December 2-8, 2023

Big news. The United Arab Emirates announced that it will no longer sell oil for dollars. This is an important fact, especially considering the visit of the Russian President to the UAE and Saudi Arabia, followed by a meeting the next day (already in Moscow) with Iranian President Raisi.

All these events mean the continued destruction of US political dominance, which is based on the deterioration of the economic situation (see the next section of the Review). At the same time, the deterioration is not yet critical, since pricing in the main markets (including the oil market) still occurs in US dollars.

In addition, we note one more circumstance. At the very end of last week, the price of gold updated the record:

Pic. 1

And although the price fell earlier this week, the trend itself is fundamental. Before the dollar, gold was a single measure of value and, with a high probability, will return to this position following the crisis. Therefore, the increase in its price, as well as the difficulties in purchasing large volumes of physical gold, is also a criterion for the intensification of the crisis.

Macroeconomics. Moody’s agency agreed with our conclusion a few weeks ago and downgraded China’s rating outlook from stable to negative:

Pic. 2

Let us note that the criteria of this agency and our criteria most likely differ significantly. However, the onset of a serious economic crisis in China has been confirmed.

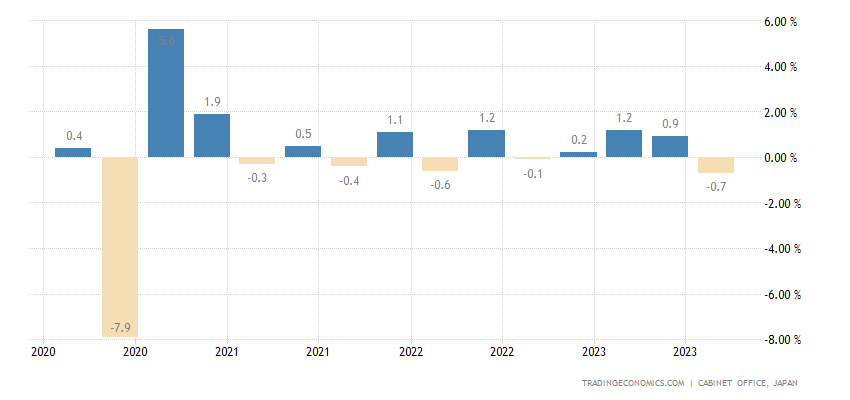

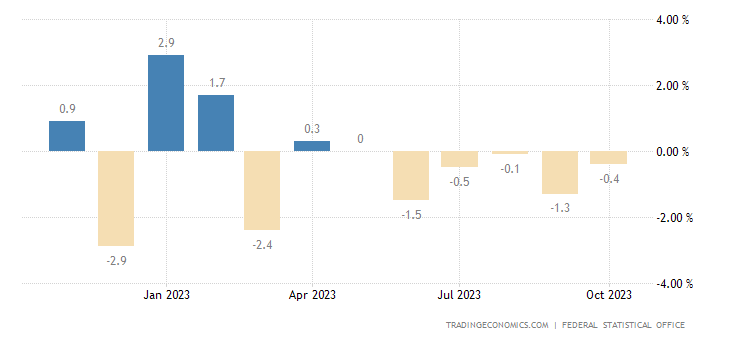

Japan’s GDP -0.7% per quarter – the worst dynamics in more than 3 years:

Pic. 3

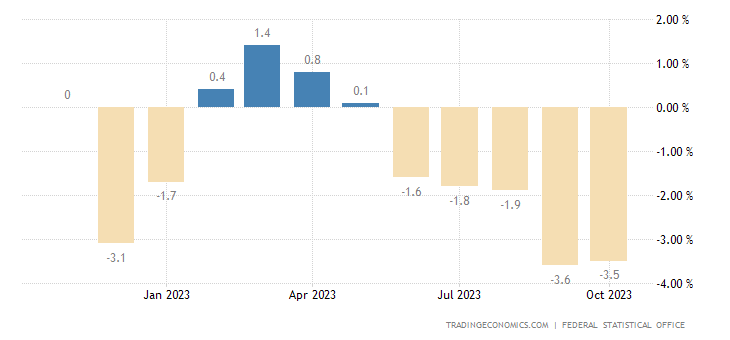

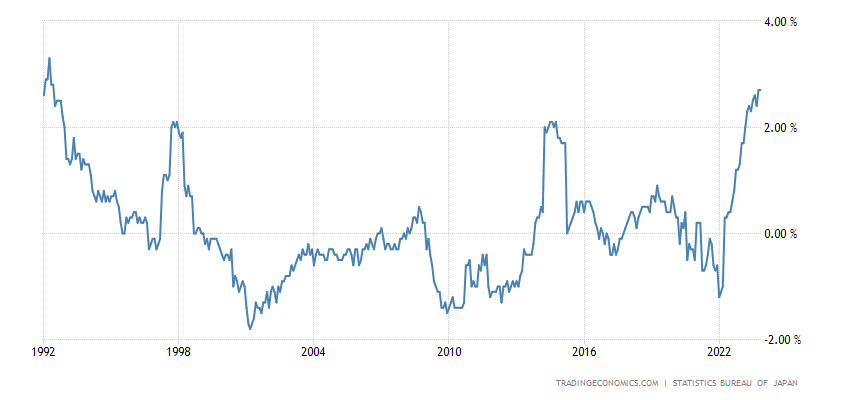

And its deflator +5.3% per year is a record for the modern history of observations:

Pic. 4

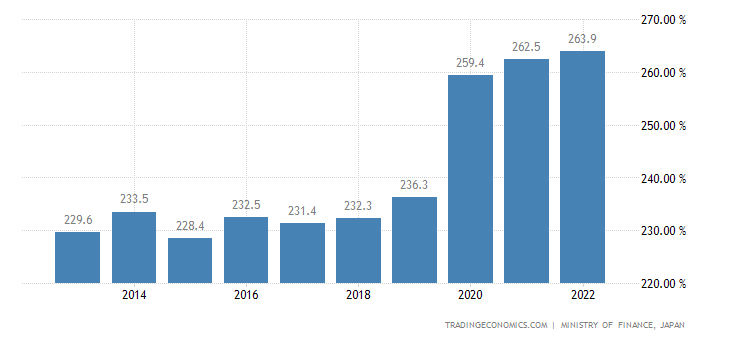

But the Central Bank is not ready to tighten policy, because public debt exceeds 260% of GDP:

Pic. 5

And yet, he gradually begins to hint at a move away from ultra-soft policies:

Pic. 6

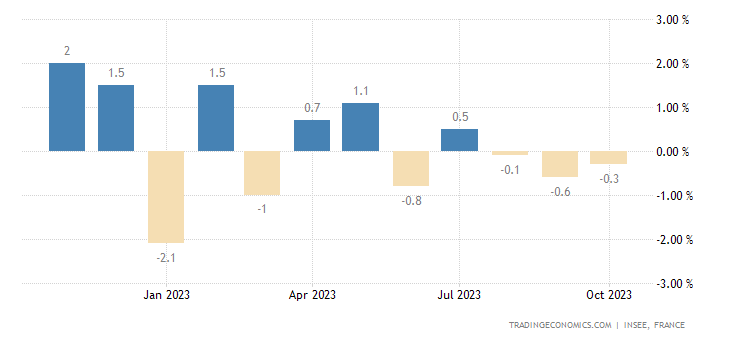

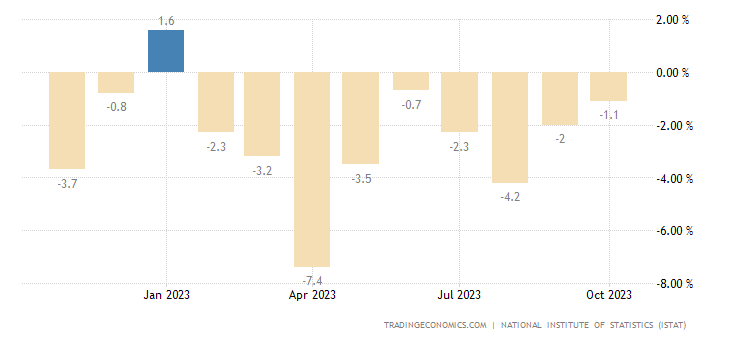

Industrial production in France -0.3% per month – 3rd minus in a row:

Pic. 7

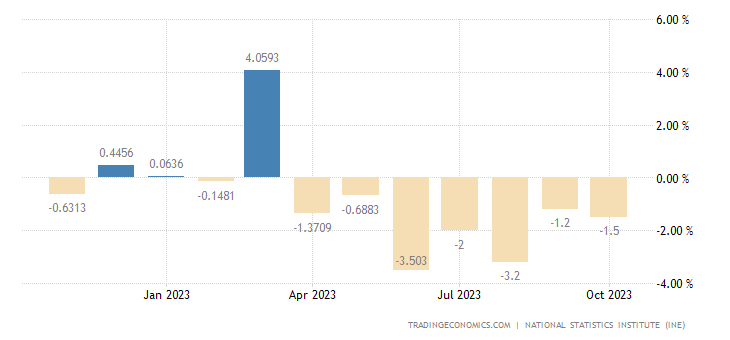

In Spain -1.5% per year – the 7th minus in a row:

Pic. 8

In Italy -1.1% per year – the 9th minus in a row:

Pic. 9

German industrial output -0.4% per month – 6th minus (or zero) in a row:

Pic. 10

And -3.5% per year – the 5th minus in a row:

Pic. 11

Deindustrialization has become the dominant trend in the EU economy.

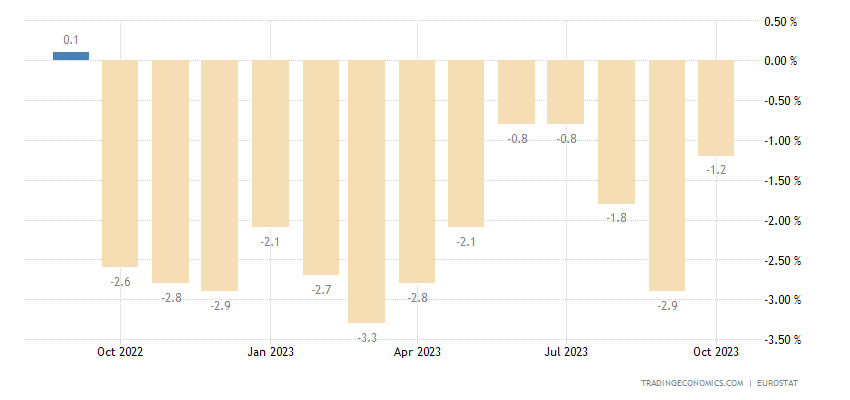

It is not surprising that eurozone retail sales are -1.2% per year – the 13th monthly negative in a row:

Pic. 12

And as problems in the financial sector intensify, problems with budget subsidies to consumers and producers will begin. And here the standard of living (and retail sales) will begin to decline much faster. And who is to blame for the Europeans?

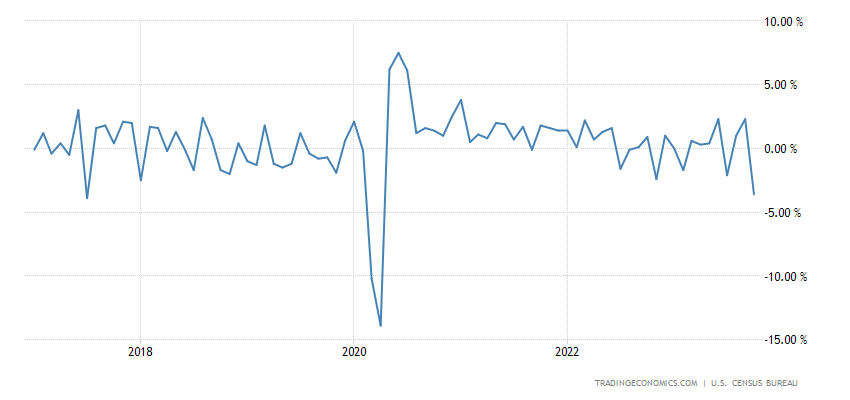

Industrial orders in the US -3.6% per month, this is the minimum since 2020, and before that – since 2017:

Pic. 13

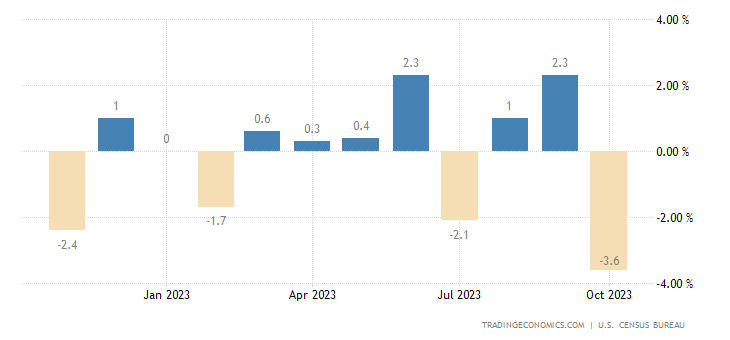

This is a fundamental point. Although the previous two quarters were positive:

Pic.14

But on a “longer” graph (in fact, this is one graph, just the first over a longer period), it is clearly visible that after compensatory growth in the second half of 2020, a long-term (and with gradual acceleration) trend toward a decline in production began.

Neither investments in the military-industrial complex nor the transfer of production from the EU show a clear effect. And this is an extremely worrying trend for the US economy.

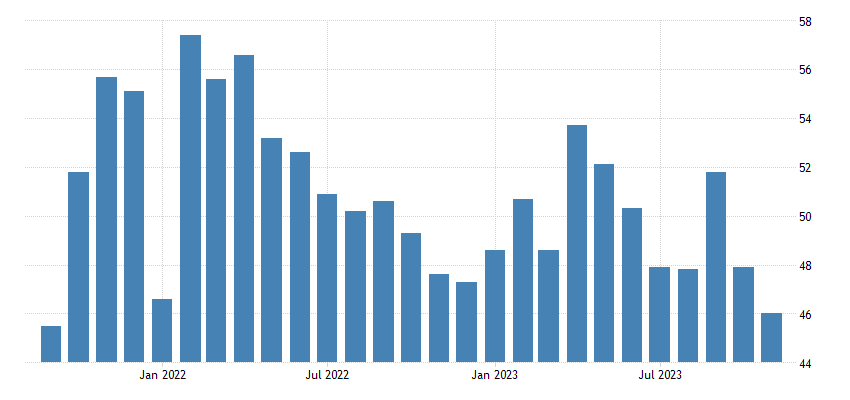

Australia’s services industry PMI (46.0) is the weakest in 26 months: below 50 means stagnation and decline:

Pic. 15

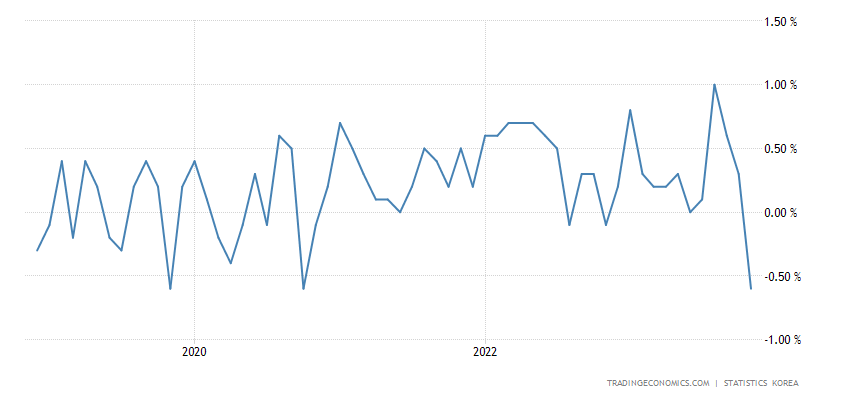

CPI (consumer inflation index) of South Korea -0.6% per month – the maximum decline in 5 years:

Pic.16

Has consumer deflation started in Korea? If this is so, then the crisis there has already reached extremely acute forms. However, for an export economy this is normal.

Tokyo Prefecture CPI in Japan without food and fuel +2.7% per year – 31-year high:

Pic. 17

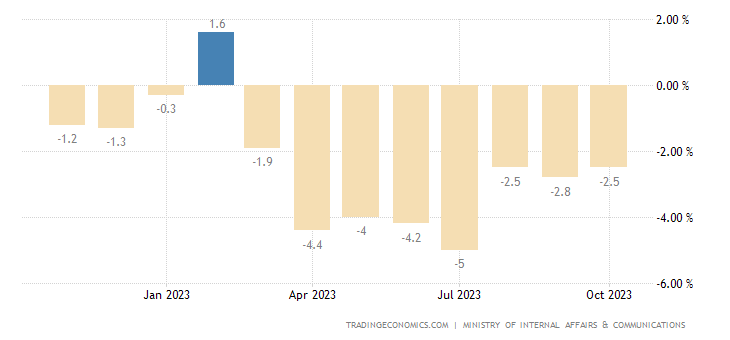

Japanese household expenses -2.5% per year – the 8th negative in a row and the 11th in the last 12 months:

Pic. 18

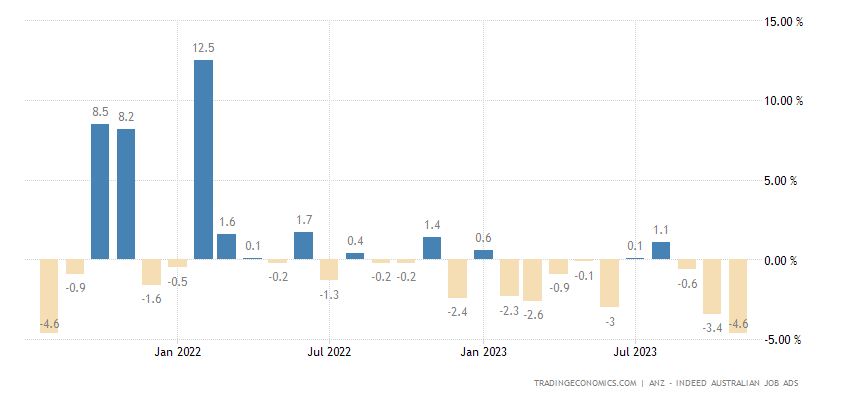

The number of job postings in Australia -4.6% per month – the worst dynamics in 27 months:

Pic. 19

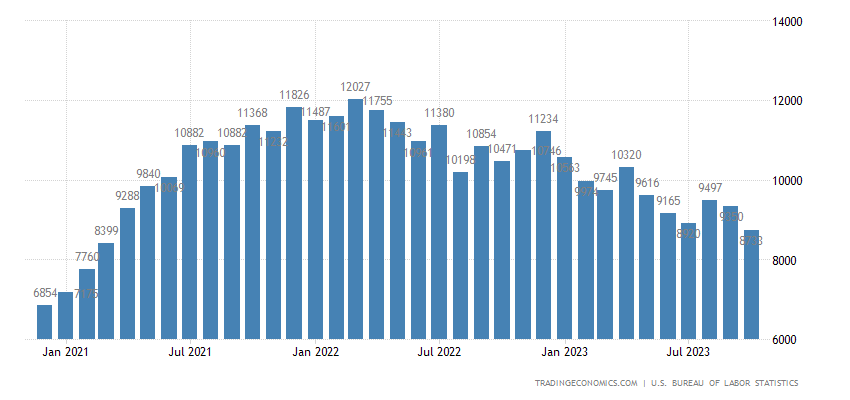

In the US, the number of available vacancies is at its lowest in 31 months, but still higher than before Covid:

Pic. 20

The Central Bank of Australia left its monetary policy unchanged, as did the Central Bank of Canada and the Central Bank of India.

Main conclusions. As usual, this section contains various kinds of indirect data on the development of the crisis.

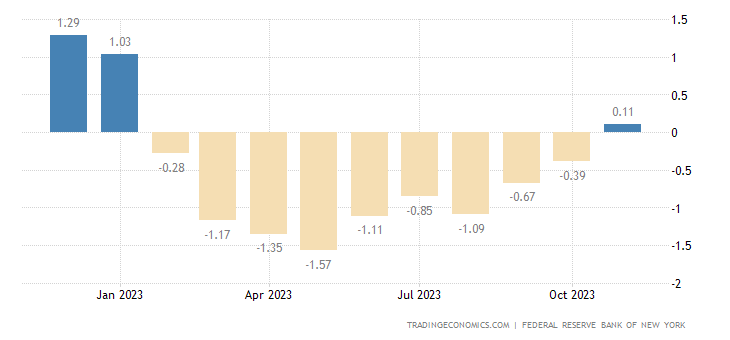

The global index of supply chain disruptions from the New York Fed has turned positive for the first time since January (i.e. there are more problems than average) and is growing quite vigorously:

Pic. 21

One confirmation of this trend is problems with uranium due to sanctions and other political reasons: prices for it are the highest in 16 years:

Pic. 22

However, in the first section we already noted that political problems did not arise by chance; they themselves are a consequence of the economic crisis.

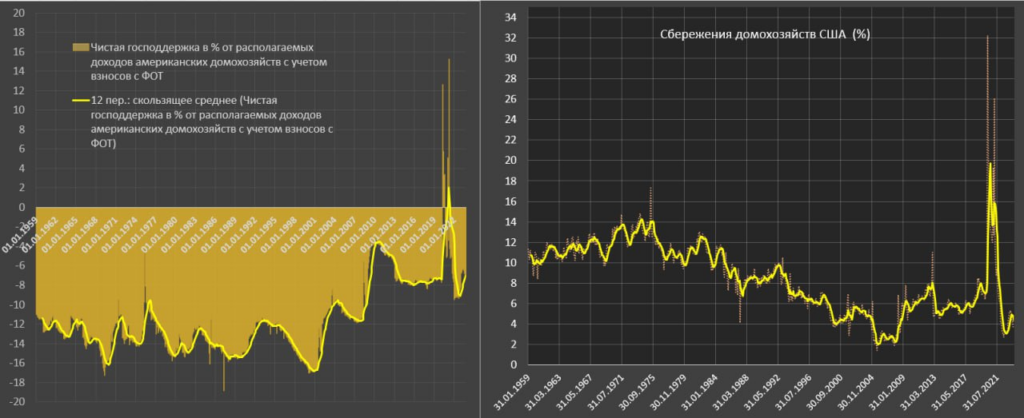

Pavel Ryabov’s analysis of the savings of American citizens.

“U.S. household savings are near a historic low of 3.8% in October, averaging 4.3% over the past 6 months, compared to the historical norm of 6.2% from 2010 to 2019 and 7.4% in 2019.

Savings rates were low just before the crisis in 2008 – averaging 2.9% from 2006 to August 2008, which led to a systemic degradation of the sustainability of household balance sheets amid high lending rates and rising debt service costs in the spending structure.

Yes, of course, with a staggering amount of assets (over 115 trillion), it is strange to talk about a shortage of financial resources, but financial resources are distributed extremely unevenly, and approximately a third of the population experiences regular financial difficulties.

The crisis is provoked not by dollar millionaires, but by the proletariat. This is where problems arise. A slowdown in income growth with a high rate of consumption and a simultaneous increase in the cost of debt servicing is sharply depleting the financial stability formed during the period of fiscal extremism and monetary frenzy of 2020-2021.

Non-mortgage interest expenses for American households reached an all-time high in absolute terms – over $570 billion for the year, compared to $350 billion before the COVID crisis.

Non-mortgage interest expenses reached 2.8% relative to disposable income, which is almost double what it was in 2021 and noticeably higher than the 2-2.1% observed in 2018-2019. The level of 2.8% is a lot, which is close to the historical highs of 2.8-3% formed in 1985, 2001 and 2007 (usually the crisis began after that).

Net government support as a percentage of disposable income is at minus 7%, i.e. the state withdraws more than it distributes targeted assistance (corresponds to the 2013-2019 average). From May 2023, fiscal policy towards the population began to tighten by approximately 1 percentage point, i.e. the accumulation of the budget deficit is not in favor of the population.”

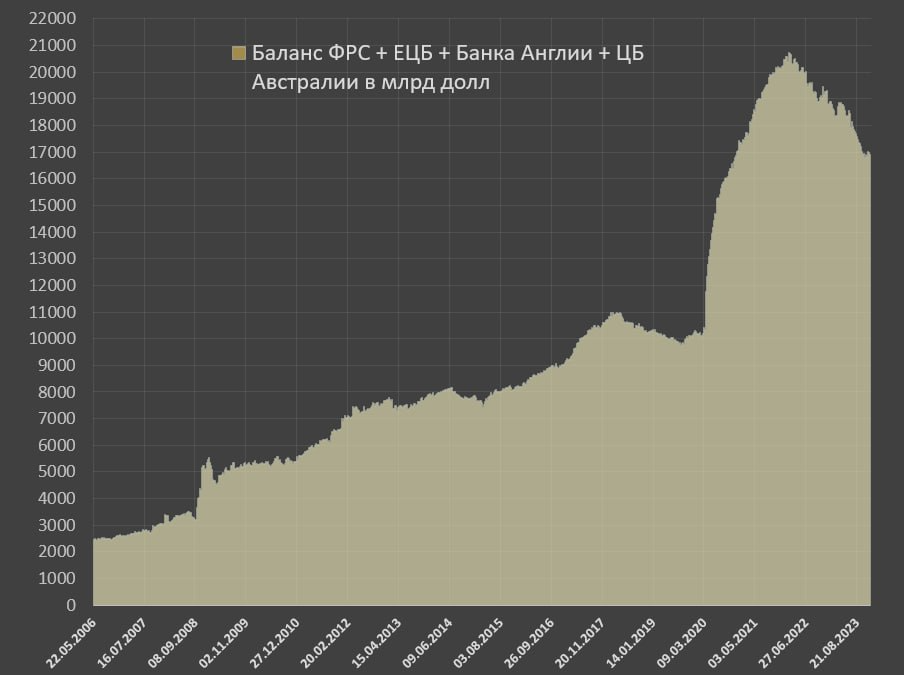

One more circumstance may be noted.

The joint balance sheet of the main Western countries clearly indicates a tight monetary policy (liquidity in circulation is declining). This means that private demand is stimulated through budgetary mechanisms, which we see in the growth of debt in the United States and other countries. We remember this policy well from the Russian experience of 1995-1998 and how it ended.

Since in those days the founder of the Khazina Foundation controlled the topic of monetary policy in the Ministry of Economy and then in the Presidential Administration, for us this feeling of déjà vu is especially strong. And we can note that such a policy, firstly, is not constructive, and, secondly, it ends quite quickly. Yes, the Fed, of course, is not the Bank of Russia of the times of Dubinin-Aleksashenko; Powell & Co’s qualifications are an order of magnitude higher. But this can only extend the time of its existence, and not the final result.

However, whoever is forewarned is forearmed. So we, together with our readers, can relax on the weekend and go to work on Monday with fresh knowledge about the development of the situation.