Time period: 27 November – 3 December 2021

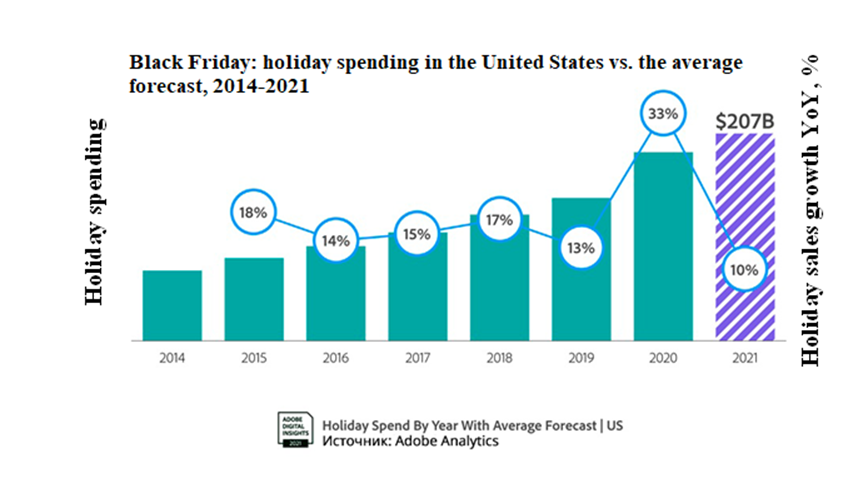

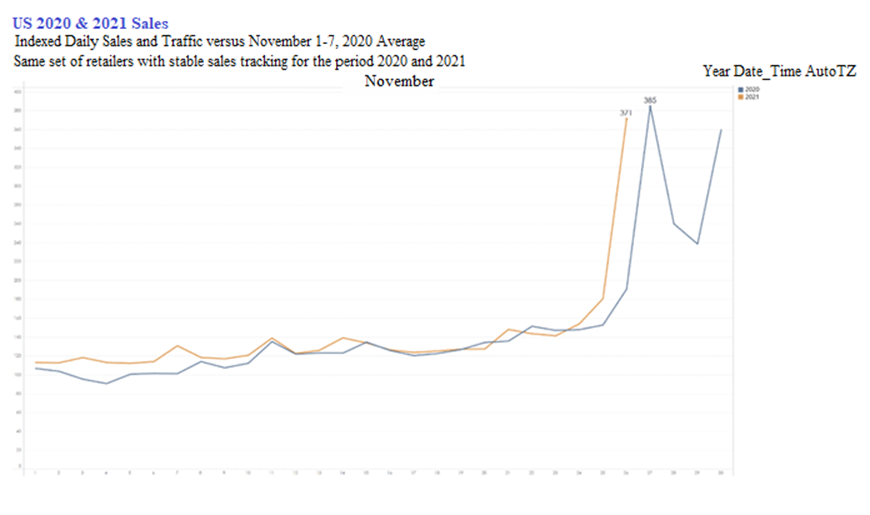

Top news story. The main news of the week is not very successful results of Black Friday.

Similar performance in the major EU countries: growth is certainly positive, but slower than in previous years. By comparing sales by day, we see a very similar picture, but one subtle thing is inflation.

In fact, given the sharp rise in prices (which is higher than the official rate of price increase that is necessarily indicated in the graph), it turns out that the volume of purchases has become slightly decreased.

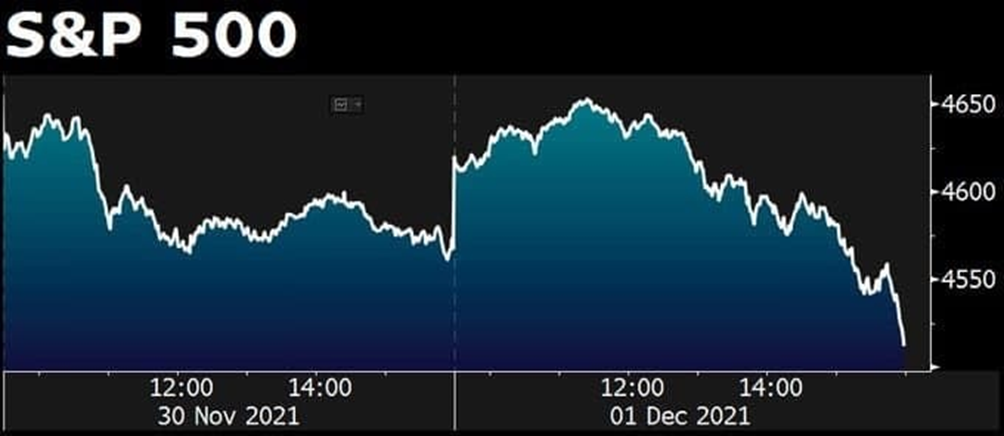

At the same time as the moderate decline of the stock market (against the backdrop of uncertainty caused by the new strain of Coronavirus “Omicron”) formed some general unfavorable atmosphere, which was never able to dispel by numerous speeches the second term head of Fed Powell (cf. the last section of the Review).

Macroeconomics

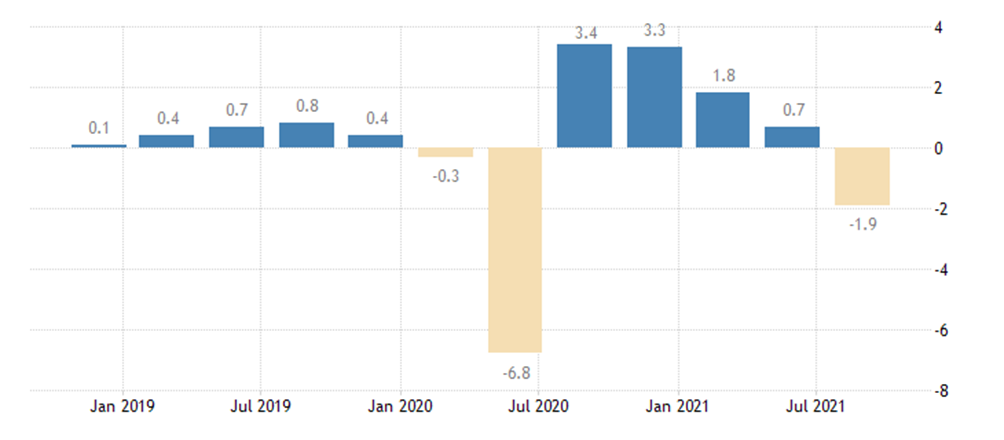

Australia’s GDP, pausing for a year, fell back to quarterly negative (-1.9%):

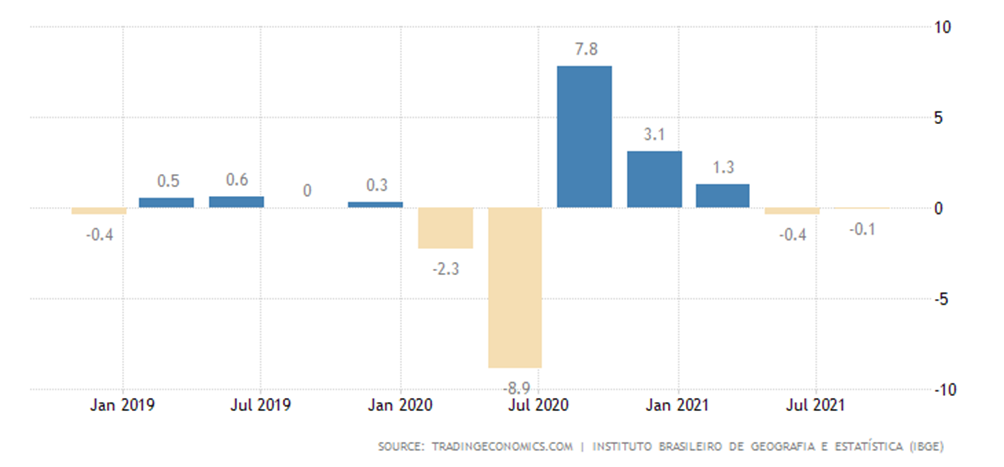

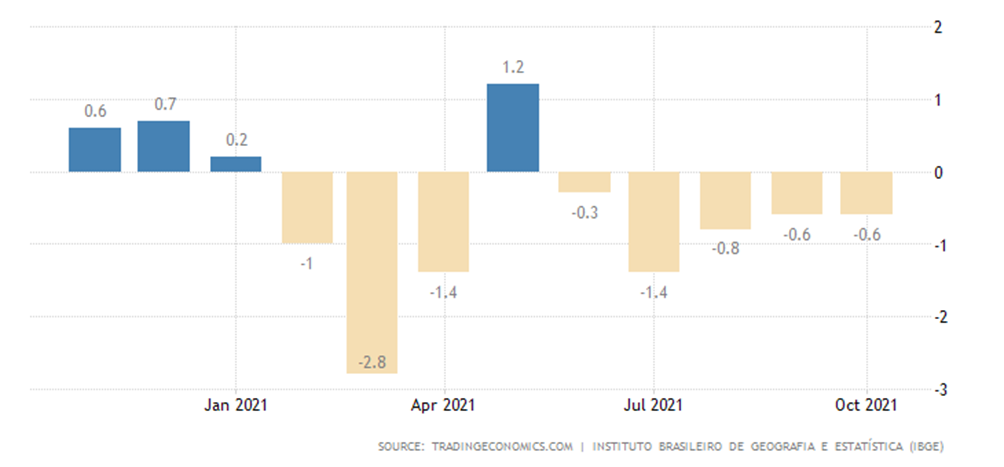

Brazil’s GDP is for the second consecutive negative:

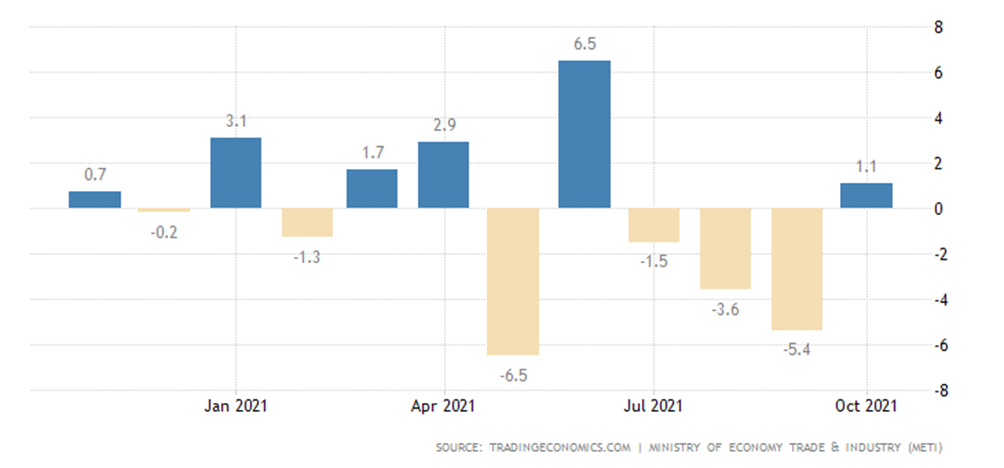

Industrial production in Japan, on the other hand, is +1.1% per month after three negative values in a row:

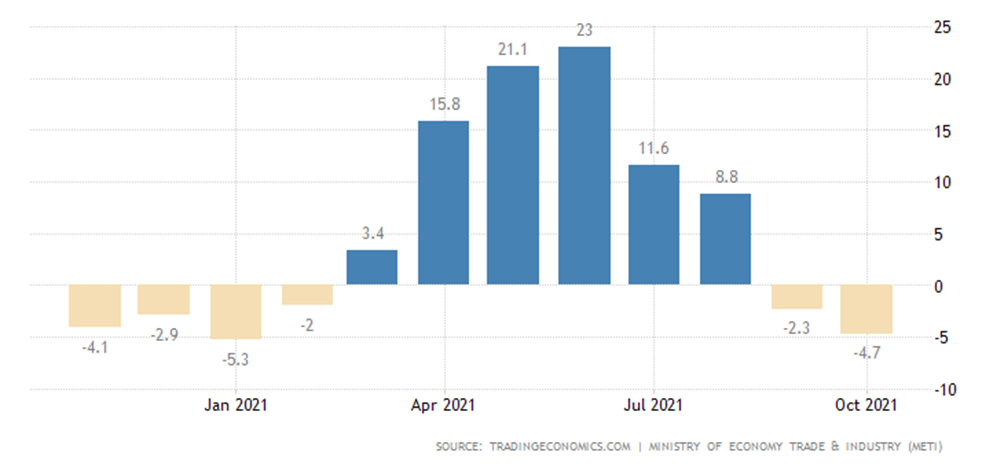

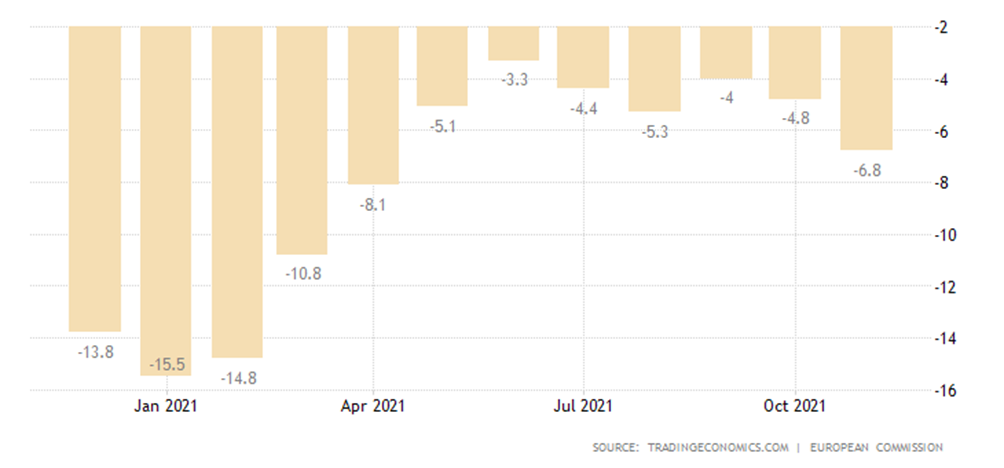

The annual performance is the worst in nine months and is increasingly falling into the recession (-4.7%):

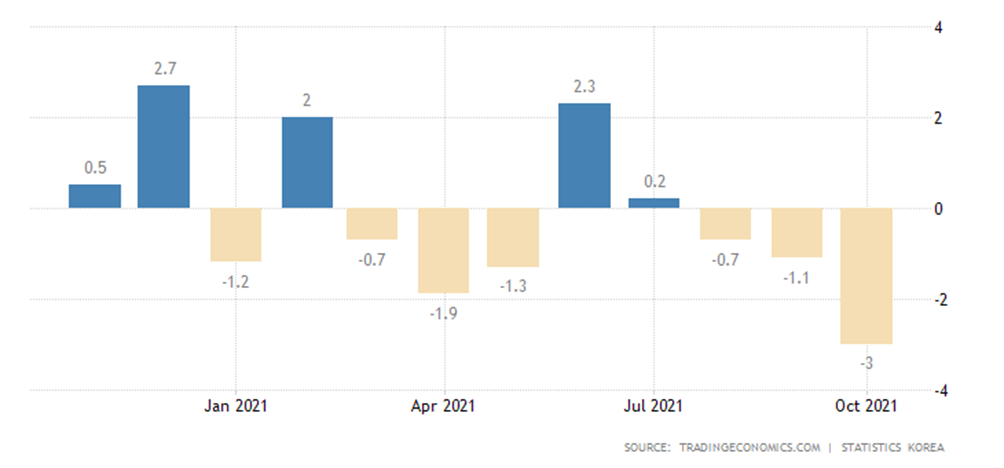

Industrial production in South Korea -3.0% per month – the third consecutive negative and sixth in the last 8 months, the worst performance since May 2020:

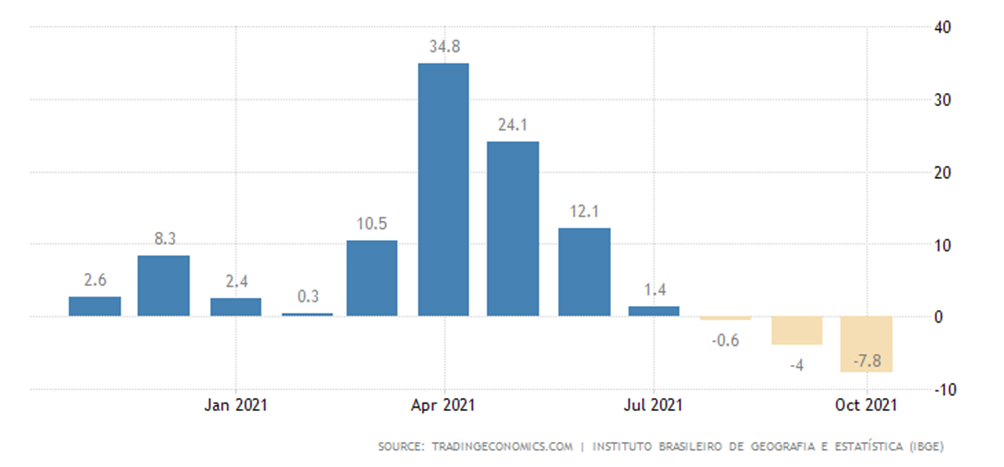

Industrial production in Brazil -0.6% per month – 5th negative in a row and 8th in the last 9 months:

As a result, the annual decline has gained to -7.6%:

PMI (Purchase Managers’ Index – an expert index that describes the state of the industry; its value below 50 denotes stagnation and decline) China, according to the official figures, has risen to only a value that is minimally above stagnation (+50.1 point):

In an independent expert assessment, pessimism is even slightly higher: 49.9 points, minimal since April 2020 –

We would point out that the behaviour of the two graphs does not coincide – this is likely to indicate that one (or both) is being adjusted. Taking into account that China’s formal economic indicators are positive (see the previous Review) and the indices show a recession, there is a suspicion that the PMI indices have been distorted in order to bring them in line with official indicators.

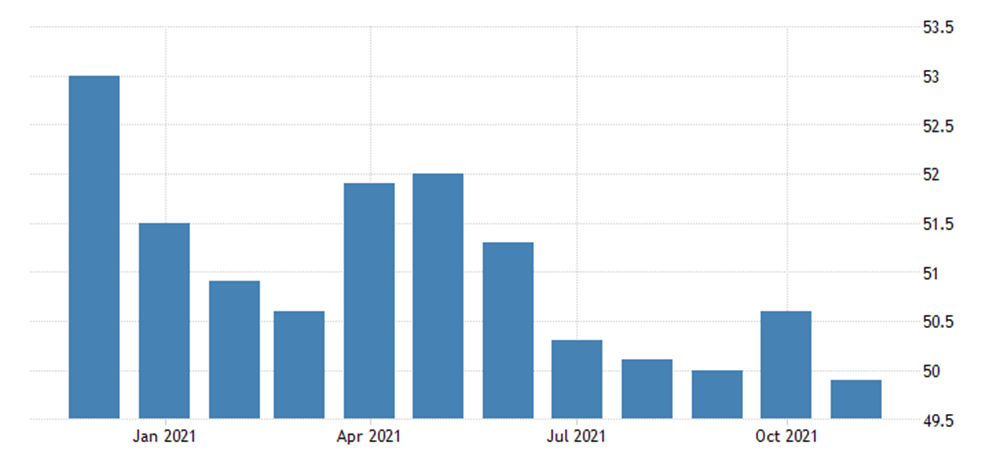

The RF service sector PMI is at its lowest in more than a year (47.1 points):

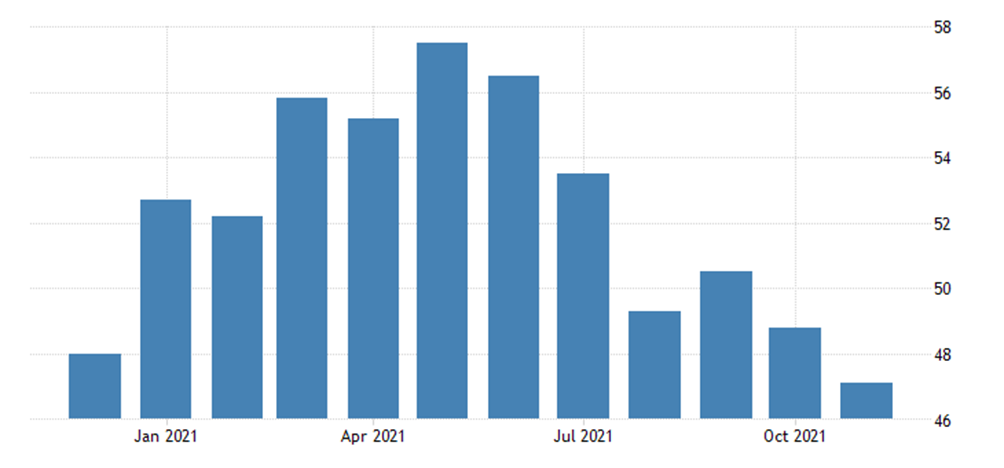

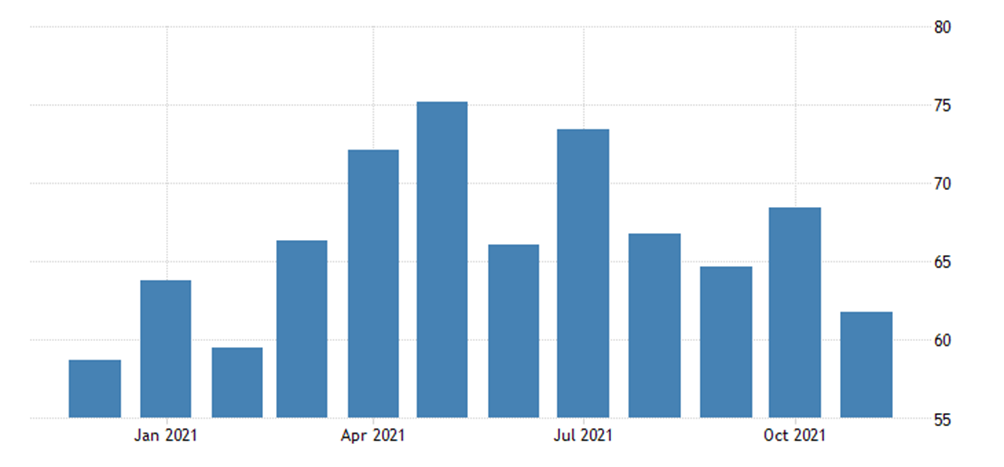

Brazil is at the six-month trough (53.6) amid record inflation:

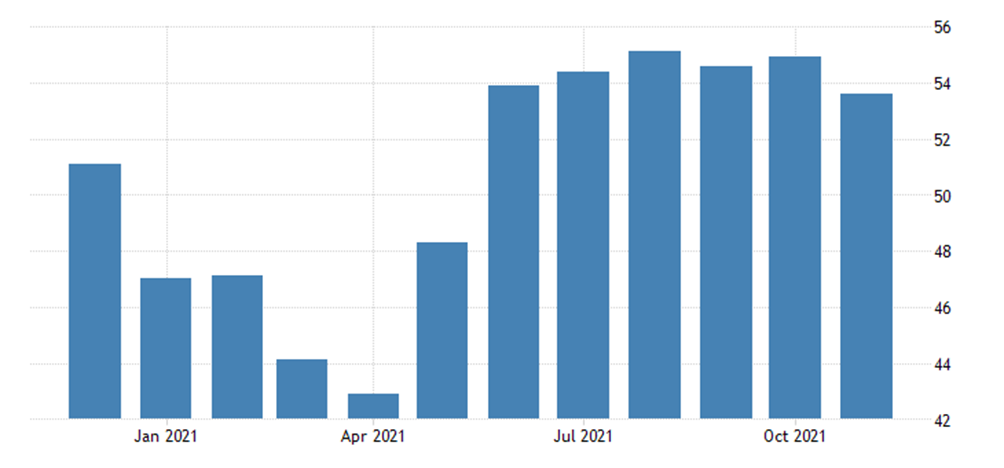

The PMI of Chicago is the lowest in nine months, although the index is still high (61.8 points):

Here, however, an interesting question arises as to how the experts estimate the performance of the services sector: on the basis of official data, or on the basis of real inflation? The first option is much more preferable than the second because in this case high inflation “eats up” a large part of nominal sales. Of course, there is no answer to that question.

Business confidence in New Zealand is weakest in over a year:

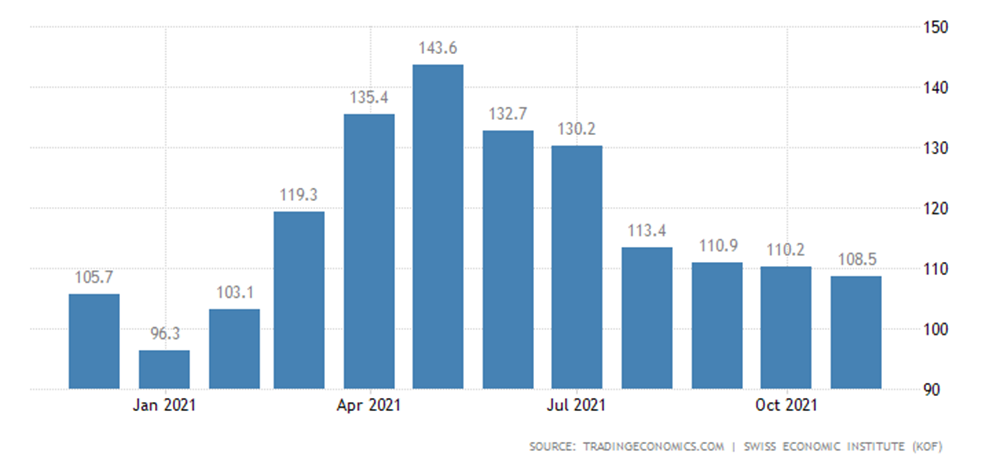

Switzerland’s Economic Barometer (business opinion) shows the worst values in nine months:

As our readers are already accustomed to, below we present record data on inflation in different countries.

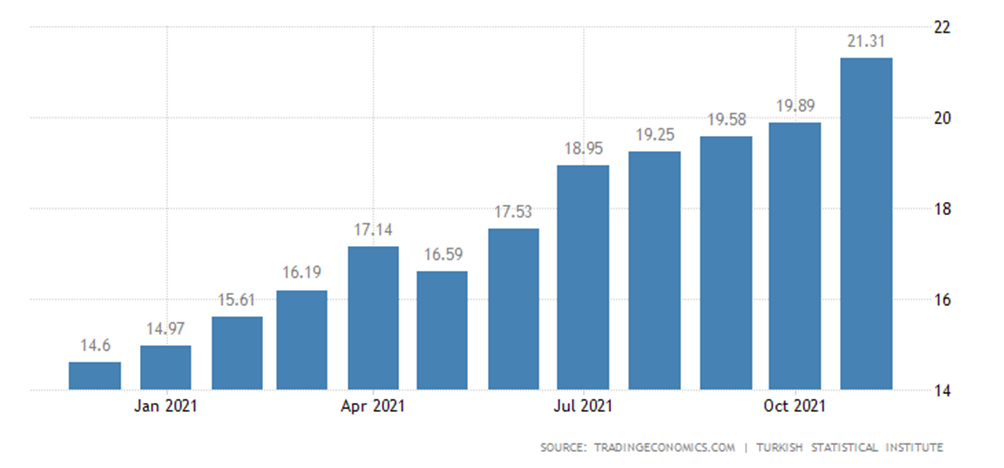

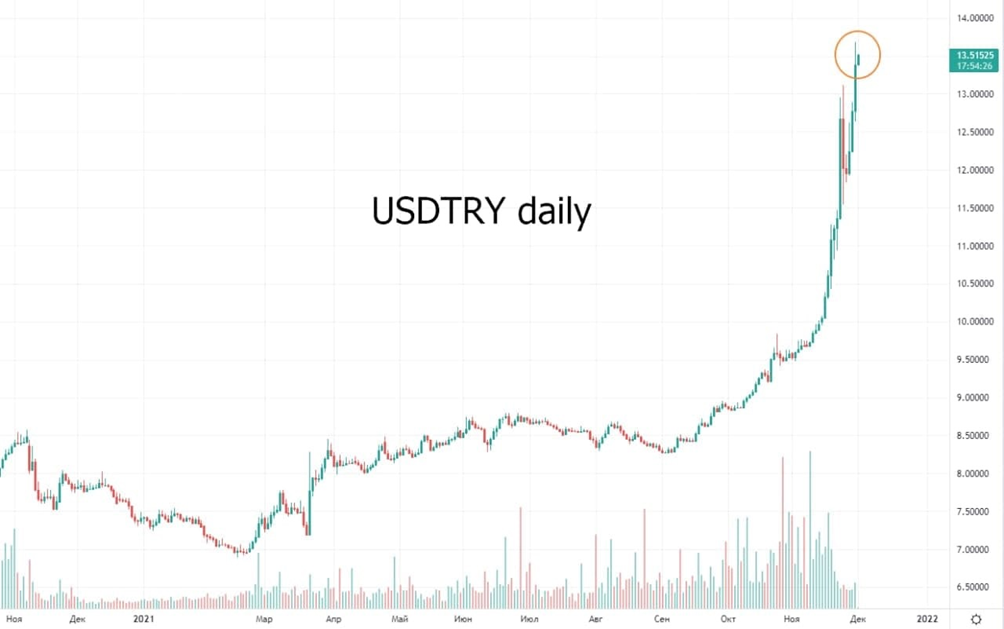

CPI (Consumer Price Index) of Turkey +21.3% per year – the highest value in 3 years:

Not surprisingly, the “health” of the Turkish currency is extremely unfavorable:

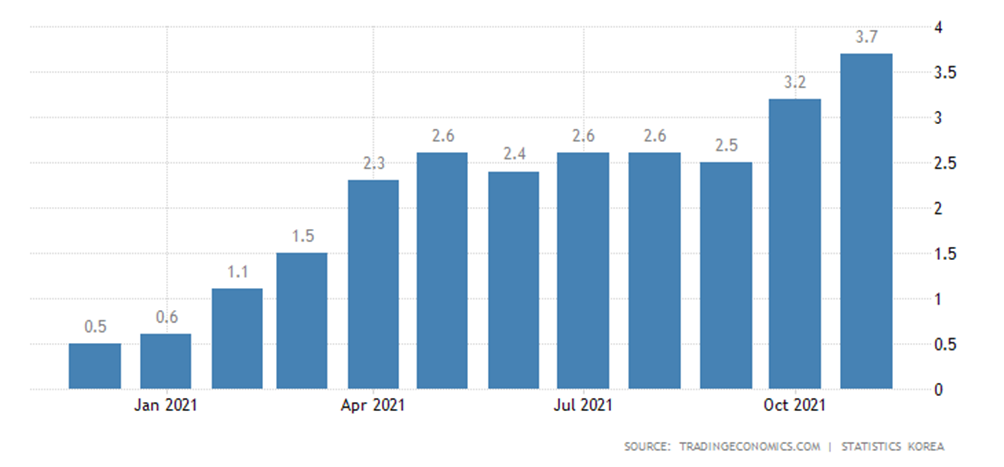

CPI of South Korea + 3.7% per year – at the top ten years:

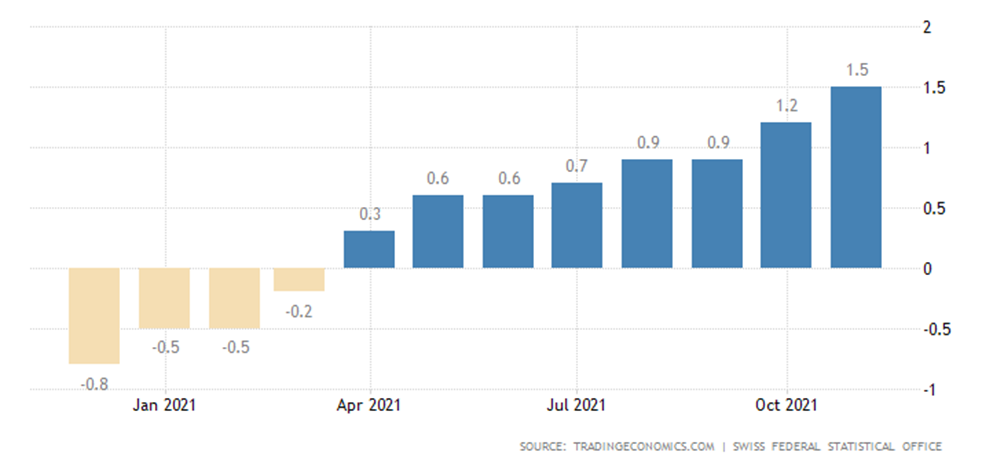

CPI Switzerland +1.5% per year, which is a peak since 2008:

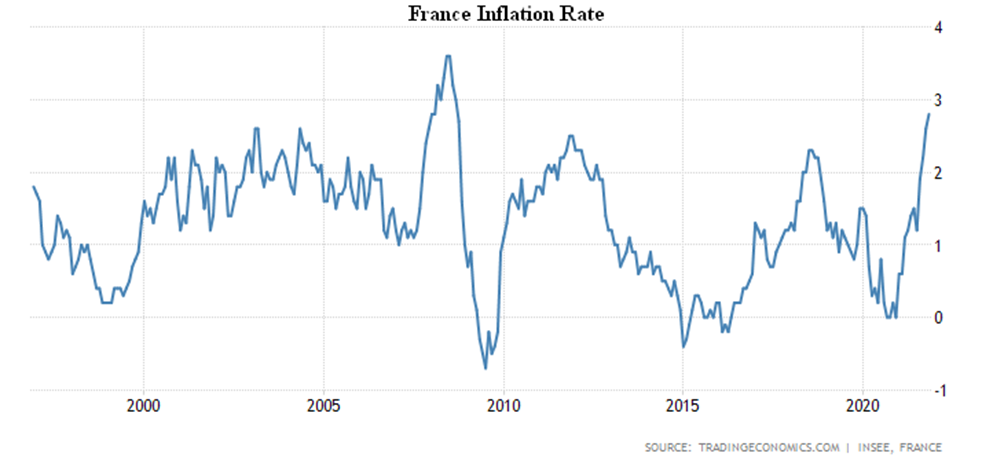

CPI France + 2.8% per year at its highest since 2008:

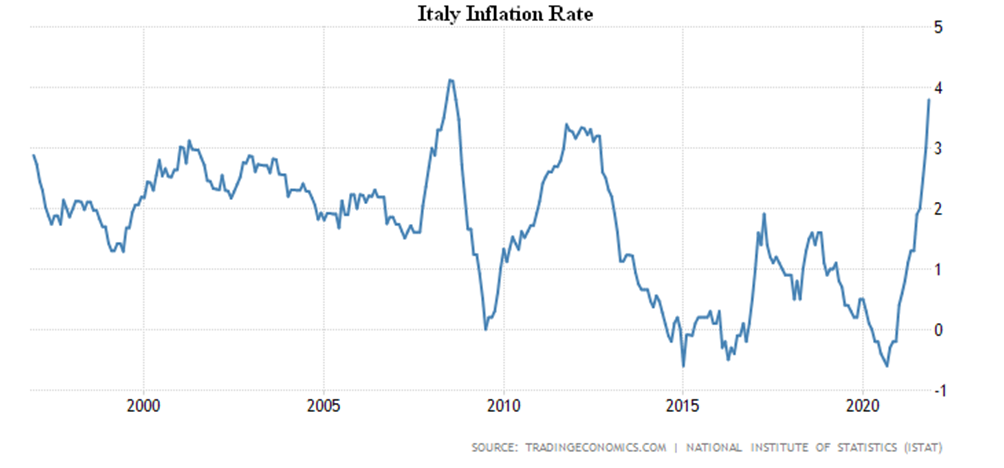

CPI Italy 3.8% per year, this is a record value since 2008 in the same way:

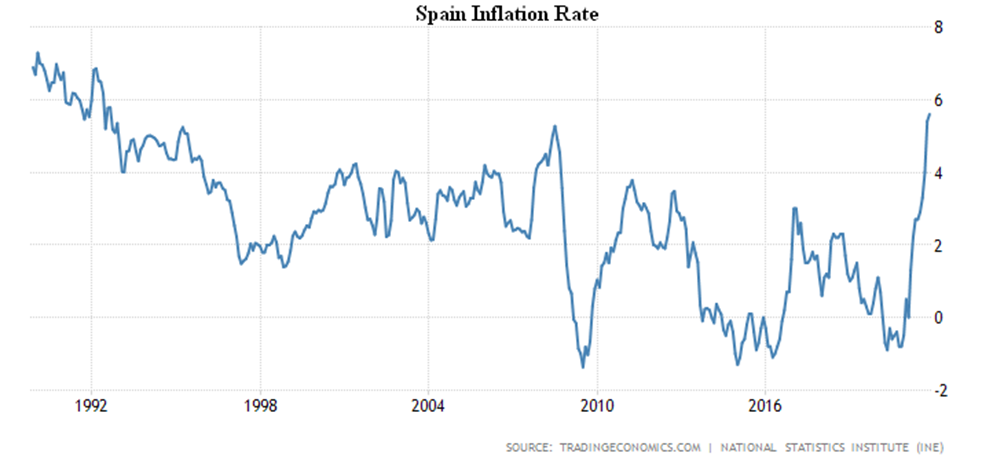

CPI of Spain +5.6% per year, it is the maximum since 1992:

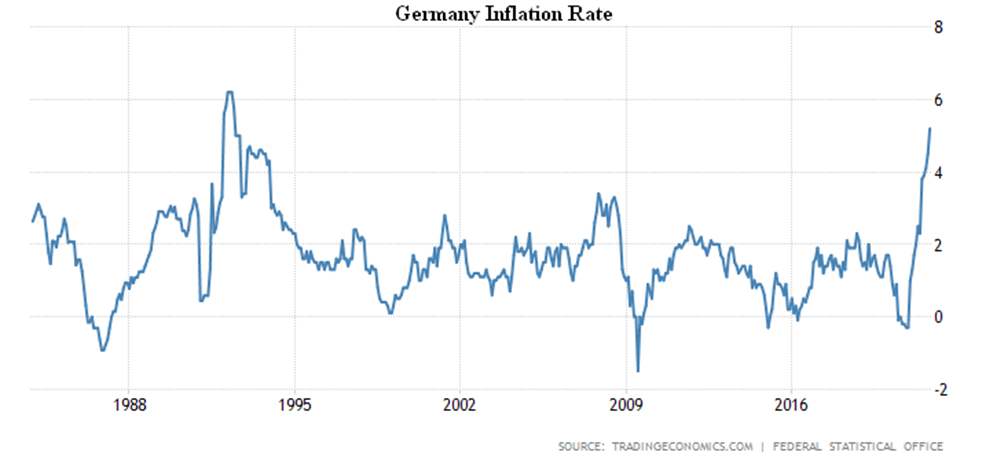

CPI in Germany +5.2% per year, this is the peak since 1992:

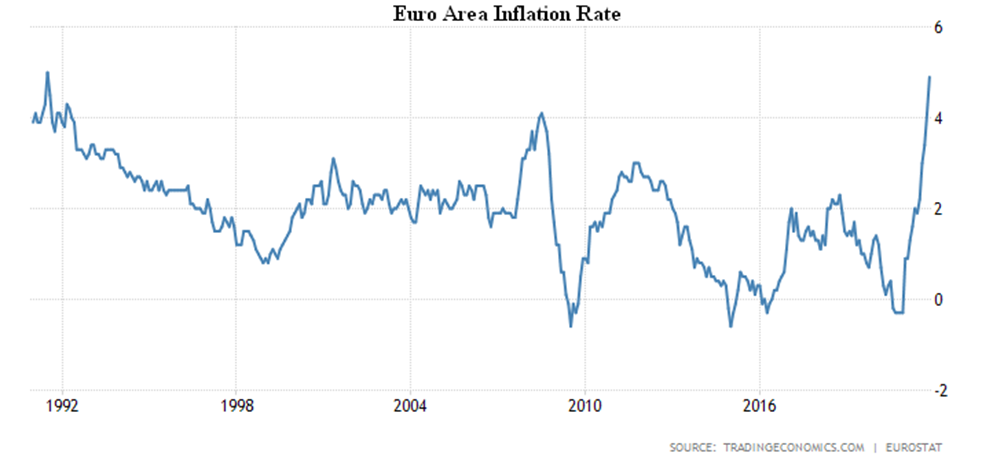

The most impressive indicators are the CPI of the Euro Area, +4.9% per year, which is the highest since 1991:

Attention should be paid to the very rapid growth, most likely due to the same fact as in the United States: the indicators of consumer inflation get started to chase the indicators of industrial inflation that greatly exceeded them. The latter, in turn, is caused not only by monetary (emission), but also by structural reasons (see the previous Review). Producer inflation is not going to stop at all, contrary to the hopes of monetary authorities in early autumn:

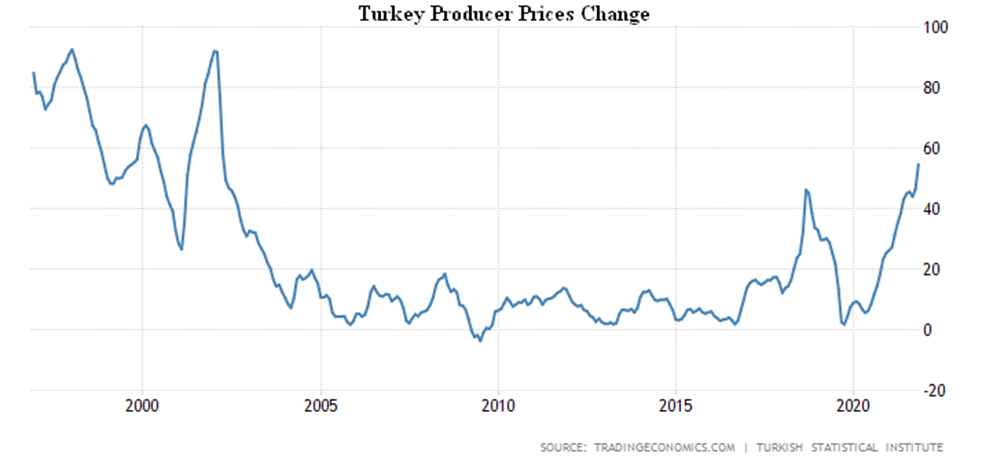

Turkey’s PPI (Producer Price Index) + 54.6% per year, it is the maximum since 2002:

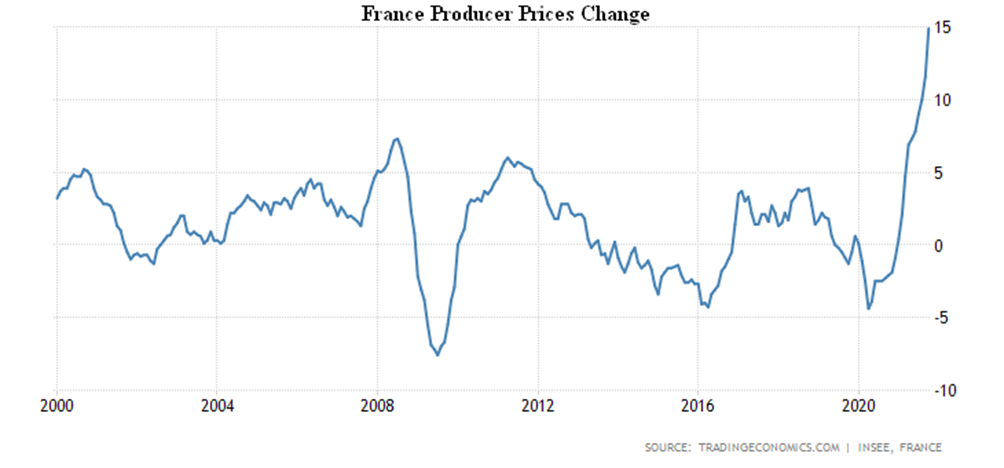

PPI of France +14.9% per year, an unprecedented rate in 22 years of observation:

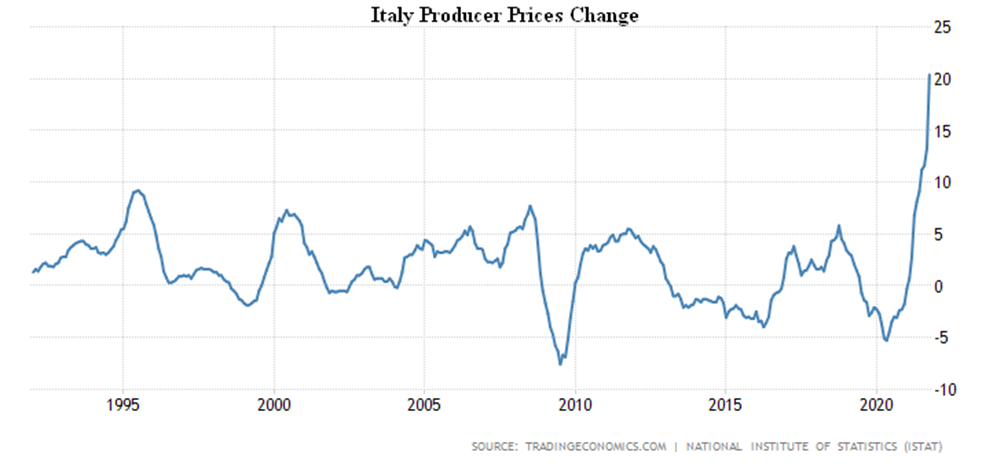

Italian PPI +20.4% per year, a record for the entire 30 years of the survey:

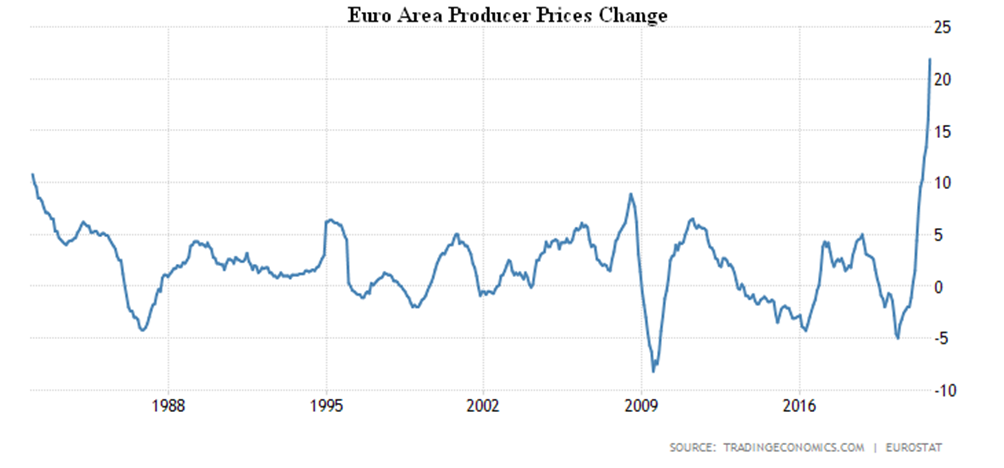

The Euro Area PPI + 21.9% per year, the highest in all 40 years of observation:

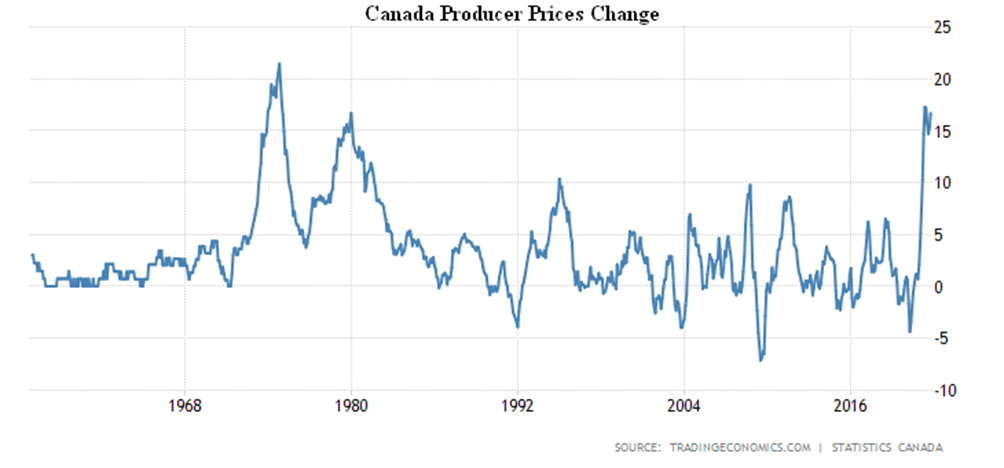

Overseas the situation is no better, Canada’s PPI is growing again, October +16.7% per year – May’s 42-year peak (+17.3%) approaches:

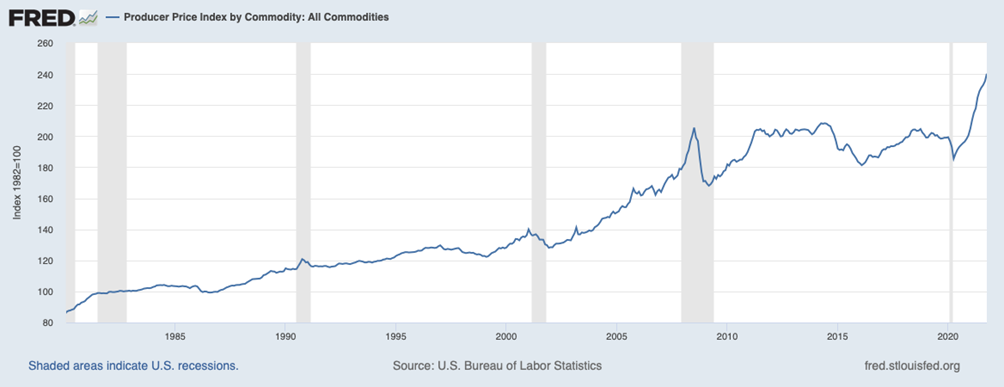

The situation of the United States of America has been discussed in detail in one of the previous Reviews, so we will only give a graph of industrial prices (not the PPI index!):

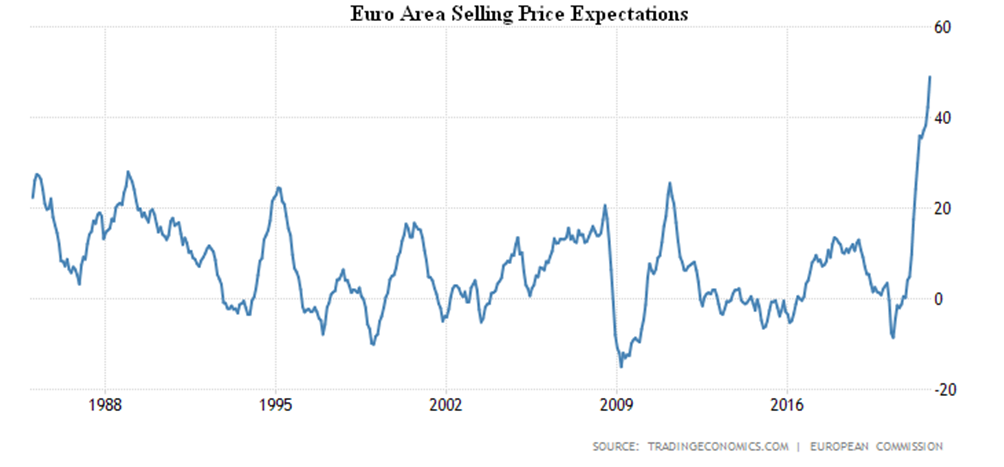

Expectations of growth in selling prices in the Euro Area are the highest for all 37 years of observation:

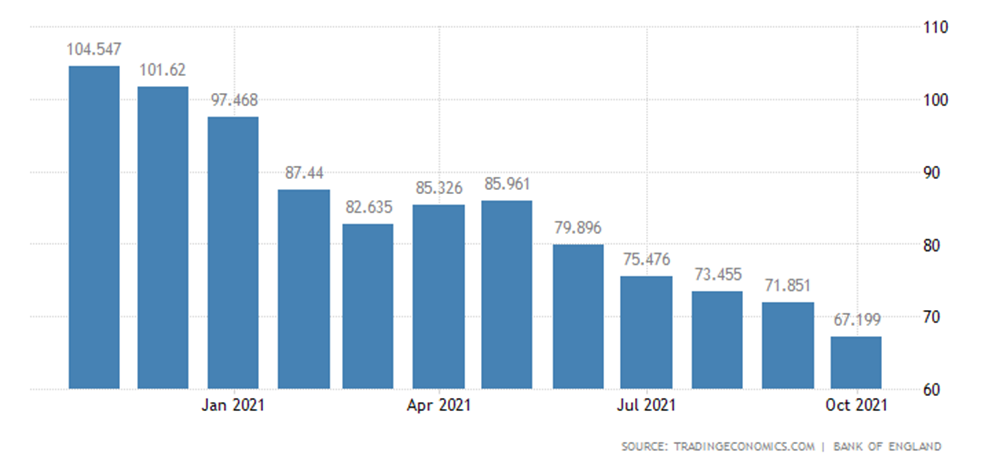

UK mortgage approvals have returned to pre-pandemic levels after taking off in 2020:

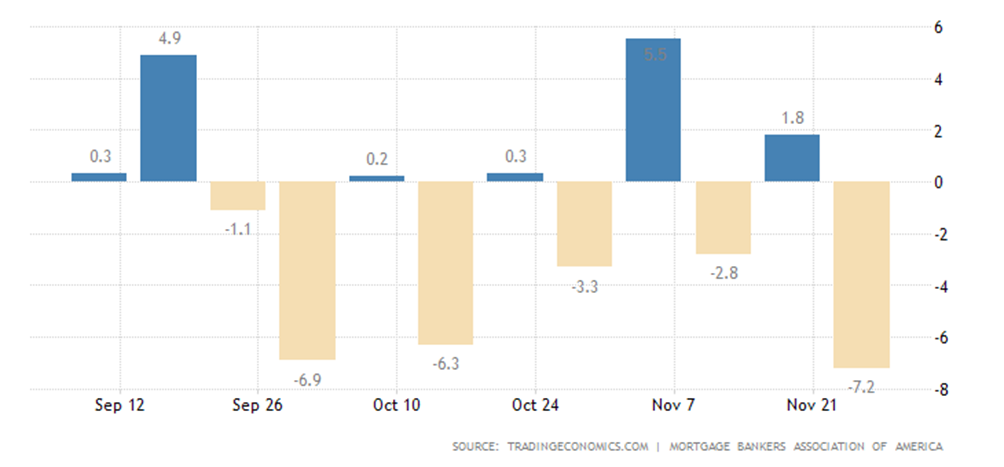

Mortgage applications in the United States -7.2% per week, the worst performance since last winter:

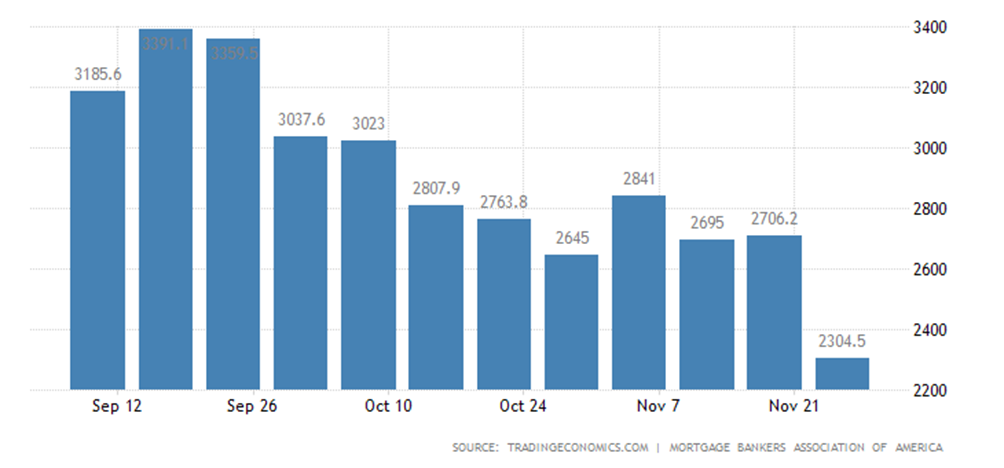

Refinancing -41% per year, the indicator dropped to the lows of the beginning of 2020:

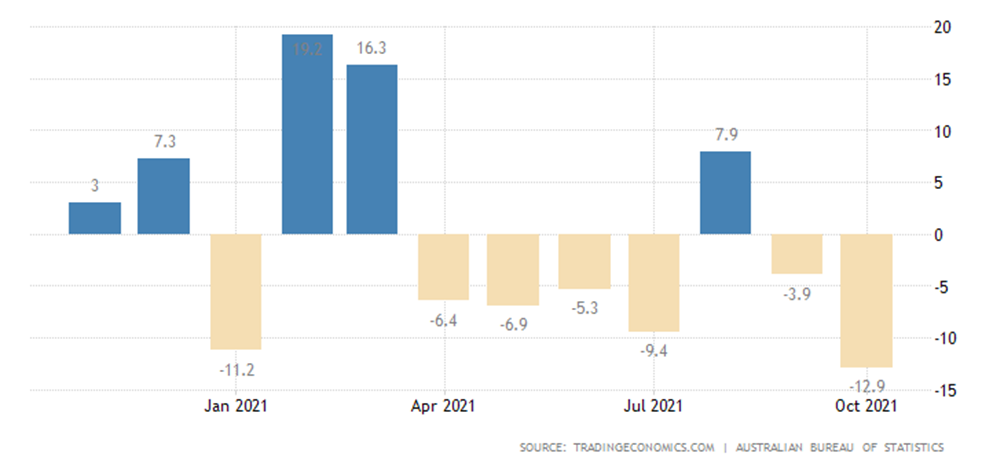

Dwelling Approvals in Australia -12.9% per month (one and a half year low, sixth negative value in the last 7 months):

Consumer sentiment in the Euro Area is the worst in 7 months:

And in the USA (Conference Board version) it is the weakest in 8 months:

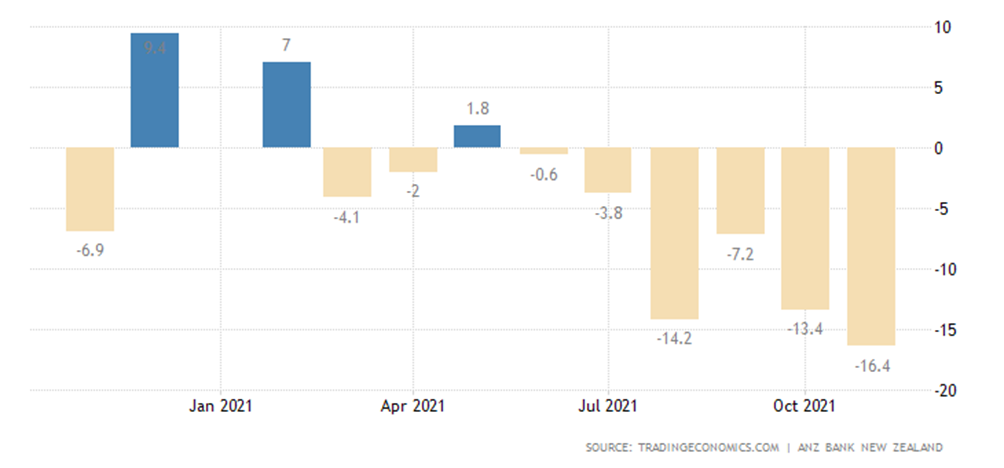

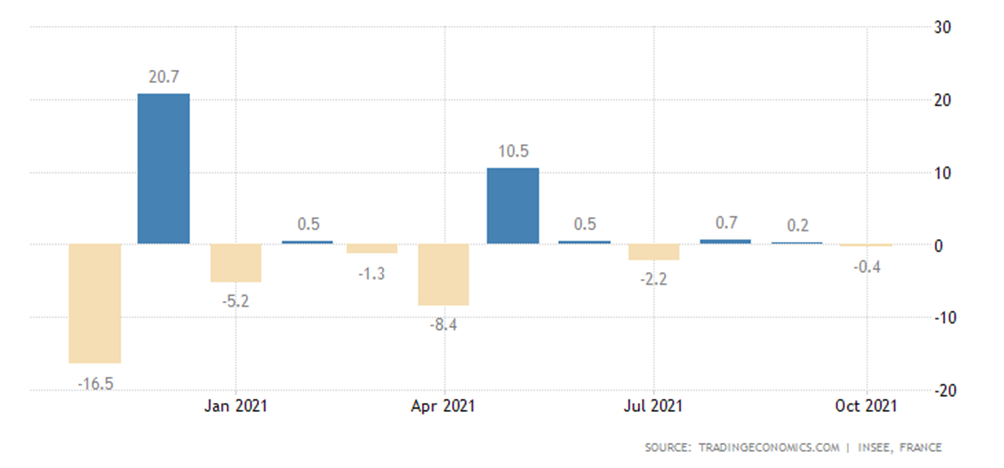

French household spending -0.4% per month:

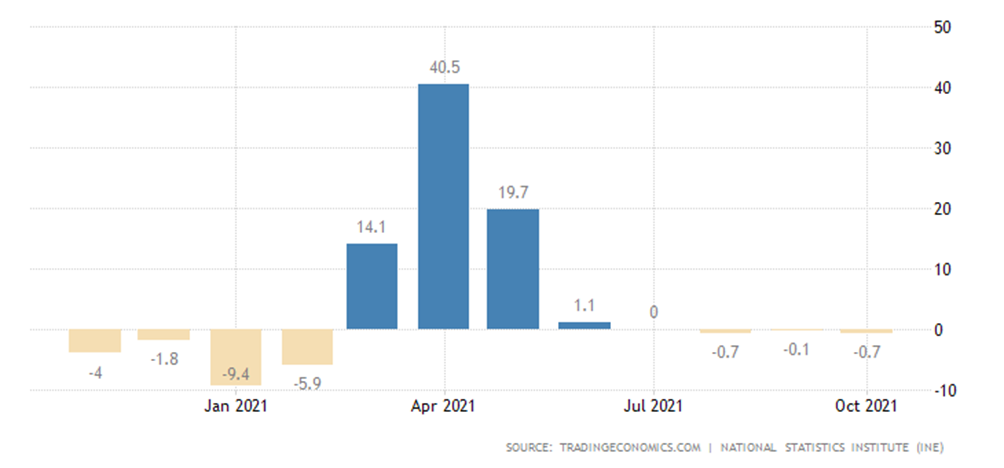

Retail in Spain -0.1% per month, in general for the last 7 months, the performance is zero:

And for the year, the performance is even negative (-0.7%):

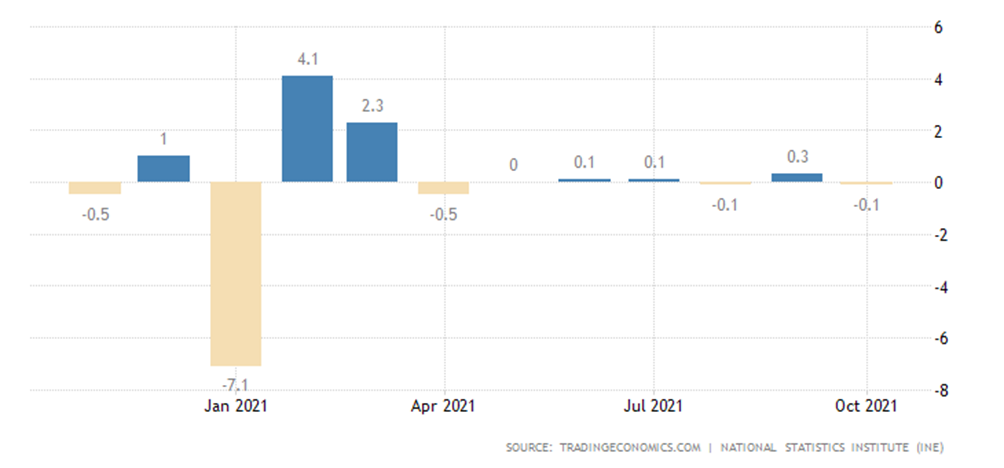

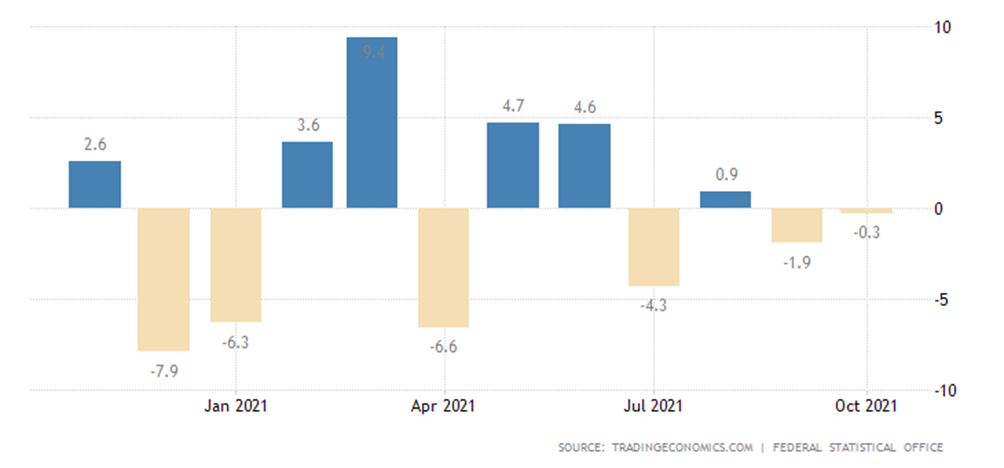

Retail sales in Germany -0.3% per month:

And -2.9% per year, that’s an 8-month trough:

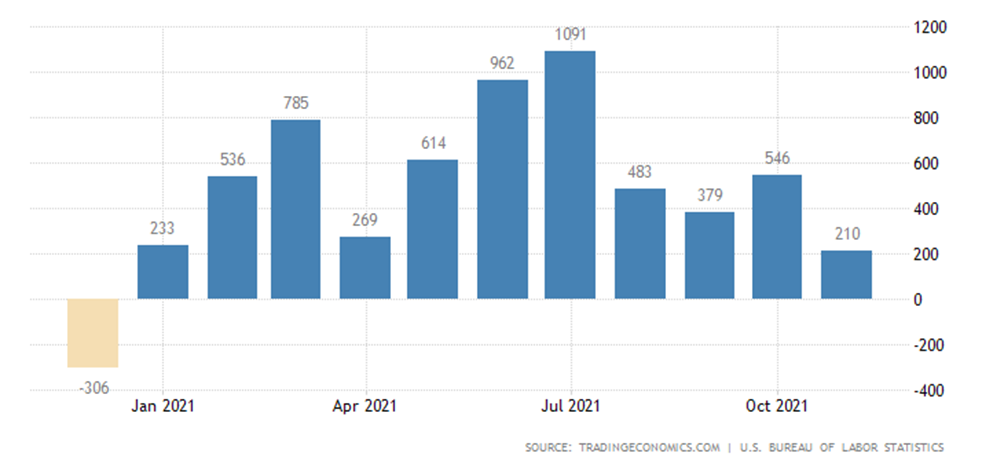

The growth of jobs in the USA in November was the lowest in almost a year and 2.5 times less than expected:

At the same time, other labor statistics data are more optimistic: the unemployment rate (U-6 indicator) in November was 7.8% compared to 8.8% in October; the level of participation of the population in the total labor force in November increased, albeit barely noticeable: 61.8% against the forecast of 61.7%; the average working week in hours also increased: in November it was 34.8 hours, in October it was 34.7 hours. However, these statistics have always been highly distorted and therefore remain problematic.

Summary. Inflation rates continue to break records, and as official figures fall behind (the authorities are expected to be encouraging), economic indicators appear to be slightly better than they are. Fed Chairman Powell recognized inflation as a long-lasting phenomenon – contrary to his forecasts a couple of months ago – and in this line began to frighten by tightening monetary policy. Since, at the same time, he also admitted that one of the reasons for the rise in prices is structural imbalances (imbalance of supply and demand), then one should not expect a simple increase in the rate, most likely, we are talking exclusively about the reduction of securities programs from the market.

There is no doubt that real inflation will have to be recognized, so the recession will be legalized, perhaps early next year. Whether a new form of epidemic, the annexation of Taiwan, or any other cause, is the cause of the epidemic is irrelevant, in our view, the structural crisis has begun and will continue until the 40-year-old imbalances are reversed (scope and details of this process, see “Reminiscences about the Future” by Mikhail Khazin).

We wish our readers a quiet, almost pre-holiday work week!