January 6-12, 2024

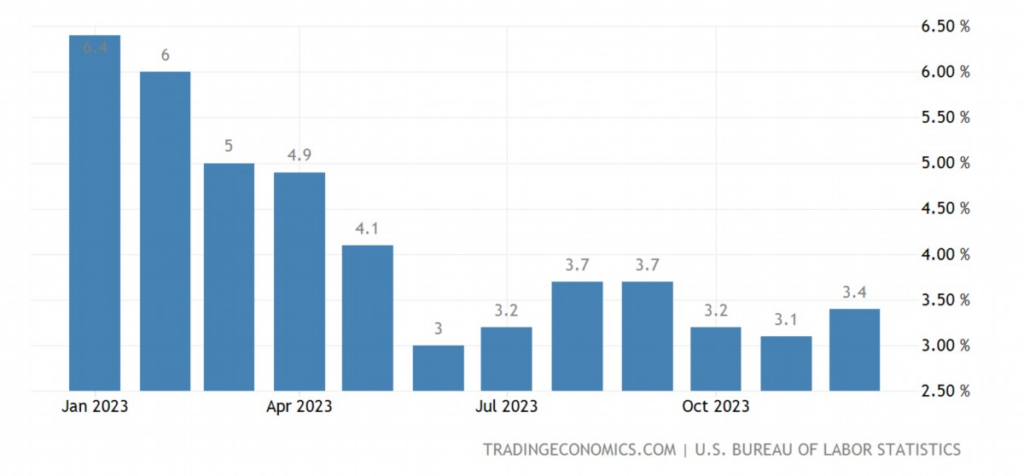

Big news. This is, of course, a sharp increase in consumer inflation:

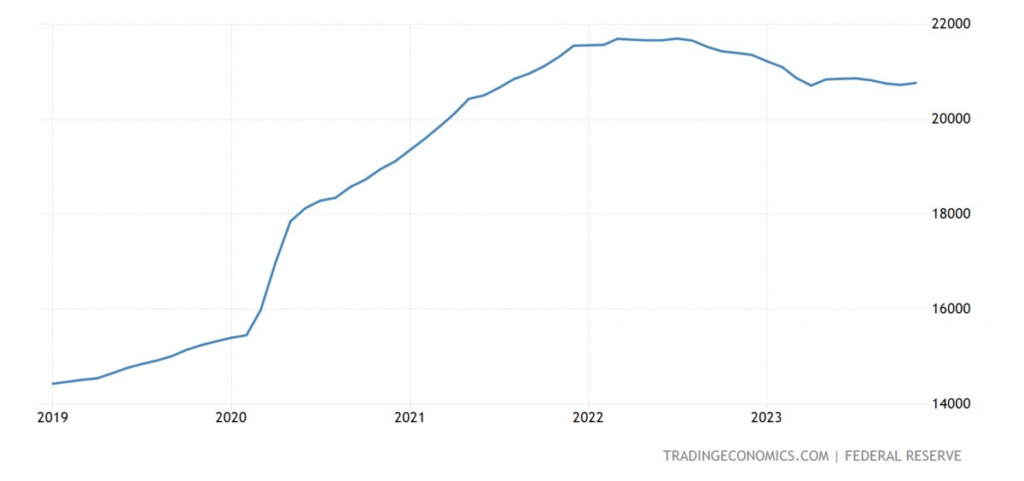

It is sharp not only because it is almost 10% of the previous value, but also because it occurred after several months of fairly tight monetary policy (see Fig. 2, graph of the M2 monetary aggregate in trillion dollars):

This is a severe blow to the leadership of the Federal Reserve, which planned to begin easing monetary policy in the very near future in the context of the beginning of deindustrialization (see the next section of the Review). We have repeatedly warned our readers that if such a policy were to begin, it would inevitably cause a sharp increase in inflation. The warning came to fruition, only inflation began to rise before monetary policy was softened. However, it is possible that during the New Year holidays some money entered the economic system.

But in general, it can be noted that, apparently, the degree of degradation of the monetary system has increased. Because even at industrial prices everything is not very good. However, more on this in the next review, when some additional data will be released.

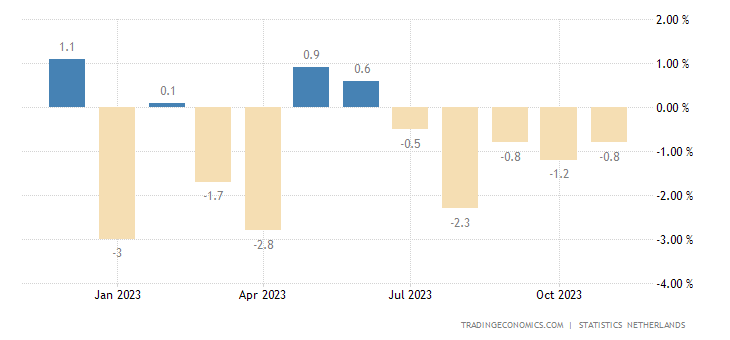

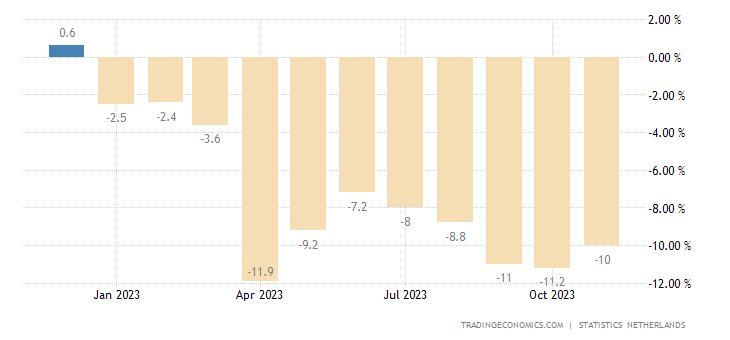

Macroeconomics. Manufacturing output in the Netherlands -0.8% per month, 5th minus in a row:

Pic. 3

And -10.0% per year, the 11th minus in a row:

Pic. 4

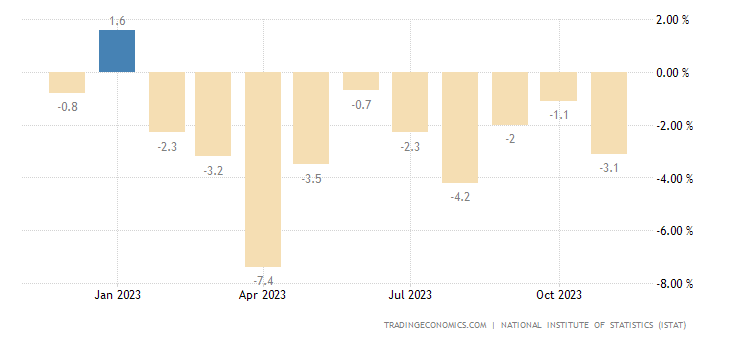

In Italy -3.1% per year, 10th minus in a row:

Pic. 5

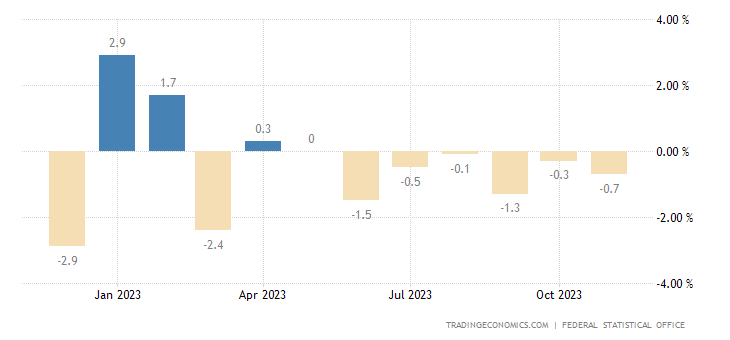

Industrial output in Germany -0.7% per month, 6th minus in a row:

Pic. 6

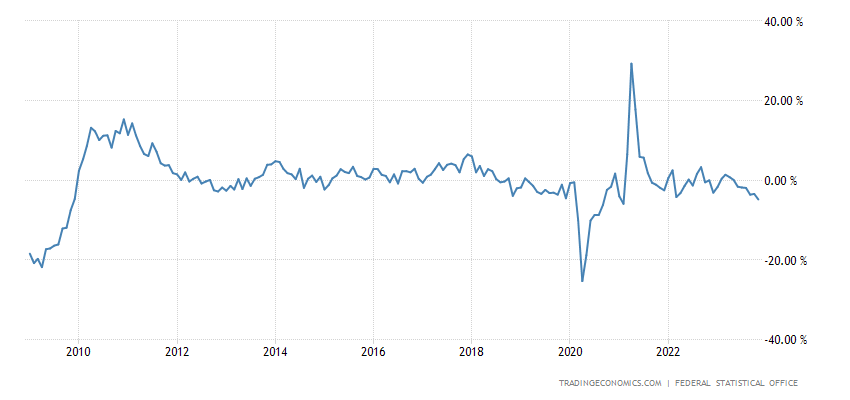

And -4.8% per year, excluding covid failures, the worst dynamics since 2009:

Pic. 7

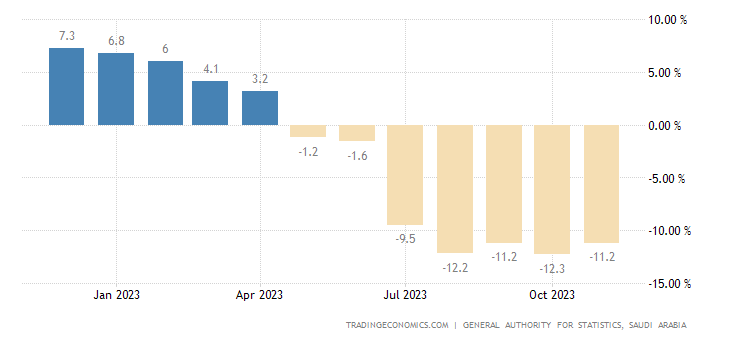

Industrial production in Saudi Arabia -11.2% per year, 7th negative in a row:

Pic. 8

Industrial production in Argentina -4.9% per year, the weakest dynamics in more than 3 years:

Pic. 9

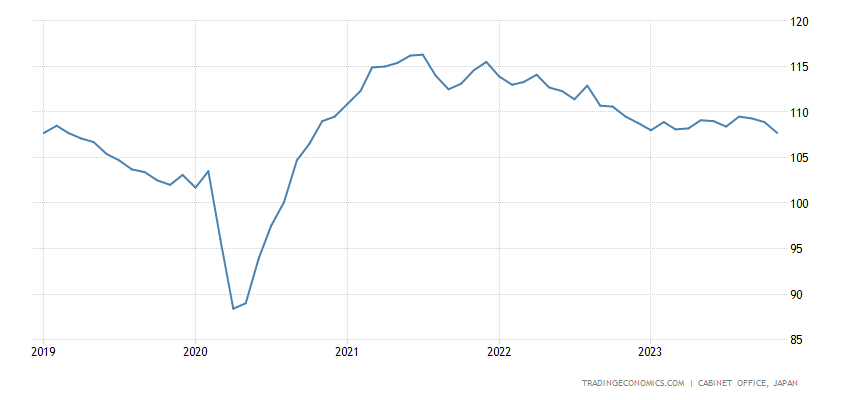

Leading indicators in Japan are at their lowest in more than 3 years:

Pic. 10

CPI (Consumer Inflation Index) without food and fuel in Tokyo Prefecture in Japan +2.7% per year, 32-year peak:

Pic. 11

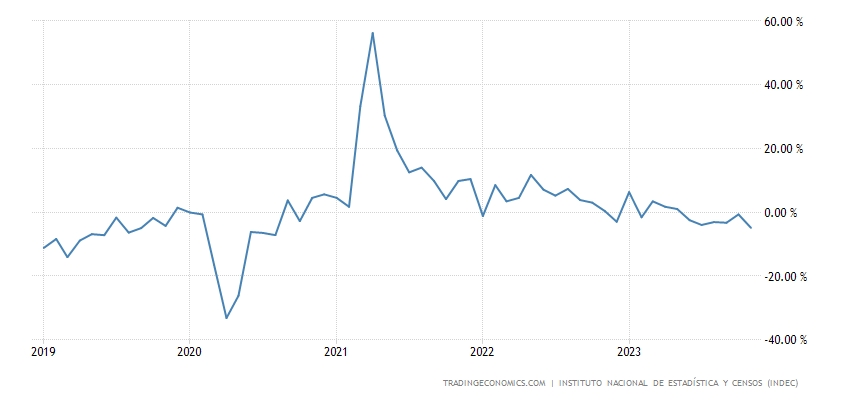

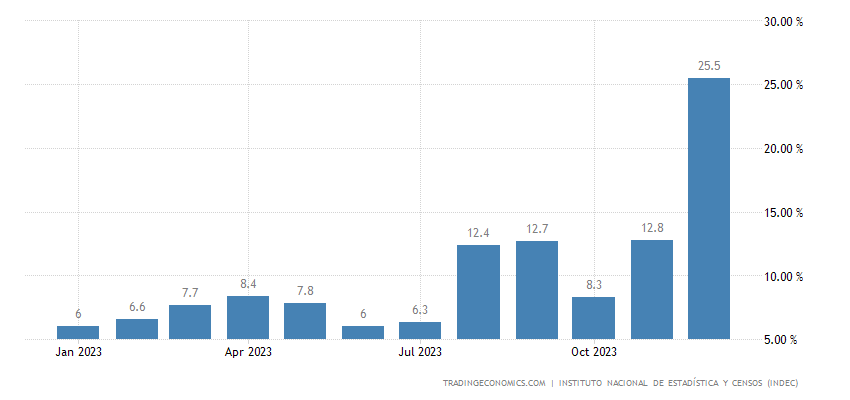

Argentina CPI +25.5% m/m, a record high, double the previous peak:

Pic. 12

And +211.4% per year, 33-year top:

Pic. 13

Prices for used cars in the USA -7% per year, 16th minus in a row:

Pic. 14

This is more likely to do with industrial prices, so let’s get ahead of things, deflation in the US industrial sector continues.

China PPI (Industrial Price Index) -2.7% per year, 15th monthly minus in a row:

Pic. 15

This means that there is a serious crisis in production, although not as severe as in Germany.

Loans in China +10.6% per year, repeating the record low of 22 years ago:

Pic. 16

Eurozone retail sales volume -1.1% per year, 14th monthly minus:

Pic. 17

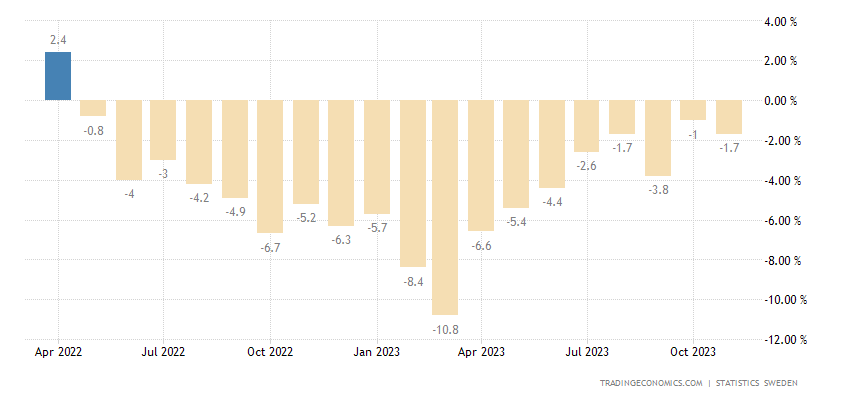

Swedish retail -1.7% per year, 19th minus in a row:

Pic. 18

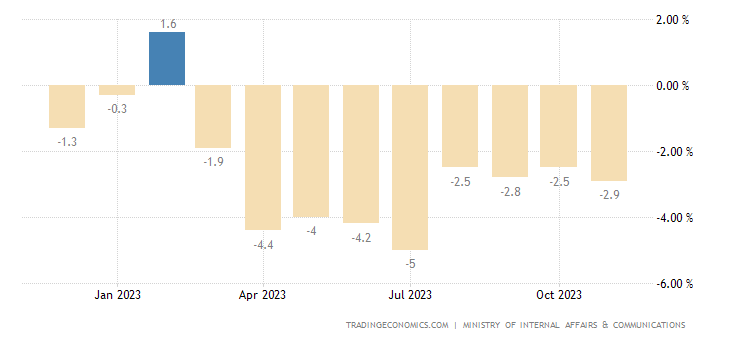

Household spending in Japan -2.9% per year, 9th negative in a row:

Pic. 19

The Central Bank of South Korea has not changed its monetary policy.

Main conclusions. The holidays are over, the number of statistics has increased, and the scale of the structural crisis has recovered. At the same time, political problems are beginning to affect the economy; the United States and Great Britain struck at Yemen. The formal goal is to respond to the closure of the Bab el-Mandeb Strait and attacks on American military vessels. But as a result, the price of oil on world markets increased by 2.5% and there is every reason to believe that similar cases will continue.

Iran seized a tanker that was formerly its own, but then was captured by the United States. Israel continues to attack the Gaza Strip and there are fears that it may transfer its activity to Lebanon… In general, the economic crisis caused a political one, which intensified economic problems, we are waiting for the next round of the political crisis… The year started off full of fun…

And in conclusion, we congratulate all former citizens of the USSR on the “old” New Year and the beginning of the new, leap year 2024. Let’s hope that this year will bring us not only economic problems, but also some joy!