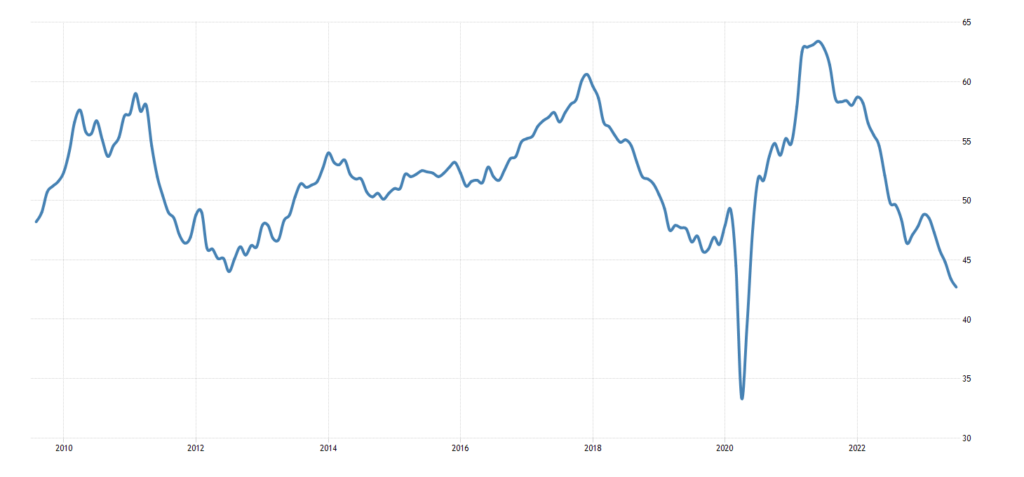

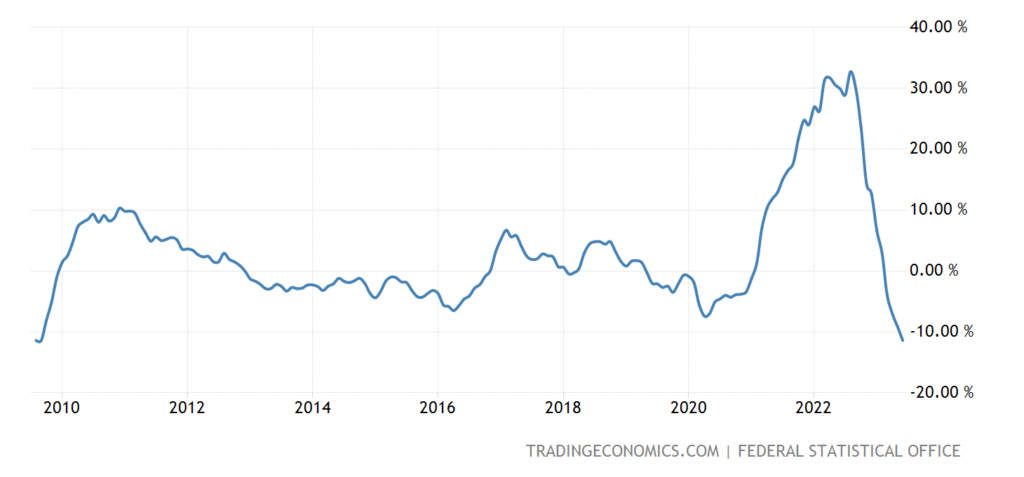

Big news. Of course, this is a reduction by the Fitch rating agency of the US rating from the highest possible AAA to AA +. Formally – due to the amount of debt and budget deficit, as well as “bad management” – https://tradingeconomics.com/united-states/rating . You can talk for a very long time about the real reasons for this phenomenon, debt, for example, has definitely grown a lot:

But it seems to us that such a decision by Fitch should be viewed from a completely different angle. The fact is that the discussion about which strategic path the American economy should take has been going on in the US elite for more than a month now. Yes, it is not public, but two basic directions (which M. Khazin first formulated on November 5, 2014 at the Dartmouth Conference in Dayton) have already been formulated quite clearly. Either reindustrialization on the AUCUS scale (at least), or the preservation of the Bretton Woods dollar model with the destruction of industry.

At the end of a year and a half of the SMO in Ukraine, it became clear that the United States needed new sales markets, without which it was impossible to raise the industry. It is for these markets that the battle between the US and China in Southeast Asia should begin (which many people have already spoken about, in particular, Henry Kissinger). The trouble is that the Biden administration refuses to make decisions. Well, or not able to.

In this situation, the split of the previously unified liberal (that is, those close to the transnational bankers, the “Western” global project) elites begins. Because some of them begin to understand that the second of the scenarios described above definitely leads to disaster. And there is reason to believe that Fitch’s actions are an attempt to warn the remaining slow-witted ones that decisions need to be made quickly.

If this version is correct, then we will soon see actions aimed at preparing for the US withdrawal from Western Europe and the Middle East. Yes, there are hints of such a development of events already now, but these are precisely the hints that require deciphering and interpretation. If we understand the situation correctly, the picture will seriously change in the very near future.

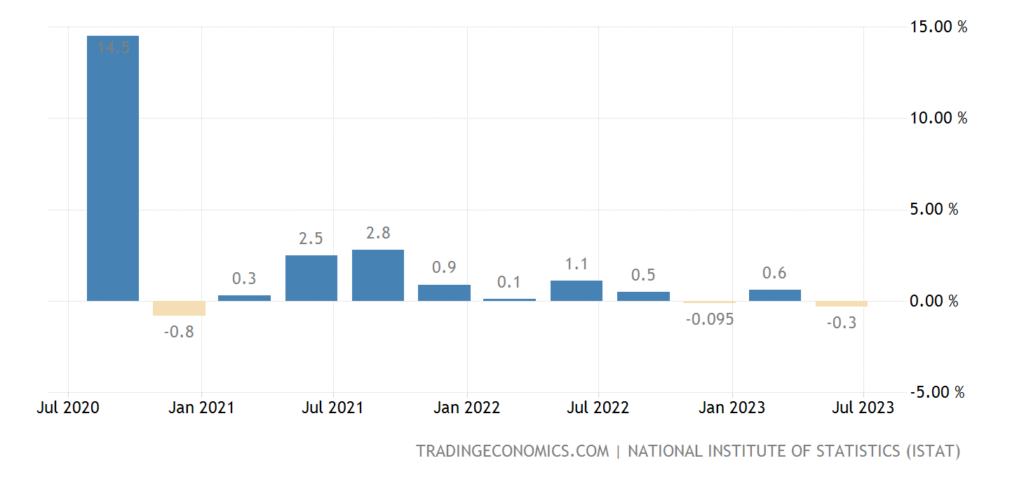

Macroeconomics. Italian GDP -0.3% per quarter:

Pic. 2

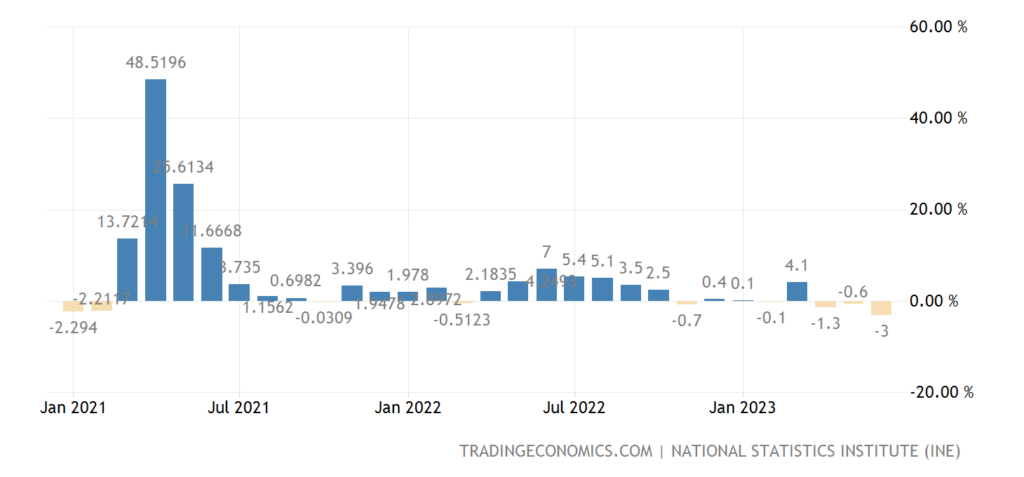

Industrial production in Spain -3.0% per year – the 3rd negative in a row and the worst dynamics in 2.5 years:

Pic. 3

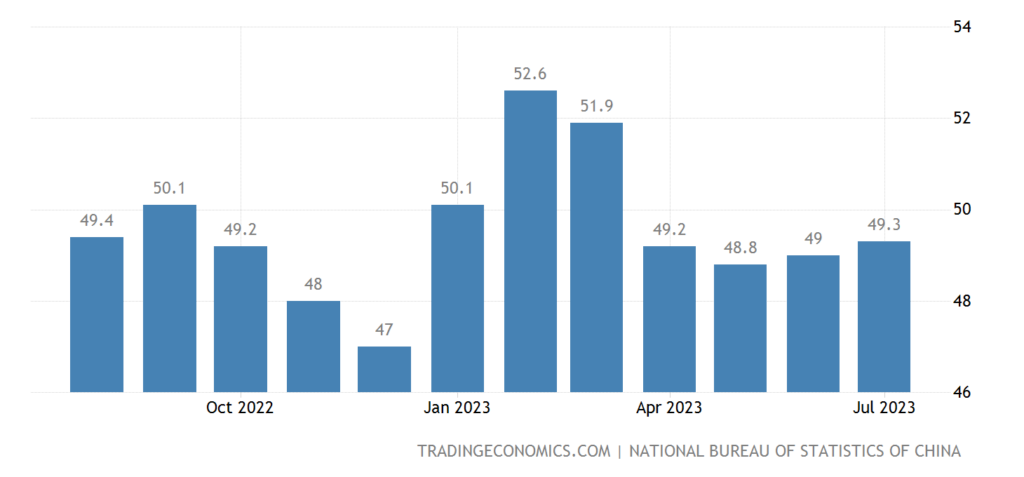

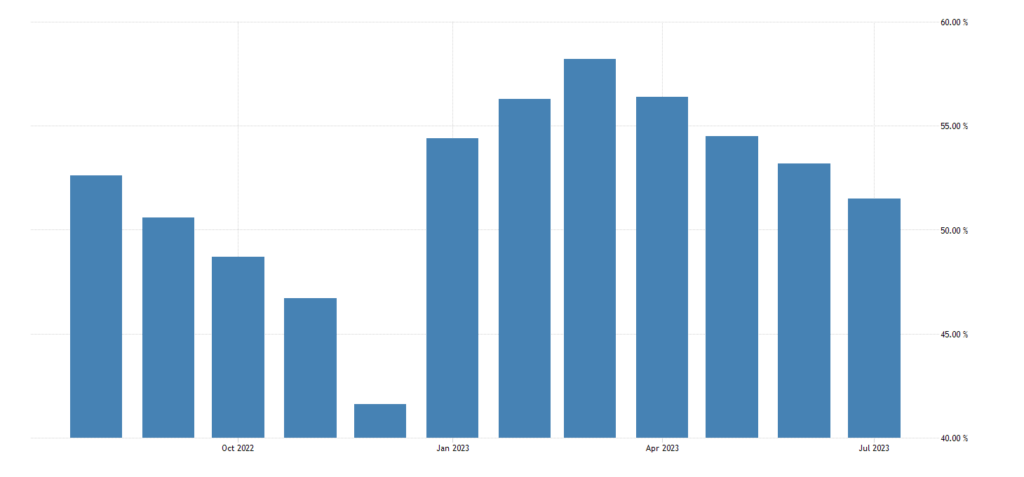

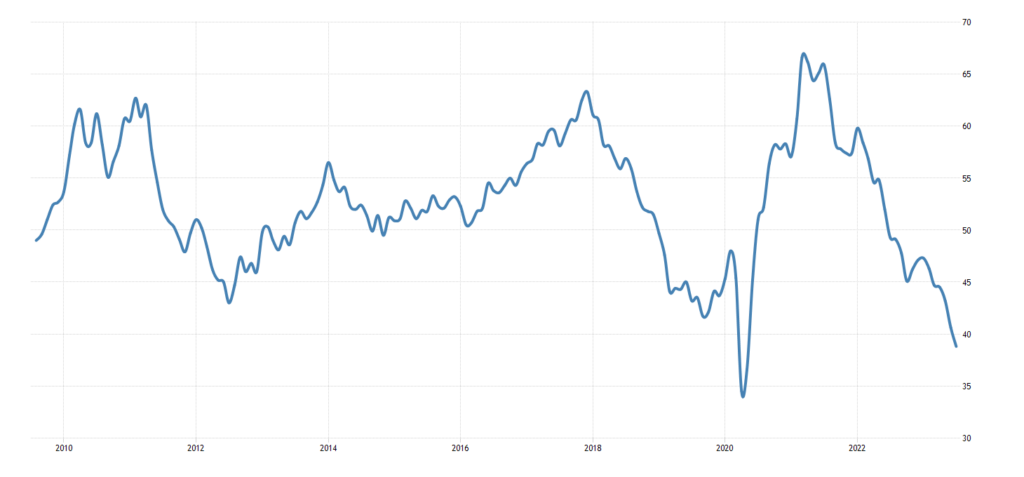

The official PMI (expert index of the state of the industry; its value below 50 means stagnation and decline) of China’s industry remains in the recession zone for 4 months in a row (49.3):

Pic. 4

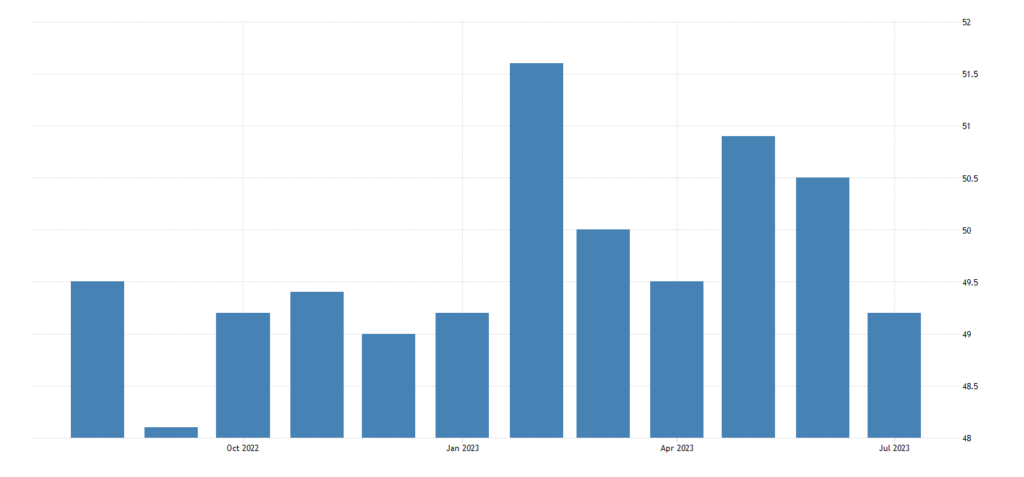

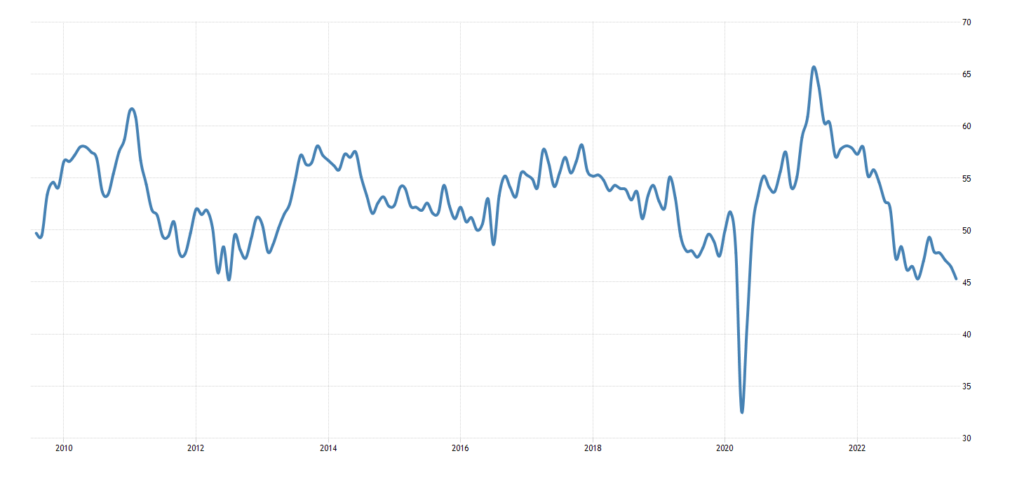

In other sectors, growth is still (51.3), but the weakest in 7 months; new orders and external sales fall for 3 consecutive months, and employment for 5 months:

Pic. 5

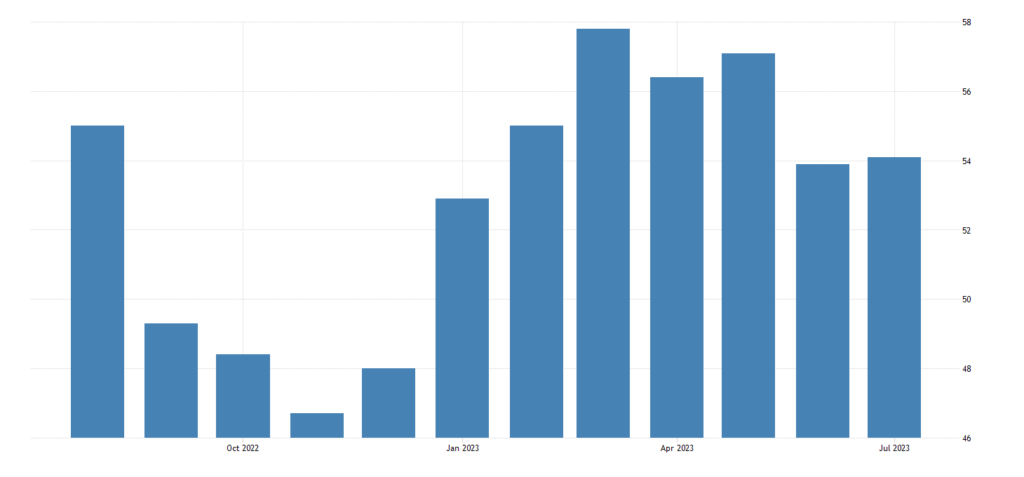

The same picture is painted by independent studies for manufacturing (49.2):

Pic. 6

But in the service sector, a mini-improvement (54.1), although still near a six-month low:

Pic. 7

Eurozone manufacturing PMI of 42.7 is a 3-year low, and excluding 2020, the bottom since 2009:

Pic. 8

Germany is especially weak (38.8), where the bottoms of 2009 and 2020 are already close

Pic. 9

Note that all experts drew attention to the increase in new orders in the industrial sector in June by 7%. The only trouble is that this is a rather volatile indicator, which does not reflect the general state of affairs. But by itself, without analysis, it looks beautiful.

Britain does not shine either (45.3):

Pic. 10

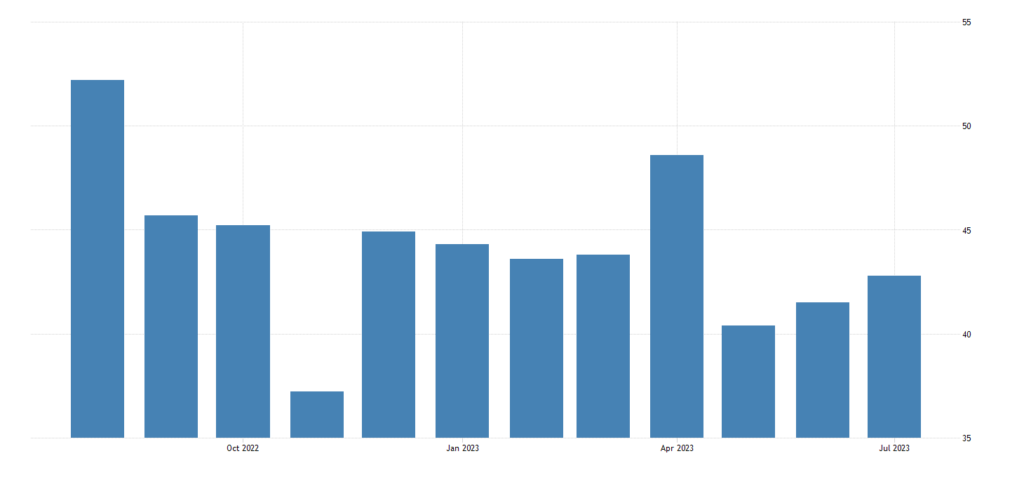

PMI Chicago keeps in the decline zone for 11 months in a row (42.8):

Pic. 11

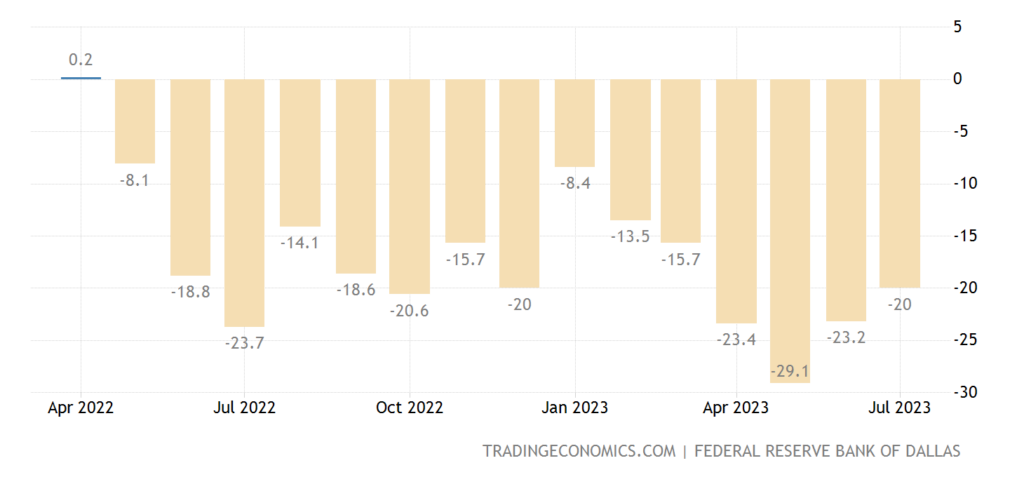

Texas Fed index in the red for 15 consecutive months:

Pic. 12

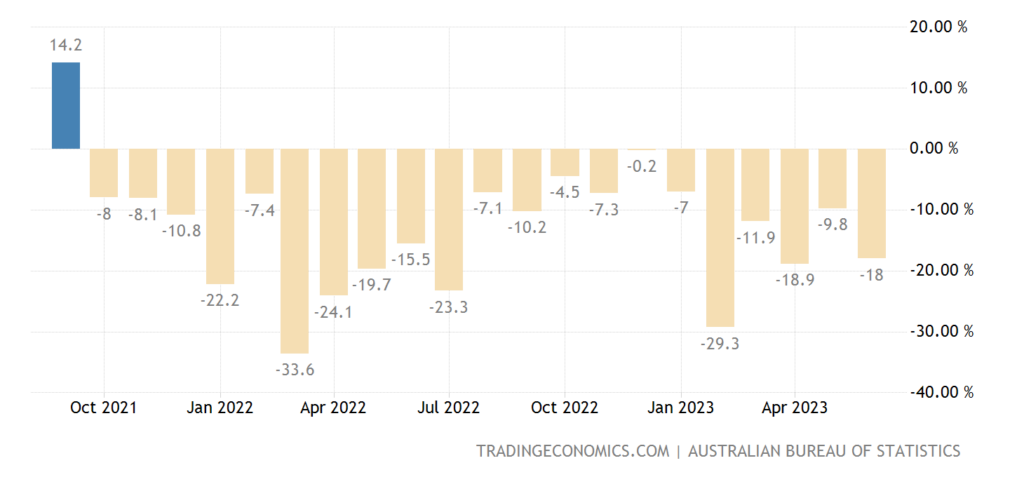

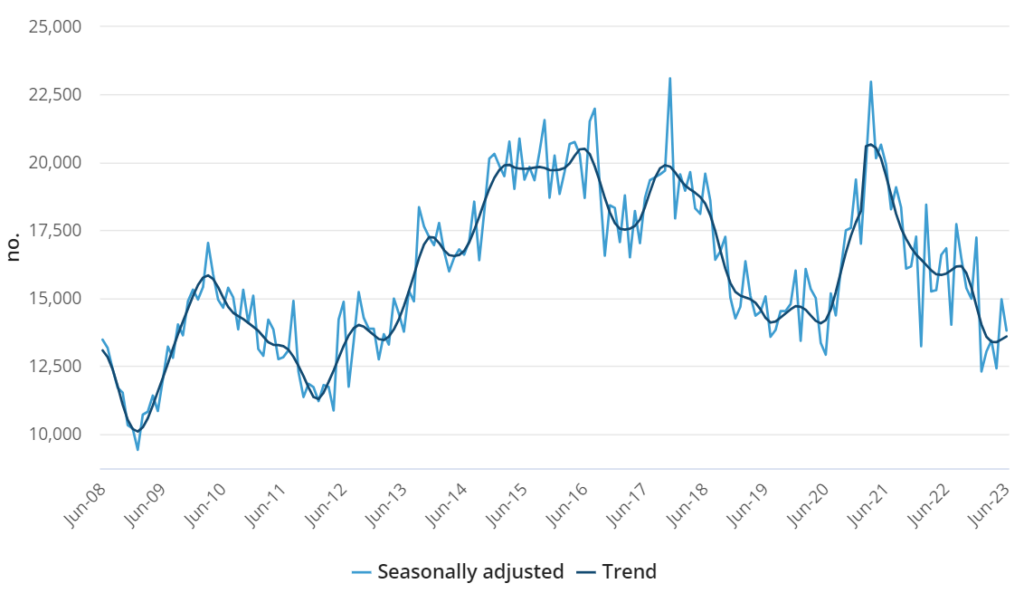

Building permits in Australia -18.0% per annum – 21st consecutive negative:

Pic. 13

And their level is approximately equal to the indicators of 2012/13:

Pic. 14

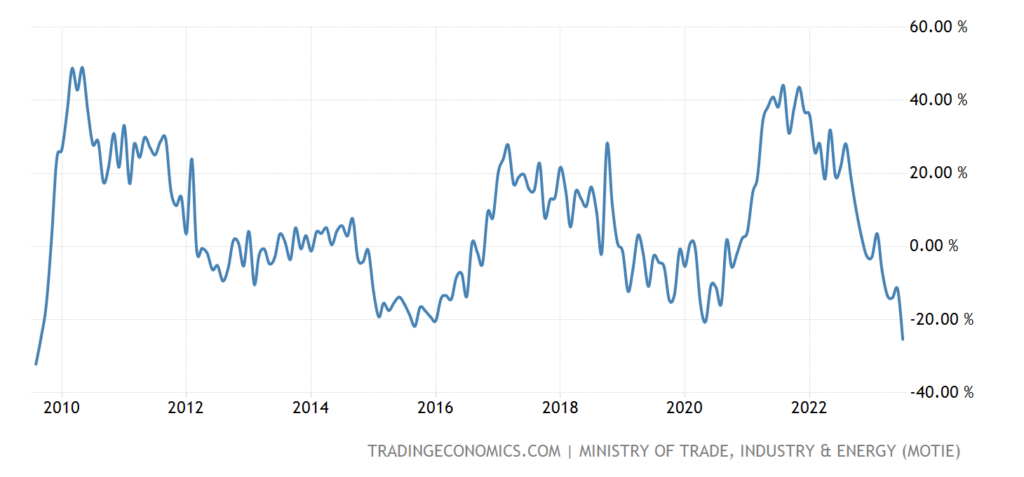

Imports of South Korea -25.4% per year – the worst dynamics since 2009:

Pic. 15

House prices in Britain -3.8% per year – the weakest indicator since 2009:

Pic. 16

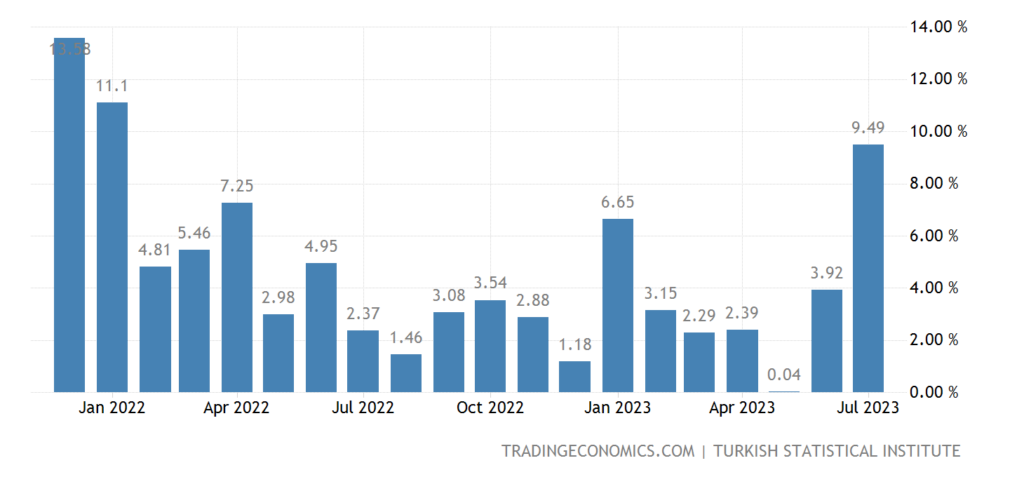

Turkey’s CPI (consumer inflation index) accelerated sharply to +9.5% per month – it was higher only twice, in December 2021 and January 2022:

Pic. 17

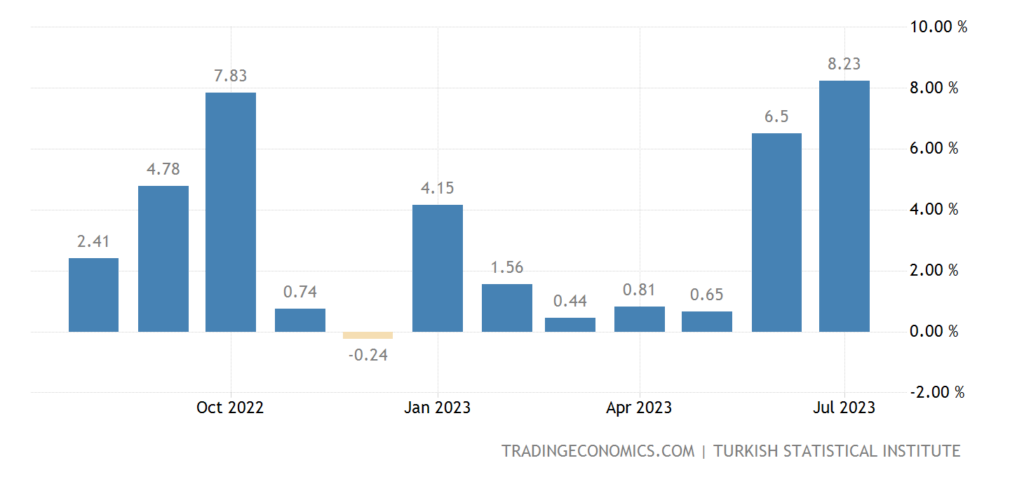

The PPI (industrial inflation index) of Turkey also clearly cheered up (+8.2% per month):

Pic. 18

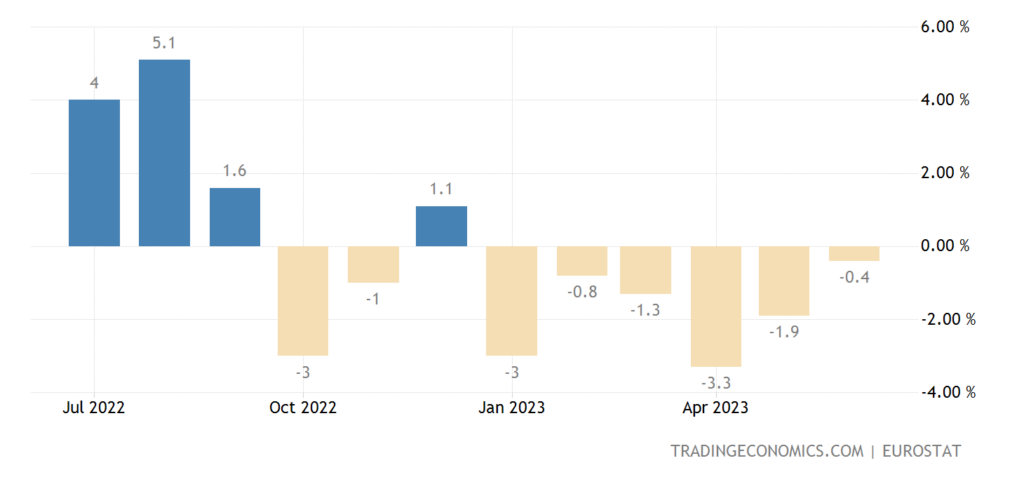

Eurozone PPI -0.4% m/m – 6th negative in a row:

Pic. 19

And -3.4% per year – 3-year minimum:

Pic. 20

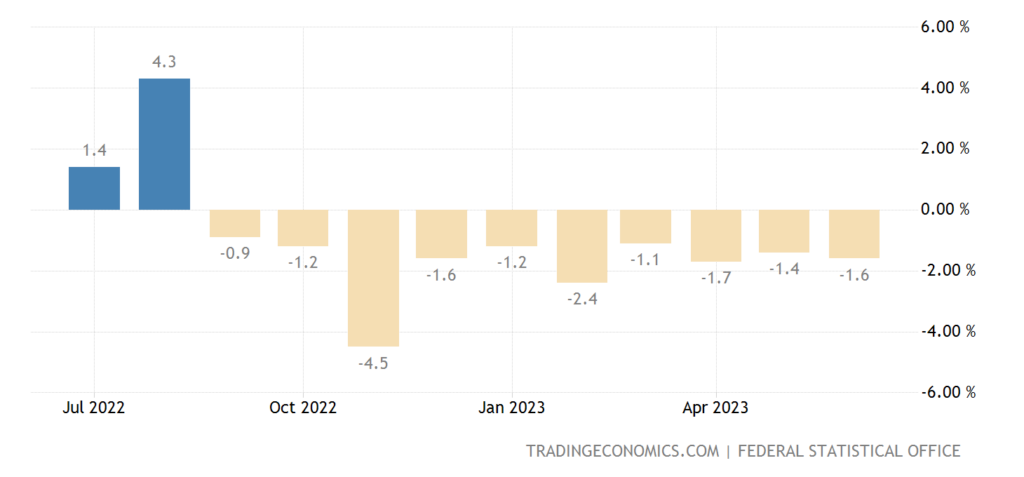

Import prices in Germany -1.6% per month – the 10th negative in a row:

Pic. 21

And -11.4% per year – next to the 36-year bottom from 2009 (-13.1%):

Pic. 22

The number of open vacancies in the United States is the lowest since April 2021:

Pic. 23

Here, however, the data say little about anything, the indicators of labor statistics in the United States are distorted especially strongly.

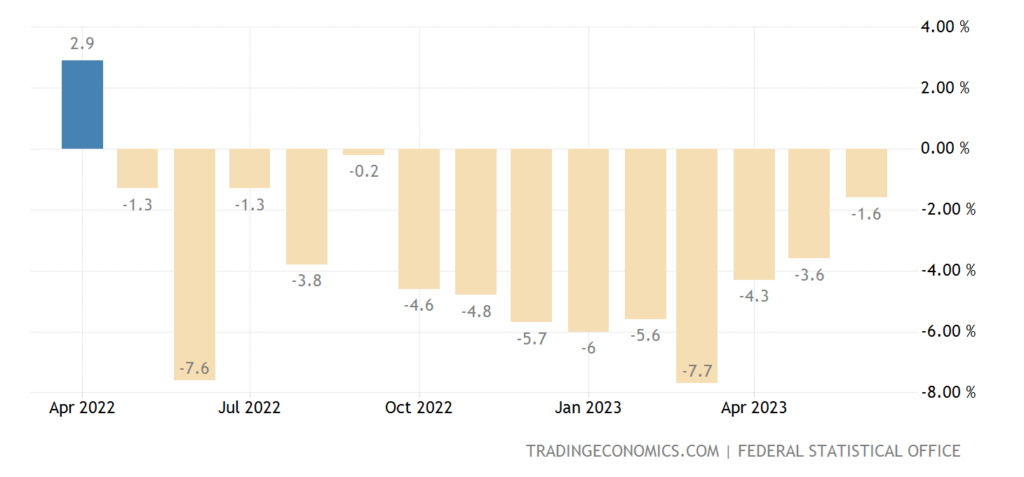

Retail Germany -1.6% y/y — 14th monthly loss in a row:

Pic. 24

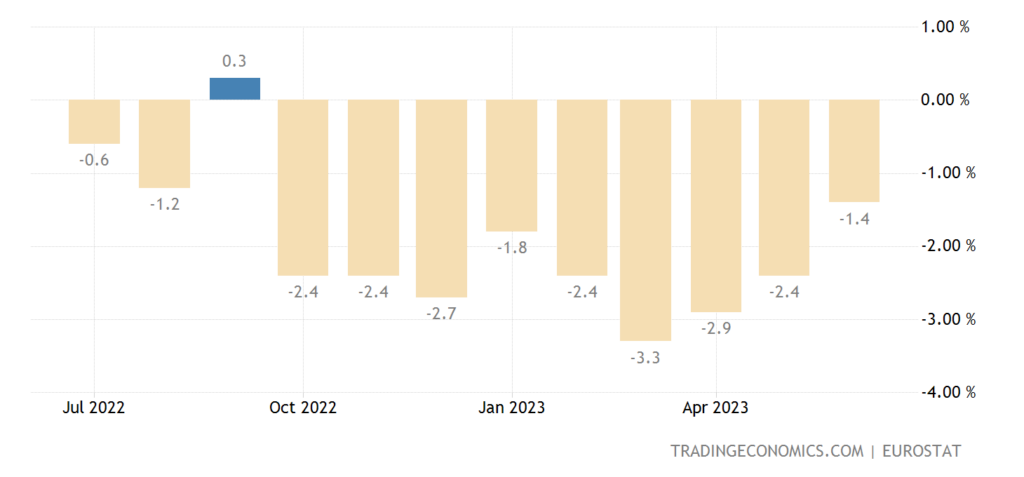

In the euro area as a whole -1.4% per year – the 9th negative in a row:

Pic. 25

The Bank of England raised interest rates by 0.25% to 5.25% (a 15-year high).

The Central Bank of Australia left rates unchanged despite the expectations of their increase, and the Central Bank of Brazil began to soften the policy altogether.

The structural crisis continues in all its glory. At the same time, problems are clearly visible in the industrial sector of the US and the EU (next week there will be information on inflation in July, let’s look at the result in the industrial sector), in which there is strong deflation. This cannot but worry the monetary authorities, but how to stimulate the industry is not very clear: the money immediately flows into the financial sector.

You can, of course, stimulate demand, but there are problems here: people prefer to buy cheap Chinese goods. They can be understood, but what should the authorities do? They have already actually canceled the WTO through the sanctions policy against Russia, now also cut off China from the world? And besides, this will lead to such a sharp decline in the standard of living of the population (in the US for sure) that the socio-political consequences will not be long in coming.

In general, the inability to make any specific decision (if you lower the rate, inflation will rise critically, if you raise it, the industry will fall even faster) creates a complete deadlock. And nothing can be done either, because the decline in the industry continues.

There are no good decisions, but since it is summer, we can endure another month, which we, in fact, are observing. So we wish our readers a pleasant weekend and a successful holiday. Most likely, there will be no economic excesses until September, unless they are caused by some political upheavals. And the latter are not within the scope of our competence!