Time period: 1-7 January 2022

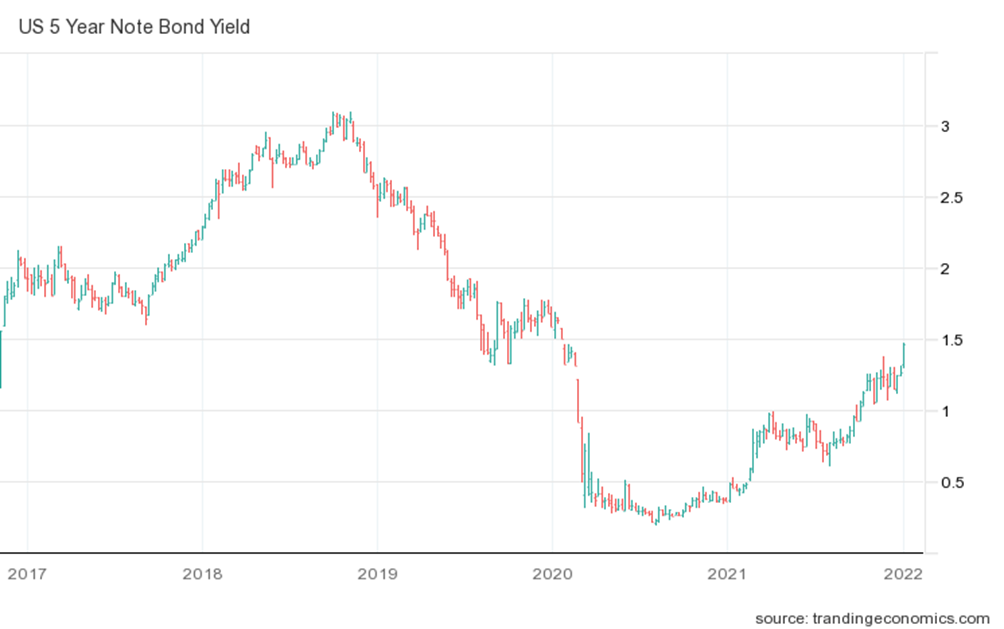

Top news story. According to the minutes of the Fed meeting, it will be quicker to roll back incentives and probably even start selling assets off its balance sheet soon after the rate hike begins. As a result, the growth in the yield of government bonds, especially short-term ones, has intensified: for example, for 5-year notes there is a 2-year high:

The debt has not disappeared, and the decline in household credit stimulus, inevitable in the context of monetary tightening, needs to be reversed. It is possible to do this only through budget programs (including restructurings), but it actually means abandoning the original “Biden plan” in favor of “Trump plan”.

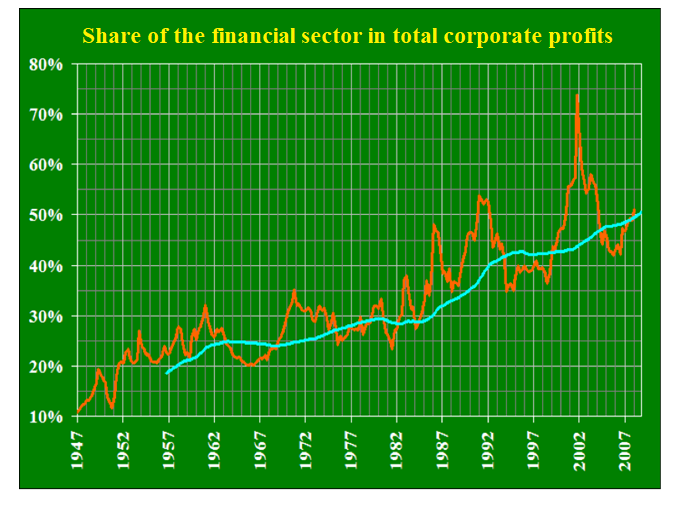

In the context of the importance of the financial sector to the economy, such a decision is tantamount to a radical departure from the policies of previous decades. Let me remind you how the financial sector leveraged the power of the Fed from the Bretton Woods conference to the 2008 crisis:

Since 2008, the situation has been difficult, including in terms of objective statistical estimation, but the share of the financial sector has definitely not fallen below 50%. But if there has been a real abandonment of the understanding of credit stimulation of private demand (that is, the main component of Reaganomics; as you can see in the graph, the main growth of financiers’ incomes began after 1980), what does this mean? That the share of financiers should decrease to the 1930s performance? Down to 5%?

There is as yet no clear answer to this question, but the very situation in which it has to be asked is one that describes the extent of change. And we all have yet to face the impact of those decisions.

Macroeconomics

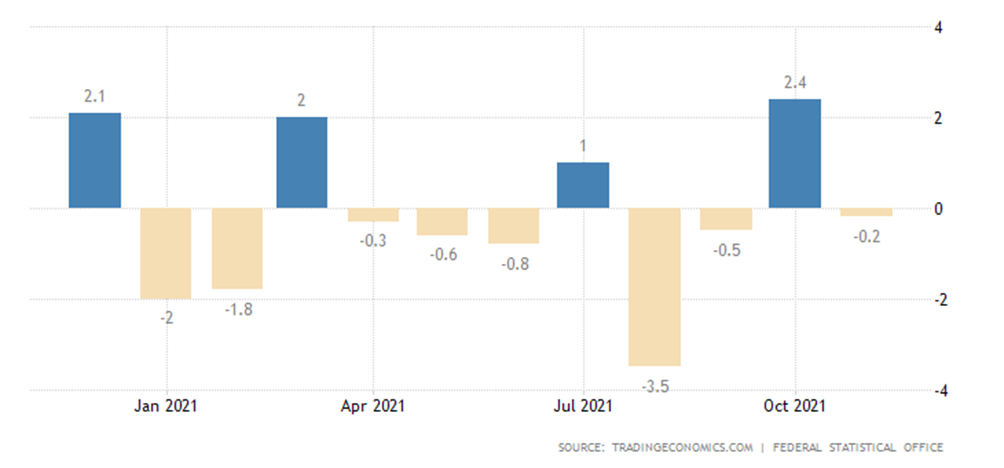

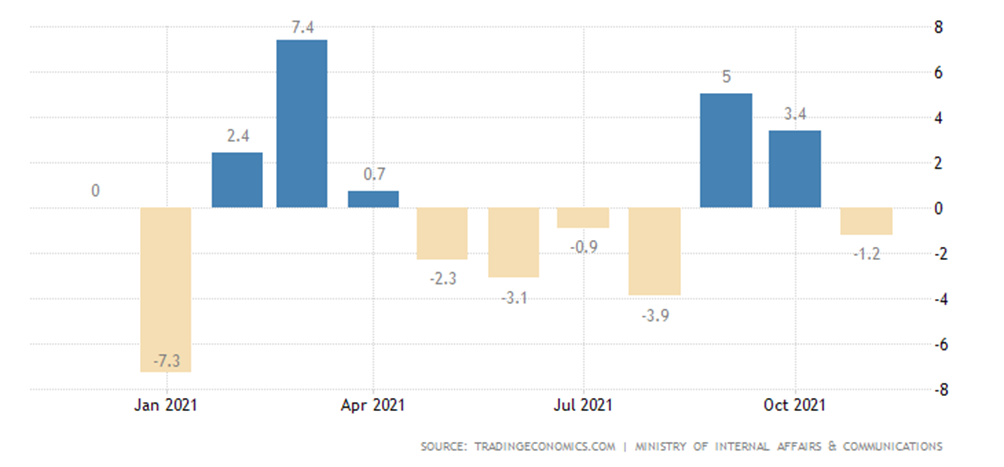

Industrial output in Germany -0.2% MoM, which is clearly lower than expected and the 8th time in the red over the past 11 months:

As a result, the annual performance deepened into the recession zone (-2.4%), this is the 3rd consecutive negative and the lowest in 9 months:

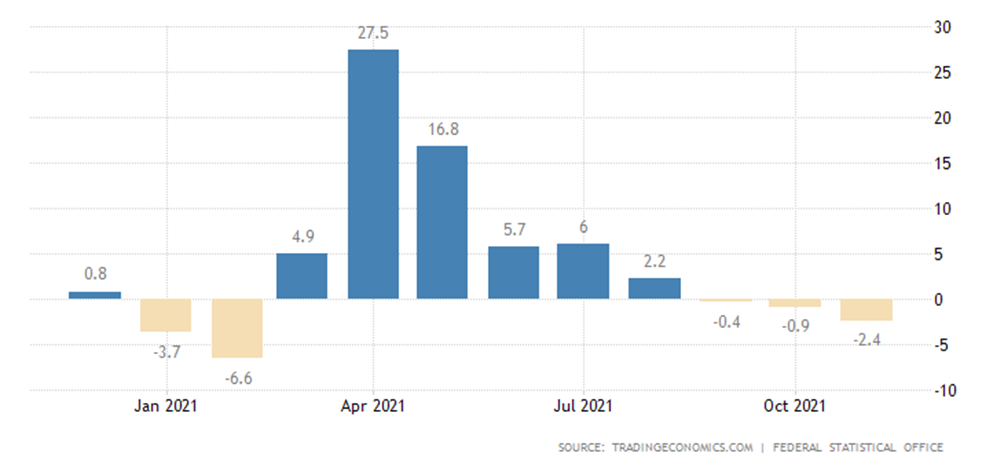

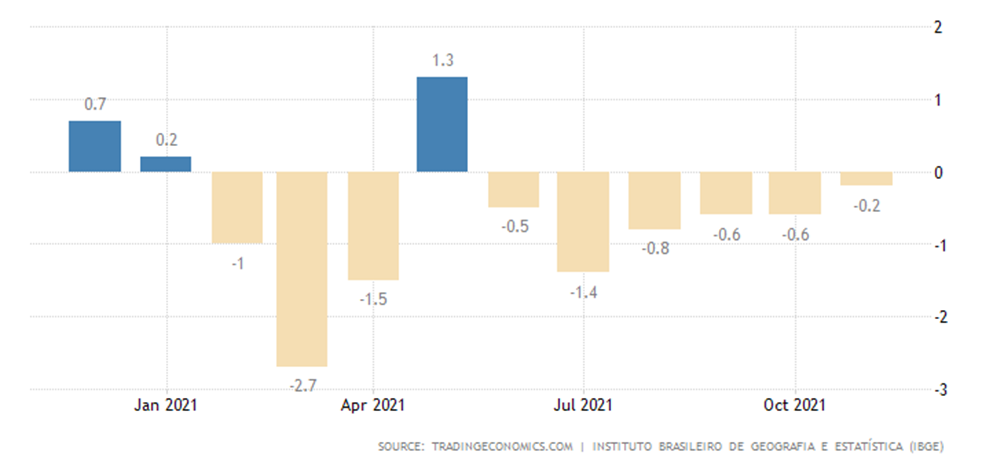

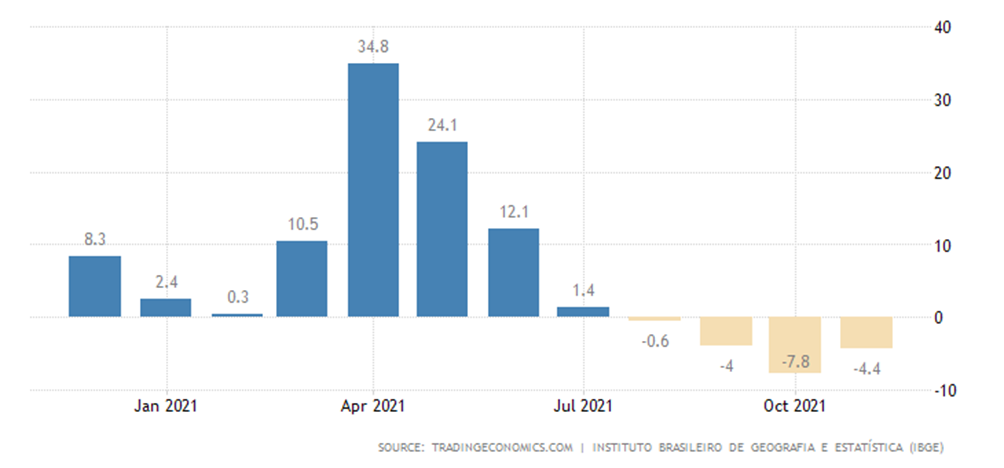

Industrial production in Brazil -0.2% per month, which is the 6th negative in a row and the 9th in the last 10 months:

And -4.4% per year, it’s the 4th consecutive negative:

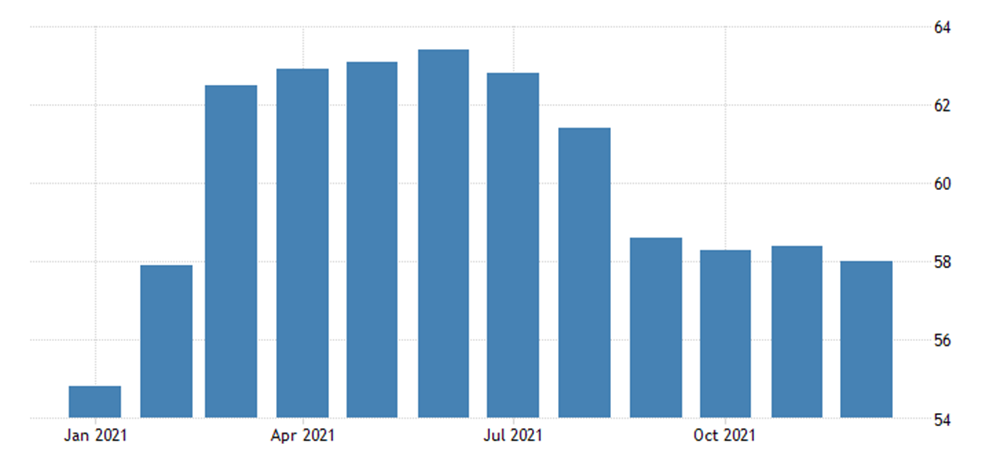

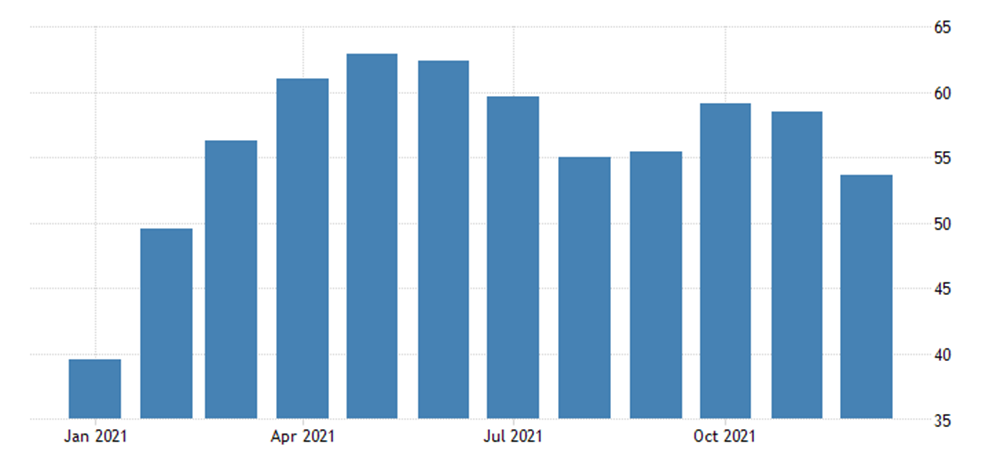

PMI (an index of expert assessment of the situation in the industry; its value below 50 indicates stagnation and recession) of the Euro Area industry is minimal in 10 months, but clearly positive (58.0 points):

In services, 53.1, which is an eight-month trough:

UK services PMI 53.6, the lowest in 10 months:

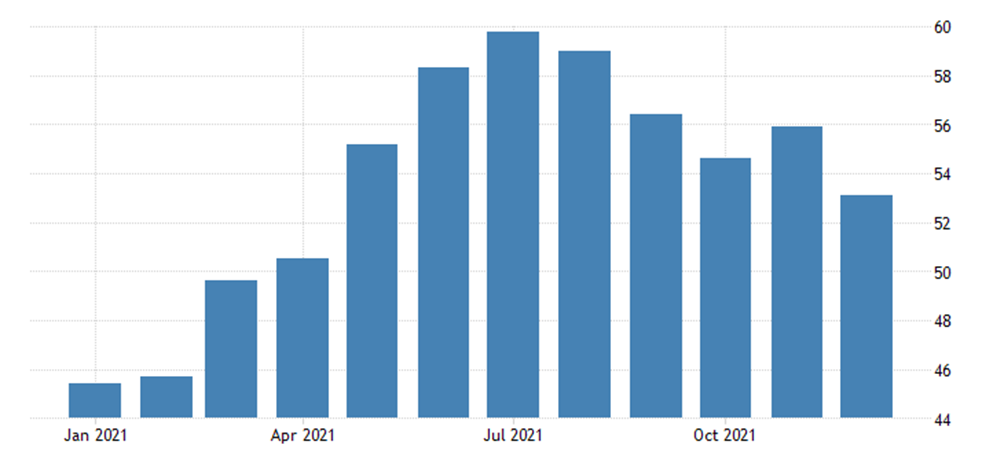

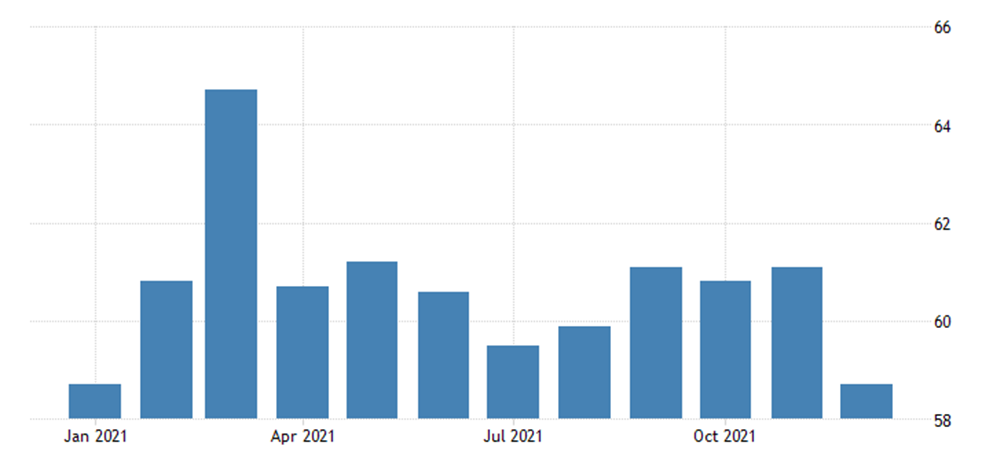

The PMI of the US industry is 58.7, which is the lowest annual value:

But just in case we remind that output of industries for estimation is formed in nominal terms, that is, the underestimation of inflation inevitably adjusts sectoral indicators for the better.

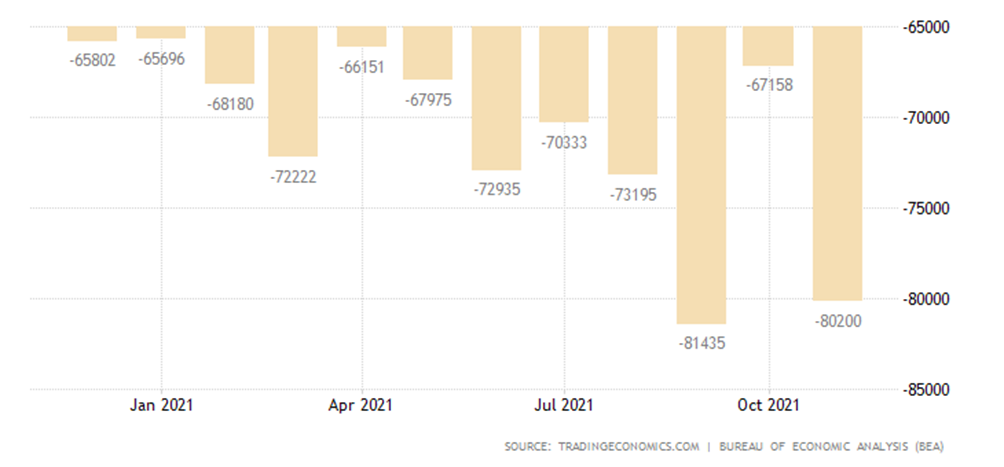

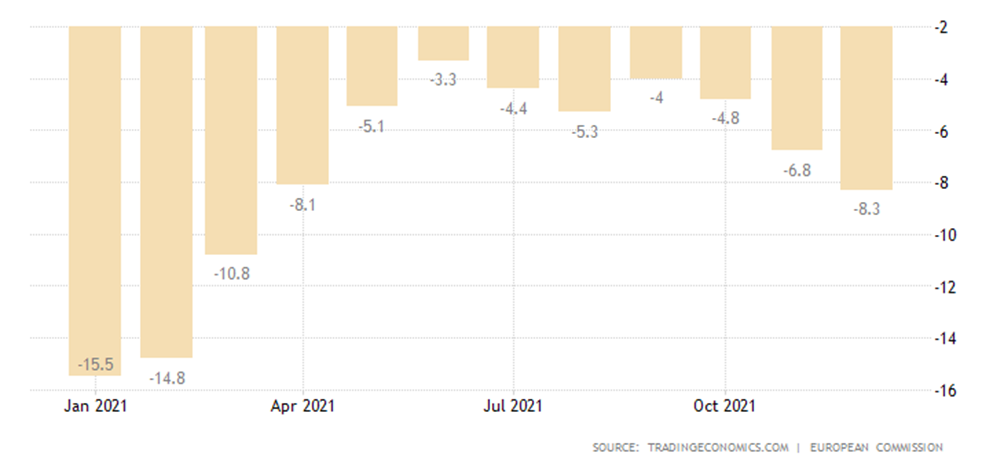

The US trade deficit nearly matched its all-time high. Exports amounted to +0.2%, and imports +4.6% (both record):

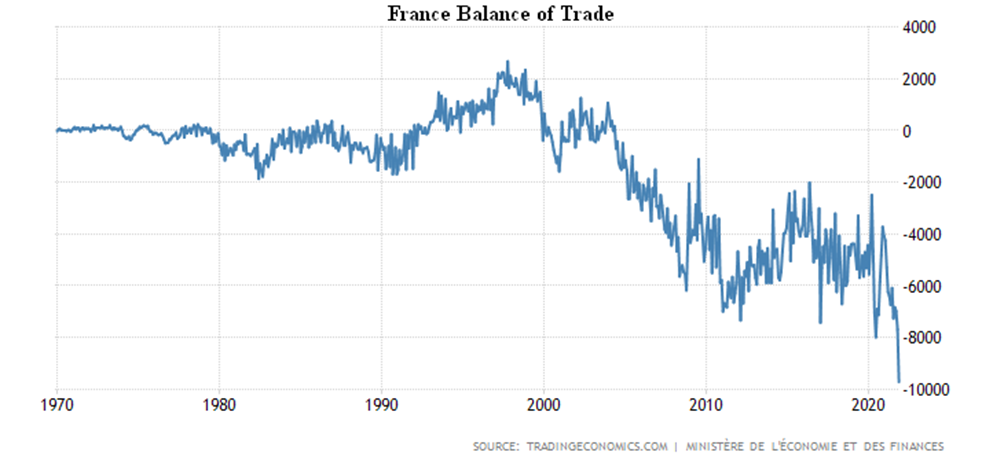

And in France, the trade deficit set a new anti-record for 52 years of survey. Exports became +1.6%, imports amounted to +5.3%:

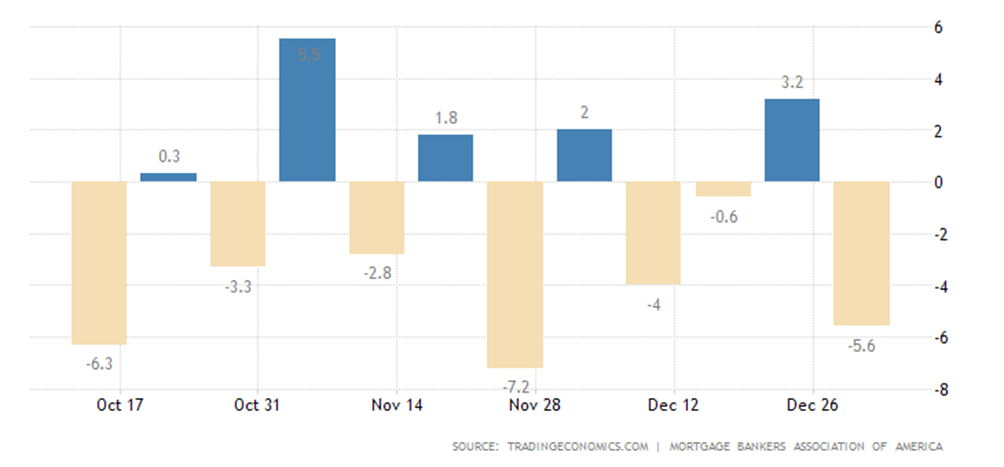

Mortgage applications in the United States were -5.6% per week and dropped to a two-year trough; purchase orders were -10.2%; credit rates peaked since April:

Inflation statistics continue to break records.

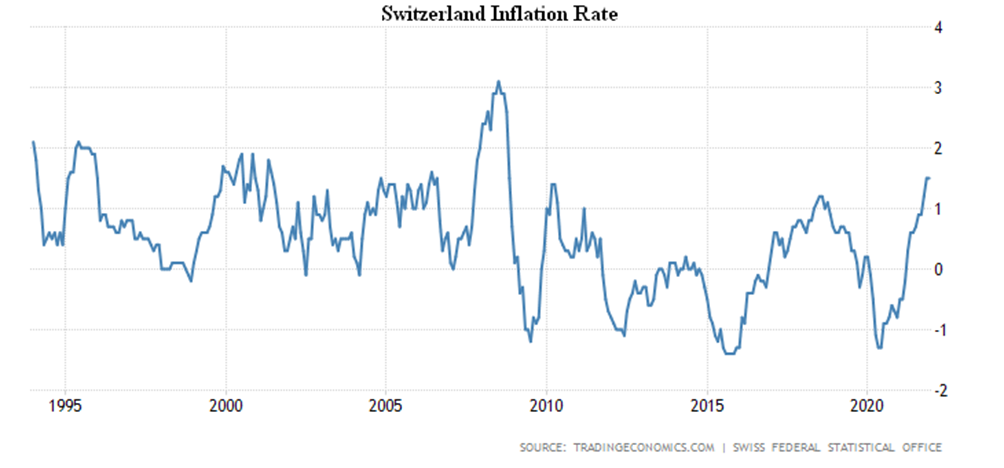

CPI (Consumer Price Index) in Switzerland +1.5% per year, is at its highest since 2008:

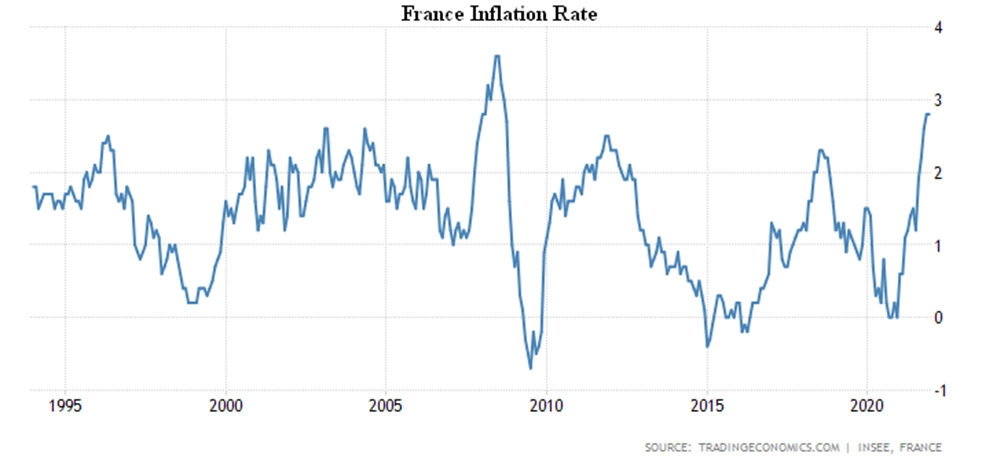

CPI of France +2.8% per year, which also has a peak since 2008:

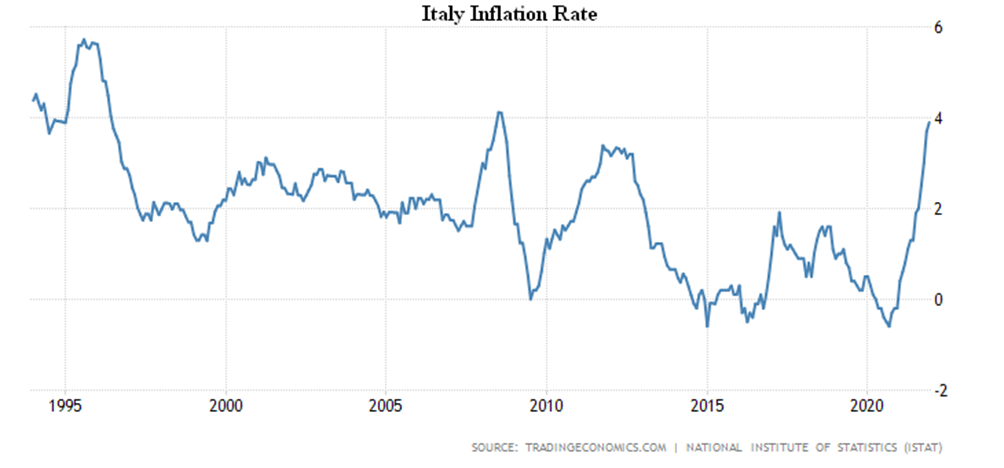

Italy’s CPI +3.9% per annum, and has seen the highest growth since 2008:

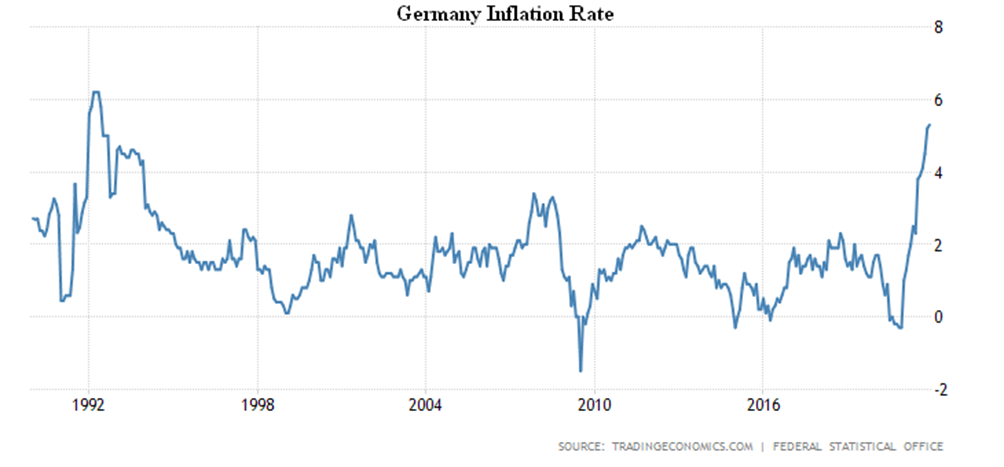

CPI in Germany +5.3% per year, has been at the top since 1992:

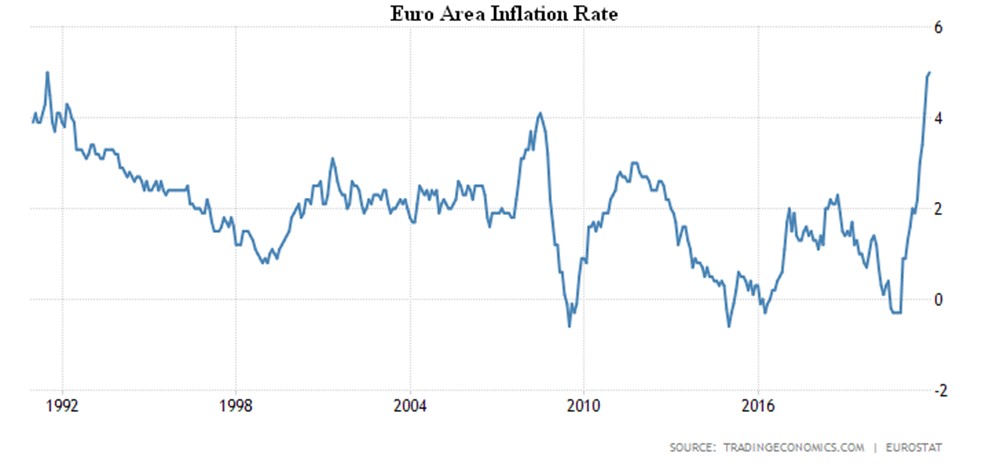

The Euro Area CPI was a record for 31 years of survey (+5.0% per year):

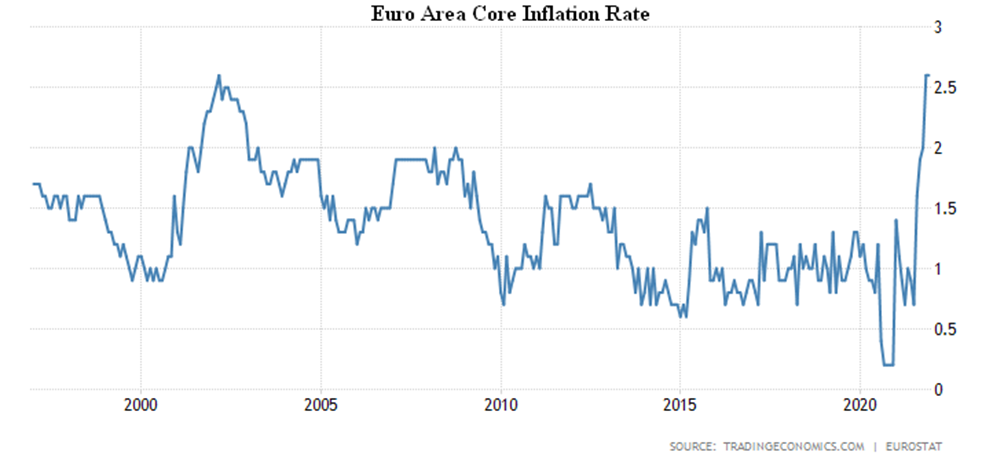

Core inflation rate (less food, alcohol, tobacco and energy +2.6%), which is also a record for 25 years of statistics:

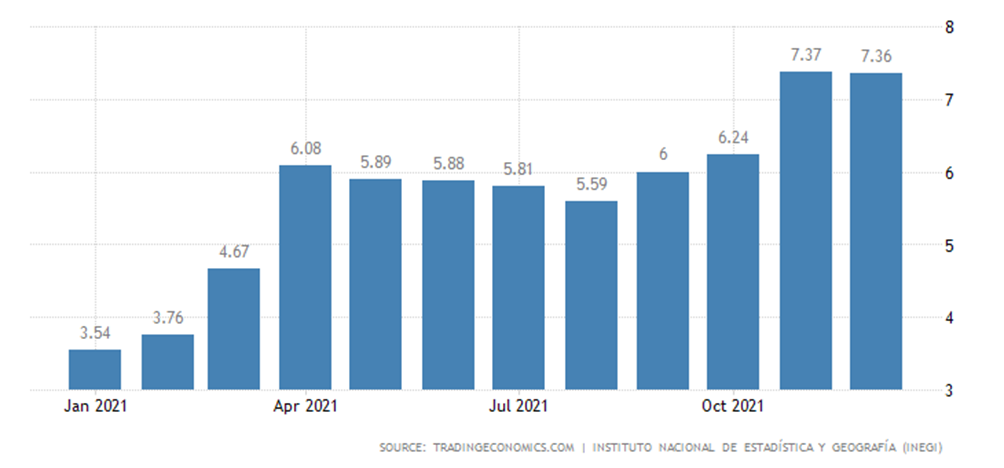

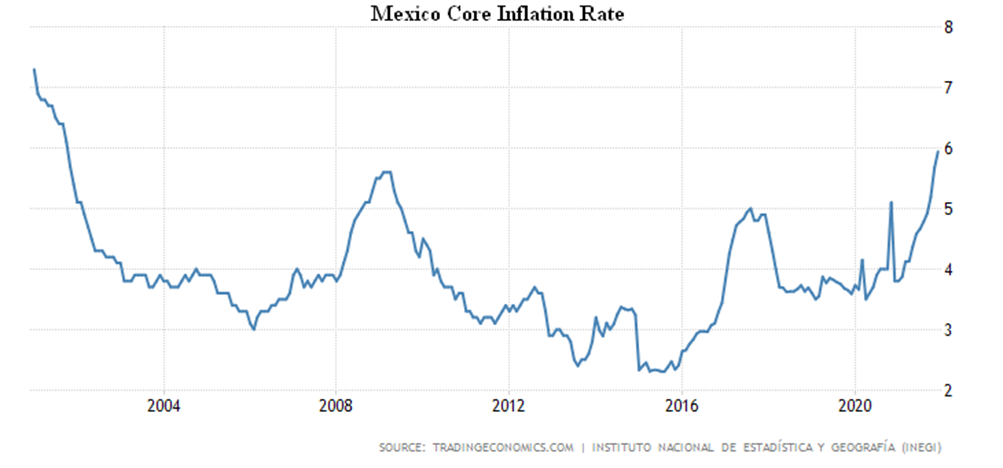

Mexico’s CPI remained at +7.4% YoY, the highest since 2001:

Excluding food and fuel +5.9%, which is also a peak since 2001:

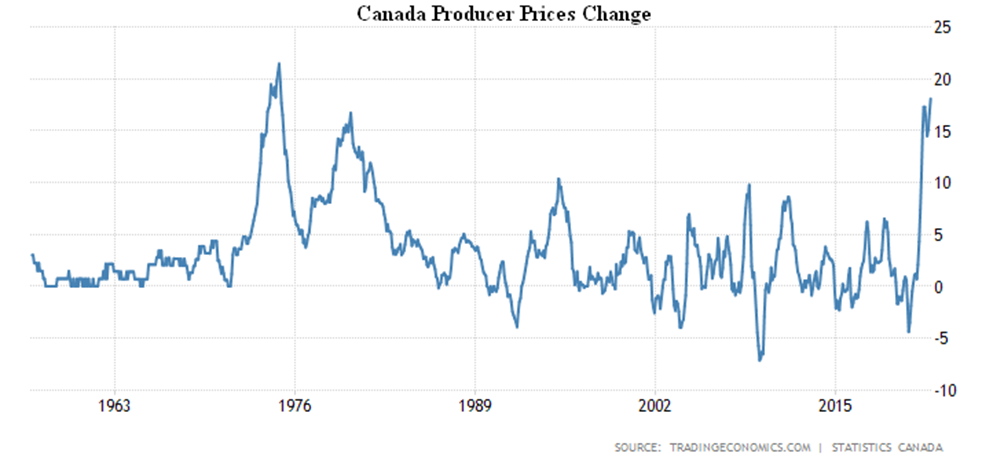

PPI (Producer Price Index) of Canada +18.1% per year, the highest since 1974:

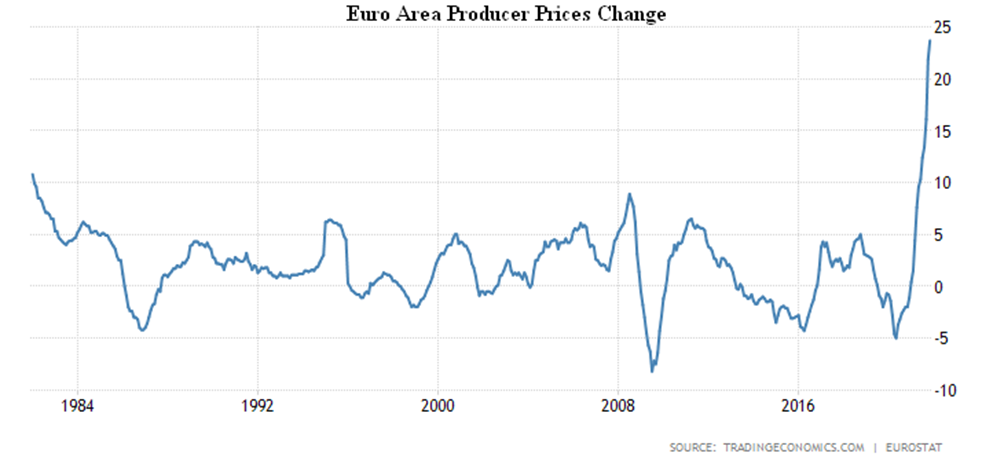

The Euro Area PPI +23.7% per year and is at a record high for all 40 years of survey:

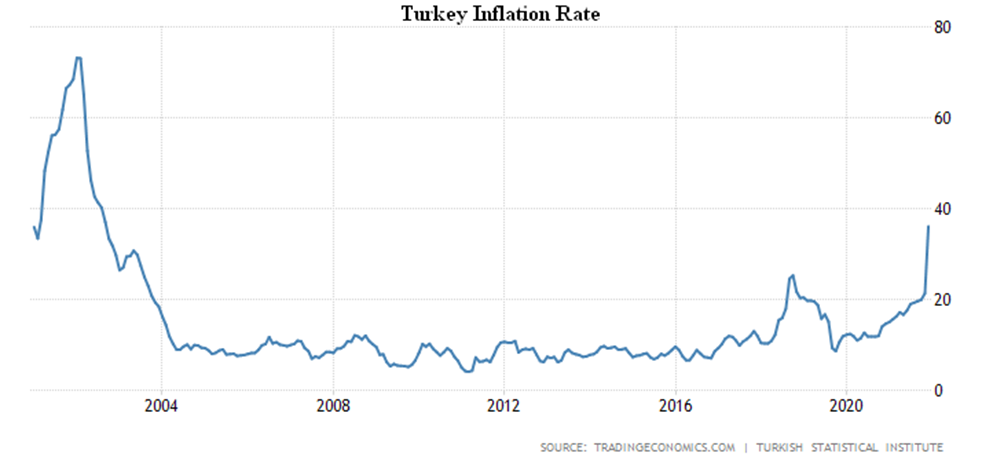

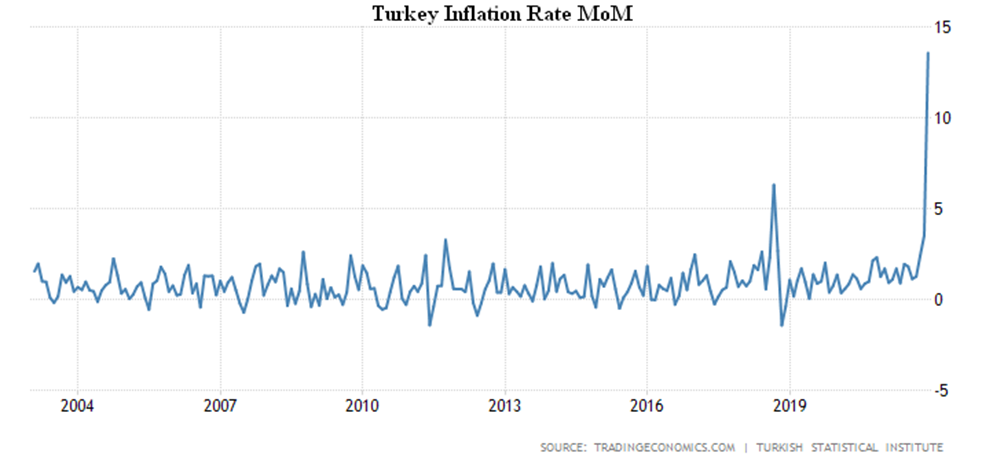

Turkey’s CPI surged to +36.1% YoY, the peak since 2002; and even +13.6% per month, which is a historical high:

Turkey’s PPI is also maximal since 2002 (+79.9%), with a monthly increment (+19.1%), the largest since 1994:

Erdoğan certainly does not get along with economic reforms. It is most likely that the President of Turkey has been unable to take control of banks and limit financial speculation, which is quite natural for a state with a negative balance of trade.

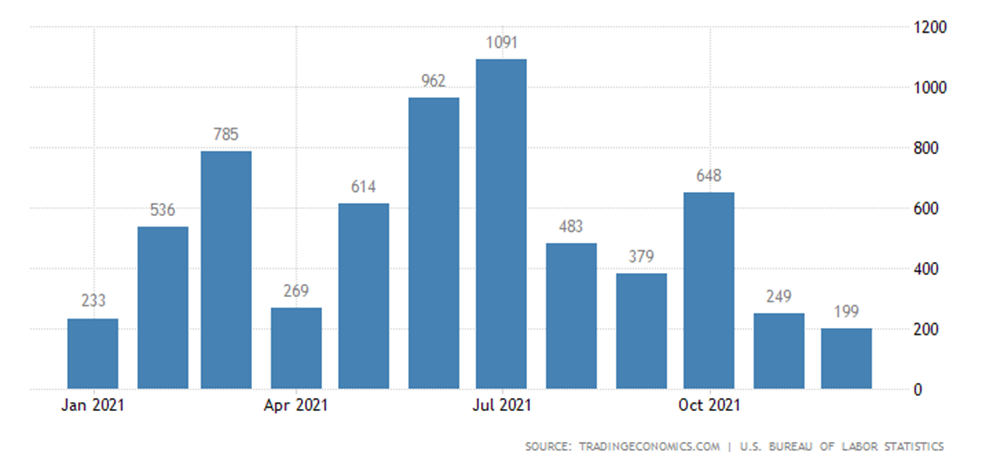

The growth of job openings in the United States shows the slowest rate in the year (+199 thousand):

The Euro Area consumer confidence is weakest in 9 months:

Japanese household spending turned negative month-on-month (-1.2%):

Summary. As we have done on many occasions, we will try to look closely at US labor statistics. On the one hand, they are encouraging. Share of population participation in the total labor force, December: 61.9% against the forecasted 61.9%, the same in November: 61.9% (revised from 61.8%); unemployment rate U-6, December: 7.3%, the same in November: 7.3% (revised from 7.8%); unemployment rate, December: 3.9% against forecasted: 4.1%, the same in November: 4.2%.

On the other hand: the average length of the working week in hours, December: 34.7 hours against the forecasted 34.8 hours, the same in November: 34.8 hours; average hourly salary, December: +0.6% MoM and +4.7% YoY, with forecasted: +0.4% MoM and +4.2% YoY, the same for November: +0.3% MoM and +4.8% YoY. And we have already given data on jobs created.

This is contrary to common sense: at first, employers increase the burden on existing employees and raise their salaries. The increase is clearly lower than the rise in prices. In other words, labor statistics are contradictory, which means that they are not trusted. Indeed, it was the labor market that was the main argument of the Fed’s leadership for positive forecasts, and if we recall the “overheating” of the labor market in Russia (according to the Central Bank of Russia), it can be assumed that the IMF’s statistical models for the labor market do not work with a strong underestimation of inflation.

The ECB’s commentary on record-breaking inflation rates can also be read. The European Union’s main bank will not act hasty to stop the rapid rise in prices in the Euro Area Member States, as it considers inflation to be a “short-term malaise”. Recall that this is exactly the reaction that Fed Chairman Powell showed in September 2021. It should be noted that last spring we explained the structural nature of inflation, leading to its further growth.

Next week, negotiations between the US and Russia will begin, and it is very possible that the fate of the global dollar zone will be seriously addressed. The United States no longer has the resources to maintain it, but what will replace it is not yet entirely clear.

We wish our readers to quickly enter the workflow after the holidays.