Time period: 8-14 January 2022

Top news story. The world (but not yet in Russia) has already begun a more or less regular economic life, and the main news is Powell’s announcement that the Fed is ready to actively raise interest rates this year.

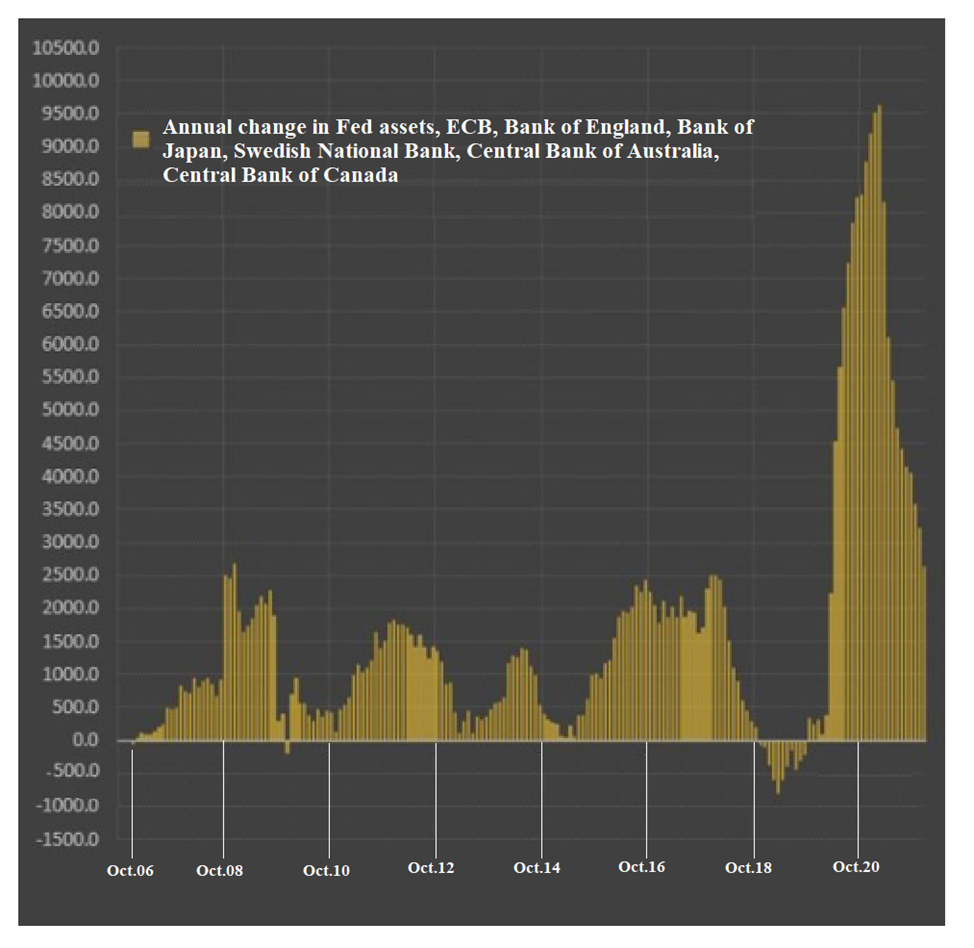

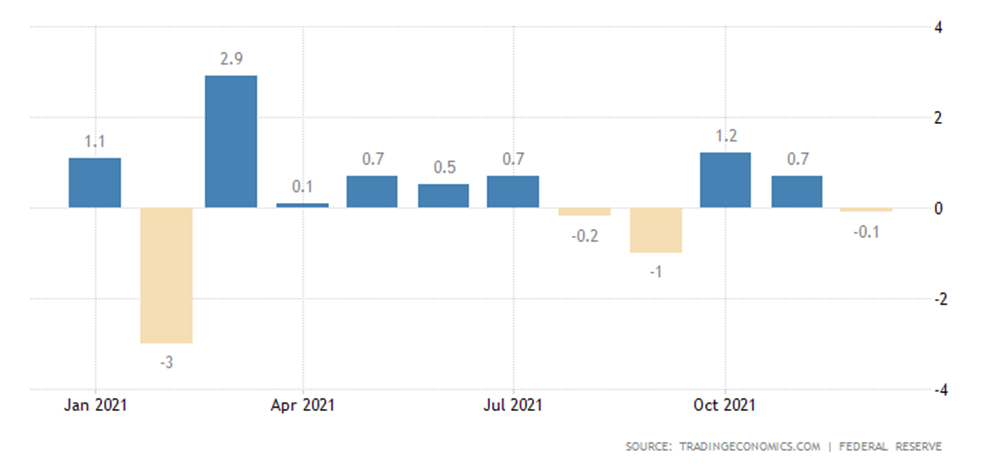

And if the annual emissions of major central banks have fallen to pre-crisis levels only:

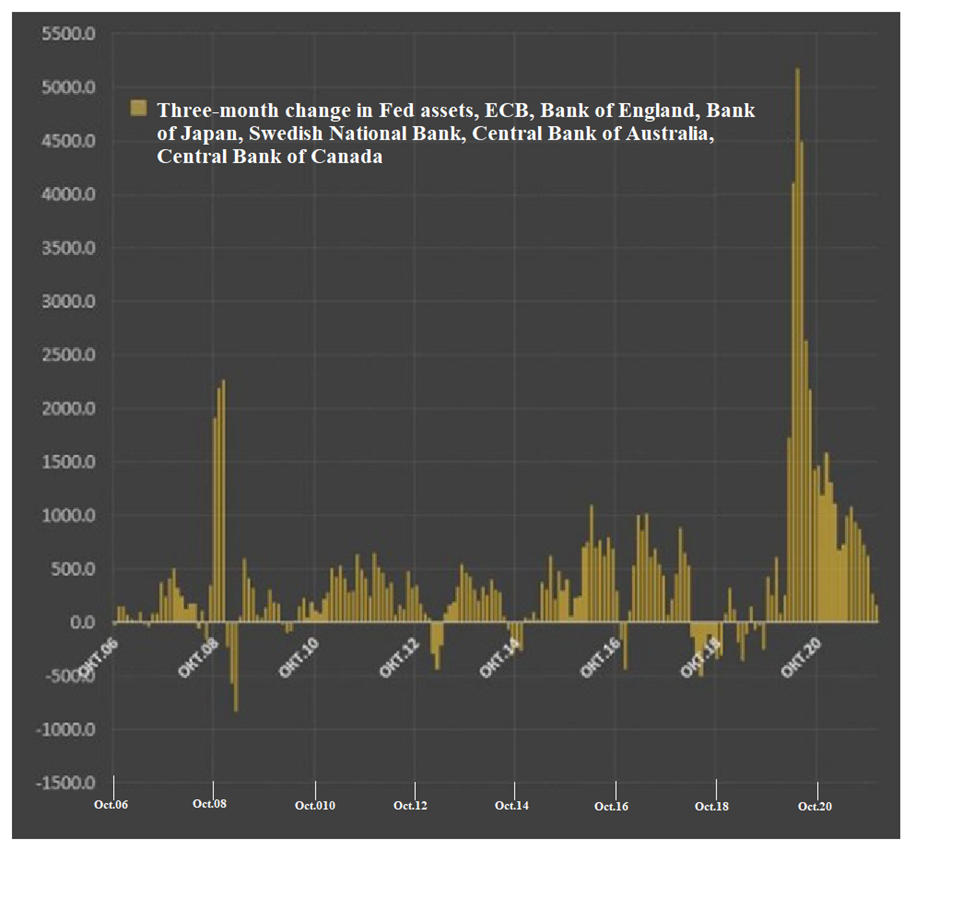

Then in a three-month period (we wrote about this in previous Reviews) the picture is much more stunning:

And after New Year’s, consumer prices began to rise in the United States. This situation explains the hawkish sentiment of the FDA leadership. But what about the debt? This is an open question, which we will answer in part at the end of the Review.

Macroeconomics

Industrial production in Mexico is -0.1% per month:

Industrial output in the US is -0.1% per month, manufacturing is -0.3%:

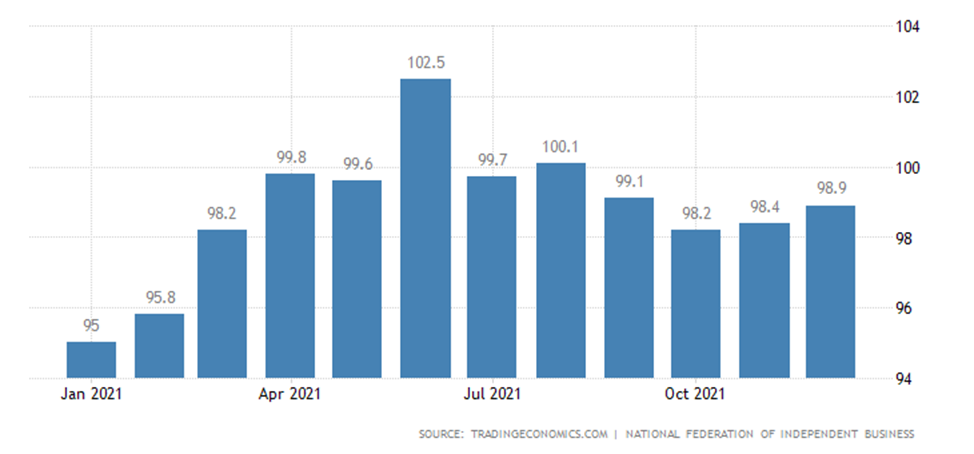

Not surprisingly, although US small business optimism has improved slightly (over the holidays!), it has remained below its long-term average:

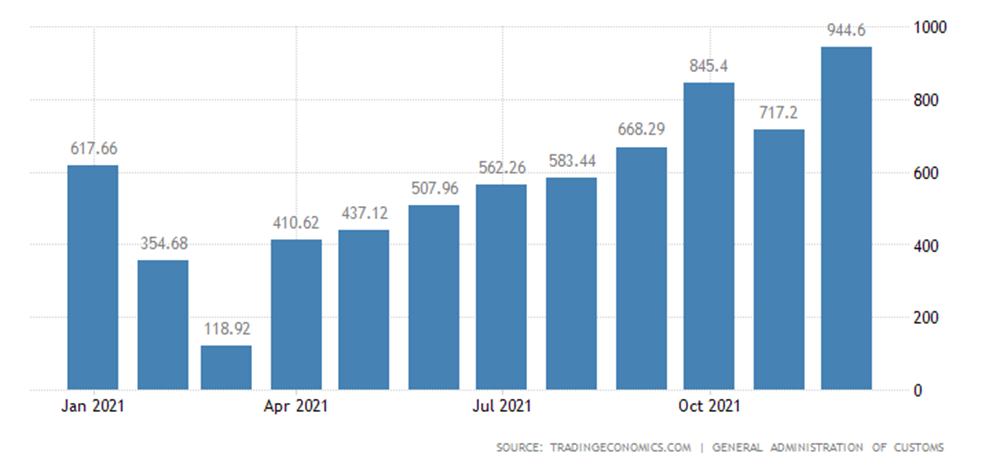

China’s trade surplus both in December and overall in 2021 was record:

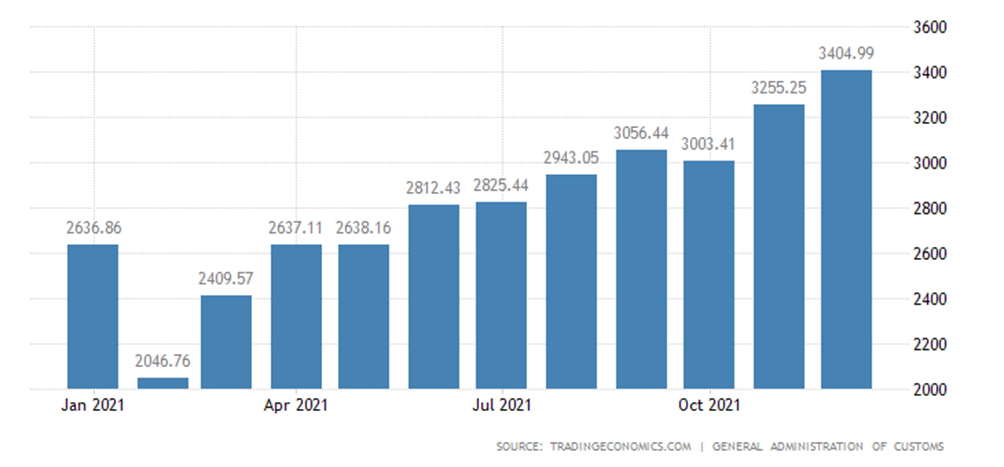

Thanks to record exports:

Inflation rates continue to break records.

CPI (Consumer Price Index) of France 2.8% per year, repeating peaks since 2008:

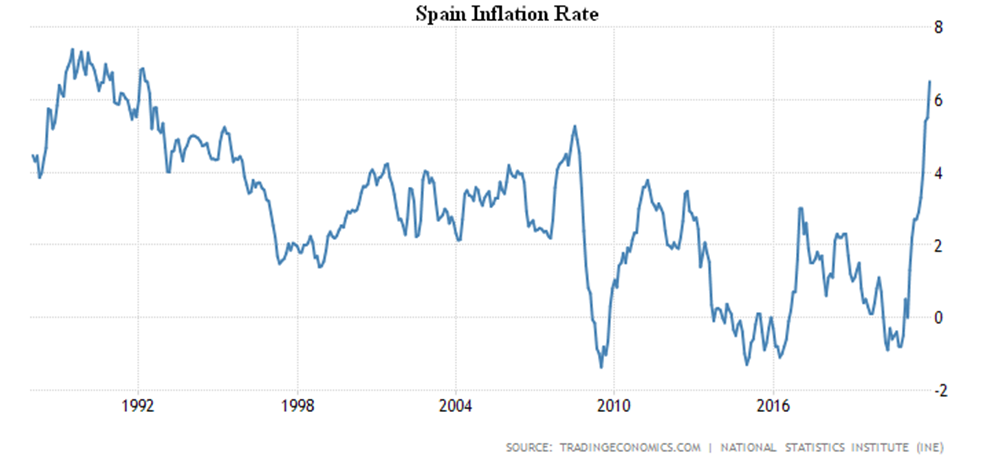

CPI of Spain +6.5% p.a., is at its highest since 1992:

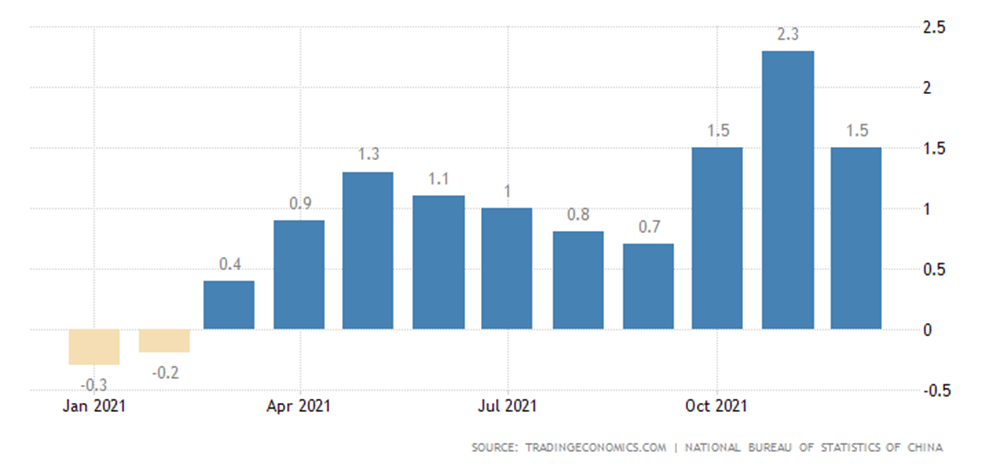

China’s CPI slowed from +2.3% to +1.5% p.a.:

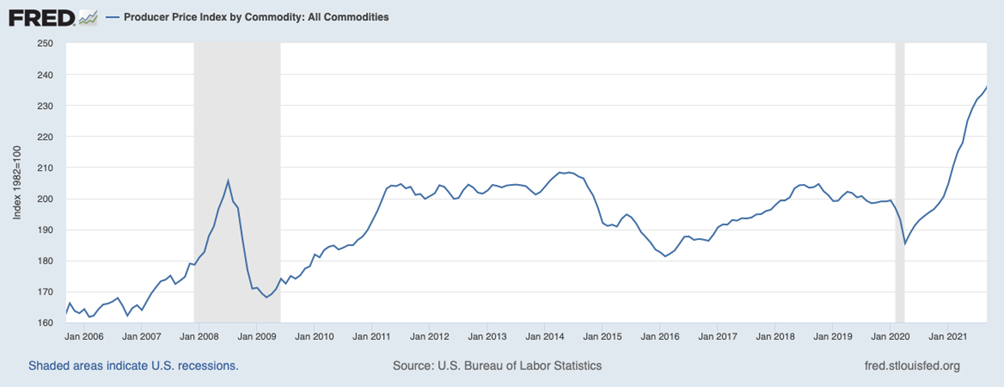

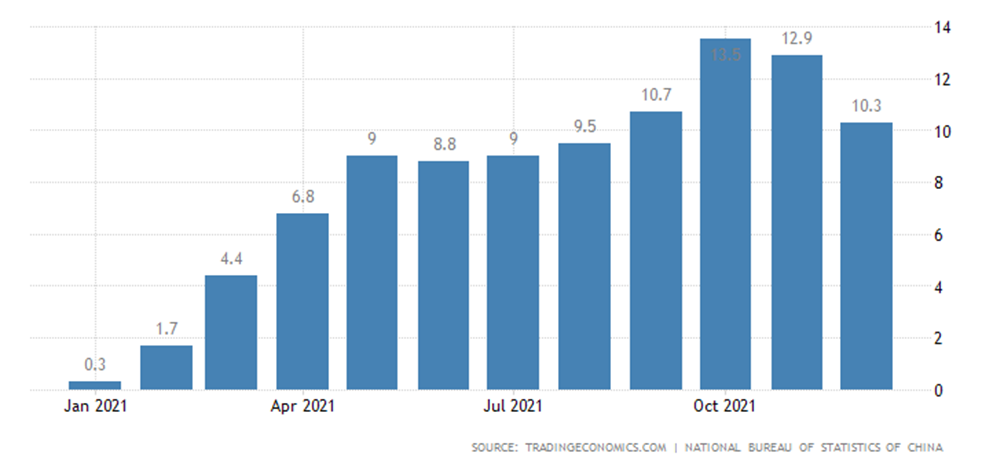

And PPI (Producer Price Index) decreased from +12.9% to +10.3%, influenced by government measures to contain price increases:

But there is also a side effect – debt on loans in yuan reached a twenty-year low and amounted to +11.6% per year:

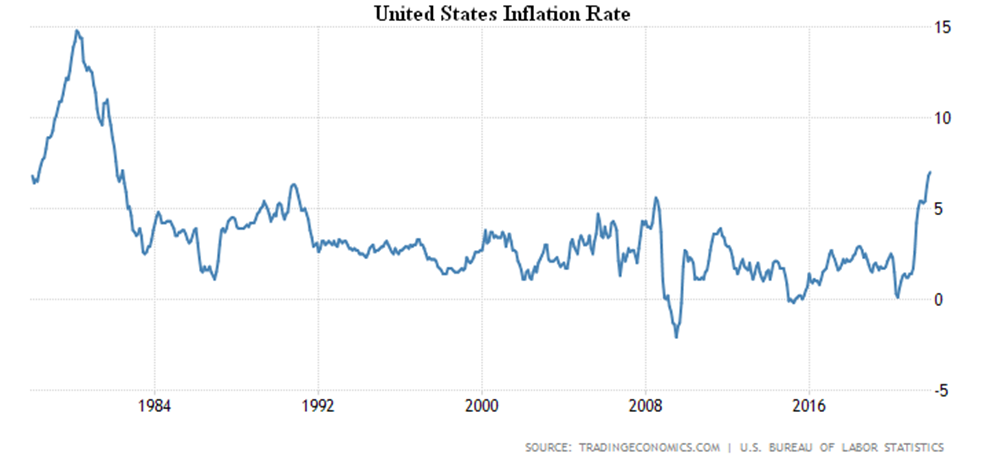

In other words, China’s economics is slumping even with export growth. US CPI +7.0% per year is the highest since 1982:

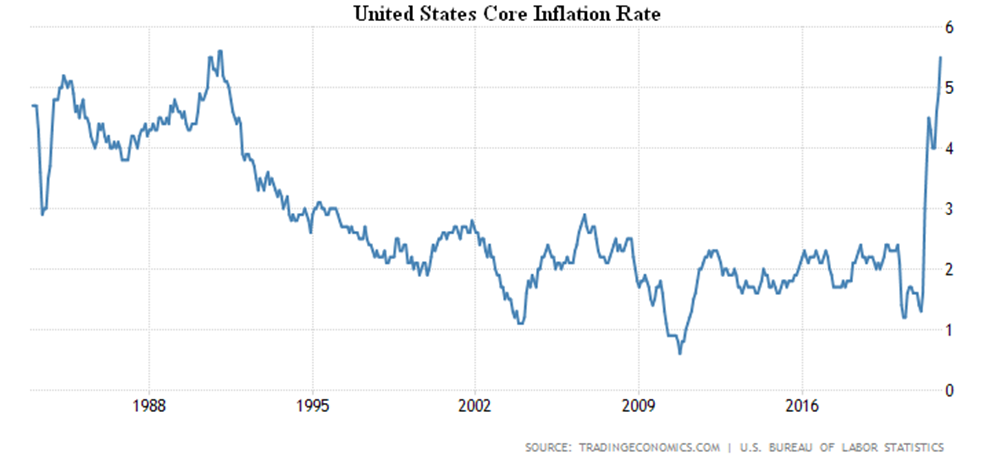

Core inflation rate (less food and energy) +5.5% p.a. is at its peak since 1991:

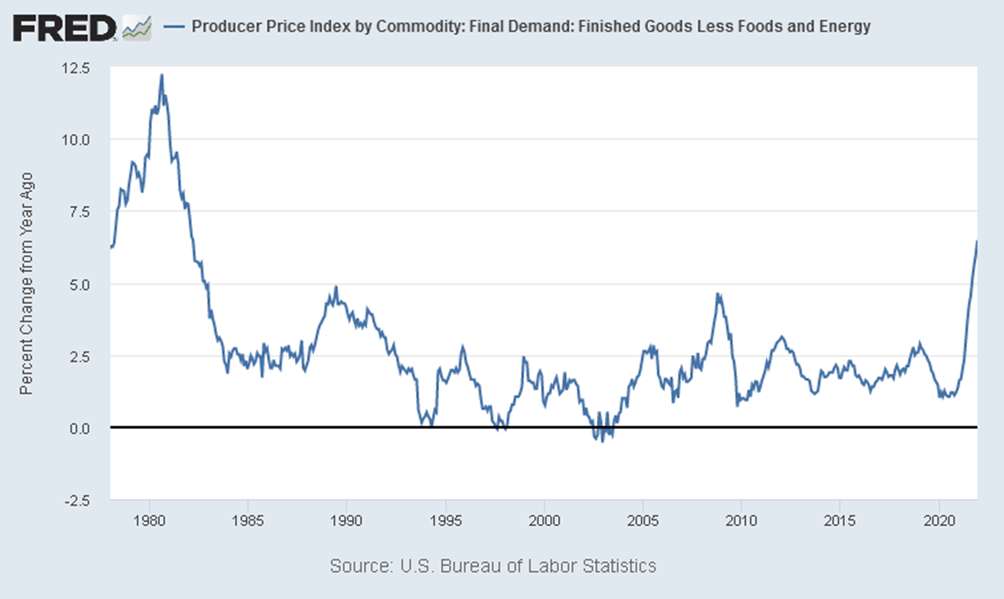

The US PPI has slowed slightly, but final goods without food and energy have a new 40-year record (+6.5% YoY):

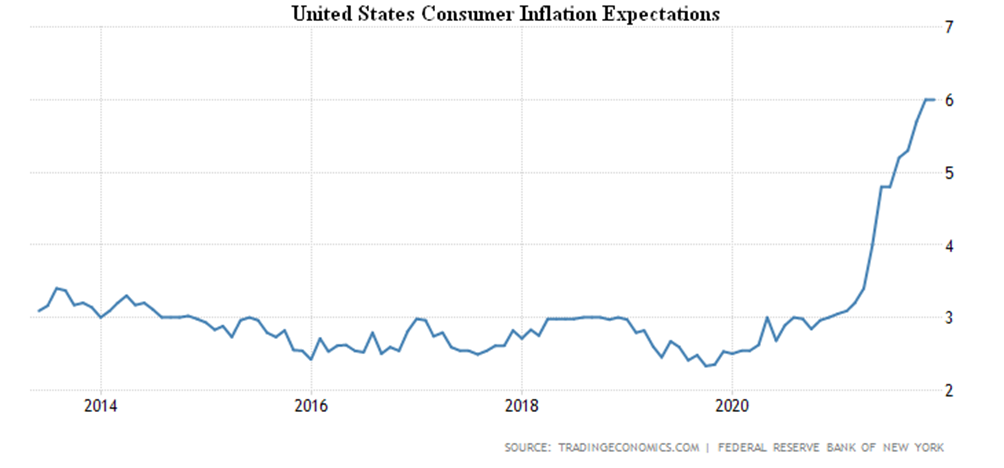

US inflation expectations remain at a record high of +6.0%:

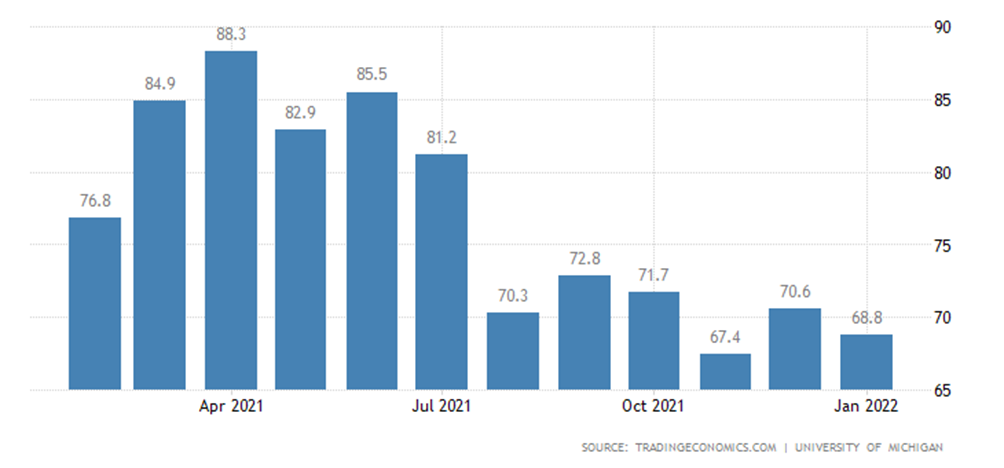

This was also confirmed by the University of Michigan, where this figure peaked in 13 years:

And his consumer sentiment index deteriorated again and returned to the locality of the 10-year-old trough:

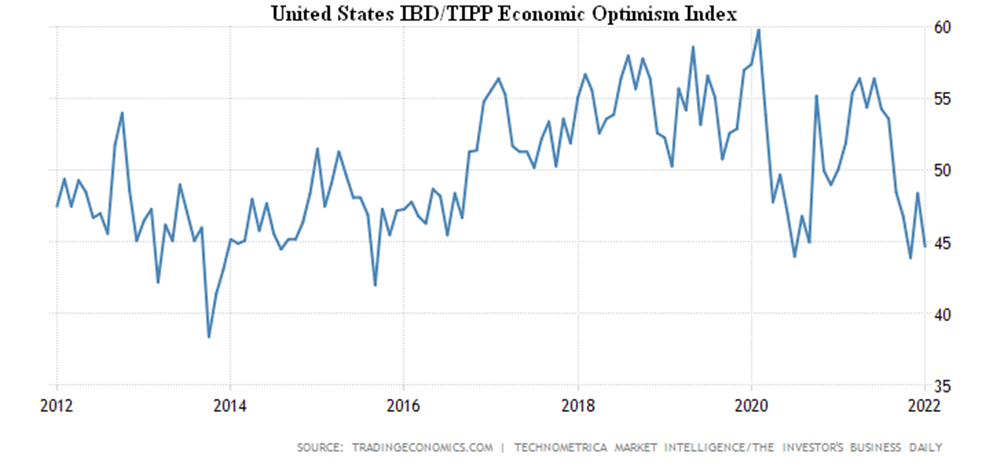

US economic optimism (IBD/TIPP Survey) is almost back to its lowest level since 2015:

Unemployment in South Korea is at its highest level in 9 months:

Retail sales in Italy -0.4% per month, this is the worst performance in 10 months:

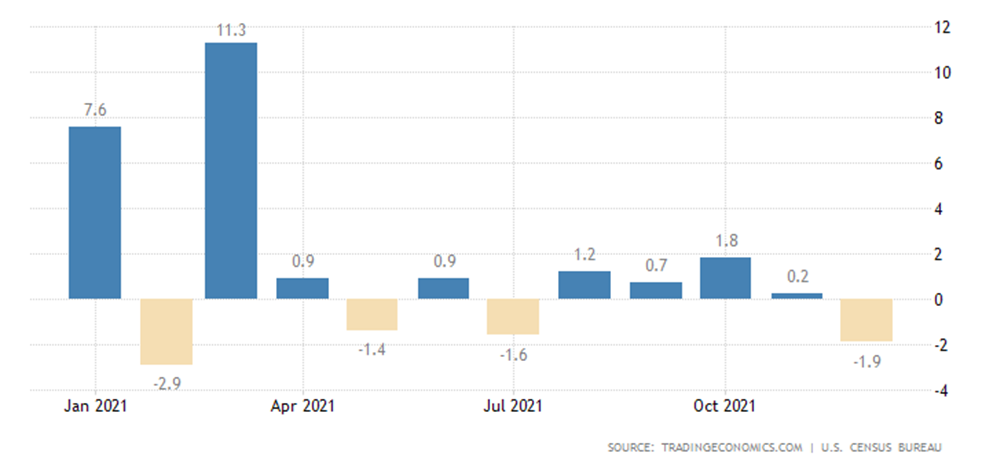

US retail -1.9% MoM, nine-month collapse:

Summary. The inflationary problems are so strong that all attempts to transfer the main problems into the field of geopolitics (discussion of the notorious «Putin ultimatum») have not succeeded. There is no doubt that industrial inflation of 25% in an election year in the US cannot be tolerated, while, say, commodity prices continue to rise:

But the huge debt of households and corporations is also not going away. And the only way to offset the increase in the cost of servicing that debt with the rate going up is through public support measures. That is, the restructuring program.

But this program supports not everyone, but only the real sector of the economy – precisely for this reason we wrote that Biden actually moved away from the original “Biden plan” in favor of the “Trump plan”. This means that support will not reach all sectors of the American economy. Or, in other words, that the US economy expects strong restructurings that will begin this year.

This is extremely important information that most of the business community does not accept. They are waiting for an end to the crisis, an improvement in the economic situation and a return to the pre-crisis situation. And the reality is that the structural crisis is just beginning and will continue for at least five to eight years, and, above all, that the structure of the economy and the scale of demand will be fundamentally different from the situation before the crisis (that is, until 2008).

The Mikhail Khazin Foundation for Economic Research has been developing crisis and post-crisis models for many years, so we are well aware of the scope of change. Moreover, we founded a specialized Strategic Forecasting Agency “Kovcheg”, whose task is to prepare a program to adapt large clients to these changes. But let us look at life wisely, and we can reach out to very few companies. And for that reason, we strongly recommend that all our readers be seriously concerned about the creation of groups, units or at least the search for specialists capable of providing more or less adequate recommendations for the development of crisis structural processes. Understanding that official structures not only ignore these processes, but also have absolutely no understanding of their mechanisms and effects.

We wish our readers a successful workweek!