Time period: 12-18 March 2022

Top news story. The week’s headline news was the decision to raise the US Federal Reserve interest rate from 0-0.25% to 0.25-0.5% and its intention to do the same at each of the remaining six meetings this year. In addition, the Fed said that it plans to start selling off assets from its balance sheet as early as the next meeting (at the end of April).

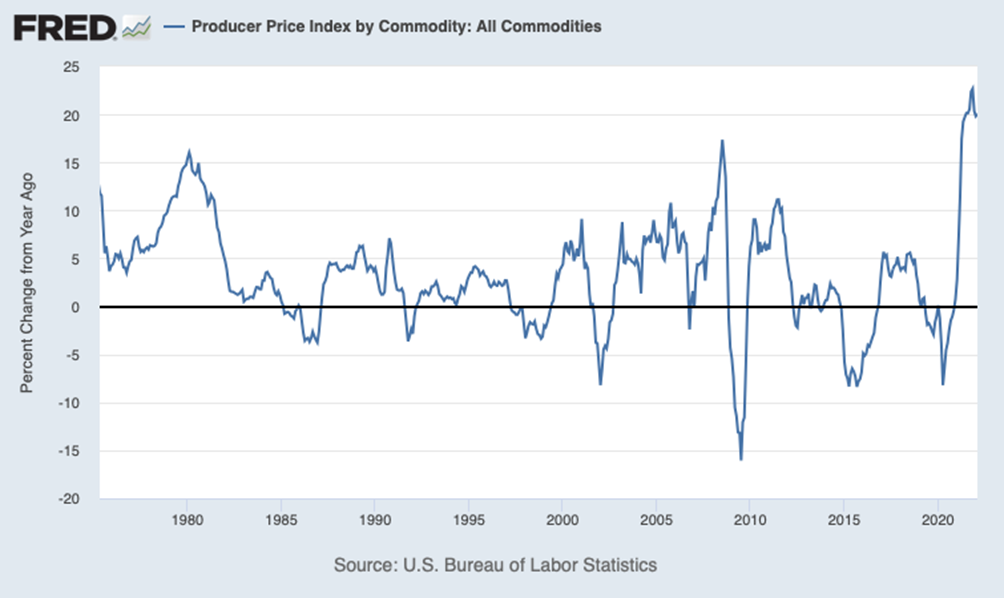

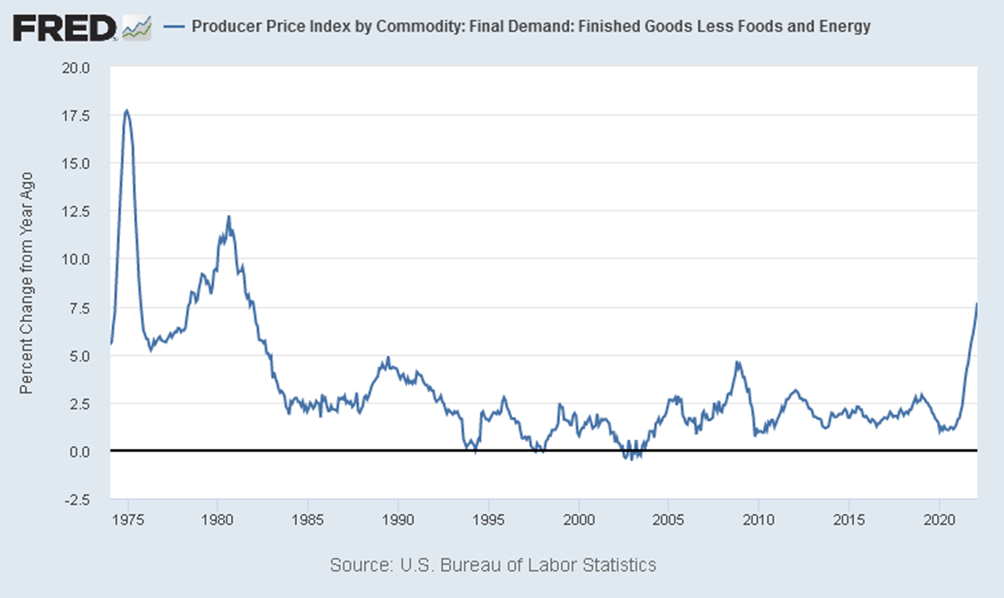

This decision is very revealing. Inflation is rising rapidly (see the next two sections of the Review) and it is necessary to act quickly, as debt instruments exhibit not just negative, but in fact double-digit negative returns. But, as we have noted in previous reviews, the experience of monetary tightening in recent months has shown that today’s inflation has a component that is not going to decline. It is enough to look at the graph of inflation for industrial goods, which sagged slightly in the fourth quarter of last year, but somehow one cannot call it a serious result:

We have explained many times the reasons for this: in contradiction to the mainstream monetary theory – and in full accordance with the new theory used by the Mikhail Khazin Foundation for Economic Research, see M. Khazin “Reminiscences about the future” – inflation consists of two components: monetary and structural. The first declines when monetary policy tightens, the second one at least does not change, and usually does. It is accompanied by a decline in GDP, and may run under one of two scenarios: deflationary or inflationary. The deflationary scenario was typical for the first (1907-08) and the second (1930-32) Crisis of capital effectiveness (see above book), the inflationary – for the third Crisis of capital effectiveness in the 1970s.

In fact, we are talking about the fact that the inflated expenditures of households since the “reaganomics” period are normalized due to the decrease in their credit and budget stimulus. Inflation is only a form of this process. And all the opportunities for monetary authorities to stop this process have run out. In fact, there is the last one, which is unable to prevent, but can prolong the agony until the November elections.

This process is the largest outflow of capital from the European Union to the U.S. (1-1.5 trillion dollars). It is related to the sanctions process against Russia, actively stimulated by the US and the UK, which is the suicide of the European economy. We are not sure that it will be successful, but there is some chance of it, and it seems that Biden and his team are seriously betting on it in terms of raising household incomes and thus offsetting the negative impact of rising prices. In other words, we are not talking about lowering inflation – this is not going to work – but only about compensation, which will allow the Democratic Party not to be thumped by the Republicans in November this year (especially in the case of the Durham investigation). Otherwise, President Biden will be impeached and many of his closest associates imprisoned. The other thing is that, as a result of such policies, both the economic system and the internal confidence go astray.

In general, we can state that the US monetary authorities have recognized their inability to fight inflation (if they believed in the effectiveness of the rate increase, they would raise it faster and more sharply). In addition, they are clearly afraid to shift the structural crisis from an inflationary scenario to a deflationary one (their experience from 1930-32 is much sadder than that of the 1970s). So the overall picture of the crisis will not fundamentally change in the coming months.

Macroeconomics

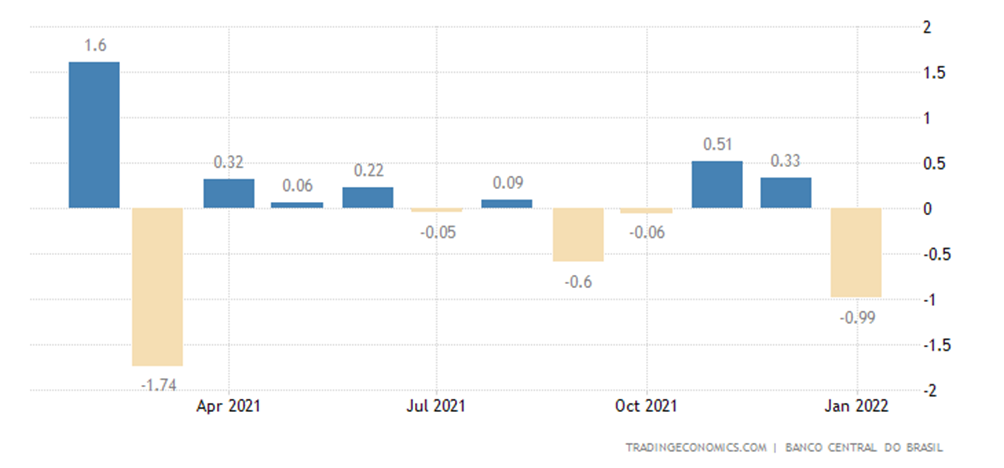

Brazilian GDP in January went into the red zone:

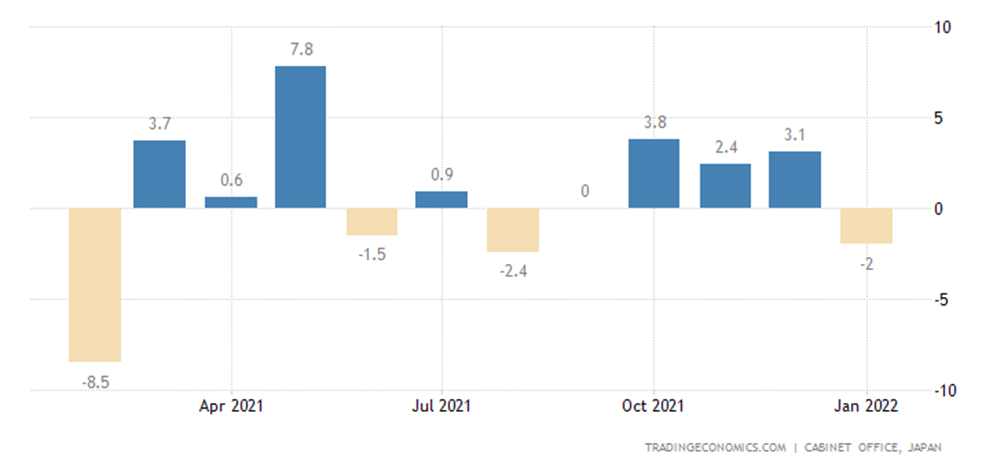

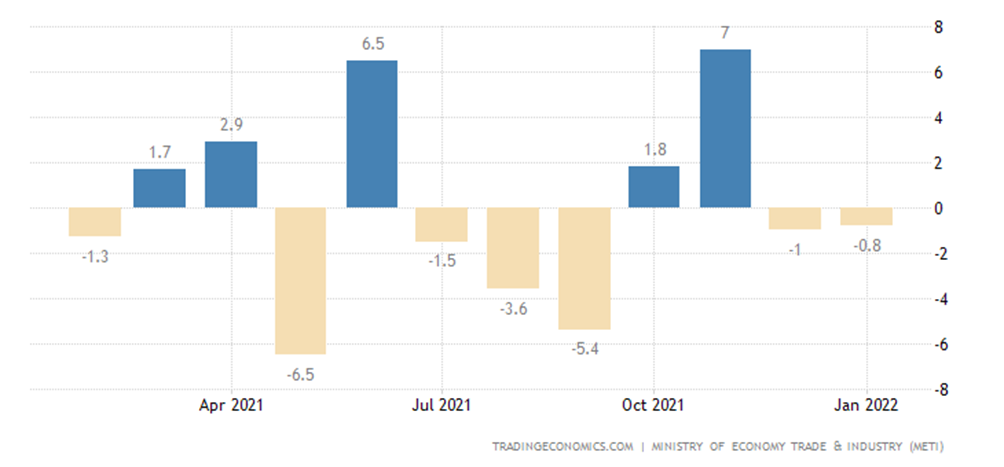

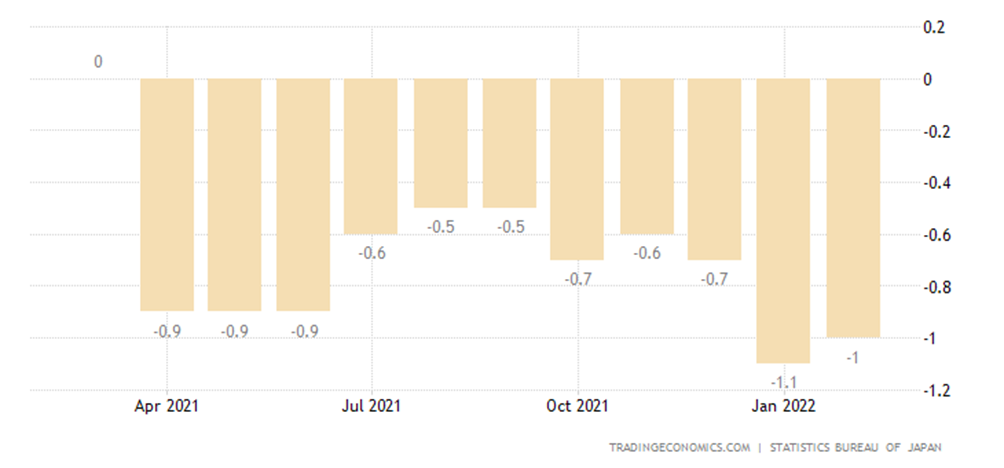

Japan machinery orders amounted to -2.0% m/m:

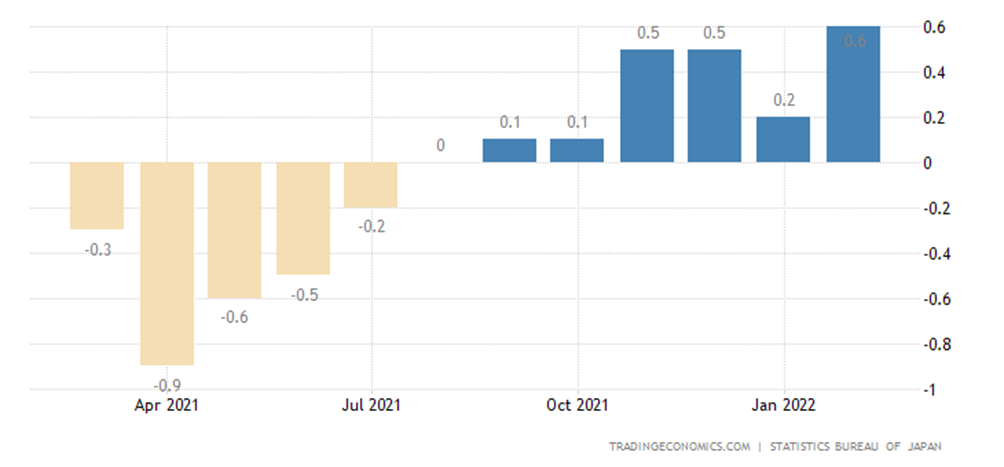

Japanese industrial production has -0.8% per month, 2nd straight negative:

And -0.5% per year:

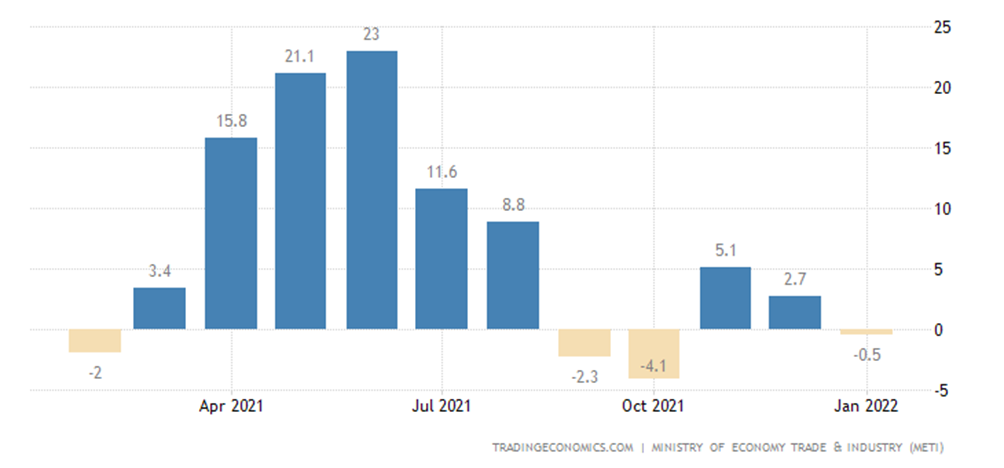

The Euro Area industrial output is -1.3% per year:

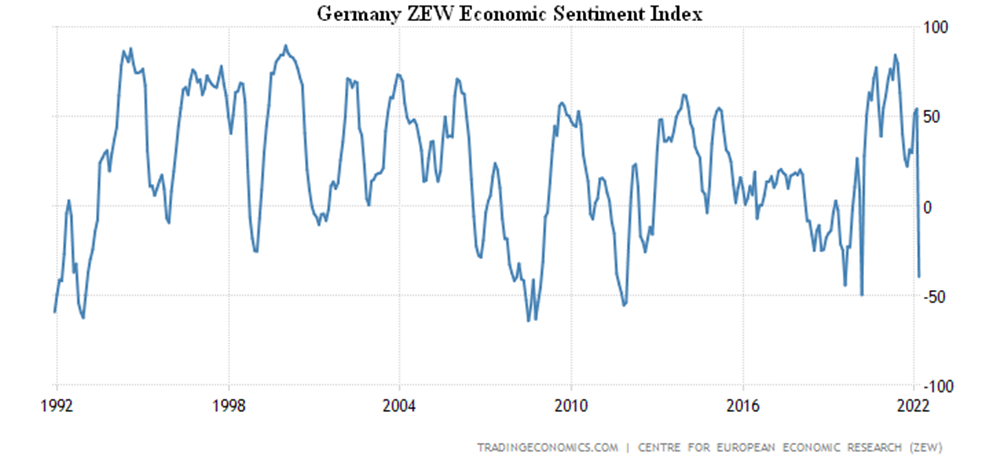

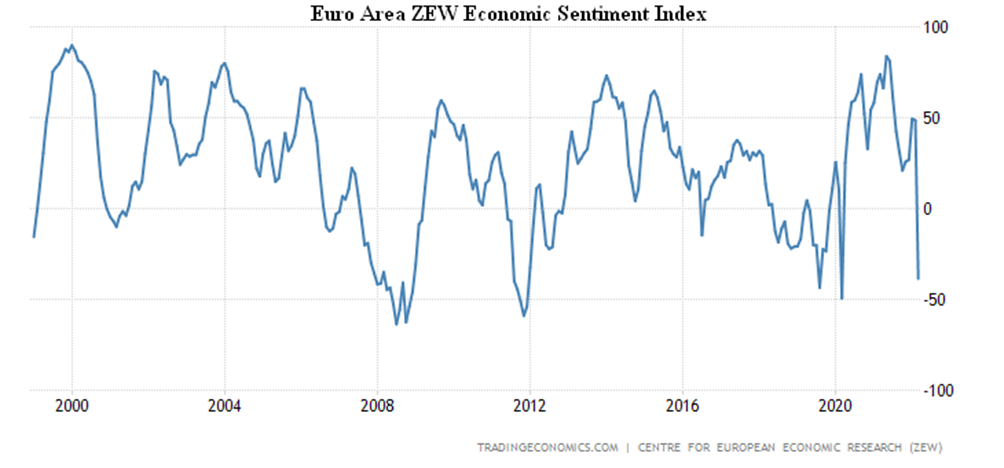

Germany’s economic sentiment from ZEW fell at most in the history of survey to the worst since March 2020:

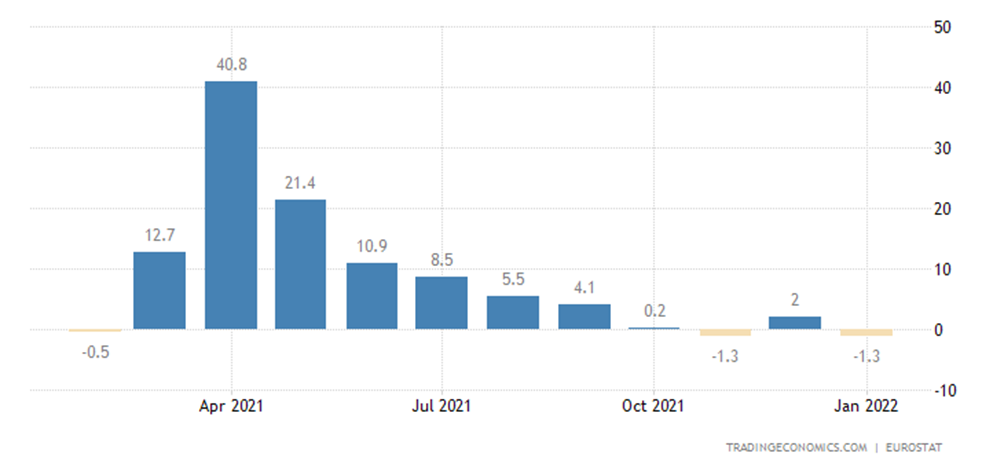

The same in the Euro Area as a whole:

Business confidence in Brazil is at an 11-month trough:

Australia Leading Economic Index was -0.2% per month:

Sales of new buildings in Australia returned to the lows of previous years and showed -7.0% per month after -8.3% before:

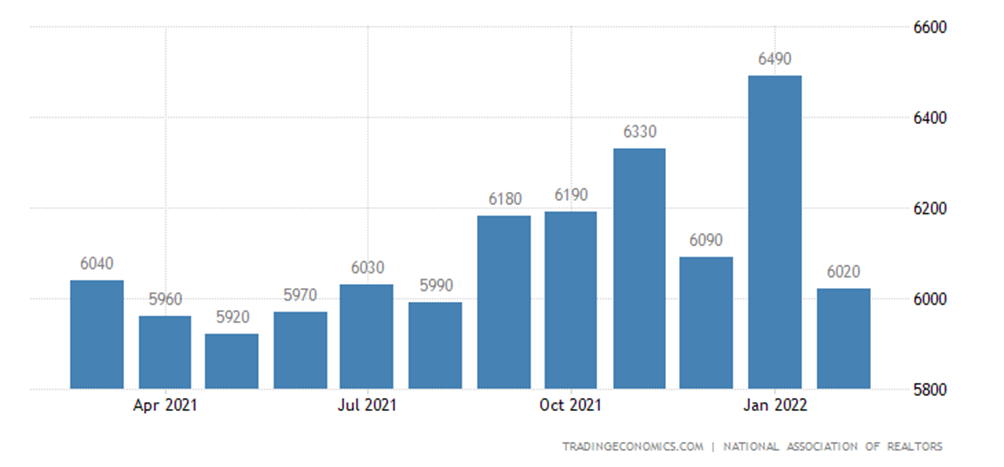

US existing home sales were -7.2% per month and slumped to a six-month low:

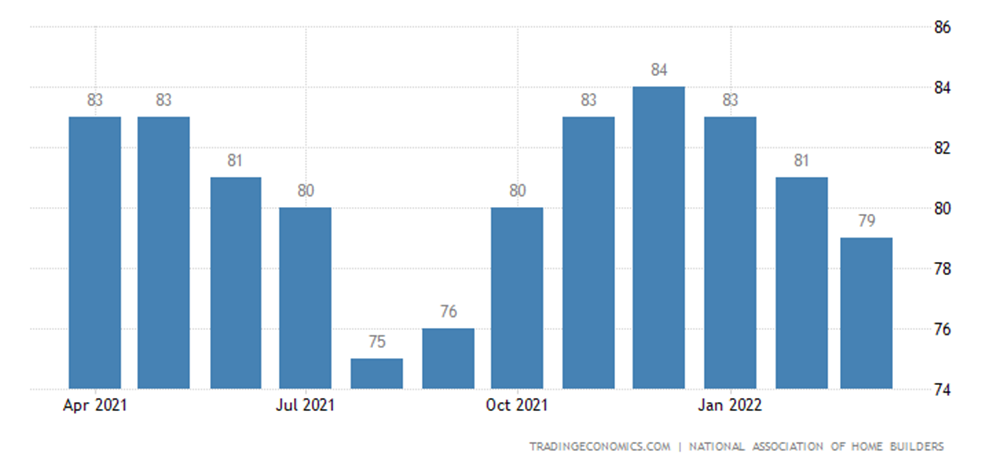

United States Nahb Housing Market Index is the weakest in six months (although high by historical standards):

Then inflationary indicators begin, already usually record-breaking.

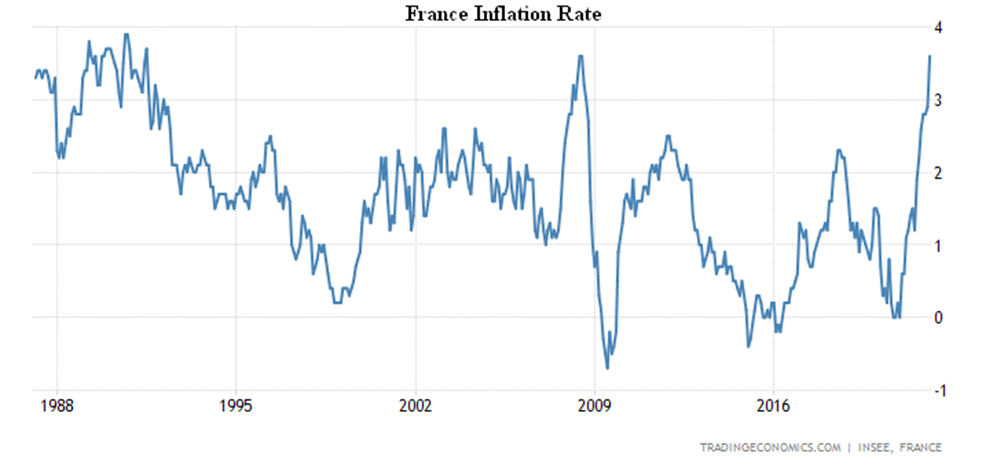

CPI (Consumer Price Index) of France was +3.6% per year and repeated the 30-year high:

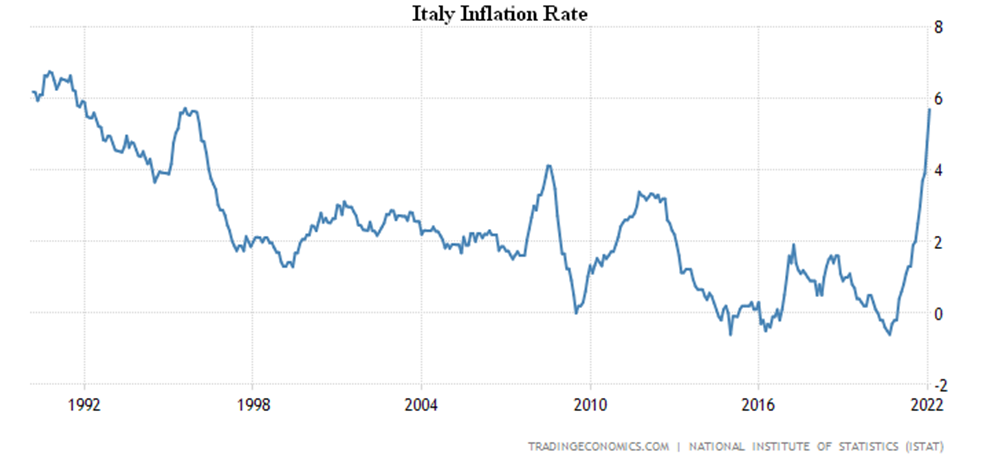

CPI Italy +5.7% per year, that is also a 30-year peak:

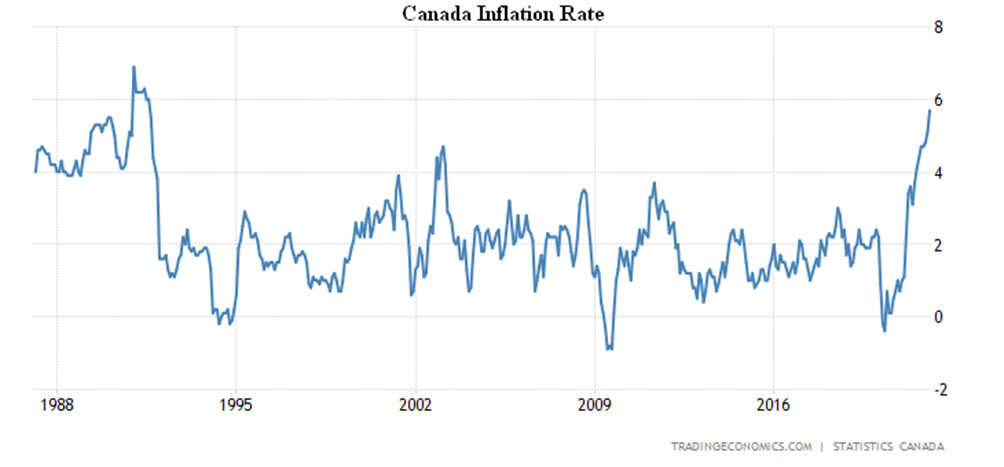

Canada’s CPI is also 5.7% per year, and there is its highest in 30 years:

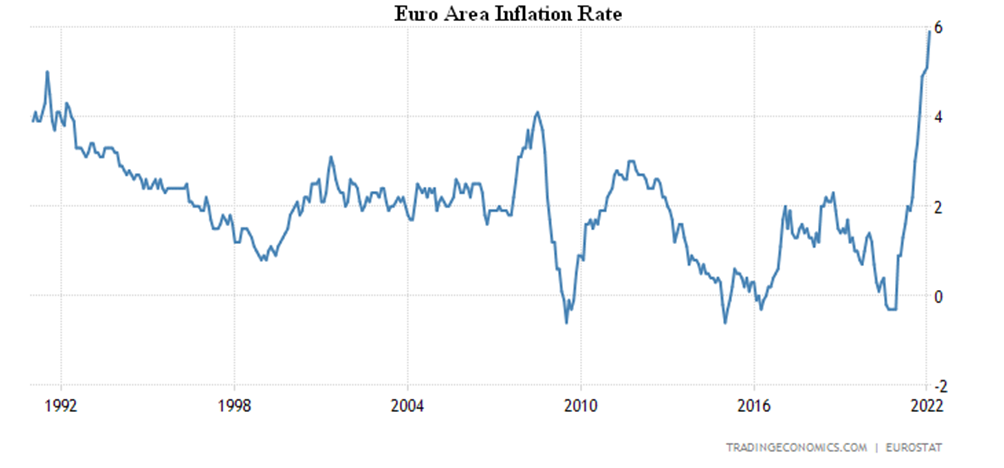

The Euro Area CPI was +5.9% y/y, hitting a record high in 31 years of observation:

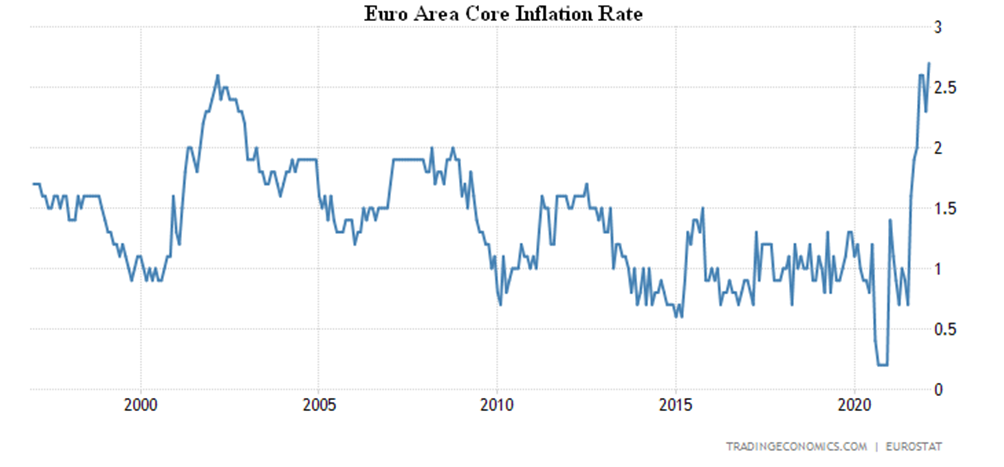

The rate of core inflation, that is, excluding highly volatile components, is also a record (+2.7%):

Japan CPI +0.9% per year, this is a 3-year high:

Without fresh food +0.6%, which is a 2-year high:

But if fuel is also excluded, it will be -1.0%, which is quite close to record deflation:

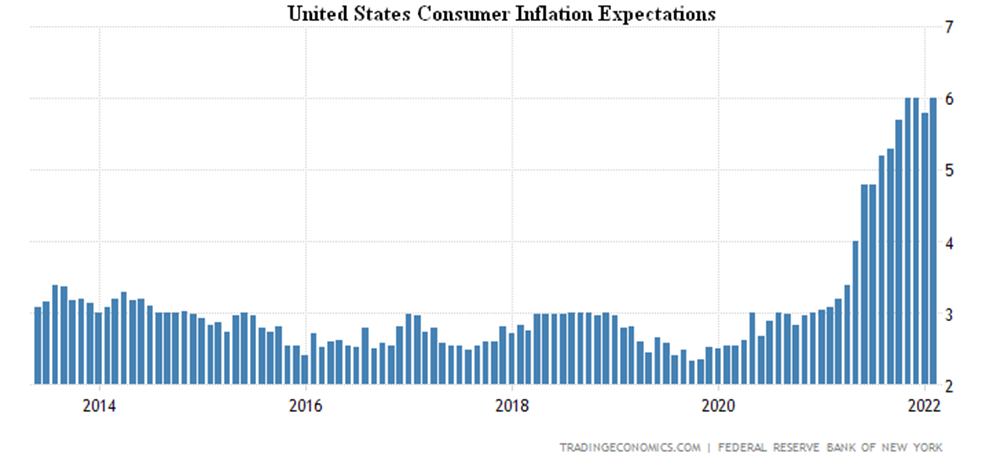

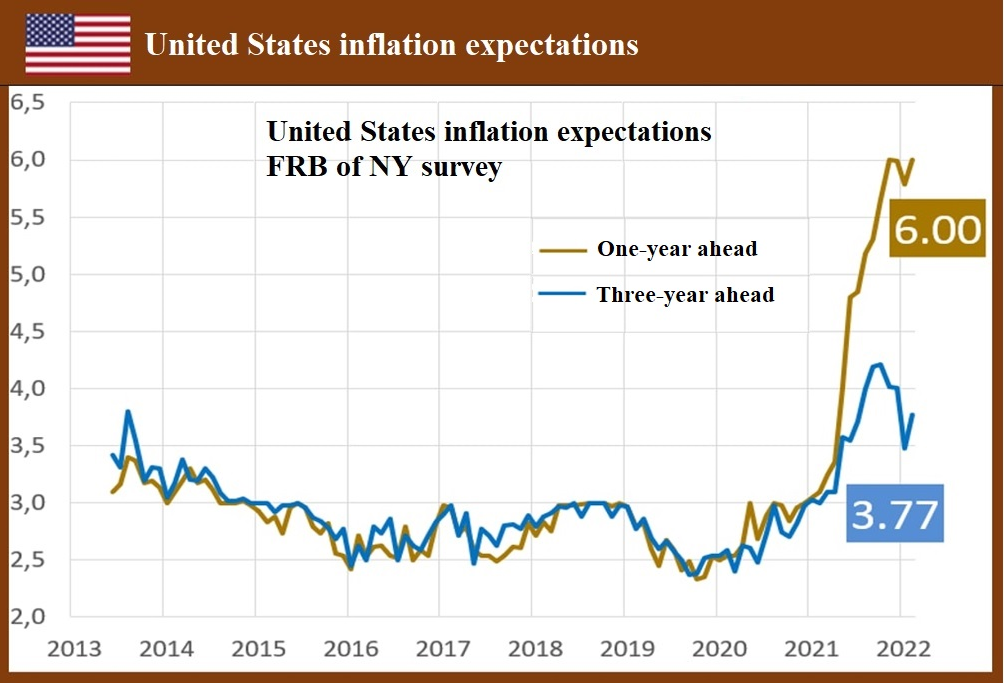

US consumer inflation expectations returned to a record +6.0% y/y:

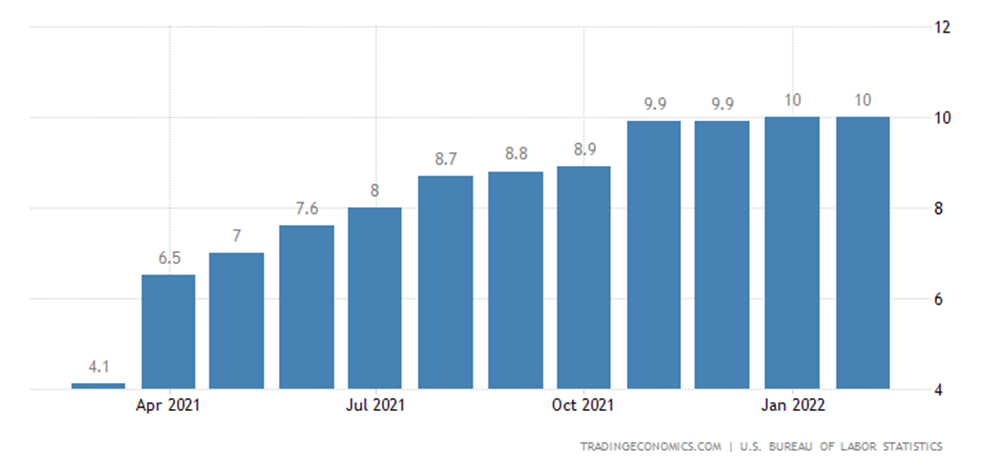

PPI (Producer Price Index) US +10.0% per year, the highest since 1981:

The prices of finished goods less food and energy +7.7% per year, which is also the peak since 1981:

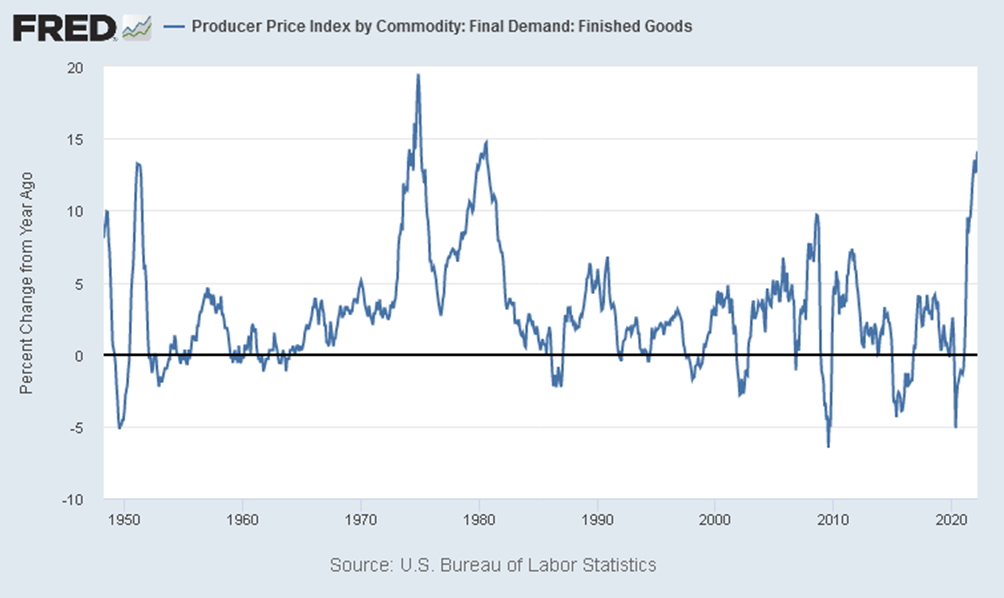

And in general, for goods of final demand +14.1% per year, the peak since 1980:

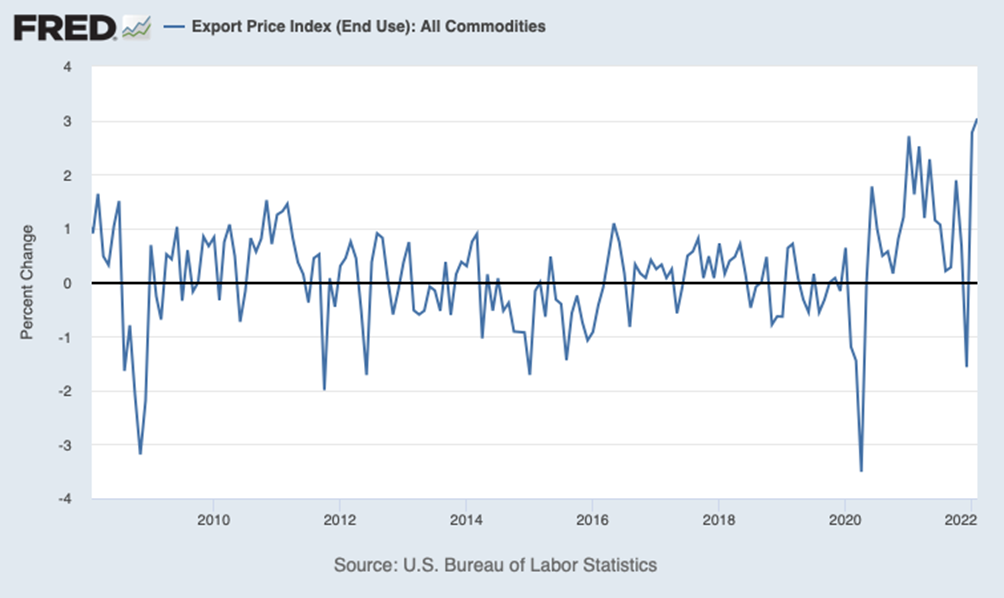

Export prices to the US +3.0% per month, unprecedented skyrocketing over 33 years of observation:

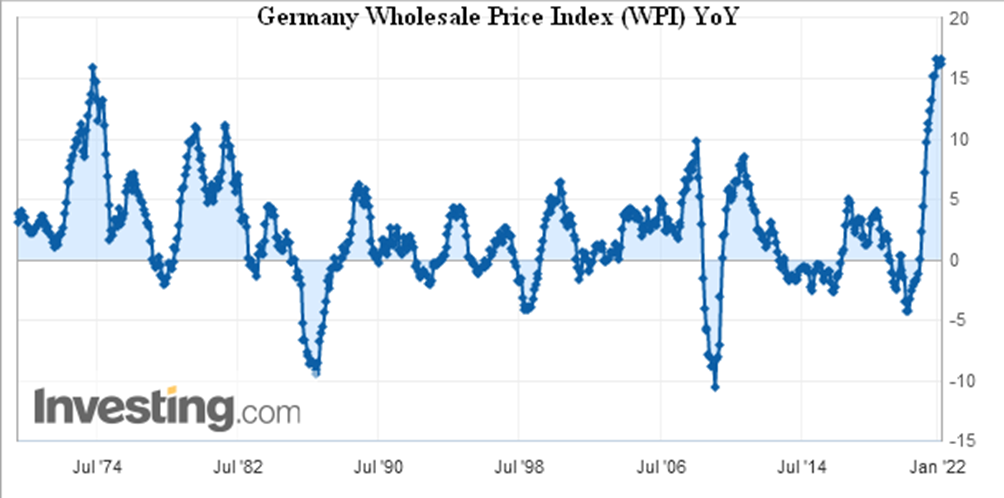

Wholesale prices in Germany +16.6% per year, repeating the record for 52 years of statistics:

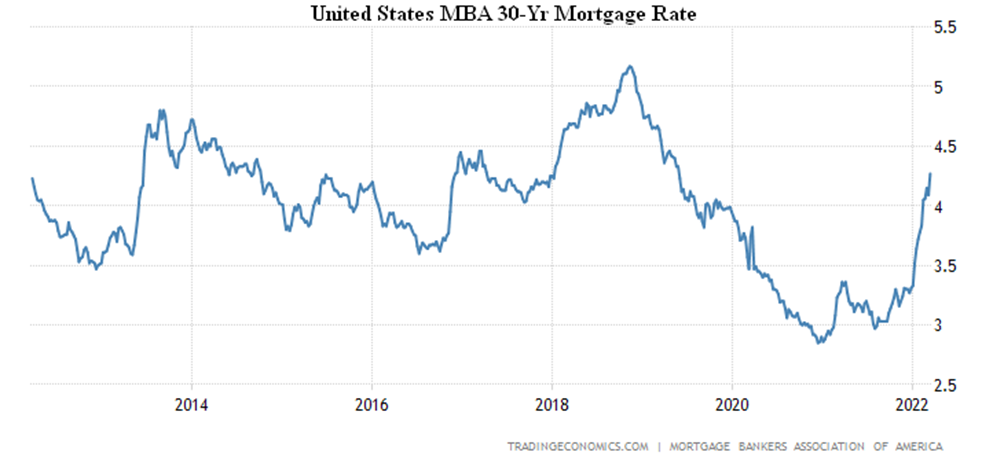

Mortgage rate in the US is the highest in 3 years:

As well as 10-year government bond yields:

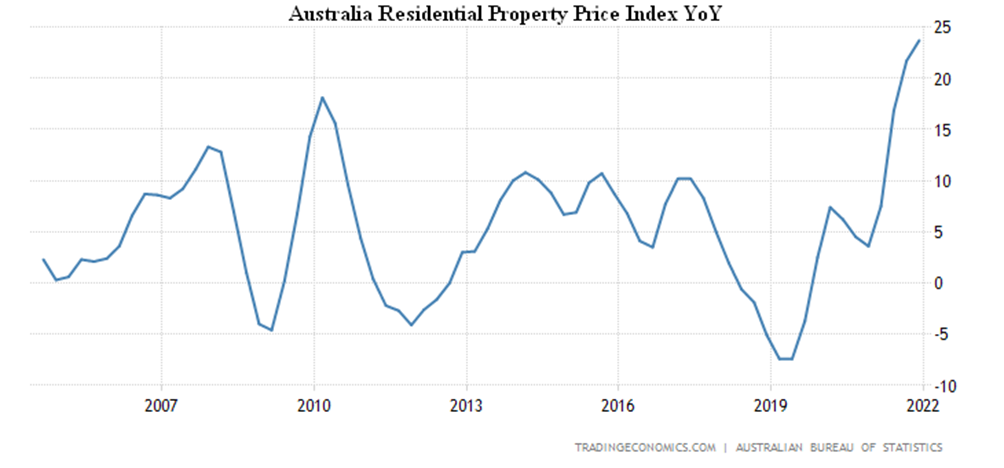

Housing prices in Australia are +23.7% per year, the highest in 18 years of survey:

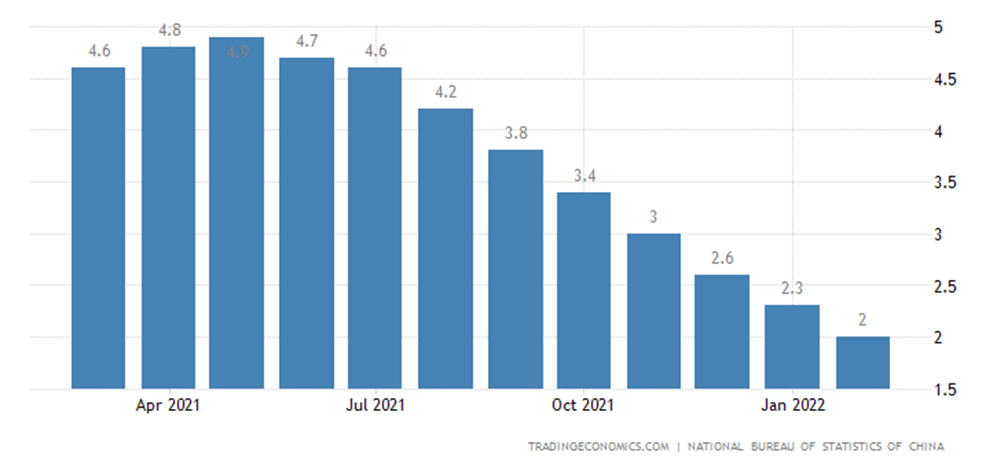

Housing prices in the 70 largest cities of China +2.0% per year, the lowest since 2015:

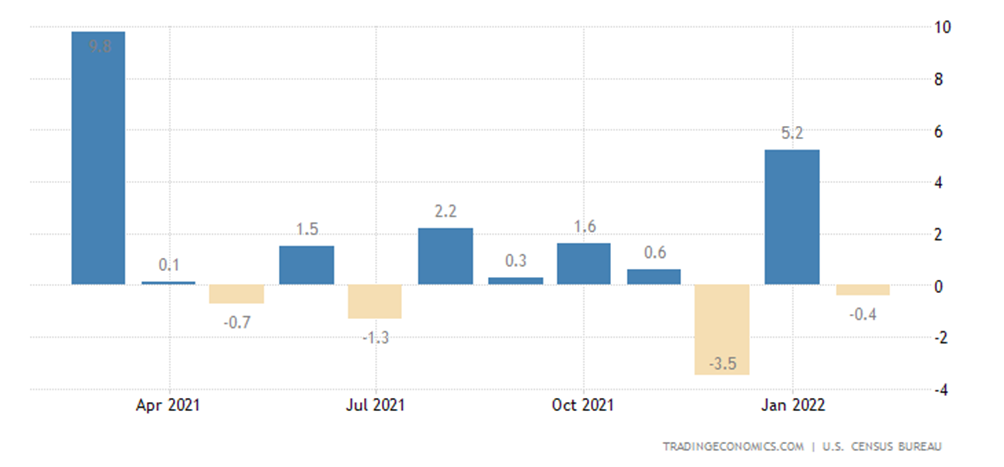

Retail sales in the US excluding gas and autos -0.4% m/m (and this is still a nominal value, without inflation):

Retail sales in Spain -0.3% per month, the second negative in a row:

The US Federal Reserve raised the rate by 0.25%, we mentioned this in the first section of the Review.

The Bank of England raised interest rates by 0.25% to 0.75%.

The Saudi Arabian Central Bank also began tightening its policy; and the Brazilian Central Bank initiated it long ago, and now another 1.00% to 11.75%.

The Central Bank of Indonesia left everything unchanged, and the Central Bank of Turkey, the Bank of Russia and the Bank of Japan followed suit.

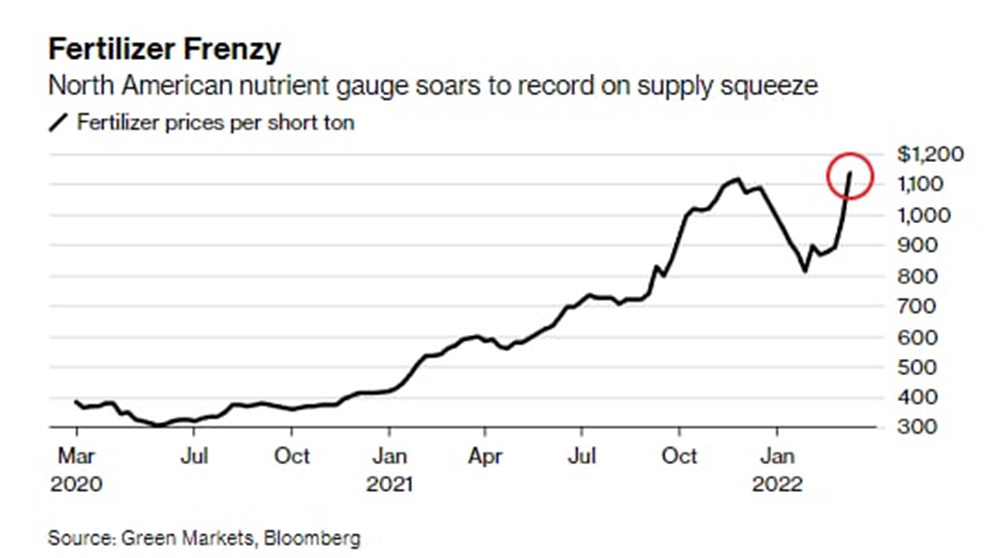

Summary. The structural crisis in the world economy is deepening and is already clearly being exacerbated by the sanctions war. In addition to the basic macroeconomic indicators, we can provide data on nutrients (already in March, that is, after the announcement of anti-Russian sanctions):

Additional statistics on US inflation expectations:

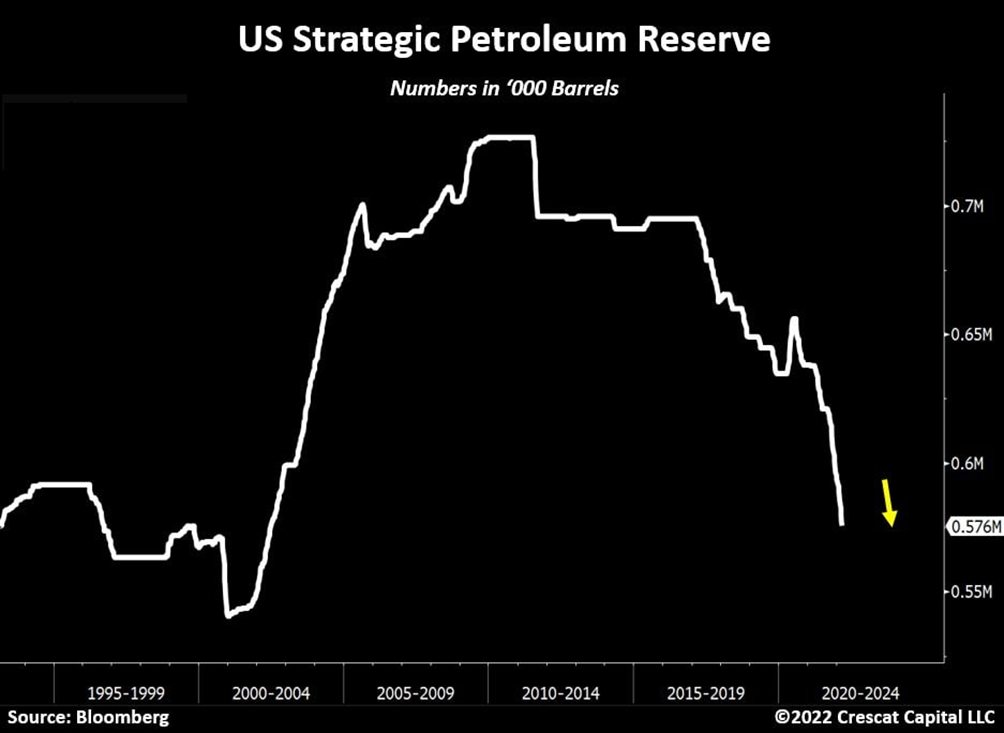

At the same time, titanic efforts to stop the rise in oil prices have not brought much fruit, and the main oil exporters from the Persian Gulf countries do not intend to take into account the arguments of the US:

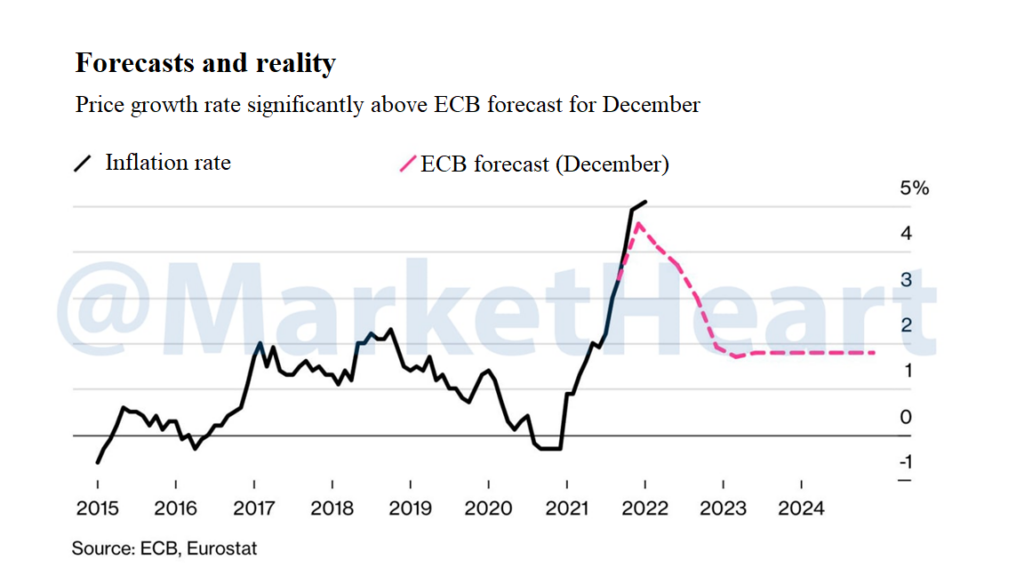

This is no longer surprising, the official authorities of the European Union (we already wrote about the US in the first section) were clearly not ready for such a scenario:

How they came to such conclusions, a separate question, the forecasts of the Mikhail Khazin Economic Research Foundation have long spoken about the growth of inflation. Actually, readers of our reviews are well aware of this, however, optimism is a good thing, another thing, that frankly deceive your readers is very bad. However, we can only say here that reading our reviews is more useful than reading Eurostat and/or Bloomberg’s estimates.

In any case, the final conclusion to be drawn from the results of recent weeks is that the sanctions war has catalyzed negative processes in the world economy and it will not be possible to stop them, even by lifting the sanctions. On the other hand, they are likely to be significantly inhibited, that is, it is theoretically possible to gain time for carrying out compensatory measures. However, for this you should study our reviews, and not the official presentations of state and related structures.

We wish all readers a peaceful working week!