Time period: April 2–8, 2022

Top news story. The main and most amazing news of the week is the insight of the US Federal Reserve within the protocols published this week.

The Fed:

“A number of participants had concluded that, at the current stage, the significant risk faced by the Committee was that high inflation and inflationary expectations could be sustained if there were public doubts about the Committee’s determination to adjust its policies.”

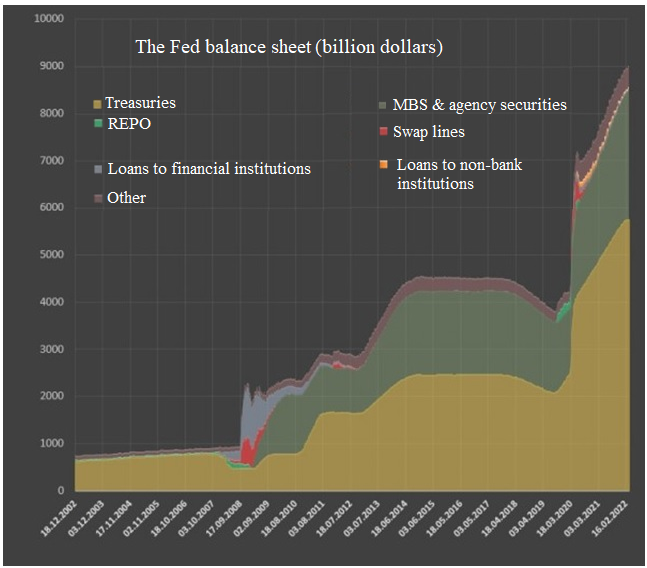

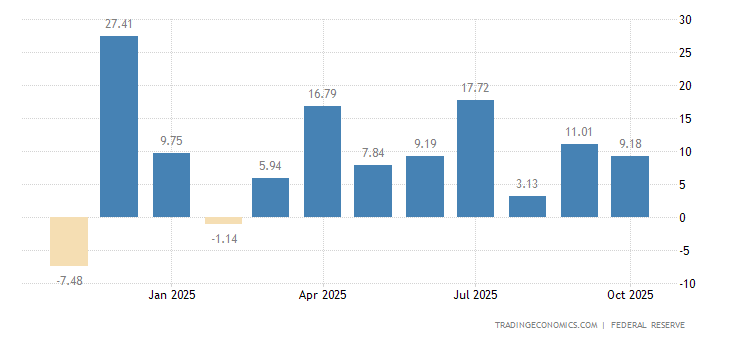

So what we talked about a year ago, and what some Fed leaders described as just one possibility, has become an official position! One can only sincerely admire! But, just in case, here is the Fed’s balance sheet at the time of insight:

The main results of the Fed protocol:

- The balance sheet reduction could start in three months at a rate of $95 billion per month (60bn treasuries +35bn MBS), which is twice as fast as in 2017/19;

- Rate hikes up to 50 BPS are allowed;

- The projected rate of increase of 2022 is about 2.5-2.75%.

Given the magnitude of the inflationary process and households’ dependence on debt refinancing, this scale of credit tightening will not have any effect. As an example, let’s show how American households’ expenditures have increased due to inflation:

There are just over 110 million households in the United States. If you multiply that by 400 dollars, that’s 44 billion dollars. Who will provide this amount in case of monetary tightening? Or does the Fed predict a priori a rapid deterioration in living standards? That’s a bold assumption, especially in an election year.

Macroeconomics

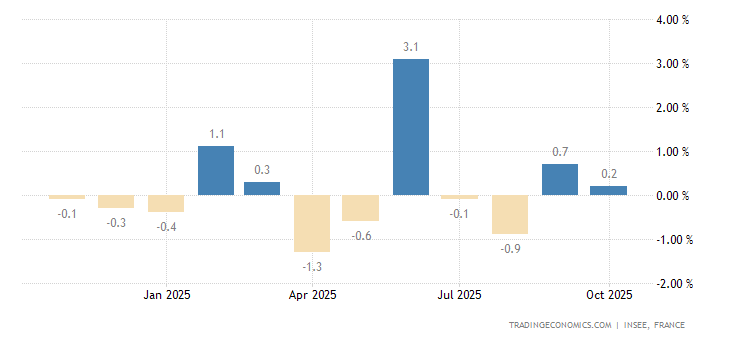

Industrial production in France was -0.9% m/m:

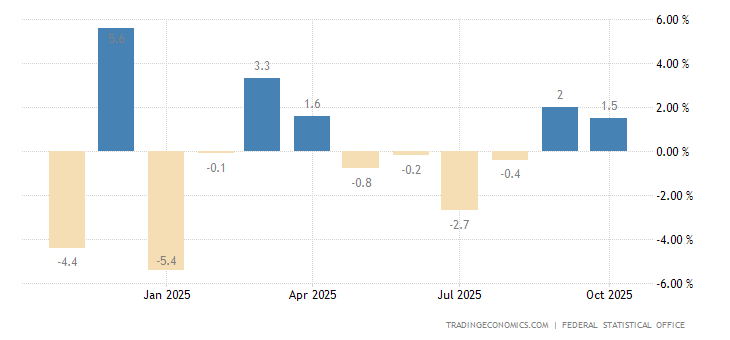

Factory orders in Germany were -2.2% m/m:

We can note that the pace of negative developments in the major EU economies has increased. If this is the result of sanctions against Russia, which is most likely, the US leadership can rub its hands — capital outflows from the EU will be constantly accelerating.

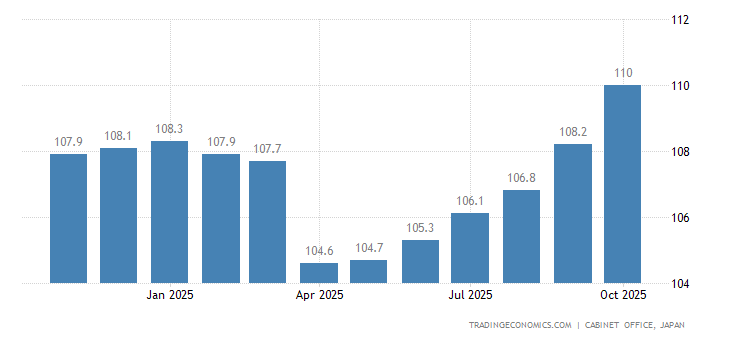

The value of Japan’s leading economic index is the lowest in 5 months:

The PMI (an index of expert assessment of the condition of the industry; its value below 50 means stagnation and decline) of the Chinese service sector rolled back to the recession zone (42.0) — for 10 years of observation it was lower only once, in February 2020:

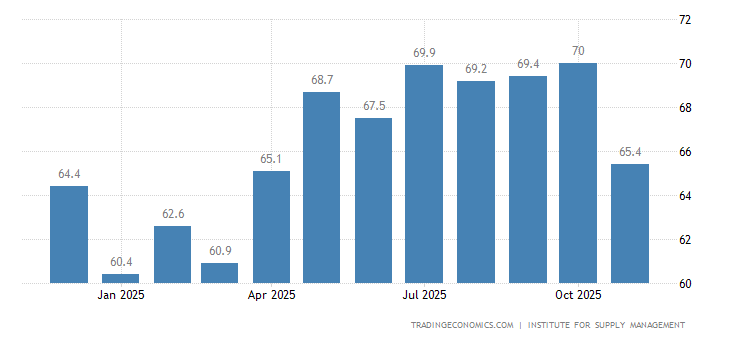

United States ISM non-manufacturing prices are only 0.1 behind the December record high:

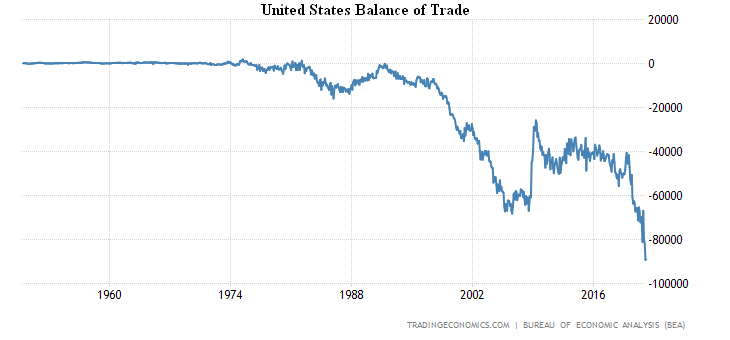

The US balance of trade stands at a record level:

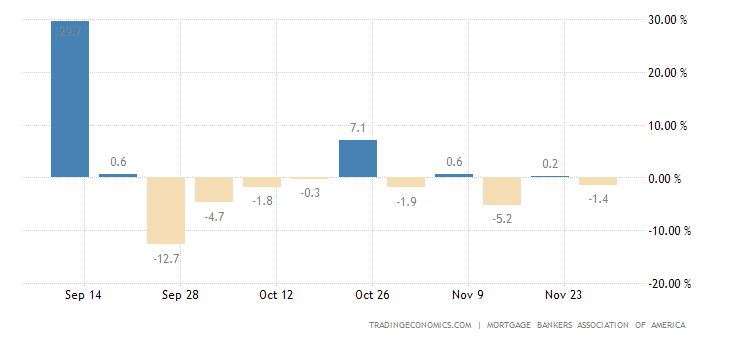

Mortgage applications in the US continue to plummet, with another -6.3% per week down to the trough of three years:

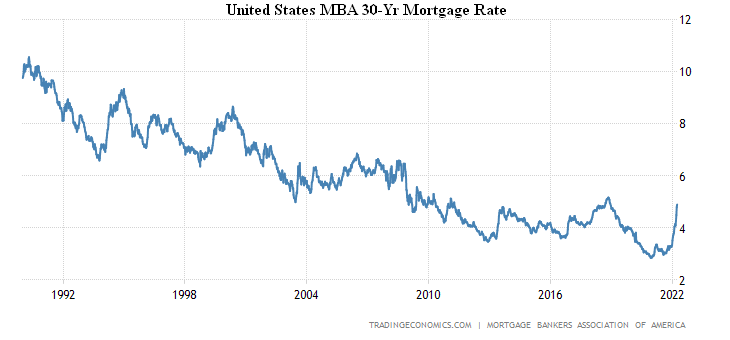

Since the mortgage rate is at its peak from 2018 (4.9%) — another 0.3%, and it will be the highest since 2009:

But the consumer credit (+41.8 billion per month) grew at most 79 years of survey, not counting 2 stimulated surges of 2006 and 2010:

With this in mind, the Fed is moving very quickly to tighten monetary policy — to wait for years of record in the economic downturn and to cut demand even more (as household money begins to drain further into debt refinancing)!

Inflationary performance is routinely breaking records.

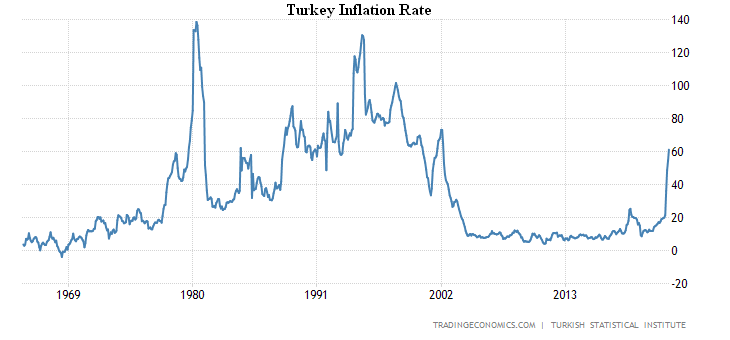

CPI (Consumer Price Index) of Turkey +61.1% per year, this is a 20-year high:

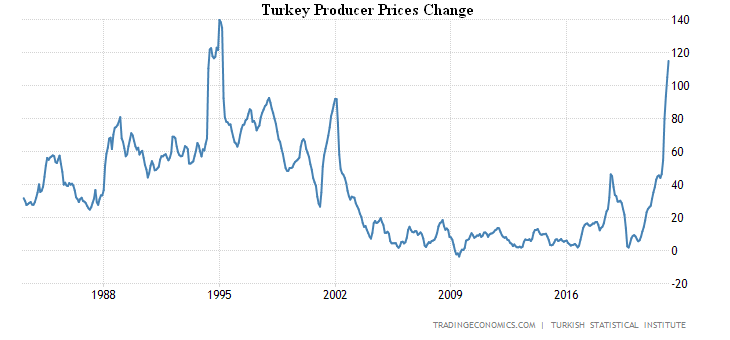

PPI (Producer Price Index) of Turkey +115.0% per year, this is a 27-year peak:

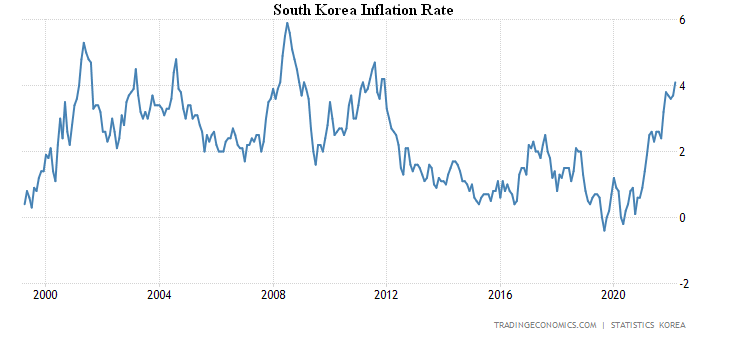

South Korea’s CPI of +4.1% per year is at its highest since 2008:

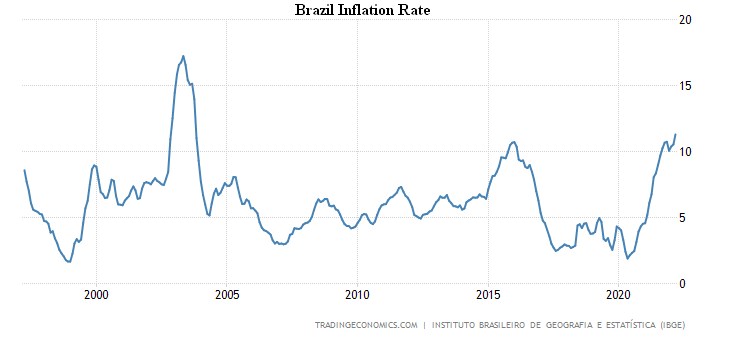

CPI of Brazil +11.3% per year, which is the peak since 2003:

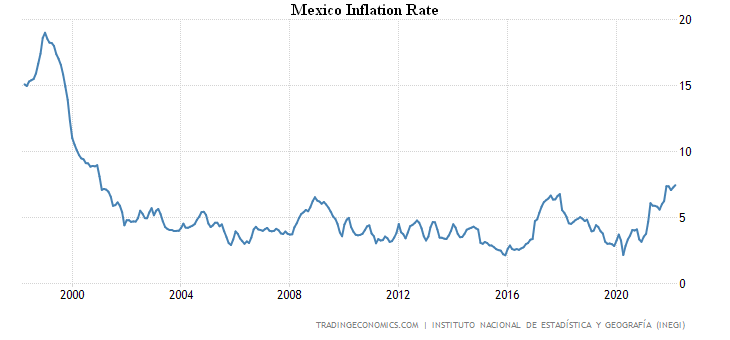

CPI Mexico +7.45% per year, the highest since 2001:

Core consumer prices in Mexico (less food and energy) +6.8% per year, also climbed to the top since 2001:

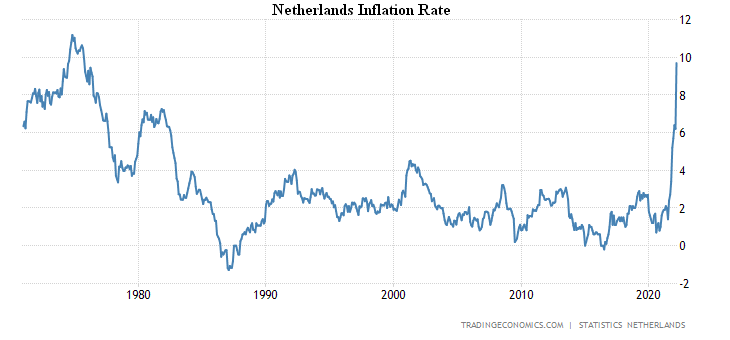

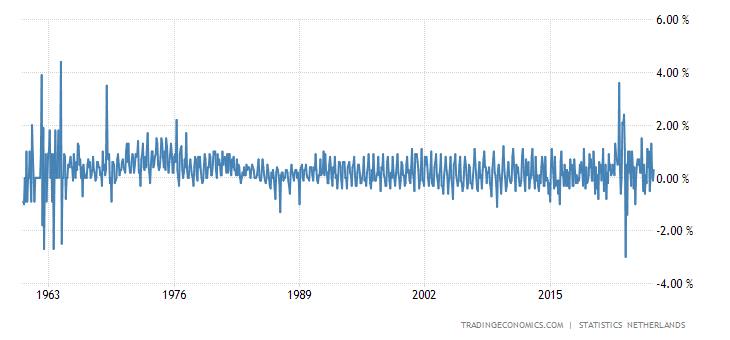

The CPI of the Netherlands is +9.7% per year, the highest since 1975:

And +3.6% per month, which is the peak since 1965:

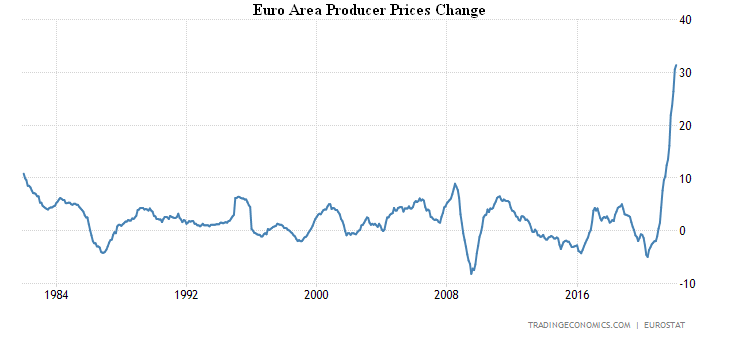

PPI of the Euro Area is +31.4% per year, a 40-year record, with a three-fold break from previous peaks:

It’s not just high inflation anymore, it’s a natural economic disaster. If this is the result of sanctions, they should be withdrawn immediately and categorically, because the consequences will be terrible!

Japanese consumer sentiment is at its worst in 14 months:

In Spain, pessimism is critical for 1.5 years, for the month the consumer sentiment became record-breaking bad:

Retail sales in France -0.6% m/m, 3rd consecutive time in the red zone:

Household spending in Japan -2.8% per month, this is the 2nd negative in a row and the 3rd in 4 months:

The Central Bank of India has left monetary policy as it is, but has indicated that it will soon tighten it. The Australian Central Bank left the rate unchanged, but removed the phrase that will be “patient”.

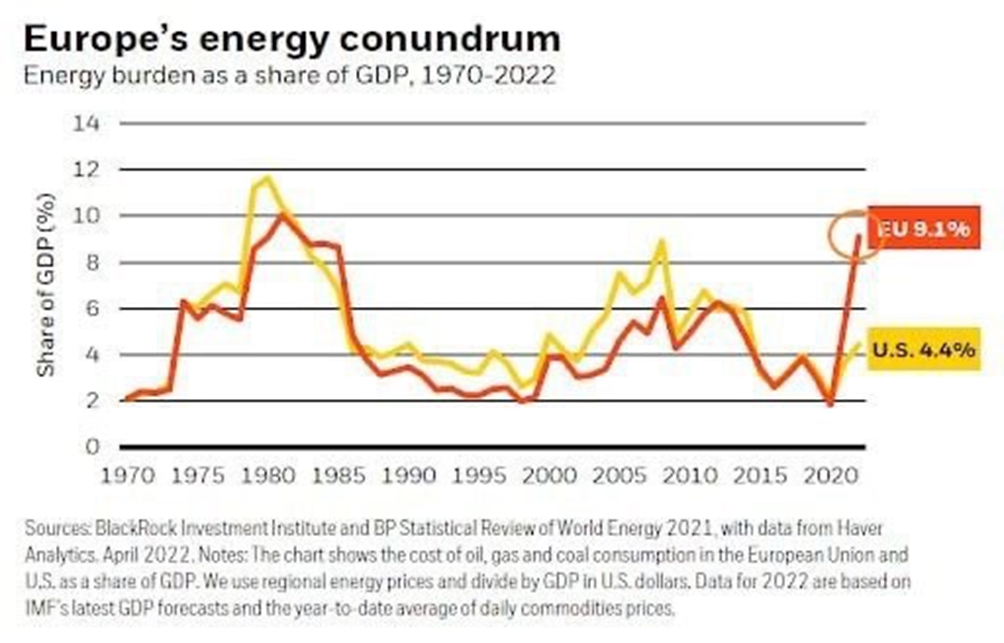

Summary. It can now be definitively concluded (since Russia’s special operation in Ukraine began in February, and March data were already fully determined in its course) that the sanctions war against Russia led to a sharp deterioration of the global economy. And this was reflected not only in the rise in prices, but also in structural changes, the most severe impact was on the European Union, which is not surprising — its GDP is most heavily dependent on energy prices:

And the rise in their prices looks very significant:

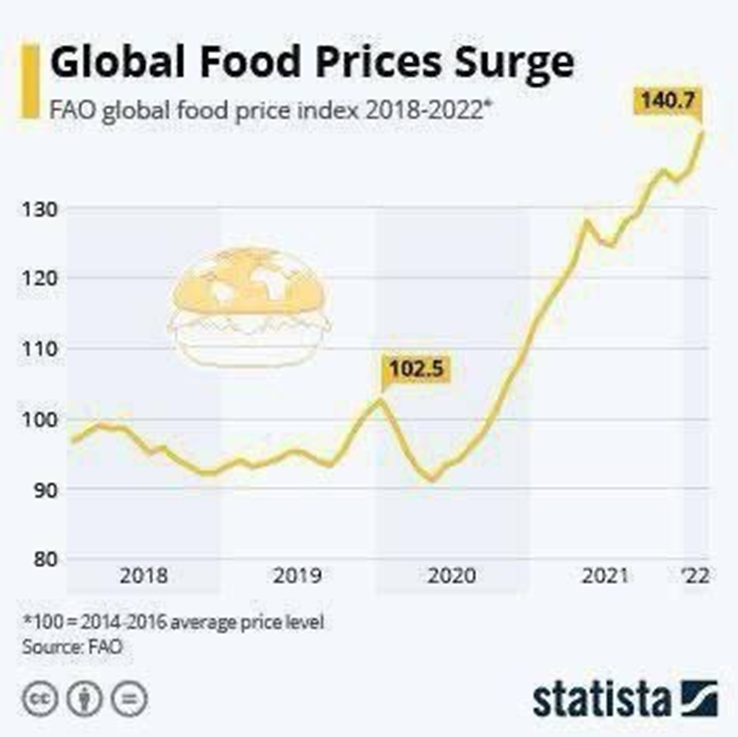

Food is equally important:

It should be noted that for the EU the situation is aggravated by the fact that a large part of the fertilizer is produced in the region from Russian gas. It is possible that with the lifting of sanctions the situation can still be saved (that is, to return to the already normal decline of 0.7-0.8% of GDP per month), while everything falls precipitously into a terrible collapse.

There is no doubt that the political authorities are not aware of this, limiting themselves to purely political games to limit Russia. The trouble is that Russia is resistant to pressure, not least because sanctions affect its economy much less than the countries that establish them. Not to mention those who do not participate in these sanctions at all (including China and India). In general, it is safe to say that Western countries are very likely to destroy with their own hands the cozy world in which they were the main beneficiaries of the world economy. By the end of this year, we will have seen the results of their activities. The trouble is that not only do they not manage economic processes (and even, it seems to us, do not follow them very much), but they also do not realize what awaits them after the crisis. We, the Mikhail Khazin Foundation for Economic Research, have been conducting this topic for more than 20 years and can responsibly state that the differences between the post-crisis world and the present will be fundamental and principled.

In the meantime, we wish our readers a good work week.