July 15-21, 2023

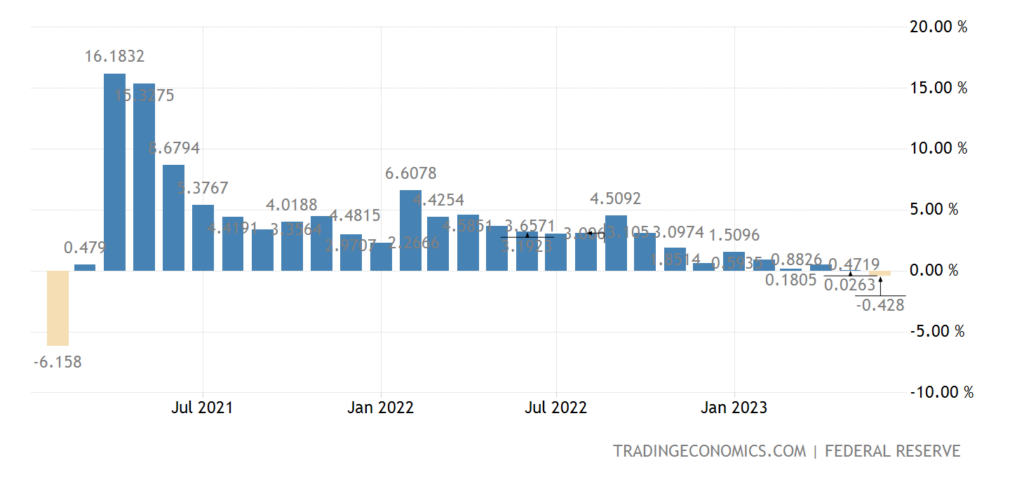

Big news. Summer, little news, but the main news is. We have been writing about the industrial recession in the United States for several months now (according to official data, in reality it has been going on since the fall of 2021). But on an annual scale, it was somewhat offset by the previous recovery growth. Again, in reality, this growth ended earlier than at the end of 2022, but, we repeat, we are working with official US data.

And now, data on US industrial growth on an annual scale for the first time after quarantine showed a decline, -0.4% per year – the 1st minus over the past 28 months:

Pic. 1

Since the real decline continues at a fairly constant rate, now this figure should gradually increase and reach in half a year (that is, somewhere by January 2024) to about minus 7-8%. Of course, in reality they will try to downplay it, but it seems to me that this will be quite difficult to do. In any case, we will keep an eye on this situation.

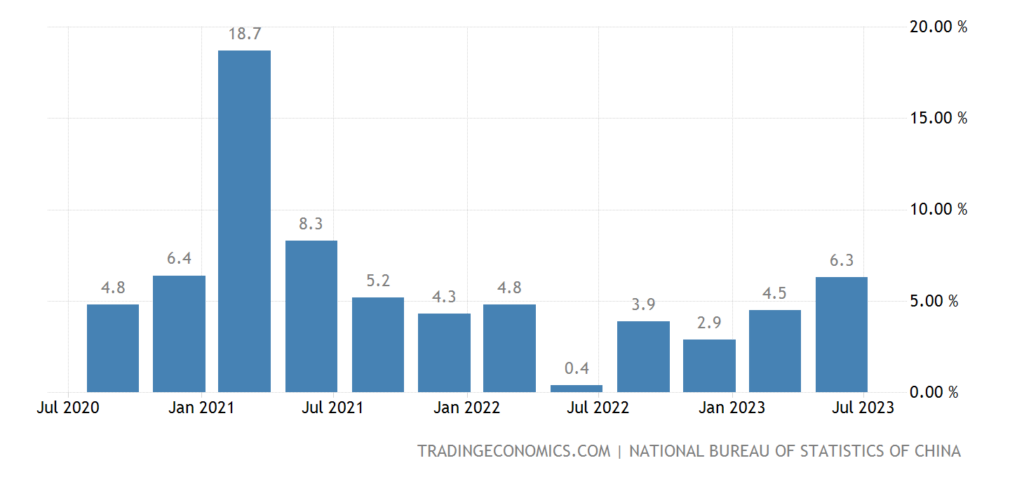

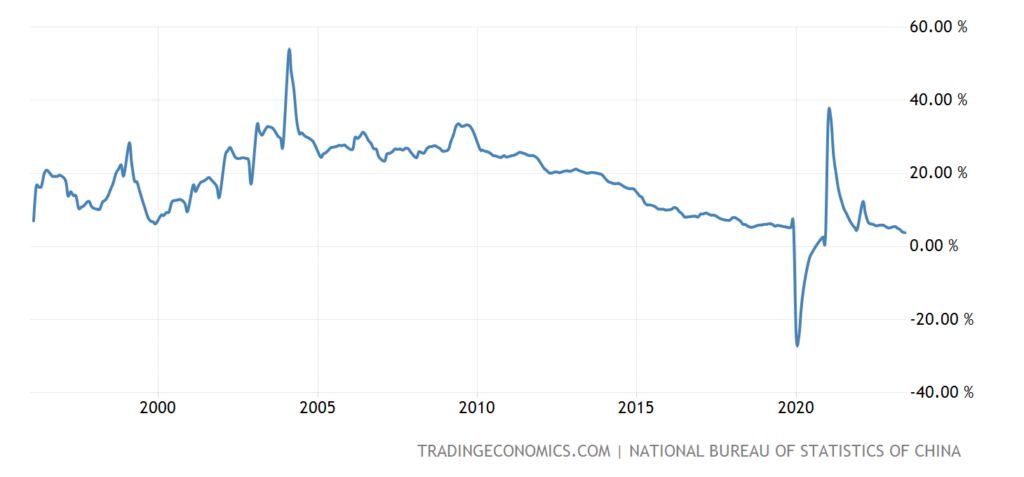

Macroeconomics. Rather, out of habit, we look at China’s data. On the whole, they disappointed again, so that the decline we have already noted has been confirmed. Although there are small gaps.

GDP accelerated due to the low base effect a year ago, but noticeably lost to forecasts:

Pic. 2

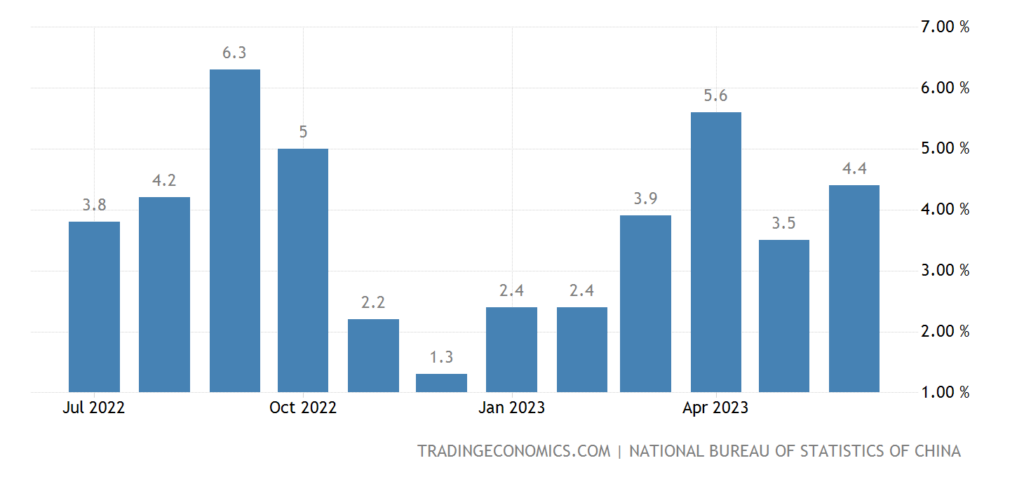

But industrial production surpassed them:

Pic. 3

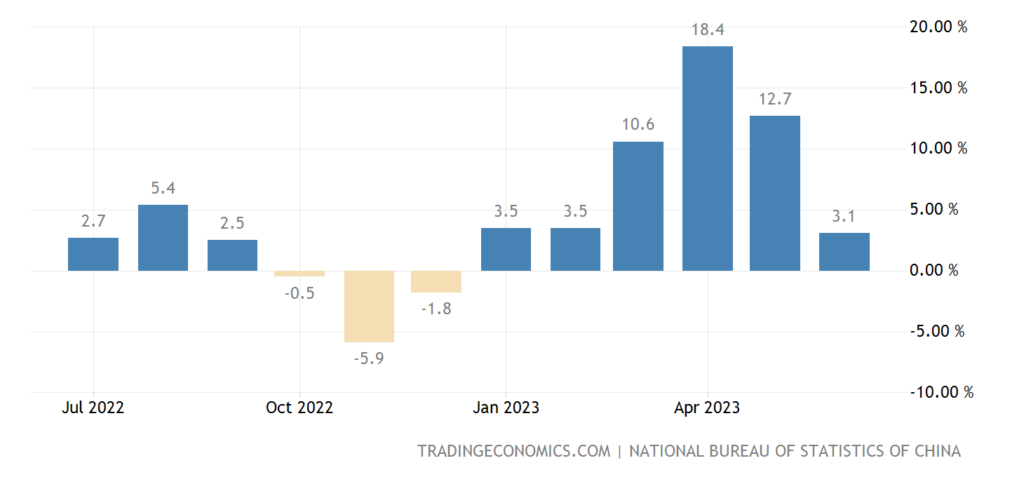

Retail sales grew at the lowest pace in six months:

Pic. 4

Investments in fixed assets showed (excluding 2020) the worst dynamics in history:

Pic. 5

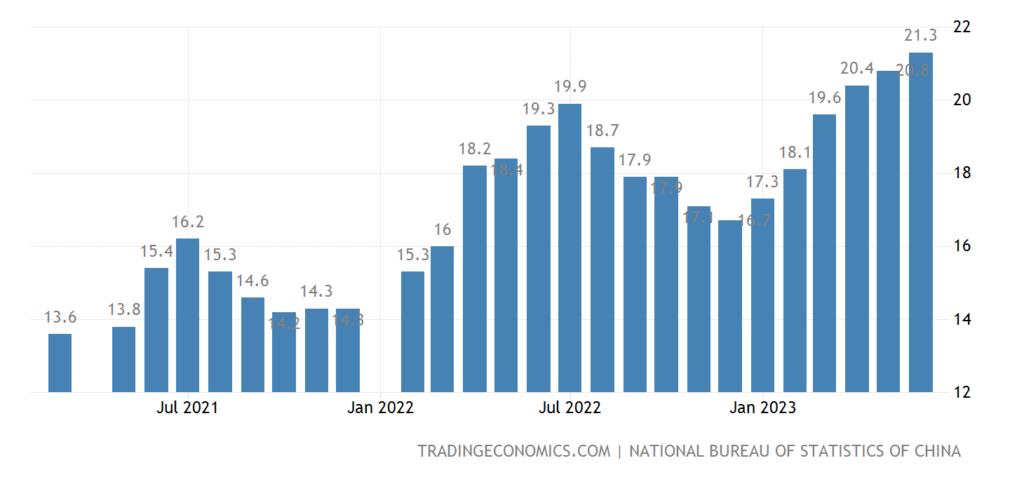

Youth unemployment also reached a record high (21.3%):

Pic. 6

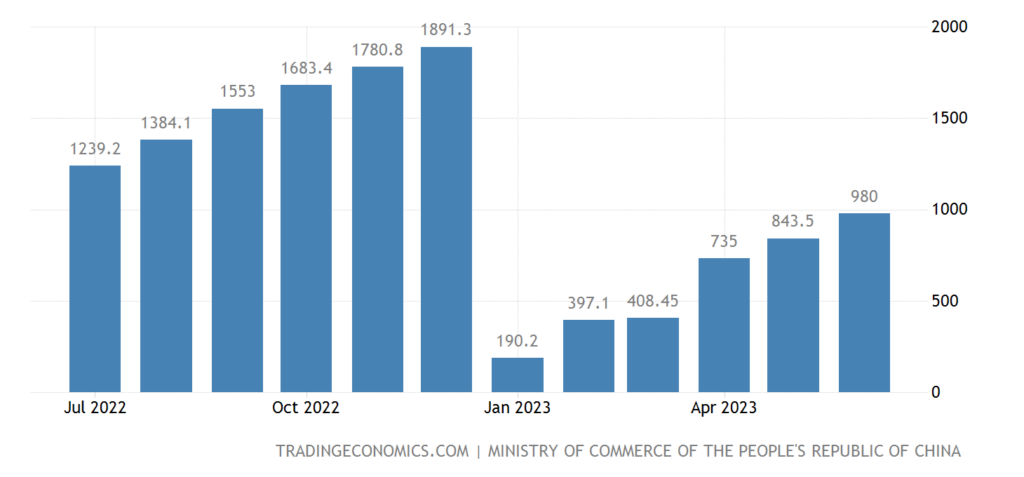

Finally, foreign direct investment again went into the red:

Pic. 7

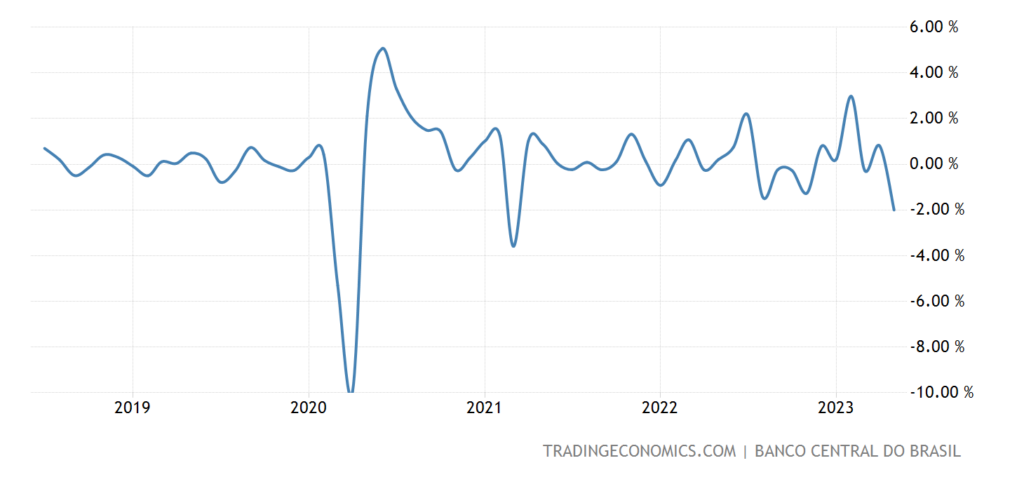

Economic activity in Brazil is -2.0% per annum, excluding the covid dip, this is a 5-year low:

Pic. 8

A similar picture in Argentina, where -5.5% per year:

Pic. 9

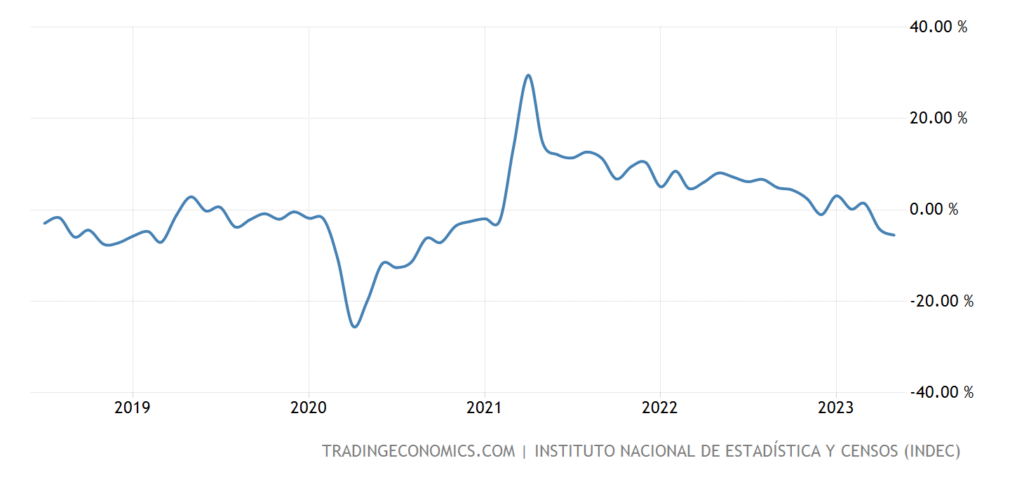

Industrial production in the USA -0.5% per month – 2nd negative in a row:

Pic. 10

Given the main news, this is almost obvious.

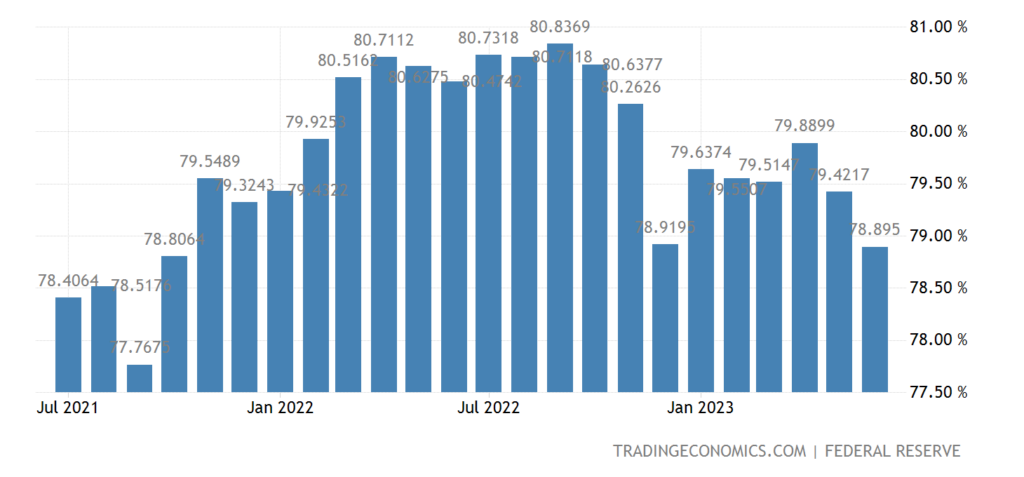

Capacity utilization is the lowest in almost 2 years (78.9%):

Pic. 11

How to restore the real sector in such a situation? Not very clear.

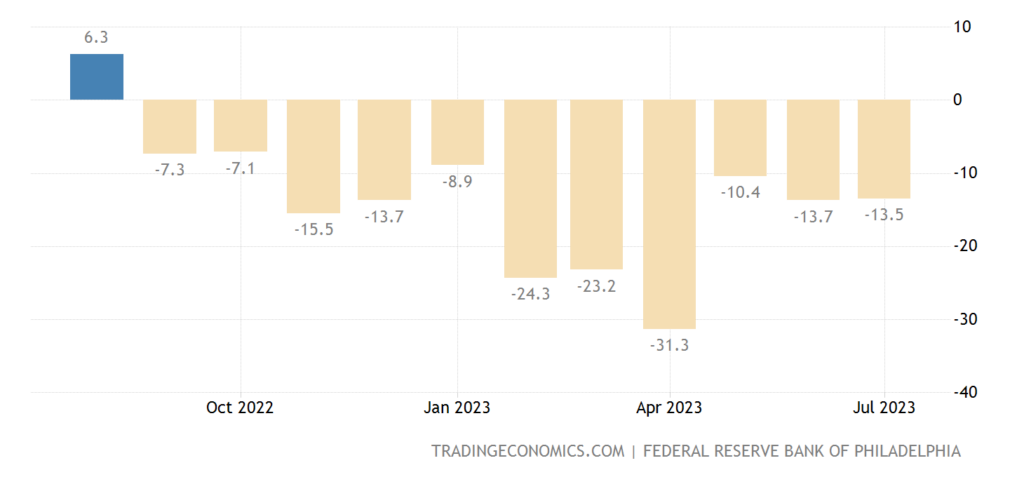

The Philadelphia Fed Zone activity index in the US has been in the red for 11 straight months:

Pic. 12

Index of leading indicators in the US -0.7% per month – the 15th negative in a row:

Pic. 13

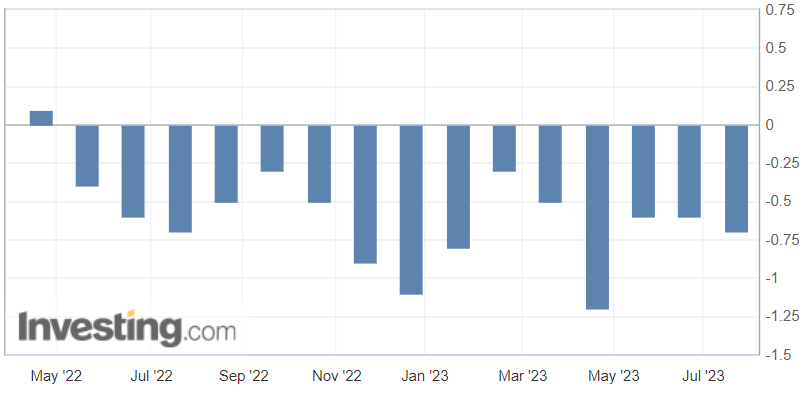

France’s business climate index is at its lowest in 27 months:

Pic. 14

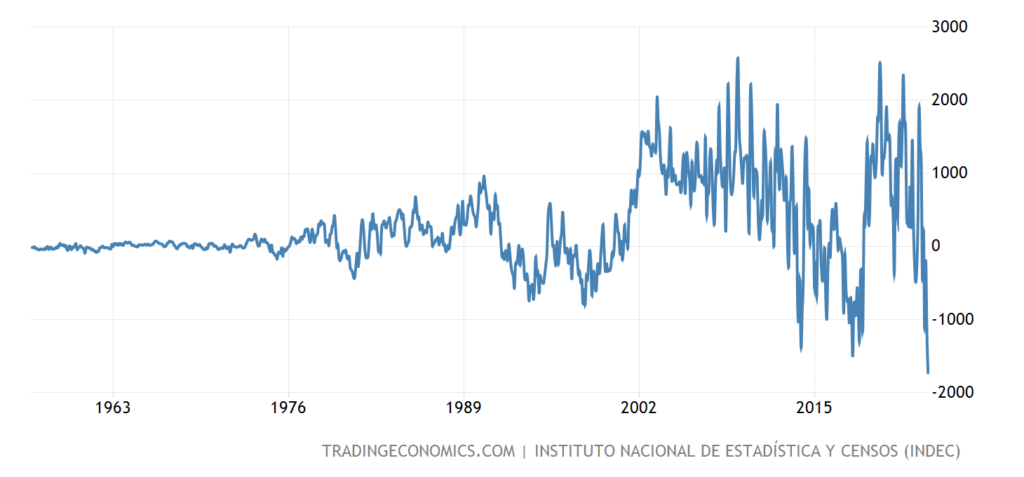

Argentina has the largest ever data collection (66.5 years) trade deficit:

Pic. 15

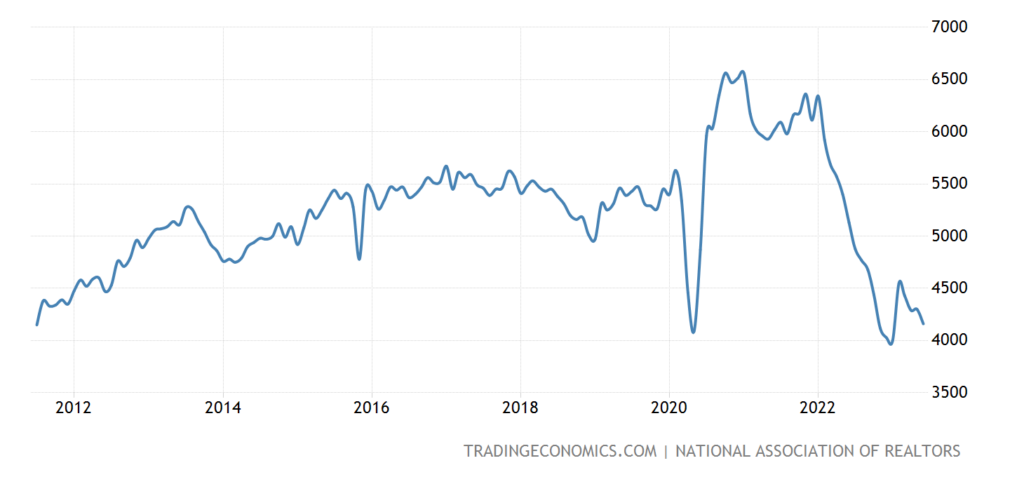

US existing home sales weakest in 5 months, 12-year low not far off:

Pic. 16

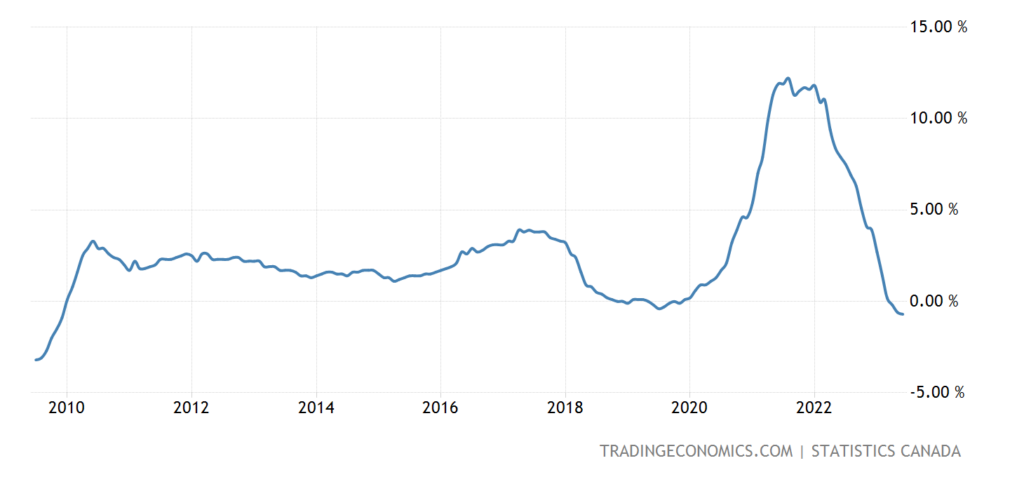

Prices of new buildings in Canada -0.7% per year – the worst dynamics since the end of 2009:

Pic. 17

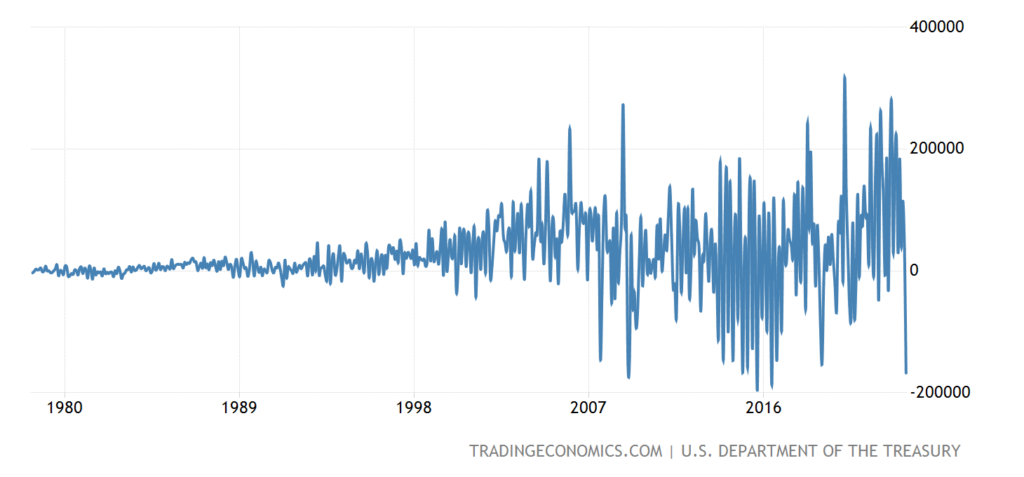

The net outflow of foreign capital from US securities in May was almost a record (-$167.6 billion), slightly worse only twice, in 2015 and 2016:

Pic. 18

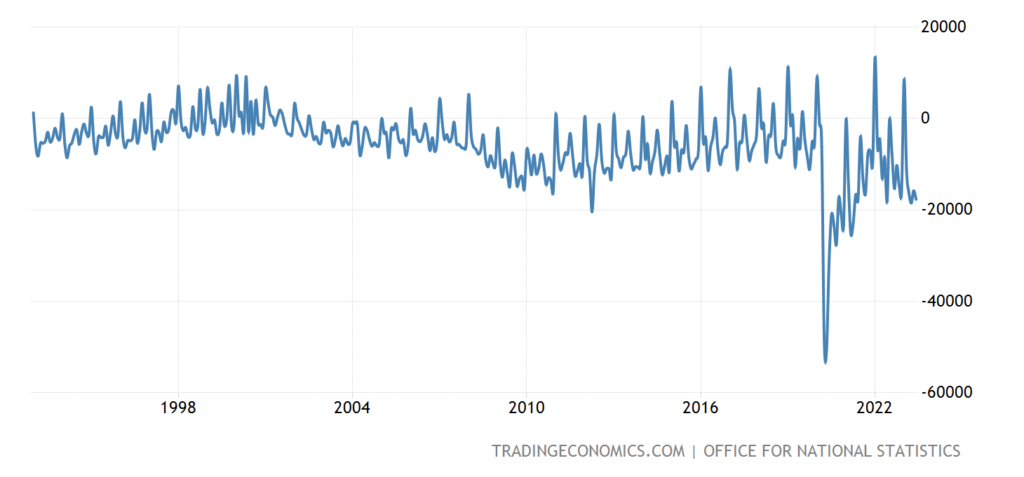

UK Budget Deficit at Historical Peaks (excluding surge due to covid):

Pic. 19

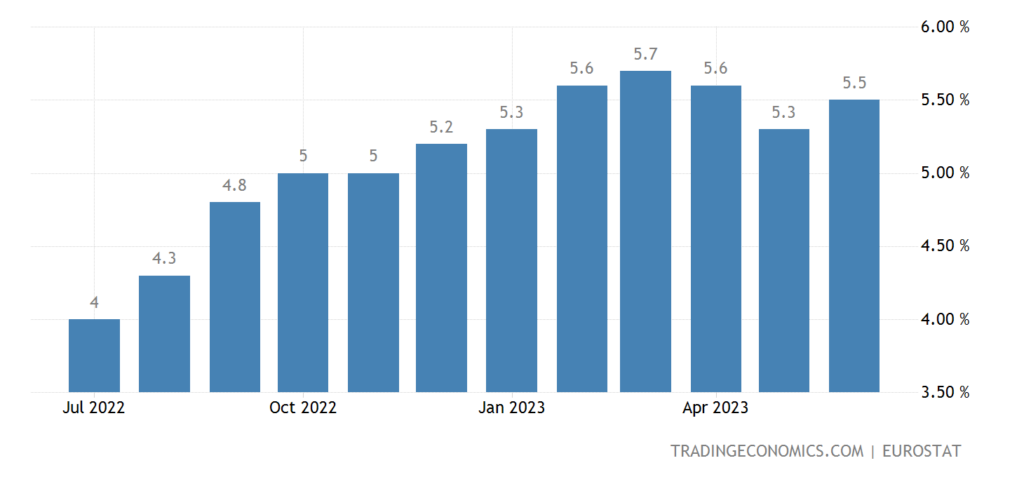

Net (excluding volatile components of fuel and food) CPI (consumer inflation index) of the eurozone accelerated again (to +5.5% per year):

Pic. 20

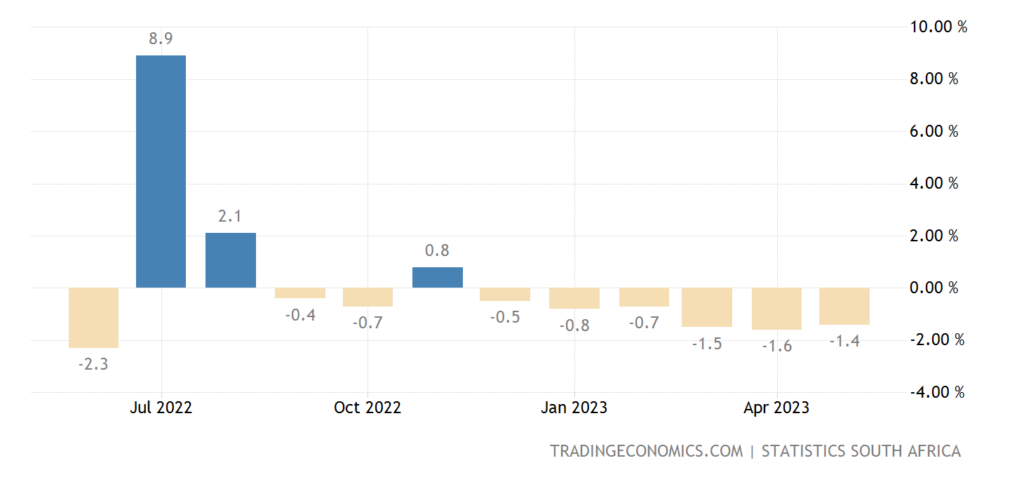

Retail South Africa -1.4% per year – 6th negative in a row:

Pic. 21

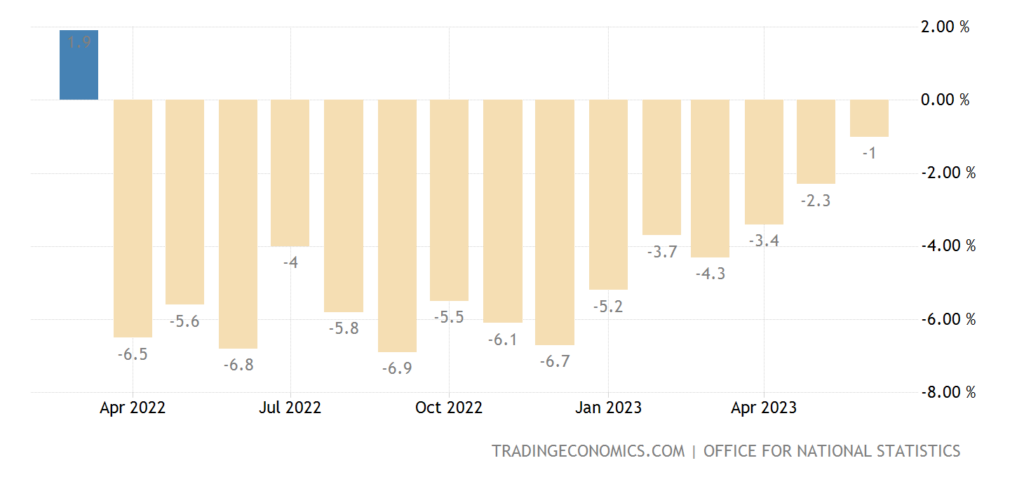

UK Retail -1.0% per annum — 15th consecutive negative:

Pic. 22

The Central Bank of Turkey raised the interest rate by 2.5% to 17.5%. The Central Bank of China left rates unchanged after cutting them a month earlier. The Central Bank of South Africa did not change anything either.

Main conclusions. As noted in the first section, summer. There are few events, more precisely, few economic events, just a lot of political events, since the economic crisis is already causing political consequences.

The structural crisis in the global economy continues as usual: here and there things get worse. But it is very interesting how the US monetary authorities will behave in terms of ascertaining the industrial decline. Either they will ignore it and the recession will intensify, or they will somehow begin to show that the situation is improving. This is the main intrigue of the coming weeks. By the way, will they correct the deflationary tendencies in the industry? Also interesting.

In the meantime, we wish everyone pleasant holidays, and if they are far away – a good weekend and a not very burdensome working week!