Period: 23-30 May 2020

Main topic: Various macroeconomic parameters show a way out of the crisis (unlike the previous week, when hopes were purely psychological). This greatly strengthened consumers’ hopes for a full way out of the crisis by the fall. Since these hopes will collapse by the middle of autumn (see the «Conclusions» section), we will inevitably face a serious psychological shock by the end of the year. However, it is possible that these hopes will reduce the upward trend in savings noted in one of the previous reviews, which, temporarily, will increase aggregate demand.

Macroeconomics

Profits from China’s industrial companies recovered in April to -4.3% per annum after -34.9% in March.

Leading indicators of Japan in March are the weakest since June 2009. Coinciding – since June 2011. As well as the activity of all sectors of the economy (see the graph).

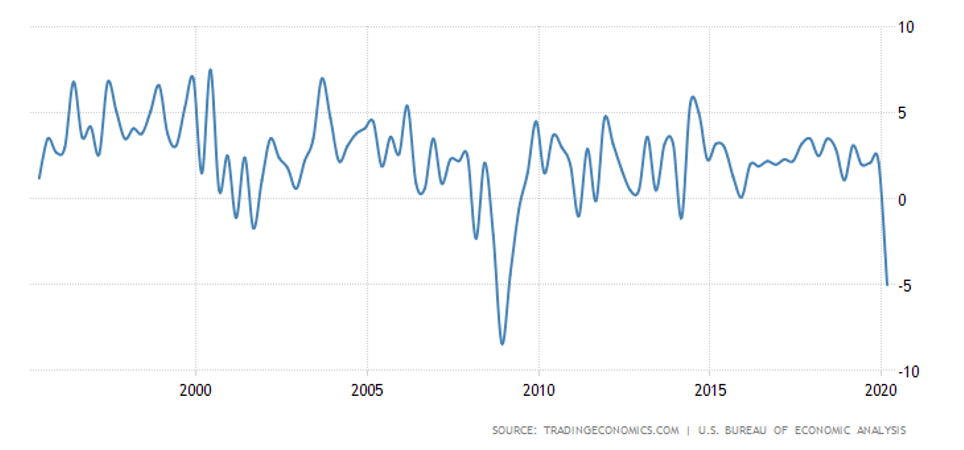

US GDP in 1 quarter revised down to -5.0% «on an annualized basis» – bottom since the end of 2008 (see chart); 2Q forecast gives -40%.

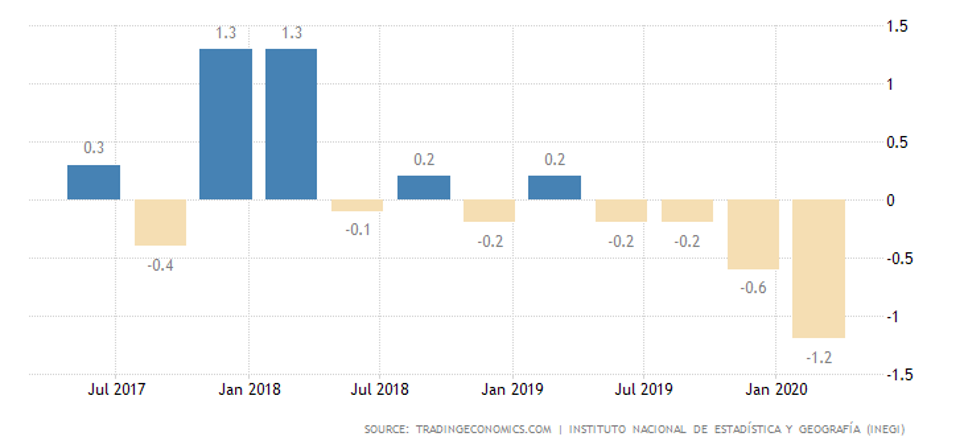

A similar picture in Mexico:

In France, -5.3% per quarter (bottom since 1968) and 5.0% per year (record minimum for 70 years of observation)

In Italy, -5.3% per quarter (anti-record for 60 years of observation) and -5.4% per year (11-year low).

Germany’s GDP in January-March fell 2.2% per quarter and 2.3% per year – both are the worst in 11 years.

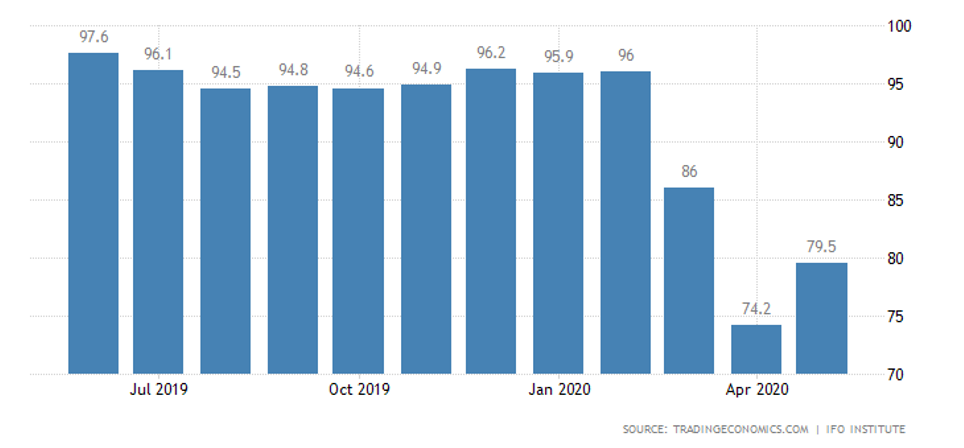

Germany’s business climate in May improved slightly from the record bottom of April (see table), but remained very weak; Assessment of the current situation has become even bleaker.

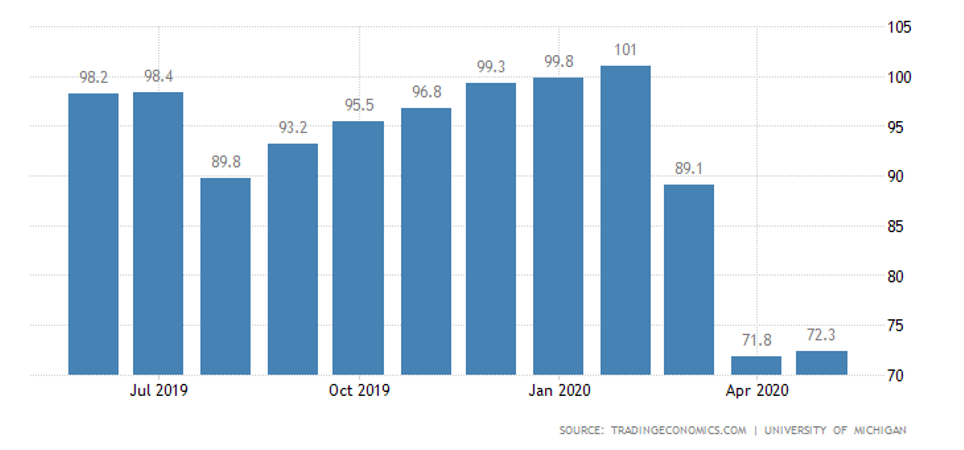

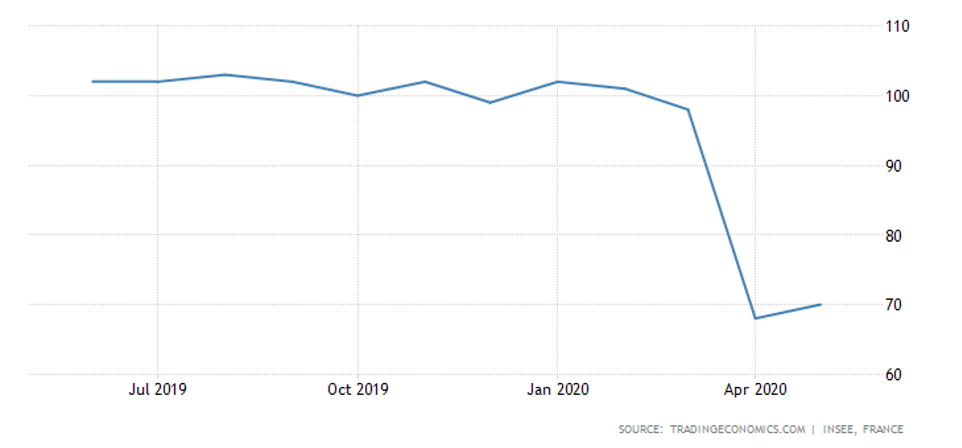

The same with consumer sentiment in Germany, Japan and the United States (see chart):

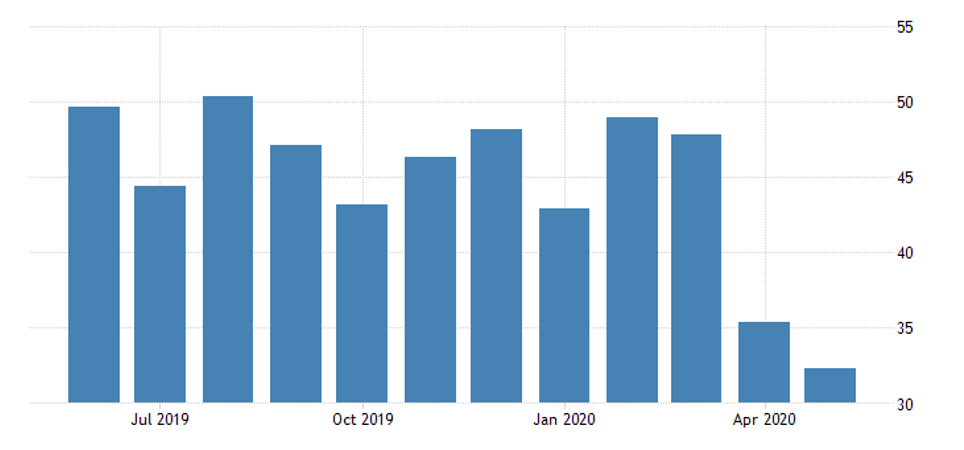

The situation with the business climate in France is the same as with business confidence (see graph):

The eurozone as a whole is still worse: business confidence is the weakest since September 2009 (see table):

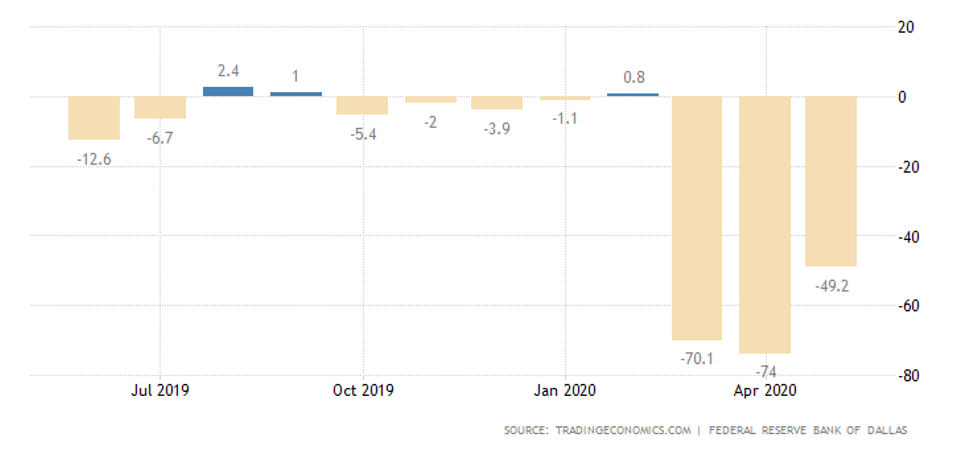

A similar picture in the regional activity indices in the USA: from the Federal Reserve Banks of Dallas:

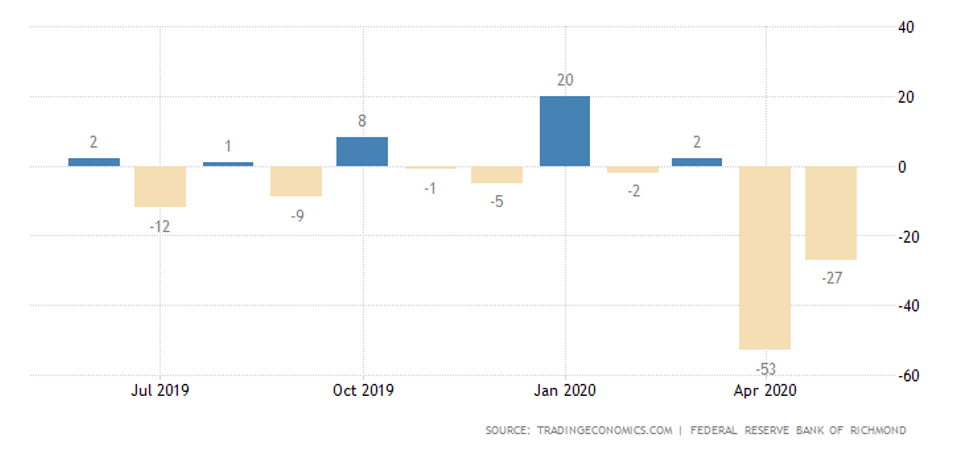

Richmond and Kansas (see below):

But the PMI of Chicago has a new low since March 1982:

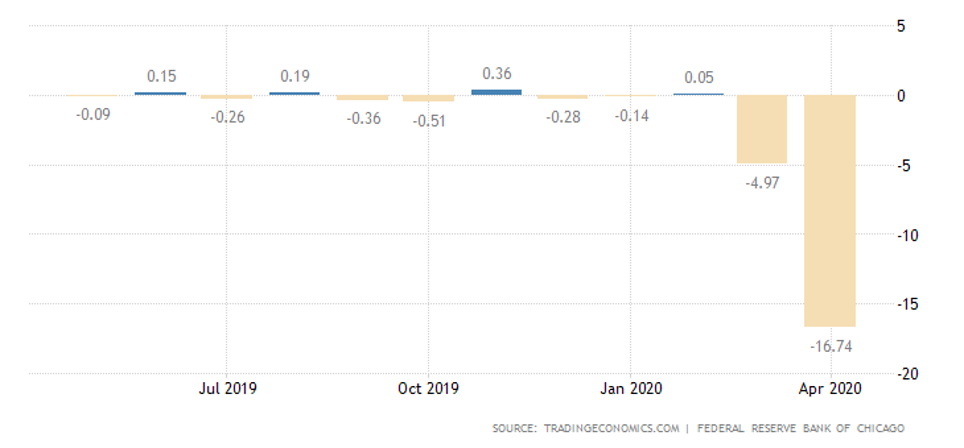

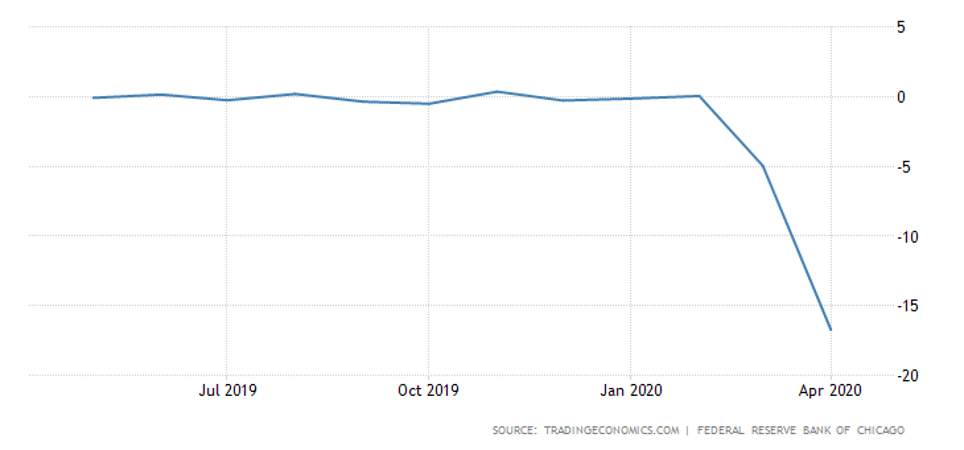

The US National Activity Index from the Federal Reserve Bank of Chicago collapsed in April at an unprecedented pace for all 53 years of observation, and the previous record (the mid-1970s) was five times exceeded right away (see table).

Industrial production in Japan in April fell by 9.1% per month and 14.4% per year – a 9-year low.

Car production in Britain collapsed 300 times a year in April, to levels unprecedented for the entire observation period after the Second World War (see graph):

Orders for durable goods in the US in April fell another 17.2% per month after a collapse of 16.6% in March.

Sales of new buildings in the US in April increased by 0.6% per month and fell by 6.2% per year; a collapse was expected, but it turned out not so bad, but the secret is simple – the median price fell by 9.1% per year, which supported demand. Incomplete secondary home sales in the States fell 21.8% per month and 33.8% per year.

Building permits in Canada in April fell another 17.1% per month (the worst dynamics since October 2008) after -13.4% in March, dropping to a 9-year low.

Retail in Russia collapsed by 23.4% per year – an unprecedented pace for all the years of observation since 1994 (actually since 1970).

It falls even steeper in Spain: by 20.4% per month and 31.6% per year.

In Japan, -9.6% per month and -13.7% per year – lowest for half a century of observations, it was worse only once, at the beginning of 1998.

In Germany, only -5.3% per month and -6.5% per year – but this is also an 11-year minimum.

Consumer spending in the US in April fell by 13.6% per month – nothing similar happened in over 61 years of observation.

Consumer spending in France in April fell another 20.2% after a collapse of 16.9% in March – the lows for 40 years of observation.

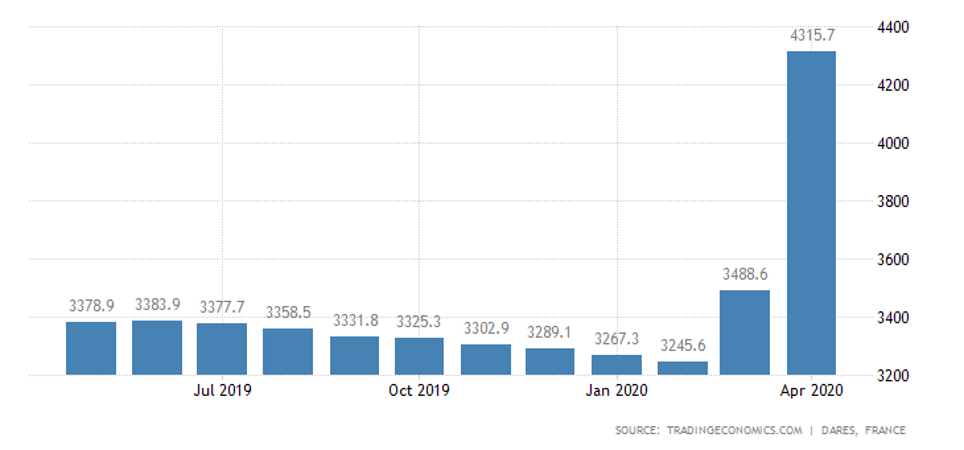

Unemployment in France soared at an unprecedented rate, as did the total number of unemployed – which, incidentally, was pretty big before the epidemic:

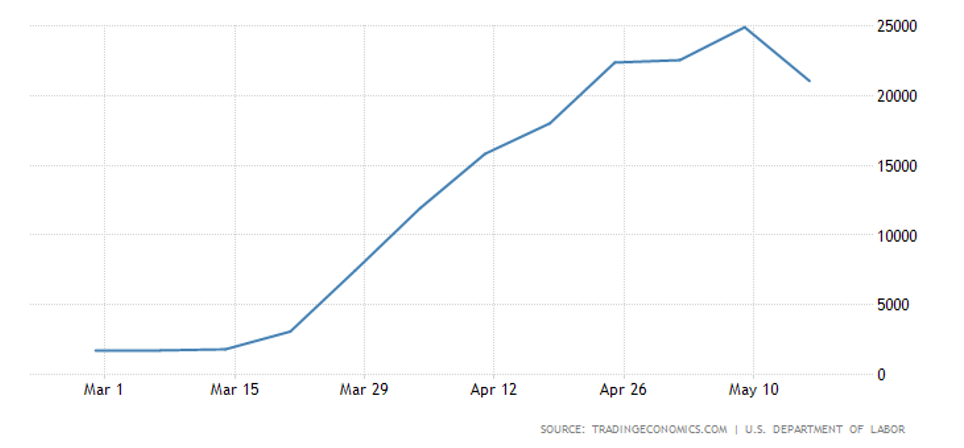

In the USA, another 2 million unemployed were added. Some enterprises have already started to work again – therefore, the total number of recipients of welfare slightly fell

The Central Bank of South Korea cut the rate by 0.25% to a record low of 0.50%.

Conclusions: The panic of the first months of the epidemic begins to end, and the enormous amount of money issued (whose entry into the economy is far from complete) also played a role. And if at the first stage of the coronavirus panic, enterprises were not inclined to restore their activities and pay wages, now this process has begun. At the same time, taking into account the money that consumers received, there is no way to understand what the real demand after quarantine will be.

We believe that, since structural imbalances today can only be maintained through direct emissions, by the end of the quarantine, aggregate demand will fall (taking into account inflationary processes). But today its real indicators are so «clogged» with money issue that it is impossible to determine them. Accordingly, the current situation is determined by the throwing of both consumers and producers from a state of panic to a state of unjustified optimism. A more or less intelligible picture can only be understood in the fall. For the United States, we suggest – by the end of November this year.

The key moment for the coming months for any entrepreneurs (and for households as well) is to evaluate their real resources and try to optimize them until the situation becomes more or less predictable.