August 12-18, 2023

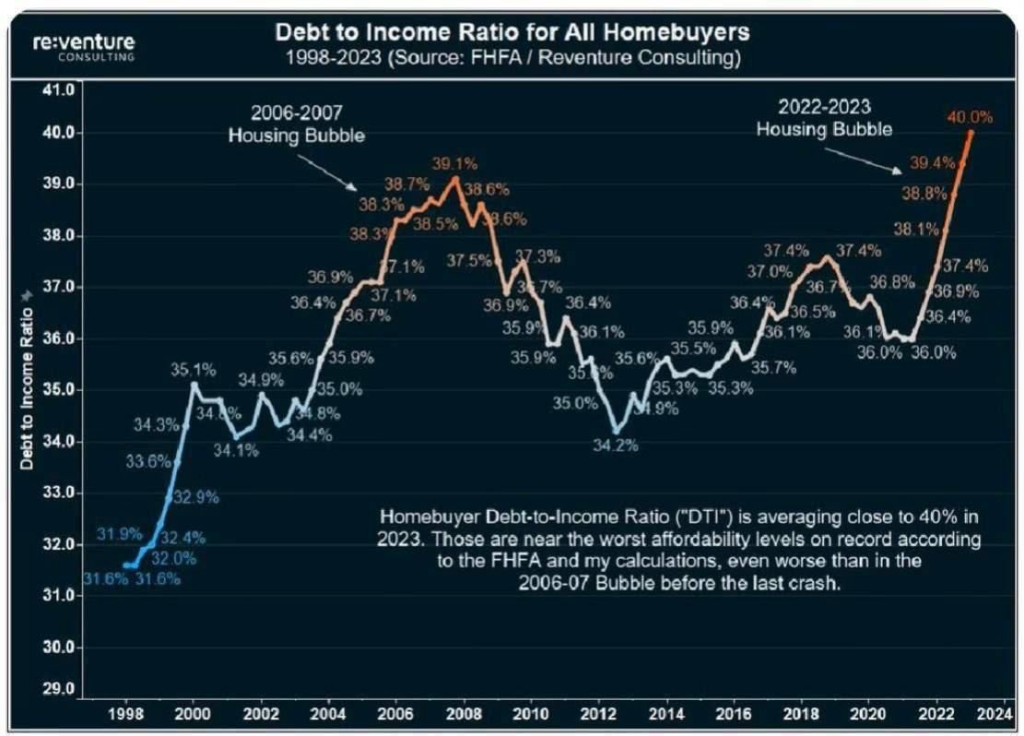

Big news. Summer, little news… But something can be noted. First of all, that the share of mortgage debt in relation to real disposable income has reached very high positions:

The indicators of 2006-2007, when the sub-prime mortgage crisis occurred, were exceeded. Of course, then – not now, but the trend in which the growth of debt in relation to income is not going to stop, causes natural fears.

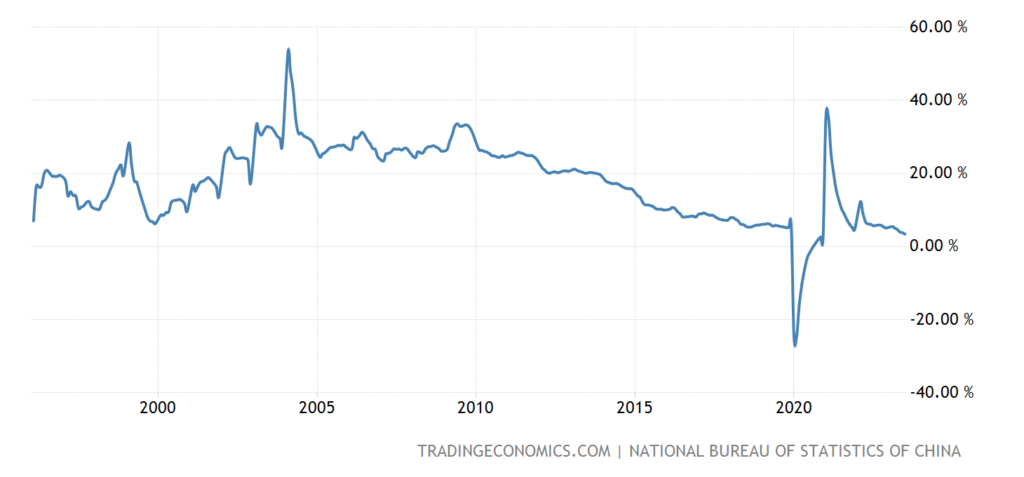

Macroeconomics. It seems that with the Chinese economy, which has firmly entered the crisis, everything is clear, but the habit of looking at it has remained. And China’s numbers continue to deteriorate.

Investments in fixed assets + 3.4% per year – excluding the failure of 2020, this is an anti-record for 27 years of observation:

Pic. 2

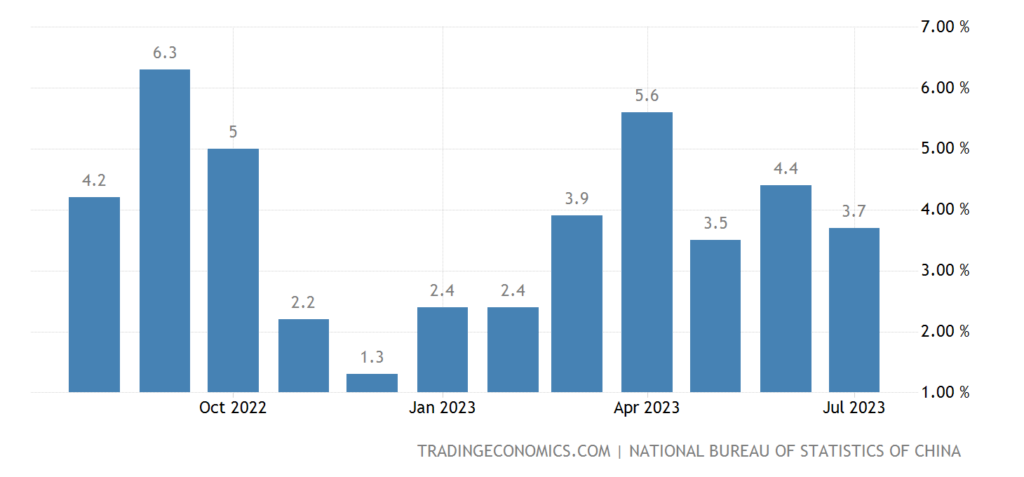

Industrial production slowed to +3.7% y/y:

Pic. 3

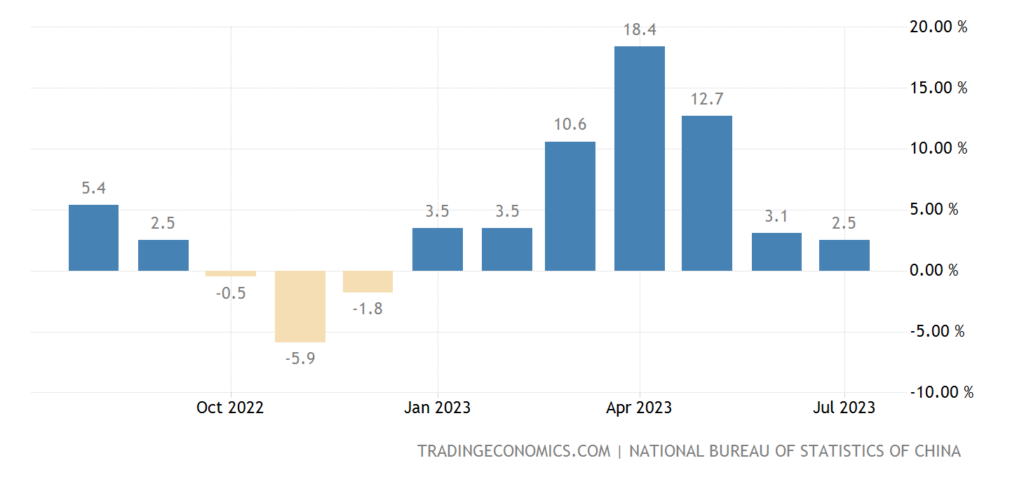

Retail +2.5% per year – 7-month minimum:

Pic. 4

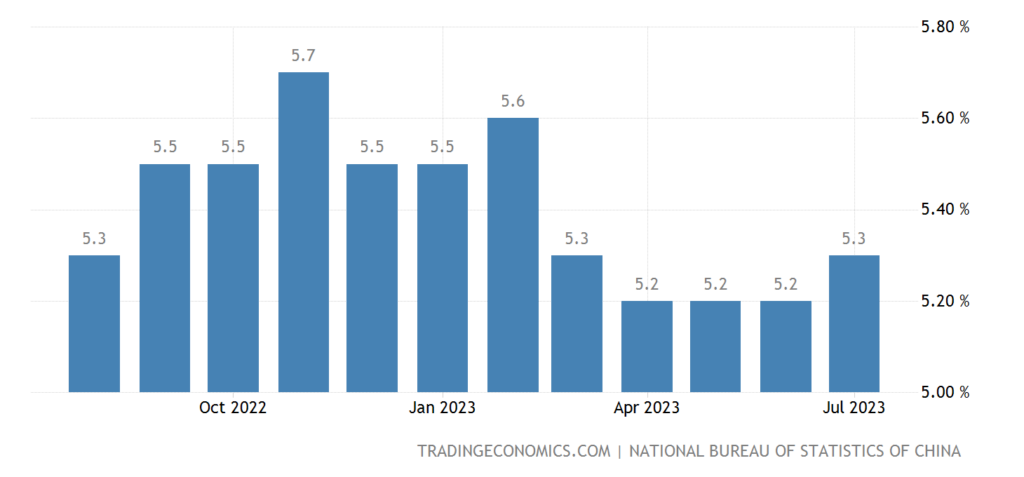

Unemployment rose to 5.3%:

Pic. 5

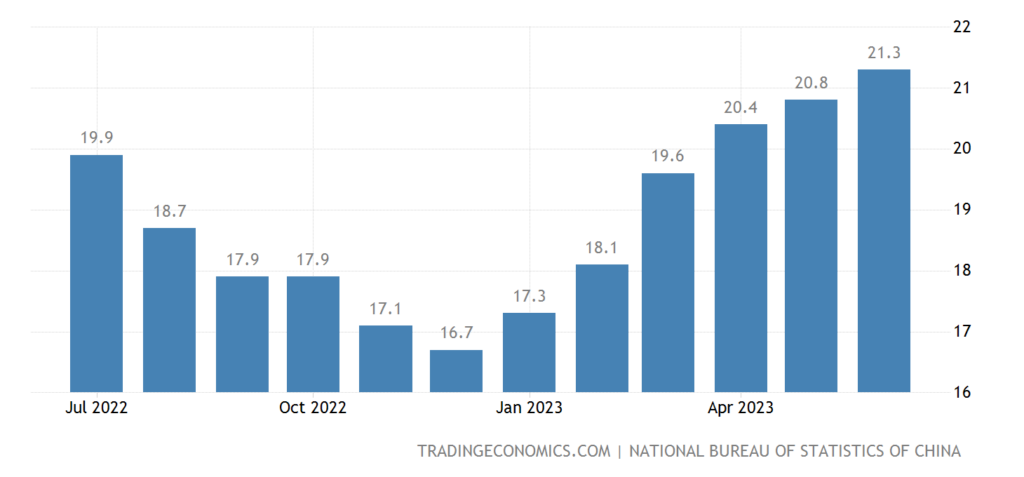

Including youth unemployment is record (21.3%):

Pic. 6

Let no one be misled by positive figures – the problem of underestimated inflation today is in the statistics of all countries of the world.

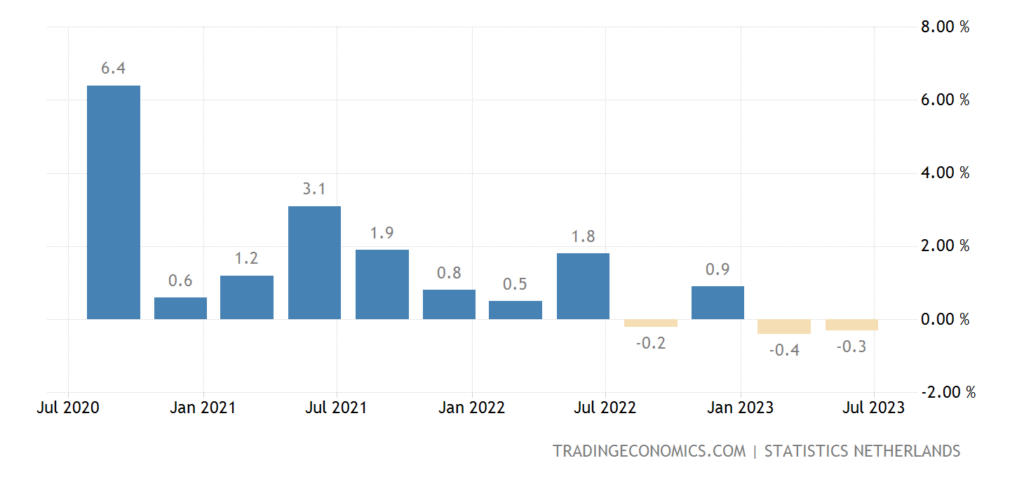

Dutch GDP -0.3% qoq – 2nd minus in a row (previously -0.4%):

Pic. 7

And -0.3% per year – returned to decline after a 2-year break:

Pic. 8

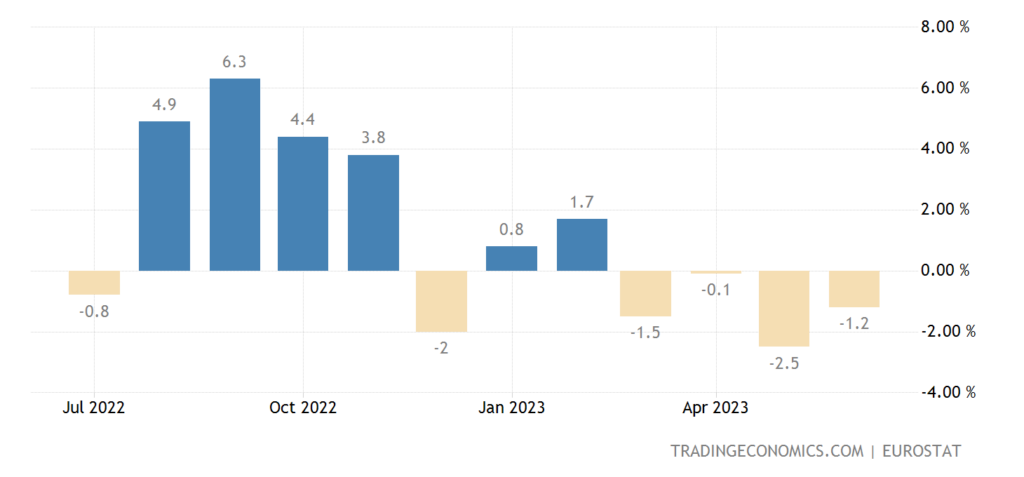

Industrial production in the eurozone -1.2% per year – 4th monthly loss in a row:

Pic. 9

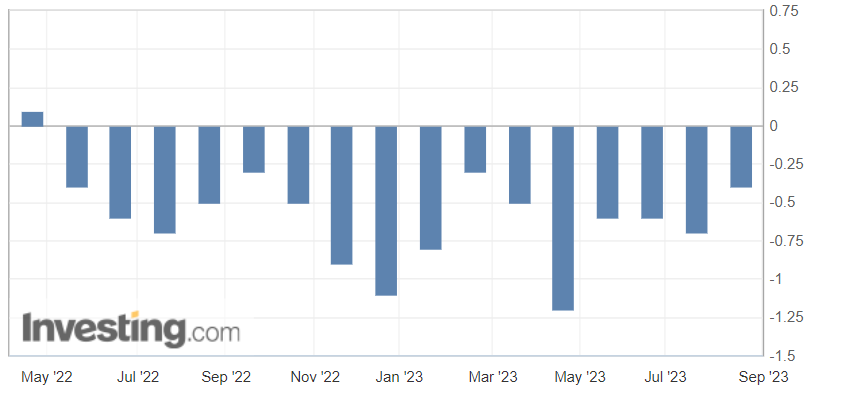

U.S. manufacturing output -0.7% pa – 5th straight minus:

Pic. 10

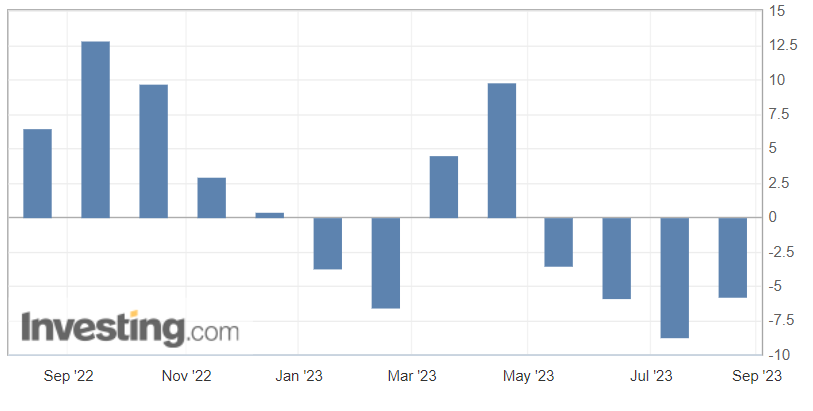

Net engineering orders in Japan -5.8% per year – the 4th negative in a row:

Pic. 11

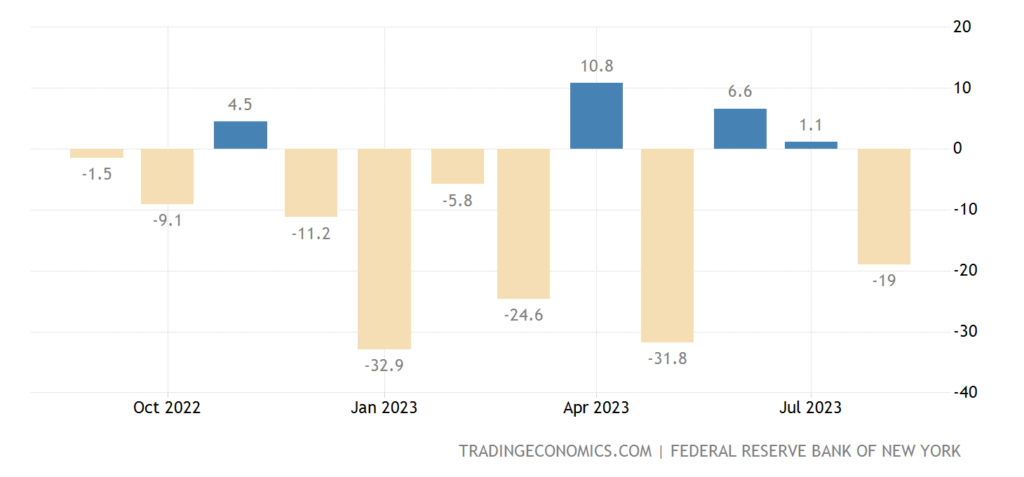

The New York Fed index again went far into the negative (-19):

Pic. 12

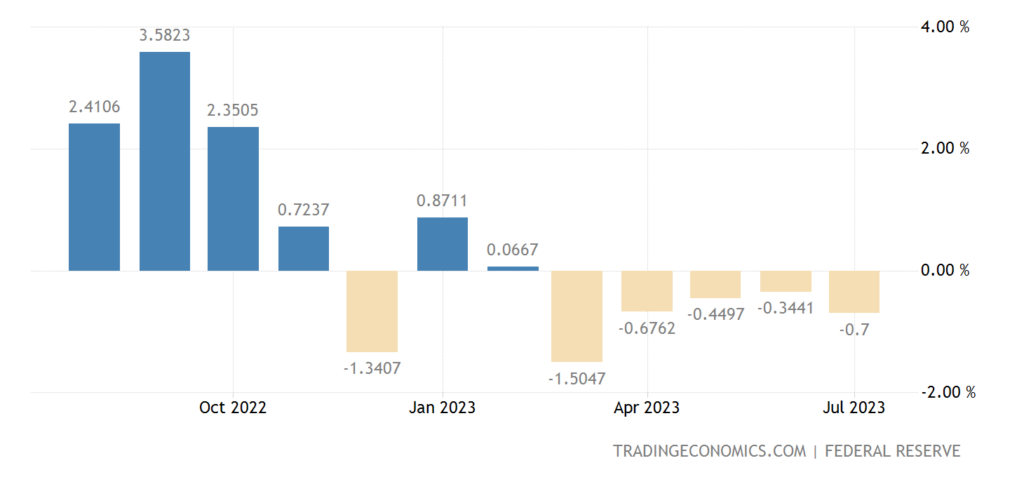

Index of leading indicators in the US -0.4% per month – the 16th negative in a row:

Pic. 13

The housing market index in the US began to deteriorate again:

Pic. 14

No wonder, in a situation where there is less and less free money (see the first section of the Review). Well, the 30-year mortgage rate in the US repeated the 22-year high last October (7.16%):

Pic. 15

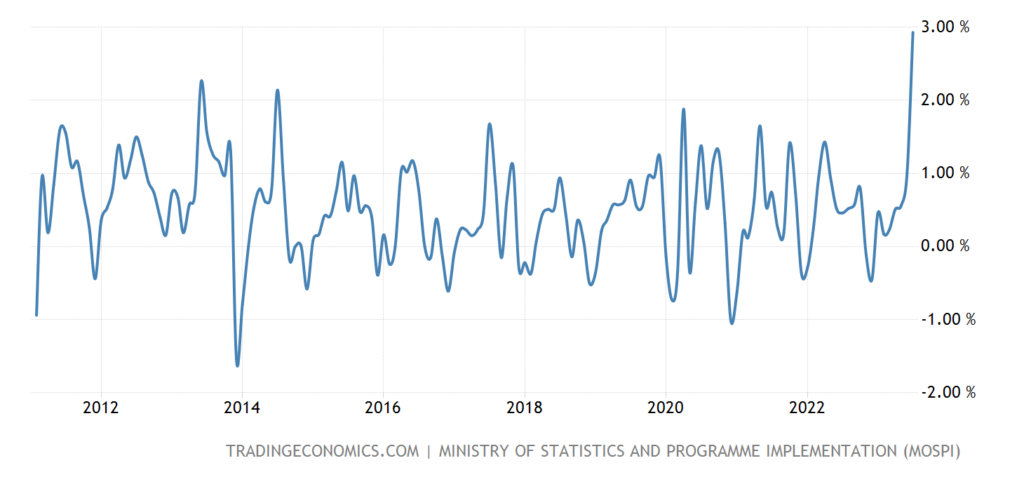

CPI (Consumer Inflation Index) of India +2.9% per month – a record for 12.5 years of observation:

Pic. 16

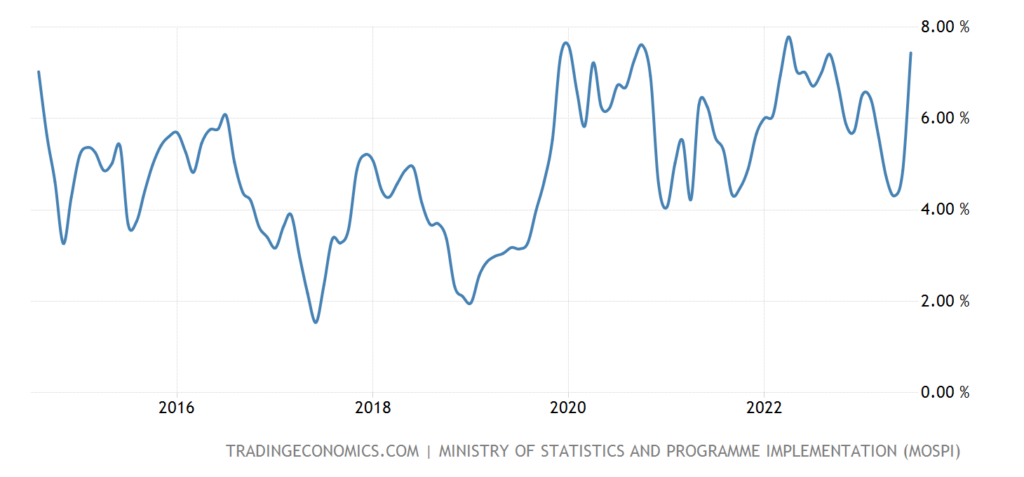

And +7.44% per year – the peak since April 2022; another 0.35% – and there will be a maximum from May 2014:

Pic. 17

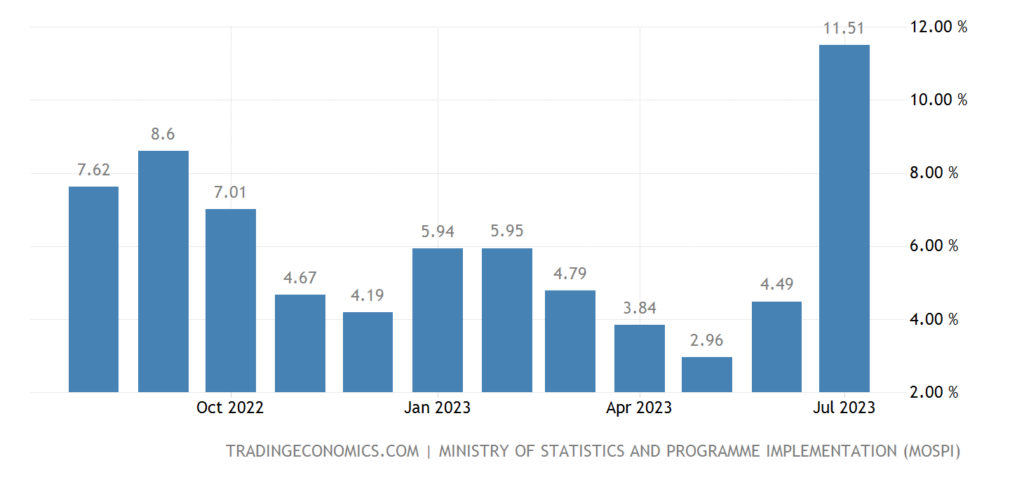

Food becomes more expensive at a faster pace (+11.5% per year):

Pic. 18

Japan’s CPI without food and fuel repeated a 42-year high of +4.3% per year:

Pic. 19

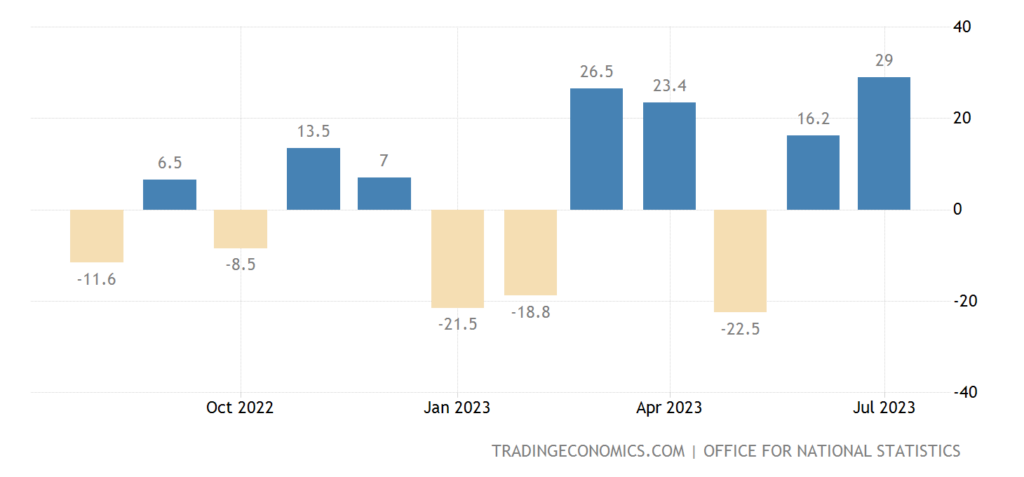

The number of registered unemployed in Britain continues to grow:

Pic. 20

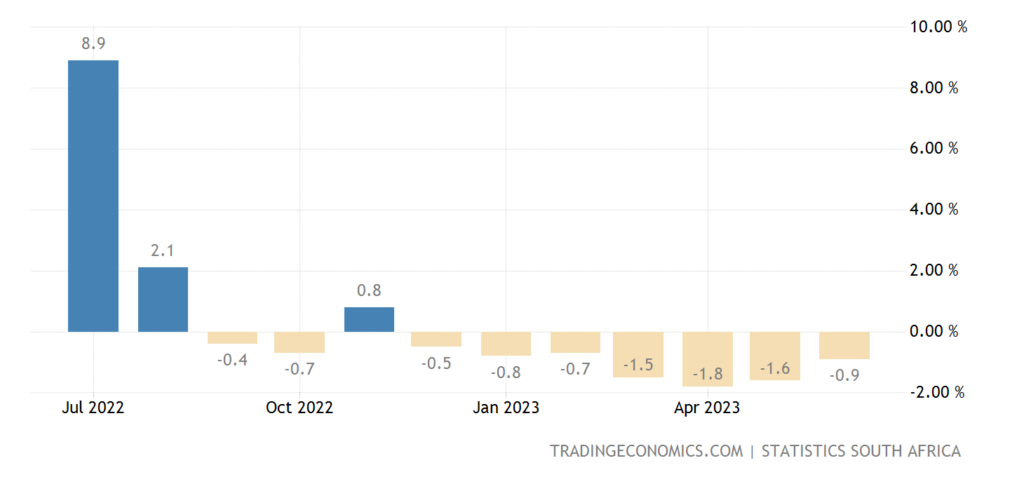

The volume of retail sales in South Africa -0.9% per year is the 7th negative in a row:

Pic. 21

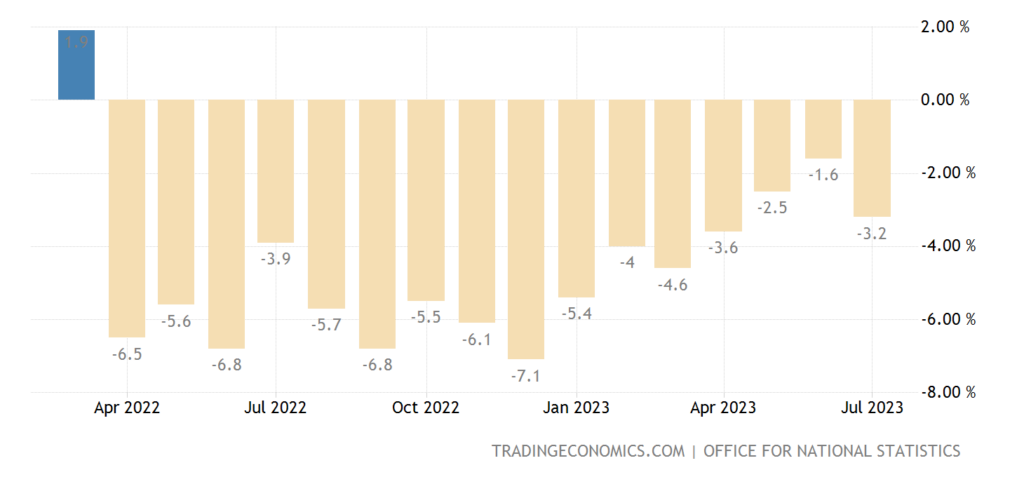

Retail UK -3.2% per year – the 16th negative in a row:

Pic. 22

Following the results of the 1st round of presidential elections, the Central Bank of Argentina at an emergency meeting raised the rate by 21% to 118%, a record for 30 years.

The Central Bank of New Zealand left monetary policy unchanged; but the Central Bank of China cut the rate by 0.15% to 2.50% amid the weakness of the economy and the financial system.

Main conclusions. From the point of view of the development of the crisis, everything is as usual. Structural decline in all its glory, the rate of decline is constant and practically does not change from month to month. But, unfortunately, the financial authorities of developed countries do not understand this.

The minutes of the last meeting of the US Federal Reserve have been released. Basic provisions:

- most officials still see inflationary risks, a potential need to raise rates;

- some officials fear that tightening financial conditions could lead to a sharper slowdown than expected;

- some officials see tighter bank lending conditions than expected;

- employees now do not expect a recession in 2023 and subdued economic growth in 2024-25;

- officials see an increase in unemployment, a slowdown in economic growth to achieve the target level of inflation;

- some officials believe that the decline in the value of commercial real estate damages banks and insurers;

- Officials will judge the next rate decisions by the “Bundle” of economic and inflation data;

- some officials see rising house prices as a sign that the sector’s reaction to the rate increase has reached its peak;

- several officials consider it necessary to take into account the risk of excessive tightening of financial conditions;

- inflation has slowed down since the middle of last year, but remains well above the target level of 2%;

- most Fed officials saw “significant” risks of rising inflation;

- inflationary risks may require further tightening.

By and large, the leadership of the Fed has clearly shown that it does not have a more or less intelligible picture of the events taking place. Actually, there is nothing particularly new in this, but since people refuse to believe that this can be so, one has to repeat it again and again. And, as you know, it looks much more convincing when the Fed leaders themselves speak about it.

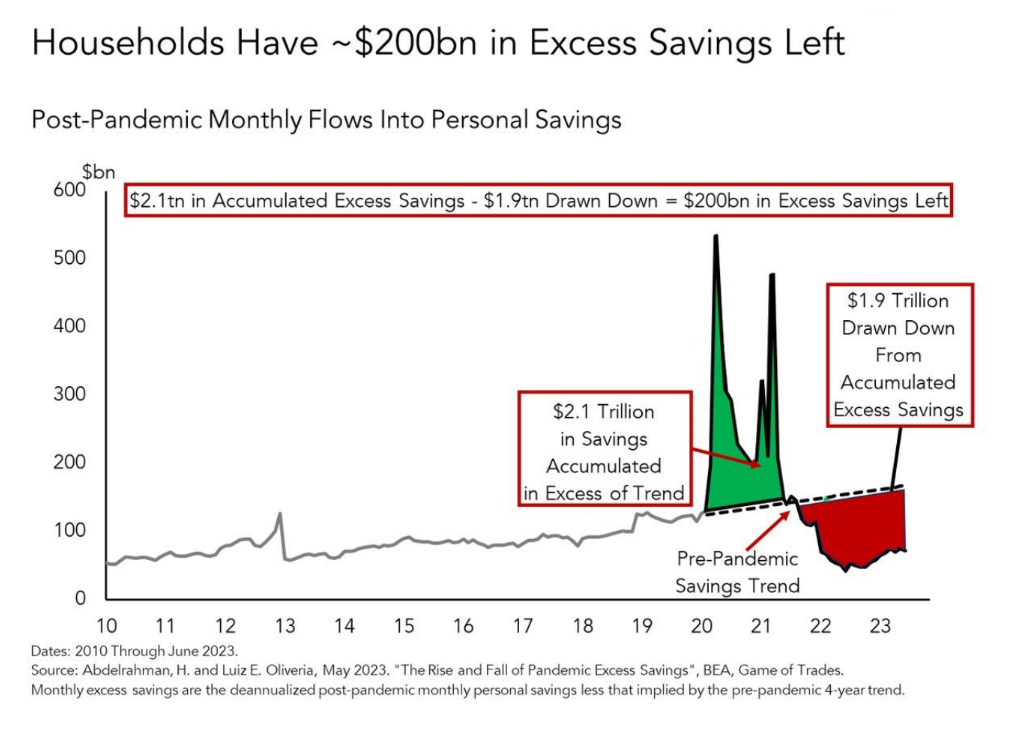

Well, as usual, a non-trivial picture.

The picture shows a graph of the growth in savings of American households relative to the average level of previous years. As you can see, during the covid period, savings grew, but over the past two years they have been falling. And the money accumulated during the quarantine period is almost over. With all the consequences.

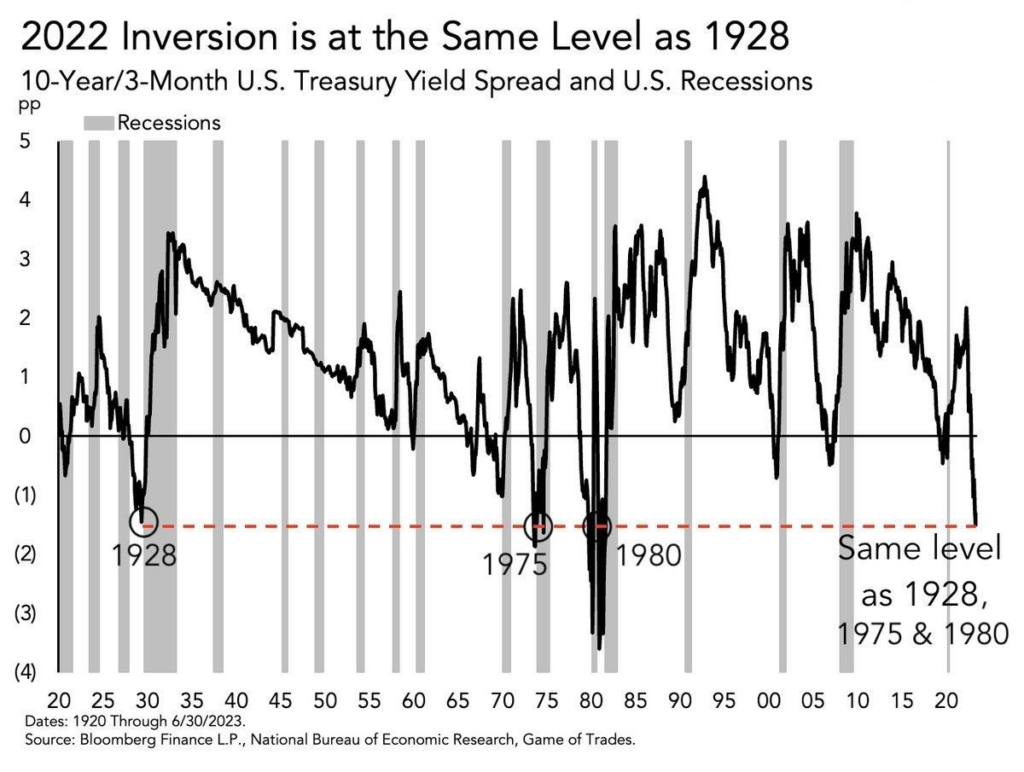

And one moment. The so-called “inversion” of government securities yields, in which short bonds are more profitable than long ones, usually indicates a crisis. In the picture below, in general, everything can be seen without comment.

However, there will still be enough for a couple of months, so our readers can safely go on vacation (or gradually get involved in work after the vacation), until the end of September, most likely, everything will be calm.