Time period. 19-25 March 2022

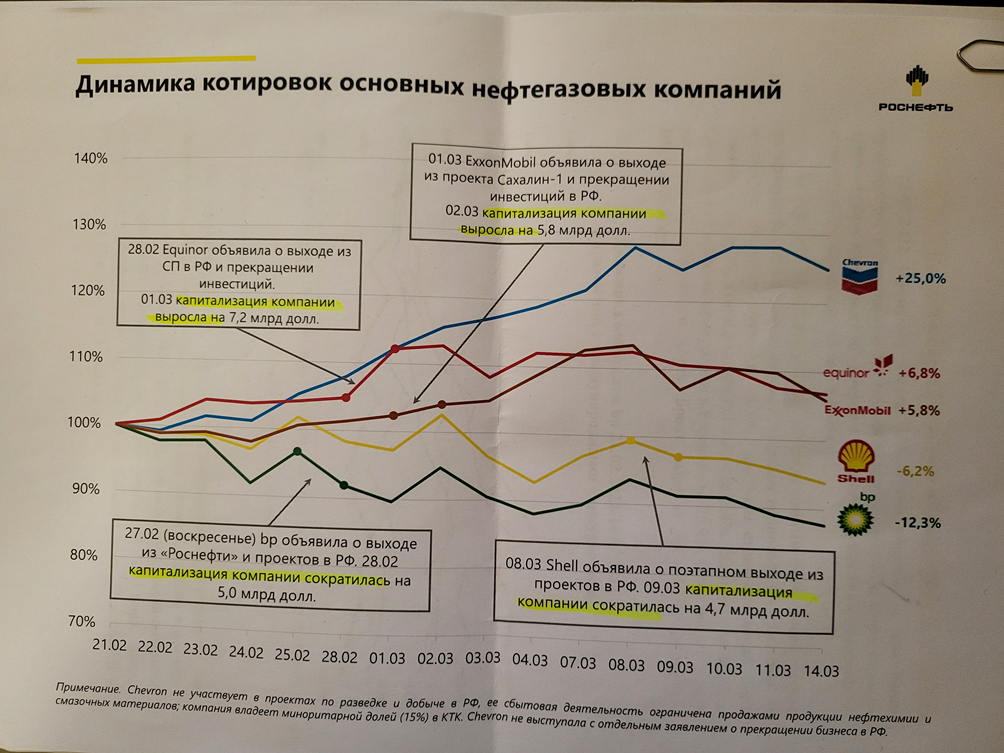

Top news story. The main news is, of course, the decision of Russian President Putin to sell a part of oil and gas resources for rubles. At the outset, it should be noted that from the formal accounting point of view, this decision does not carry a serious meaning – as a result of the transaction, buyers in any variant receive a product, and Russia – dollars or euros, changes only the procedure. However, the situation is more complicated. Firstly, this procedure has a serious psychological implication, as can be seen on the cost chart of the major oil companies immediately after this announcement (the chart was sent to the Khazin Foundation by a private reporter):

On February 27 (Sunday), bp announced its withdrawal from Rosneft and projects in Russia. On February 28, the company’s capitalization shrank by $5.0 billion.

On February 28, Equinor announced its withdrawal from the Russian Federation’s JV and the termination of investments. On March 1, capitalization of the companies increased by $7.2 billion

On March 1, ExxonMobile announced its withdrawal from the Sakhalin-1 project and the termination of investments in the Russian Federation. On March 2, the company’s capitalization increased by $5.8 billion

On March 8, Shell announced a step-by-step exit from projects in Russia. On March 9, the company’s capitalization shrank by $4.7 billion.

It is clear that the Chevron company, which is practically not involved in Russian projects, has kept its capitalization and even increased it against the background of the rise in oil prices, but all the others have clearly lost.

We will not assess the mechanisms of this psychological picture, as this remains outside the scope of the macroeconomic review. The second crucial factor is sanctions. The model proposed by Russia today does not suit the EU and the US, because in one form or another it forces to violate the restrictions they have accepted against Russia. Since these restrictions were imposed by the Western countries themselves, they can easily adapt them to Russian requirements, but such an action alone will make the treatment of all sanctions pressure much less serious. And not only in Russia, but all over the world: Saudi Arabia, by the way, also hints that it will trade its oil for the yuan.

There’s a third component that’s even more important, but it’s not tactical, it’s strategic. The fact of the matter is that the dollar’s power is not so much in that it is mainly making calculations in the world economy – the main thing is that pricing on the world markets is carried out exclusively in dollars, and if somewhere there will appear ruble oil markets, in theory, it opens the way to the fact that there may be a ruble oil exchange, the prices on which will be determined in rubles!

And that would be the biggest blow to the dollar’s hegemony! In theory, the US, the US Federal Reserve, as the regulator of the dollar, and the Bretton Woods institutions (the IMF and the World Bank and the WTO) should not allow this. However, the reality of recent years has fundamentally changed, and this directly shows that the Bretton Woods dollar system is in a severe crisis.

Separately, it should be noted that the actual withdrawal of Russia from the WTO (sanctions ban on the most favored nation treatment in trade with the United States), the seizure of its foreign exchange assets (in fact, the US default on its obligations to support the global dollar system) and attempts to ban companies from working with Russia poses issues, which have been raised by the Mikhail Khazin Foundation for Economic Research for many years. It is about the collapse of the model of legitimizing property within the Bretton Woods economic model.

We will not consider this issue in more detail here, it is clearly beyond the scope of the macroeconomic review, but it was impossible not to mention it, because the destruction of the property system automatically causes a complete failure of the entire economic system. And the Hazin Foundation plans to come back to this problem.

Macroeconomics

Orders for durable goods in the US -2.2% per month, this is the trough since April 2020:

Attention! These are February statistics (as well as some subsequent ones), a special military operation began in Ukraine only at the very end of the month.

Manufacturing PMI (an expert assessment of industry conditions; its value below 50 means stagnation and recession) of the Euro Area is the worst in 14 months –

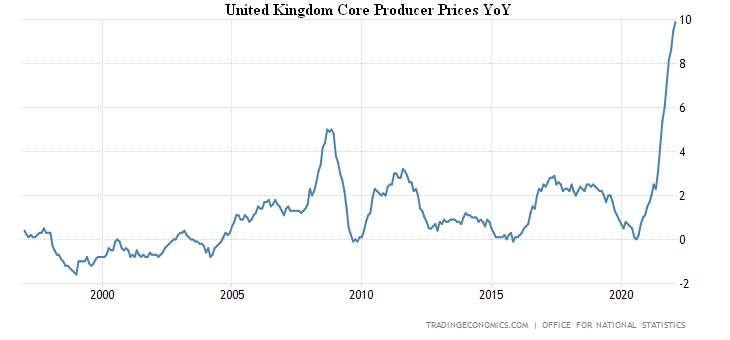

And for 17 months in Britain:

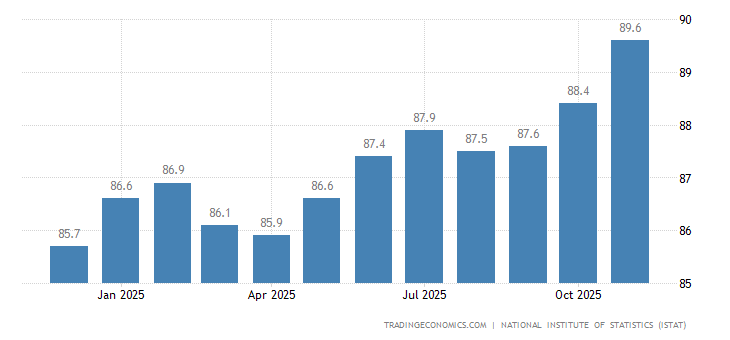

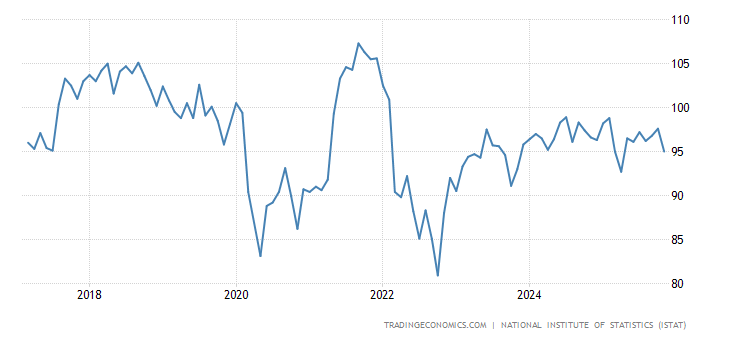

Business confidence in Italy is at the bottom for 11 months:

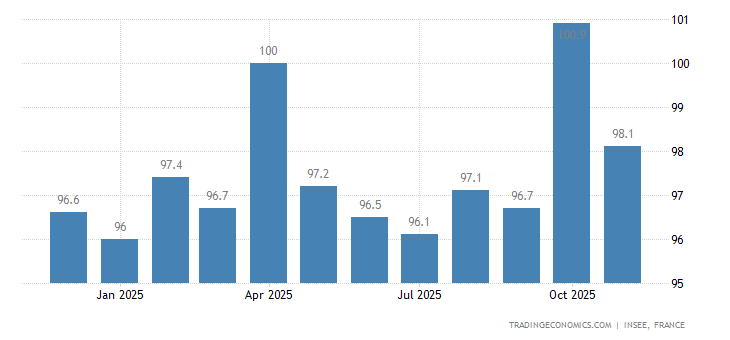

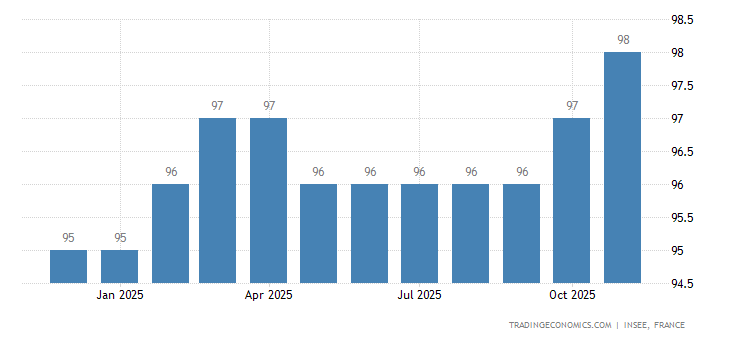

Business confidence and business climate in France are the weakest in a year:

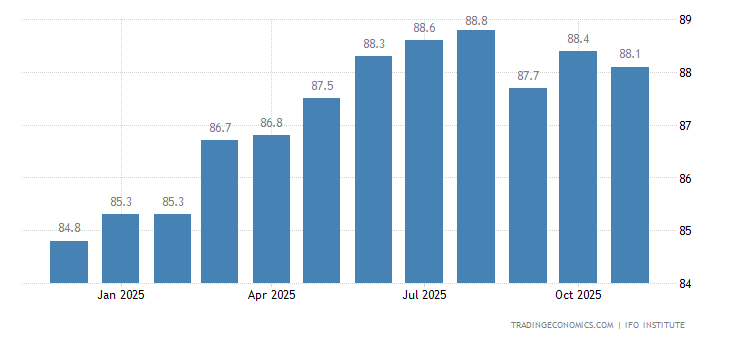

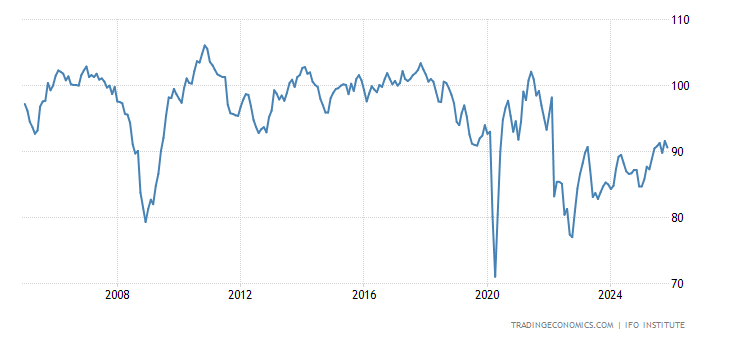

German business climate (IFO survey) is the worst in 14 months:

Including the Ifo Expectations Indicator:

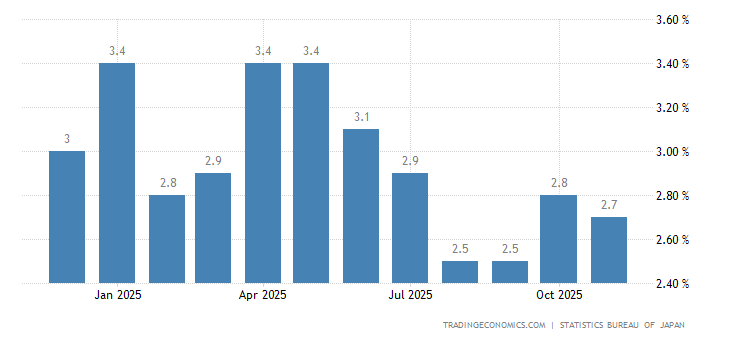

The CPI (Consumer Price Index) of the Tokyo Region peaked for 3 years (+1.3% per year), and energy prices for 41 years (+26.1%):

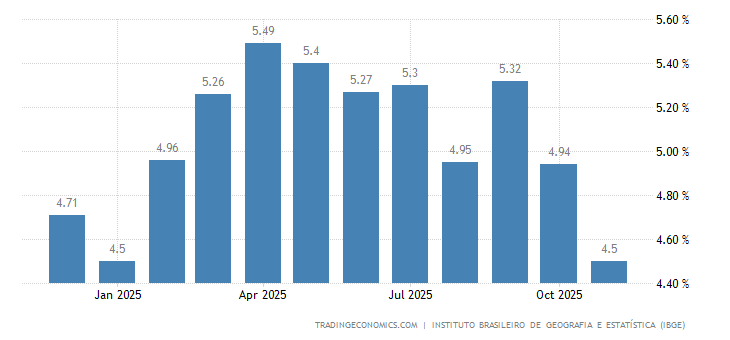

Brazil’s CPI is at its highest since early 2016 (+10.8% y/y):

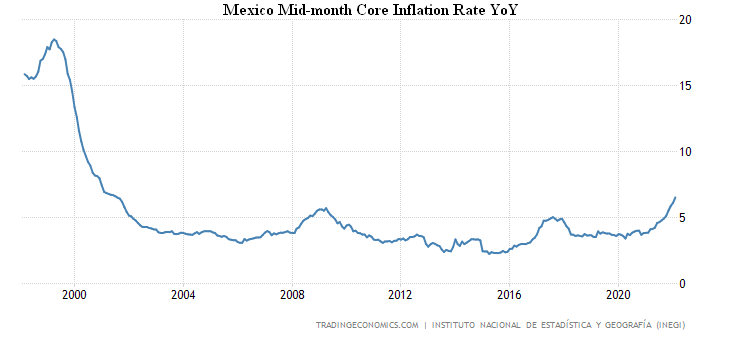

Mexico mid-month core inflation rate is the highest since 2001 (+6.7% per year):

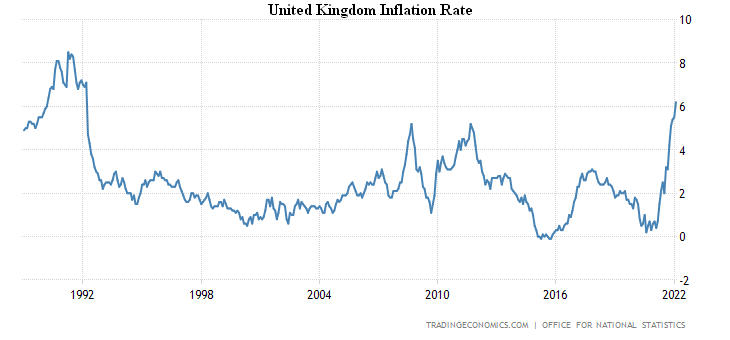

UK CPI +6.2% per year, the highest since 1992:

Less food, energy, alcohol and tobacco + 5.2%, which was a record for 25 years of survey:

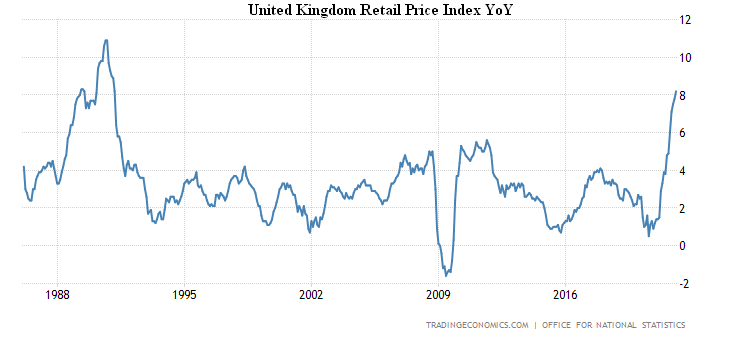

Retail Price Index (which reflects consumer concerns much better than CPI) +8.2% per year, the highest since 1991:

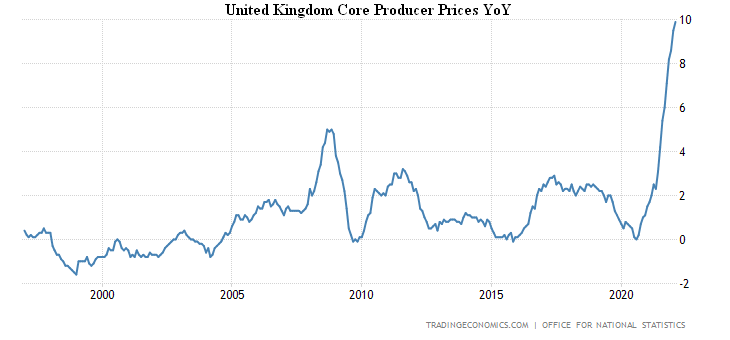

UK PPI (Producer Price Index) +10.1% per year, the highest since 2008:

Excluding food, energy, alcohol and tobacco + 9.9%, which is a record for 25 years of survey:

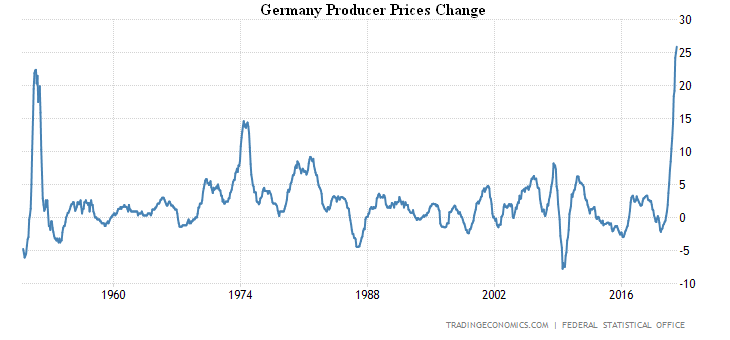

PPI Germany +25.9% per year, which was a record for 72 years of observations:

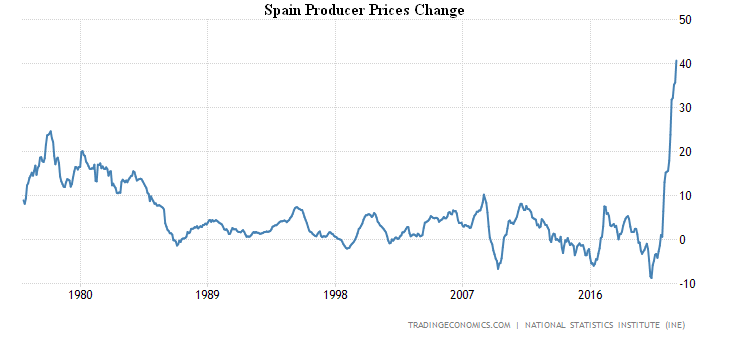

PPI Spain +40.7% per year, a record for 46 years of statistics:

We note that the price growth rate has increased over the past month. It is likely that this is due to Russia’s special operation in Ukraine, but this still needs to be verified.

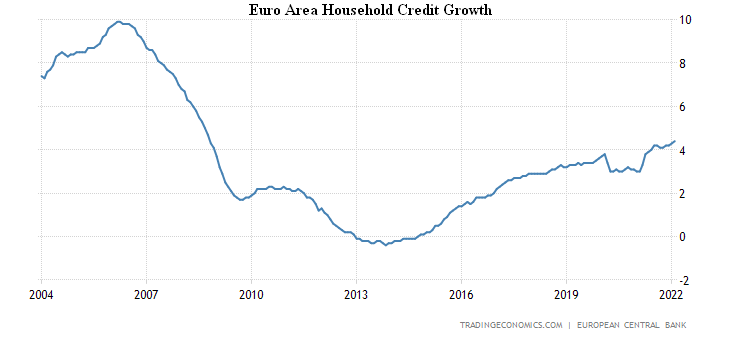

The growth rate of credit to the Euro Area households is the fastest since 2008 (+4.4% per year):

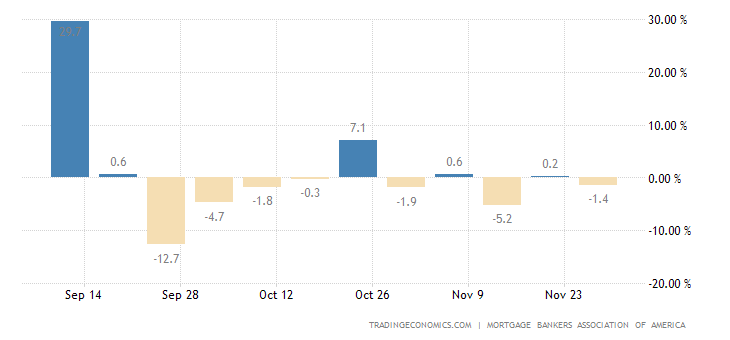

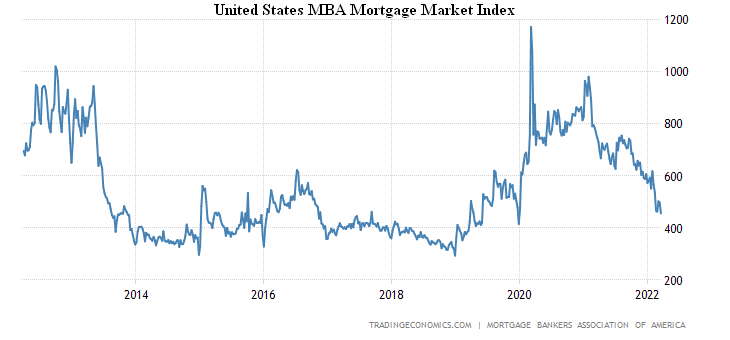

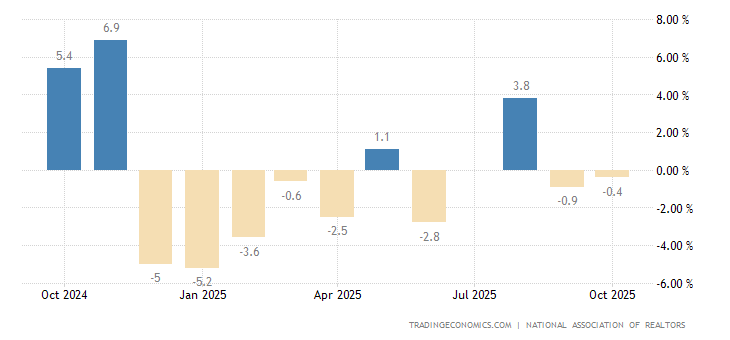

Mortgage applications in the US were -8.1% per week:

They’ve been down to their lowest since late 2019:

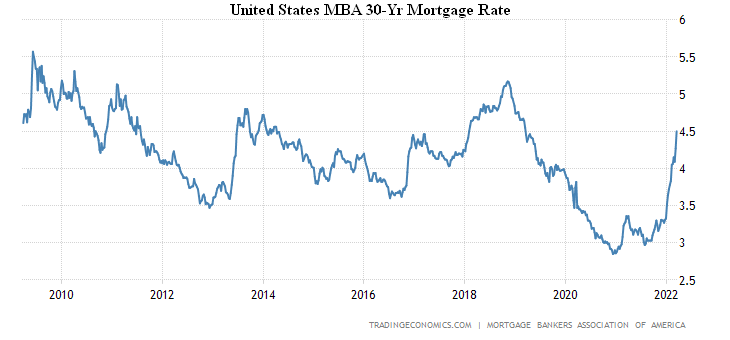

Because the mortgage rate is at its peak since 2018:

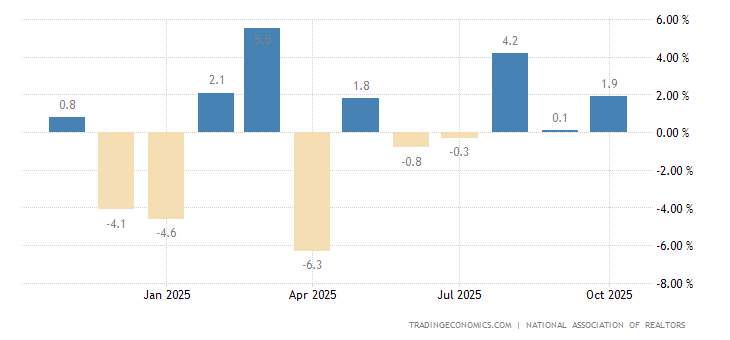

US new home sales -2.0% m/m after previous -8.4% due to skyrocketing prices (+10.7% y/y median, +25.4% avg):

U.S. existing home sales pending -4.1% m/m, 4th straight loss:

And -5.4% per year, 9th time in a row in the red:

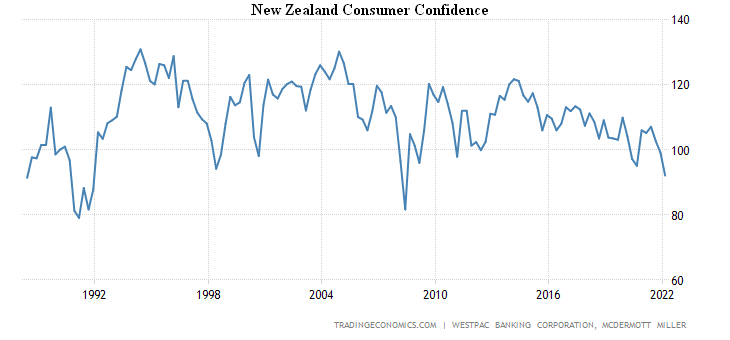

New Zealand consumer sentiment is at its worst since 2008:

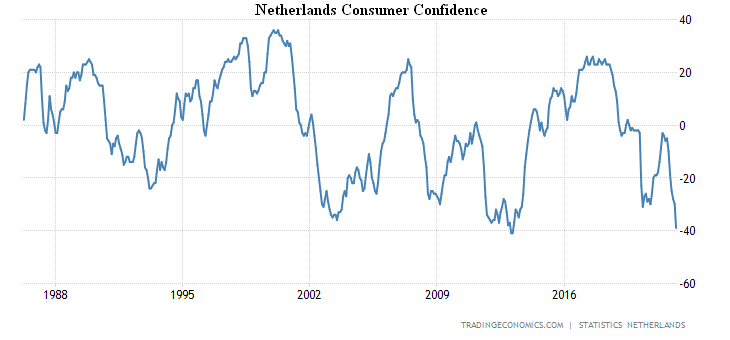

And the Dutch have the gloomiest since 2013 and very close to the global anti-record:

Italians are extremely gloomy in 14 months:

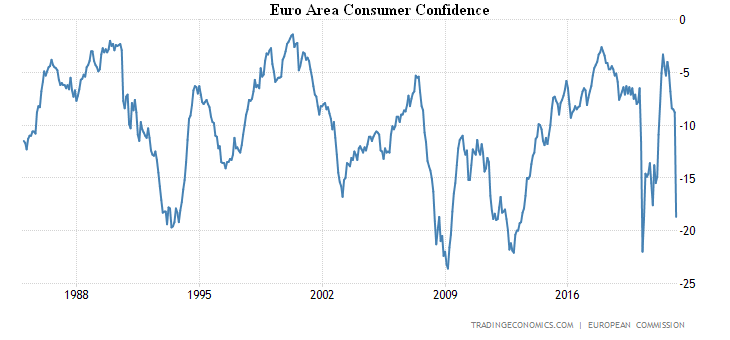

In the Eurozone, the trough for 2 years:

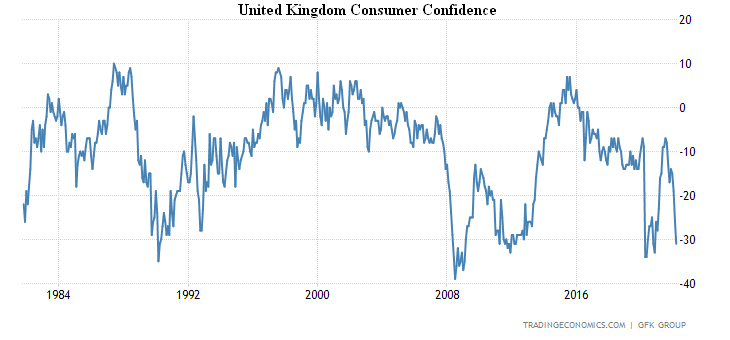

In Britain, it’s 16 months, and those numbers are 80% likely to portend a recession:

Note that the use of the term “recession” here is not entirely appropriate, see the next section of this Review.

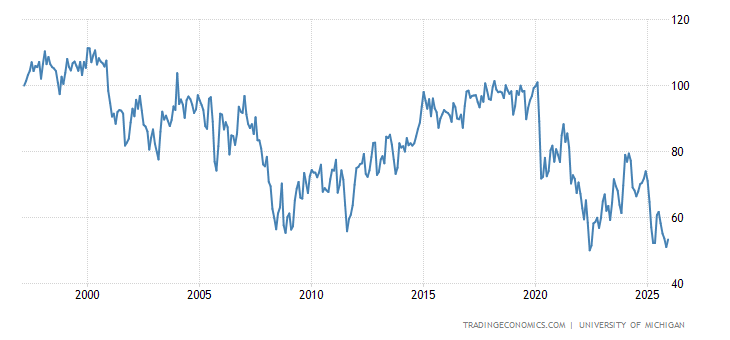

Consumers in the US have been extremely pessimistic since 2011:

And the current economic conditions are from 2009:

Inflation expectations (+5.4%) peaked since 1981:

UK retail balance is getting weaker –

And the retail falls. As a whole (-0.3%):

And excluding fuel:

The Chinese Central Bank left monetary policy unchanged, but may soften it in April. The South African Central Bank raised the rate by 0.25% to 4.25%. The Central Bank of Mexico raised the rate by 0.5% to 6.5%.

Summary. Fed board members (including Powell) have signalled that they are ready to tighten policy more quickly, and may raise the rate by 0.50% at the next meeting in early May. This is understandable, because inflation is rising, its negative effects are sweeping the economy, and the Fed has to take action – the problem is that it is not clear exactly what.

The increase in the rate in the current situation, as the experience of the end of last year showed, does not have much effect, and readers of our reviews understand this, its structural component only increases from an increase in the rate, since the higher the cost of the credit, the higher the pace of the structural crisis, that is, the degenerative changes in economics. But the theory used by the Fed’s leadership and the rhetoric it has been pursuing for decades has no place for the notion of “structural crisis”. The Fed insists that inflation must be regulated through rate changes, and for this reason it has to do so even in a situation where many of its leaders realize that this is pointless.

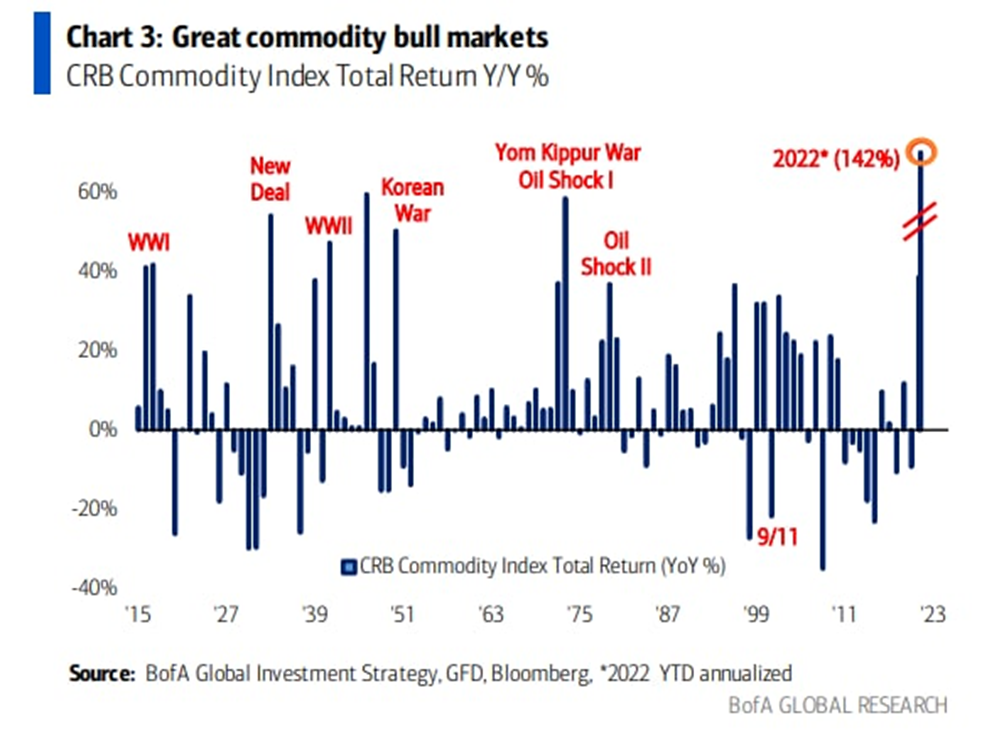

If the rate of price growth were somewhat lower, the situation could be prolonged, but the elections in November of this year, the rise in the price of gasoline and diesel fuel, the threats to destroy some world markets force the Fed’s leadership to demonstrate “violent activity”. As a consequence, they might be happy to refrain from raising the rate, but they can’t do this. Thus, households, governments, and corporations must be prepared to substantially increase the cost of servicing previously accumulated debts. In other words, a full-fledged structural crisis has unfolded in the world, as can be clearly seen on the graph of the overall change in resource prices:

As we can see, the current crisis has become the largest in more than 100 years, which is understandable: the fourth Crisis of capital effectiveness (see M. Khazin, “Reminiscences about the future”), which, unlike the first two, follows the inflation scenario. It is not without reason that a similar (though smaller) growth was in the 1970s, when the third Crisis of capital effectiveness took place, which was overcome by the policy of Reaganomics.

Let’s look at the yield of 5-year bonds of Germany:

This shows the strain on the public debt of this (relatively prosperous, against a general background) country. And these negative processes will continue as the outcome of the structural crisis will align household income and expenditure (balance), which in the current conditions of the economy is possible only after a fall in expenditures (that is, a decrease in welfare) about twice.

It is precisely because of the long-term and structural nature of the crisis that it is totally unacceptable to use the notion “recession” to assess it. It implicitly assumes the cyclical nature of the crisis, and cyclical downturns are always limited in time. In our case, this is not applicable, the structural crisis can last for a long time (in our case, if not slowed down, about 5 years). The problem is that attempts by official statisticians to give voters a more pleasant picture cause statistical indicators to be highly distorted, for example, by underestimating inflation.

In our reviews we try to identify the contradictions in these distortions and to make a more or less objective assessment, but it must be understood that these are just assessments. The models of the Mikhail Khazin Economic Research Foundation provide a more accurate picture, and we regularly publish the results on the Foundation’s website. But still, we have to warn our readers that they will increasingly face the discrepancy in their work between the official and real conditions of the economy.

We wish a constructive working week to all our readers!