Period: 20-26 September 2020

Top news story: This week’s top story is the resumption of quarantines in various countries. The trend was set for half a month ago, but it was this week that it became clear that the world economy would remain under the impact of the notorious “second wave” for many months to come.

Here again, it makes sense to describe in detail the possible reasons for such a development of events. In theory, there may be a real increase in the incidence of COVID-19, but why is this increase starting now? However, our previous two reviews (and, looking forward, this one too) show that the autumn has not lived up to the optimistic expectations. It is clear that the world economy will return to decline without recovering from the spring and summer turbulence. This means that the authorities of all the major economies of the world (small ones allow themselves to blame the big ones) must look for objective grounds for their mistakes.

For the readers of our reviews, the situation is very clear: the coronavirus quarantine has simply triggered the structural crisis of the world economy. For that reason, we warned early in the summer that the wait for recovery was unrealistic. However, political expediency and the dominant liberal economic theory demanded the opposite and, as a consequence, there is now an urgent need to find an «objective» factor to blame for the fact that growth has not occurred.

It should be noted that, in an apparently nervous market environment close to panic, it is not possible to consider them as a source of reliable information on which to base any outlooks. Prices may rise or fall, indices may surge (as they did on Friday 25 September) or fall (as they did at the beginning of the week), but this has nothing to do with long-term (and less often medium-term) trends. Look at macro-data and, if possible, interpret it according to an adequate theory.

Macroeconomics

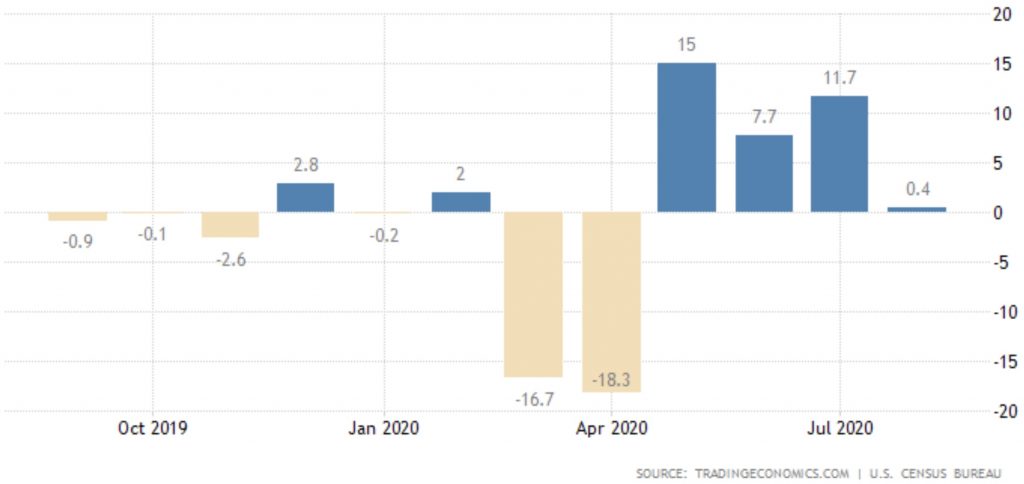

The monthly increase in orders (as of August) for durable goods in the United States almost reached zero in August; the annual decline remained significant (-4,6% excluding inflation):

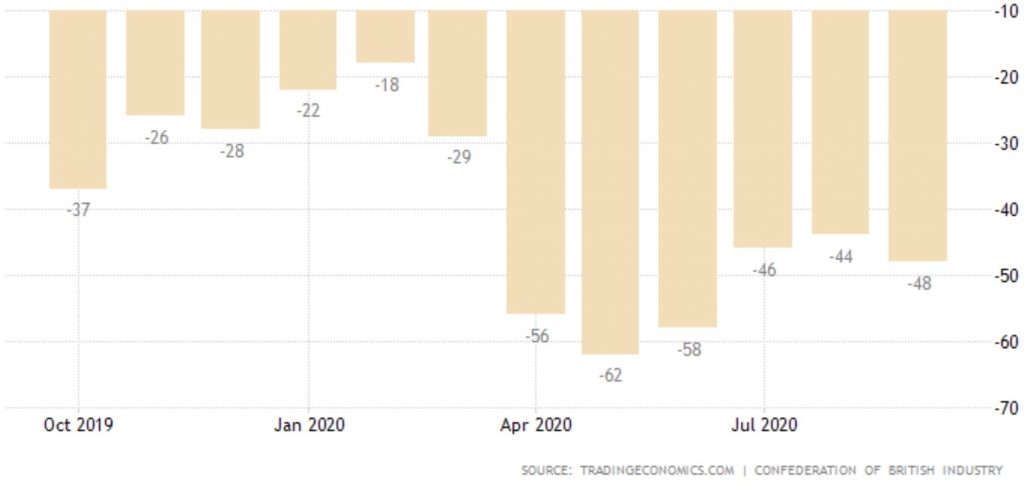

The balance of industrial orders in Britain suddenly began to deteriorate in September:

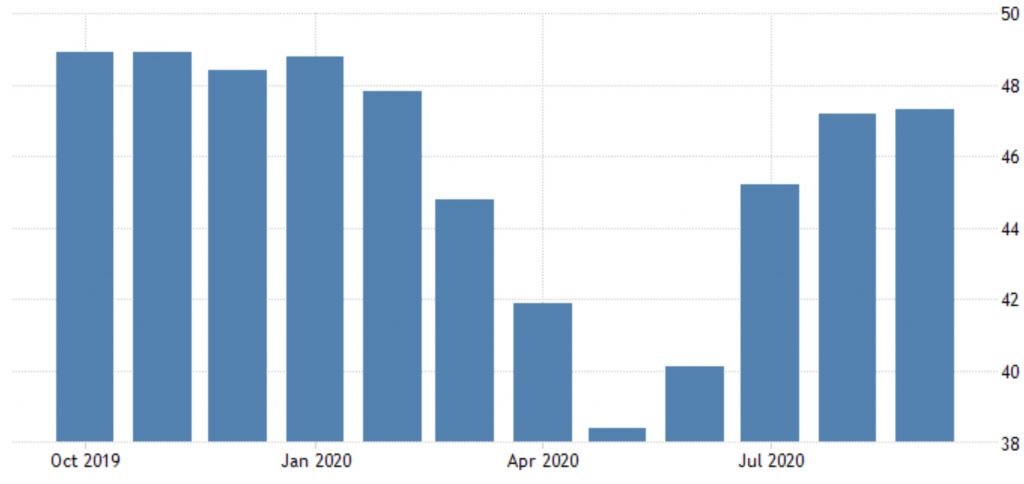

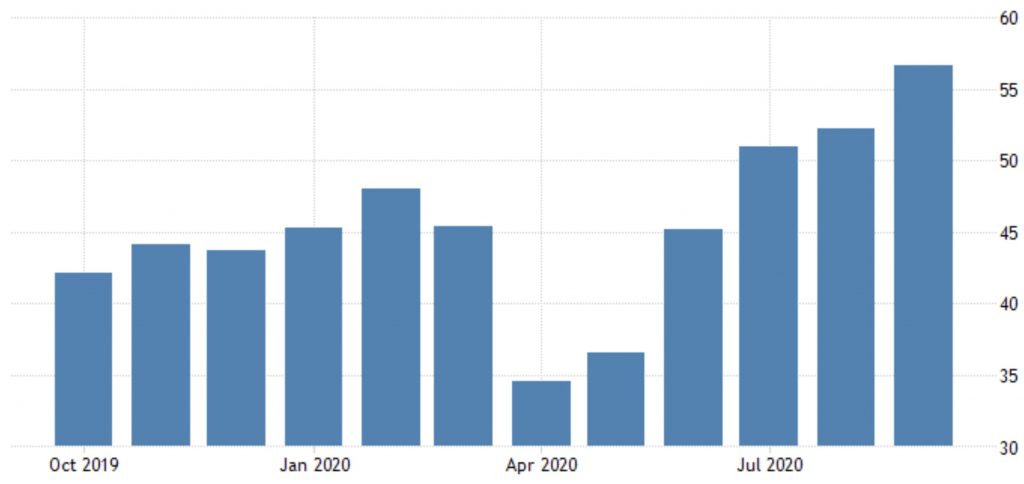

Japan’s PMI nearly stopped improving in September, remaining deeply in recession:

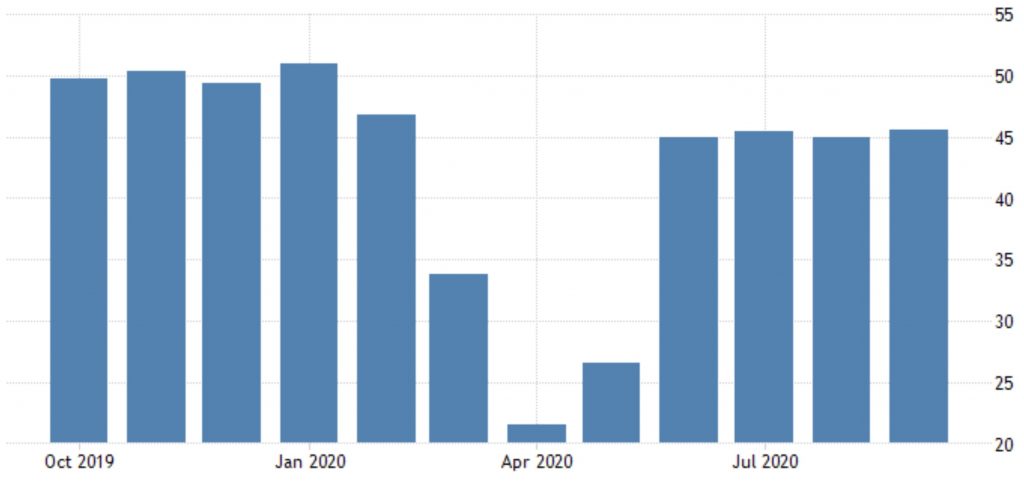

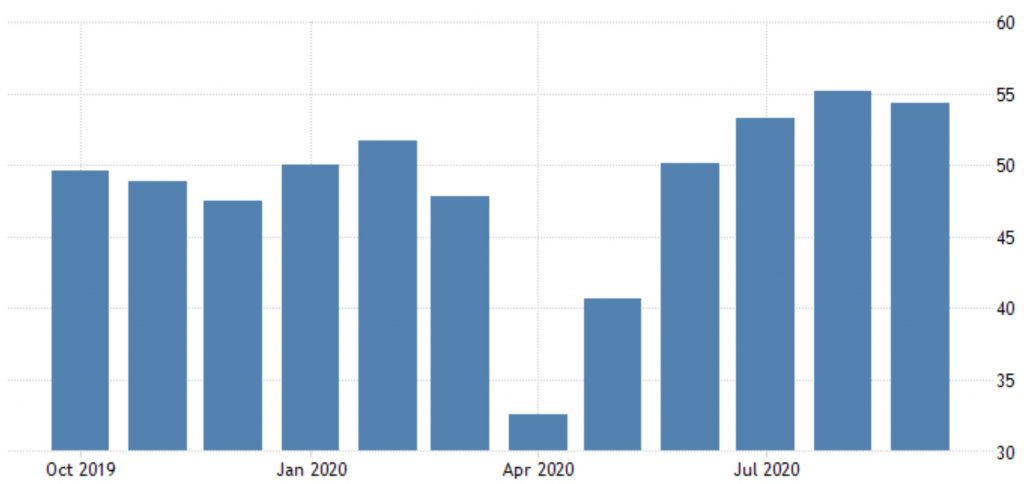

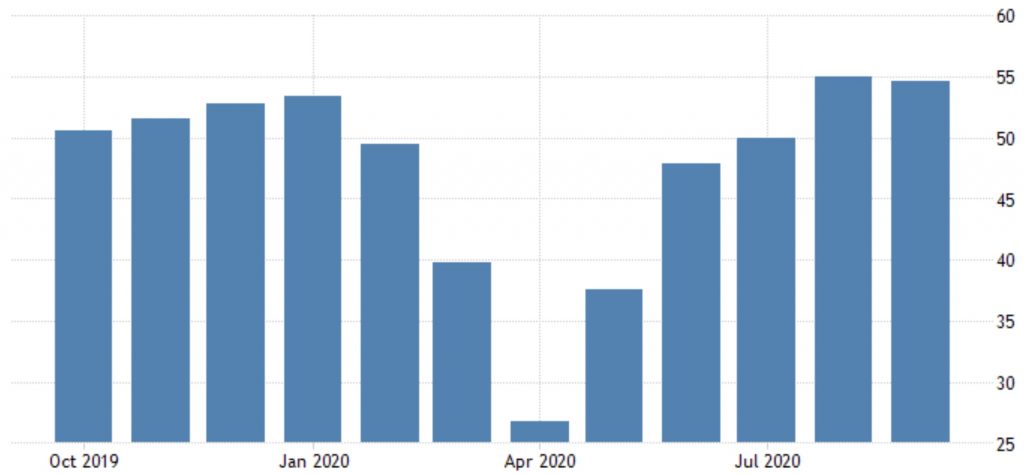

France’s manufacturing PMI improved slightly, but the service sector collapsed into recession.

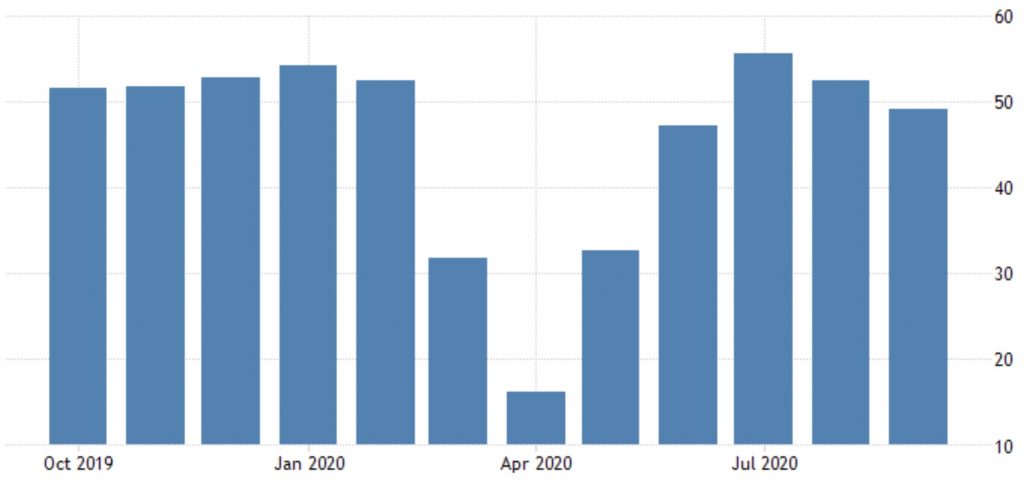

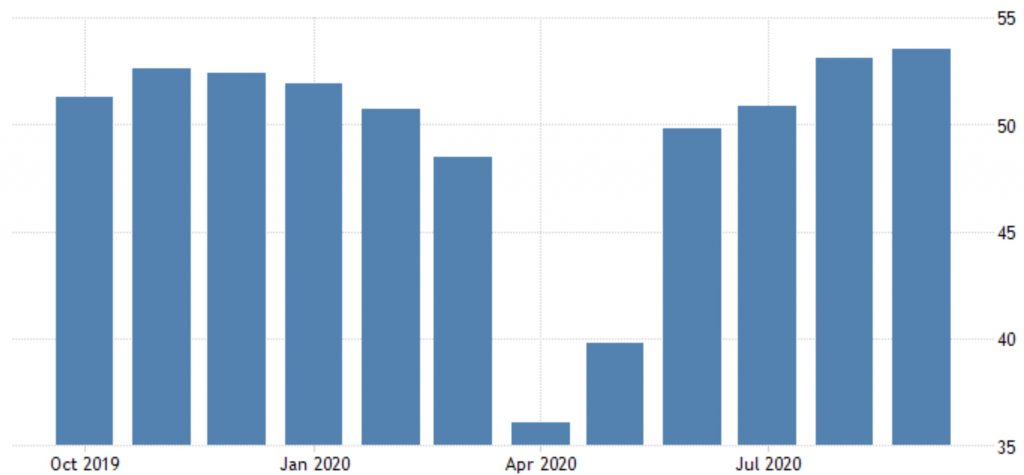

The same picture in Germany – only the absolute values of the indices there are slightly better:

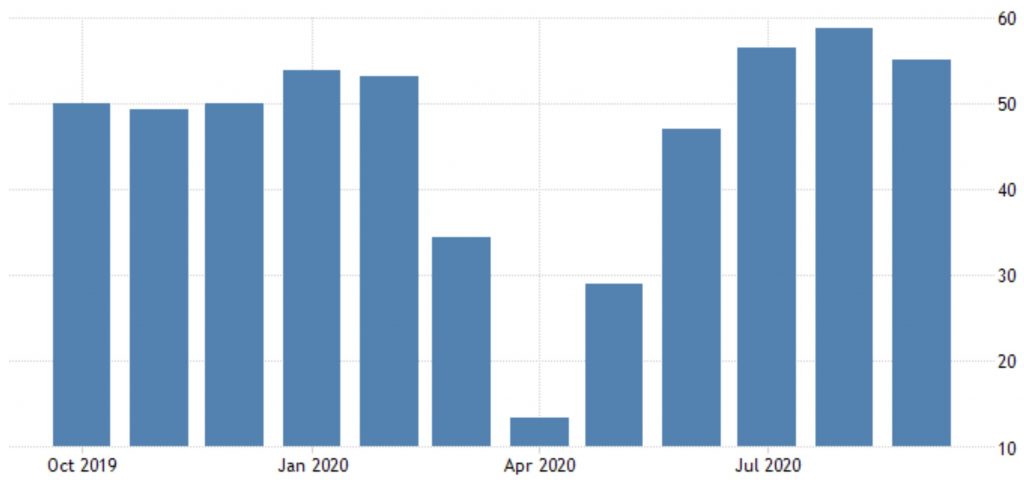

Overall, the Euro Area performance is somewhere in the middle between Germany and France.

In Britain, the decline in all sectors – but the performance so far remains positive:

Note that since the PMI index is a poll result, the optimism described at the beginning of the review still plays a role. The public mood is still far from panic.

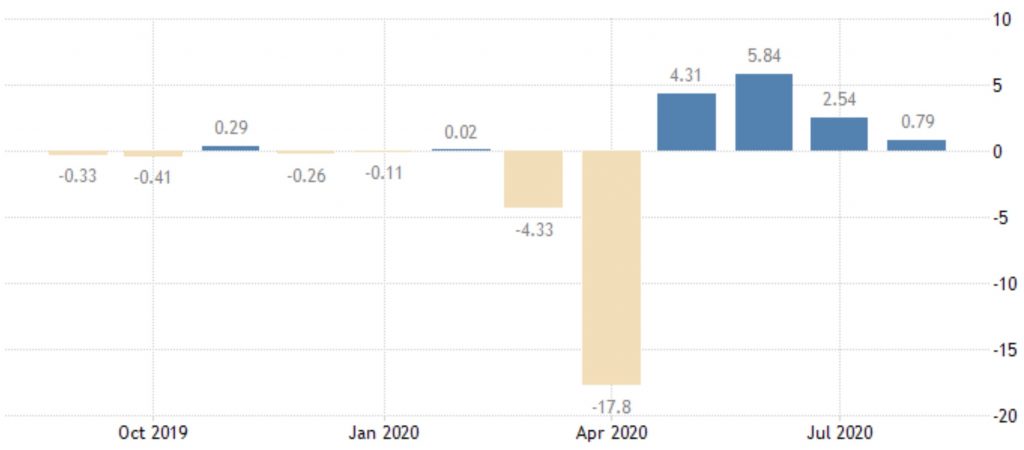

In the US, expansion stabilization:

But the more objective Index of National Activity in the United States from the Federal Reserve Bank of Chicago continued to reduce the pace significantly in August:

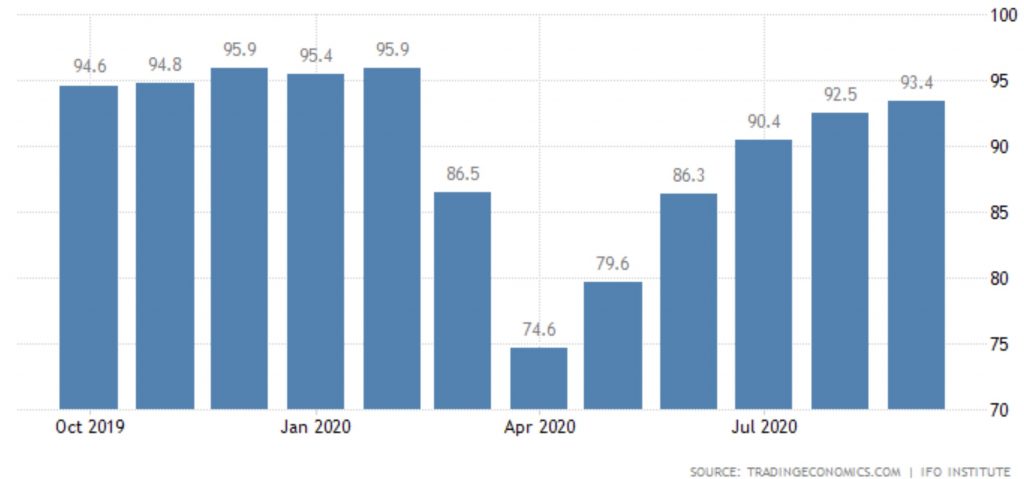

The German business climate according to IFO is improving slower than expectations:

South Korean sentiment deteriorated sharply in September:

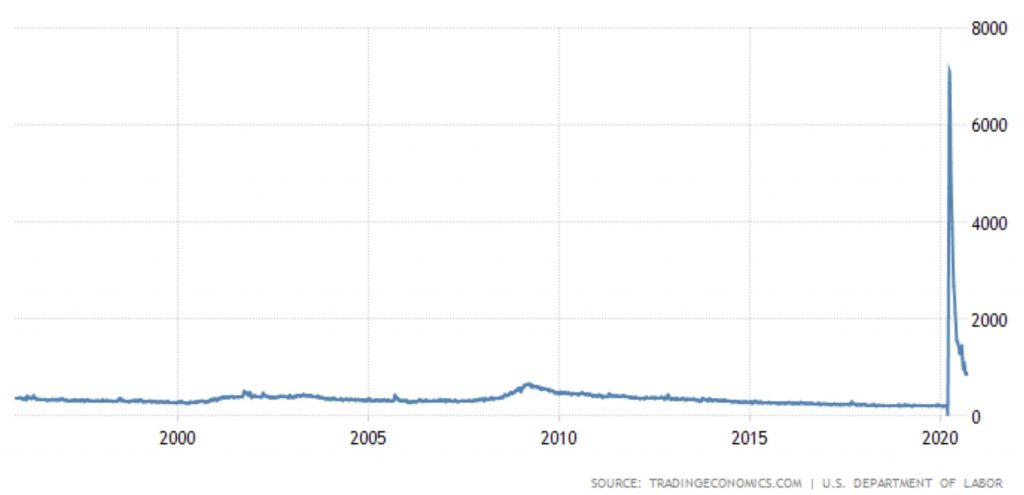

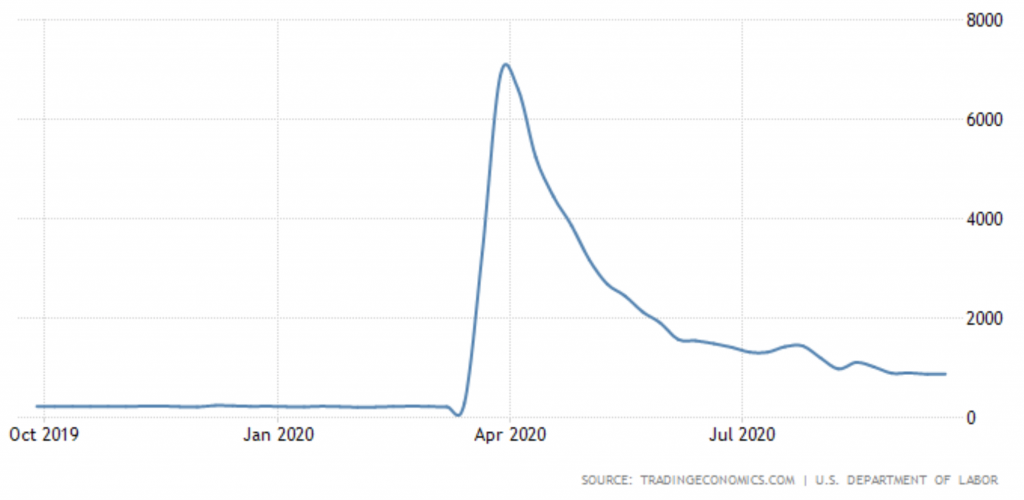

Weekly US jobless claims were maintained at levels that significantly surpassed the 2009 peak:

In more detail, the situation in recent months is as follows:

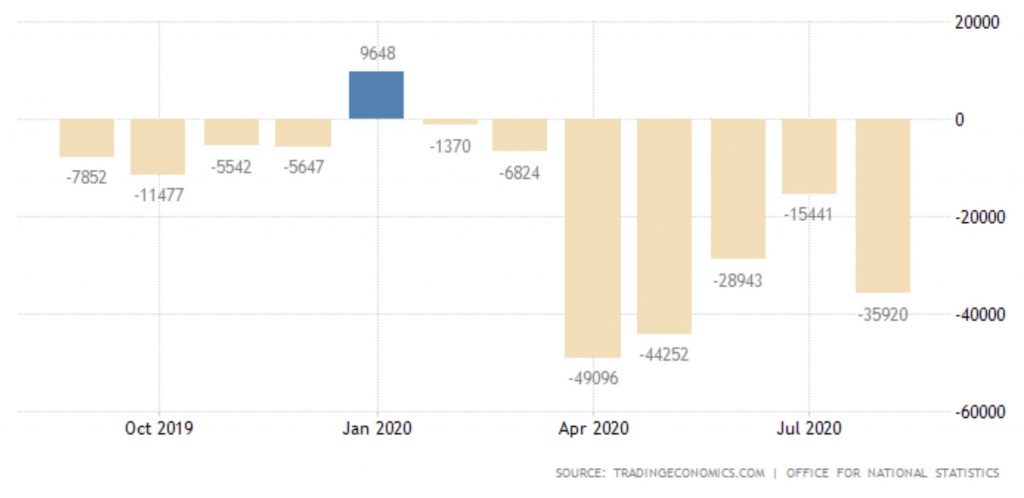

Britain’s budget deficit increased significantly in August:

The Mexican Central Bank cut the rate by 0,25% to 4,25%.

The Central Bank of China has left its policy completely unchanged

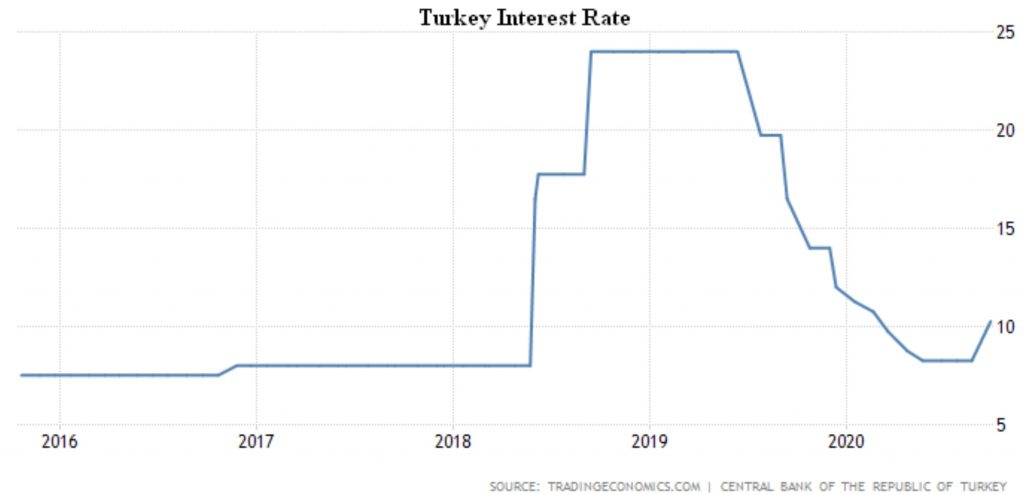

Whereas the Central Bank of Turkey was forced to raise the rates by 2% at once (up to 10,25%) due to inflation and a weak Turkish Lira:

Summary: It is very difficult to assess the objective economic situation of the following conditions: distortion of statistical data, the huge (still unknown) emissions and, as a result, the far-from-market behaviour of most market players. Consumers come first in this case. A number of individual indicators contradict each other and, for this reason, their correct interpretation becomes a priority.

The Michael Khazin Foundation for Economic Research in this situation relies on its long-standing experience of studying the theory of crisis: the first articles were published back in 2000 and the first book «Sunset dollar empire and the end of the «Pax Americana» – in 2003. It is these studies that give us reason to assess some statistical data and forecast the situation. So far, these forecasts are coming true, so we recommend that all our readers assume that there will be no economic growth in the coming years.