anyary 27 – February 2, 2024

Big news. A sharp drop in the average working week in the US, it is only 0.1 above the Covid bottom. Previously, such numbers were only at the beginning of 2010:

There is a lot to be said about which indicators can be interpreted as a hint of (possible) growth, and which ones contradict them. But the length of the working week definitely indicates a recession; with economic growth, employee workload always increases. If there may be different opinions about wages (see the next section of the Review), as well as about unemployment (here are complaints about the methodology of the Ministry of Labor), then there can be no disagreement here.

Therefore, we say with confidence that the US recession continues (in our opinion, from the fall of 2021), which is masked both by understatement of inflation and mechanisms for converting the growth of capitalization of financial assets into GDP. What the authorities will do when capitalization falls is an open question and inaccessible to us.

In any case, the continuation of the decline will sooner or later make itself felt from the point of view of the state of financial markets.

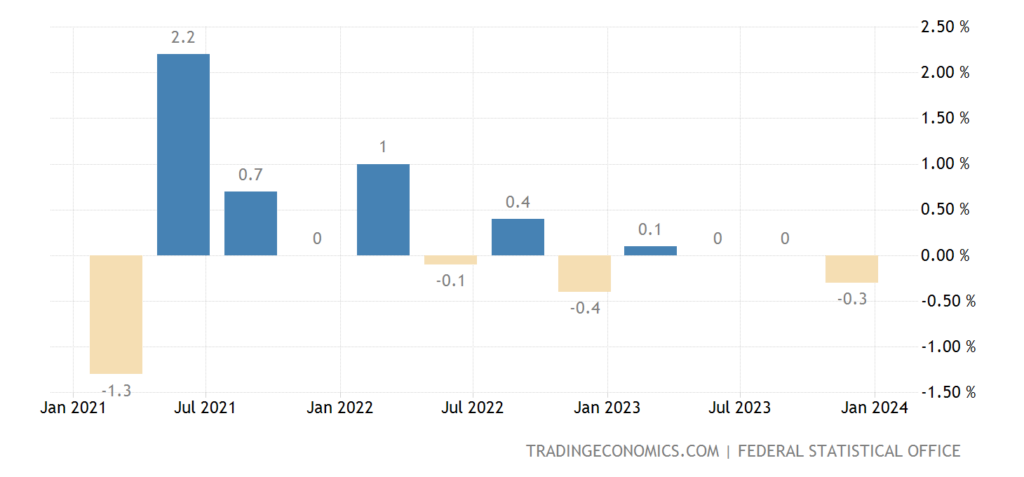

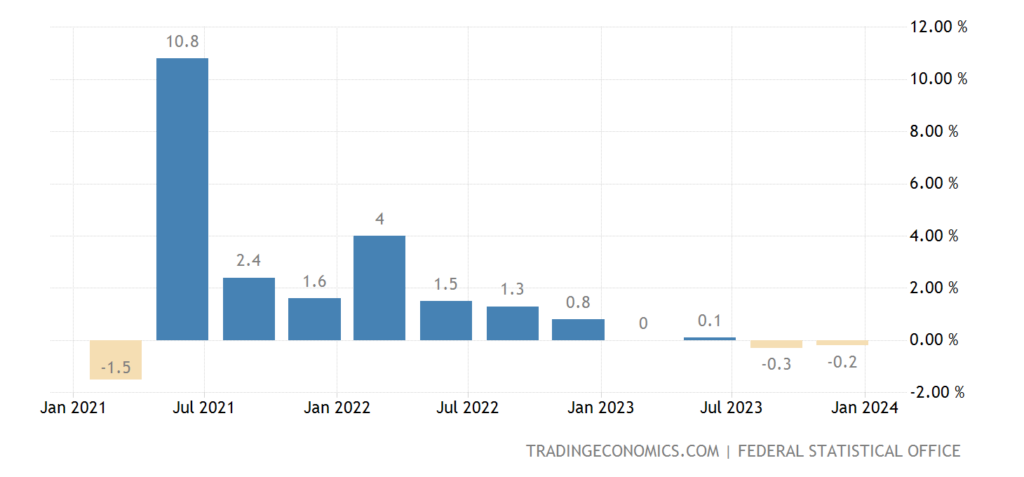

Macroeconomics. German GDP -0.3% quarterly after two zero quarters in a row:

Pic. 2

And -0.2% per year, 2nd minus in a row:

Pic. 3

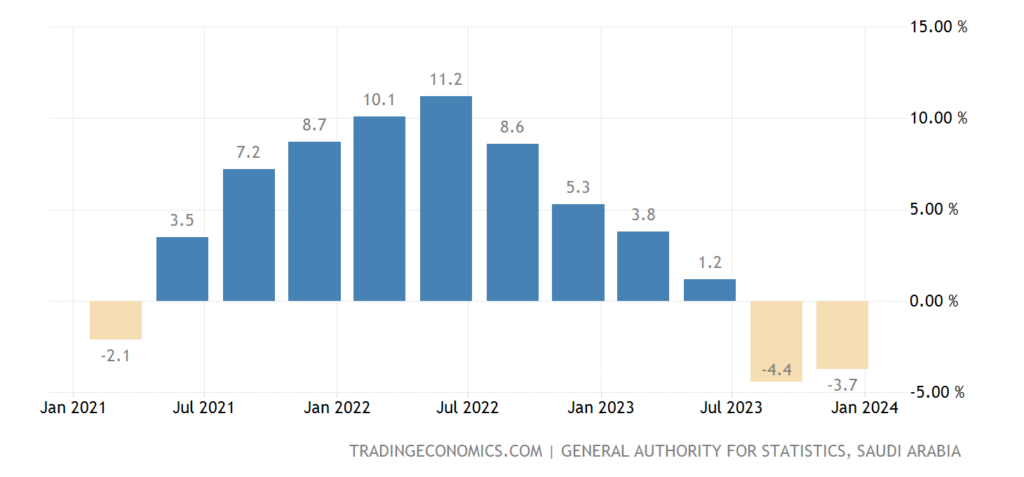

Saudi Arabia’s GDP -3.7% per year, 2nd minus in a row:

Pic. 4

Industrial sales in Italy -3.4% per year, 8th negative in a row:

Pic. 5

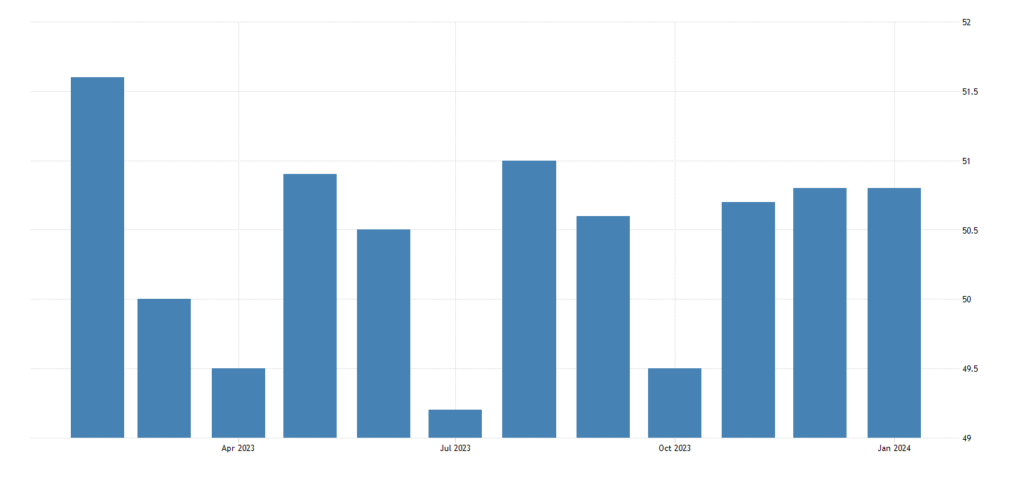

The official PMI (expert index of industry health; its value below 50 means stagnation and decline) of China’s industry is in the recession zone, over the past 10 months it has left it only once:

Pic. 6

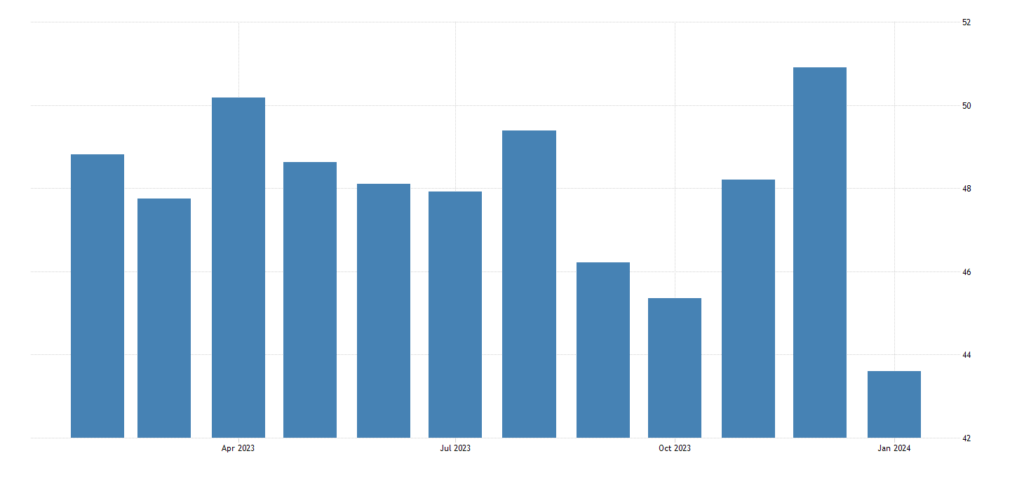

An independent study is less pessimistic (50.8 there):

Pic. 7

South Africa’s PMI fell into depression (43.6):

Pic. 8

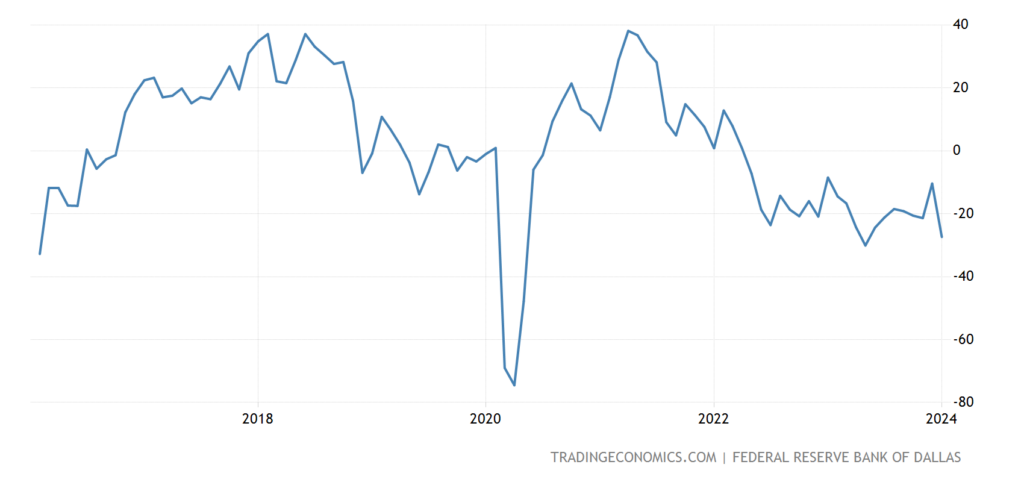

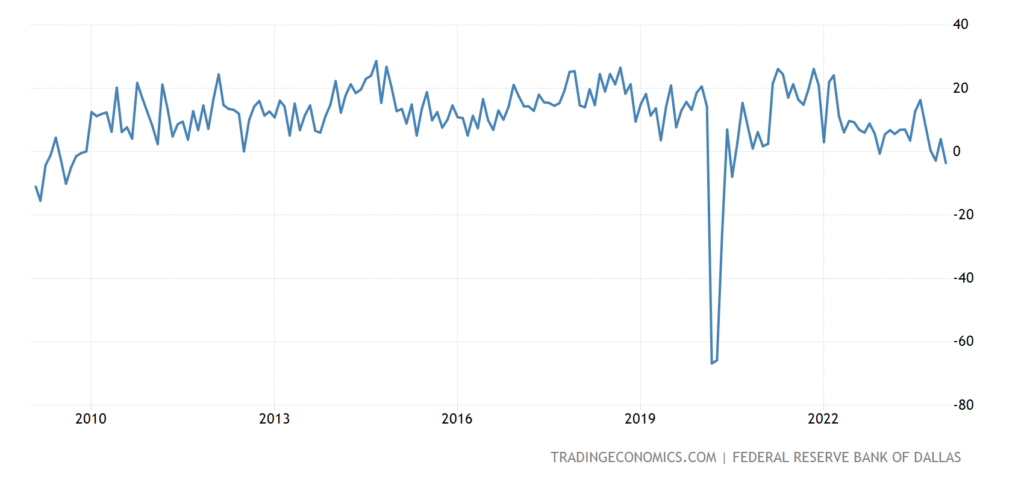

The Dallas Fed area industrial activity index has been in the red for 21 months in a row and near an 8-year bottom (excluding Covid):

Pic. 9

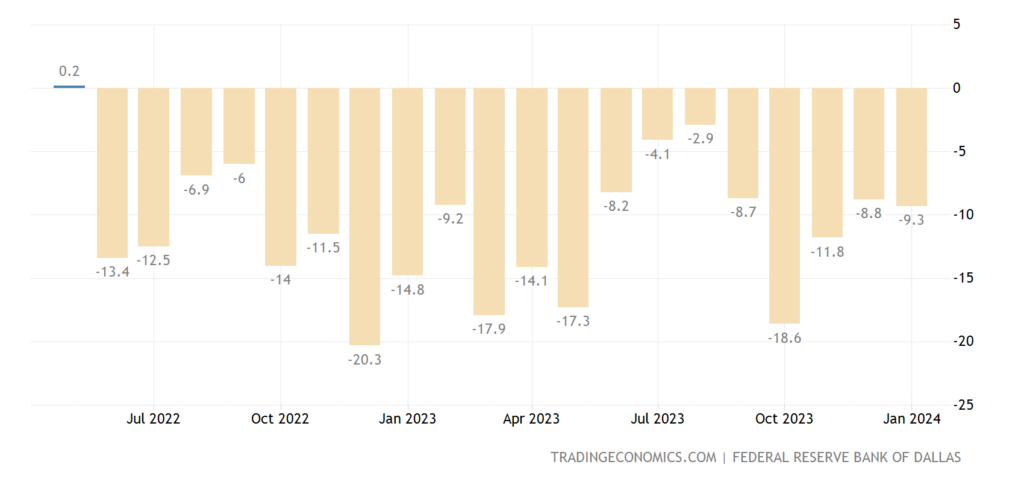

The service industry in the same region (Texas) is in the red for 20 months in a row:

Pic. 10

Moreover, the revenue dynamics of service companies is the worst since 2009 (not counting Covid):

Pic. 11

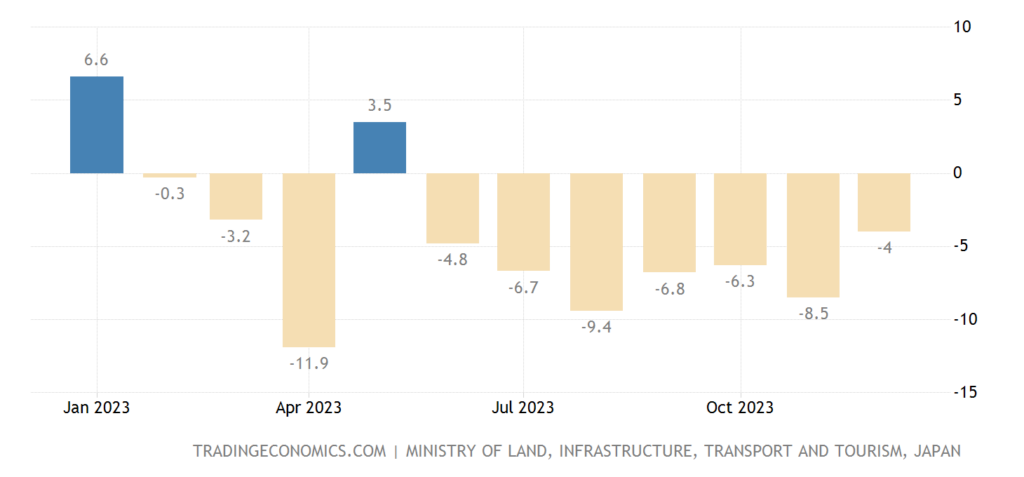

The number of new buildings in Japan -4.0% per year, the 7th minus in a row:

Pic. 12

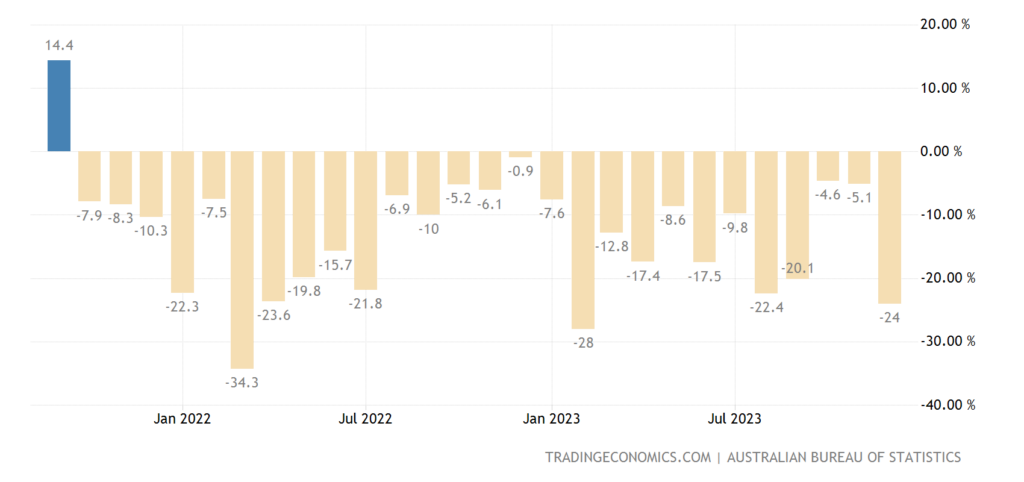

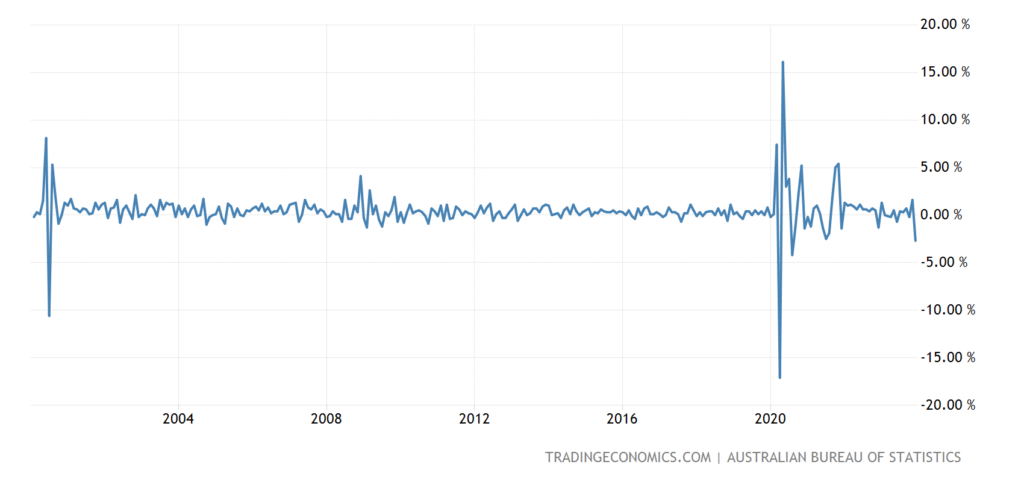

Building permits in Australia -24% per year, 27th minus in a row:

Pic. 13

Their level still remains at the values of 2008/12:

Pic. 14

PPI (industrial inflation index) of Italy -16.0% per year, an anti-record for all 32 years of data collection:

Pic. 15

Retail Australia -2.7% per month. Apart from Covid fluctuations, it was worse only once, in July 2000:

Pic. 16

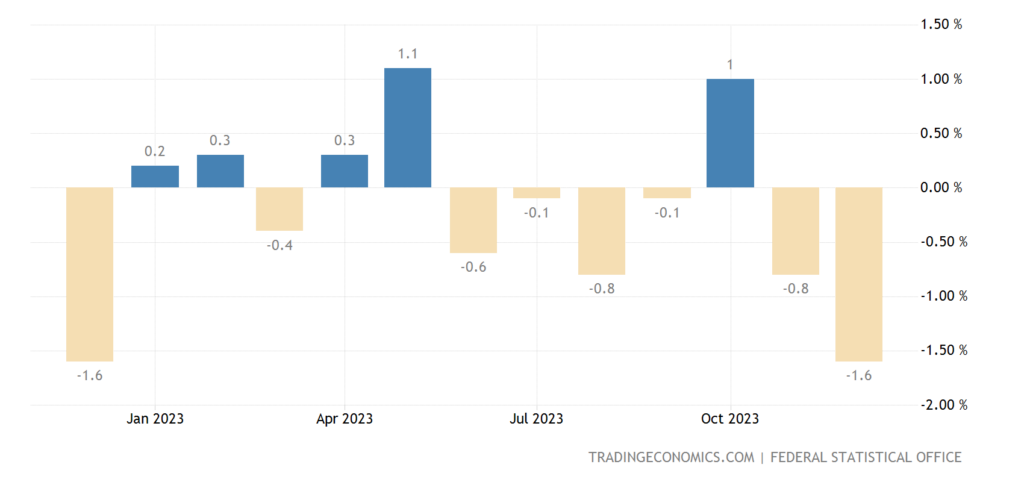

German retail -1.6% per month, 14-month bottom:

Pic. 17

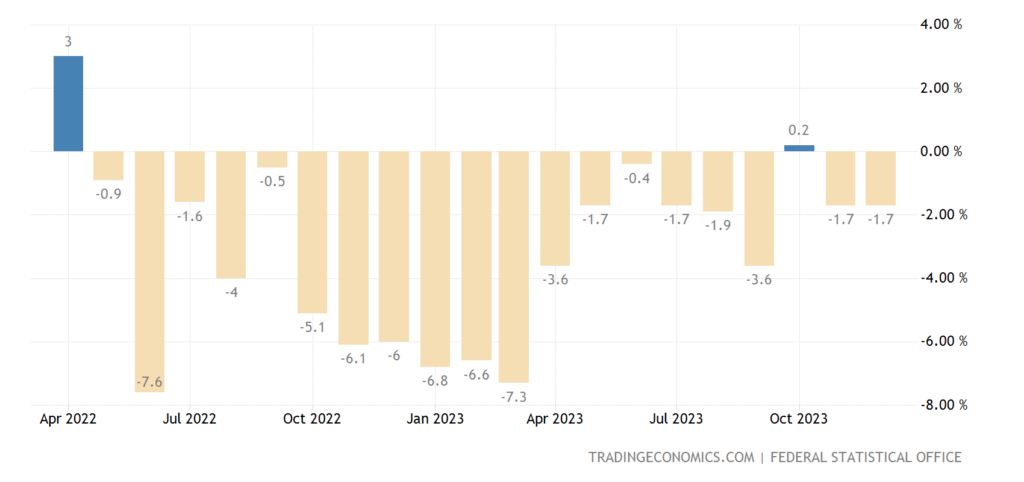

And -1.7% per year, the 19th minus in the last 20 months:

Pic. 18

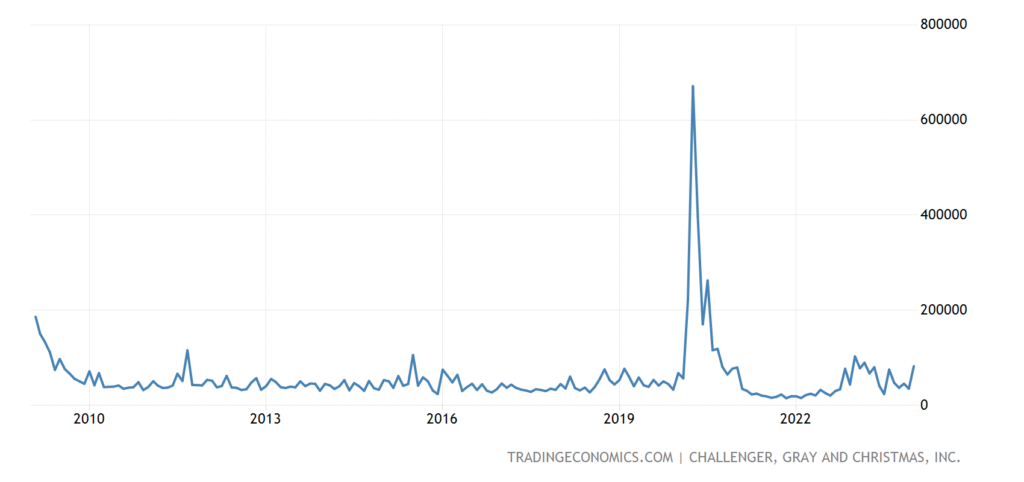

In January, the US saw a surge in layoff announcements – this is the second worst January (after last year) since 2009; Major cuts in the financial and technology sectors:

Pic. 19

However, it is possible that this is the effect of euphoria from the use of “artificial intelligence”.

The number of recipients of unemployment benefits in the United States has again reached its peak in more than 2 years, which was set in November 2023:

Pic. 20

However, as we have noted more than once, the scale of falsification of this indicator is very large and it cannot be considered as an adequate indicator of the state of the economy.

Average hourly wage in the US +0.6% per month, 2-year maximum:

Pic. 21

And +4.5% per year, the top for six months:

Pic. 22

These data can be interpreted in different ways, since it is not very clear in which sectors wages have increased and why. In any case, a decrease in the length of the working week is a much more informative indicator.

The average price of new homes fell in December:

The US Federal Reserve left monetary policy unchanged; in the text of the press release (see the next section) there is no longer a threat of a further increase in rates, but at the same time, there is no talk of reducing them yet:

Pic. 24

The Bank of England also left everything as it is, 2 board members voted for tightening policy, but another 1 voted for easing it. The Central Bank of Brazil lowered the rate by 0.50% to 11.25%.

Main conclusions. The US Federal Reserve’s Open Market Committee did not change the key rate. The Fed’s cover letter states:

▪️ More balanced risks associated with the labor market and inflation in the United States are emerging;

▪️ The Fed does not believe that it is advisable to start cutting rates until there is confidence in the trajectory of inflation towards 2%;

▪️ Fed balance sheet contraction continues (QT);

▪ ️Everything depends on incoming macro data.

In previous sections of the Review, we noted serious factors indicating a negative development of the situation in the American economy. This is most likely what Fed officials have in mind. In any case, it is obvious that the trends are multidirectional: inflation, judging by December data, is not going to fall, and the decline in the real sector of the economy requires a rate cut. Let’s see what the US monetary authorities will do.

At the press conference, Powell said:

▪️ I don’t know how many months it takes for the Fed to gain confidence in 2% inflation in the US;

▪️ We will not keep secret our belief in the inevitable 2% inflation in the US;

▪️ I personally think we need to see CONFIRMATION that we are heading towards 2% inflation;

▪ ️The Fed is in “risk management mode”;

▪️ Today no one suggested that the Fed should start lowering the rate;

▪️ But we will lower rates if we see a weakening in US employment;

▪️ Tailwind – disinflation in the commodity market;

▪️ Inflation is still high in the US, but we have made serious progress;

▪️ Namely, there is “Good progress” without a significant increase in unemployment in the country;

▪️ Fed rate in restrictive territory;

▪️ More balanced risks associated with inflation and the labor market have emerged;

▪ ️Long-term inflation expectations look reasonable;

▪ ️Our long-term inflation target = 2%;

▪ ️The rate is most likely at its peak values;

▪️ Progress on inflation is not guaranteed;

▪ ️We will lower the rate THIS YEAR if the US economy develops as we expect;

▪️ The Fed is ready to keep rates at current levels LONGER if the country’s economy requires it;

▪ ️We need more inflation data than in the last 6 months;

▪️We do not see stronger economic growth as a problem;

▪ ️Almost ALL Fed chairmen believe it is worth cutting rates this year;

▪️ We are not considering actively reducing rates;

▪️ I would not say that we have already achieved a soft landing of the economy;

▪️We are not declaring victory!

▪ ️Most of the economic growth is the strong recovery from Covid-19;

▪️ I will start to worry if inflation stubbornly begins to stabilize above 2%;

▪ ️If inflation rises again significantly from current values, it will be an unpleasant surprise for the Fed;

▪ ️MARCH – we are unlikely to lower rates this month. This is not our basic scenario;

▪ ️There are risks that may force us to reduce rates more slowly or faster;

▪ ️I plan to conduct thorough negotiations on the Fed’s balance sheet in March (QT).

Note that although the rate has not been changed, the policy of reducing the Fed’s balance sheet (withdrawing money from the economy) continues. At the same time, Powell understands that emissions may have to be restored (pre-election year). The talk about a “soft landing” looks like a response from Nabiullina, who was clearly too hasty with her optimism. However, she was guided by completely different reasons.

Powell explicitly warned that inflation could start to rise despite the Fed’s policies. Well, what he will do in this situation – it is directly said that decisions will be made according to the situation. If we could ask Powell questions, the main question would be: which sectors are growing GDP and how rate policy takes into account the length of the work week.

In general, the structural crisis in the global economy continues. And there is no reason to believe that the situation will change in the coming years. However, our readers can feel quite confident even in this situation and we wish them a pleasant weekend and a relaxing work week!