September 24-30,2022

Big news. There are two main news this time, and it’s hard to even say which one is the main one. The first is the blowing up of the Nord Stream and Nord Stream 2 gas pipelines, carried out by the United States and Great Britain. Formally, this has not yet been proven, but there are two main arguments. One – more than 90% of Germans think so, which is surprising in itself. The other is that the entire horde of liberal (and there are no others in the West) media is silent as grave. The conclusion from this is simple – they were ordered not to stir up the topic, which in itself clearly indicates who is to blame.

But there is another piece of news. In the middle of the week the Bank of England, in fact, opened an unlimited issue of the pound sterling. Most likely, according to a number of experts), the reason was the state of individual financial institutions that were on the verge of bankruptcy. As a result, the pound sterling collapsed:

Both events signify the collapse of the Bretton Woods financial and economic model. The destruction of the international logistics infrastructure has opened a Pandora’s box (“What, could it be?”, An old joke) and now similar events will occur more and more often, there are no more forces that could prevent this.

And the events in England show that the US no longer has the resources to maintain the stability of the world monetary system. It should be noted that the elections in Italy became another confirmation of this. The right-wing coalition that won the elections quite harshly said that it would protect the standard of living of the population. It is economically impossible to do this within the euro zone, which means that Italy will leave the euro zone and revive the national currency, which can be issued and support the social part of the budget.

Numerous statements by the Fed leaders this week showed that they are only interested in the situation in the US, primarily in the reduction of inflation. How they will do this is the question, there is no reason for this, and the readers of our reviews even know, unlike Fed officials, why. But the stability of the global financial system is clearly not in the interests of the American regulator today, or is a deeply secondary task.

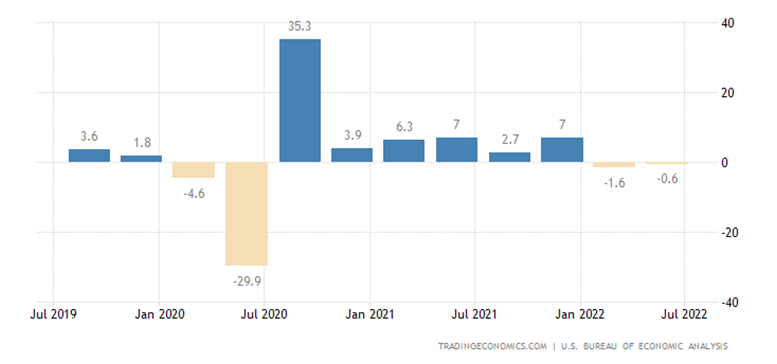

Macroeconomics. 2 consecutive quarters of falling US GDP confirmed the final estimate for the II quarter:

United States GDP Growth Rate

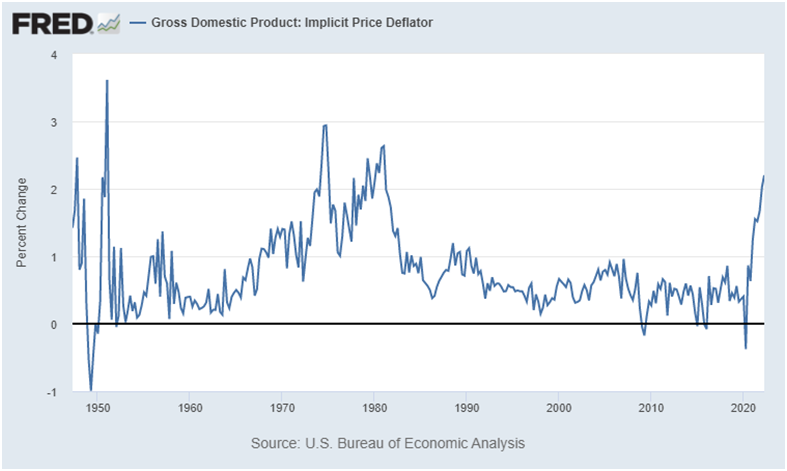

At the same time, the deflator +2.2% per quarter is the highest since 1981:

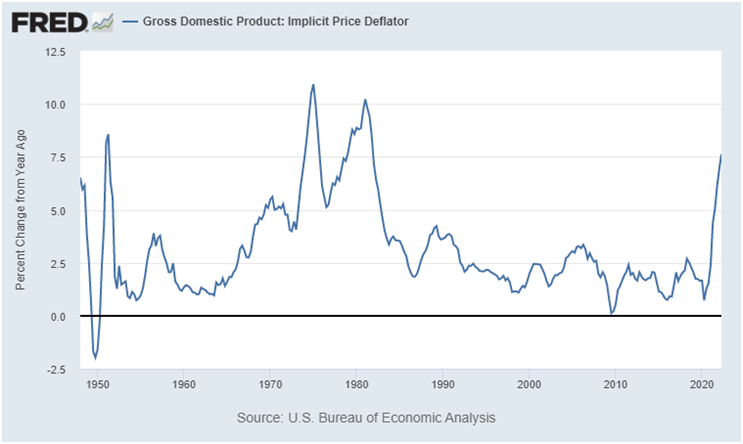

And +7.6% per year – also the highest since 1981:

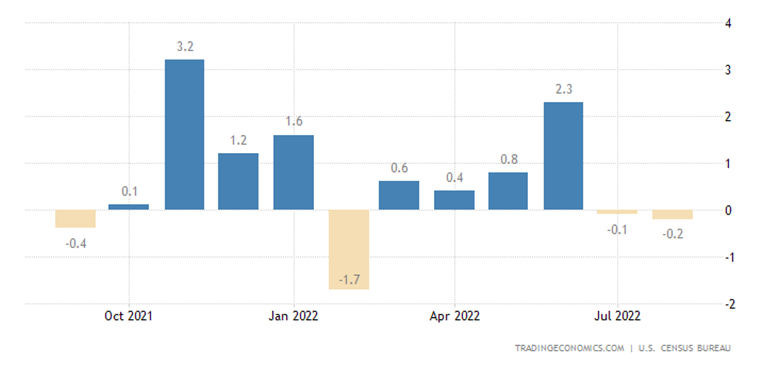

US Durable Goods Orders Decline for 2 Months in a Row:

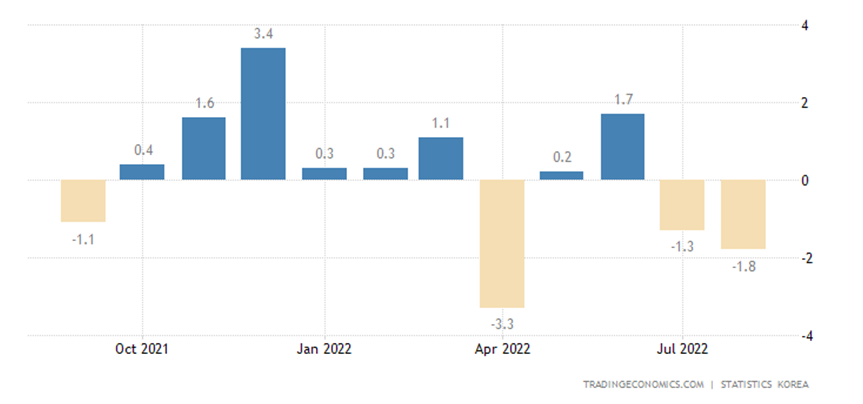

Industrial production in South Korea has been declining on a monthly basis for 2 months in a row:

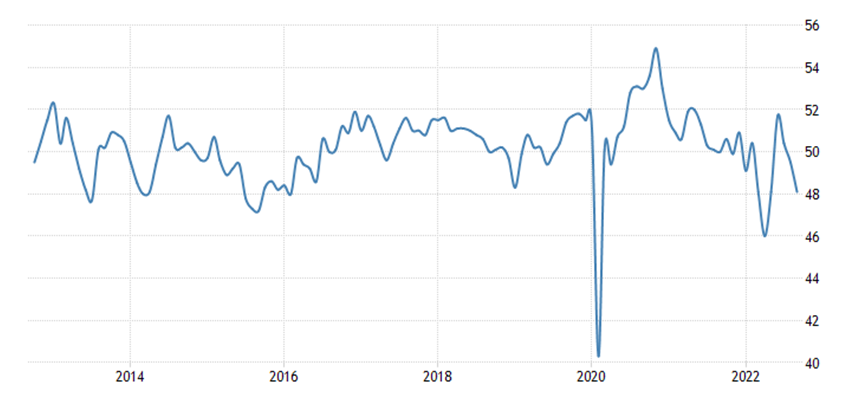

Japan manufacturing PMI weakest in 20 months:

And in China, it went deep into the recession zone (48.1), selling prices are falling the most in 7 years:

The National Activity Index in the USA from the Chicago Fed returned to zero, out of the last 4 months, only 1 was in positive territory:

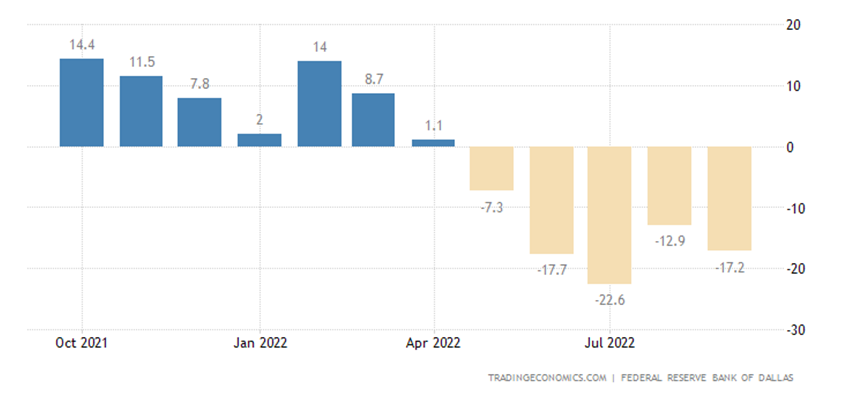

The regional industry index in the Texas Fed zone in the US has been in the red for 5 months in a row:

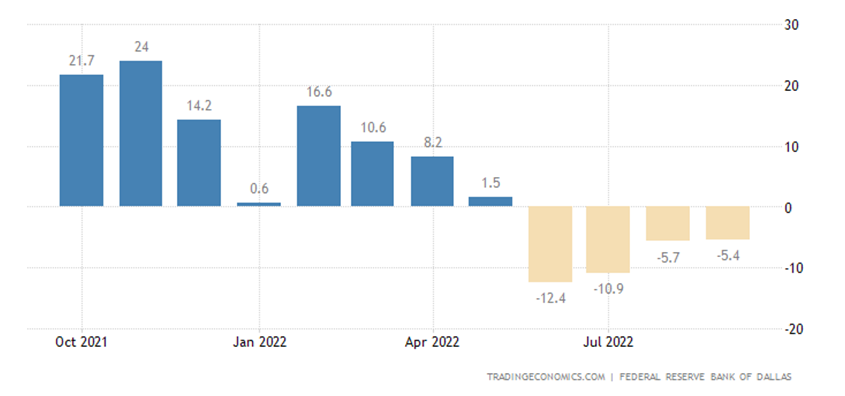

And its index for the service sector – 4 months in a row:

Activity in the US Midwest (Chicago PMI) fell into the downtrend zone (45.7) for the first time in 27 months:

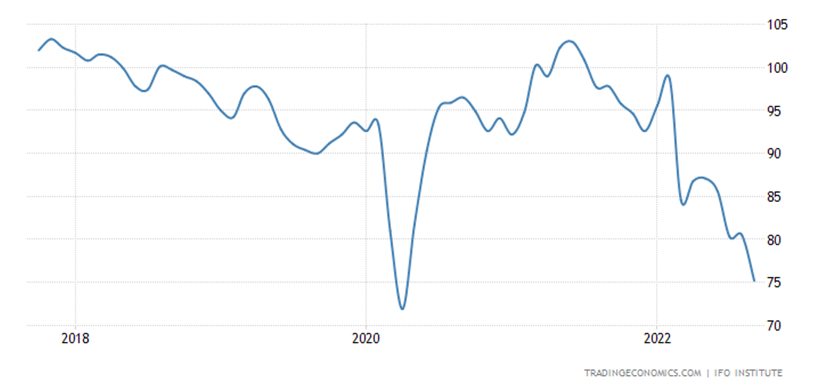

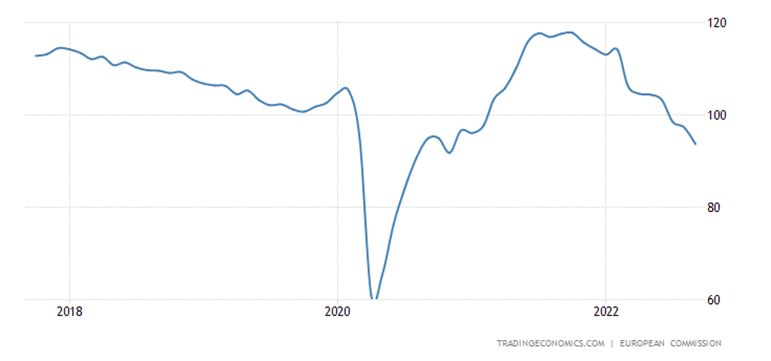

The business climate in Germany (IFO review) has been at the bottom since April 2020, and before that – since 2009:

Moreover, the expectations component has almost surpassed the covid anti-record:

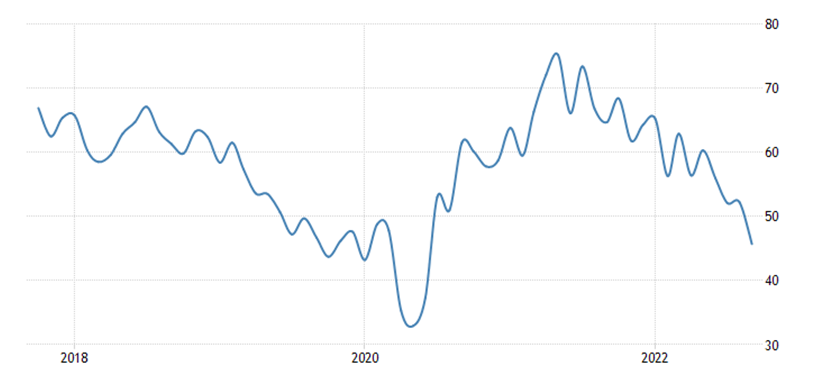

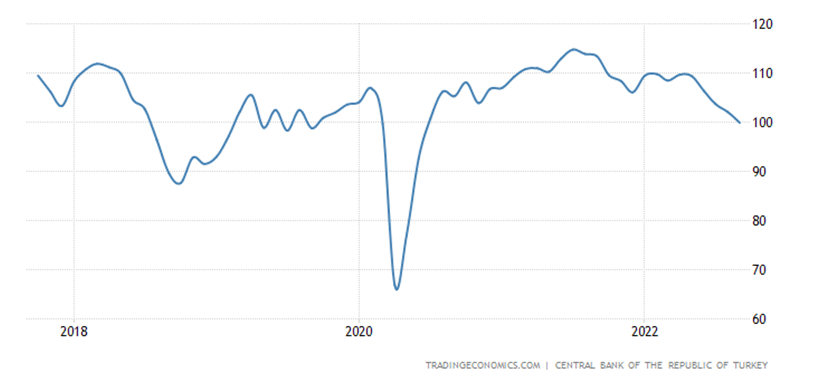

Business confidence in Turkey at its lowest in 27 months:

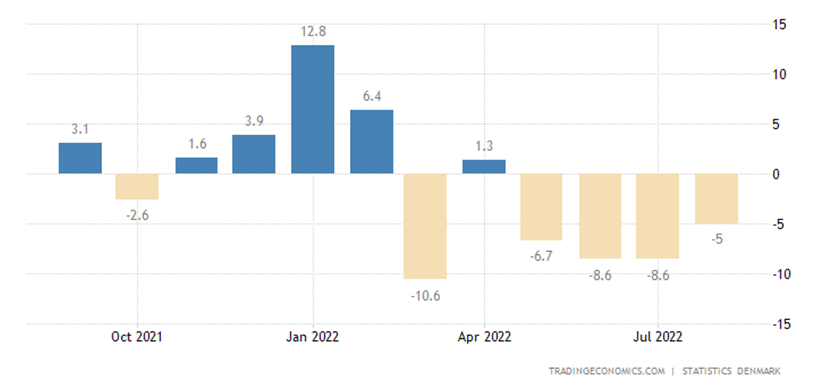

In Denmark – for 2 years:

In South Korea – in 22 months:

As in Austria:

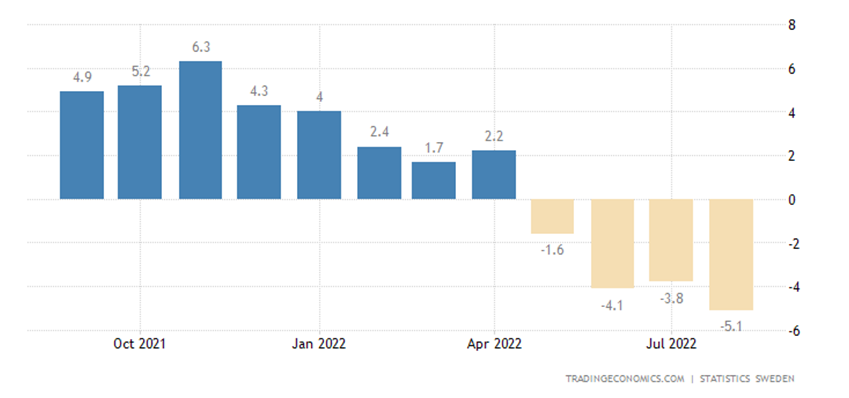

In Sweden – in 20 months:

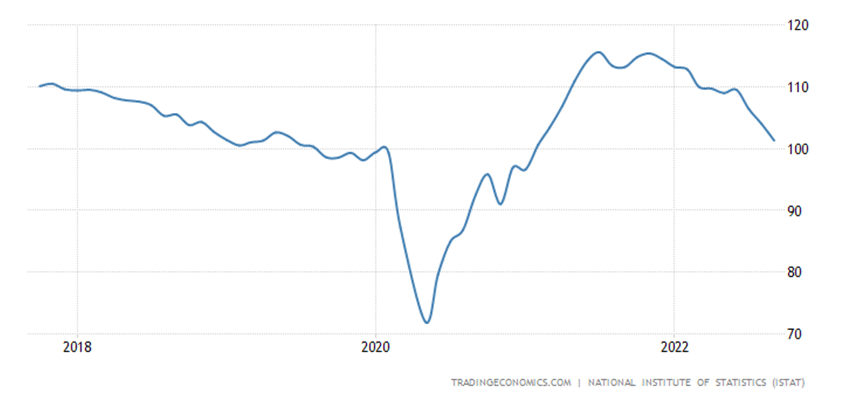

As in Italy:

Economic sentiment in Switzerland near record lows

In the EU, they are the worst in 22 months:

Canada’s business barometer is at its lowest in 26 months:

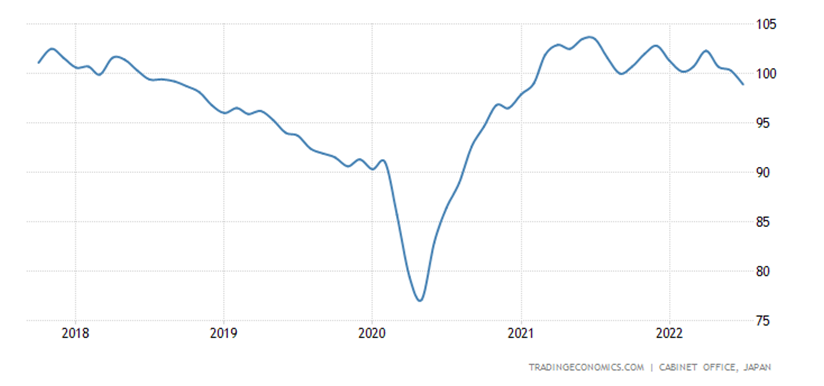

Leading indicators in Japan at the bottom for 1.5 years:

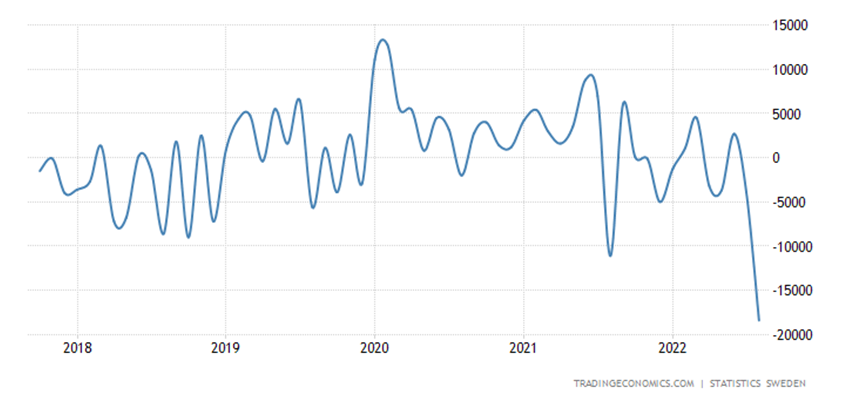

Sweden has a record foreign trade deficit:

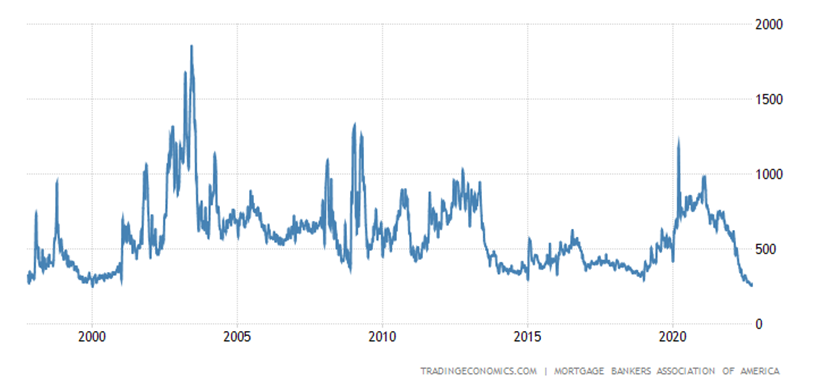

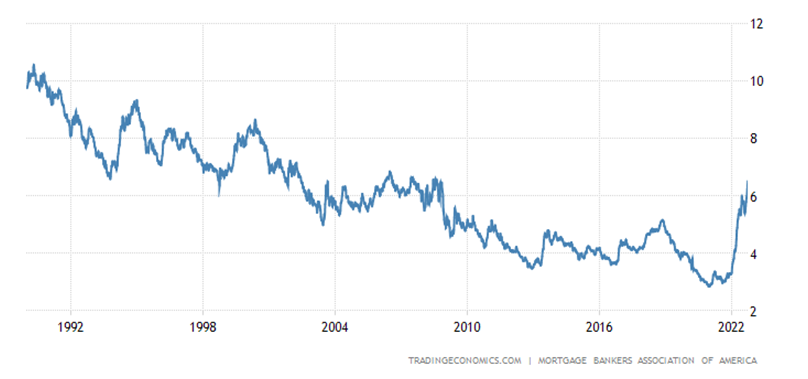

U.S. mortgage applications hit 22-year low:

Against the backdrop of a 14-year peak in interest on loans, they are near the peaks of the 21st century:

Prices for single-family homes in the US -0.6% per month – the worst dynamics since 2011:

And for a similar S&P/Case-Shiller index – since the beginning of 2012:

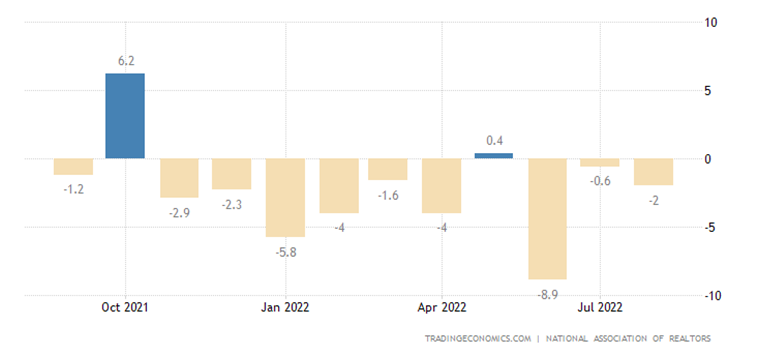

U.S. pending existing home sales monthly in the negative 10 months out of the last 12:

Why the annual dynamics is approaching a record low (-24.2% per year):

CPI (Consumer Inflation Index) Germany +10.0% per year – 70-year peak:

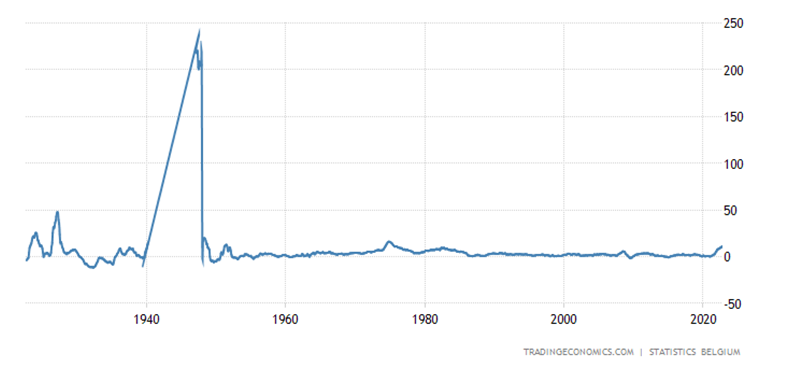

Belgian CPI +11.3% per year – the highest since 1975:

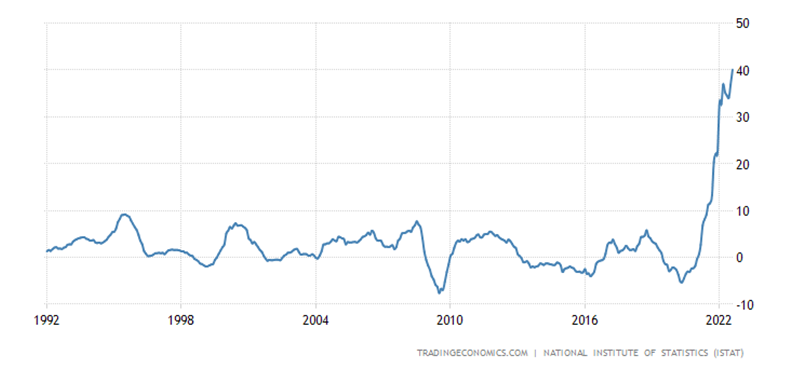

Italian CPI +8.9% per year – the highest since 1985:

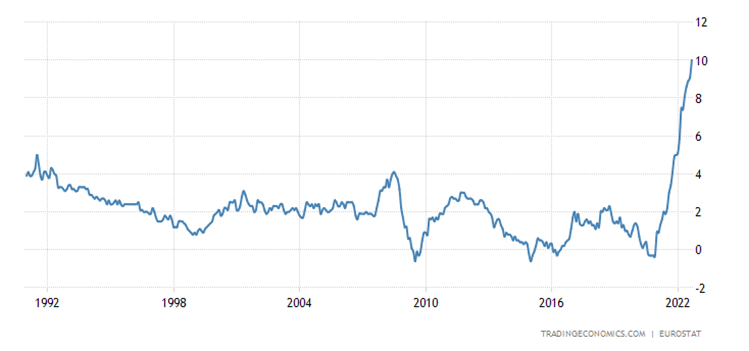

Eurozone CPI +10.0% per annum – a record for 32 years of data collection:

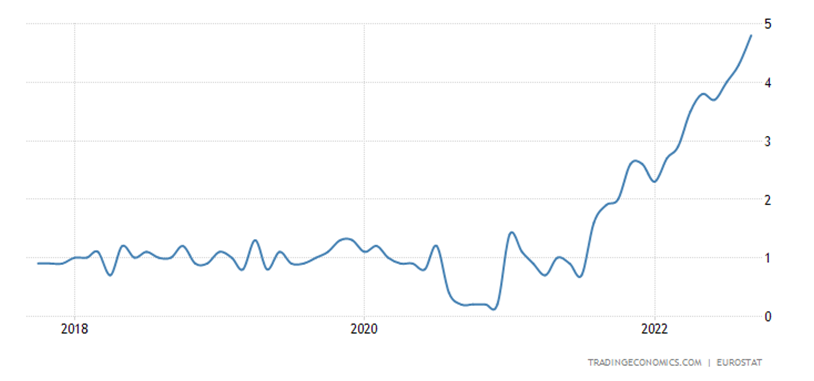

“Net” (excluding highly volatile components of food and fuel) Eurozone CPI +4.8% – and it is also a record:

Which, by the way, suggests that the problems in the EU economy are not only in energy prices.

PPI (industrial inflation index) Italy +40.1% per year – a record for 31 years of observation:

PPI France +29.5% per year – also a record figure:

Retail sales in Denmark remain in the annual red for 4 months in a row:

As in Sweden:

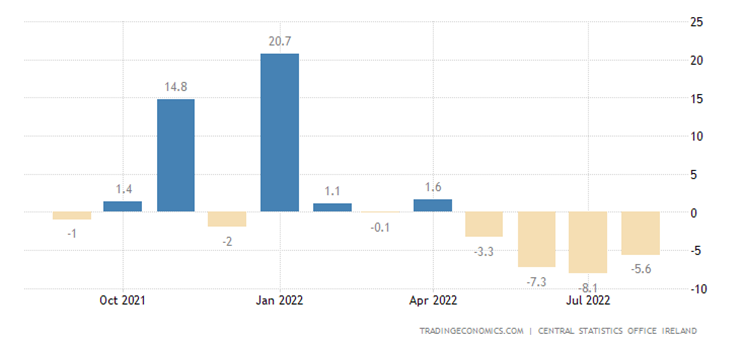

And in Ireland:

In South Korea – 8 months:

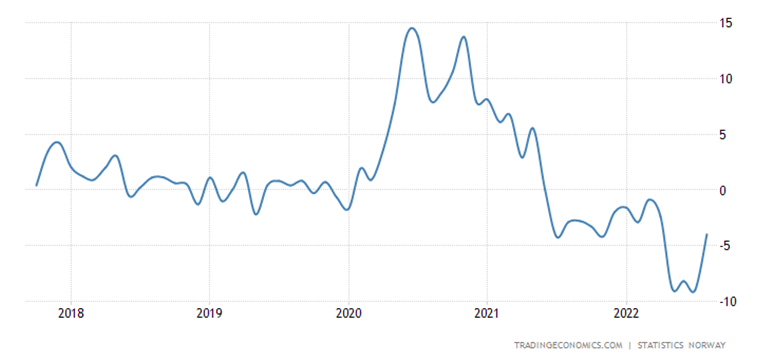

And in Norway – already 15 months:

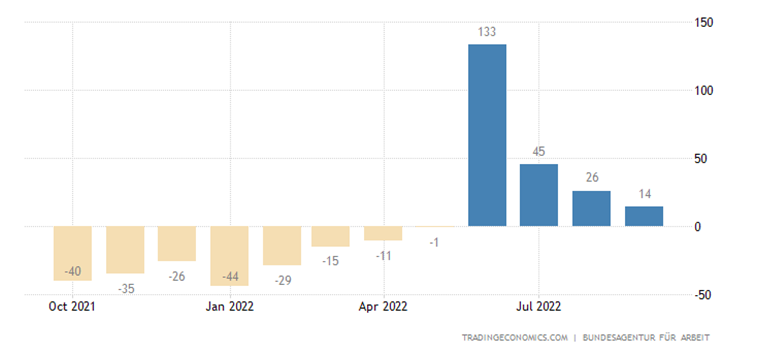

In Germany, unemployment is growing for 4 months in a row due to Ukrainian refugees:

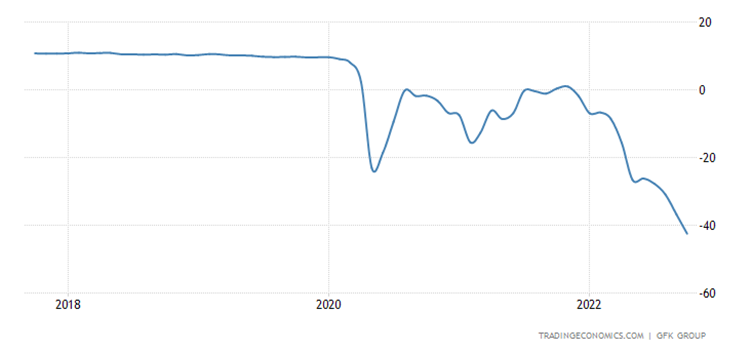

Finns are the most pessimistic for all 27 years of keeping statistics:

The Germans are also record-breaking:

Note that this is an estimate before it became known about the exploded gas pipelines.

And the French:

The eurozone as a whole has an all-time poor performance over the 38 years of data collection:

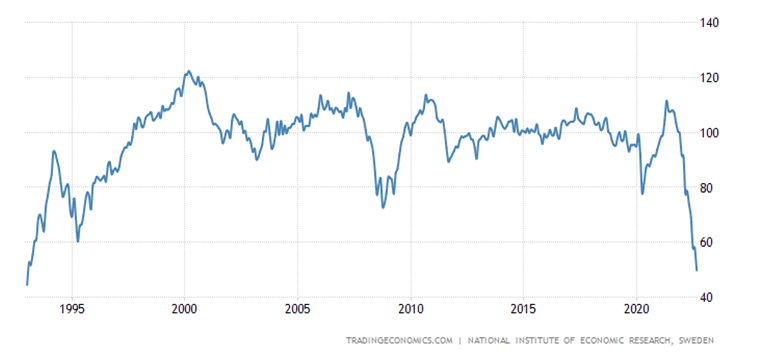

Swedes have the worst mood since 1993:

Against the background of record high inflation expectations (+11.8% per year):

The Central Bank of Mexico raised the rate by 0.75% to a record 9.25%.

The Central Bank of India raised the interest rate by 0.5% to 5.9%.

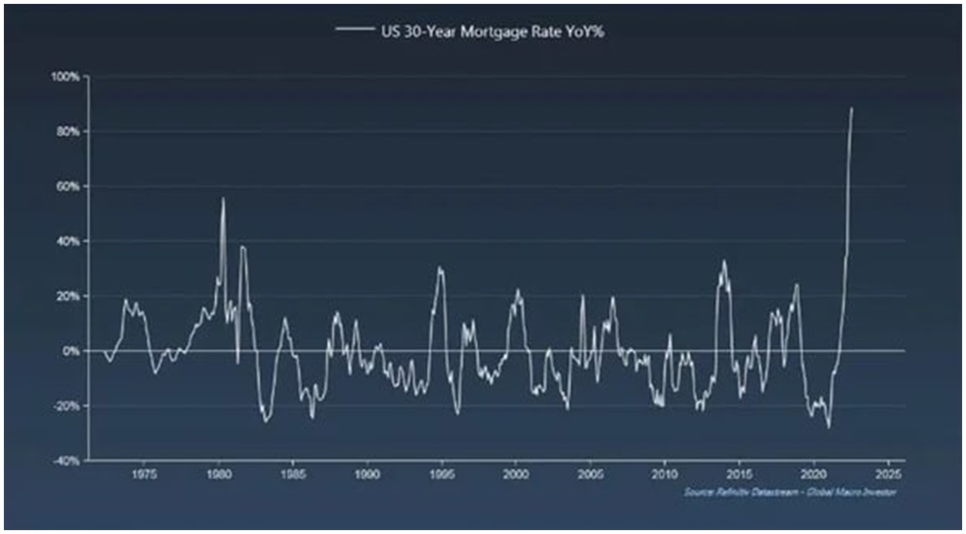

Main conclusions. We have returned to the situation at the beginning of the month, a typical picture of a structural crisis, when every month in various countries records is set for falling sales, rising prices or reducing production. As it usually happens, a sharp deterioration in individual countries is followed by a slight rollback, which official commentators then pay attention to, but we look at the systemic picture and it turns out to be quite typical. In addition, let’s add some pictures. The first is the relative cost of a 30-year mortgage in the US (absolute figures are approaching 7%):

Note that real incomes in the US are not growing, but falling, so it is not surprising that the volume of mortgages taken (see the previous section) is falling.

The second graph is consumer inflation in Germany’s most populated state of North Rhine-Westphalia:

It is already double-digit and it is possible that the reality is higher than the official figures. In any case, the gap with 45% industrial inflation is too high. And here we recall Powell’s reasoning from the beginning of last fall, when he said that the growth of industrial inflation in the United States is a short-term phenomenon and soon everything will return “to normal”. At that time, we wrote in our reviews that, on the contrary, consumer inflation would begin to catch up with industrial inflation.

We then turned out to be right and today we can say that with a high probability, the picture will be similar in Germany. That is, the growth of consumer inflation will continue. Regardless of the campaigns of the leadership of the European Central Bank. However, England has already shown the way, and the euro is quite actively falling against the US dollar.

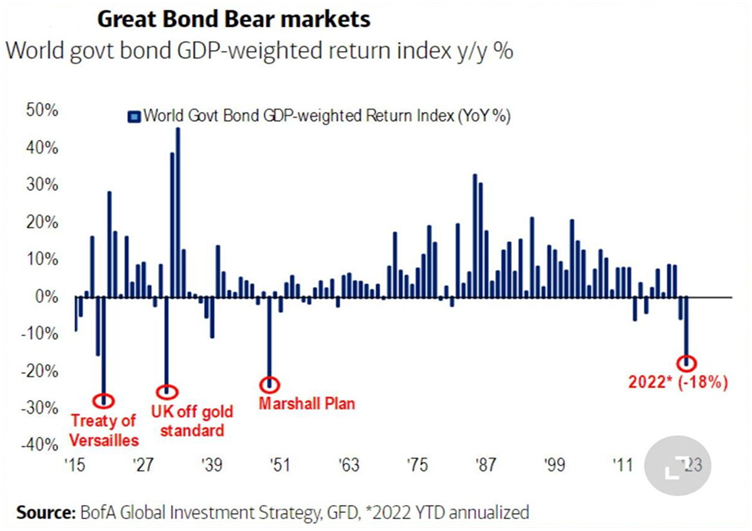

The last picture is the most interesting:

In fact, this is the scale of the crisis that has already occurred, based on the fall in the value of government bonds. As you can see, the three biggest crises have not yet come, but the process has just begun.

In conclusion, we note that there is a combination of individual recessions in different countries, which may not coincide in time, and the systemic process of the destruction of the dollar Bretton Woods model. However, who, like our readers, is warned, he is armed! So we wish you all a peaceful weekend and a successful work week!