July 23-29, 2022

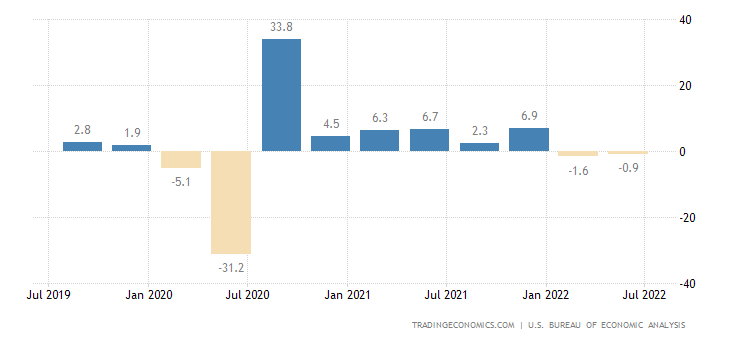

Big news. The change in US GDP in Q2 was -0.2% per quarter after -0.4% in Q1 (these are quarterly figures, data are usually given on an annual basis) – there is a technical recession:

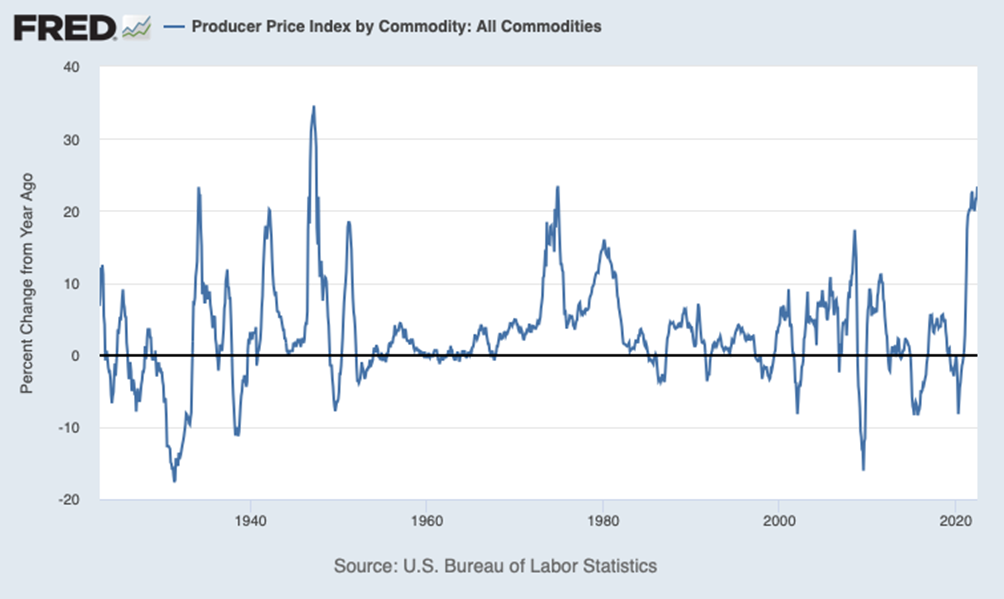

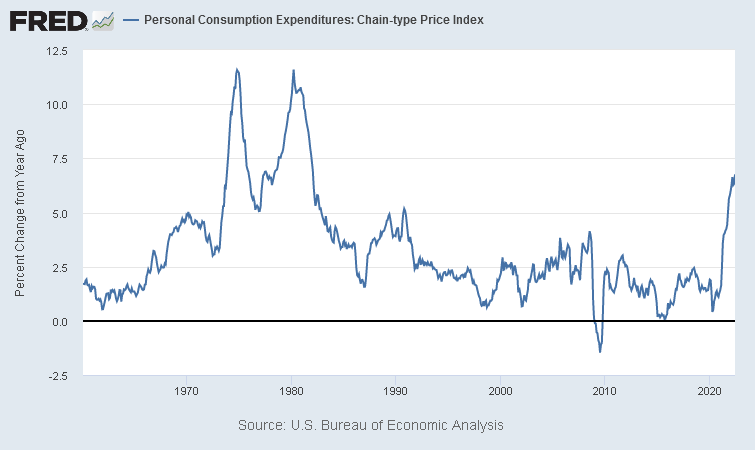

As readers of our reviews are well know, in reality, the recession in the US economy began in the fourth quarter of last year, 2021. This is clearly seen in the graph of industrial inflation, which jumped sharply in September last year:

It is clearly seen that inflation has exceeded the level of the 1970s and now it exceeds only the peak of 1947. Since official inflation figures are heavily underestimated, GDP automatically increases, so the picture on paper looks much more optimistic than it is in reality. Well, the reasoning about the recession does not hold water at all. So we wil discuss it in the final section of this review.

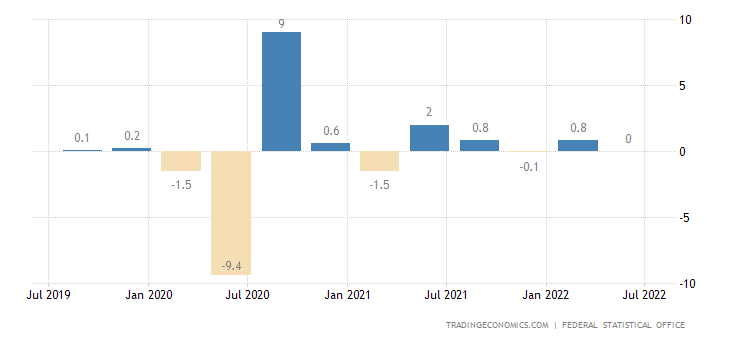

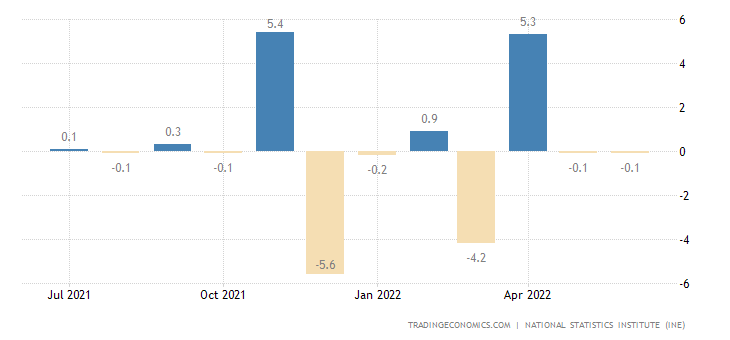

Macroeconomics. German GDP growth in Q2 reset to zero:

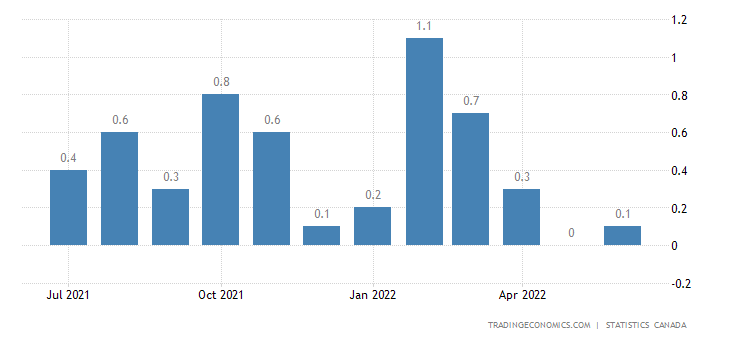

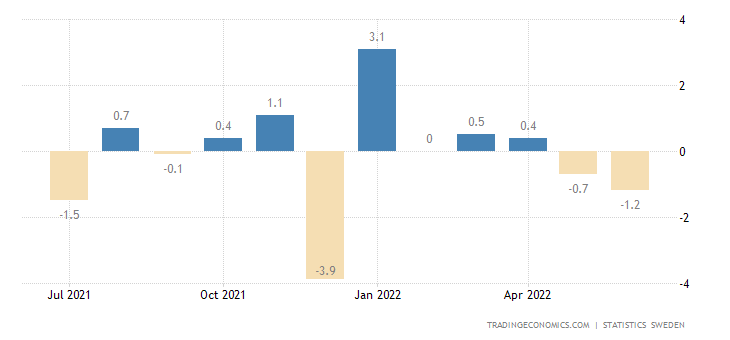

Stagnation (monthly) and in Canada’s GDP:

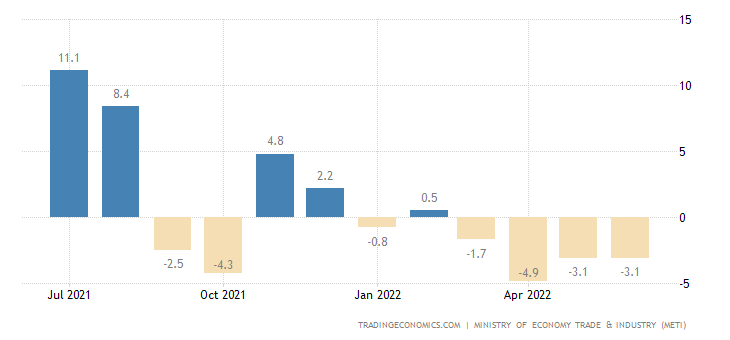

Industrial production in Japan (-3.1% per year) has been in the annualized minus for 4 months in a row:

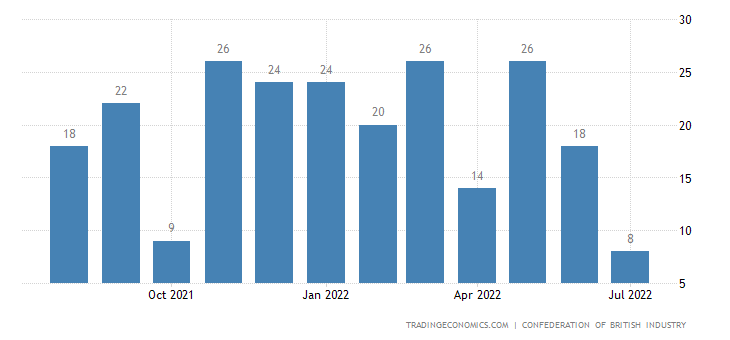

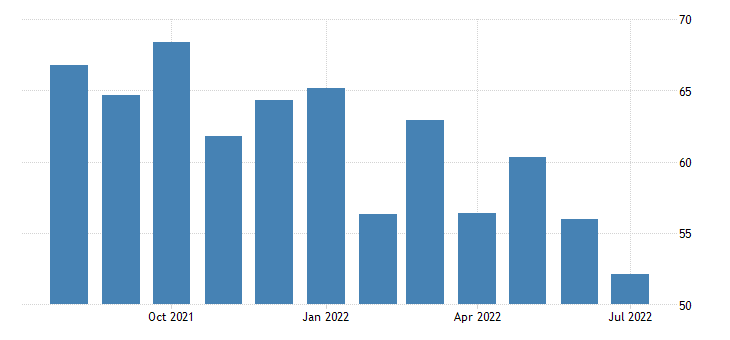

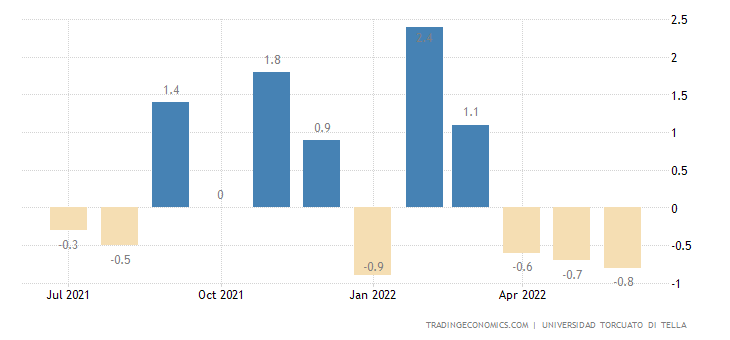

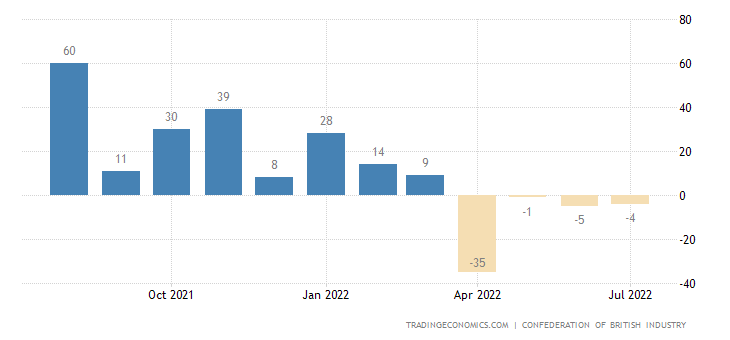

UK industrial order balance on 15-month day:

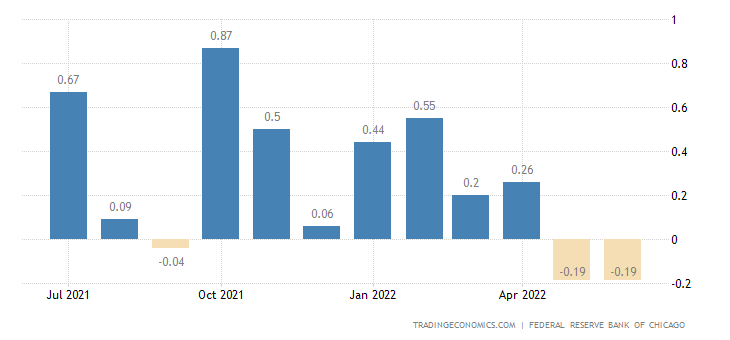

The National Activity Index in the US from the Chicago Fed is the weakest in 1.5 years, in the red for 2 months in a row:

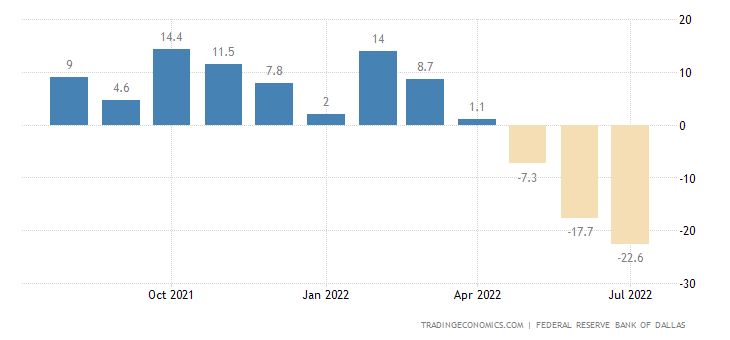

Texas Fed Regional Manufacturing Activity Index is the worst in 2 Years:

Same with PMI Chicago:

Service sector in Richmond Fed zone in the red and at the bottom for the last 2 years:

Note that all these indices are calculated under conditions of low inflation. For this reason, the key is to compare them over the past months – and the dynamics are just negative.

Business confidence in Turkey is the lowest in 2 years:

In Italy – in 16 months:

And in Spain – for 16 months:

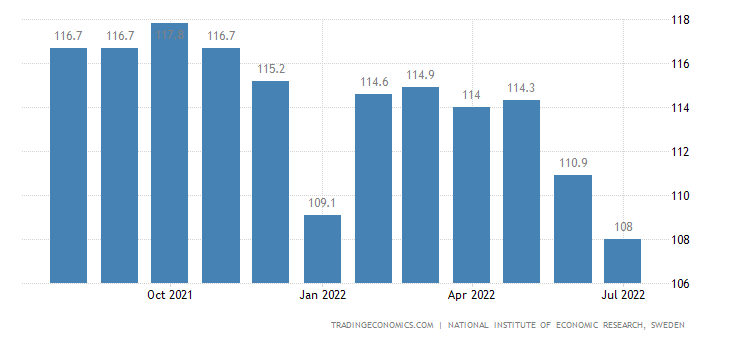

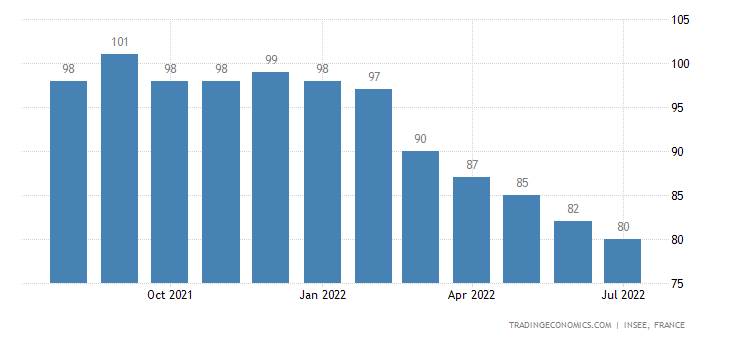

In Sweden – also in 16 months:

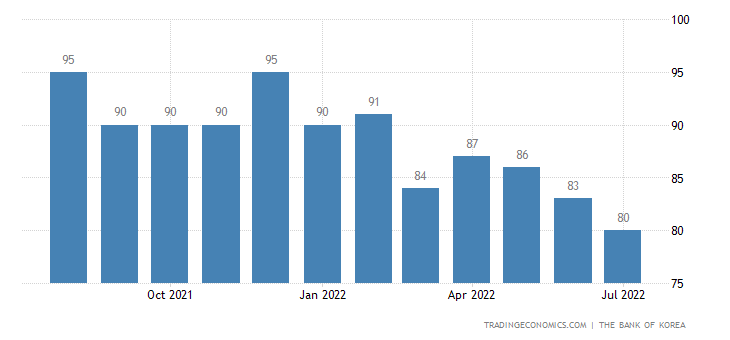

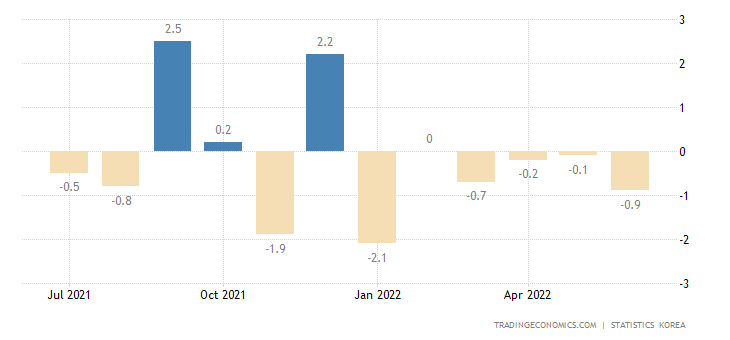

IIn South Korea is the lowest over 21 months:

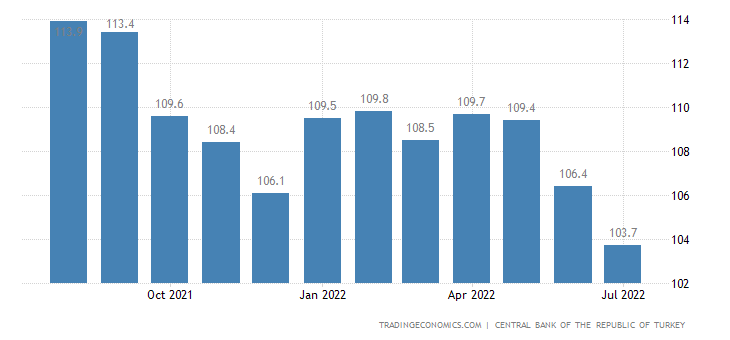

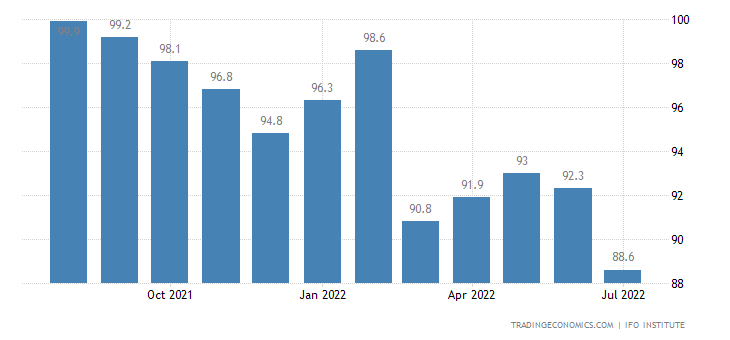

The business climate in Germany (IFO version) is the worst in more than 2 years:

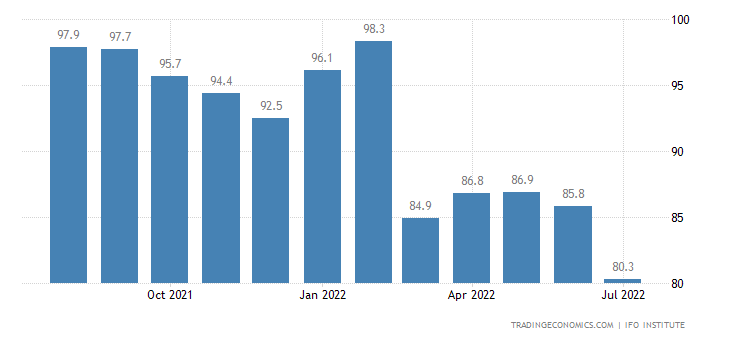

And its component of expectations is already near the bottom of 2008:

Economic sentiment in the Eurozone is at its lowest in 17 months:

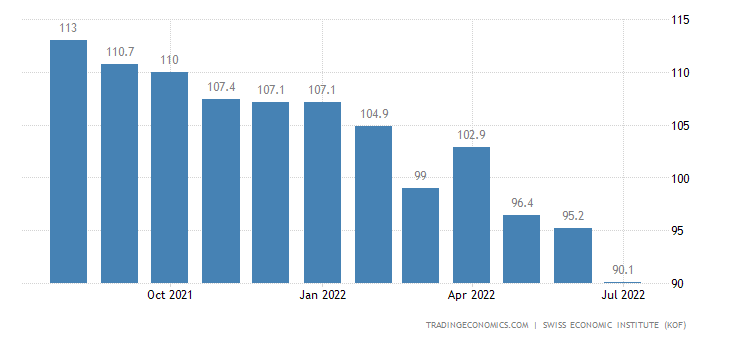

Swiss leading indicators are the weakest in 2 years:

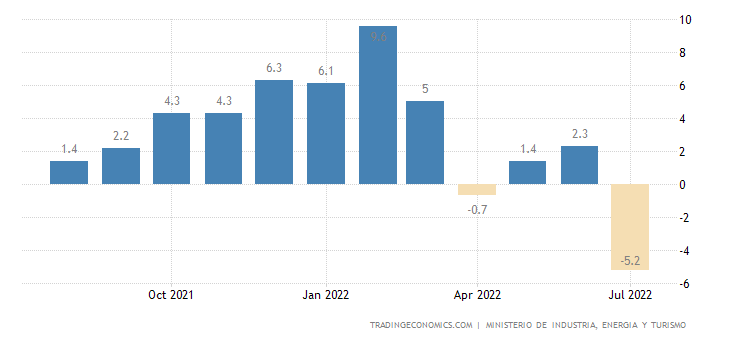

Leading indicators of Argentina fall with acceleration for 3 consecutive months:

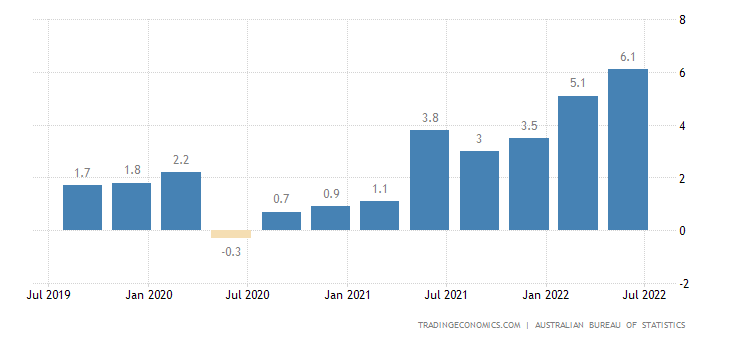

Australian CPI (Consumer Inflation Index) +6.1% per year – the highest since 1990:

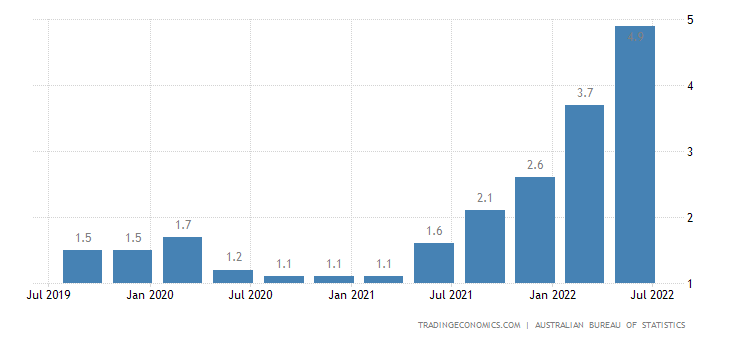

Net CPI (excluding highly volatile food and fuel components), +4.9% since 1991:

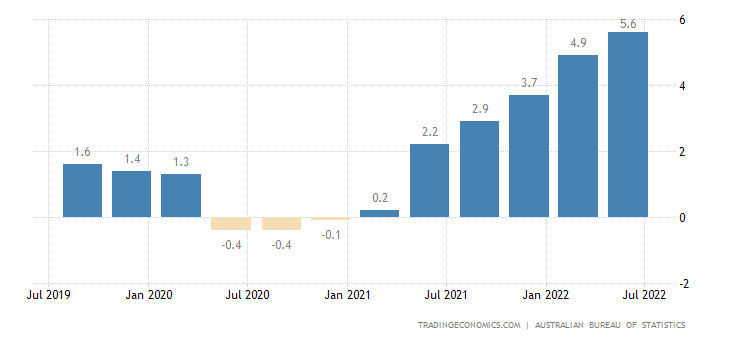

Australian PPI (industrial inflation index) +5.6% per year – peak since 2008:

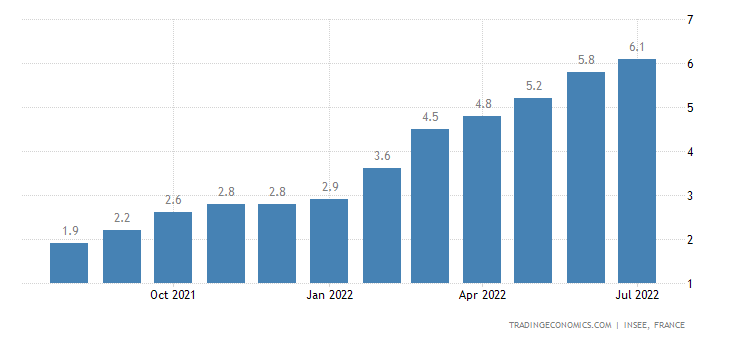

French CPI +6.1% per year – the highest since 1985:

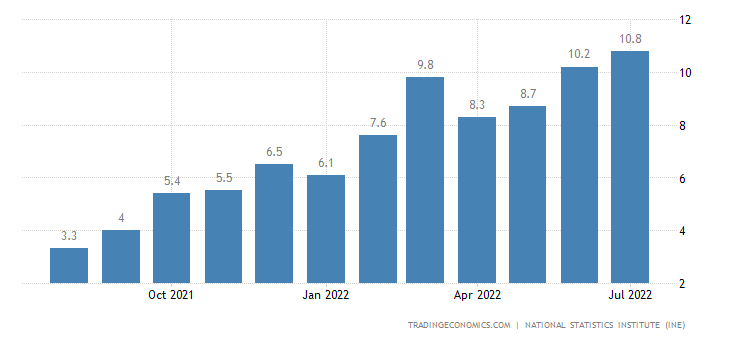

Spanish CPI +10.8% per year – peak since 1984:

Eurozone CPI +8.9% per year – a record for 31 and a half years of observation:

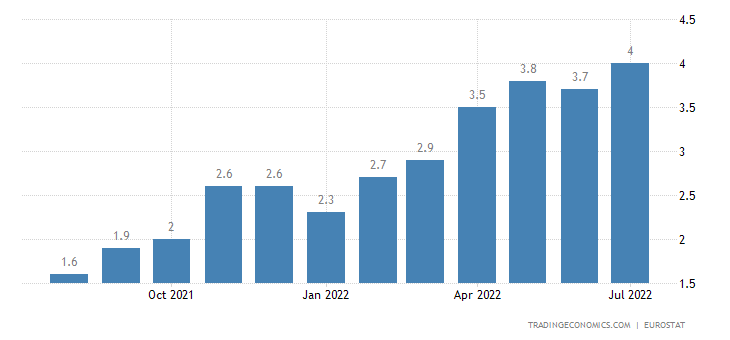

Record “net” Eurozone CPI (+4.0% per year) –

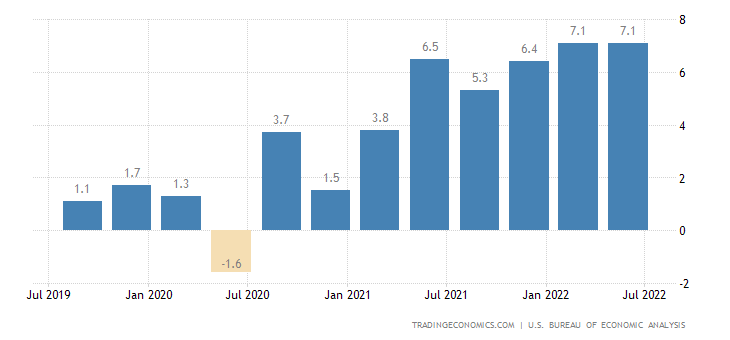

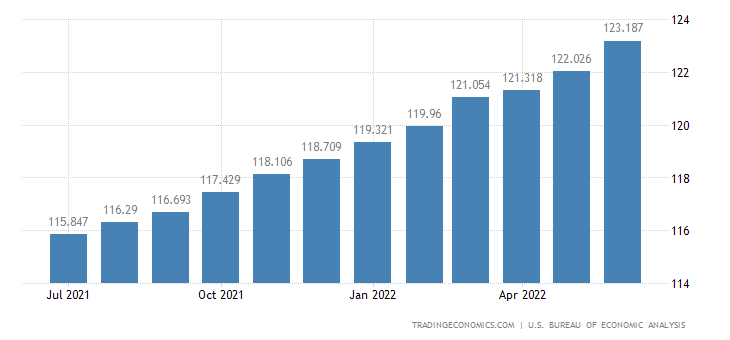

Consumer basket price index in the US +1.8% qoq – the highest since 1981:

Monthly it is +1.0% – the peak since 2005:

Annual change +6.9% – maximum since January 1982:

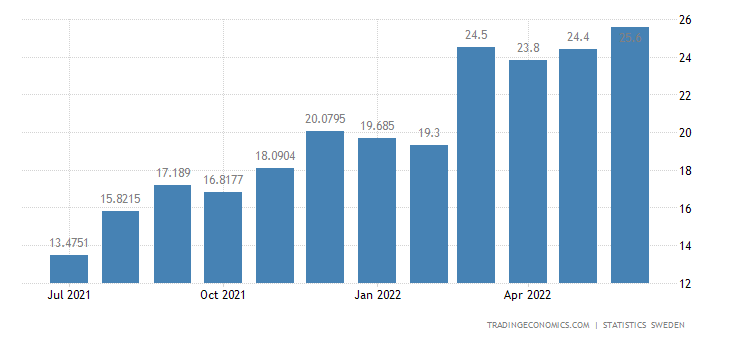

PPI Sweden +25.6% per year – a record for 31.5 years of observation:

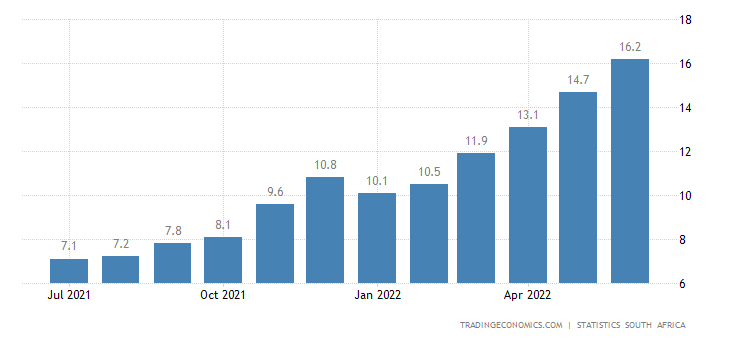

PPI South Africa +16.2% per year – also a record:

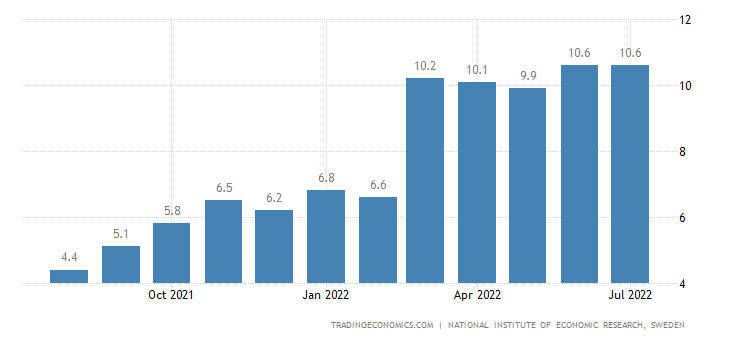

Swedish inflation expectations are at a record high (+10.6% per year):

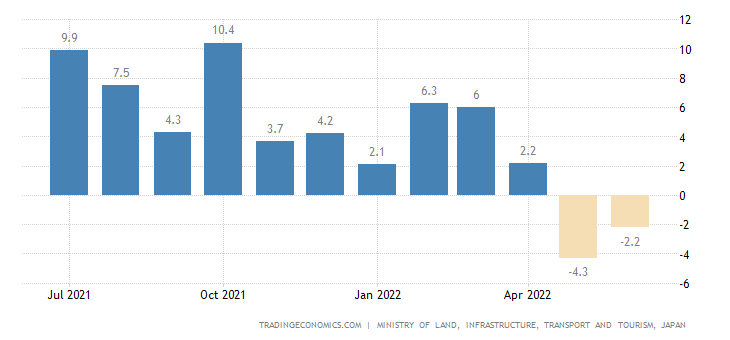

The number of new buildings in Japan -2.2% per year – the 2nd negative in a row:

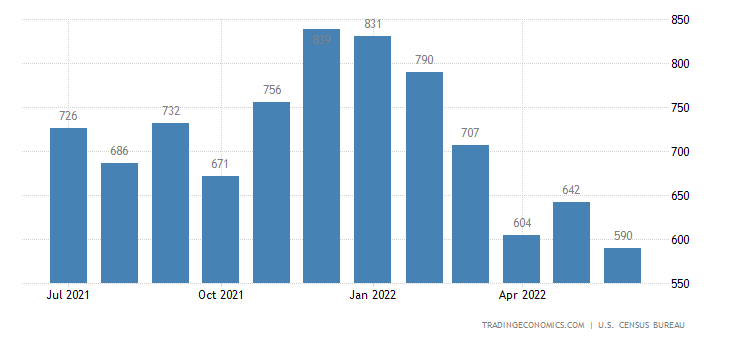

New home sales in the US -8.1% per month and -17.4% per year – the covid-19 bottom of 2020 almost reached

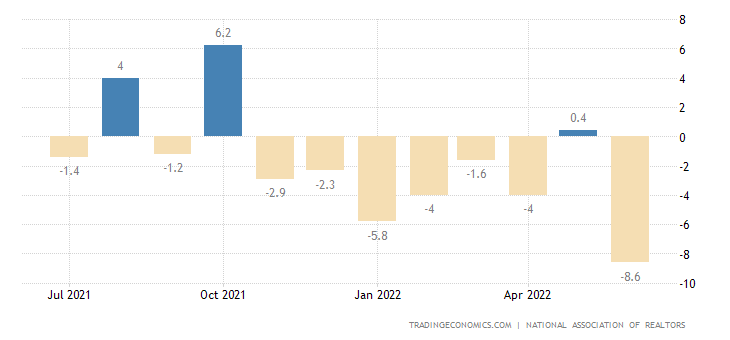

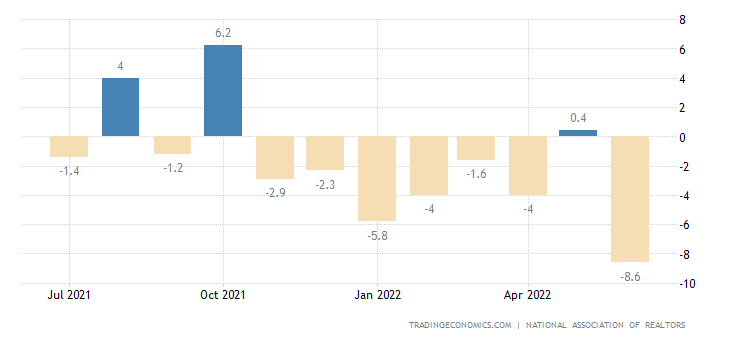

Pending home sales in the US -8.6% per month – without counting the failure of 2020, this is the worst trend since 2010:

And -20.0% per year – excluding the covid recession, this is the minimum since 2011:

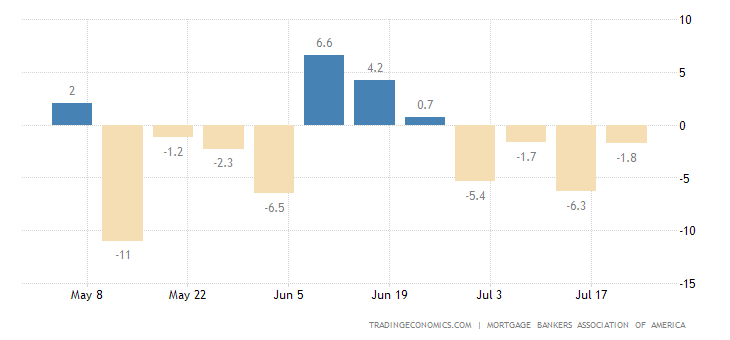

Mortgage applications in the US are falling 4 weeks in a row (another -1.8%)

To a fresh bottom in 22.5 years

The balance of retail sales in Britain has been in the red for 4 months in a row

Retail sales in Sweden -1.2% per month – 2nd negative in a row:

And -3.6% per year – the weakest dynamics since 1994:

Spanish retail -0.1% per year — 2nd negative in a row:

Retail South Korea -0.9% per month – 6th negative (or zero) in a row:

This is why the annual dynamics went negative (-1.5%) for the first time in 2 years

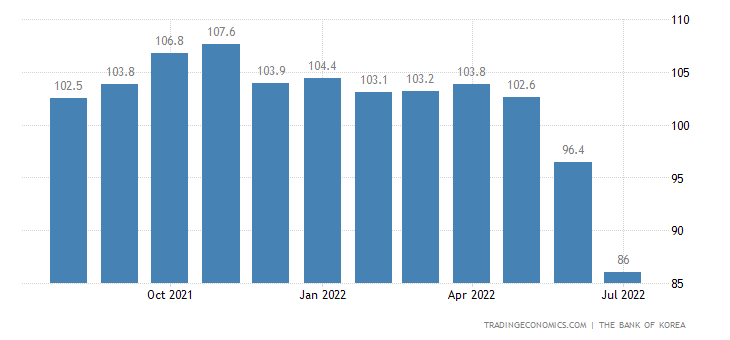

South Korean sentiment is worst in 2 years (record inflation expectations):

As in Italy:

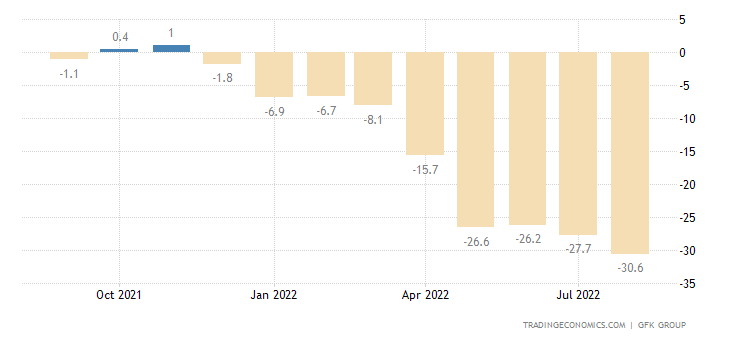

In France – for 9 years and near the bottom for a half a century of the existence of the review:

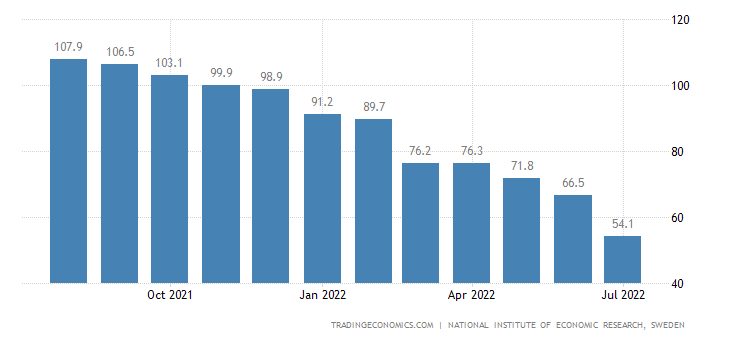

In In Sweden – for 29 years, the worst values are nearby:

In Germany, they are record bad, and the propensity to buy at the bottom since 2008:

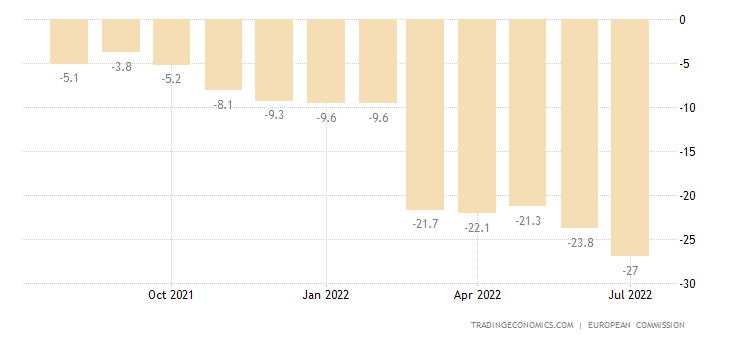

Record bottom in the Eurozone:

US consumers (Conference Board review) are pessimistic at the most in 1.5 years:

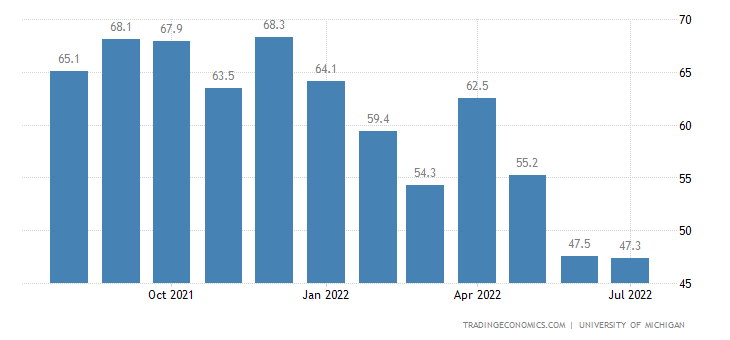

A University of Michigan study found the worst consumer expectations in 42 years:

The US Federal Reserve raised the rate by 0.75% to 2.25%-2.50% – the highest since 2008.

The Central Bank of Saudi Arabia also raised the interest rate by 0.75% to 3.00%.

Main conclusions. The crisis continues at about the same pace, despite the summer when business activity is decreasing. However, the structural crisis does not depend on the scale of business activity (this emission correlates with the volume of production, the cost of production, which grows in the context of a structural crisis, does not depend on this).

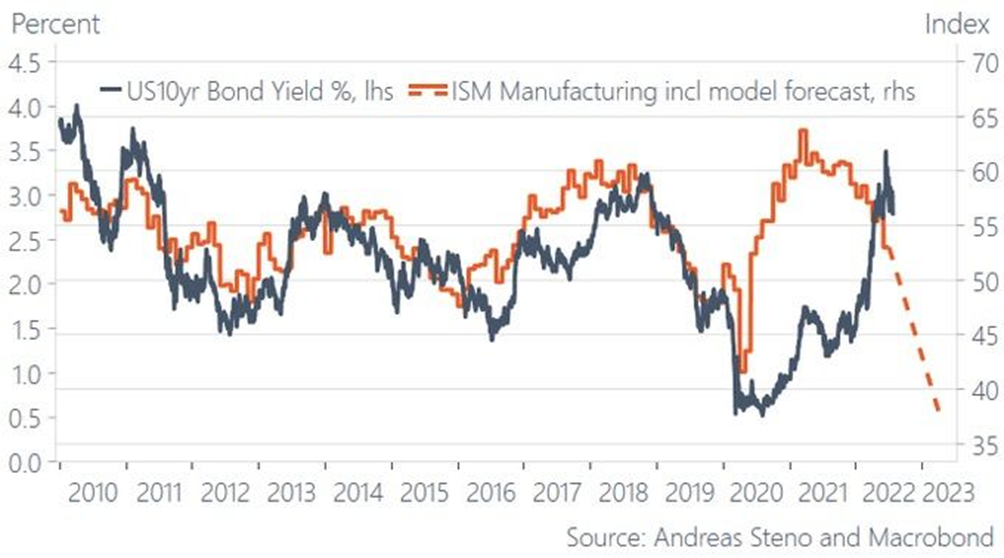

By the way, another proof of the structural crisis is the yield chart of 10-year US Treasury bonds and ISM indicators for industrial production. As you can see, this correlation begins to break down. A similar result was in the late 70s and was called “stagflation”.

Note that the phenomenon of stagflation in the liberal economic theory has not received an explanation. And from the point of view of modern theory (see M. Khazin “Memories of the Future. Ideas of the Modern Economy”, https://fondmx.pro/professionalam/), the reasons for this phenomenon are obvious, this is the already mentioned structural crisis.

There is a very interesting discussion in the US about whether what is happening in this country can be considered a recession or not. Again, from our point of view this is a meaningless formulation of the question.The economic mechanism of the present crisis has nothing to do with cyclical processes, to which the “recession” phenomenon belongs. Therefore, discussing this issue from the point of view of understanding current economic processes is nonsense; rather, one can think whether the economic recession began in September 2021 or November.

This discussion makes sense only on the eve of the November elections and it has a purely political meaning. But the fact that they are not discussing real processes in the economy but absolutely scholastic and unrelated to reality indicates the complete helplessness of both the monetary authorities and US financial and economic experts. And this means that the crisis will develop according to the most negative scenario, because without understanding the current processes, reasonable measures to minimize its consequences can only be taken by accident.

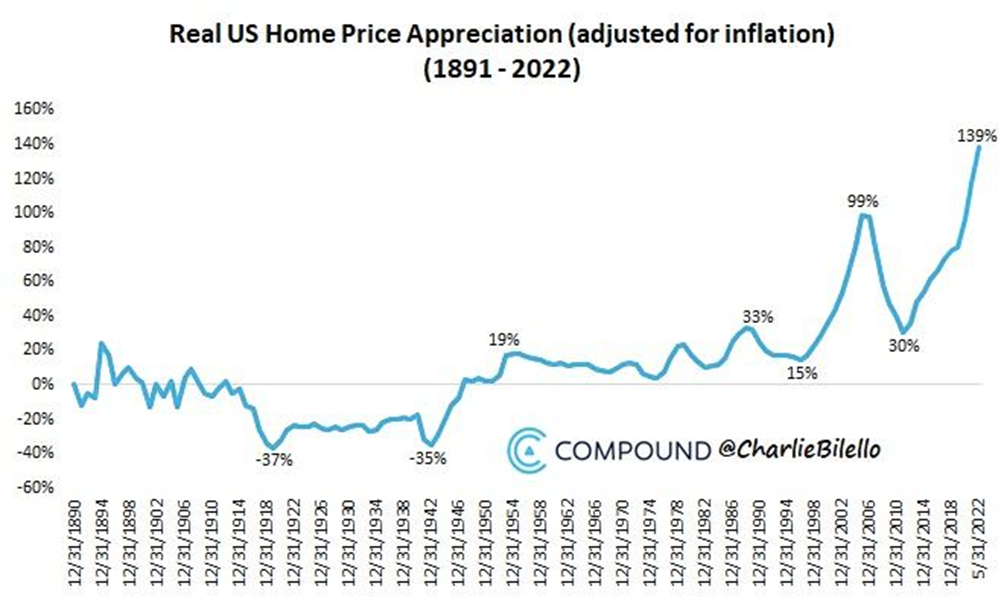

At the same time, the rise in prices in the consumer sector is gradually starting to catch up with consumer inflation:

The growth in housing prices over the past year has already exceeded 18%, which is much closer to industrial inflation than to official consumer inflation (just over 9%). If this process continues (and with an increase in the rate, we recall that the structural component of inflation grows), then the picture of the US economy will deteriorate significantly by autumn.

In conclusion, we wish all readers of the site good summer weather for the weekend and the work week without unpleasant surprises.