Time period: 11 – 17 September 2021

Top news story. We have two major news this time. The first is purely statistical. The NASDAQ Hi-Tech Index hit a record high against the Dow-Jones:

Similar figures were in 1999-2000, before the so-called “dot-com crisis”, so there was another indirect confirmation that financial markets were gradually starting to exceed critical figures.

The second news is that according to the Financial Times, Chinese authorities have banned alternative financial forecasts. At the same time in Shanghai authorities arrested 14 suspects in stock manipulation, removed more than 17 thousand entries in the Network with “malicious information” and closed more than 8 thousand illegal online accounts. One possible reason for this is described at the beginning of the next section of this Review, but it is also not encouraging in itself. We’ve written a lot about official officials distorting the statistics – one can assume that for China, these shifts have reached a scale that is already visible to the naked eye. It is fair to say that the United States has long ceased to publish some data on the dollar money supply.

Macroeconomics

Chinese statistics in August recorded a sharp deterioration in all sectors of the economy. Investment in fixed capital is strongly constrained:

Industrial production on a 13-month trough (+5.3% per year):

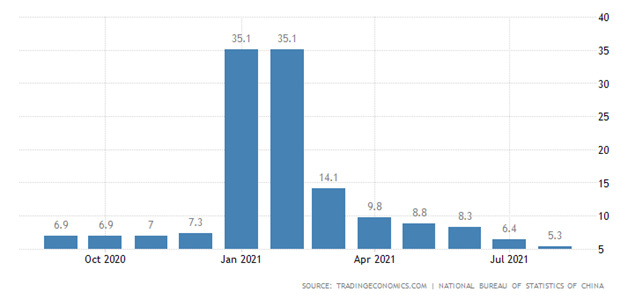

Retail sales statistics are the worst for the year (+2.0% per year):

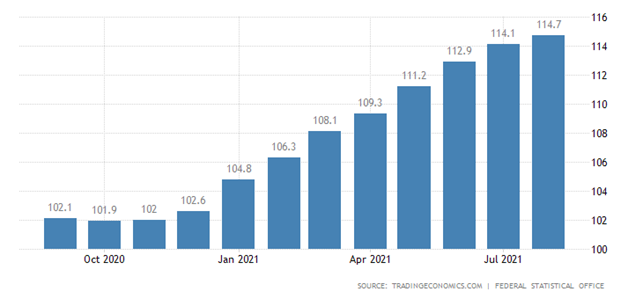

The rate of increase in newly built house prices is the lowest in 7 months (+4.2% per year):

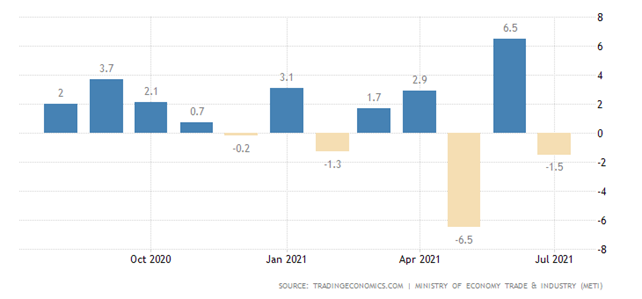

Once again, since the tradition in official economic statistics is to underestimate inflation, for the United States, industrial inflation is roughly three times lower – the real values of the indicators listed, probably a little worse. Thus, it cannot be ruled out that, in fact, China’s economy has already turned to recession. Industrial production in Japan is again in the red (-1.5%):

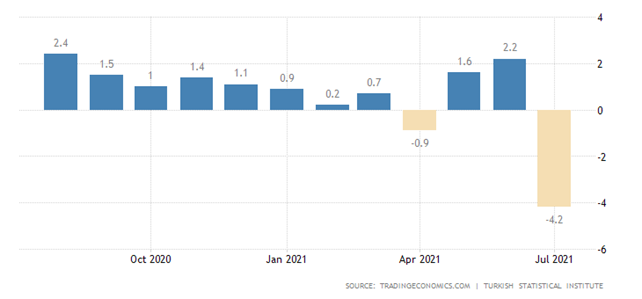

It fell even more in Turkey (-4.2%):

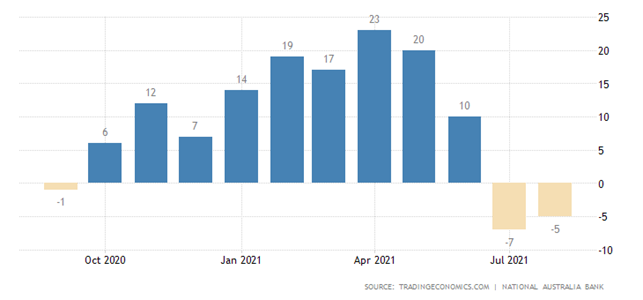

Given the extent of industrial inflation in Turkey (about 40%, see the previous section of this Review), this figure cannot be trusted. It’s probably even worse. Business confidence in Australia remains in the red:

In Japan, it deteriorated to a five-month minimum in industry and went into decline in services:

It should be noted that by the beginning of autumn industry indicators usually start to grow. Unfortunately, this year the effect seems to be much weaker than usual.

Then we begin to provide data on inflation. I remind you, reality usually exceeds official data, sometimes very significantly.

Wholesale prices in Germany are 12.3% per year, a record since 1974:

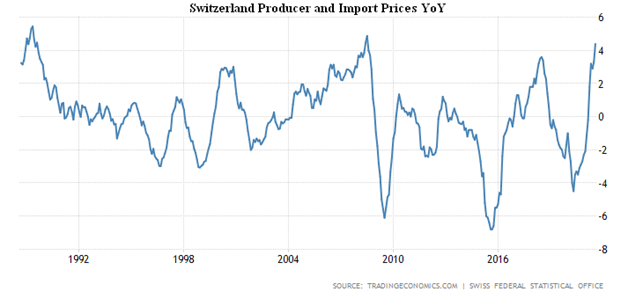

Swiss PPI (Producer Price Index) +4.4% per year, the highest since 2008 and near the peak since 1988:

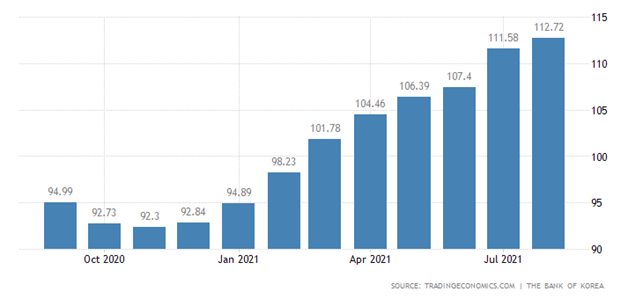

Export prices in South Korea + 18.6% per year – the highest since February 2009:

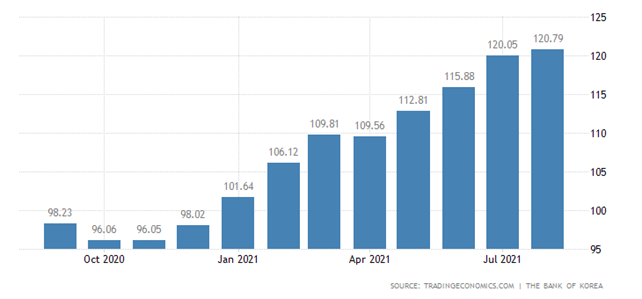

Import prices +21.5% per year, this is the peak since December 2008:

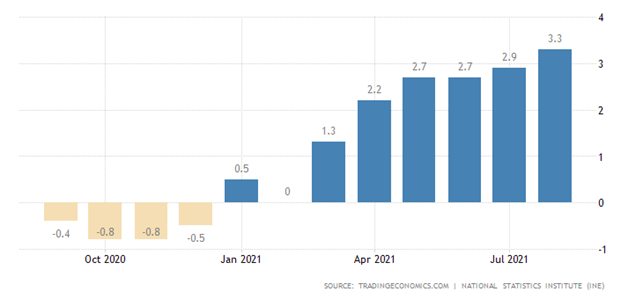

CPI (Consumer Price Index) of Spain +3.3% per year, maximum since 2012:

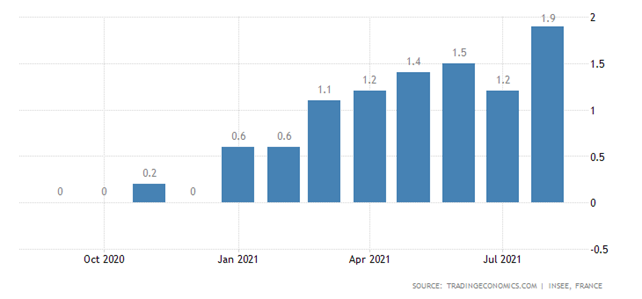

CPI France +1.9% per year – peak since 2018:

CPI of Italy 2.0% per year – the highest since 2013:

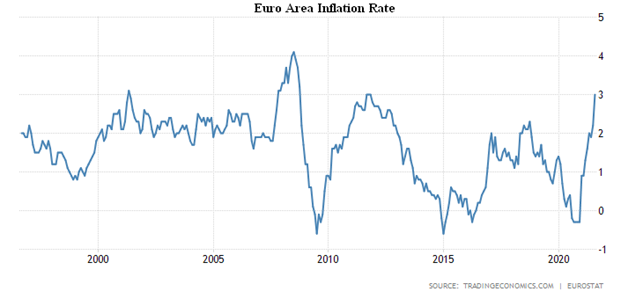

The Euro Area CPI + 3.0% per year, maximum since 2008:

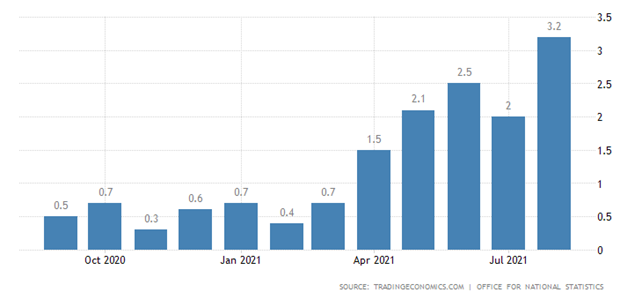

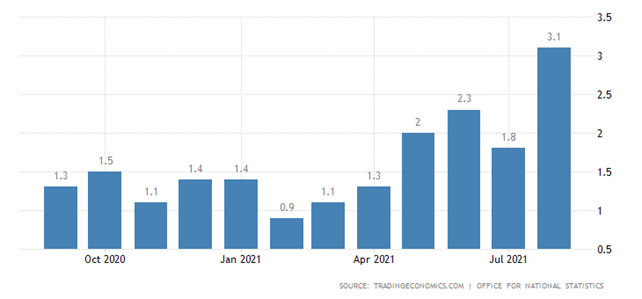

UK CPI + 3.2% per year, it’s a peak since 2012:

Without food and fuel (core inflation rate) – since 2011 (+ 3.1%):

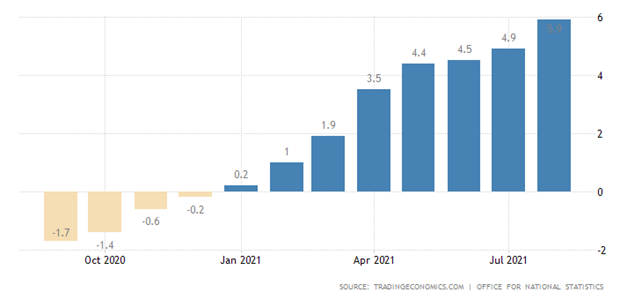

At its peak since 2011, also the British PPI (+5.9%):

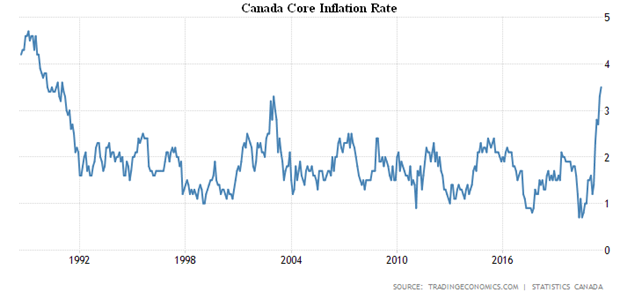

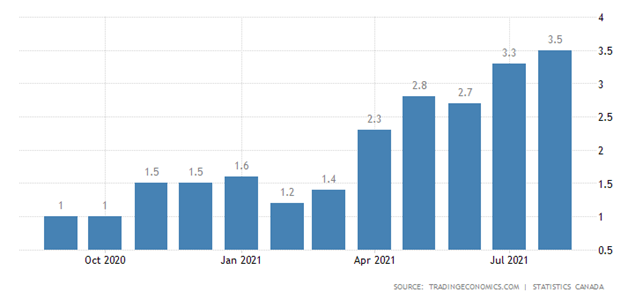

CPI Canada 4.1% per year, it’s the highest since 2003:

Without food and fuel 3.5%, which is the peak since 1990:

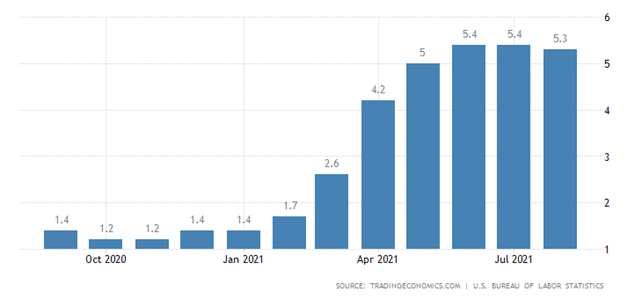

In the US, inflation (i.e., Consumer Price Index [CPI]) became slightly slower (+ 5.3% per year after a record + 5.4%):

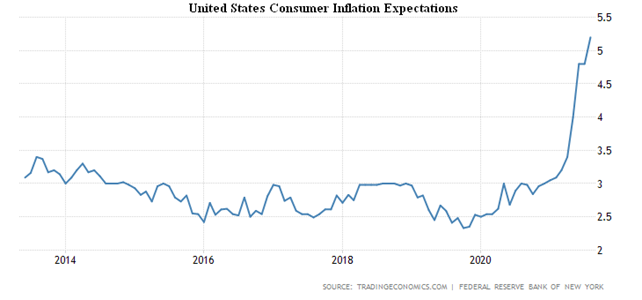

Nevertheless, inflationary expectations in the US are at a record high (+5.2%):

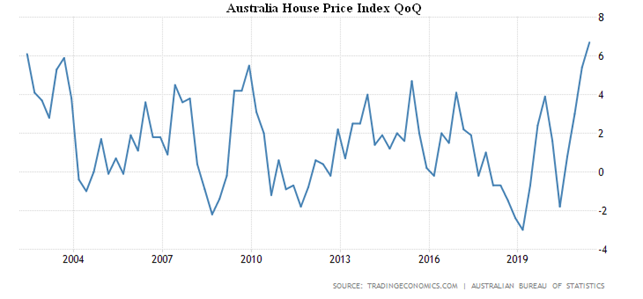

Housing prices in Australia in 2 quarters are +6.7% per quarter and +16.8% per year, the highest in 18 years:

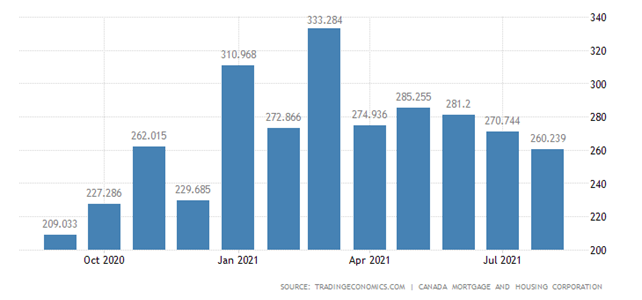

The number of new buildings in Canada is the lowest in eight months:

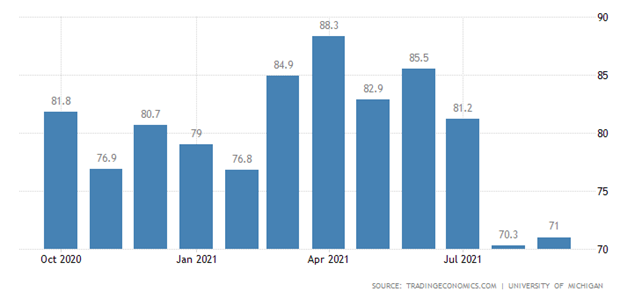

American sentiment has only slightly moved away from a 10-year low:

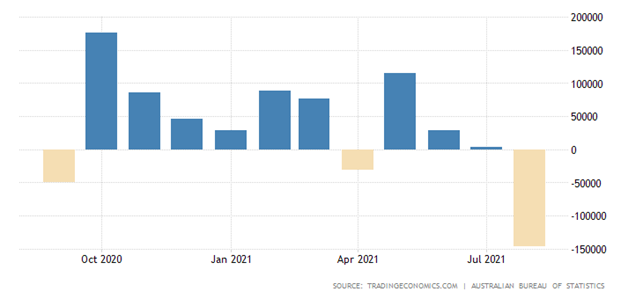

Employment in Australia declined at the worst rate since May 2020:

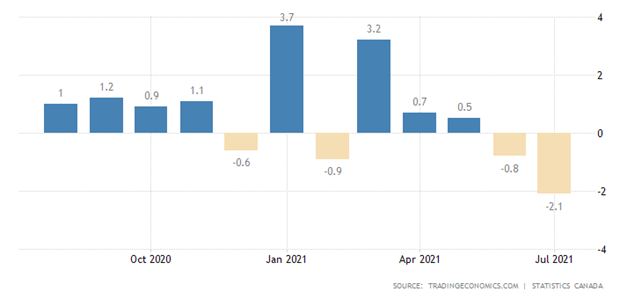

Wholesale sales in Canada -2.1% per month, the second consecutive negative and the worst decline in 16 months:

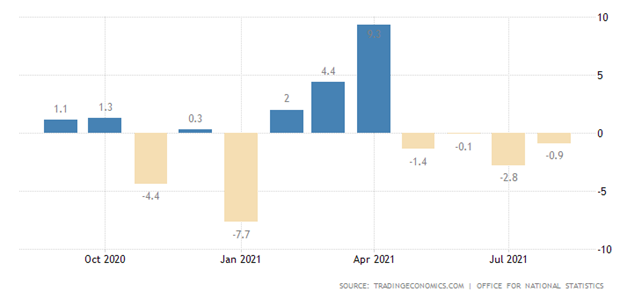

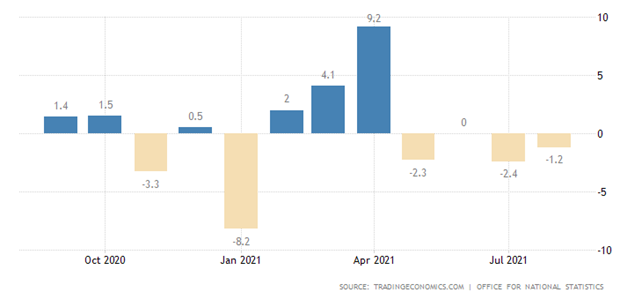

Retail sales in Britain have been slumping on a monthly basis for 4 consecutive months for the first time in 25 years of observation:

The same is true for sales without gasoline, where the decline is even more pronounced:

Summary. Despite the end of the holidays, there are no signs of recovery from the crisis. Moreover, inflation indicators are deteriorating everywhere, and the relatively positive performance of industrial growth is likely to be the product of official statistical creativity in data correction. Indirectly, this view is confirmed by the fact that once we go beyond traditional statistics (which official experts spend most of their energy on improving), indicators deteriorate significantly.

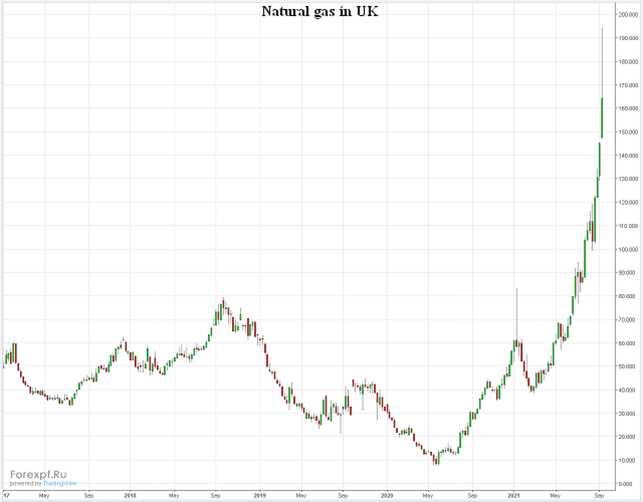

In this sense, the policy of the Chinese leadership (see the first section of the Review) is highly revealing, since, given the huge emissions by the Chinese Government into the real economy, it certainly does not depend on the deteriorating investment environment. And we can add a variety of individual signals that are coming up more and more frequently in the news. For example: “The rise in energy prices in Europe creates risks of power outages this winter, especially if the cold weather depletes already low reserves of natural gas earlier,” warns Goldman Sachs.

Against the backdrop of gas prices in England, this news is somewhat irritating:

Of course, optimists might say that this is just an attempt to drive the market apart, but trends are still worrisome.

We wish you all comfortable to enter the working season!