Period: 22 – 28 August 2020

Top news story. There were two headlines last week.

- The first is not formally economic but political. As a result of the convention (congress) of the US Democratic Party, the rating of its main opponent – Donald Trump has increased. This has never happened before in our memory, or even perhaps in history. This shows not only the political problems, but also that the Democratic Party (which represents the interests of the financial community, which have been shaping the economic agenda for decades) does not have any, even hypothetical, models for improving the economic situation.

- The second news is that stock markets have grown dramatically despite a very pessimistic picture in strategy. This means that the inflationary process has begun to have a negative impact, and the consequences will be apparent within a few months.

Macroeconomics

Q2 GDP figures show that the scale of the quarantine crisis is enormous.

Germany’s GDP slumped by 9,7% per quarter and 11,3% per year in in Q2 – a record decline in 50 years of observation. France’s GDP -13,8% per quarter and -19,0% per year – is the lowest in 70 years of observation. Mexico’s GDP -7,1% per quarter and -18,7% per year – is also the worst in history.

US GDP -7,9% per quarter and -9,1% per year – record lows in 72-73 years of observation. However, even these negative indicators raise questions. If we take (we are talking about official data) the nominal value of GDP and divide it by the nominal value of the GDP deflator, we get -9,1% per quarter, and not at all -7.9%.

At the same time, the US budget deficit grew 4 times and tripled the anti-record of 2009, due to which the aggregate domestic demand in Q2 skyrocketed 11,2% per quarter (sparking record highs in retail and housing in the summer). This growth in financial markets is due to the fact that money is still returned to the financial sector through repayment of debts. That money requires some use. But real private demand has slumped by 9,8%; of course, such deficits cannot be sustained for long, so early payback is inevitable. This is likely to happen even before the 3 November elections.

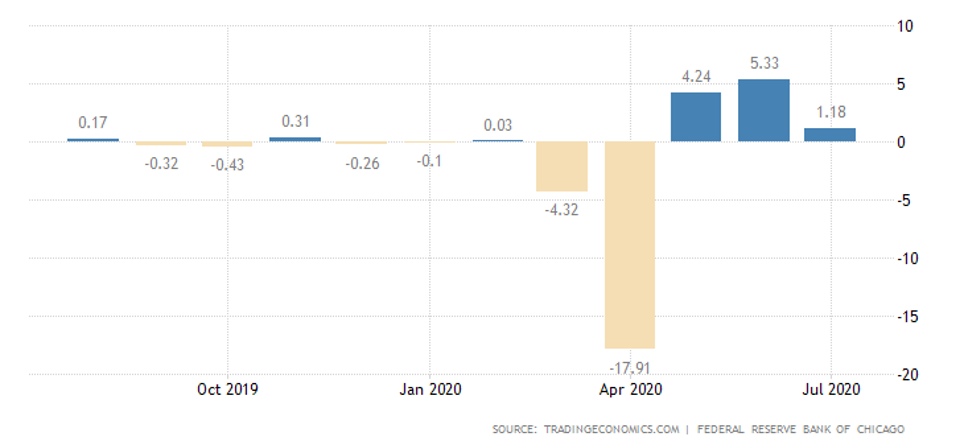

United States Chicago FED National Activity Index fell sharply from July:

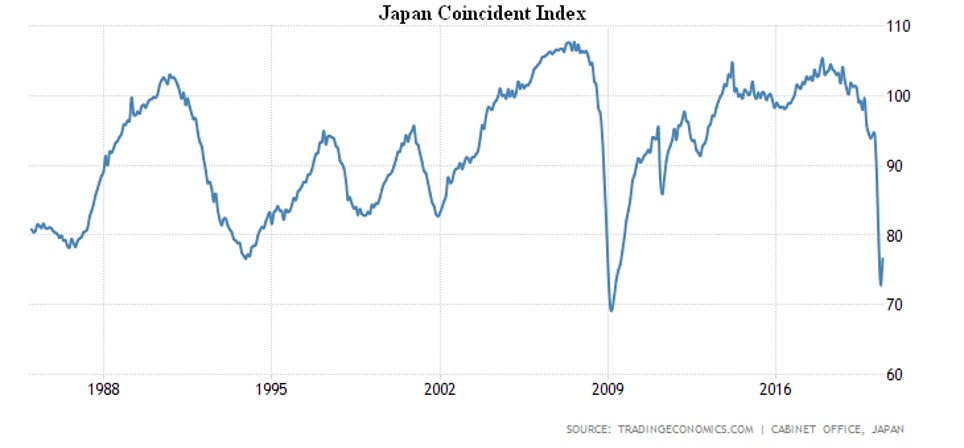

Leading indicators in Japan are recovering slowly, while coincident indicators are not improving at all:

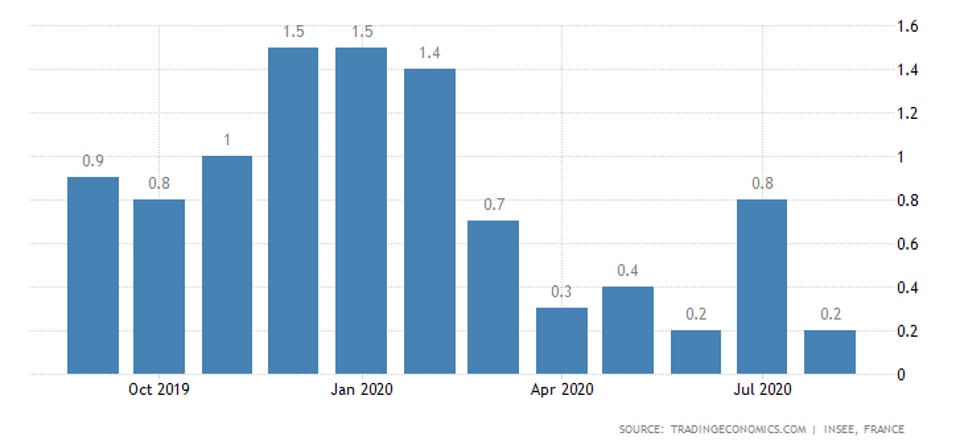

France’s CPI slowed again to a 4-year minimum:

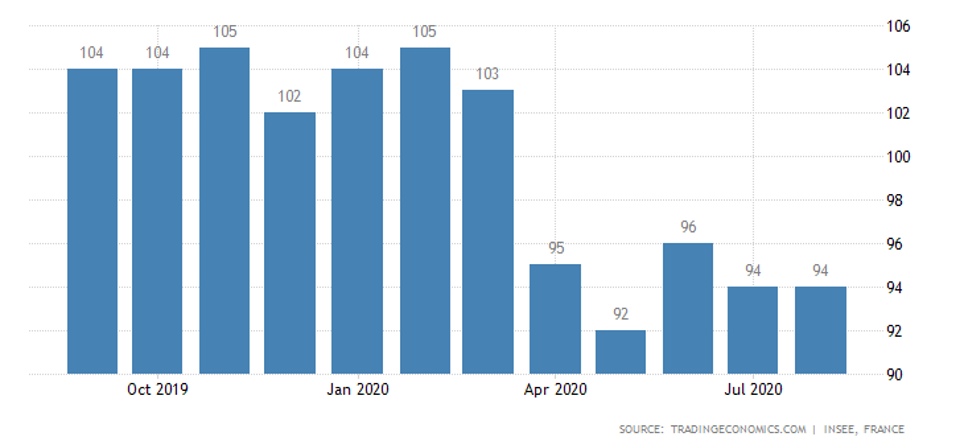

French consumers’ market sentiments are stuck at levels far from optimistic:

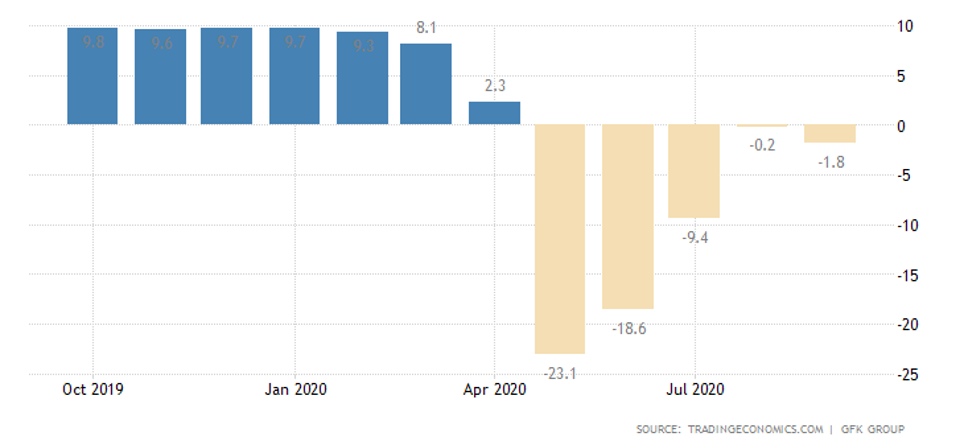

German market sentiments have even worsened:

The Conference Board’s American market sentiment in August fell below the worst at the peak of the coronavirus crisis. They scored worst since May 2014.

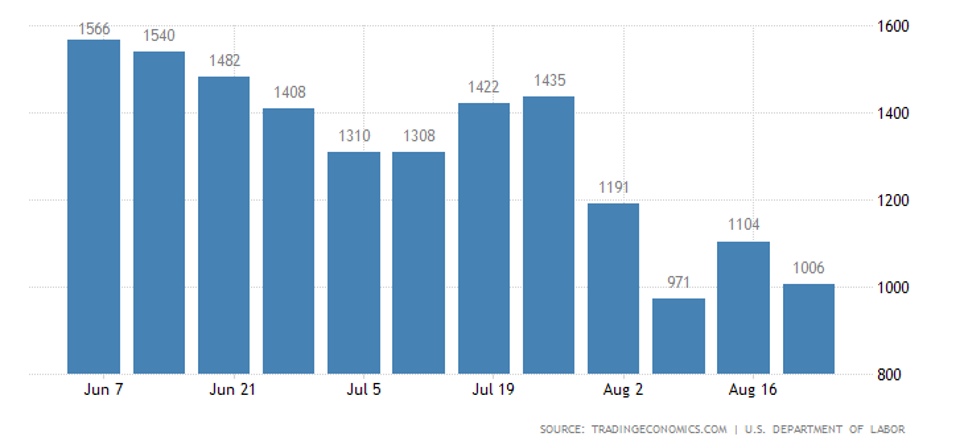

The number of initial jobless claims in the U.S. again exceeded 1 million per week:

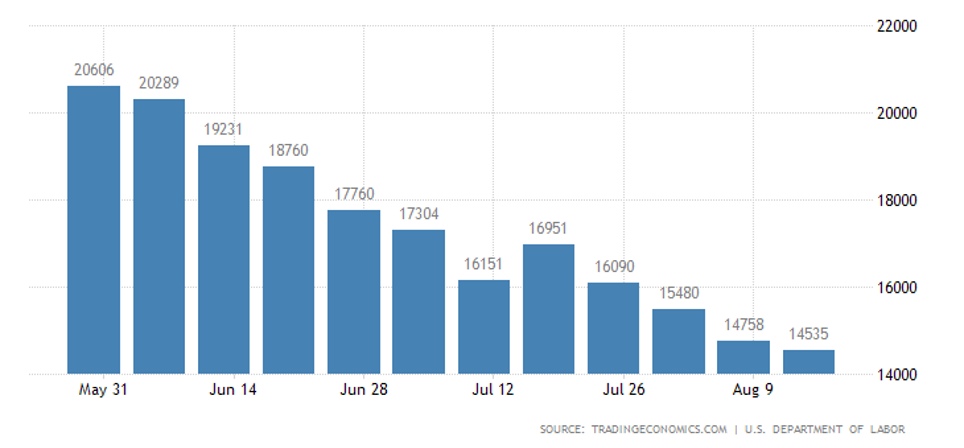

The number of continuing jobless claims is decreasing slowly:

The total number of beneficiaries in all programmes remains huge, over 27 million.

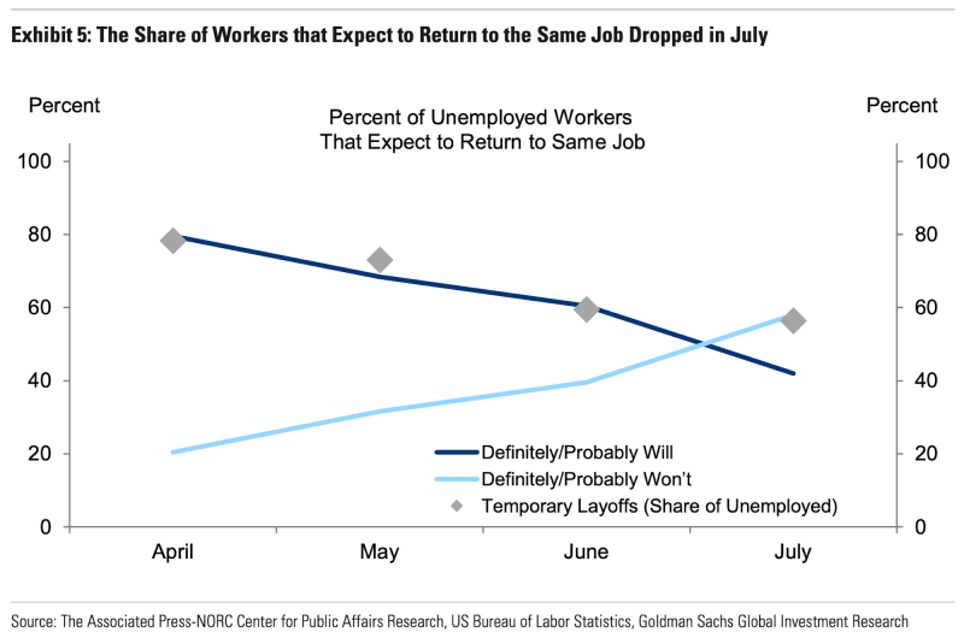

At the same time, unemployment is perceived as increasingly hopeless. While in April 80% of those who lost their jobs considered it a temporary condition and hoped to regain their previous positions, only 40% now do so, and 60% of the unemployed believe that previous jobs have been irretrievably lost.

New Zealand retail sales plummet 14,6% per quarter and 14,2% per year in Q2, the worst in history.

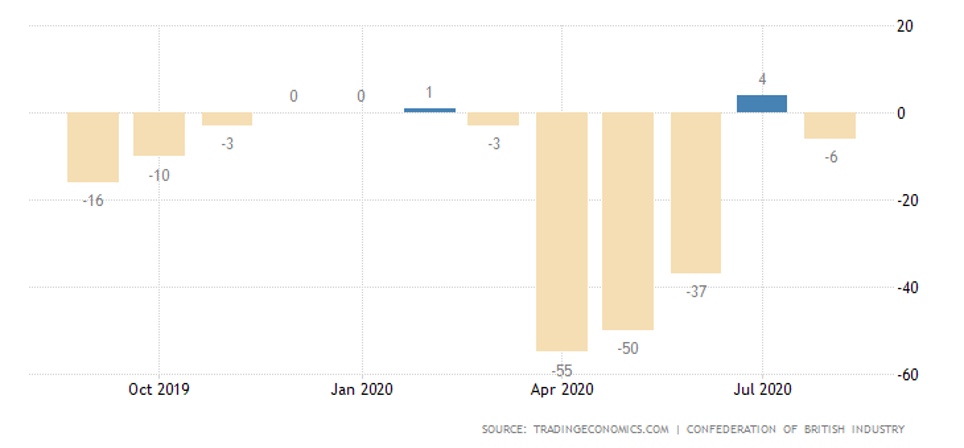

The retail balance in Britain in August suddenly went negative again:

FED Chairman Powell, speaking at a virtual conference held this year in Jackson Hole, announced a change in inflation targeting. The target of the new inflation targeting will not be current inflation but average inflation. If the CPI surpasses the 2% target, this will be interpreted as compensation for today’s low inflation. Policy tightening will be considered only if the CPI is kept above this level for a long time.

The Central Bank of South Korea left the rate at a record low of 0,5%, while the projected GDP for 2020 fell to -1,0%.

Summary. US monetary authorities are aware of the inevitability of inflation (CPI – consumer inflation), but no immediate action is being taken. Indeed, the nature of these measures remains unclear. Whereas the classic measure to combat inflation is tightening monetary policy, i.e. increasing the value of debt. With the current level of debt, this would almost automatically cause all financial markets to collapse. In fact, FED Chairman Powell admitted that the size of the accumulated debt does not allow fiscal tightening.

At the same time, persistent debt refinancing is already a threat, as it leads to rapid financial «bubbles». However, it is equally dangerous to slow down the process, as reducing the amount of credit in this situation is tantamount to increasing its cost. Thus, the question today is not whether financial markets will collapse or not, but when they will collapse.

But US household consumption before the election will not be affected – thanks to the FED, Donald Trump has enough money to ensure their standard of living. But immediately after the election, the rampant consumption with printed money will cease. The consequences will be far worse than in the 1930-32 crisis.