Time period: 6-12 November 2021

Top news story. Reading the materials of numerous media outlets, one can conclude: the main news is the record consumer inflation in the US. However, for the readers of our Reviews, there is nothing new in this: we have explained many times in detail both the reason why an increase in consumer inflation is inevitable and the reason why industrial inflation will not be reduced. We will repeat this in the following section.

And here’s the real headline: The Glasgow Environmental Summit ended quietly. What the failure of the “green” project is to be, became clear a few months ago. Let’s be clear: a few months ago, it would have been possible to find information for an overage user (not a professional), from which this would have uniquely followed. But last week the situation became clear – and even the outspoken apologists of this development realized that the chances of success are almost indistinguishable from zero.

This does not mean that no attempt will be made to do anything, in particular – the new German government may, in a hopeless attempt to introduce “green” reforms, wipe out and exhaust all the resources that could be used to combat the crisis. Moreover, there are countries in the world (“Who said, ‘London?’”) that will support such a suicide policy of Germany. We are obliged to take this situation into consideration and to communicate it to our readers, but the objective picture is already finished.

Macroeconomics

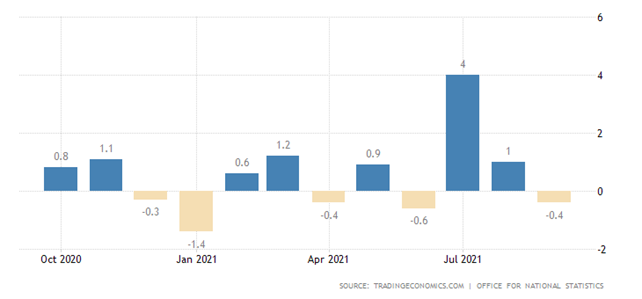

Britain’s industrial output slumped by 0.4% per month:

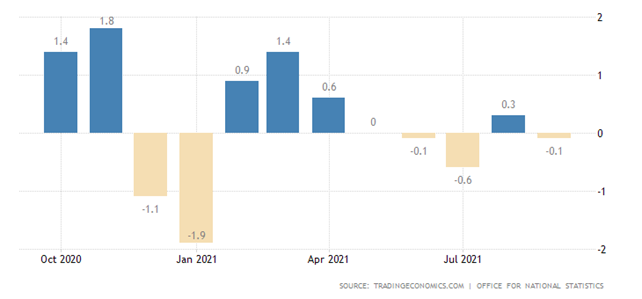

Worse still, in manufacturing, where there has been only one positive indicator in the last five months:

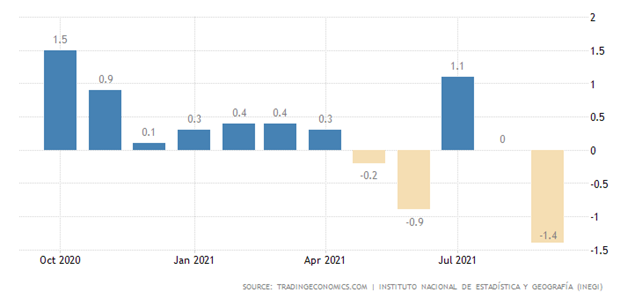

Similarly, in Mexico, the single positive rate is 5 months, and in September -1.4% (the lowest since April 2020):

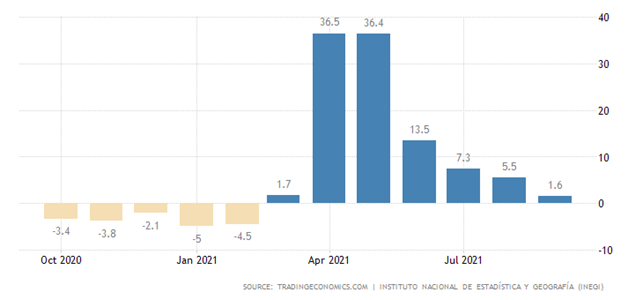

And the annual growth rate is the worst in seven months (+1.6%):

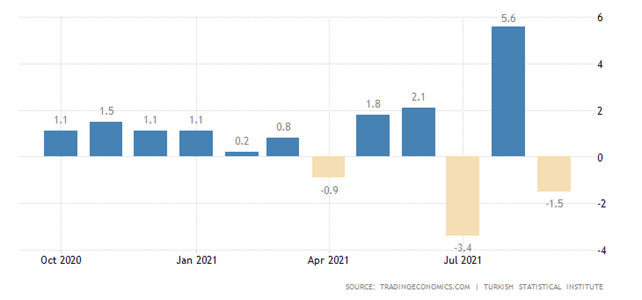

Industrial production also dropped in Turkey (-1.5% per month) – for the second time in the red zone in the last 3 months. However, with industrial inflation rate above 40% (see the previous Review), this is not surprising:

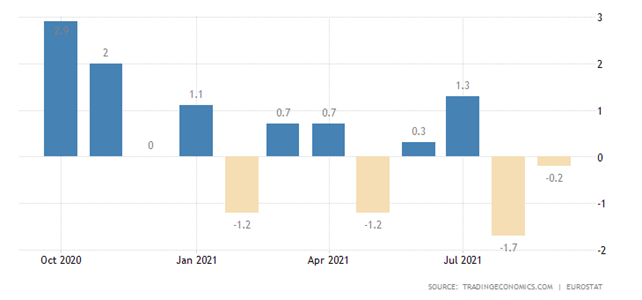

In the industrial production of the Euro Area, the second-monthly consecutive negative:

It is very likely that the last peaks in the previous two graphs, in Turkey in August and in the Euro Area in July, are caused precisely by the underestimated inflation indicators: the authorities were completely unwilling to recognize the real economic situation.

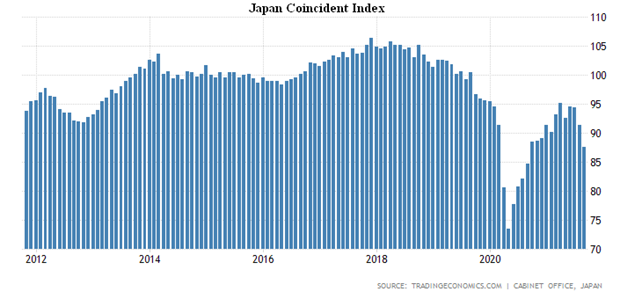

Japan’s Coincident Index is the worst in a year:

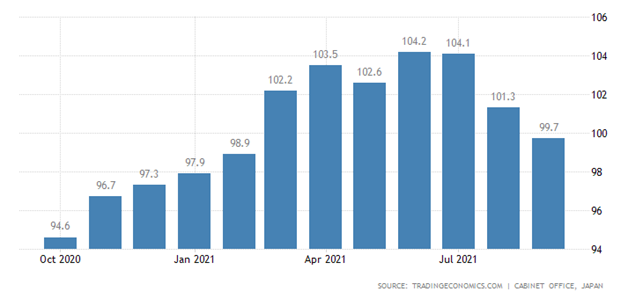

Leading indicators at the trough for 7 months:

Accordingly, business sentiment in the Japanese manufacturing industry (Reuters Tankan survey) is the weakest in 8 months:

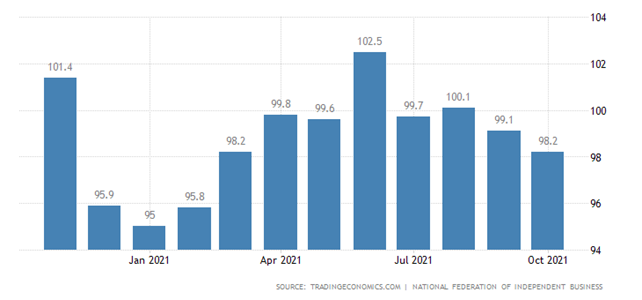

Exactly the same pattern is seen with optimism by small businesses in the US, the weakest in eight months:

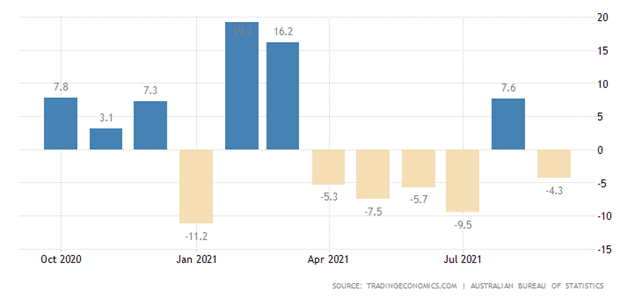

One can only be happy for the collective wisdom of small businesses in the US, which predicts the situation almost as much as we do, and admits the negative trends in the economy, far ahead of official sources. Building permits in Australia -4.3% per month – 5th time in the red in the last 6 months:

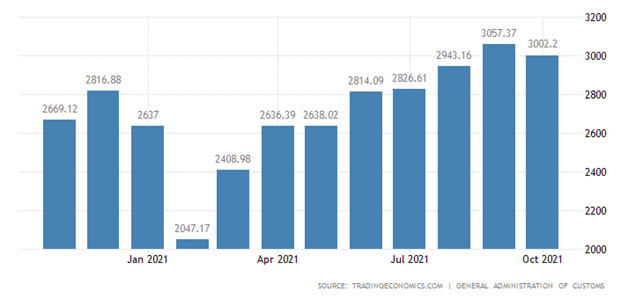

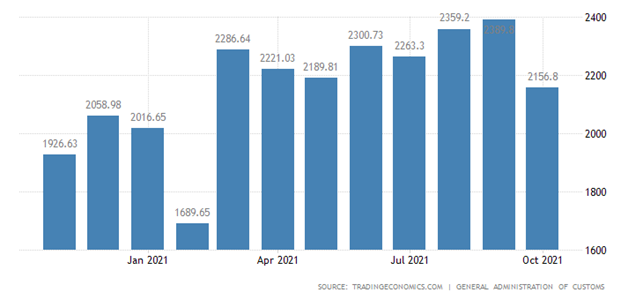

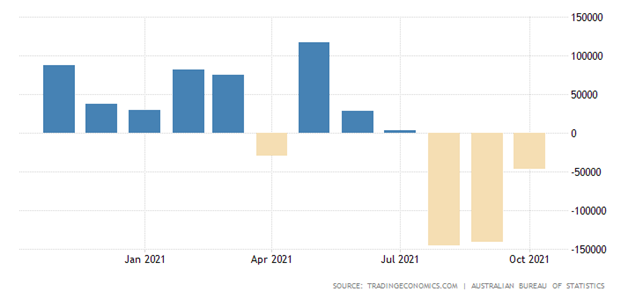

China’s trade surplus in October is record-breaking:

However, exports and imports have slightly moved away from the historic peaks of September:

Britain’s trade deficit is the worst in eight months:

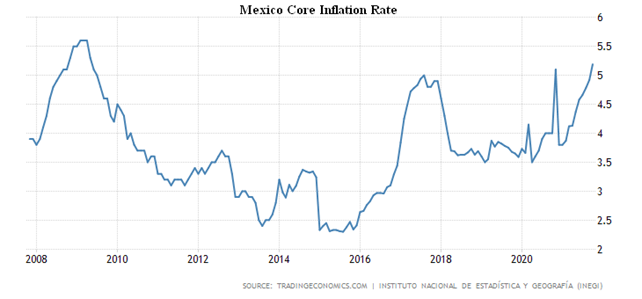

And then we start with inflation data, which, of course, our readers are prepared for, but it’s still very conspicuous. CPI (Consumer Price Index) of Mexico is the highest since 2017 (+6.2%):

Without food and energy, the minimum since 2009 (+5.2%):

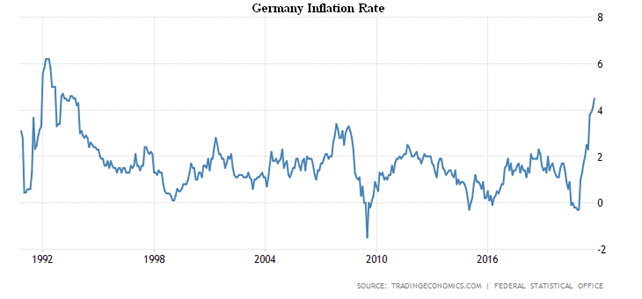

CPI Germany (+4.5% per year) is on the top since 1993:

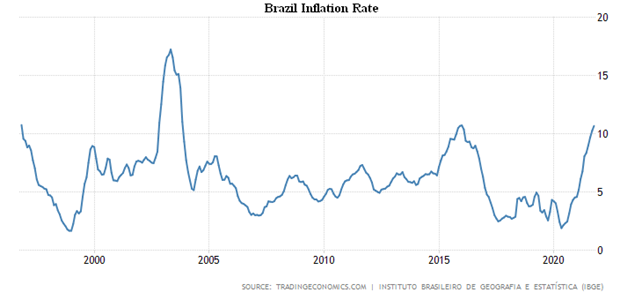

CPI Brazil +10.7% per annum, repeating 2003 peak:

CPI of China (+1.5% per annum) the highest in 13 months:

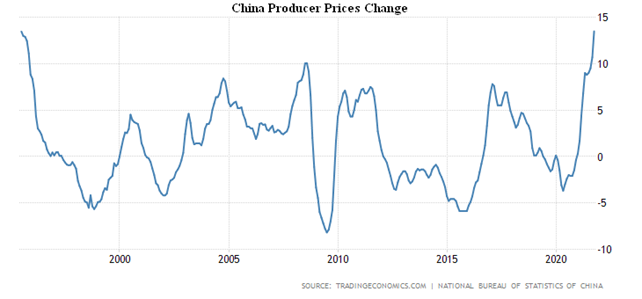

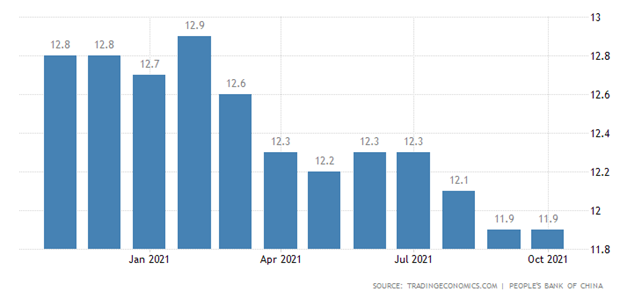

PPI (Producer Price Index) of China (+13.5% per year) is the highest ever observed since 1995:

And this is happening against the backdrop of a credit crunch – its performance (+11.9% per year) is the worst since 2002:

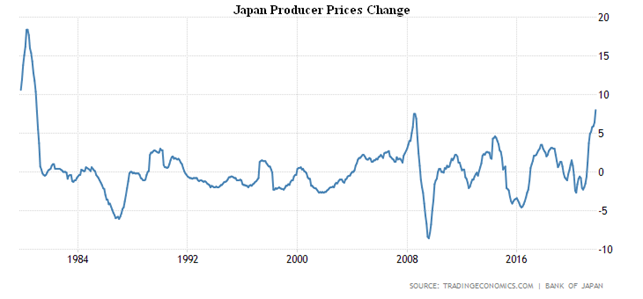

Japan’s PPI +8.0% per annum, peak since January 1981:

And now, the promised US figures.

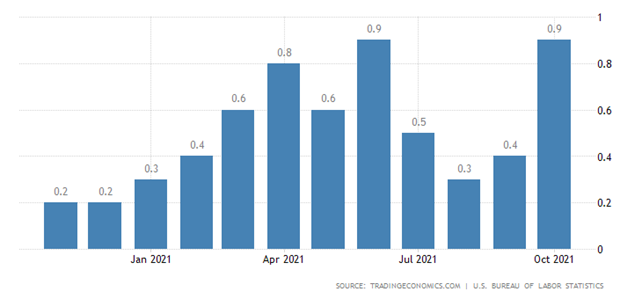

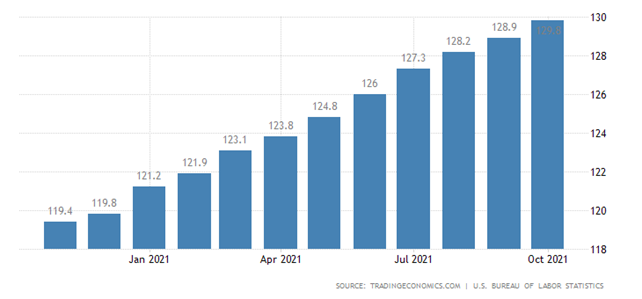

US CPI + 0.9% per month repeats the record since 2008:

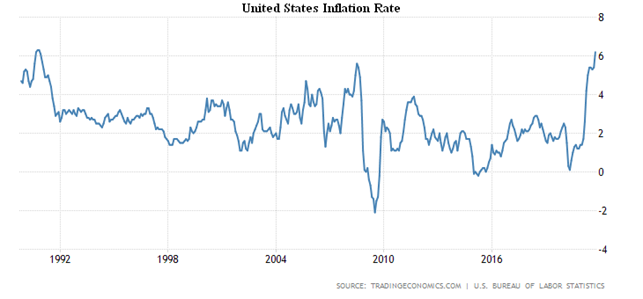

And +6.2% per year, which is only 0.1% of the 1990 peak:

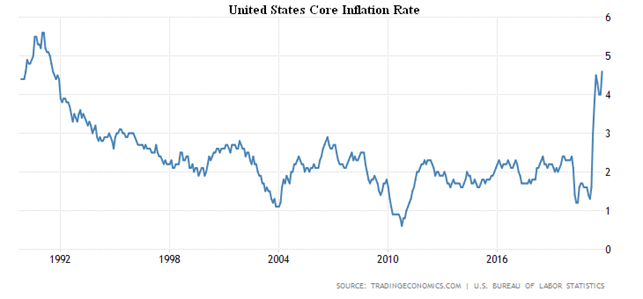

Without food and energy +4.6% per year, which is the maximum since 1991:

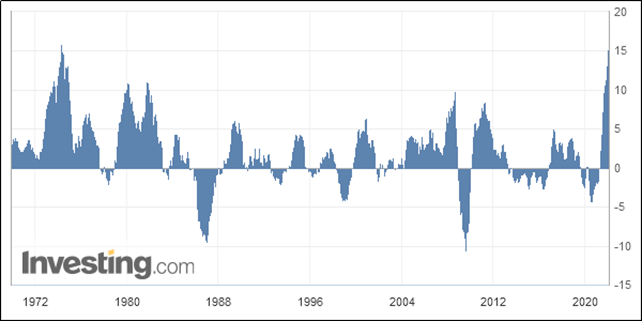

US PPI +0.6% per month amid rising commodity prices (+1.2%):

Already +8.6% per annum has been reached in a year, which is still the highest since 2008:

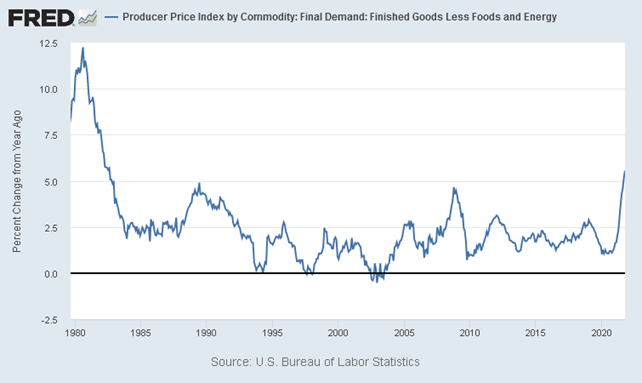

And then there are some interesting indicators that reviewers tend to hide from the public. PPI for finished goods excluding food and energy +5.5% per year is the highest since 1982:

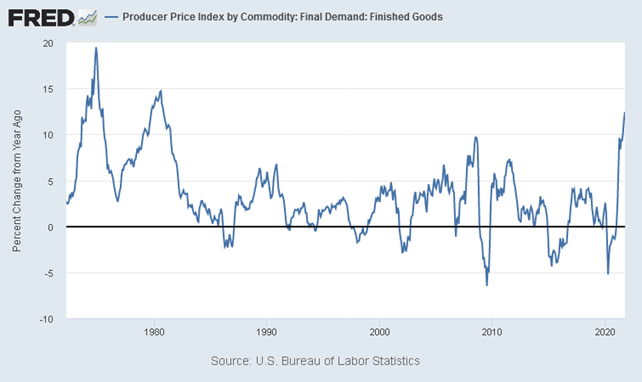

For finished goods as a whole 12.2% per year, which is on the top since 1980:

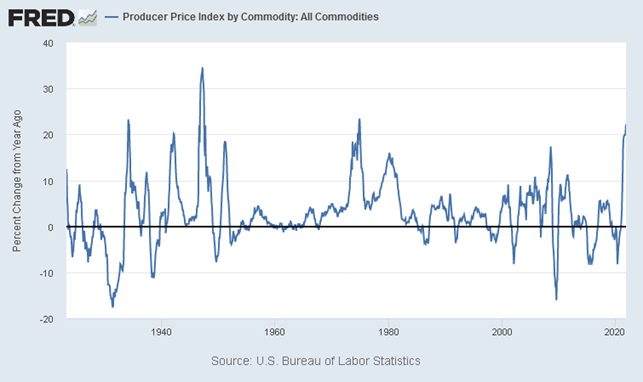

And finally, for all commodities +22.2% per year – this is a record figure since 1974 and is only 1.2% from the peak since 1947:

This, the last one, is a graph that we’ve been going over the last six months a couple of times to show where inflation actually is going. Let us note that the Fed’s leadership (Powell, in particular), when referring to the short-term nature of high inflation, meant that this last graph would turn down. We predicted that the graph of consumer inflation would go up, and that is exactly what happened. The picture is similar all over the world. Wholesale prices in Germany +15.2% per year, in the entire history it was higher (+15.9%) only once, in April 1974:

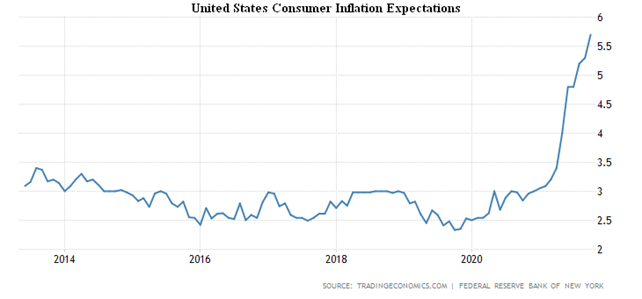

As a result, inflationary expectations in the US (New York Fed survey) renewed a record high (+5.7% y/y):

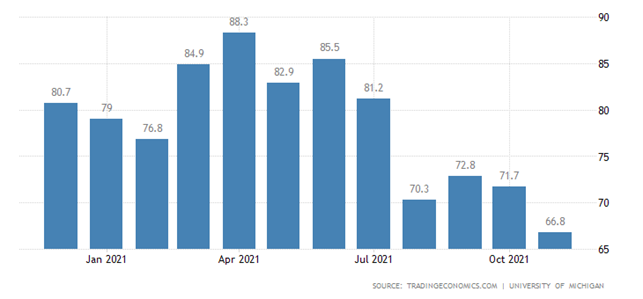

They also plunged consumer sentiment to the worst in 10 years, according to the University of Michigan:

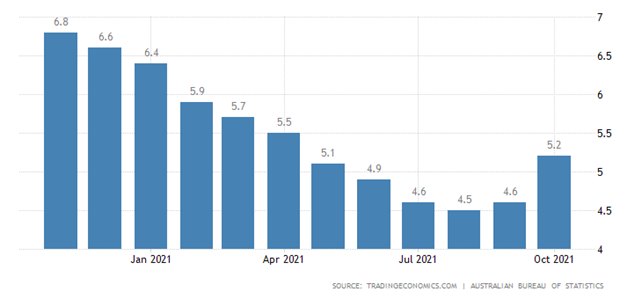

Employment in Australia has been falling for 3 consecutive months:

Why the unemployment rate rose to its highest in six months:

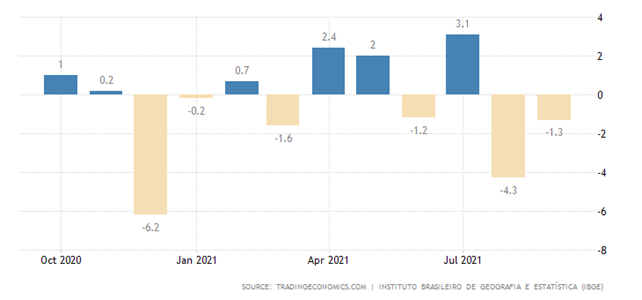

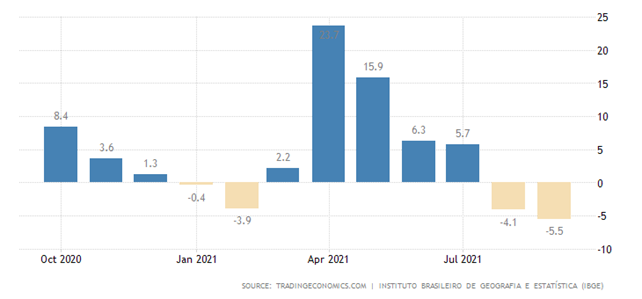

Brazilian retail -1.3% m/m after -4.3% m/m the month before:

And -5.5% a year, that’s the worst performance since May of 2020:

The Central Bank of Mexico raised the interest rate for the 4th time in a row, by 0.25% to 5.00%.

Summary. They relate to the economy to a lesser degree (we have already said everything in recent Reviews), but rather are more of a political-economic nature. In fact, the monetary authorities and other financial statisticians have recognized the soaring inflation rate. As the proxy data show – from our Reviews to the Small Business Confidence Graph in the United States in Section II – it is very safe to say that these entities have been aware of the real situation for at least a few months.

This means that some response to the ongoing crisis will be made public in the very near future. In the EU, by the way, the campaign has been going on for some time, and the blame for the rise in energy prices and, by extension, for everything else, rests with Russia. In recent days, Belarus has been added. Of course, this has nothing to do with reality, but this choice of reason means that the monetary authorities of the European Union are not going to do anything.

In the US, however, the authorities have already begun to realize that price increases are due not only to emissions (which are concentrated in the financial sector and have little impact on consumer inflation), but also to two other important factors. The first is the failure of the banking system to lend to the real sector (the banking multiplier has collapsed to extremely low values, about 2, which is about half of the lower limit of the norm in the range of 4 to 6).

The second factor is the structural economic downturn, which is also manifested in the logistics crisis. In this case, monetary methods are completely useless – the mismatch between production and real demand is treated for a very long time, years, sometimes decades, and certainly not by changing the money supply to consumers. Here, we should expect major changes in investment flows, which can only take place after the end of the structural recession. However, the details are set out in M. Khazin’s book “Reminiscences about the Future.”

In conclusion, we wish our readers to avoid crisis troubles during the beginning of the working week.