Period: 20-26 June 2020

Top news story: The stock market crash on Wednesday and Thursday was the highlight of the week. It occurred amid massive cash injections and the beginning of recovery growth. This collapse clearly shows that optimistic sentiments are extremely weak. From a formal point of view, the fear of the second wave of the pandemic has caused the recession, but its scope suggests that the actual state of the economy appears to be threatening.

Macroeconomics

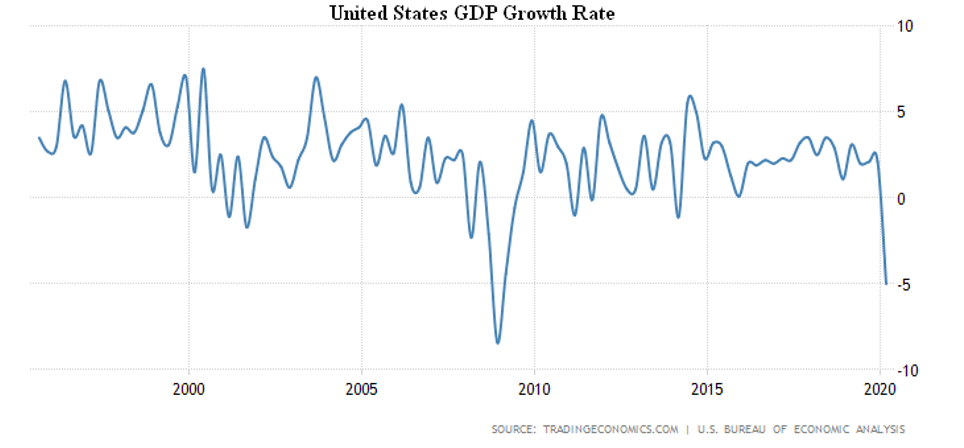

US GDP was confirmed at -5.0% per quarter on a year-over-year basis in Q1 2020 – the worst performance since 2008:

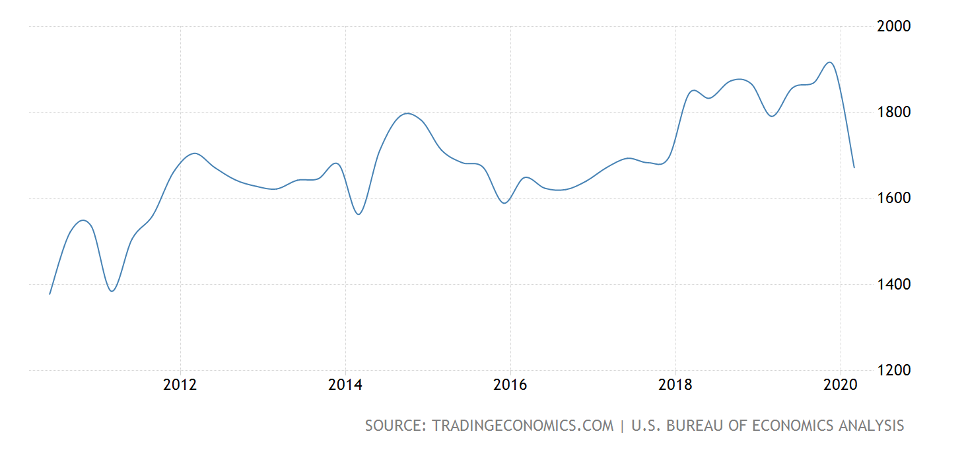

At the same time, corporate profits decreased by 12.4% (trough since 2008) to average 2012/17:

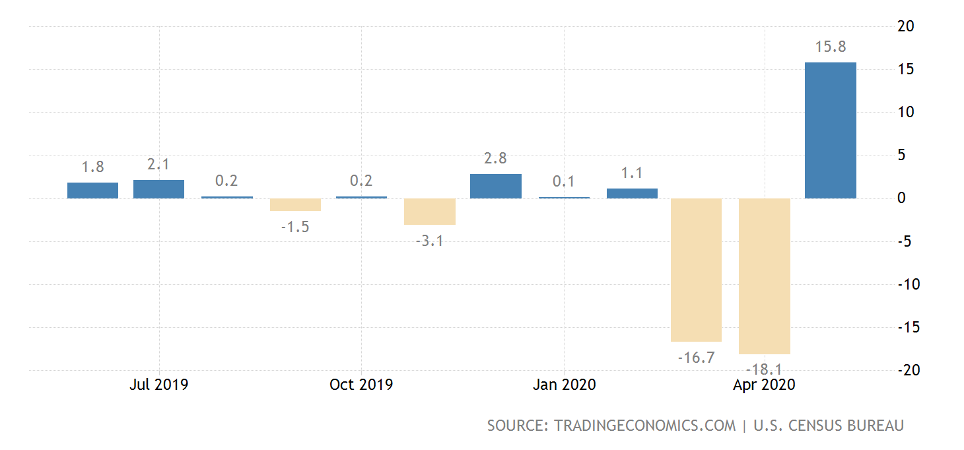

Durable goods orders (DGO) surged in May 2020 and remain 21% below the February level, offsetting less than half of the losses in March-April (month-to-month):

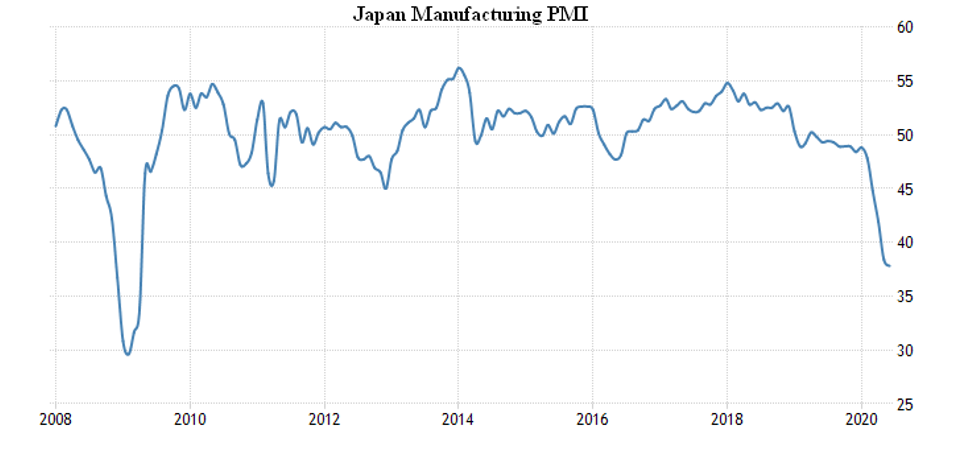

Japan’s All Industries Activity Index fell to 6,4% per month and 11,8% per year to a record low.

Both the coincident index and the Leading Economic Index are the weakest in 11 years:

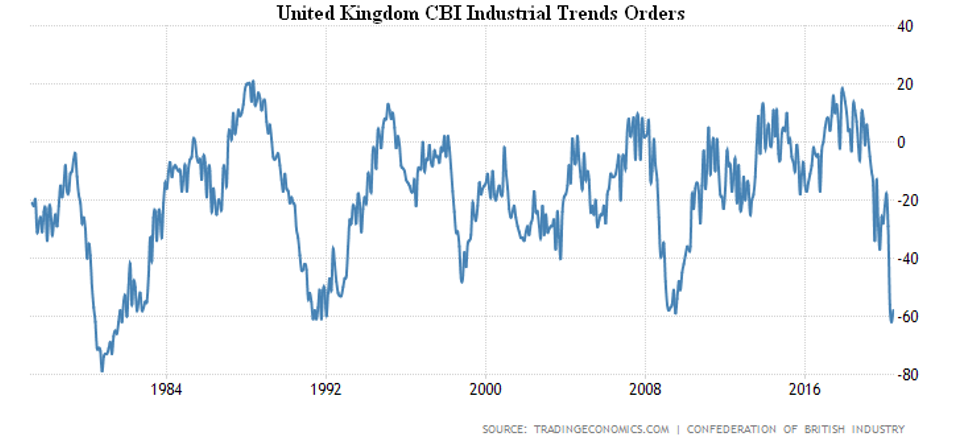

In June, the British industry’s order balance moved very slightly from its May level, the lowest since 1981:

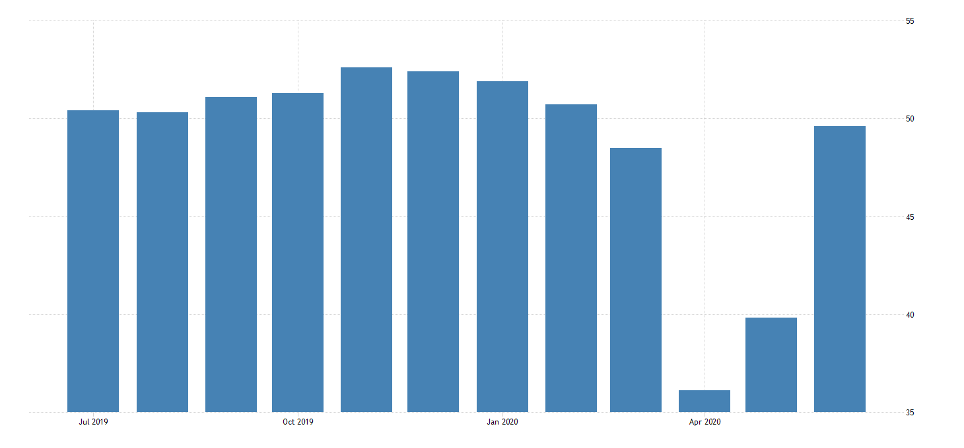

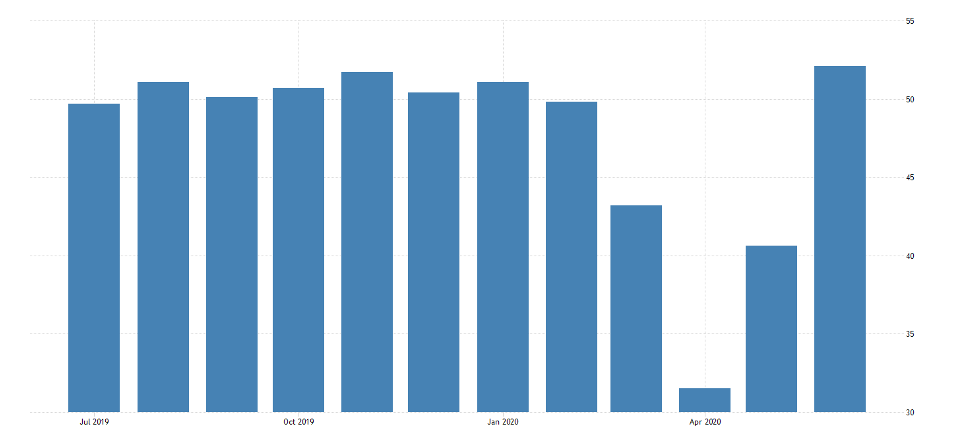

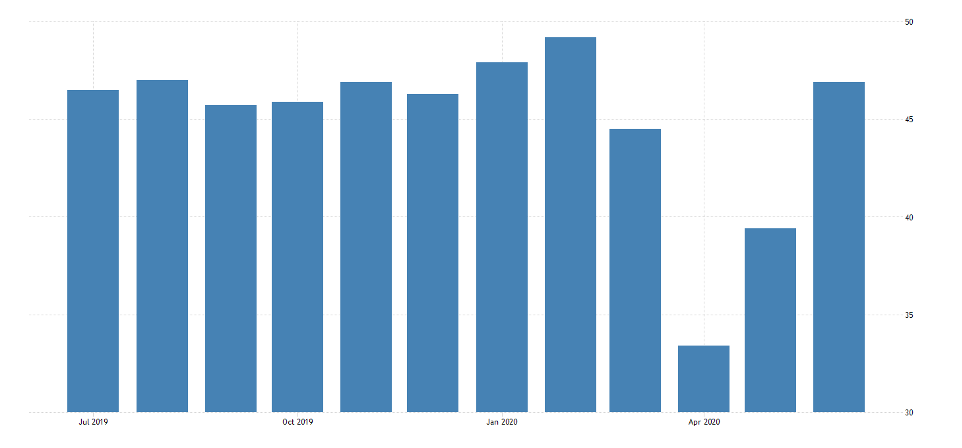

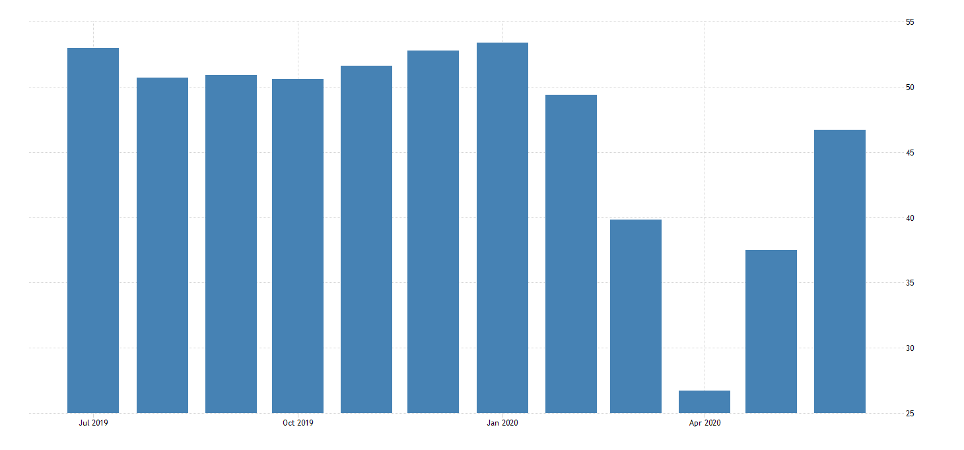

The industrial PMI index in June everywhere recovered sharply from the April-May failures:

France returned to growth zone:

Just like United Kingdom (UK).

US treads a fine line between decline and growth.

In the Eurozone in general, and in Germany in particular, there is still a decline.

In Japan, it even approached the trough in 11 years.

The same is true for services in Japan, France, Germany, the Eurozone, UK and the US:

Recall that PMI is a balance of positive and negative responses about a firm’s activity compared to last month. In fact, this index just marks the beginning of recovery growth following the March-April recession

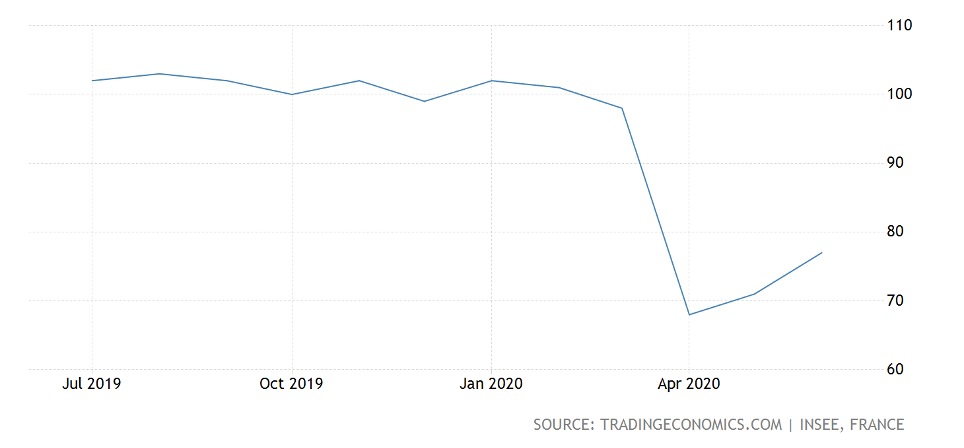

In France, business confidence is increasing, but it is still far from normal

In the same way as the business environment in it

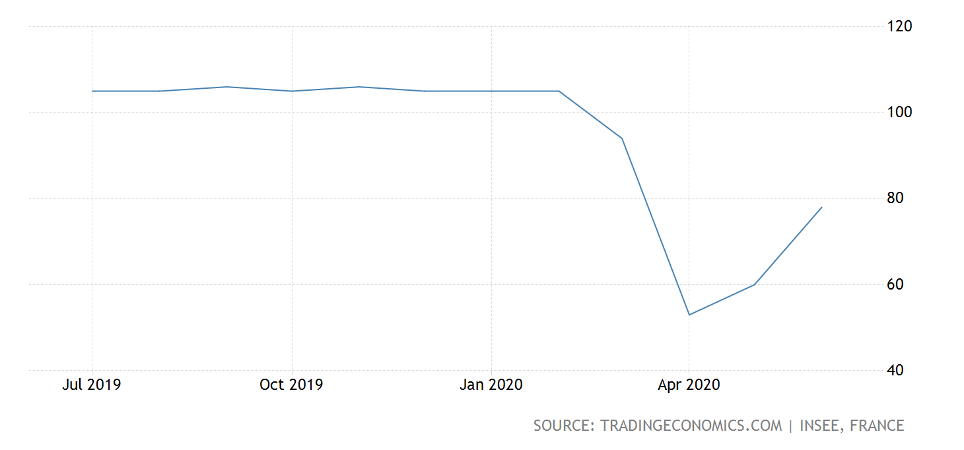

It’s the same in Germany.

In the US existing home sells fell 9,7% per month and 26,6% per year in May to the 10-year minimum (the worst trend since 1982), while sales of new buildings surged to 16,6% per month and 12,7% per year.

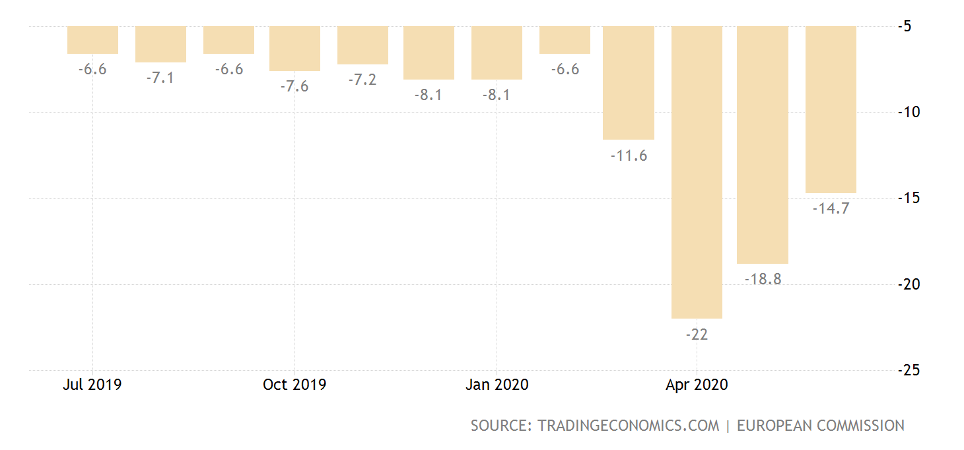

Eurozone consumers’ sentiments are slowly improving, but remain negative:

It’s the same in Germany, France and US

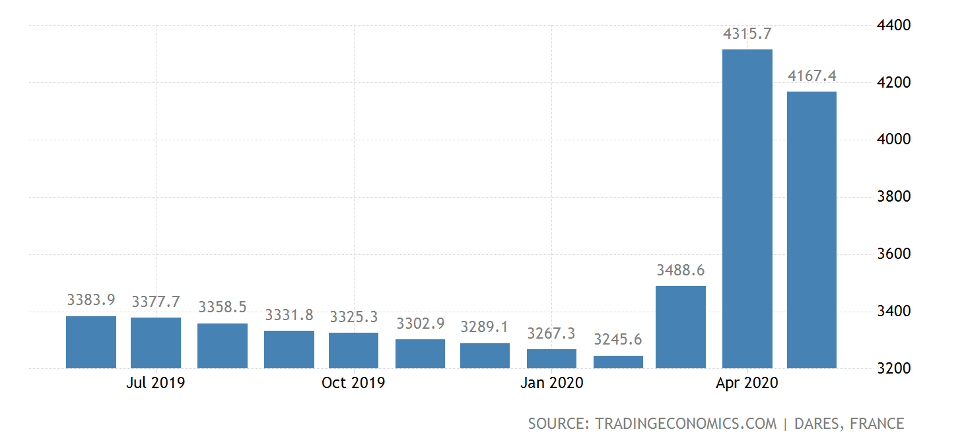

As yet, France has a huge number of unemployed, but their number has finally begun to decline.

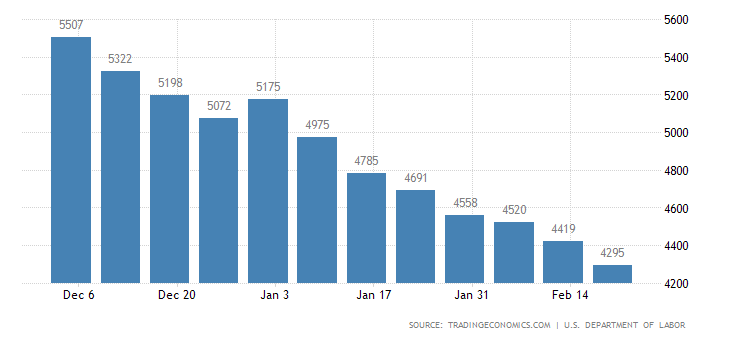

It’s the same in US:

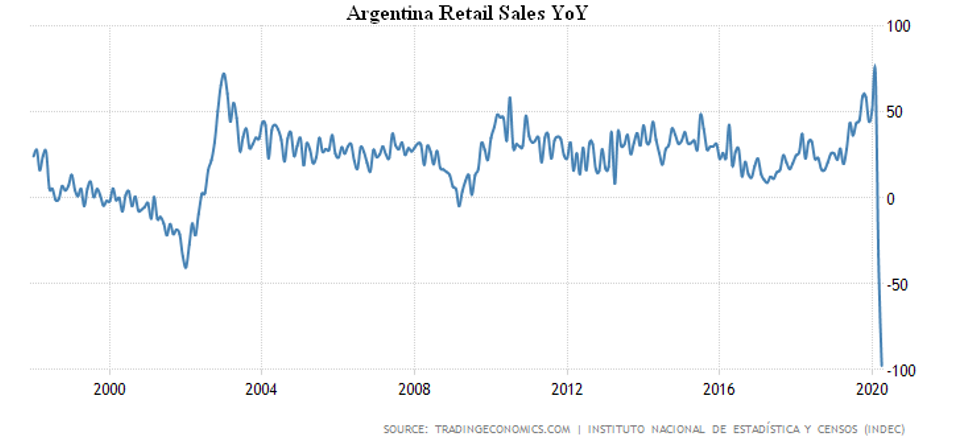

Retail sales collapsed worldwide in April, but the record went to Argentina, where sales dropped 97,6%, i.e. 42 times a year.

The Central Bank of Mexico cut the interest rate by 0,5% to 5,0%, and the Central Bank of China kept its monetary policy unchanged. The Central Bank of Turkey did the same, although the experts were waiting for further relief.

The ECB has launched a program to supply euro-currency to central banks outside the eurozone, but made it clear that it is ready to remove all recent incentives while easing COVID-19 shocks.

Summary: Almost the entire world economy has begun to recover, inevitably following sharp downturns. However, there are two main issues. The first is whether growth will stop in a few months or it will continue. The second is whether the recession will start again.

We expect continued growth until the autumn (perhaps until November, i.e., before the US elections), but the world economy, like the economy of developed countries, will not reach the level of the end of last year. At the same time, by the end of the year, the recession will have resumed owing to the earlier structural crisis of the world economy or, otherwise, the impossibility of further stimulating global aggregate demand.