June 24-30, 2023

Big news. Apparently, summer has come – there were no bright events during the week. With some stretch, we can say about the collapse of the Turkish lira:

We already wrote that the sharp increase in the rate by the Central Bank of Turkey did not comply with the policy of the Fed (and usually banks follow the Fed, not ahead of it) and looked somewhat pretentious. However, it is possible that this leadership of the Fed decided to “train on cats.” In any case, the result turned out to be very convincing so that no one would repeat it. At the same time, Powell resolved the issue with everyone who advises him to raise the rate “like under Volker.”

In general, summer comes into its own and, most likely, there will be less economic news for some time. Well, or we will have to prepare for extremely difficult times. This, of course, will be, but I want the summer not to be spoiled for us.

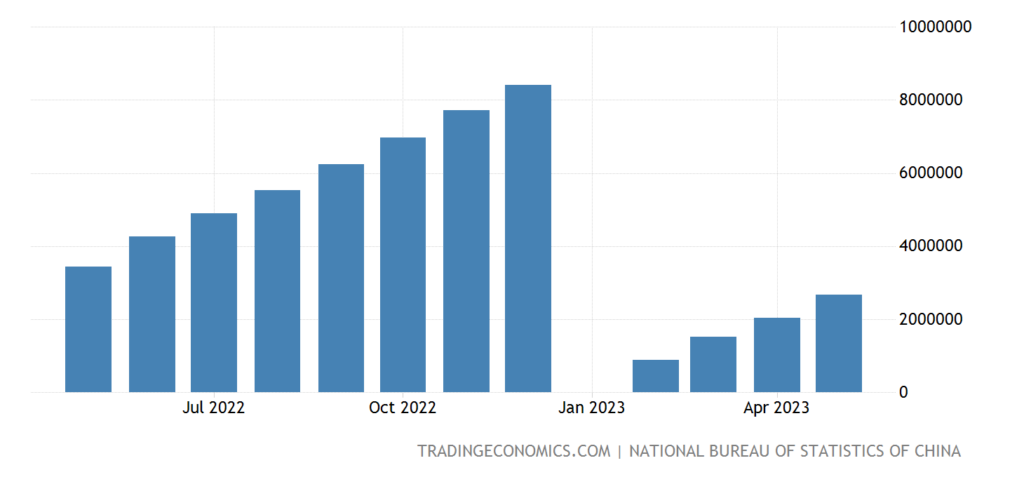

Macroeconomics. According to the already established local habit, let’s look at the situation in China. Profits of industrial companies in China in January-May -18.8% per year:

Pic. 1

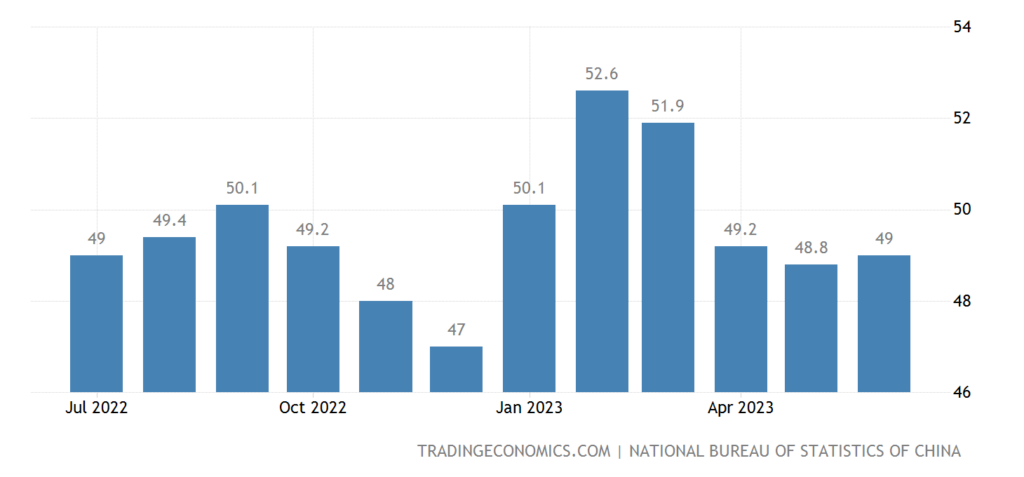

The official PMI (an expert index of the state of the industry; its value below 50 means stagnation and decline) of the PRC industry remains in the decline zone (49.0) for the 3rd month in a row:

Pic. 2

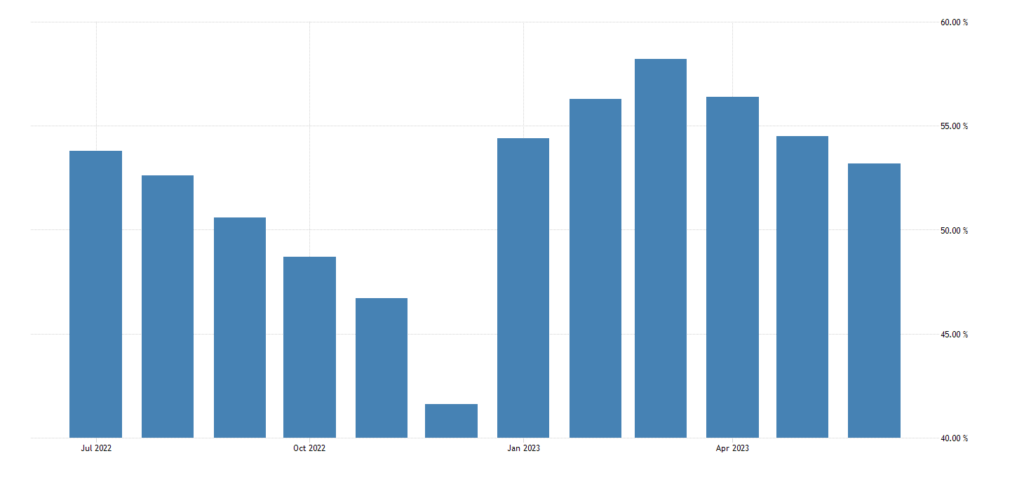

And other sectors, although they remain in the growth zone (53.2), showed the worst value for six months:

Pic. 3

In general, the crisis in China is developing, everything is in accordance with the theory.

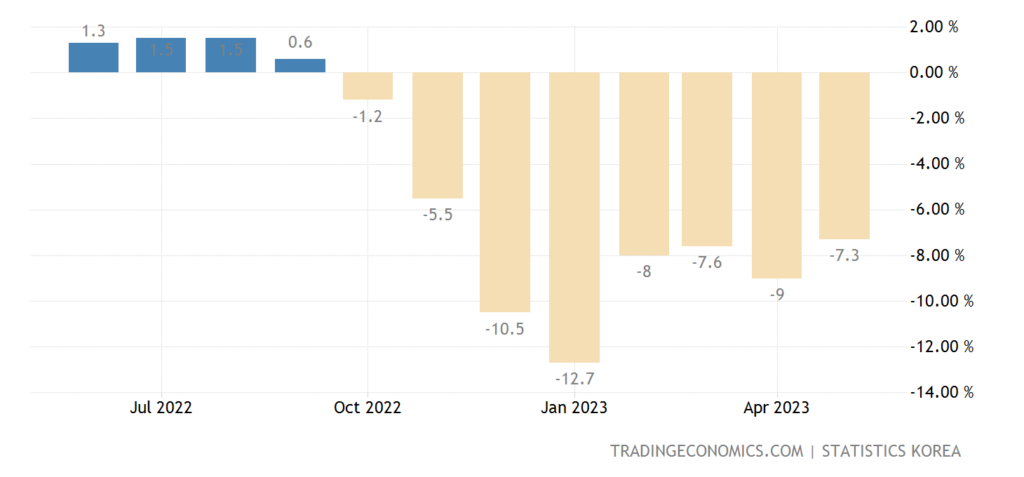

Industrial production in South Korea -7.3% per year – the 8th negative in a row:

Pic. 4

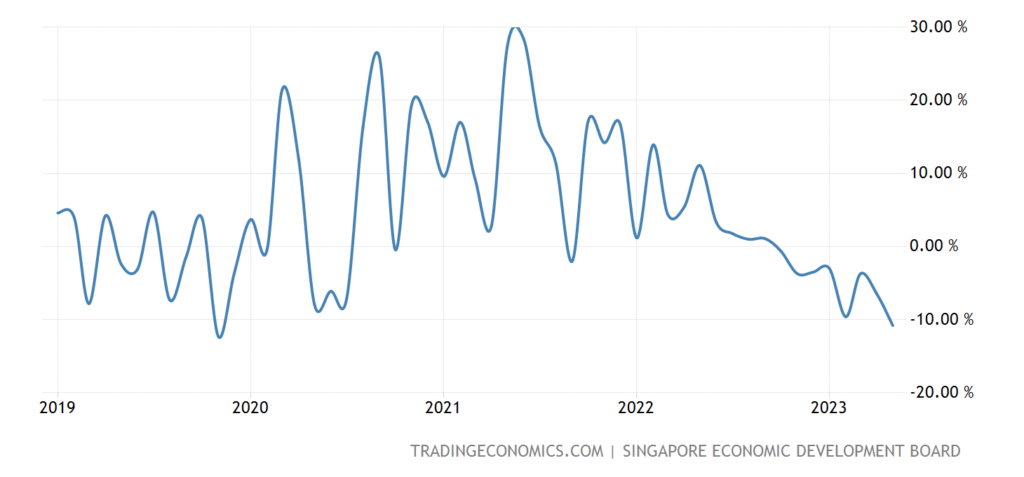

Singapore manufacturing output -10.8% y/y – worst performance in 3.5 years:

Pic. 5

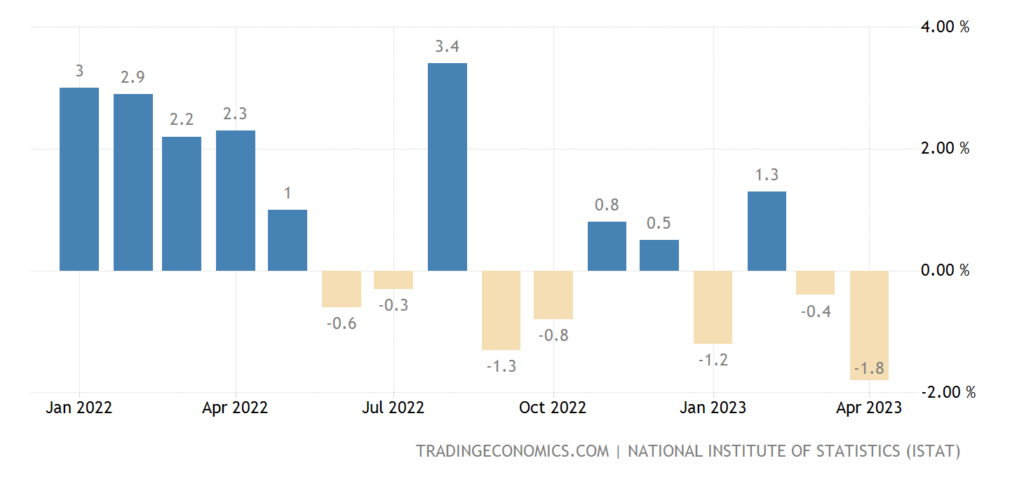

Industrial sales in Italy -1.8% per month – 2nd negative in a row and the strongest decline in 1.5 years:

Pic. 6

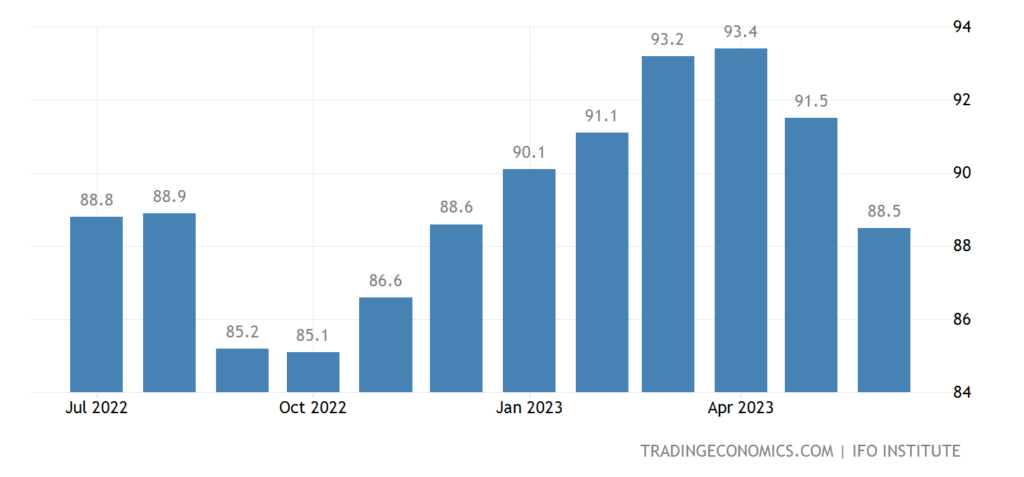

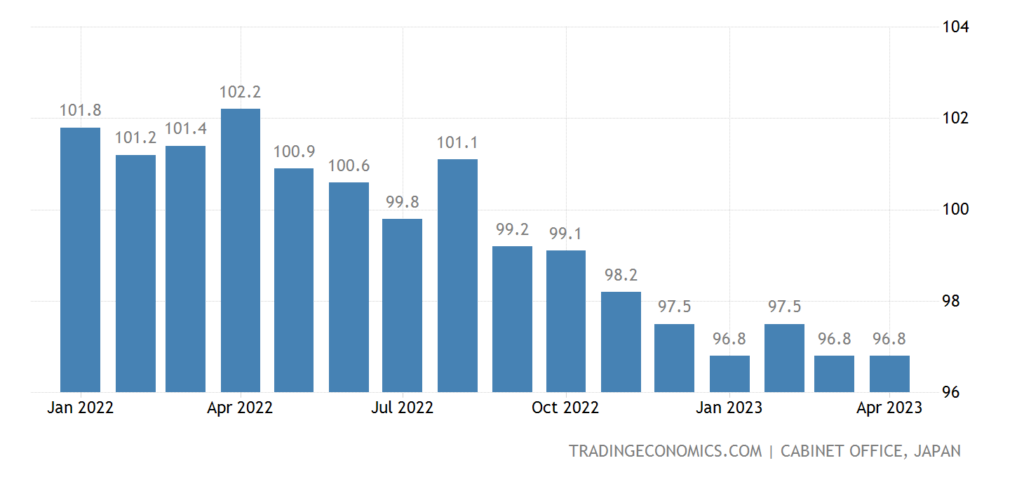

Business climate index in Germany (IFO review) is the weakest in 7 months:

Pic. 7

Business confidence in Italy at least 2.5 years:

Pic. 8

As in Spain:

Pic. 9

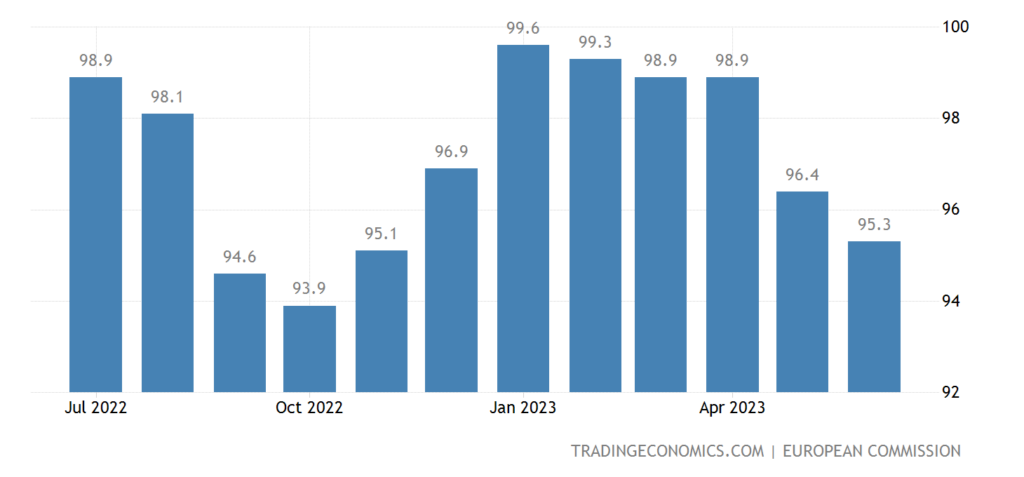

Economic sentiment in eurozone worst in 7 months:

Pic. 10

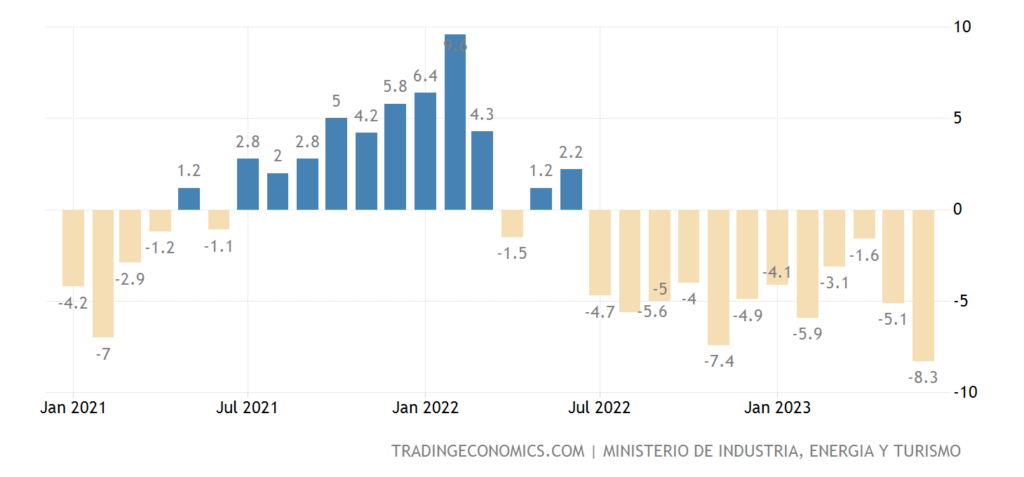

Loans to households in the eurozone +2.1% per year – the weakest dynamics since the end of 2016:

Pic. 11

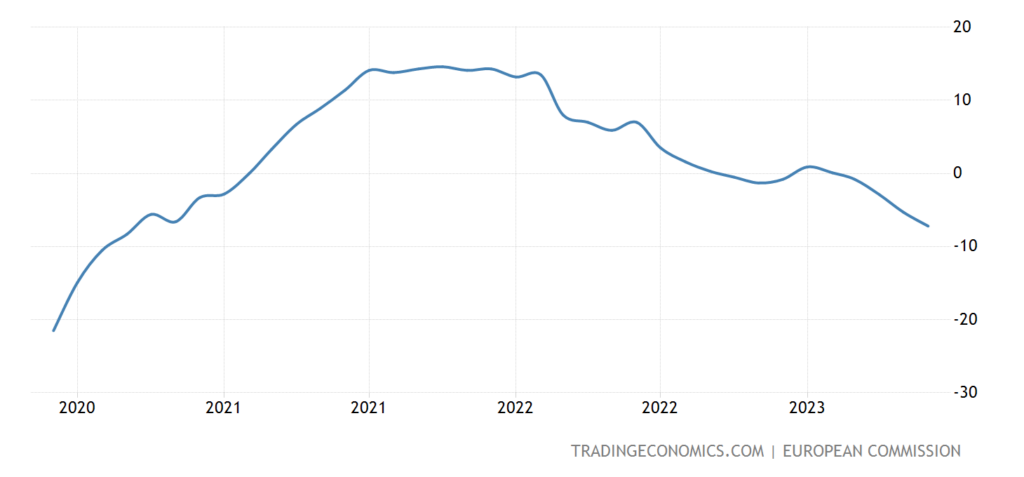

Moreover, the industry is pessimistic for a maximum of 3 years:

Pic. 12

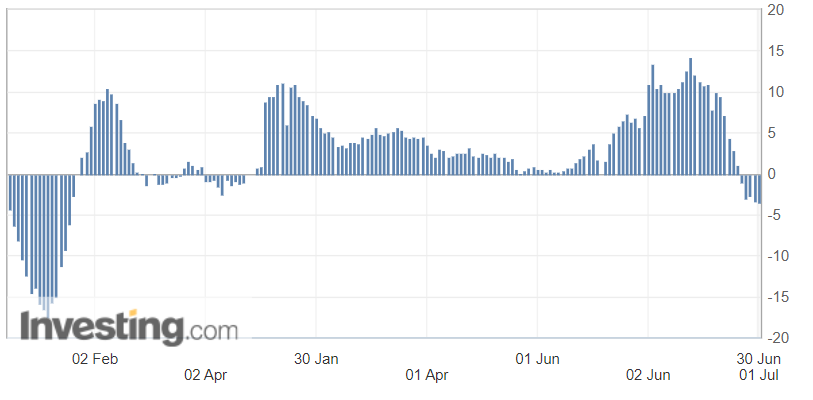

PMI Chicago has been in the downtrend zone for 10 consecutive months, now the decline is very deep (41.5):

Pic. 13

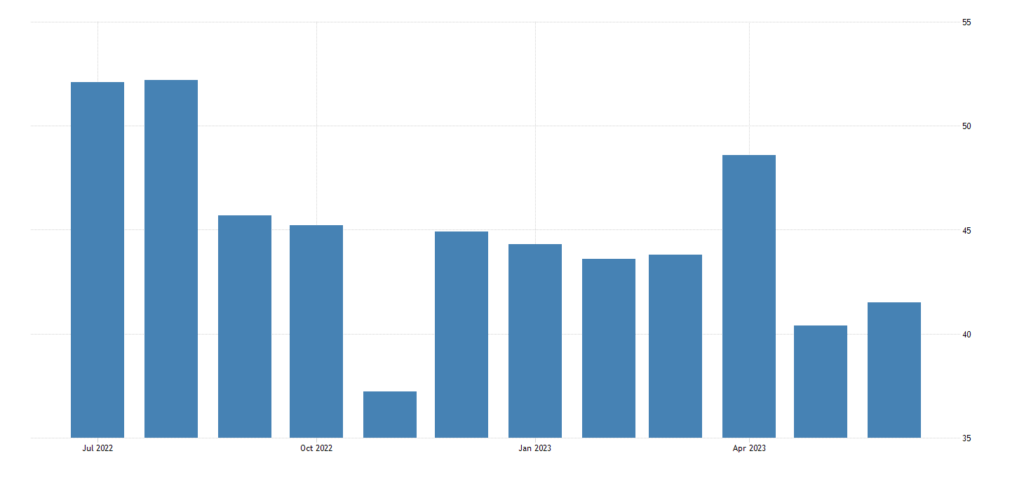

Leading indicators of Japan at the bottom for 1.5 years:

Pic. 14

U.S. pending home sales -22.2% pa – 24th straight negative, worst streak since 2005/09:

Pic. 15

After a short pause, US housing prices resumed growth:

Pic. 16

House prices in Britain -3.5% per year – the strongest decline since 2009:

Pic. 17

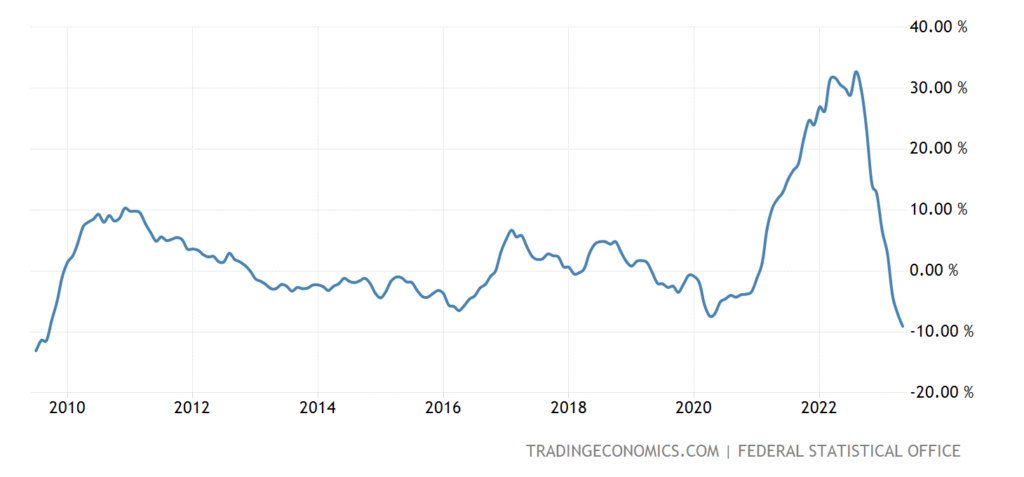

“Net” (excluding highly volatile components of food and fuel) CPI (consumer inflation index) Germany +5.8% per year – a repeat of the 31-year high:

Pic. 18

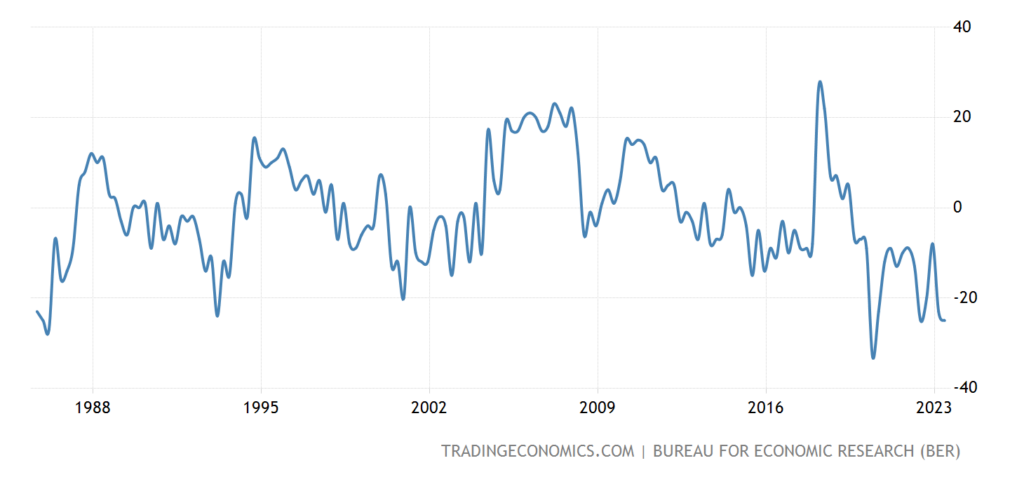

PPI (industrial inflation index) Spain -6.9% per year – not counting the failure of 2020, this is the minimum for 47 years of observation:

Pic. 19

Singapore PPI -15.3% per year – 8-year bottom:

Pic. 20

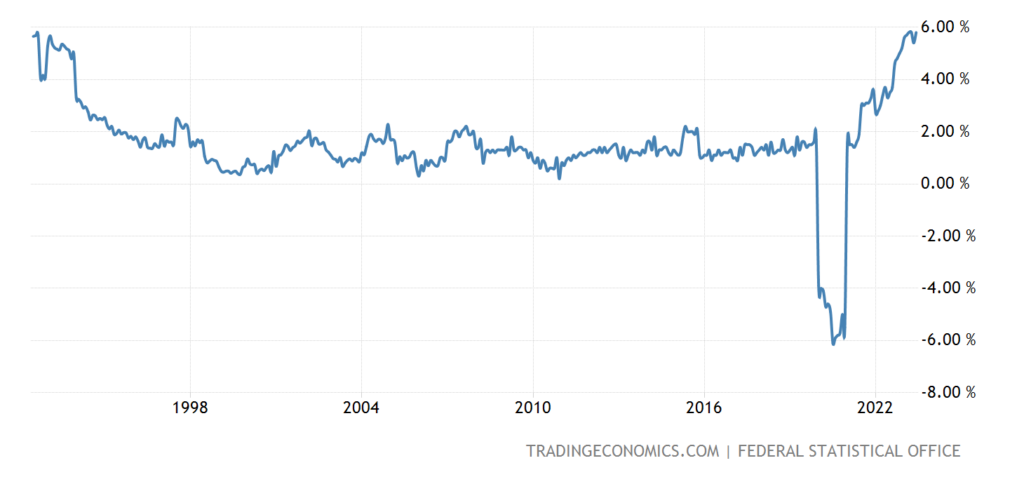

Import prices in Germany -9.1% per year – the strongest decline since 2009:

Pic. 21

Consumers in South Africa, apart from the failure of 2020, are the most pessimistic since 1985:

Pic. 22

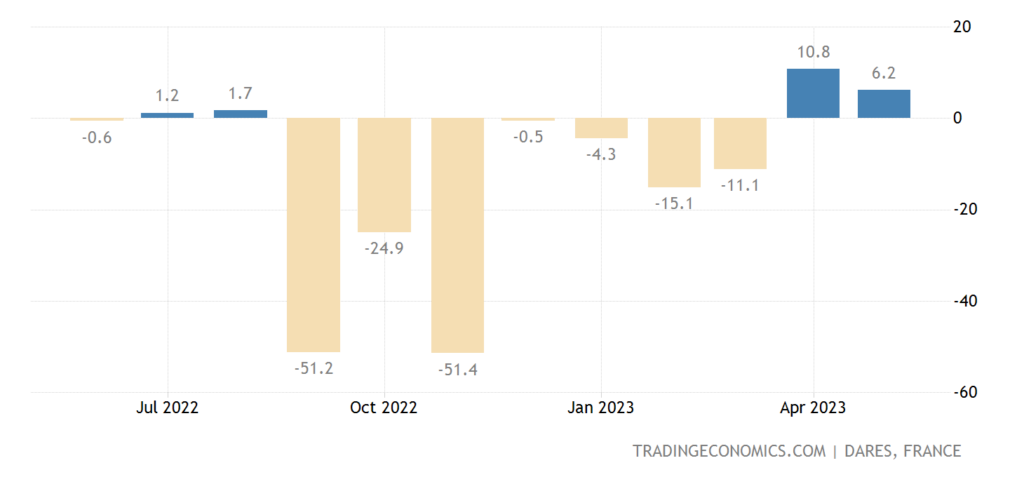

The number of registered unemployed in France is growing for 2 months in a row:

Pic. 23

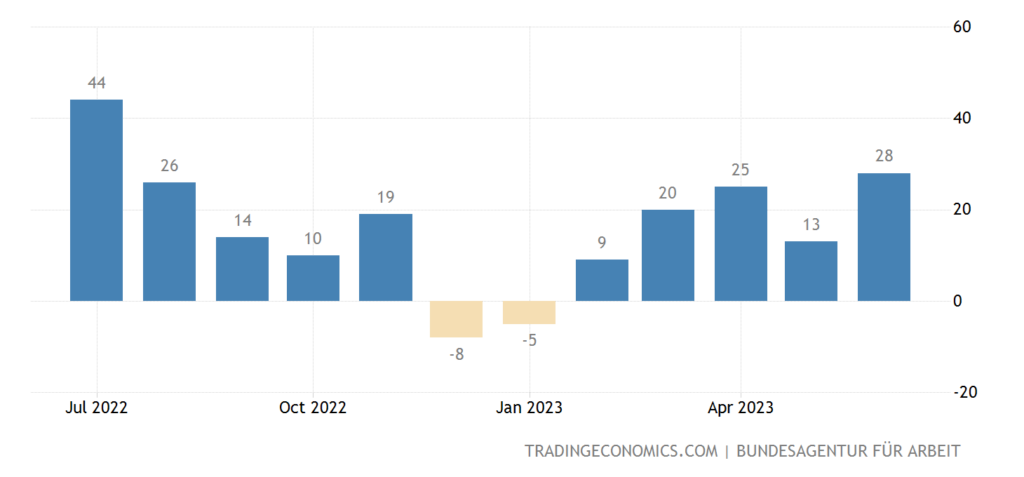

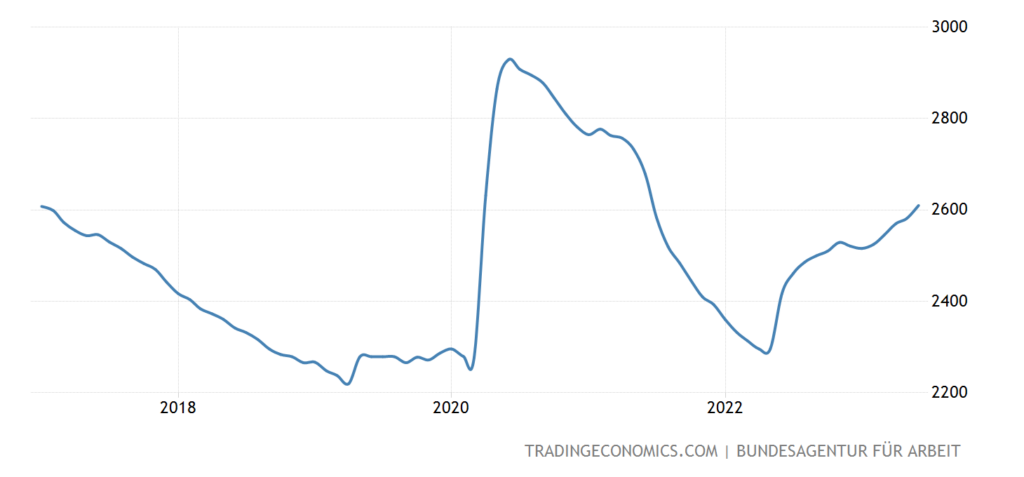

The number of unemployed in Germany has been growing for 5 months in a row:

Pic. 24

And it has already reached the levels of the beginning of 2017:

Pic. 25

Like the unemployment rate:

Pic. 26

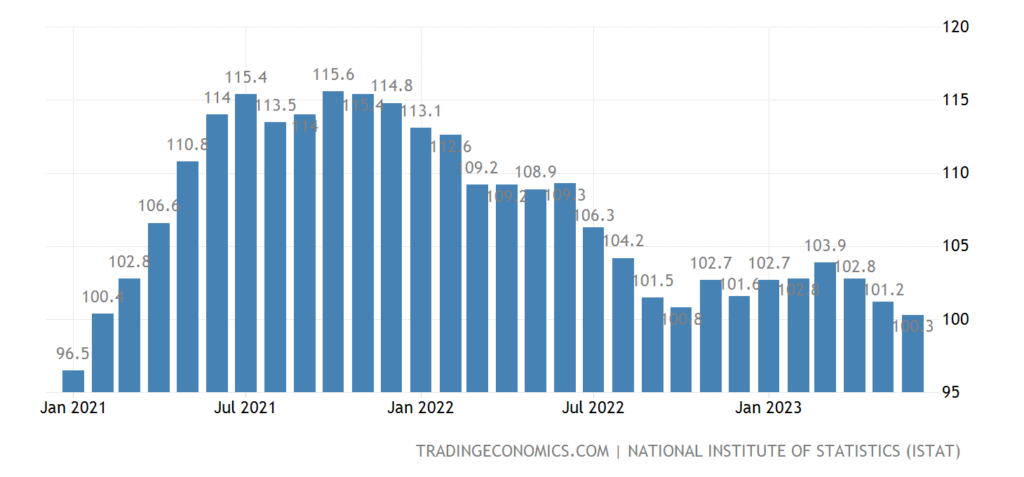

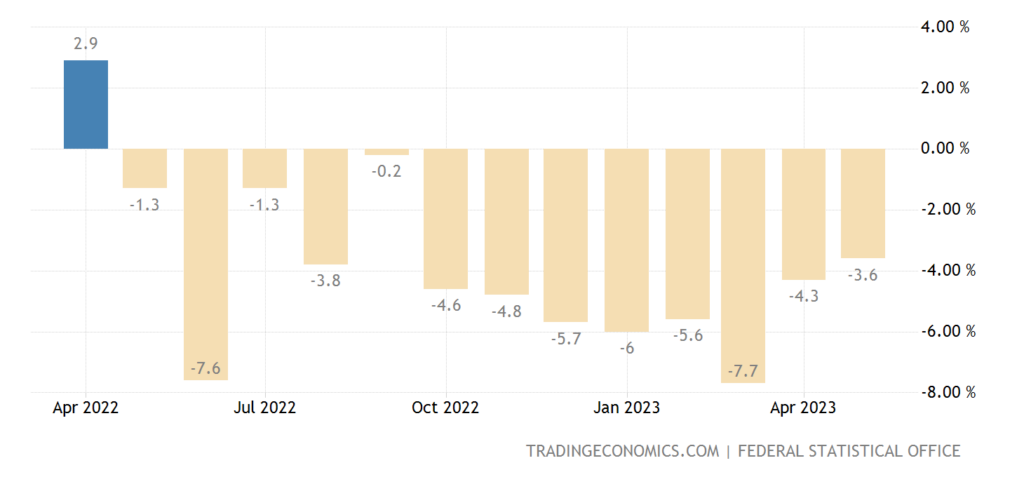

Retail sales in Germany -3.6% per year – the 13th negative in a row:

Pic. 27

Main conclusions.

Clearly, there is high inflation in the consumer sector and at the same time deflation in the industrial sector. The latter is understandable – this is a drop in real demand, which is distributed along technological chains. And, most likely, the farther from the end consumer, the greater the fall in prices, because otherwise it is absolutely impossible to keep your customers.

But why is there no deflation in the consumer sector? But the fact is that no one canceled the growth of costs during the structural crisis. It’s just that for industrial companies there is a wide spread in real costs (someone was able to save on something and survived, while others went bankrupt) and therefore everything is (relatively) good for some companies, while others are very bad. In full accordance with the theory of work in falling markets.

But in consumer markets, this does not work out, everything depends on the demand that needs to be met and international competition. Roughly speaking, American consumers of intermediate industrial goods compete not only with each other, but also with Chinese imports, which are a priori cheaper than American products. Accordingly, the demand for intermediate goods of American production falls. And China is increasing its exports.

This does not help China, because this increase in exports is not enough to compensate for falling domestic subsidies (which, in turn, cannot be increased because of the danger of inflation). But on the other hand, it allows you to partially compensate for internal problems, while in the United States the opposite is true.

In general, it can be noted that the structural crisis is developing in all its glory, and in some details it is accelerating. However, it is possible that this is a consequence of the fact that the previous months the recession was hidden in the hope that it would end. And now we have to admit the obvious.

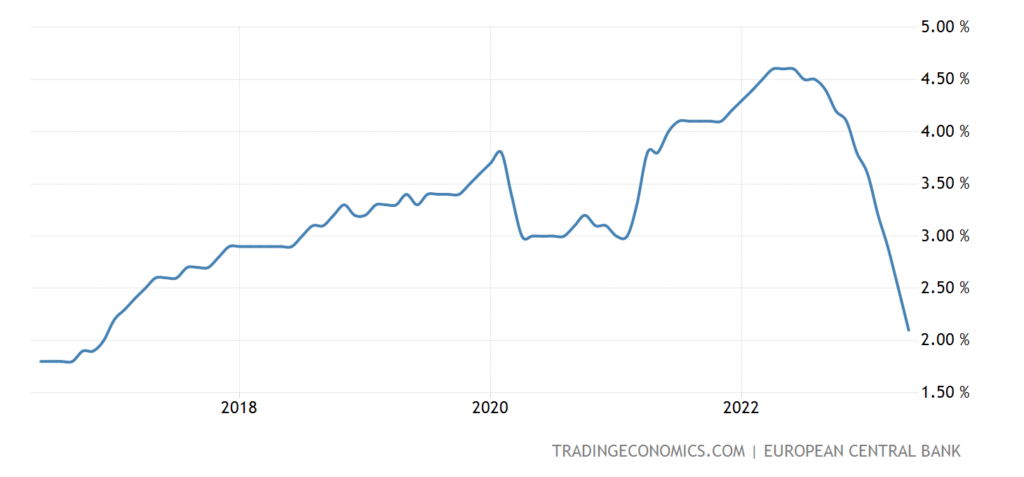

In conclusion, a few words about what the monetary authorities say. Powell and Lagarde spoke for weeks, their keynotes. Powell:

Expect “TWO OR MORE” Fed rate hikes;

the balance of risks is close, but not today;

more cooling of the labor market is needed to reduce inflation in the service sector;

the labor market is cooling more slowly than we need;

there is a possibility of a recession, but this is not the base case;

Significant disinflation is looming, but services are still months away;

the labor market can soften without large job losses;

banking stress in March is part of the reason for our pause in June.

Lagarde:

if core inflation does not decrease, we will raise the rate in July!;

little evidence that core inflation has turned down;

we still have work to do;

we do not consider a pause in raising rates;

our decisions depend on macro data;

we are all concerned about geopolitical developments. This has an impact on supply chains and trade.

What is “disinflation” is not very clear, maybe it is a synonym for the word “deflation”, which you don’t want to pronounce, so as not to give associations with the crisis of the 30s. But the general logic is clear: they are sincerely convinced that inflation can be suppressed.

Well, a few other opinions. Powell:

Moderate pace of interest rate decision-making is expected to continue;

most Fed speakers expect 2 or more rate hikes by the end of the year;

the risk of excessive tightening of monetary policy is not yet balanced, it is necessary to monitor macro data to assess the impact of monetary policy on the US economy.

The US banking sector is generally strong and resilient.

Fed stress test results:

in the worst-case scenario, the big banks will lose $541 billion!

the largest banks are resilient to rising rates in the face of a market shock and are well positioned to continue lending in a severe recession.

Bank of America:

The Fed will start cutting interest rates in May 2024.

Raphael Bostic, Chairman of the Reserve Bank of Atlanta:

I do not see the need for an urgent increase in the interest rate, as other members of the Fed say;

now it is more convenient to watch the market, if inflation does not decrease, we can raise the Fed rate.

To summarize all these opinions, they assume a regular development of events. Nobody sees the structural crisis, its causes and consequences. And we can only quote our own conclusion of August 2021, when we explained that Powell does not understand the situation and therefore will make serious mistakes. Actually, today we can only repeat and add that all those whom we have quoted will make the same mistakes.

By the way, Kristalina Georgieva is just silent, because she taught political economy and understands that something is going completely wrong. But he prefers to remain silent. From the point of view of the theory of Power, a very reasonable decision. In general, so far in the United States and the European Union there are no those who could say something reasonable. Except, of course, our readers, to whom we wish you a pleasant weekend and upcoming vacation!