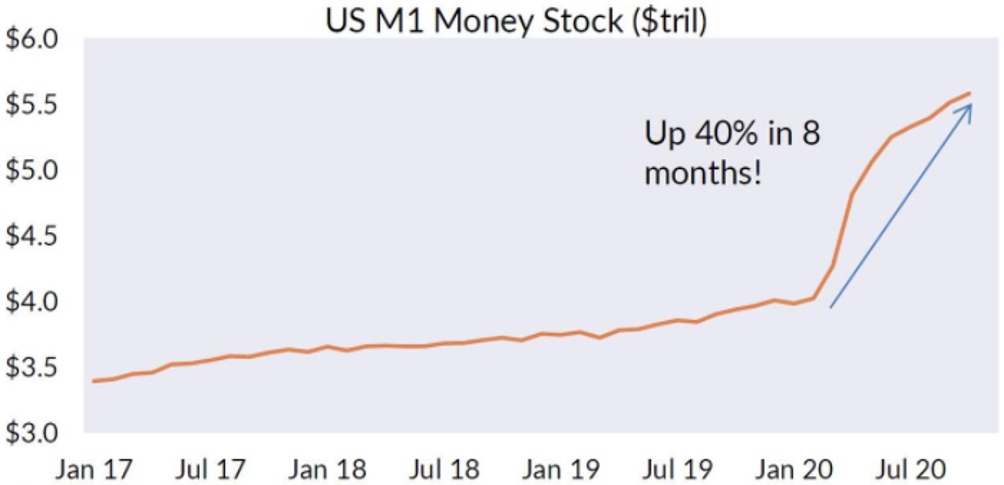

Top news story: How lively the past week has been in the political sphere (the counting of votes in the US elections), so it was economically sluggish. Neither the OPEC meeting nor the discussions of various international organizations on electronic currencies can clearly be considered the main news. Yes, one can confirm that the state of the Global Dollar (Bretton Woods) System leaves much to be desired, but to understand this one can only look at one figure:

Please note that the US economy has not changed much compared to previous years (taking into account the pandemic). In other words, this increase in the money supply was necessary to maintain the status quo!

But it is clear that this rate of growth of the money supply cannot be sustained, and that is why. The concentration of money in the speculative financial sector (and where else should it go? Inflation in the US is not yet high) will lead to one option: either inflation will build up, or bubbles in speculative markets will collapse. Or the emissions will cease, causing markets to collapse as well. With all the consequences.

Put it differently: the question today is not whether the world economy will collapse, but when it will collapse. It is obvious that macroeconomic indicators are not always able to provide an unambiguous answer to this question (although in 2008 the moment of decline almost exactly coincided with the moment of zeroing the base interest rate). Nevertheless, we will attempt to predict this point in the analytical part of our reviews, of course, on the basis of objective data.

Macroeconomics

Industrial production in South Korea -1,2% per month (5-month low), annual dynamics returned to negative (-2,2%). In fact, South Korea, which had borne the brunt of recovery almost the longest, has given in to the situation in almost all other countries.

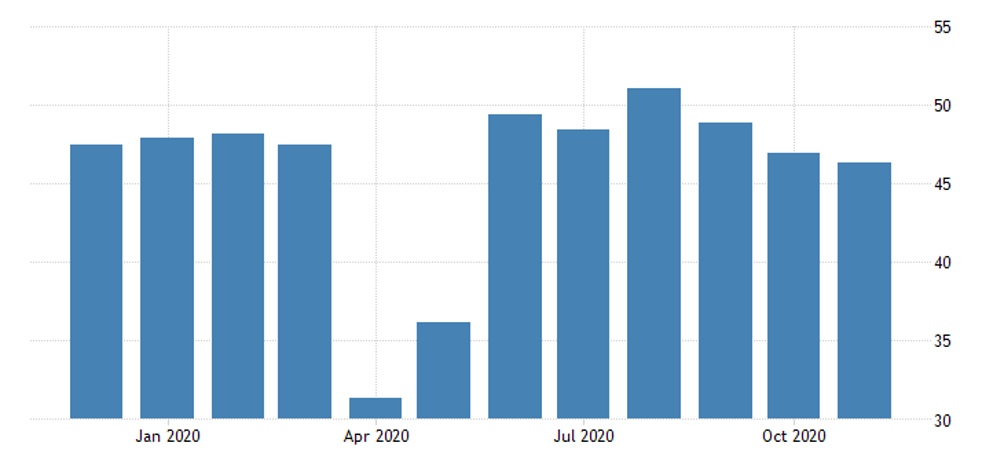

PMI in the Russian industry is the worst in six months:

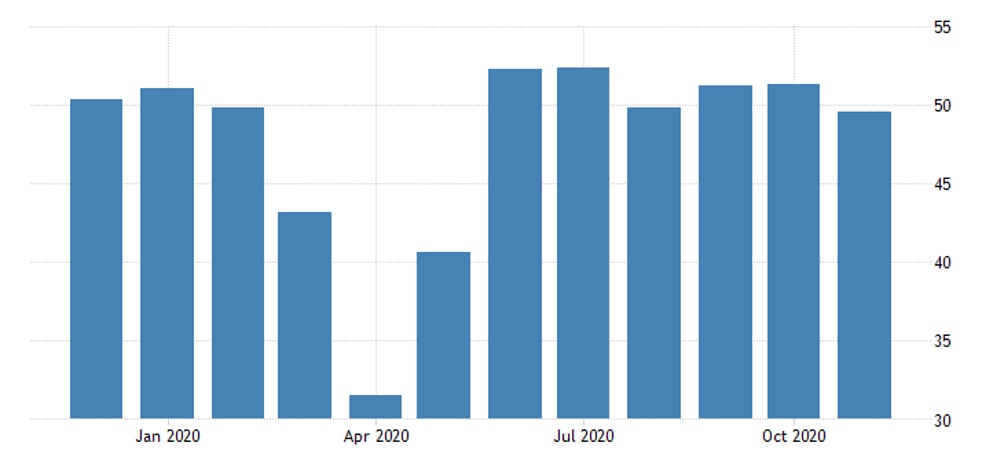

As in France:

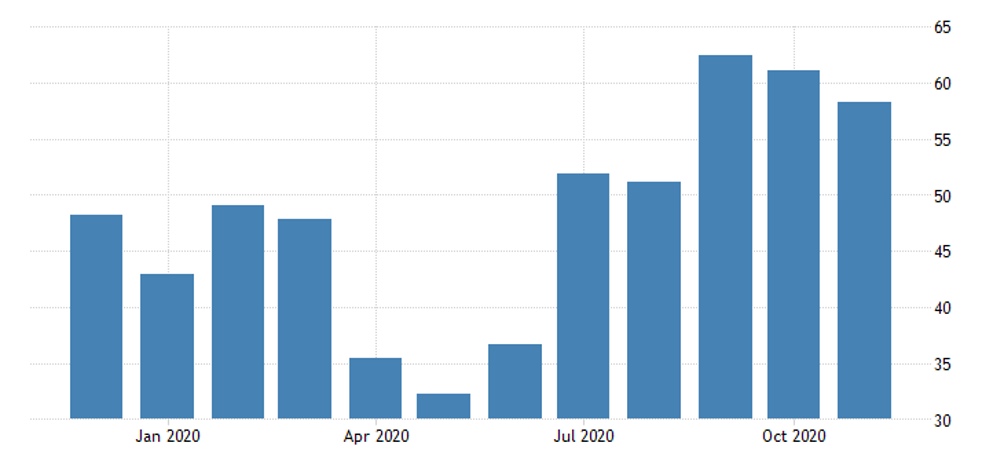

Spain’s manufacturing PMI is lowest in 5 months.

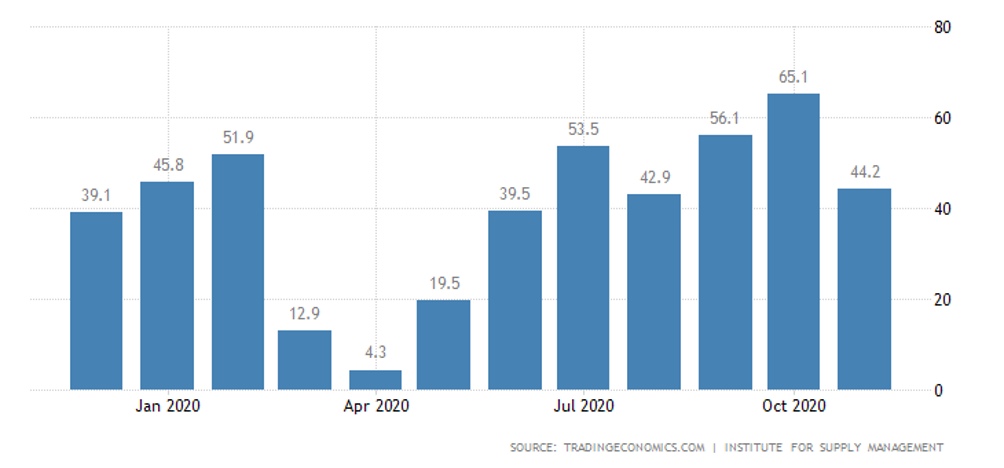

United States Chicago PMI slowed down, but remained in the growth zone:

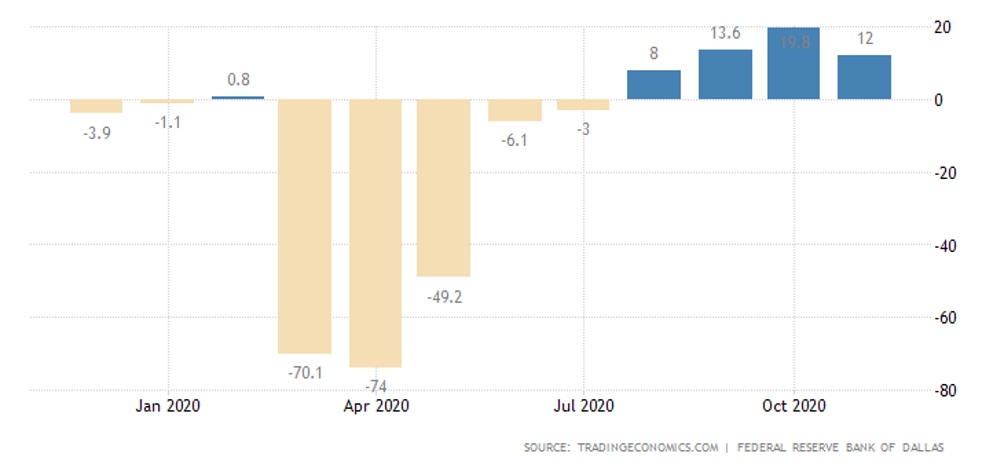

Same as the United States Dallas FED Manufacturing Index:

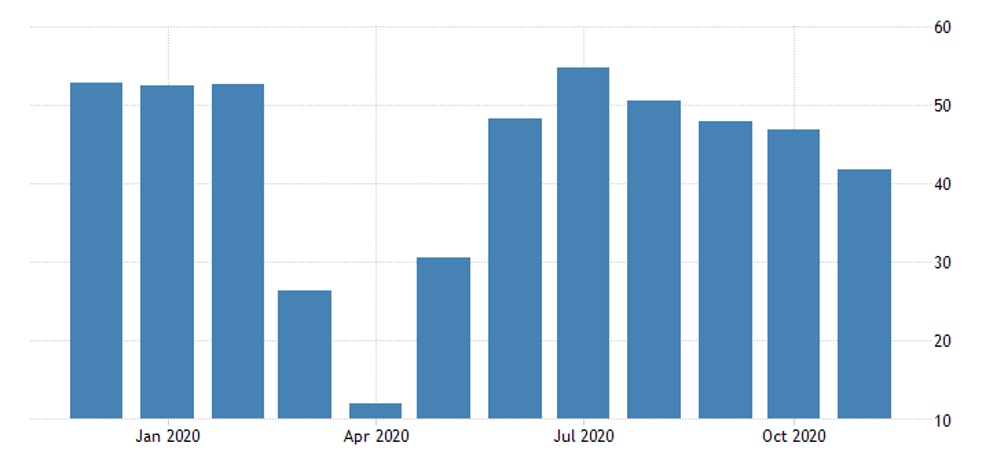

United States ISM New York Index plummeted into a slump amid a collapse in employment and purchases:

In November, the service sector in Europe sagged again in Spain, Italy, France, Germany and the Euro Area as a whole:

In the UK, the situation is similar:

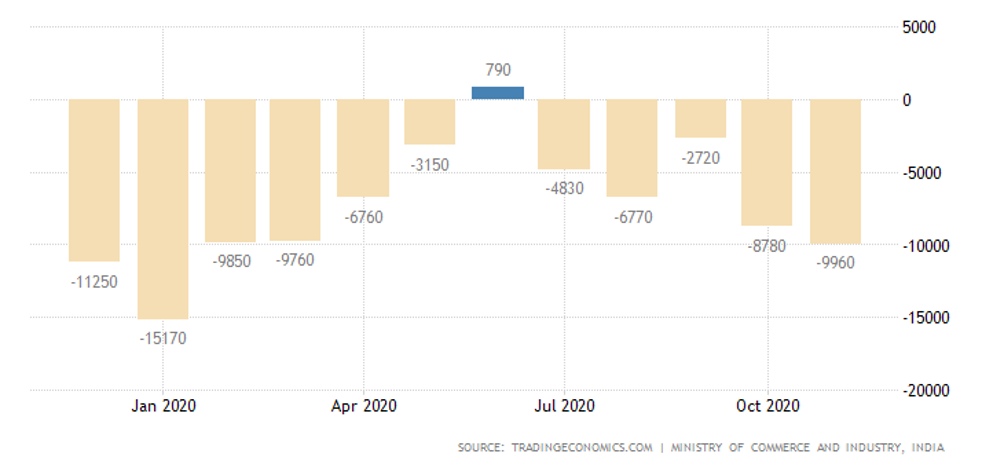

India’s trade deficit is the worst in 10 months:

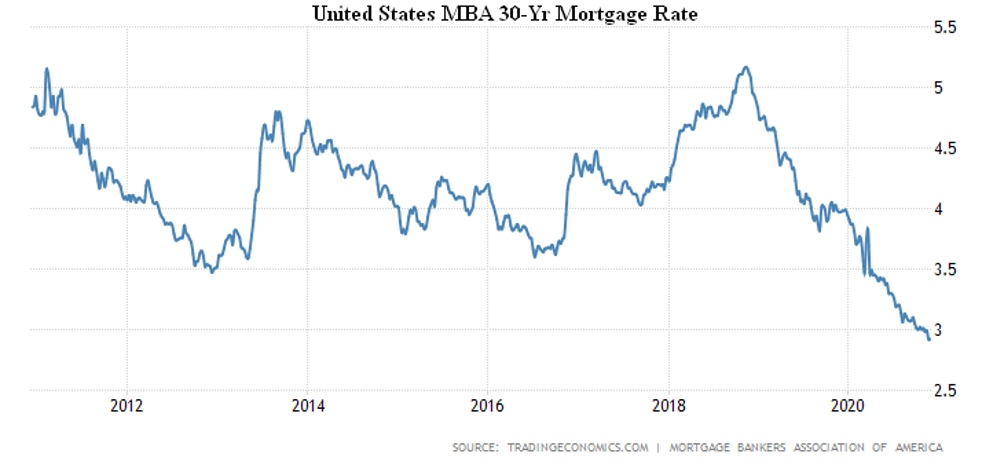

Uncompleted home sales in the US are slowing, but still at 20% per year. Mortgage rates are at a record low (2,92% on 30-year loan).

Housing prices in Britain are 0,8% per month and 6,5% per year – for a maximum of six years.

Germany’s CPI is -0,8% per month (6-year low), per year -0,3%, also the trough since January 2015 and only 0,1% of the 34-year low.

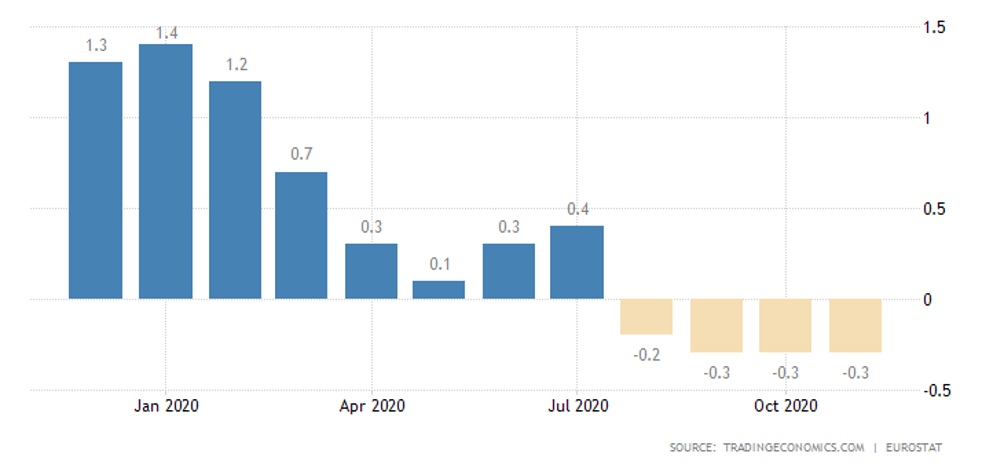

The same picture for the Euro Area as a whole:

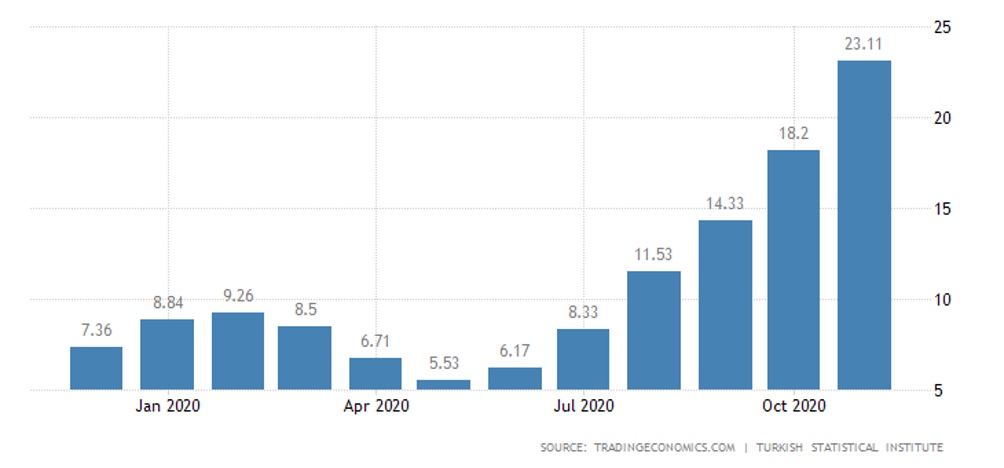

Net inflation in Indonesia is at an all-time low (1,7% per year), while in Turkey it continues to grow:

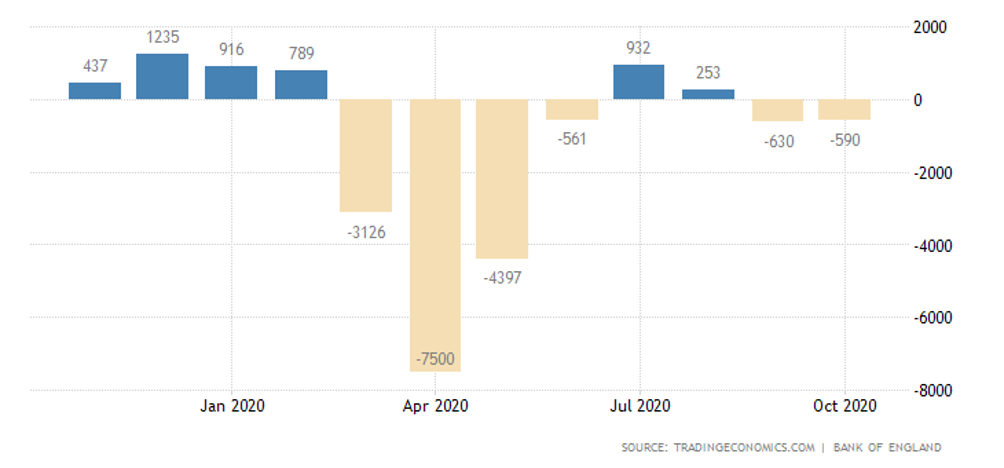

UK consumer credit continues to fall:

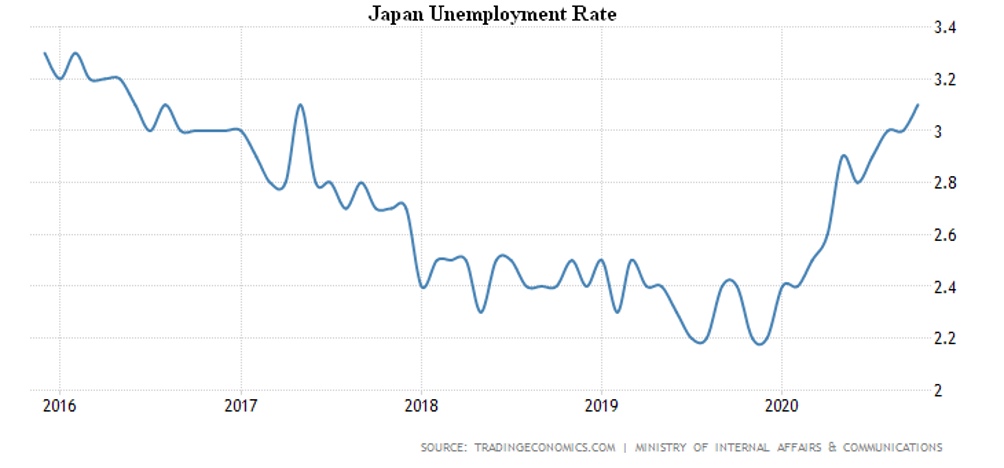

Japan’s unemployment peak since May 2017:

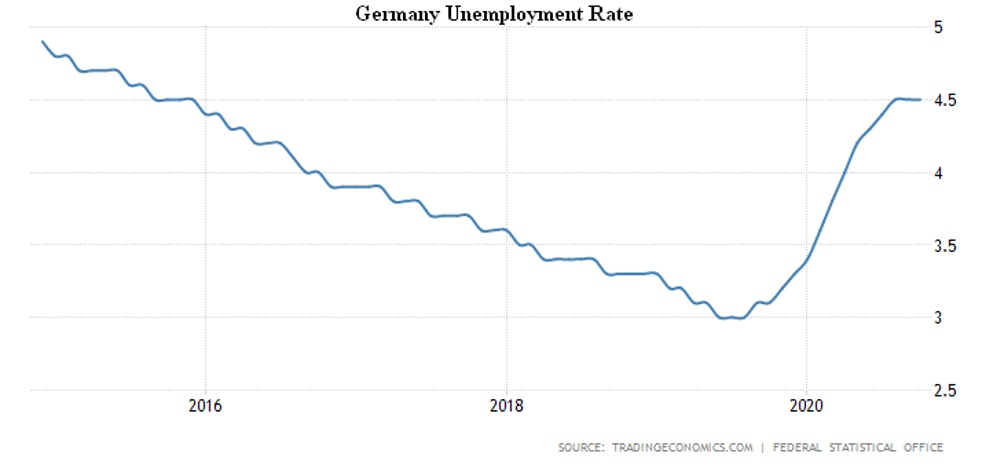

And in Germany, since December 2015:

US private sector employment growth continues to decline:

As with the economy as a whole (7-months low), jobs are now 9,8 million fewer than they were in February.

Retail in South Korea went down monthly (-0,9%), on an annualized basis, the same process

(-0,2%).

The Central Bank of India left monetary policy unchanged.

Summary: The discourse on e-currencies, coupled with the need for continued support for the economy in the context of a prolonged downturn (this week, optimism has disappeared from almost everywhere), may offer an interesting insight. Let me remind you that in the first phase of the FED’s existence, the issue money was used on a limited scale only to support banks. Then, little by little, they became used to support the real sector. Trump made it the rule. But today this scheme no longer works – what is the point of supporting a real sector enterprise if households are unable to purchase their products?

As we have repeatedly mentioned, banks have stopped lending to households, there is no possibility under existing schemes to increase demand (only it can be reduced by raising the rate). What if the introduction of the electronic currency and the opening of direct accounts to citizens in the FED (and central banks generally) were to be used for direct issuance in favor of households? In the form of unconditional income, not from the budget, but with the aid of emission money?

It is not possible to give an exact estimate of the consequences of such an innovation today, but the experience of «Reaganomics» indicates that it is most likely for some time it will prolong the agony of the existing system. If it’s two or three months, it doesn’t matter, but what if it’s eight or ten years? In that case, the current generation of politicians will be able to step off the stage calmly and shift the responsibility to the younger generation, which is clearly not prepared to face such challenges.

In general, we do not rule out that by the middle of next year we will have seen the most dramatic innovations in the financial system, with the consequences unknown even to the founders. However, the expectations are totally misplaced, as is evident from, inter alia, the rhetoric of the chief executives of the current system (Jerome Powell, Kristalina Georgieva-Kinova) and from the indicators we give at the very beginning of this review.