Period: 27 March – 02 April 2021

Top news story: No doubt the big news this week is that Biden has announced an economic program. And even, more specifically, a third increase in corporate taxes. The core of the problem lies in the mismatch between household income and expenditure, and households spend significantly more. Details about the structural crisis in the world and American economy are given in the book M. Khazin «Reminiscences about the Future. Ideas of a New Economy», English version. Here, it must be emphasized that simulating private demand is a key challenge in the US economy. But tax increases hit aggregate demand – it only goes down. However, even if all of the money from these taxes were diverted to infrastructure, it would still not increase citizens by the amount by which they decreased in the process of their withdrawal.

In other words, Biden plan will not improve the economy, as aggregate demand will only fall. And hes still has to be stimulated with an emission boost. Given that inflation is already on the rise, this can only accelerate the decline. We note that in the report of the M. Khazin Foundation for Economic Research on the comparison of the «Trump Plan» and the «Biden Plan», published before the elections in the United States, we analyzed the scope of the respective processes.

The M. Khazin Foundation for Economic Research will analyze the implications of Biden policies in more detail in its new reports in the near future, but the main conclusion is that it is impossible to come up with any real measures to improve the state of the US economy.

Macroeconomics

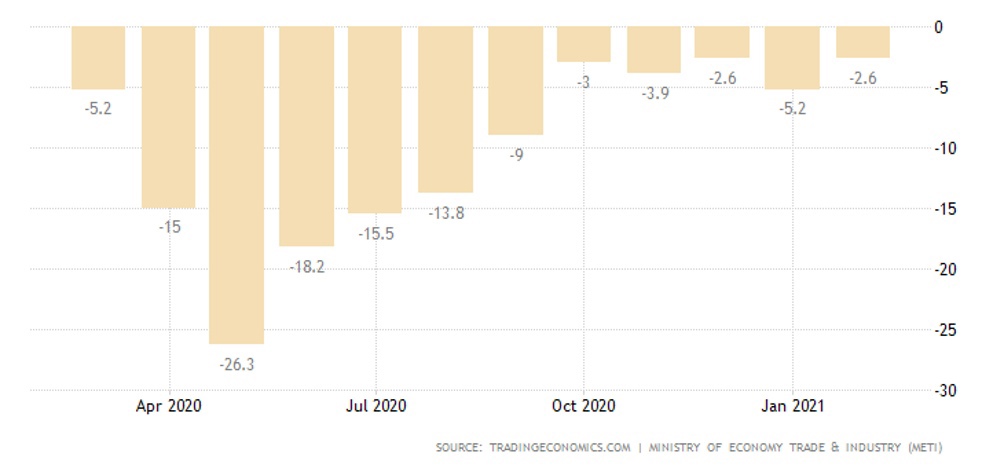

Industrial production in Japan has returned to a monthly loss, and the annual loss also stands:

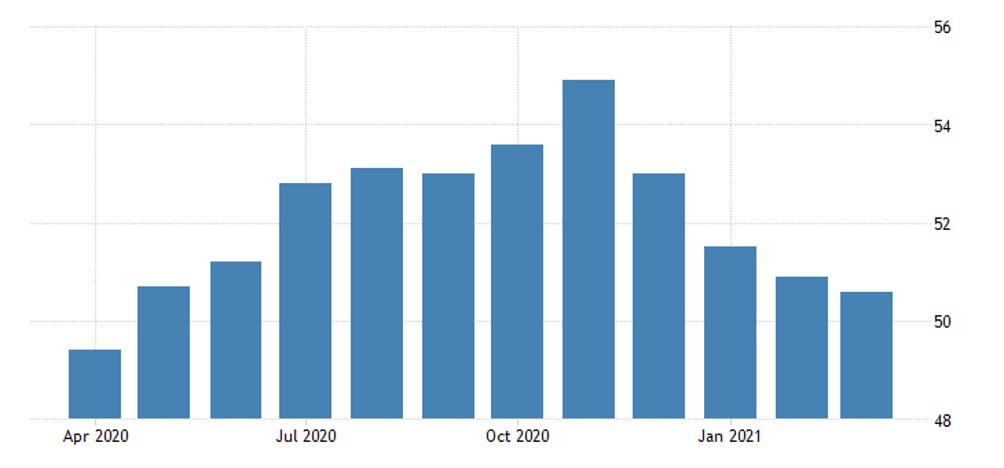

Chinas lowest manufacturing PMI (Purchasing Managers Index) in a year:

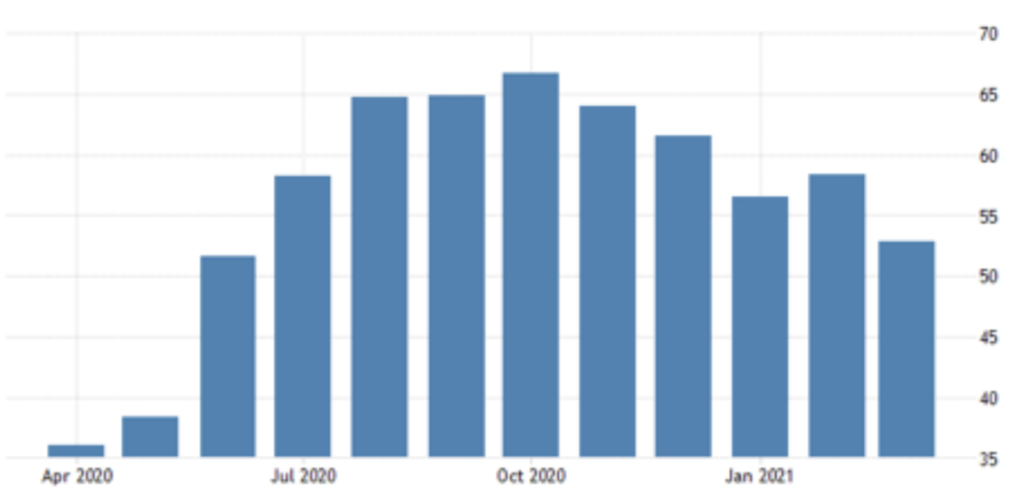

A similar situation is seen in Brazil:

Let us remind that the value of this index more than 50 means growth of the respective industries, less than 50 – decrease.

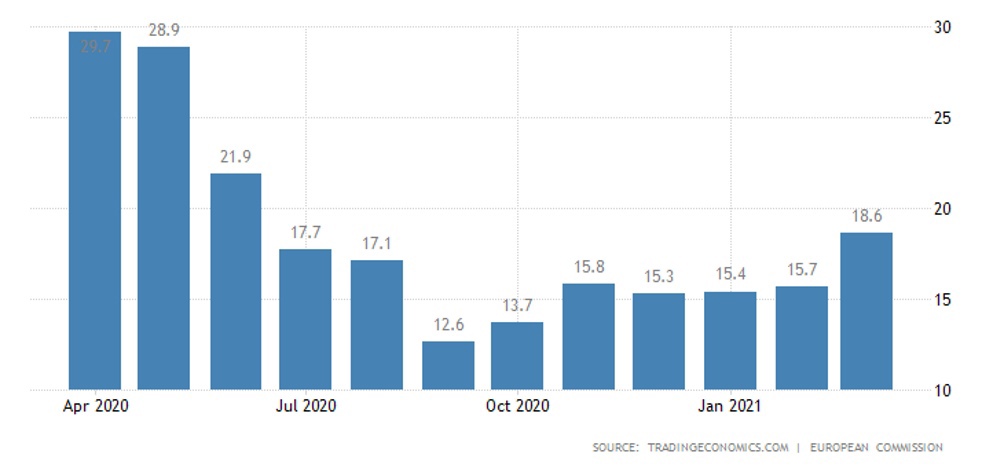

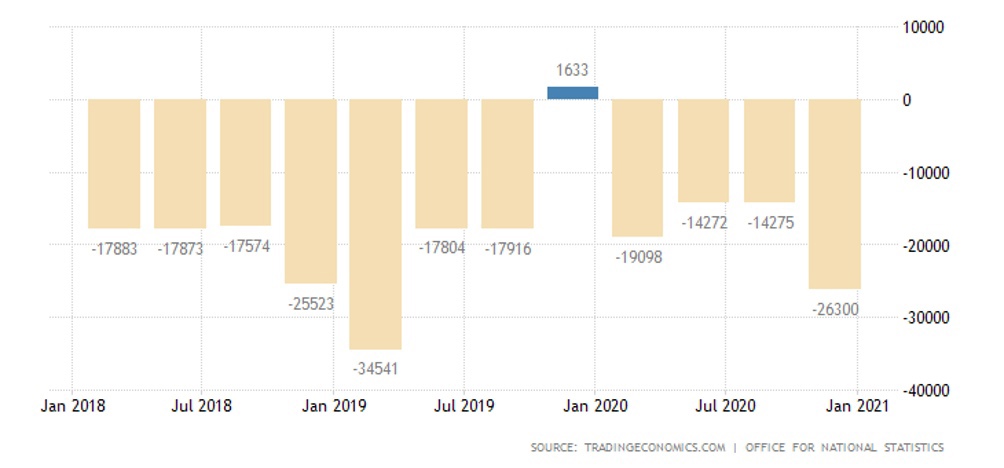

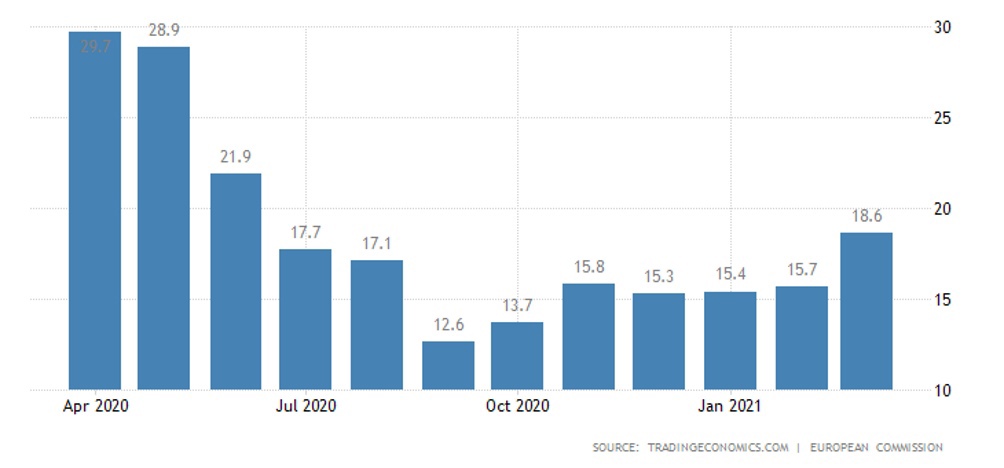

Britains current-account deficit approached a peak in early 2019:

Import prices in Germany rose by +1,4% per year, up from almost two years. The PPI (Producer Price Index) in Italy is the highest since June 2019, + 0,7% per year. PPI of France at its peak in 2 years (+ 1,8% per year).

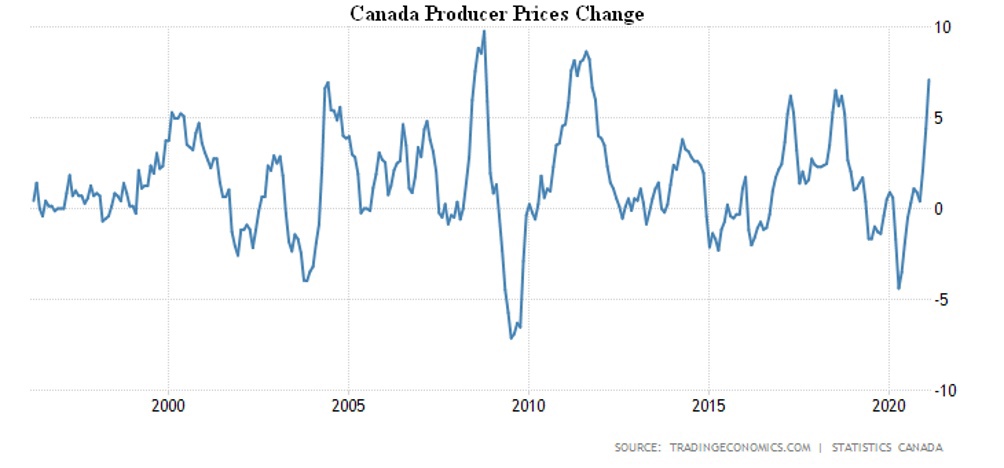

PPI of Canada surged by 2,6% per month (a record in 41 years), making the annual growth (+7,1%) the largest since 2011:

Inflation expectations in the Euro Area are the strongest in nine months:

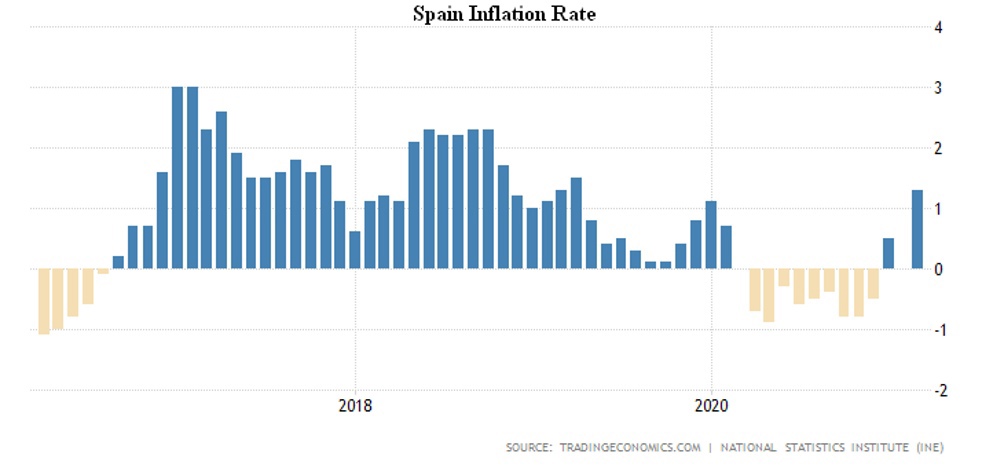

CPI (Consumer Price index) of Spain at its peak in 2 years (+1,3%):

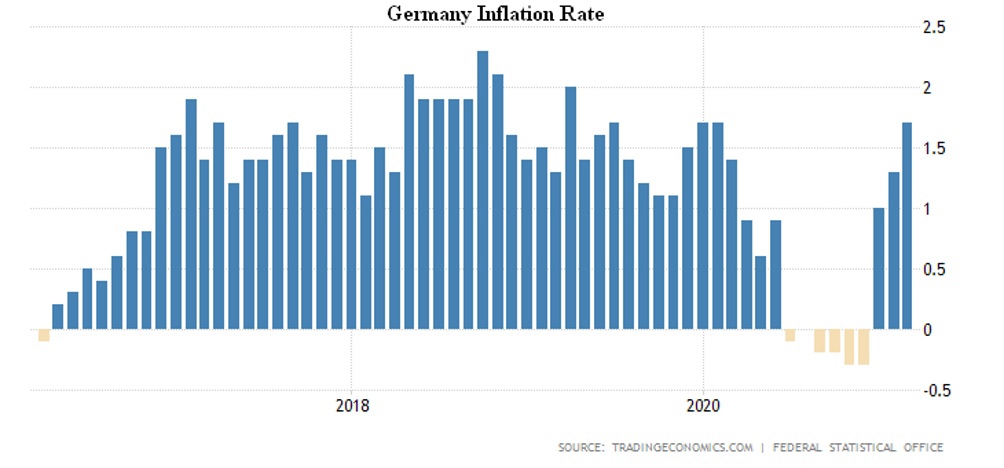

Similarly in Germany:

Consumer prices are rising in Italy and France, 0,8% and 1,1% respectively, the annual maximum.

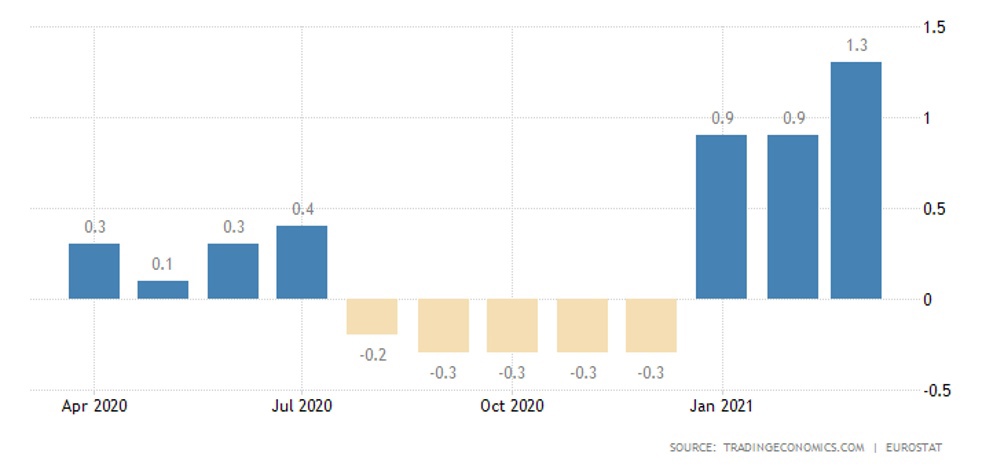

Similar processes across the Euro Area:

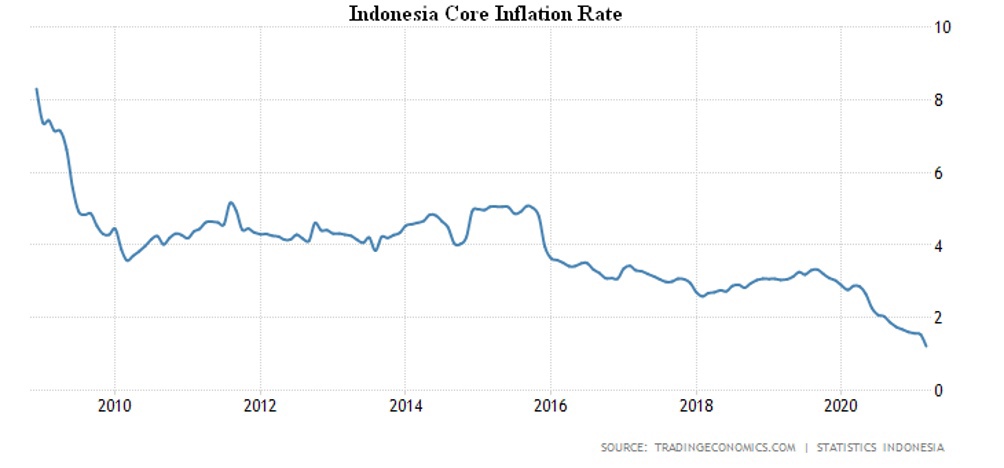

In South Korea, the peak since November 2018 (+1,5%), the same as in Indonesia, net inflation is at a record low (+1,21% per year), indicating a predominance of deflation trends:

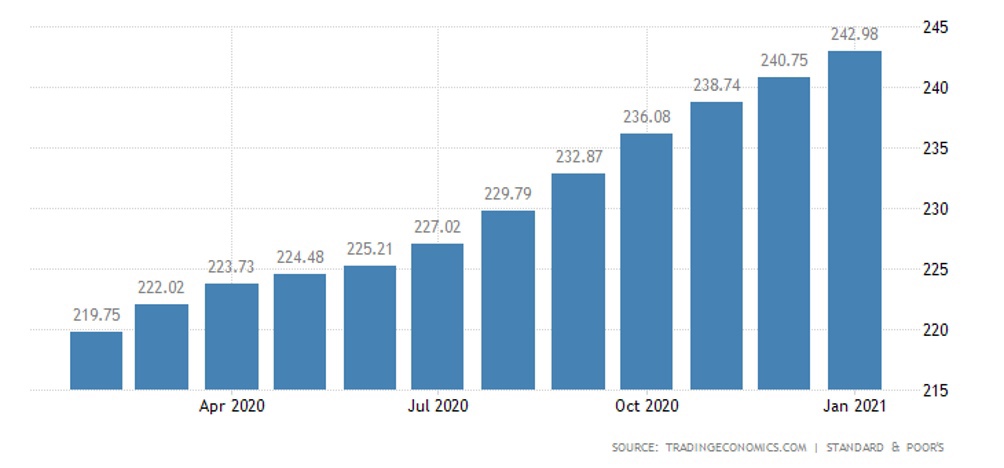

S&P/CoreLogic/Case-Shillers US housing prices are rising at the fastest rate in 16 years (11,2% per year):

Official statistics vary slightly, 12,0 % per year.

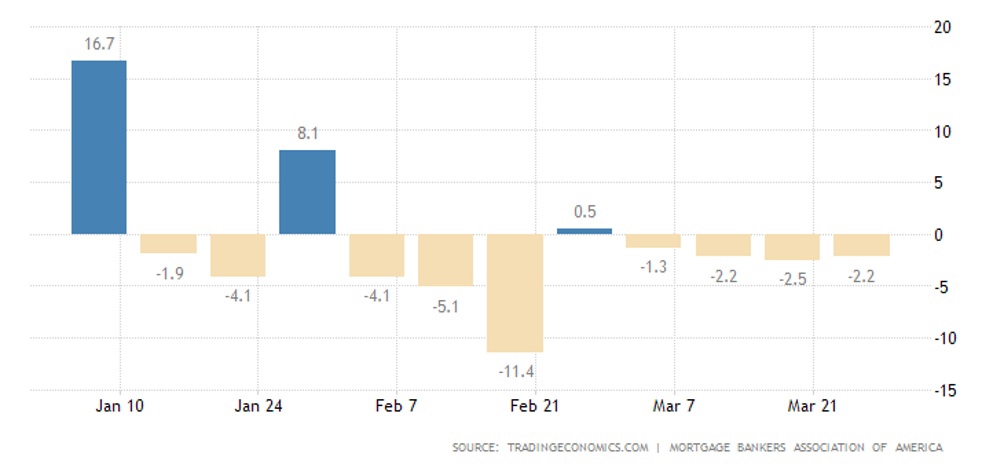

The number of approved applications for mortgages in Britain is minimal in six months, in the US, the decline also continues:

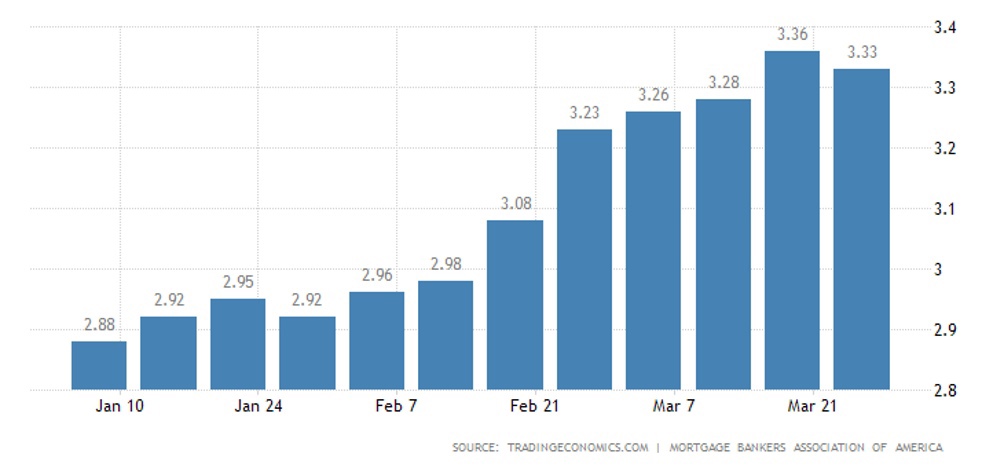

Notwithstanding the stabilization of mortgage rates:

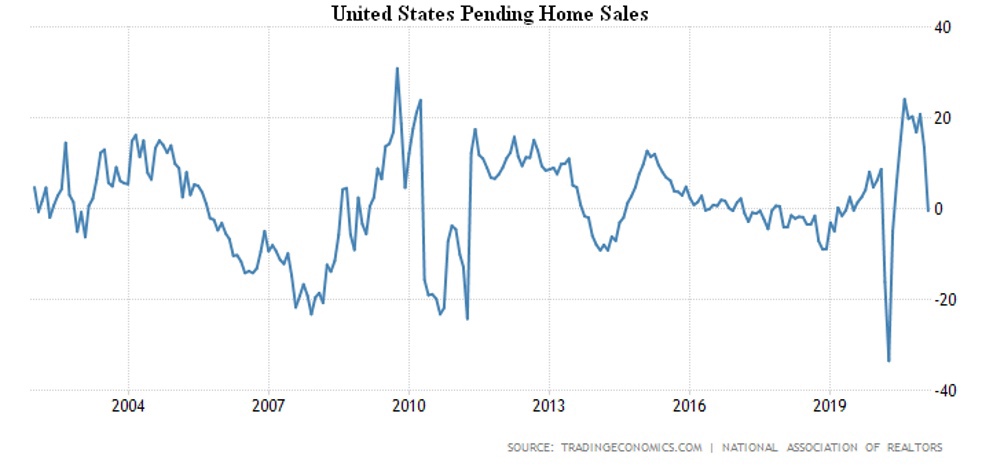

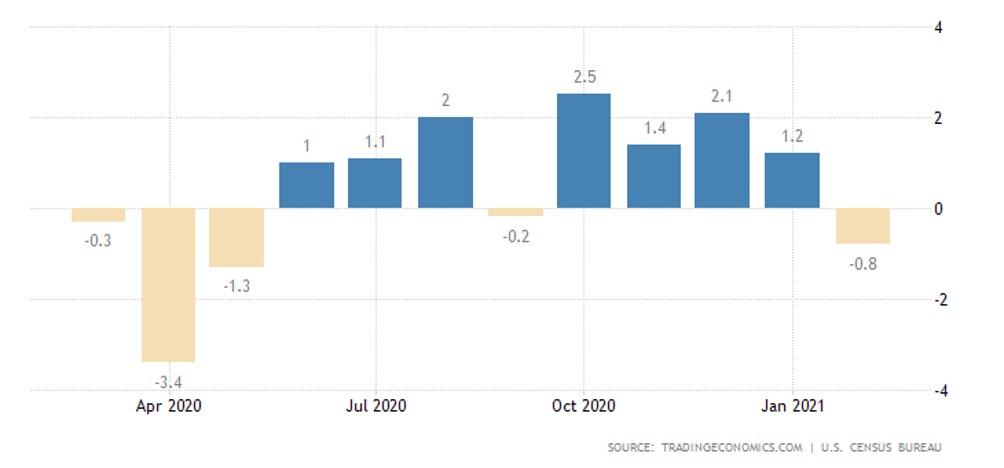

Incomplete home sales in the United States fell 10,6% per month and 0,5% per year, the first annual loss since May 2020:

Construction spending also decreased:

Brazilian unemployment rises again amid worsening Covid-19 situation.

Summary: In general, the assumption made in the previous review – that inflation has started in the world – is confirmed. Accordingly, since official inflation rates are always much more optimistic than reality, we will be witnessing a decline in aggregate demand in the coming months and, as a consequence, a decline in production. This may be a mix of price increases (i.e., nominal increases in financial flows), but as households measure their wealth not by money, but by purchases, we will inevitably see a fall in purchasing optimism.

As a result, the pace of the global recession will become faster, and either the monetary authorities will continue their stimulus (with inflation and real disposable incomes gathering pace), or monetary policy will be tightened. In this case, the simulation of private demand will be reduced, meaning that sales will fall again (albeit for another reason).

In general, this is typical and characteristic of a structural crisis until real household income and expenditure are balanced. Biden’s plan, described at the beginning of the review, in this situation is not able to change anything, it’s only a matter of the rate of recession. It is likely that before the crash of financial markets in the US, it will not change very much.

We wish all our readers a happy weekend and a good work week!