November 25 – December 1, 2023

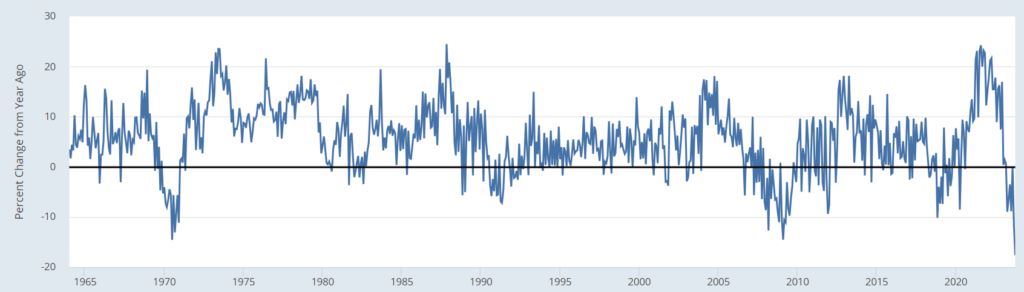

Big news. There are no sensations in pure economics. More precisely, there is no news that would show any clear picture, but there is a continuation of current trends. As a kind of palliative, we can mention the record collapse in prices of new buildings in the United States, which amounted to -17.6% per year – a record decline for all 60 years of data collection:

Рис. 1

But one important symbolic event has happened this week: on November 29, at the age of 101, Henry Kissinger, who in the 70s of the last century made titanic efforts to lure China to the side of the United States against the USSR, died.

Then this operation ended in success (give or take), today this economic model is completely dying, the USA and China are on the verge of a fierce confrontation for the markets of Southeast Asia and recovery is no longer possible. This is an extremely difficult situation for the whole world, including because the United States and China together account for more than 40% of the world economy. And while they worked in unison, it was completely impossible to cope with them. Today the situation has changed.

This creates problems for both the US and China. The latter multiplied its economy through American demand, the former saved money for the development of a high-tech economy by replacing national consumer goods with Chinese ones. Today they are faced with extremely difficult tasks, and there is no simple solution to them. In addition, the inevitable decline in living standards in both countries will lead to serious socio-political changes, for which their elites, in general, are also not very ready.

This creates problems for both the US and China. The latter multiplied its economy through American demand, the former saved money for the development of a high-tech economy by replacing national consumer goods with Chinese ones. Today they are faced with extremely difficult tasks, and there is no simple solution to them. In addition, the inevitable decline in living standards in both countries will lead to serious socio-political changes, for which their elites, in general, are also not very ready.

In general, Kissinger’s death coincided with the end of the era of struggle against the USSR and the division of its inheritance. Today it is already clear that Russia will return what was lost and this is a completely different era. Which has not yet given birth to its Kissinger.

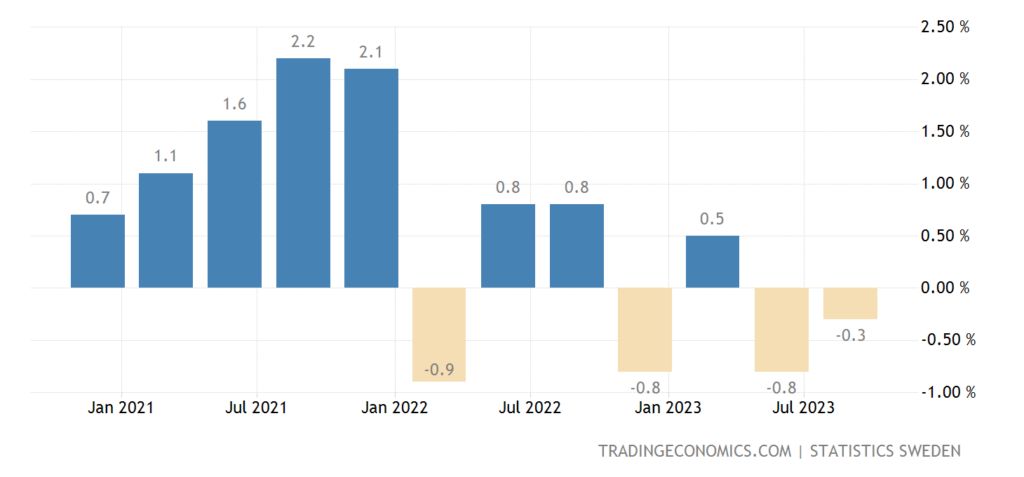

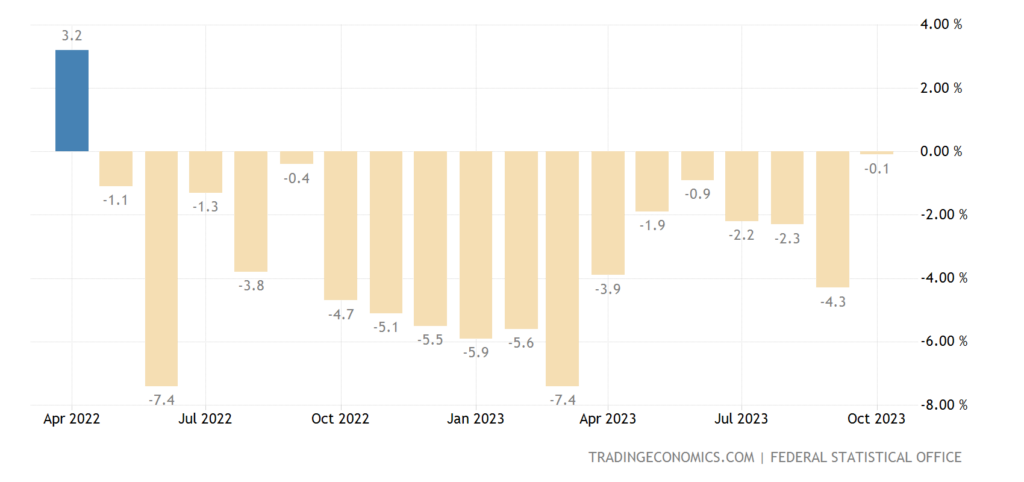

Macroeconomics. Sweden’s GDP is -0.3% per quarter – the 2nd negative in a row. those. formal recession:

Рис. 2

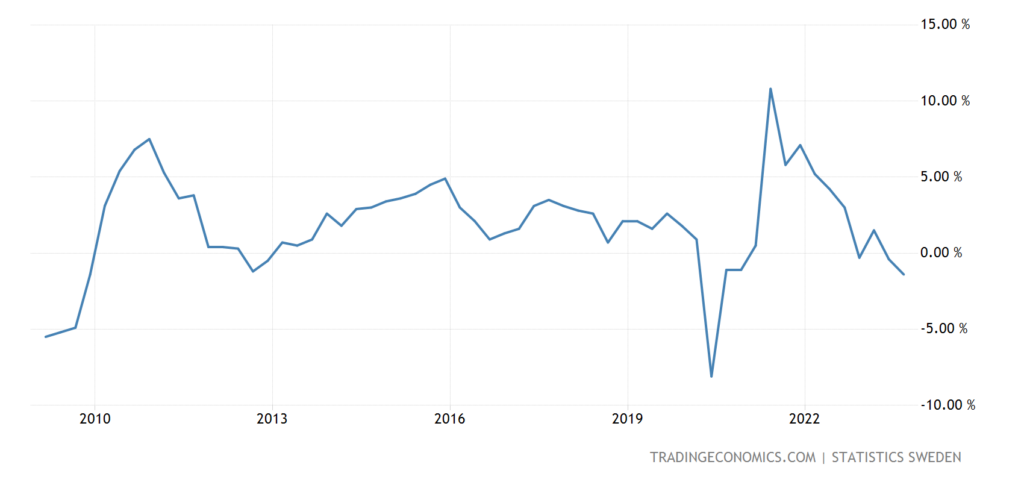

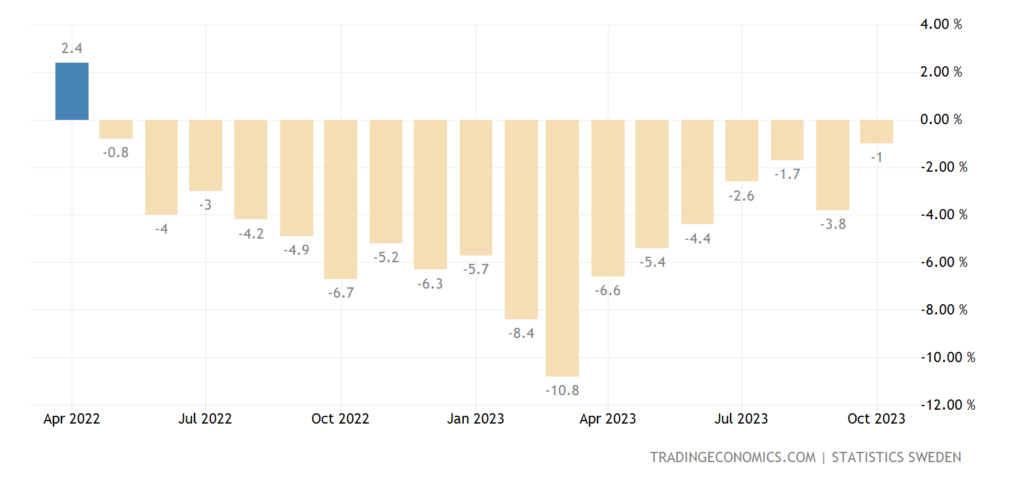

And -1.4% per year – not counting the failure of 2020, this is the bottom since 2009:

Рис. 3

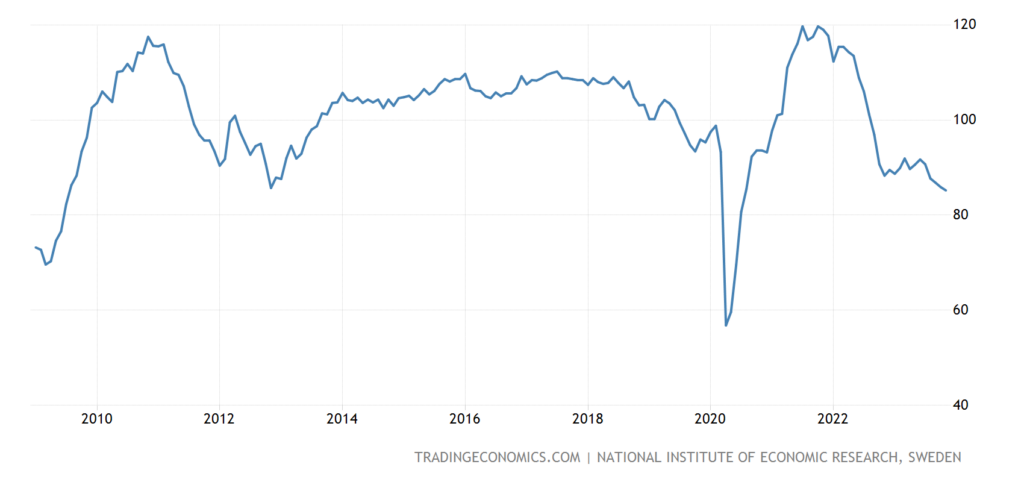

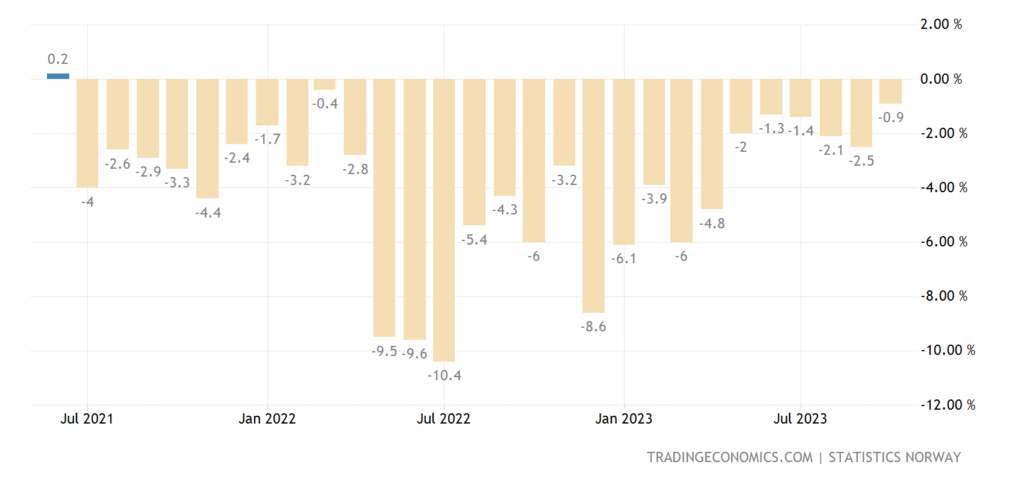

Business confidence in Sweden is also at its lowest since 2009 (excluding 2020):

Рис. 4

Business confidence in Spain has been at its lowest since the summer of 2020, and before that since the beginning of 2014:

Рис. 5

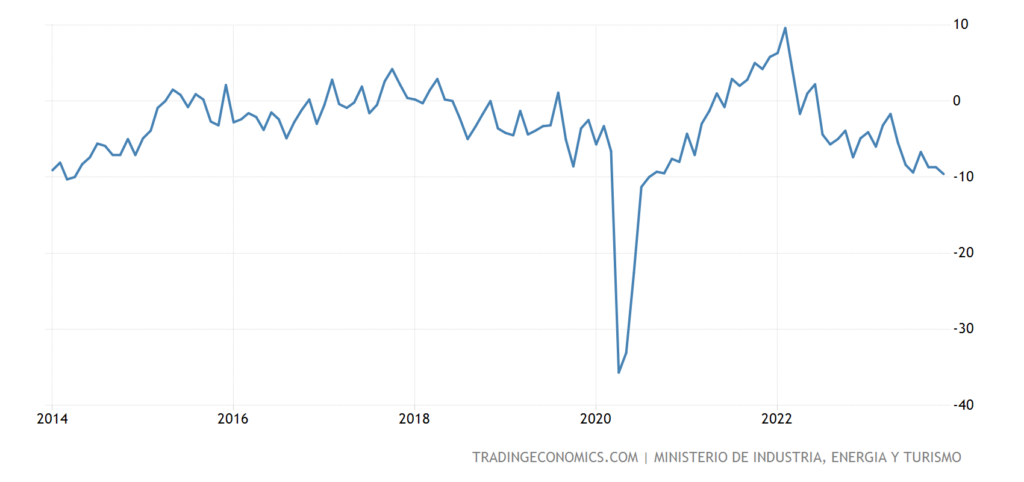

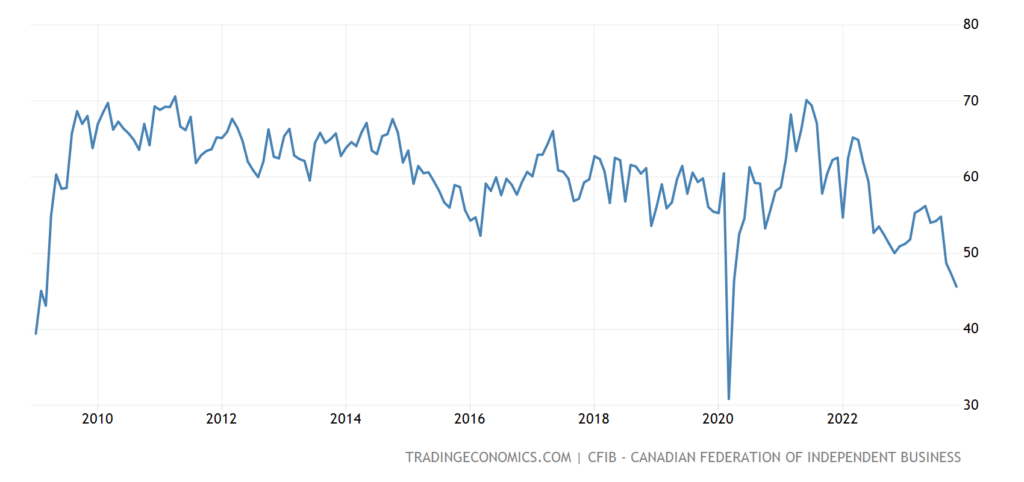

Small business sentiment in Canada is the most pessimistic since 2009 (excluding 2020):

Рис. 6

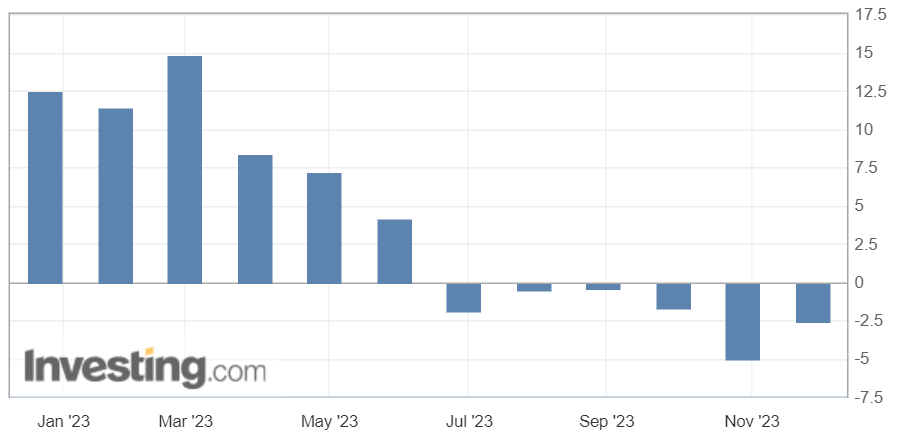

Industrial sales in Italy -2.6% per year – 6th negative in a row:

Рис. 7

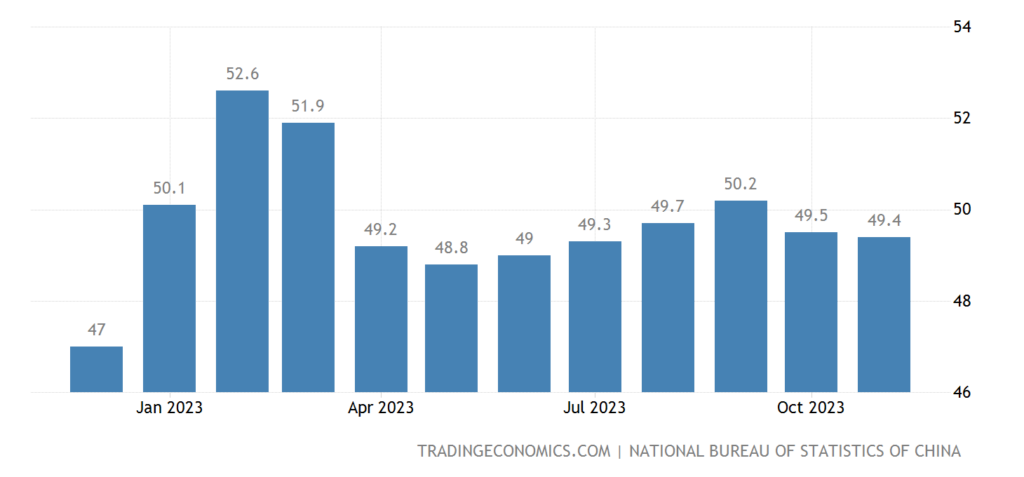

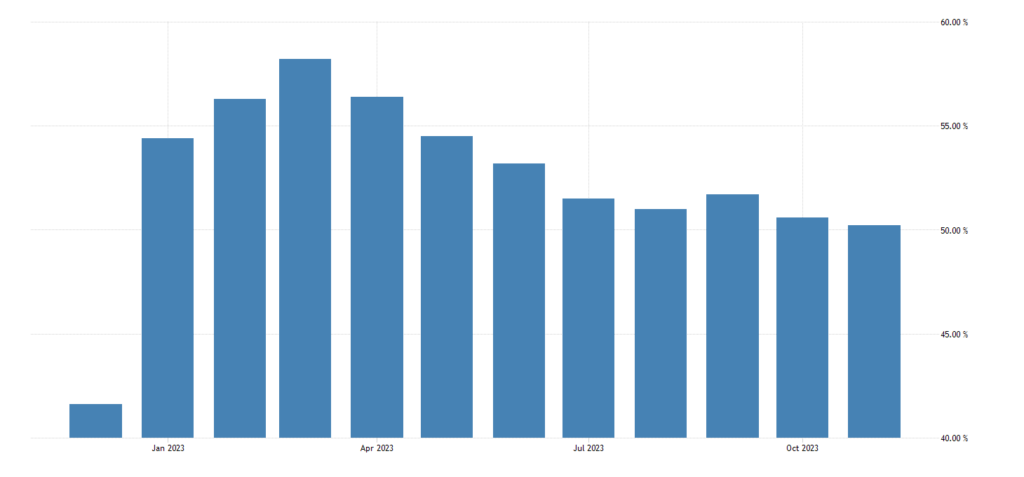

The official PMI (expert industry health index; a value below 50 means stagnation and decline) of the Chinese industry has gone deeper into the recession zone (49.4, 4-month low):

Рис. 7

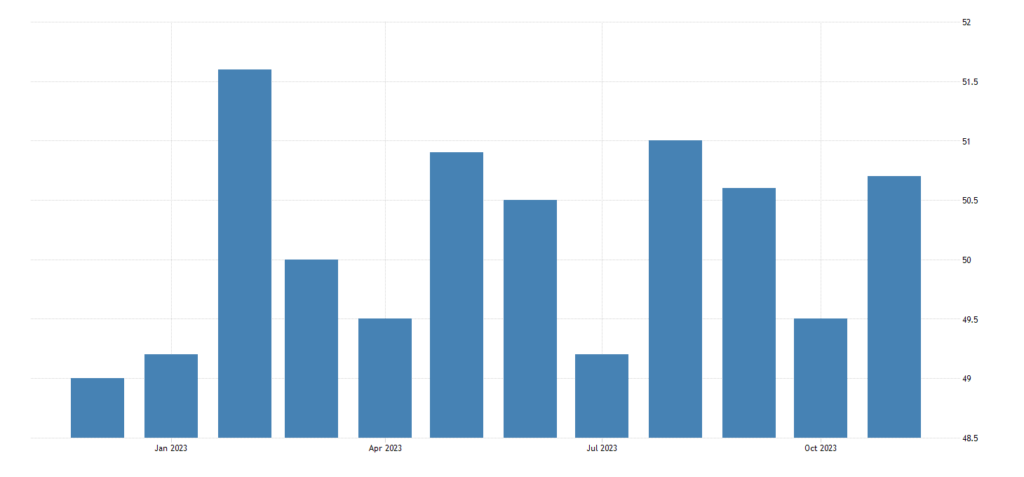

And the indicator for other industries stopped one step away from it (50.2, 11-month bottom):

Рис. 8

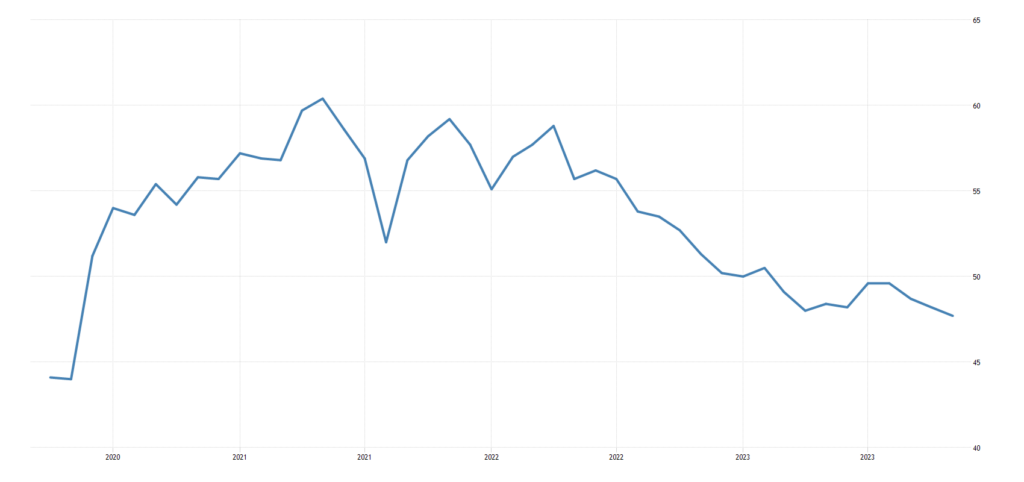

An independent study is less pessimistic – the industry index is in the growth zone (50.7):

Рис. 9

Australia’s manufacturing PMI is at its 3.5-year low (47.7):

Рис. 10

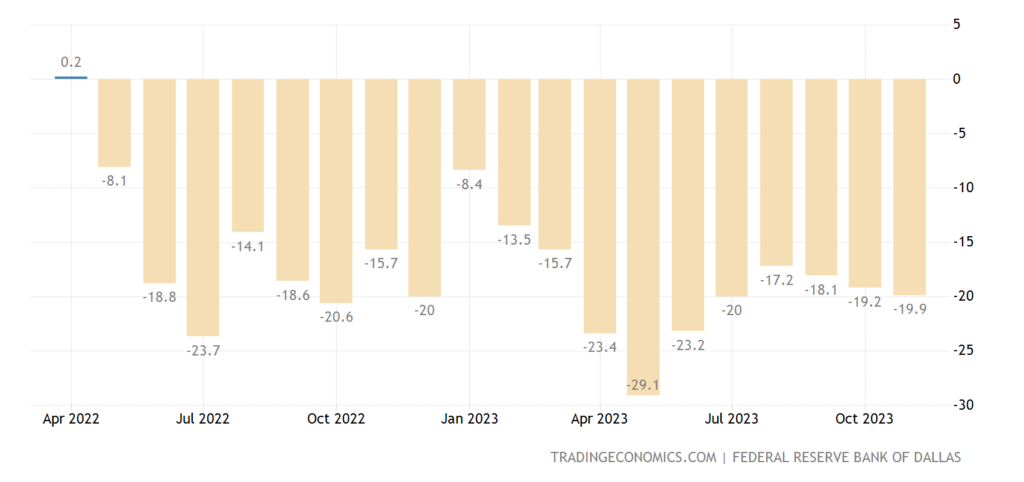

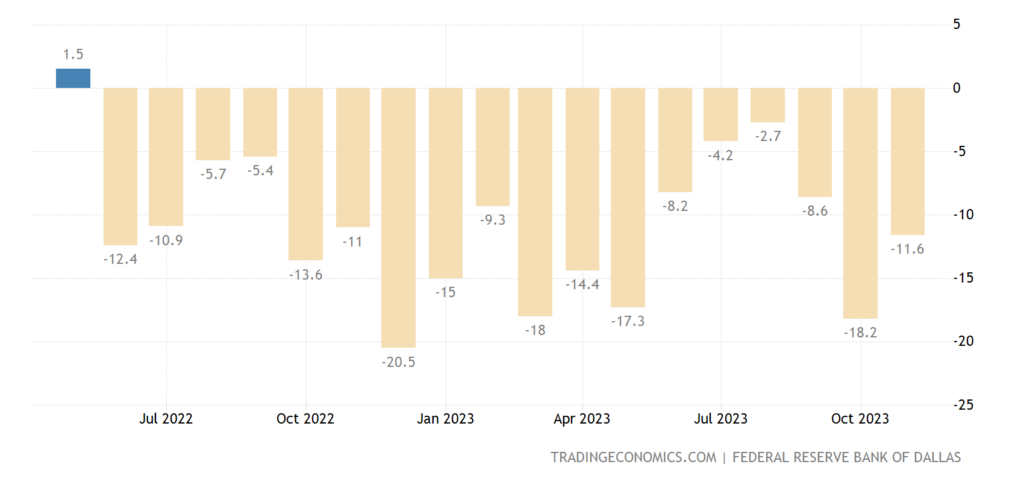

The index of manufacturing activity in the Texas Fed zone in the United States has been in the red for 19 months in a row:

Рис. 11

And the service sector index of the same region is 18 months in a row:

Рис. 12

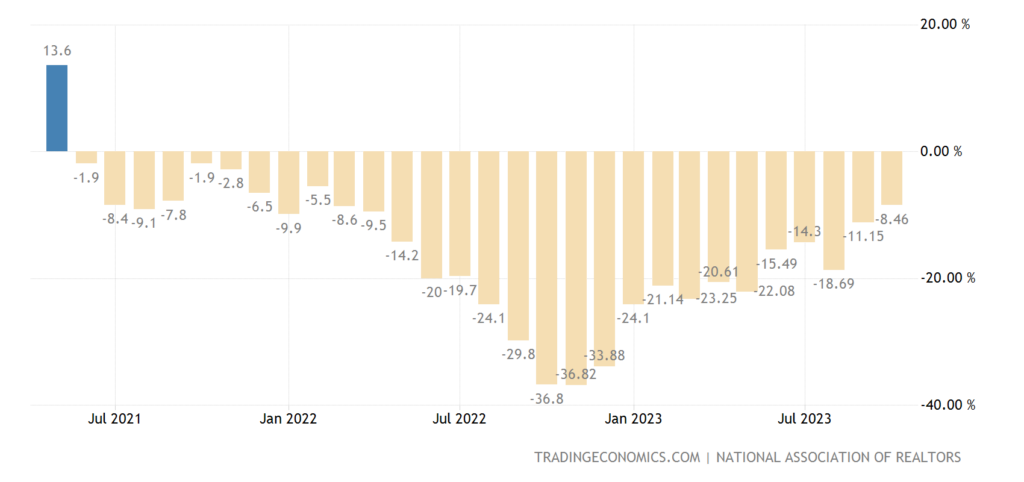

Pending sales of secondary housing in the US -8.5% per year – the 29th negative in a row:

Рис. 13

Eurozone household loans +0.6% per annum – 8-year minimum:

Рис. 14

The same bottom applies to corporate lending (there -0.3% per year) –

Рис. 15

German retail sales volume -0.1% per year – 18th negative in a row:

Рис. 16

Swedish retail -1.0% per year – also the 18th negative in a row:

Рис. 17

Retail in Norway -0.9% per year – 28th negative in a row:

Рис. 18

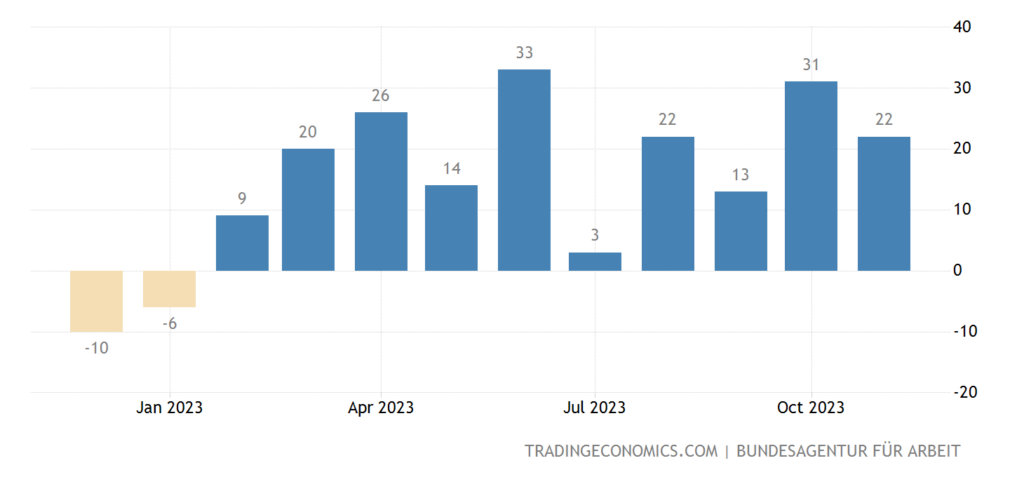

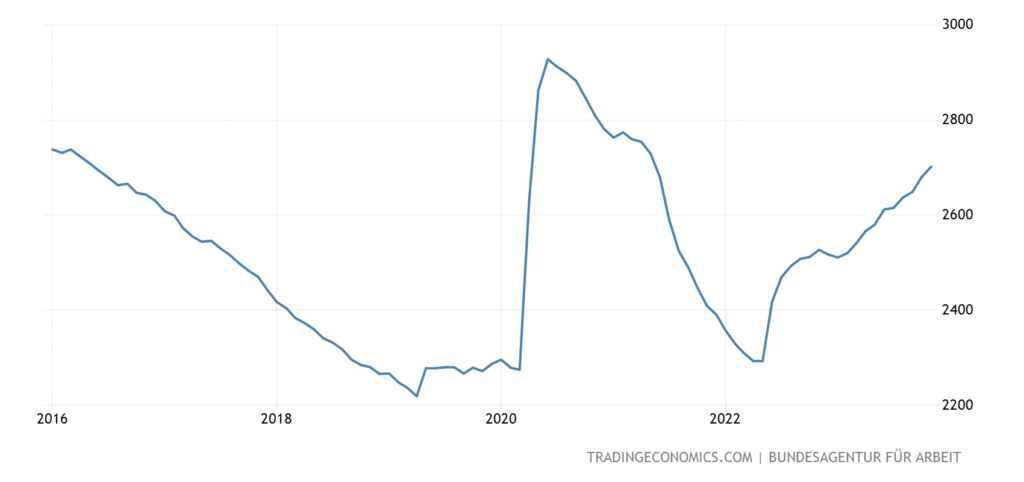

The number of unemployed in Germany has been growing for 10 months in a row:

Рис. 19

The number of unemployed in Germany has been growing for 10 months in a row:

Рис. 20

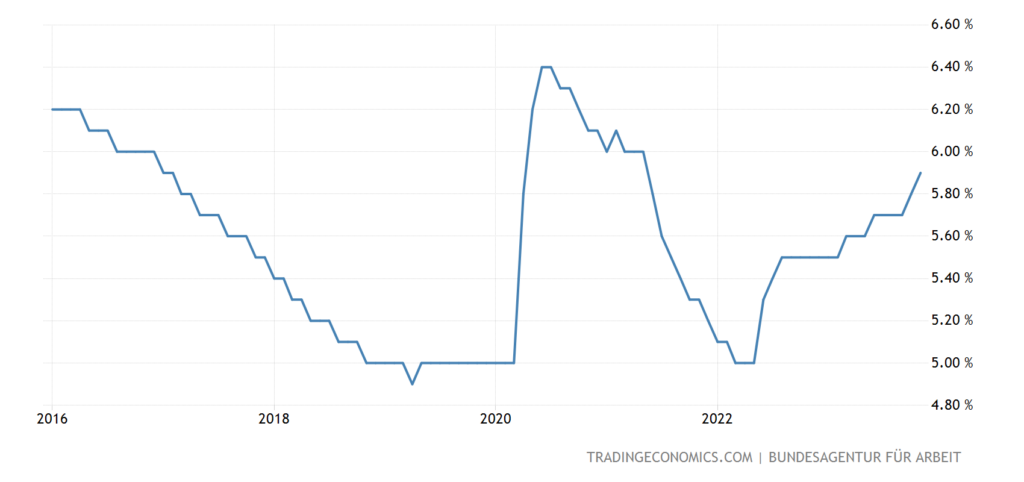

The same picture with the unemployment rate:

Рис. 21

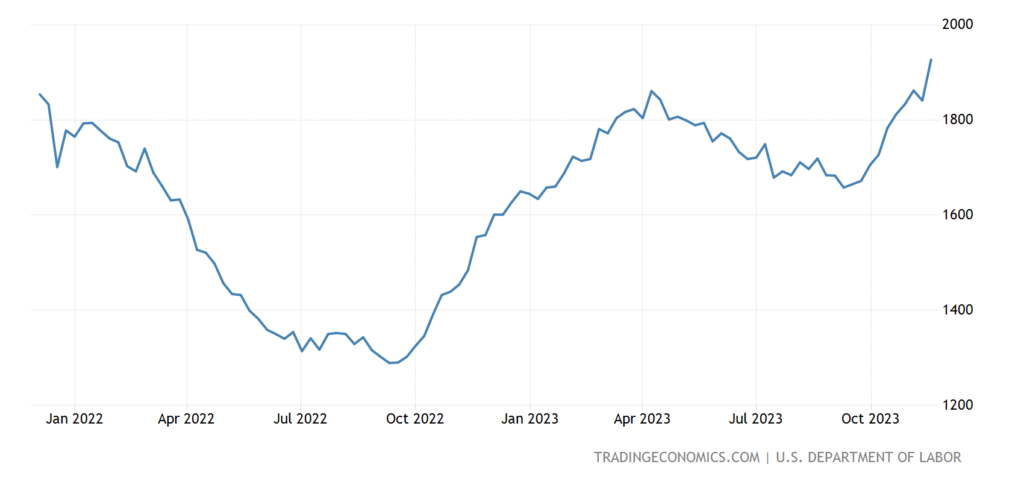

The number of recipients of unemployment benefits in the United States is the highest in 2 years:

Рис. 22

Not surprising given the drop in working hours we talked about a few weeks ago. I wonder how there can be economic growth in such conditions?

The Central Bank of New Zealand left monetary policy unchanged, as did the Central Bank of South Korea.

Main conclusions. The economic picture of the world is becoming boring, this is especially clearly seen against the background of the political picture, which shines with all its colors more and more every day. True, we must pay tribute to the economy: all political upheavals are a consequence of the ongoing economic crisis. And it is impossible to count on the fact that political processes will stop: the structural crisis continues.

We have explained this many times already, but here is the very case when it can be repeated: the specificity of a structural crisis is that it continues evenly, without acceleration or deceleration, until the structural distortions are compensated.

The corresponding theory is more or less fully described in M. Khazin’s book “Memories of the Future. Ideas of modern economics” (https://www.amazon.com/Crisis-capital-effectiveness-useless-solve-ebook/dp/B08KCC878V/ref=sr_1_1?crid=1JNJERAJA0H8Q&keywords=khazin+mikhail+book&qid=1701458287&sprefix=khazin%2Caps%2C398&sr=8-1 ). But if we limit ourselves to dry conclusions, then we must say that the structural decline will continue at the same pace for at least another 3-5 years. It is almost impossible to estimate accurately, since GDP statistics are extremely dependent on calculation methods. One can only note that according to its results, the US GDP will be in the region of 7-7.5 trillion current dollars, and China – about 8 trillion.

We very much hope that an adequate assessment of the development of the situation will give our readers the right guidelines in a crisis world. For now, we just wish them a good weekend and a relaxing work week.