Period: 26 September – 2 October 2020

Top news story: This time, the top two news stories, the second one literally came on the last day of the week.

- The first news is the US presidential candidates’ debate, which has shown that neither Donald Trump nor Joseph Biden can articulate the strategic goals and plans they want to realize if they win. The question of which of the two won the debate is of little interest, but virtually all commentators drew attention to the poor quality of the statements of both candidates. In fact, this means that the level of uncertainty, not only economic, but also socio-political, is already becoming such that even the US leadership has little idea how it is possible to stabilize it at least in some way through simple and socially understandable actions. And if anyone else had any illusions about it, after the debate, they almost disappeared.

- The second news is that US President Donald Trump has contracted Coronavirus, too, does not improve stability, because if Trump won the debate, it was because he looked exactly like a potential crisis manager in a crisis. The possible health problems of the American president in this situation only exacerbate the general state of uncertainty.

Macroeconomics

Britain’s GDP rebounded slightly in the second quarter, but the recession is huge (-19,8% per quarter and -21,5% per year) – 2020 is expected to be the worst performance in 300 years. Investments in the same period fell by 26,5% per quarter and 26,1% per year.

In August, industrial production in South Korea slumped by 0,7% per month and deepened the annual decline to 3,0%. In manufacturing, it dropped to 3,1% per year. In construction, even the minimum in 18 months (-9,4% per year). And the retail increase is almost zero (+0,3% per year).

US GDP in April-June -9.0% per quarter and per year – the trough since 1946.

Industrial orders in the US in August dramatically reduced the topic (to +0,7% per month):

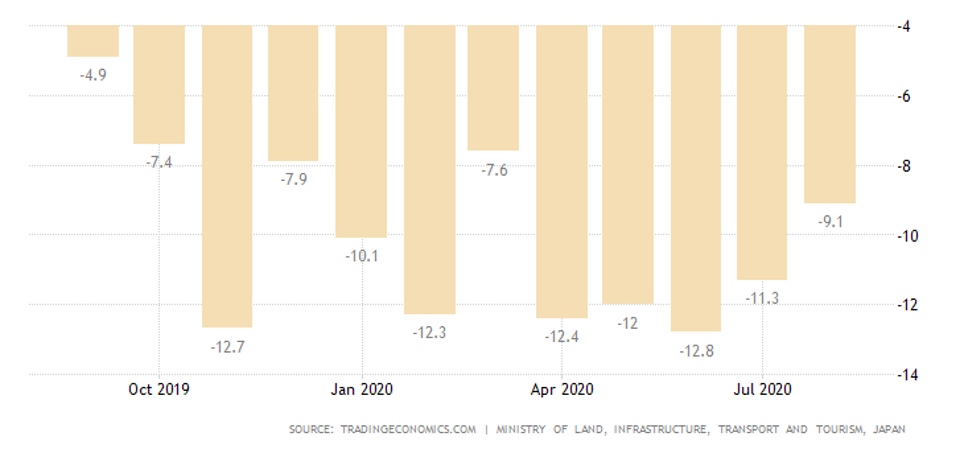

Japanese industrial production is recovering weakly: in August -13,3% per year after -15,5% in July. Because monthly growth has slowed down sharply, from +8.7% to +1,7%

Retail is +4,6% per month, but after -3,4% in the previous month it’s not much. Accordingly, the annual decline in sales is maintained (-1,9% after -2,9%).

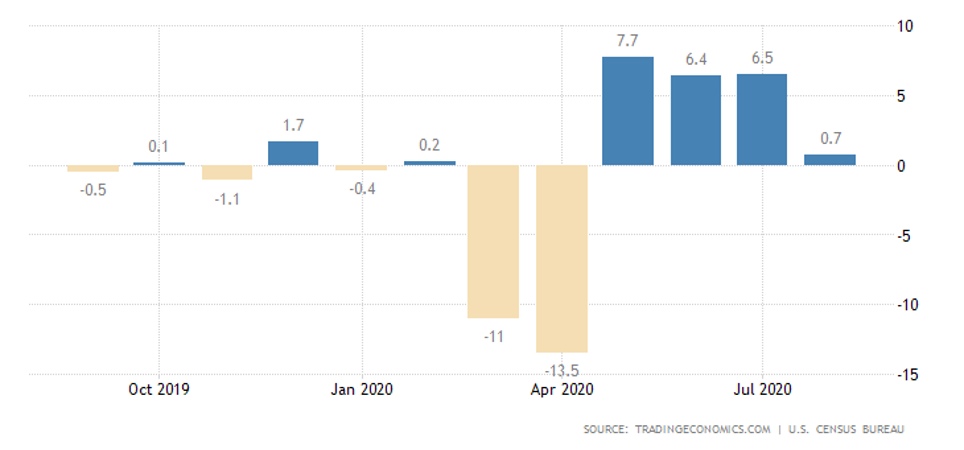

It’s the same with the housing starts:

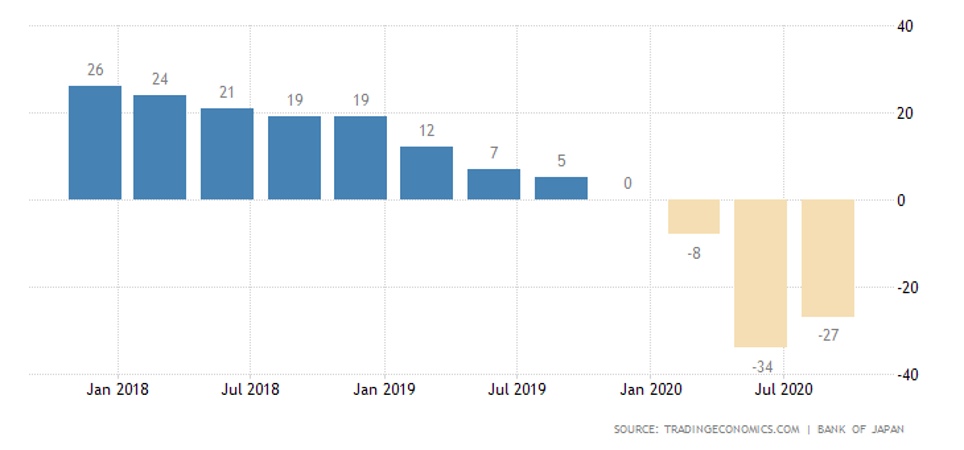

The Third Quarter Business Survey of the Bank of Japan «Tankan» showed a very sluggish improvement among large manufacturing firms:

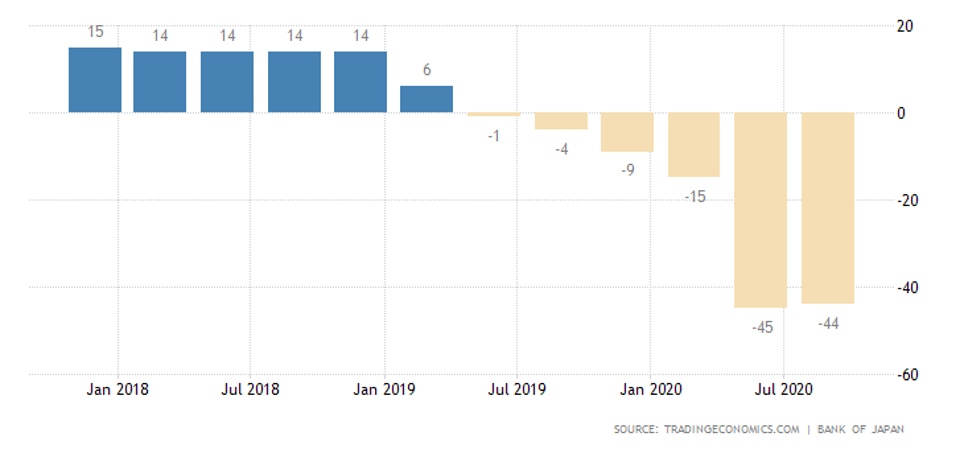

And the complete lack of progress of small businesses:

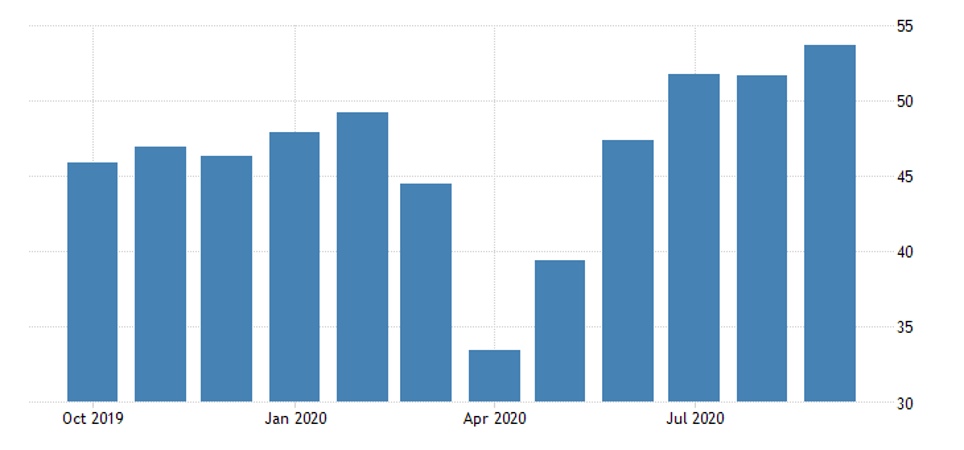

The Euro Area Manufacturing PMI hit a two-year peak in September:

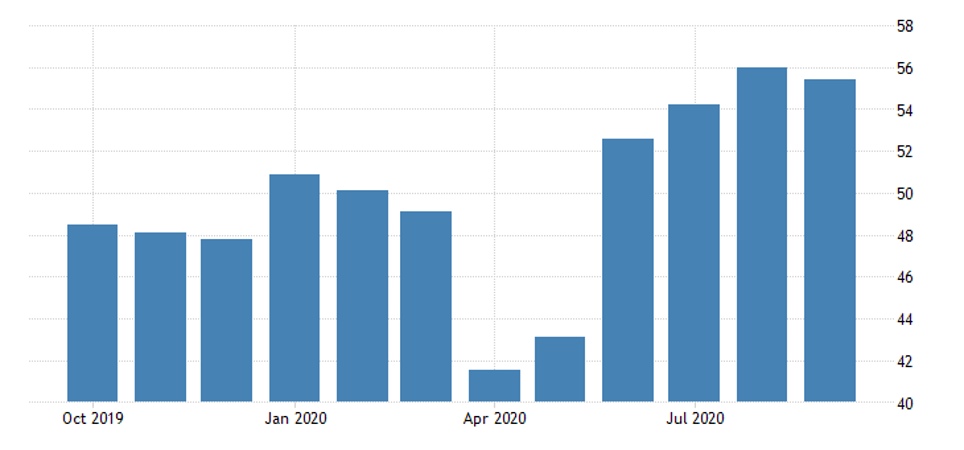

In Britain, it has slowed, but it is still clearly expansionary, as in the US:

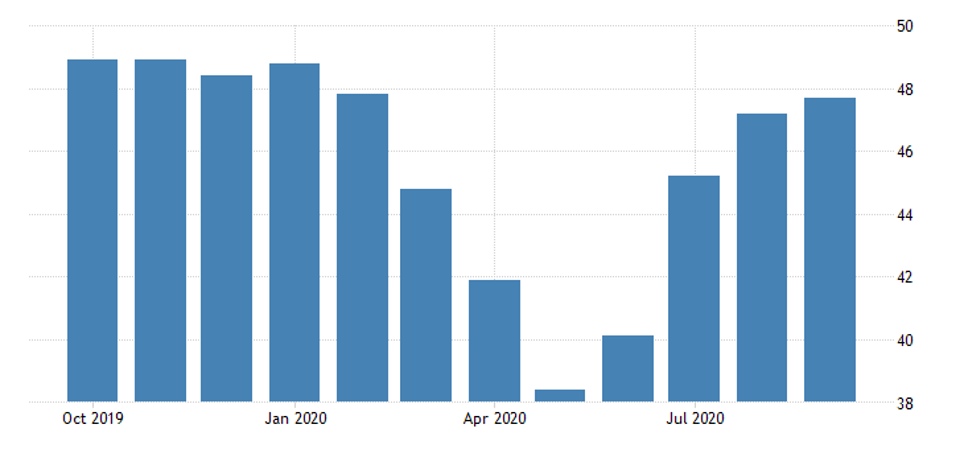

In Russia, it has returned to a recession. And in Japan, it hasn’t left for almost two years:

The US foreign trade deficit in August was a record (-$82.9 billion).

In Germany in September, the CPI fell 0,2% a month and the same amount a year – to its lowest level since January 2015; in the event of a fall another 0,3% will be the bottom since December 1986 (-0,9%).

In France, CPI 0,1% per year is the minimum since May 2016. Overall, the eurozone is at -0,3% per year – trough since late 2014. And without fuel, food, alcohol, and tobacco, the CPI is +0,2% per year – the record low for 23 years of observation.

In Britain, consumer credit fell from £1,1 billion to £0,3 billion in August. The annual decline increased from -3,7% to a record -3,9%.

In the US, private revenues fell by 2,7% a month in August – combined with other months, this almost offset the April surge on government incentives.

In Australia, the retail outlet plummeted 4,0% per month in August.

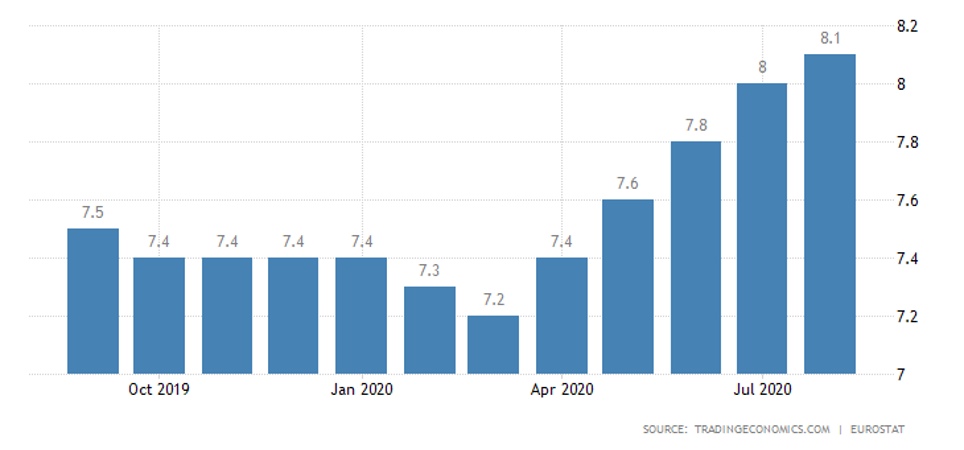

In the Euro Area, unemployment is the worst in two years:

And in Japan, in more than three years.

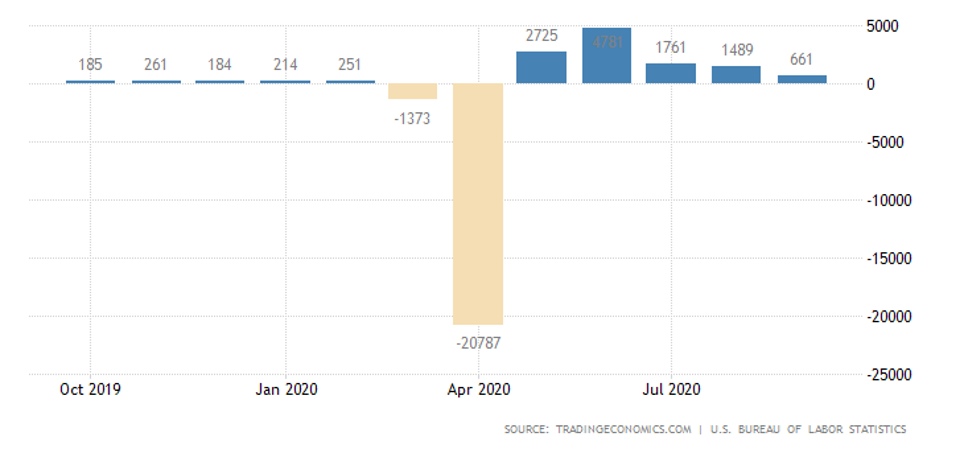

In the US, jobs in September added much less than expected:

Unemployment fell only because of the mass exodus of people from the labor force – the ratio of the latter to the adult population fell to a minimum in 4 months:

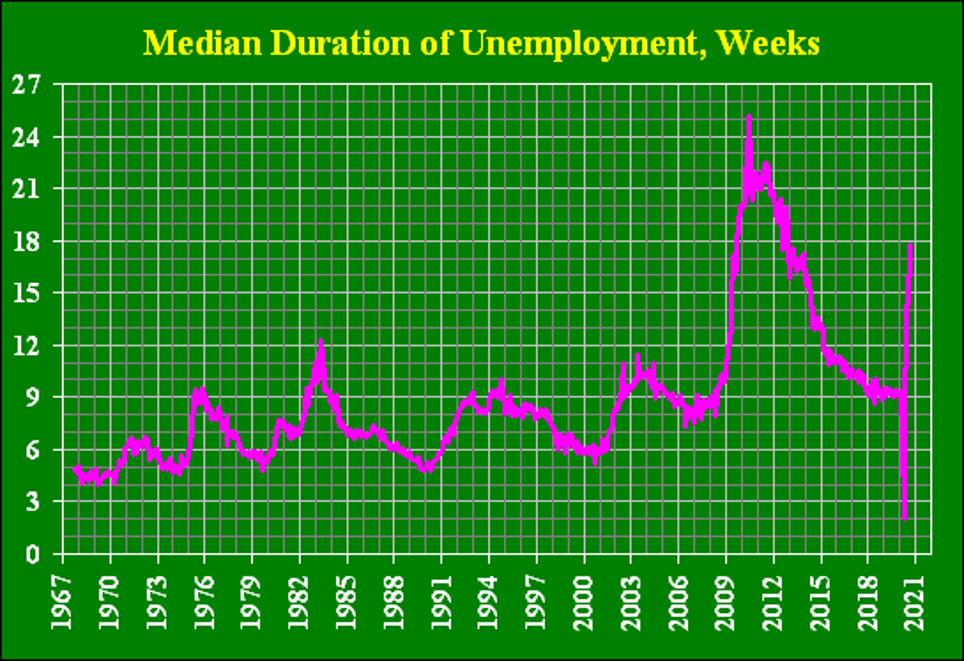

The median period of unemployment has peaked in eight years:

Probably a further deterioration: due to the loss of incentives and the lack of new ones, a number of large corporations began announcing massive layoffs of staff: just this week Disney announced a reduction of 28,000 people, American Airlines announced a reduction of 19,000, United Airlines announced a reduction of 12,000, Shell – 9 thousand, Allstate (insurance giant) – 3,8 thousand, Goldman Sachs – 400.

Summary: Overall, the picture roughly coincides with the previous week: business activity slows down, unemployment grows, no «growth points» are obviously not observed. The investment process is stalled (which, however, began before the COVID-19 epidemic), which is in line with the theory that the Mikhail Khazin Foundation for Economic Research has been developing in recent years.

Given the decline in income, rising unemployment and a decline in business activity, it would be very naive to expect a recovery in the investment process. This means that the process of correcting structural imbalances will continue – in full conformity with the theory. It appears that by the end of the year this process will have dominated the