August 5-11, 2023

Big news. After Fitch downgraded the US rating, Moody’s downgraded 10 small and medium-sized US banks and threatened to downgrade several large ones: https://www.reuters.com/markets/us/moodys-downgrades-10-us -banks-warns-possible-cuts-others-2023-08-08/ . As is clear, the point here is not in the specific names of specific banks, but in principle, but all this is no longer the main news. And the main one is the continuation of deflation in the US industrial sector:

And although the decline in prices was not as strong as in June (-7.0% versus -9.4%), however, it is clear and unconditional. And this is a sure sign of a serious recession in the industrial sector.

Note that the industrial inflation index PPI is fundamentally different from the one given above, since it considers only prices at the end of production chains. It is much higher (0.3% for July against the forecast of 0.2% and the indicator for June of 0.1%). In fact, this difference means that the demand for intermediate manufactured goods in the US is falling.

There may be several reasons. It may turn out that foreign components are cheaper, and American manufacturers are switching to imports. Maybe the producers of the final products are guided by the sales prices to consumers and are trying to compete with banks and trading companies for potential profit. Finally, it may be that the overall scale of profits drops significantly and competition is already taking place within the technological chain. Here, too, the influence of the banking sector speaks its word (some lend on more favorable terms than others).

In general, there may be several reasons, perhaps the situation is different in different industries, but the most important conclusion is that in general, there are very serious problems in the US industrial sector. And they’ve been going on for several months. And there can be no question of any process of reindustrialization in such a situation.

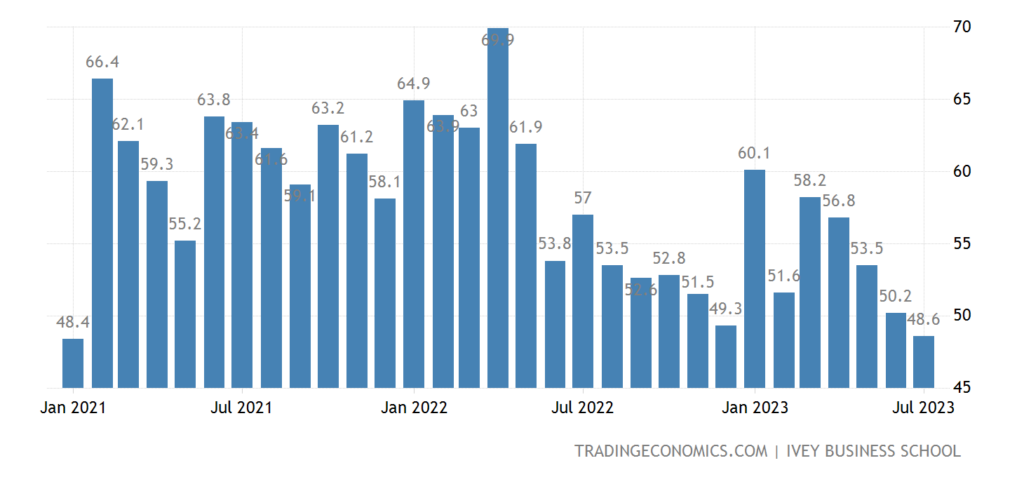

Macroeconomics. PMI (expert index of the state of the industry; its value below 50 means stagnation and recession) of Canada at the bottom for 2.5 years and in the recession zone (48.6):

Рис. 2

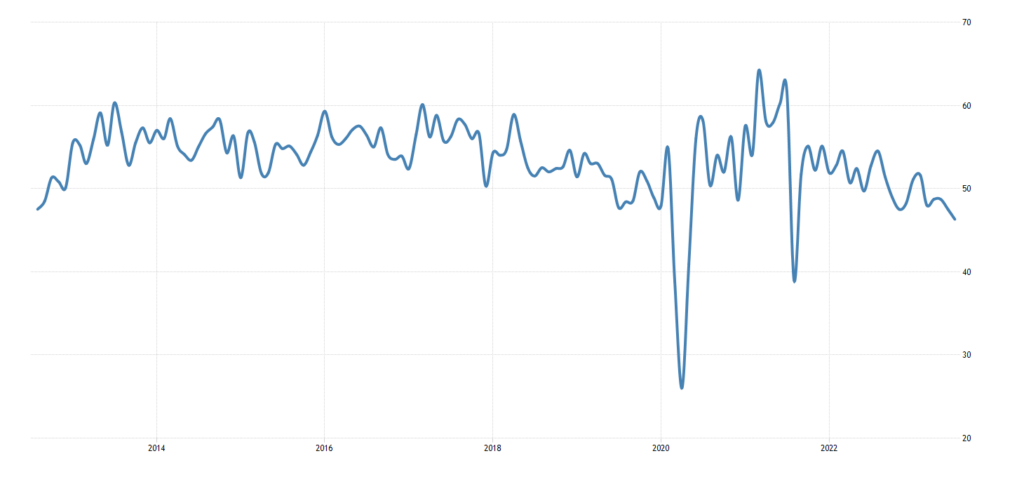

In New Zealand for at least 2 years, and excluding covid failures – for 11 years:

Рис. 3

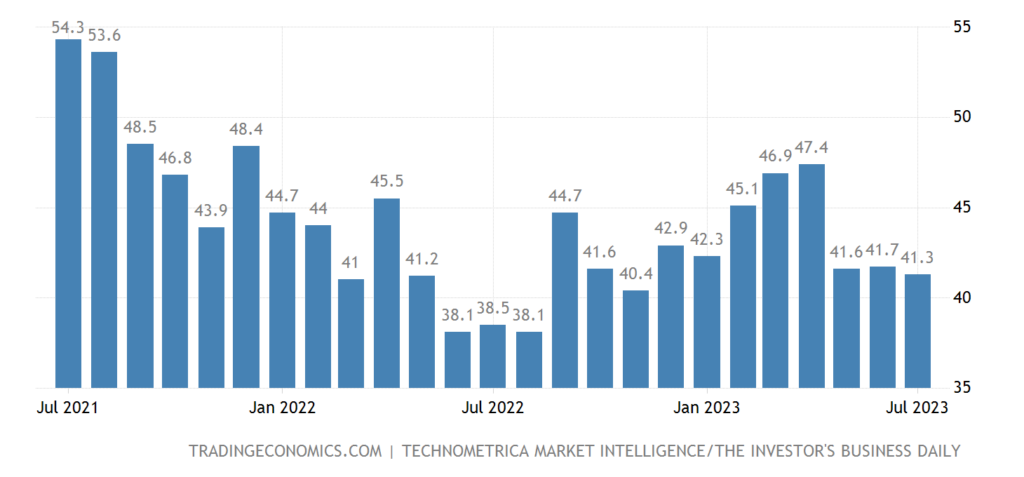

The index of economic optimism in the US is the worst in a year, has been in the recession zone for 24 months in a row:

Рис. 4

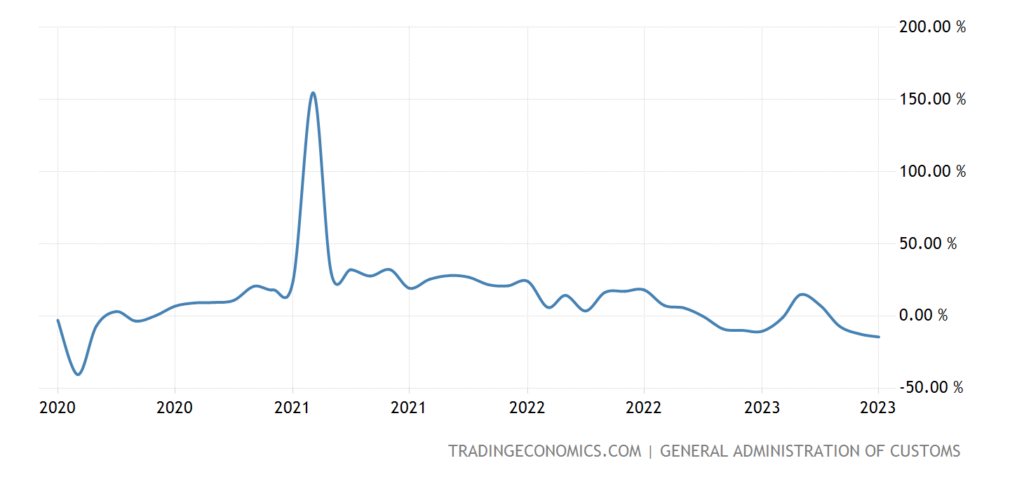

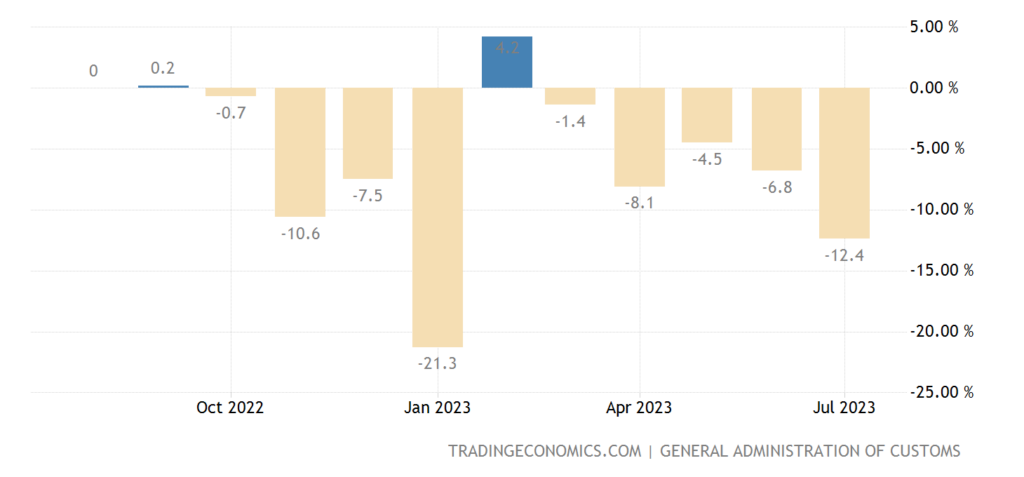

Export from China -14.5% per year – the worst dynamics in 3.5 years:

Рис. 5

Import -12.4% per year:

Рис. 6

If this is not a serious recession in the economy, then I don’t even know what to call a recession then …

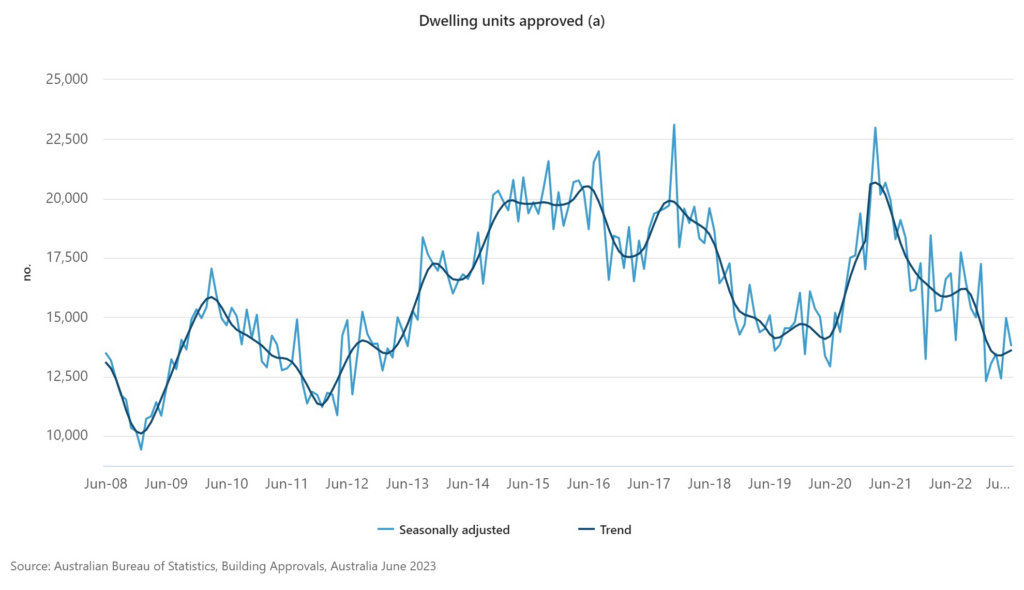

Australian building permits are back to 2007/12 levels:

Рис. 7

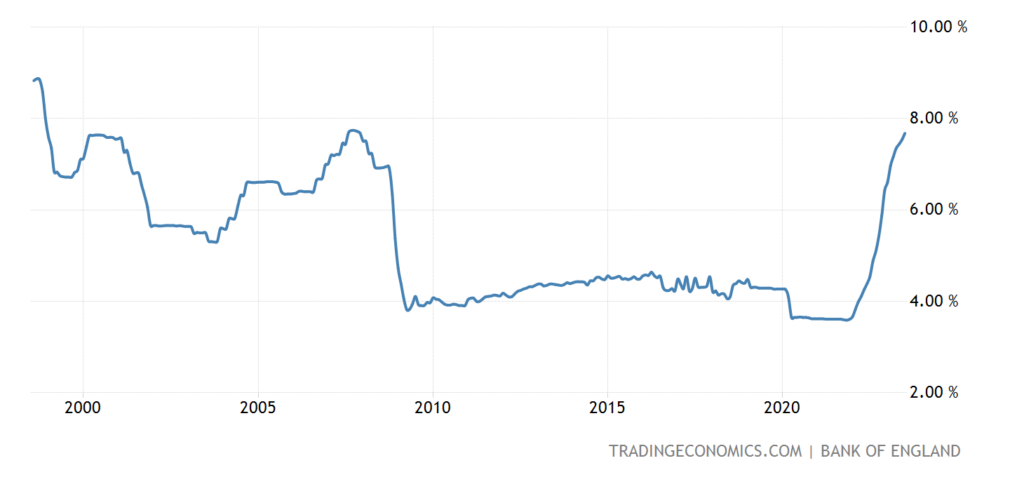

The UK mortgage rate of 7.68% is only 0.06% from the peak of 2007, upon reaching which a 25-year top will be formed:

Рис. 8

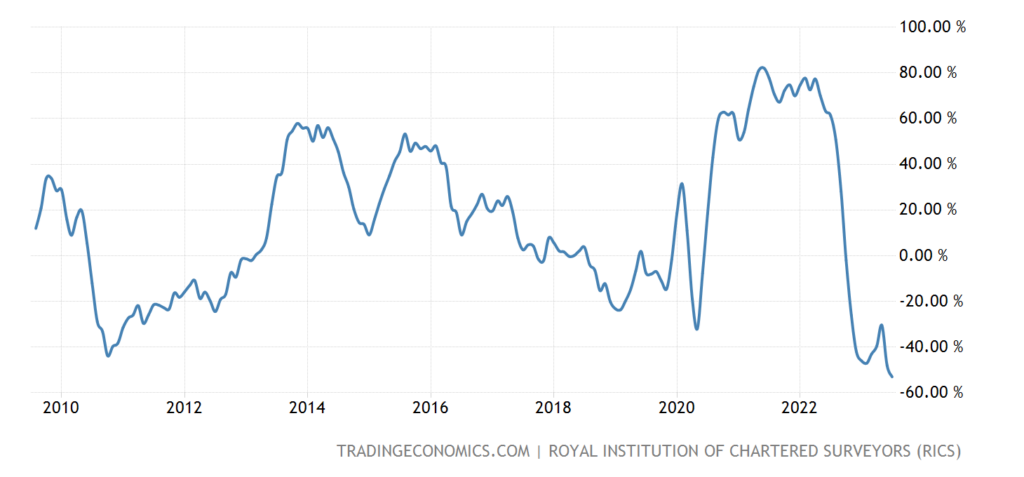

UK house price balance -53% – 14-year bottom:

Рис. 9

In the US, 7.09% is near last fall’s 21-year peaks:

Рис. 10

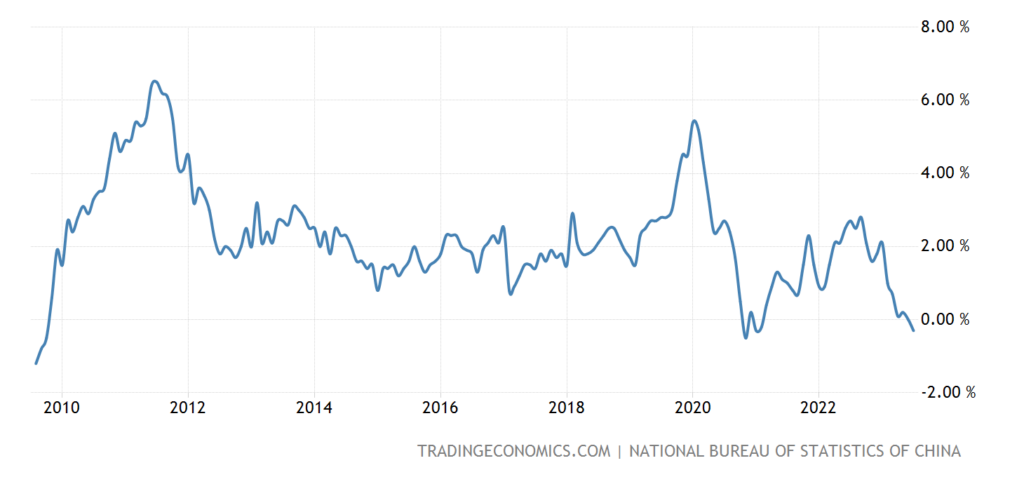

CPI (Consumer Inflation Index) China -0.3% per year – not counting the failure of 2020, this is the lowest since 2009:

Рис. 11

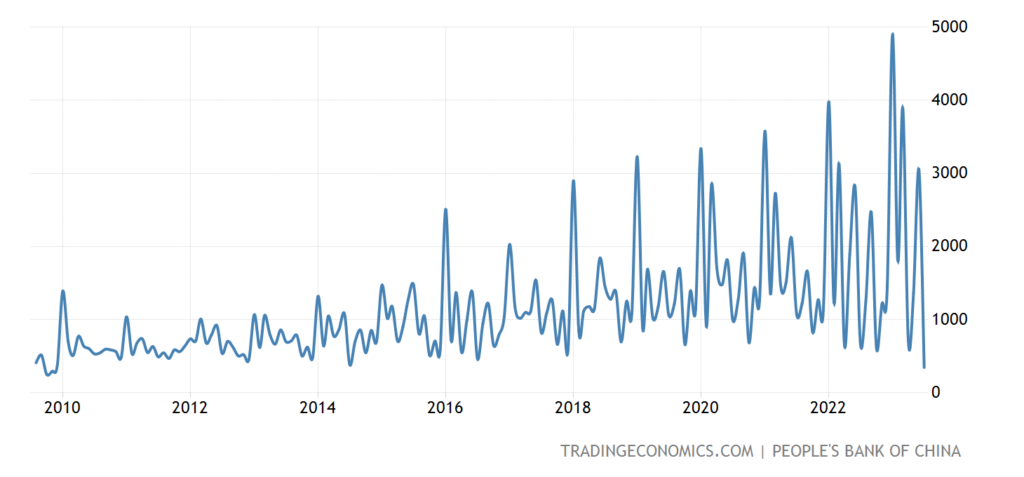

New loans (in yuan) in China are the lowest since 2009:

Рис. 12

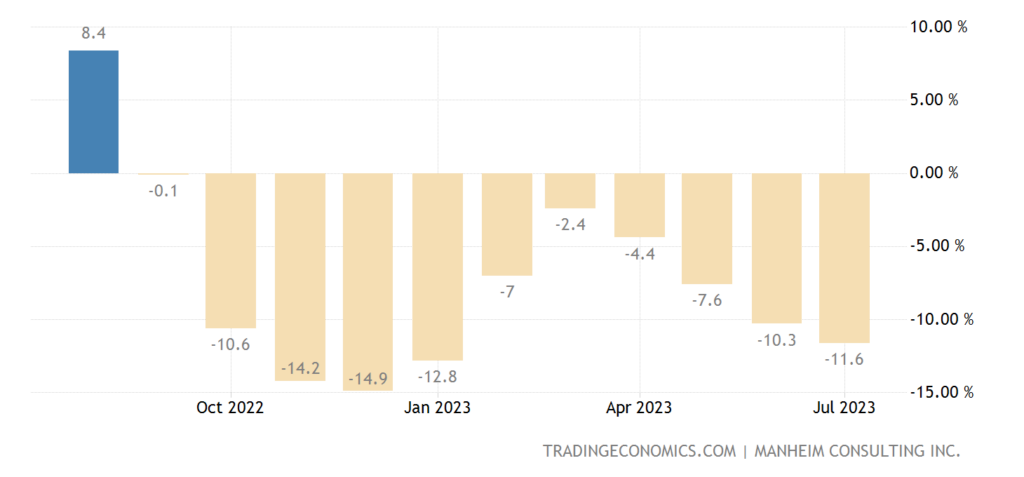

Used car prices in the US -11.6% per year – the 11th consecutive minus:

Рис. 13

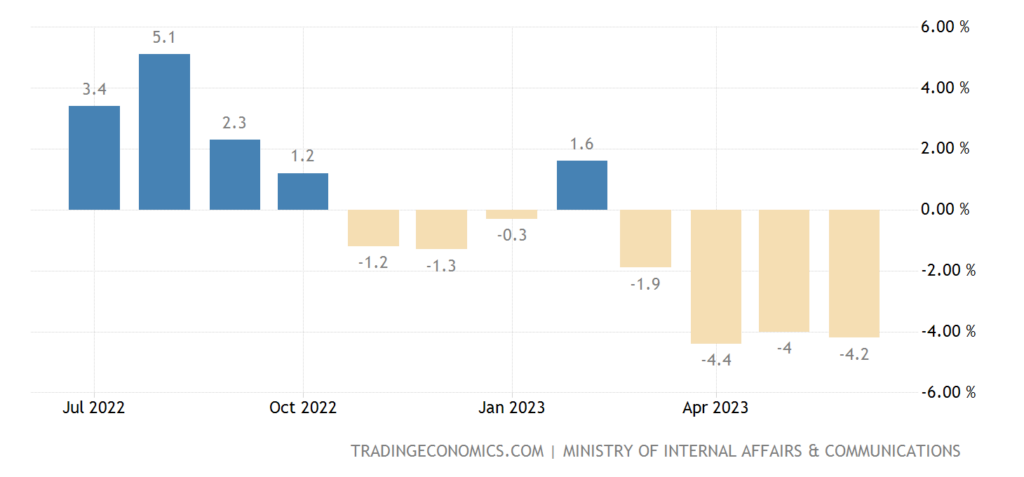

Japanese household spending -4.2% per annum – 4th negative in a row and 7th in the last 8 months:

Рис. 14

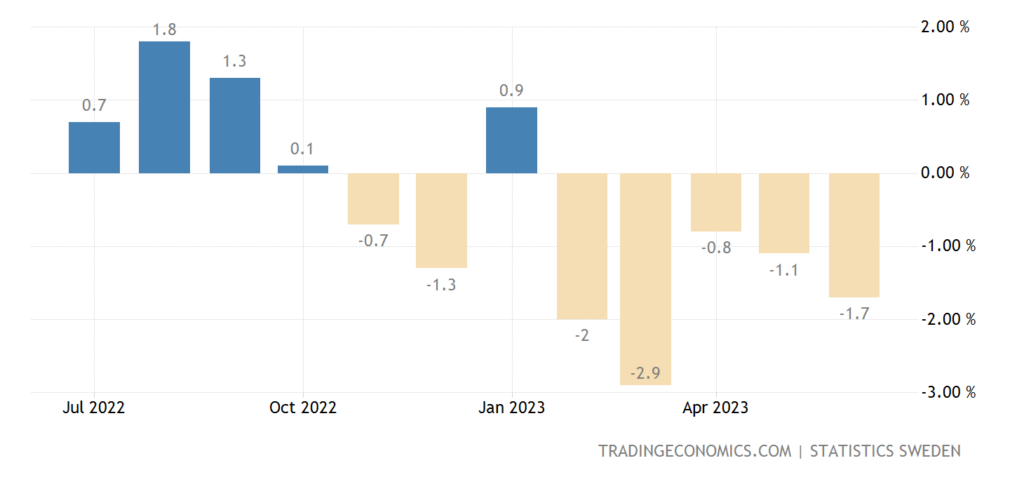

Swedes spending -1.7% per year – 5th negative in a row and 7th in the last 8 months:

Рис. 15

The Central Bank of India did not change anything in its monetary policy, as did the Central Bank of Mexico.

Main conclusions.

Summer, informative news is scarce. But the situation in the US clearly shows a very serious recession. We have already noted that, from the point of view of theory and various kinds of indirect data, most likely, the recession in the United States began in the fall of 2021 (simultaneously with rising inflation) and continues to this day. The rate of this decline, according to the theory, should be on the scale of 6-8% of GDP per year, and these figures are confirmed by indirect data. Well, the final picture will become clear later.

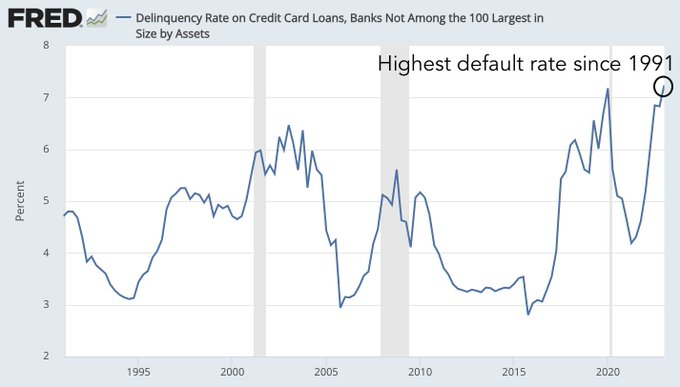

As usual, a few more charts. Here, for example, is the rate of delinquency on credit cards from banks outside the top 100 by assets:

By itself, this graph may not mean anything, but coupled with data on industrial inflation, it most likely indicates that workers in industrial enterprises in crisis (mainly in the provinces) cannot service their debts normally.

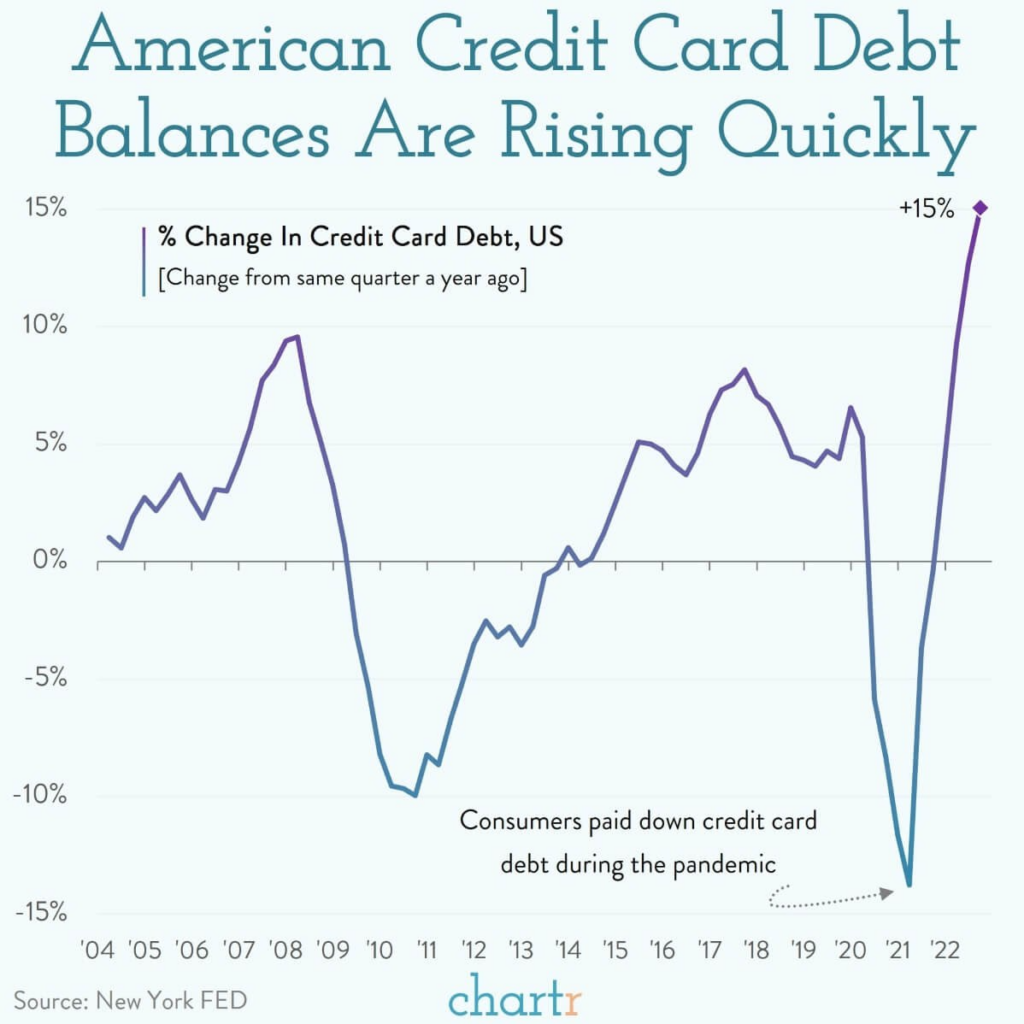

The following graph is similar, but not quite, this is the change in credit card debt, quarter to the same quarter a year ago:

The graphs, as you know, are similar, but, nevertheless, these are different indicators.

In general, it becomes clear why the rating agencies have begun to lower the ratings: they cannot but see the negative processes and understand that they need to be responded to. Otherwise, you can again fall into the situation of 2008, when the credibility of them was drastically shaken due to serious problems of the companies with the highest rating. In fact, it was about bankruptcies, which were avoided only thanks to the colossal assistance of the state.

Of course, all participants in the process would like to reach an agreement on the sly, but in the current situation, unlike earlier times, this is apparently not possible. And this means that if the situation in the economy worsens, and it will worsen, disagreements in the economic elite will become more and more public.

However, what are we talking about sad, summer is the holiday season! We wish everyone a pleasant weekend and for those who are just getting ready for a vacation, do not strain too much during the working week!