Period: 2 – 8 January 2021

Top news story: Undoubtedly, storming the Capitol cannot be considered major economic news. The reasons are, its not clear who organized it, and it didn’t affect economic performance. This by itself testifies that from the point of view of business entities, this incident does not play a leading role.

The fundamentals are different: the very circumstances that made this assault possible suggest that the system of managing world stability, including economic stability, has virtually ceased to exist. There can be a long debate about how this system was designed and who might have influenced it, but its very existence is beyond question. It is another matter that the creators of this system are long dead, and the system itself has become so complex that there is no certainty that there are people who, if not capable of managing it, but just imagine its structure in a more or less complete portrait.

Despite the fact that there are specialists in certain details, but they are no longer able to coordinate their steps. Roughly speaking, you can lower unemployment, you can raise the stock market, you can lower emissions… However, it is not possible to take these measures at once. In particular, economic growth has not been achieved throughout the world economy. Naturally, US policy is irritating around the world. After all, the economy is still built on the basis of the US dollar, added value is formed directly in the dollar, it is also GDP.

It should be understood that the problem of choosing between D. Trump and J. Biden is a choice between two negative scenarios. Simply because none of them offers a constructive version of the course of events. The Mikhail Khazin Foundation for Economic Research has elaborated this topic many times, the most complete version is presented here.

Now we will not repeat what we said before. However, avoiding a severe collapse of the American economy, more severe than in 1930-32, is likely to be impossible. The only question is what scenario the recession will follow.

Our analysis presented in M. Khazin’s book «Reminiscences about the Future» indicate that the USA has started a structural crisis similar to the mentioned recession of 1930-32. And the economy will not be able to get off this track, regardless of the policy option.

Macroeconomics

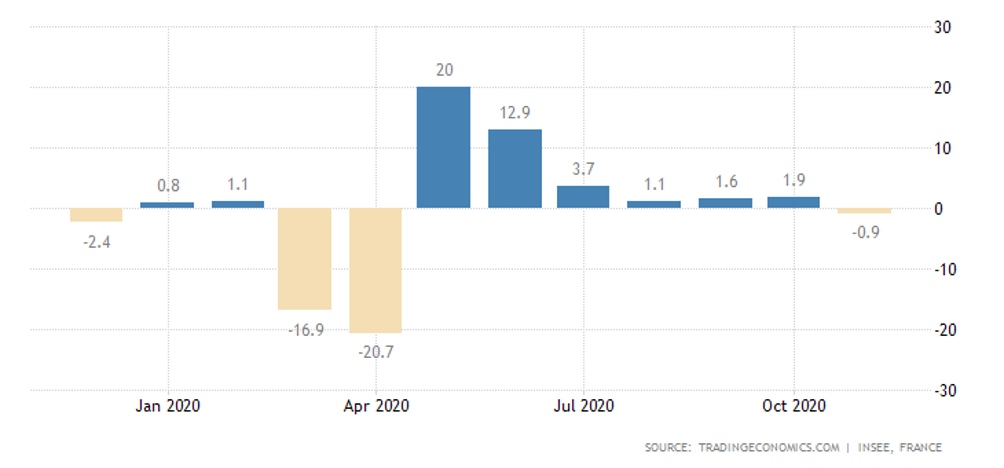

Industrial production in France slumped by 0,9% in November:

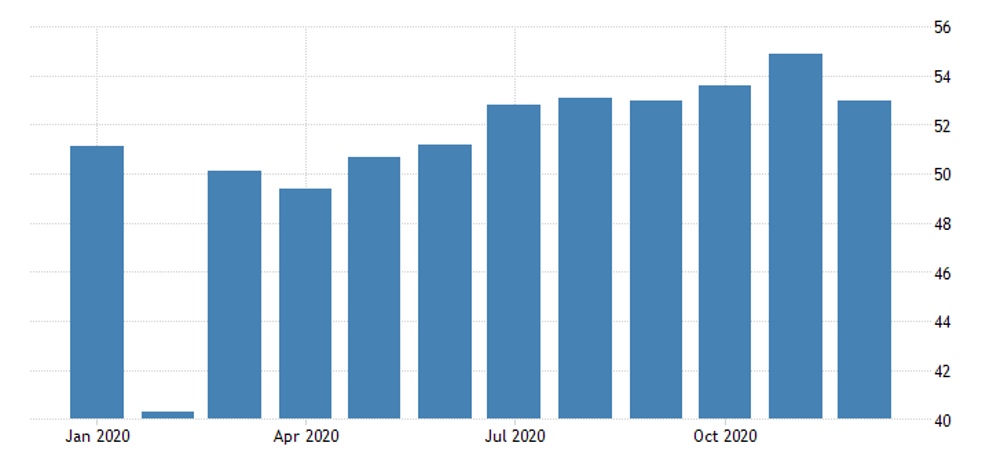

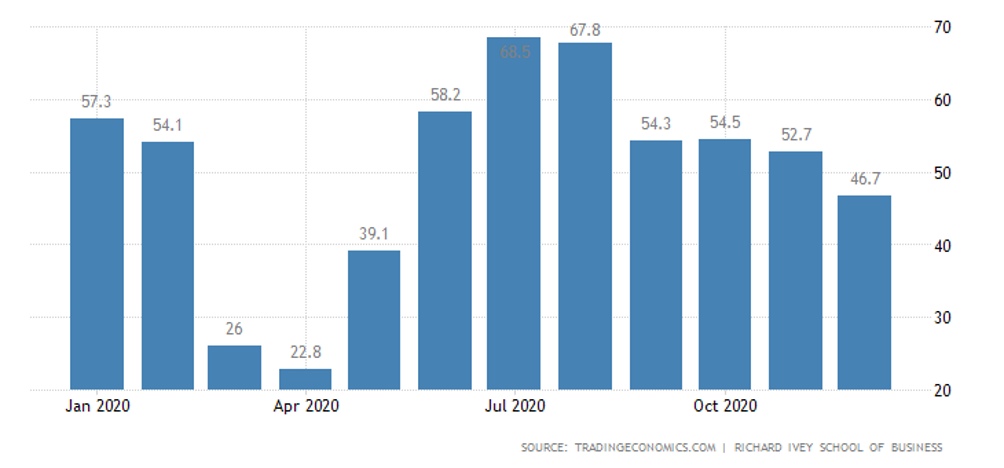

China’s manufacturing PMI slowed down slightly:

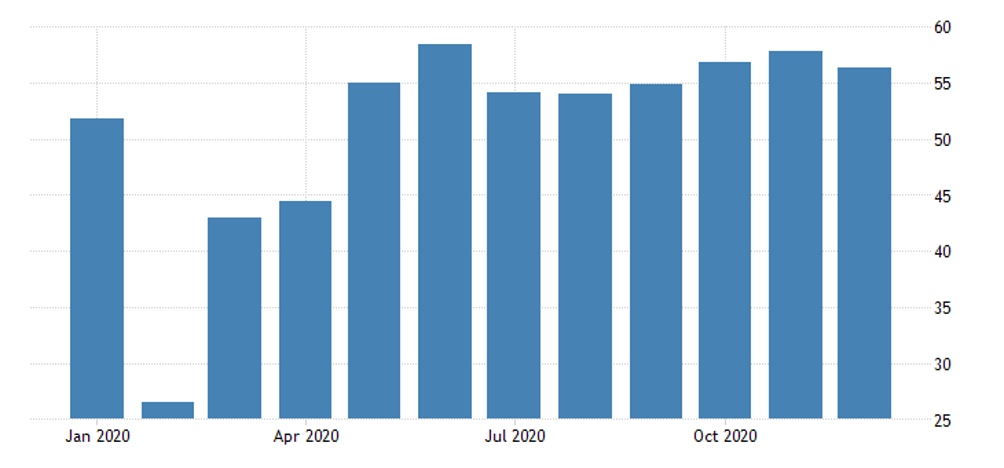

As in the service sector:

Let us recall that PMI is a specially processed measure of the expert assessment of the state of an industry (or a group of industries), if its value is less than 50, then there is a decline if more – on the contrary. In their assessments, however, the experts are highly dependent on (and sometimes attempt to shape) the market sentiment of the relevant market participants, which should be taken into account when assessing this parameter, especially if it is around 50.

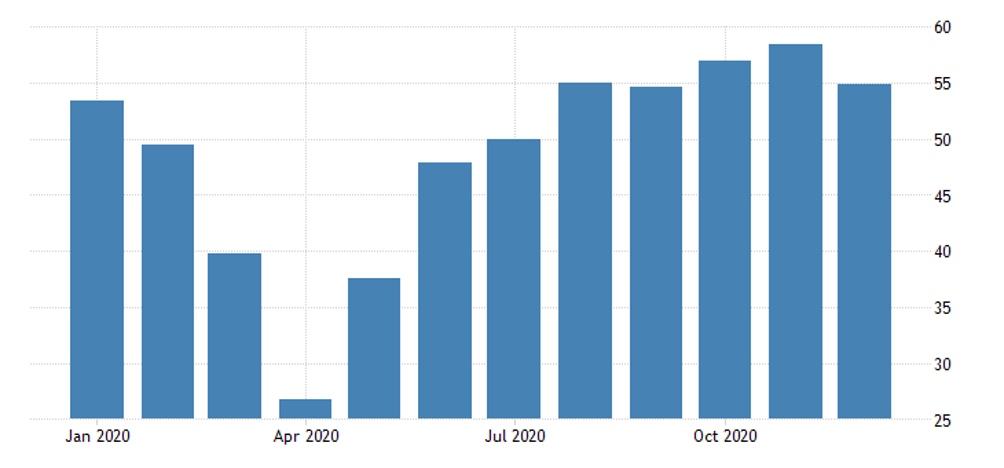

The latter figure also declined in the US:

Canada’s PMI (across all industries) returned to recession for the first time in seven months:

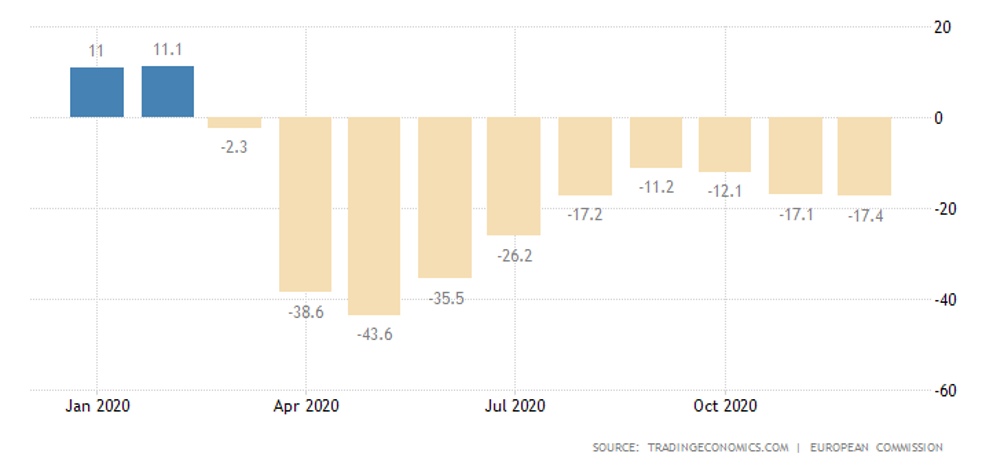

Similar developments in the Euro Area (market sentiment in the sector is the worst in five months):

It’s not PMI, but it’s an identical index.

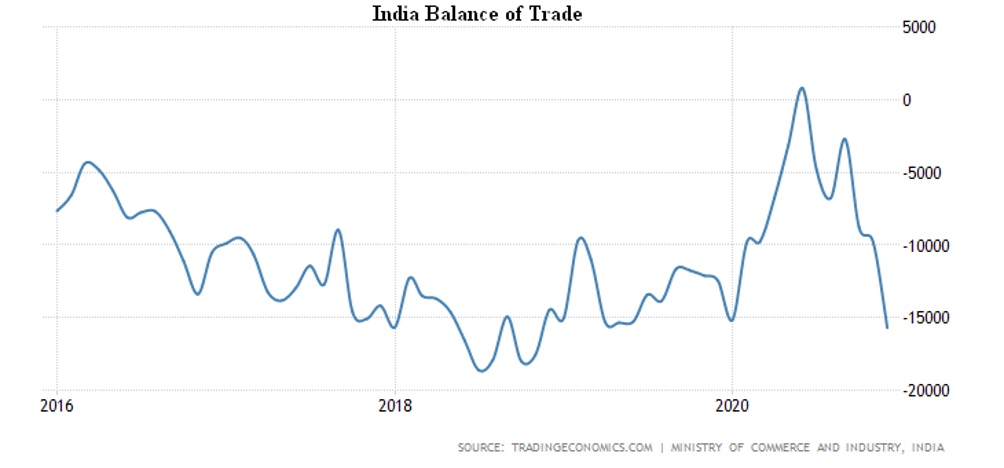

India’s foreign trade deficit in December has been maximal since November 2018:

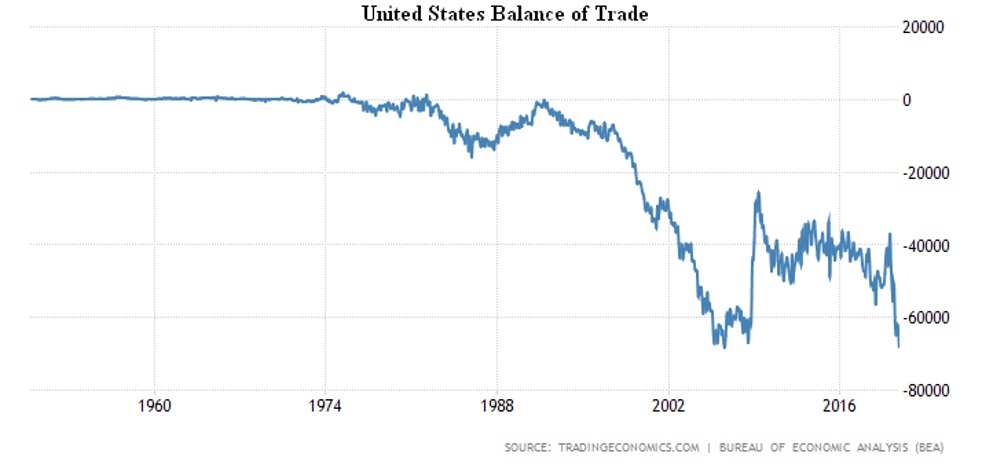

While in the US it almost reached the August 2006 value, the record worst in 71 years of observation:

Oil reserves in the United States have been declining for four consecutive weeks. At the same time, oil prices rose to their annual maximum (Brent about $55 per barrel).

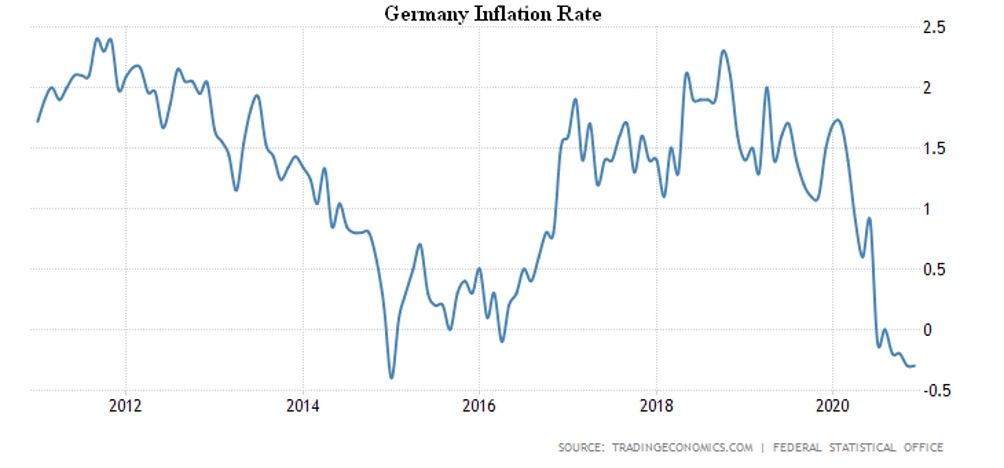

The CPI (Consumer Price Index) of France has returned to the trough in five years (0,0% per year). And German CPI – in 6 years (-0,3%) and only 0,1% of the trough since 1986:

As in the Euro Area as a whole (also -0,3%).

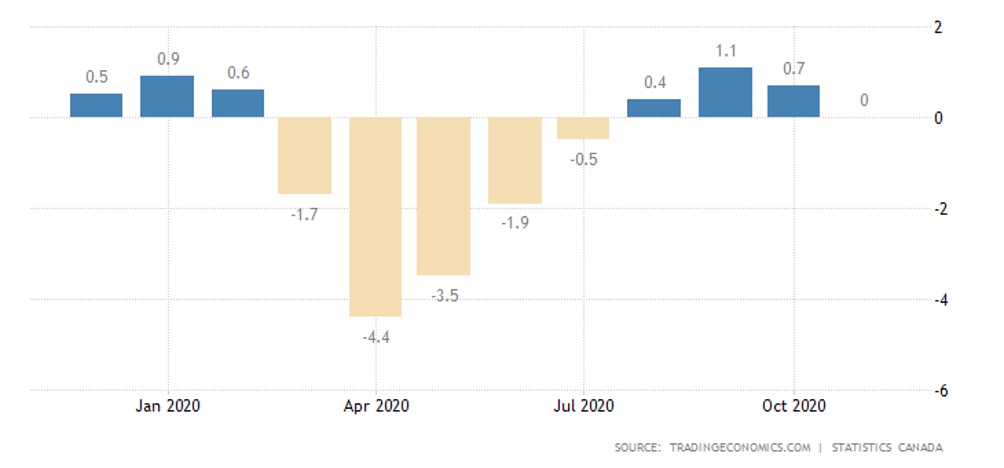

Canada’s PPI (The Producer Price Index) is minimal for 4 months (0,0% per year):

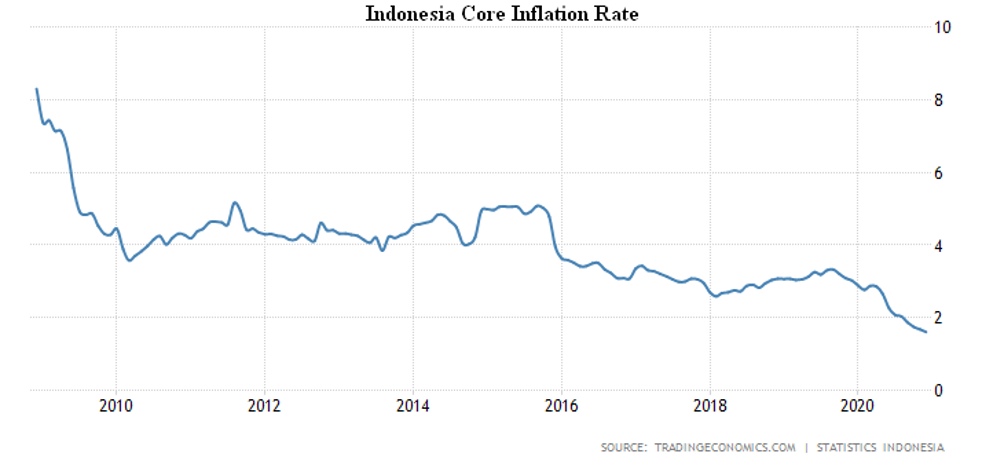

Indonesia’s net CPI is the weakest in its history (+1,6% per year):

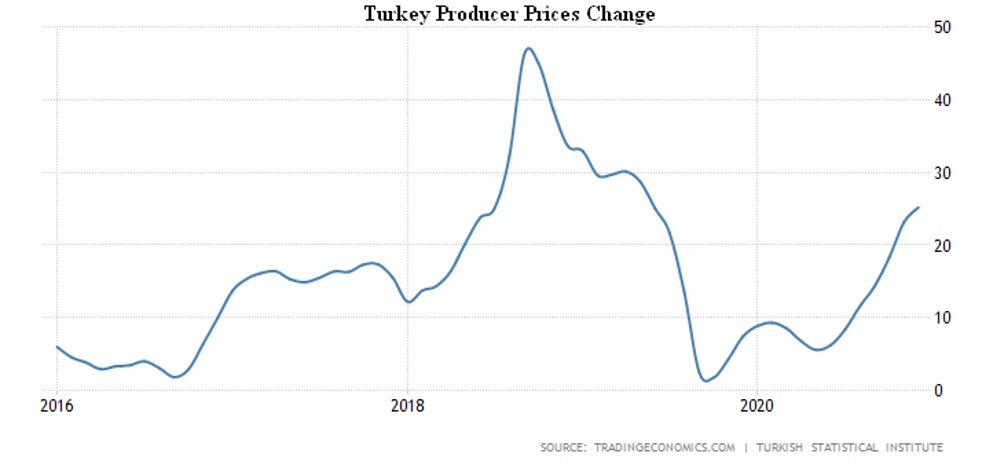

In Turkey, however, the CPI peaked in August 2019 and the PPI in May 2019:

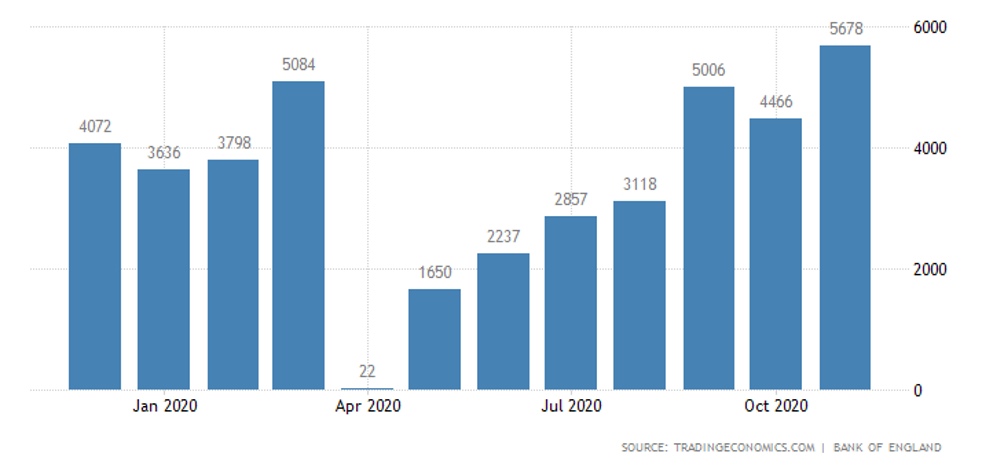

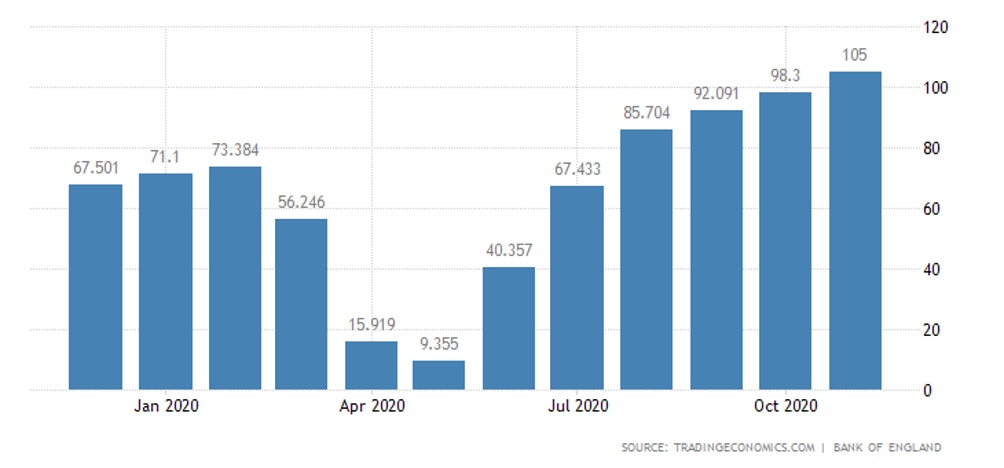

Consumer lending in Britain is the weakest in six months, despite its record-high five-year mortgage:

Meanwhile, mortgages continue to rise, and the number of approved mortgage claims in Britain has peaked since August 2007:

Japanese wages in November are -2,2% per year, which is almost the same as the May minimum (-2,3%) and approaching their lowest levels in 11 years.

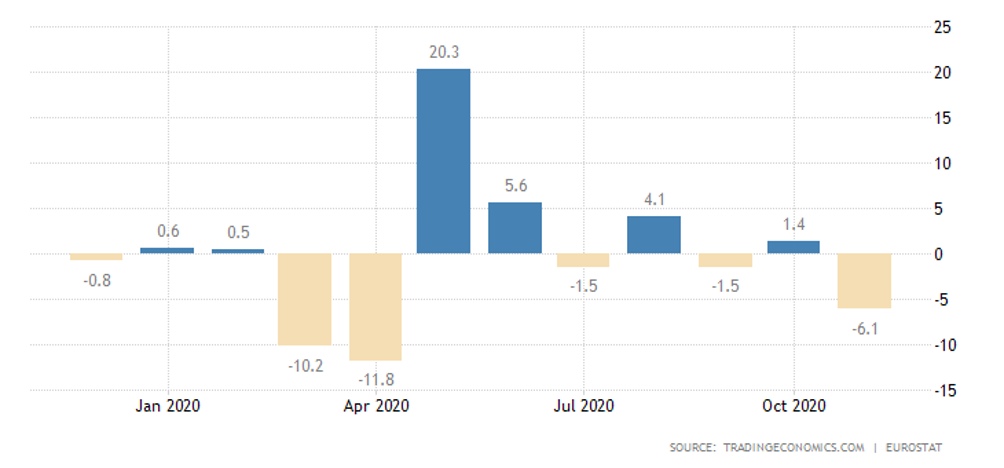

The Euro Area retail sales collapsed at 6,1% per month in November:

As a result, its annual performance was the worst in seven months (-2,9%).

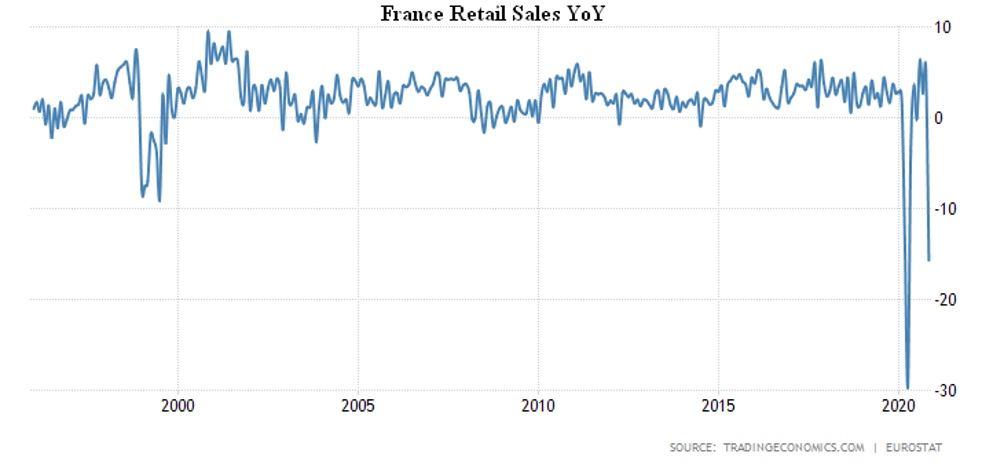

But, in this sense, the Euro Area is far behind France, where the monthly recession (-18,0%) surpassed even the April figure, with the annual recession reaching -15.7%.

Household spending in France dropped to -18,9% per year in November, lower than the April historical anti-record (-18.7%):

Unemployment in Germany remains at its 5-year peak:

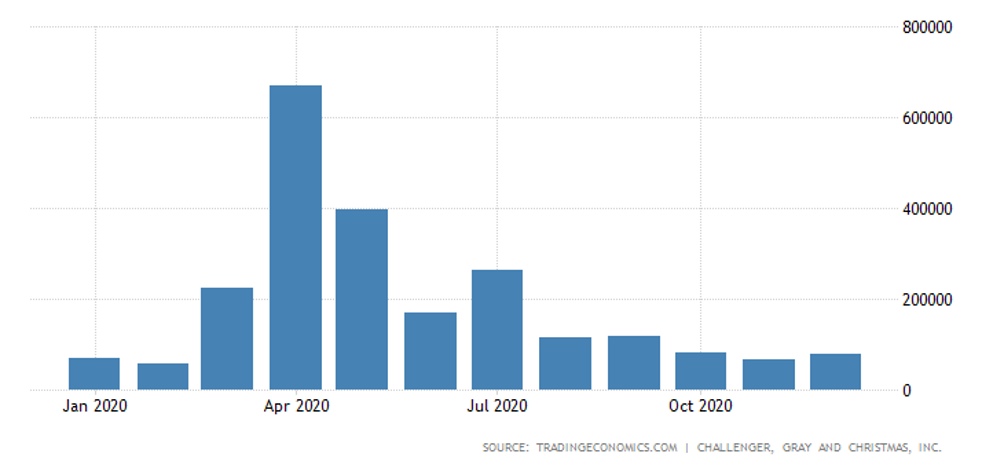

More announced job cuts in the US again:

United States Challenger Job Cuts

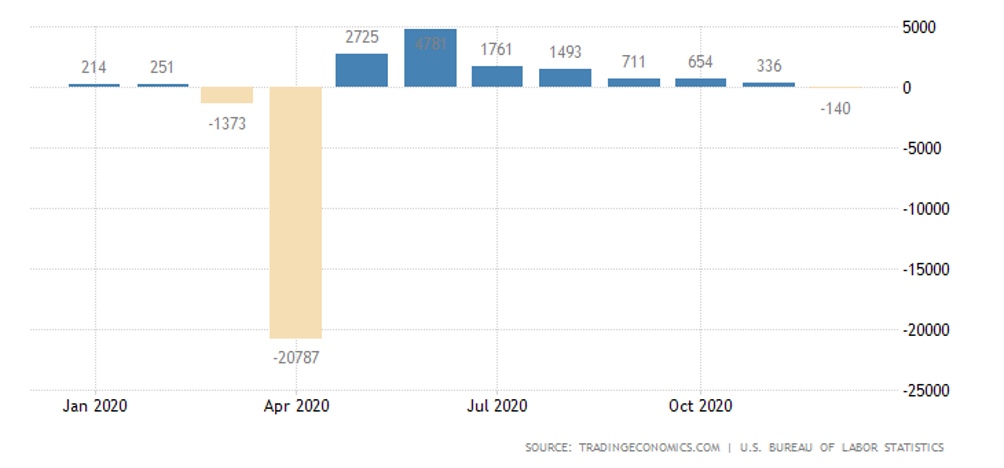

Employment in the US private sector (according to the ADP survey) declined in December for the first time since April, and in a Department of Labor report, employment fell for the first time since April:

From the minutes of FED, it appears that it intends to continue actively printing money.

But, with the Democrats winning, new fiscal stimulus and a gradual exit from monetary stimulus are expected – so government bond yields have peaked in 10 months:

Summary: Once the structural crisis has begun, it is almost impossible to stop it. The crisis can be halted by emissions, but this will inevitably lead to a crisis that will eventually resurface, only on an even larger scale. If in 2008 the structural crisis should have led to a 50% drop in US GDP, today the situation is different.

The official GDP of the US today is between $21 and $22 trillion. But this amount is due to the fact that the increase in the value of financial assets through emissions is rewritten into the increase in value added by purely accounting methods. Indeed, US GDP is about $14-15 trillion, slightly less than China’s GDP, which is about 16 trillion, with the same stimulus. And as a result, the equilibrium level of GDP will be U.S. $7-7,5 trillion after the crisis. But, relative to the current value, that actually means a threefold reduction.

This is, of course, the final point to be reached in the next few years. But the scale of the process is enormous, and it is not possible to hope that the basic economic model of recent decades will be maintained in the world.