January 13-19, 2024

Big news. Actually, there was no interesting macroeconomic news this week. But there were economic ones, and we can mention three at once, closely related to each other. The first news is another attempt to confiscate the seized assets of Russia. The second is France’s refusal to accept a major contract for the supply of aircraft to Iran. The third is the economic forum in Davos. The main news here is that nothing was said about the economy.

All three news points to one thing: no one is seriously considering the option of preserving the Bretton Woods model, with all its institutions, the IMF, the World Bank and the WTO. Even in theory, no one proposes or discusses measures to restore the world dollar system and unified global institutions.

A few weeks ago the situation was different. Yes, everyone had already recognized serious problems, but the question, nevertheless, was how to somehow overcome these problems. Today, apparently, everyone has already understood that this is impossible in principle and the question has arisen differently: how the ruling elites can maintain their status. Because those who lose it will certainly lose all their accumulated wealth.

In addition, the question is about what the new regional elites will look like. It is clear that it is no longer possible to abandon the concept of currency zones, but it is also impossible to recognize them publicly until the new elites of the new currency zones recognize the assets of the old financial elites. This is due to the fact that the assets of the old elites are mainly of a financial nature and are closely related to various accumulated debts. And if dollar assets depreciate, then debts will be much more difficult to write off. And, most importantly, those who declare defaults en masse will not be able to claim high positions in the world.

And if we also take into account that financiers do not have direct control over the security forces, the situation for them becomes even more complicated. We have written a lot about how the transition through the crisis will be a separate, very difficult task for any more or less large company. But the events of the last week suggest that even the elites of the world dollar system recognized this, albeit indirectly. Which means that there is very little time left before serious events begin.

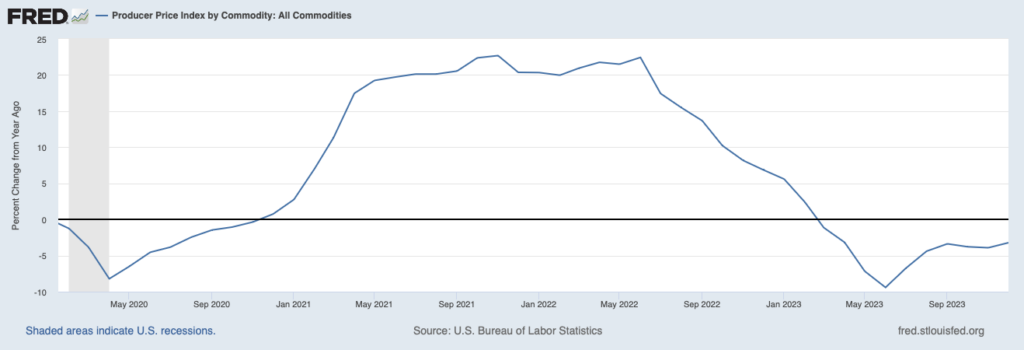

You can also add data on US industrial inflation for the entire volume of goods:

The December figures (-3.2%) turned out to be better than in November (-3.9%), but in themselves they do not say anything; the changes are too insignificant. We can only state that deindustrialization continued in December.

Macroeconomics. As we promised, we are returning to Chinese data again. They are mixed and not at all as bad as many news channels broadcast.

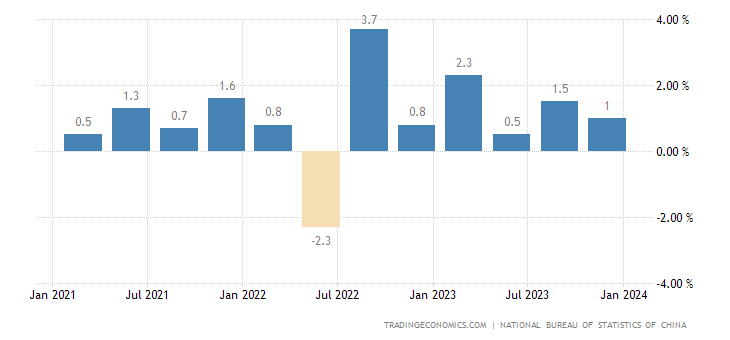

GDP slowed to +1.0% QoQ, as expected:

Pic. 2

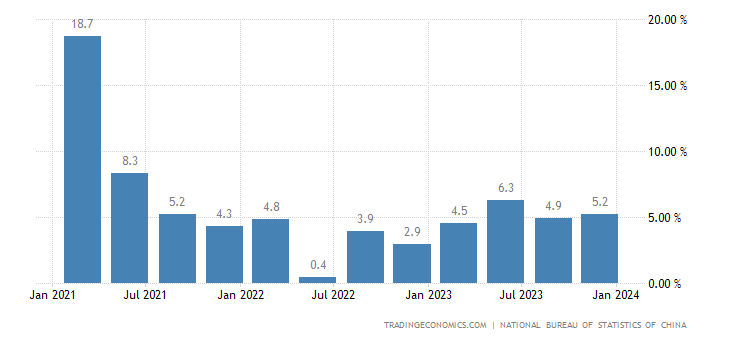

Annual growth accelerated slightly (+5.2%):

Pic. 3

Investments in fixed assets moved away from the historical minimum by 0.1% (now +3.0% per year):

Pic. 4

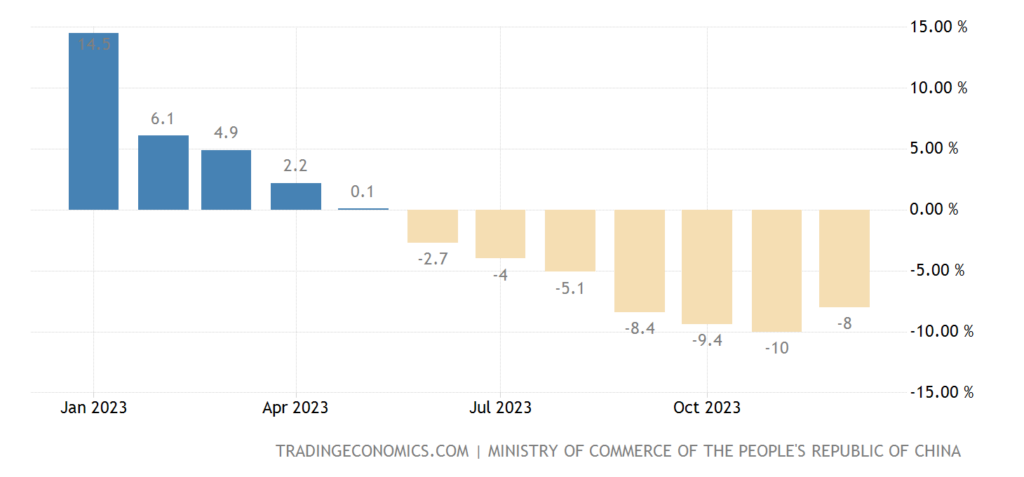

Foreign direct investment slowed its decline from -10.0% to -8.0% per year:

Pic. 5

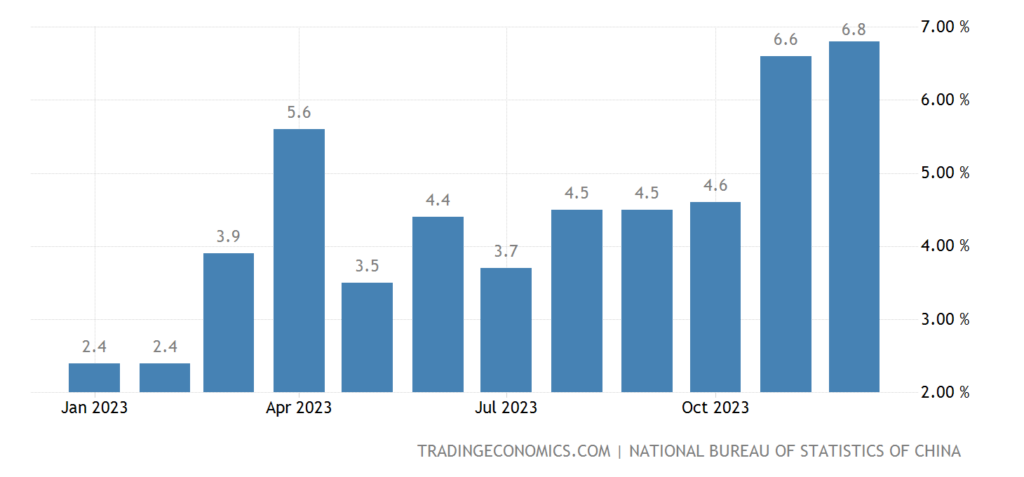

Industrial production is growing at the fastest rate in almost 2 years (+6.8% per year):

Pic. 6

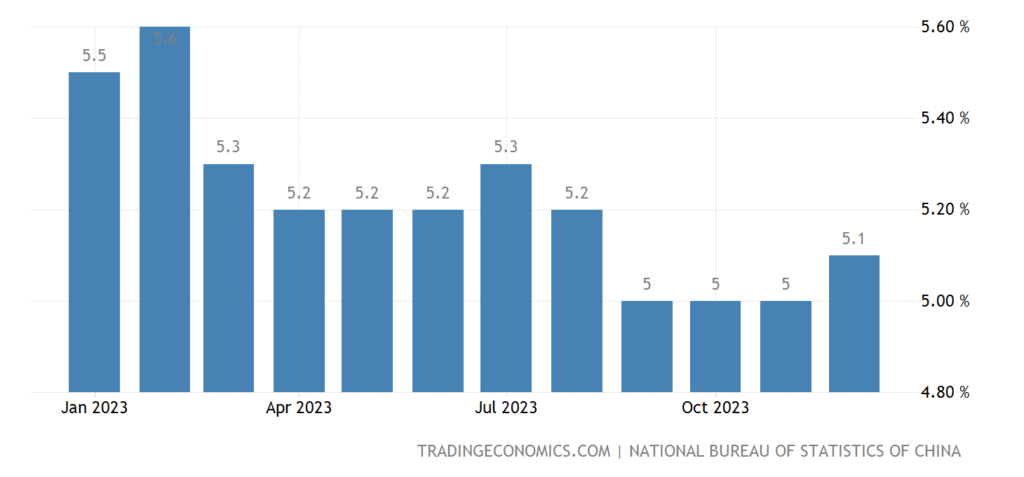

Unemployment has increased slightly:

Pic. 7

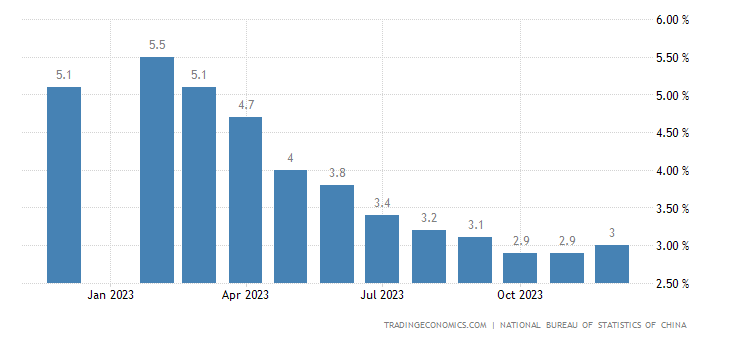

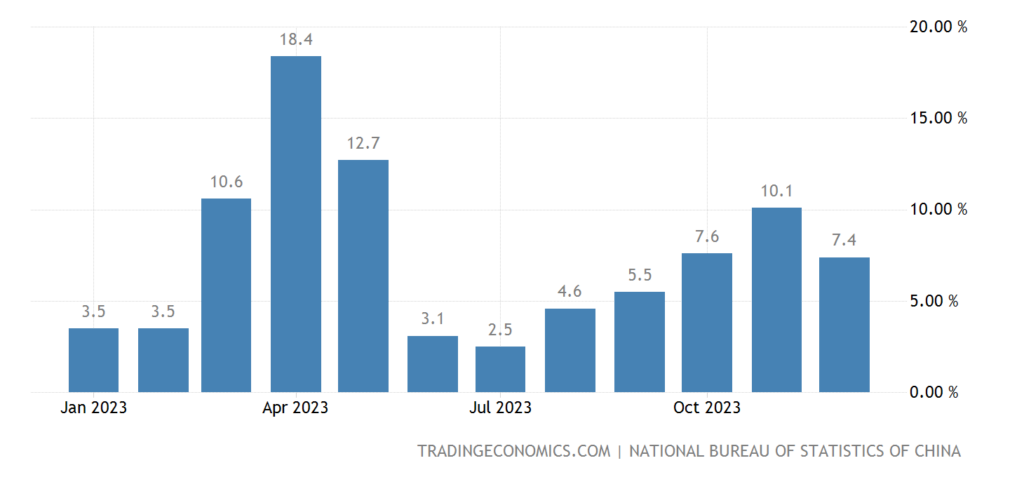

Retail slowed down (+7.4% per year after the previous +10.1%):

Pic. 8

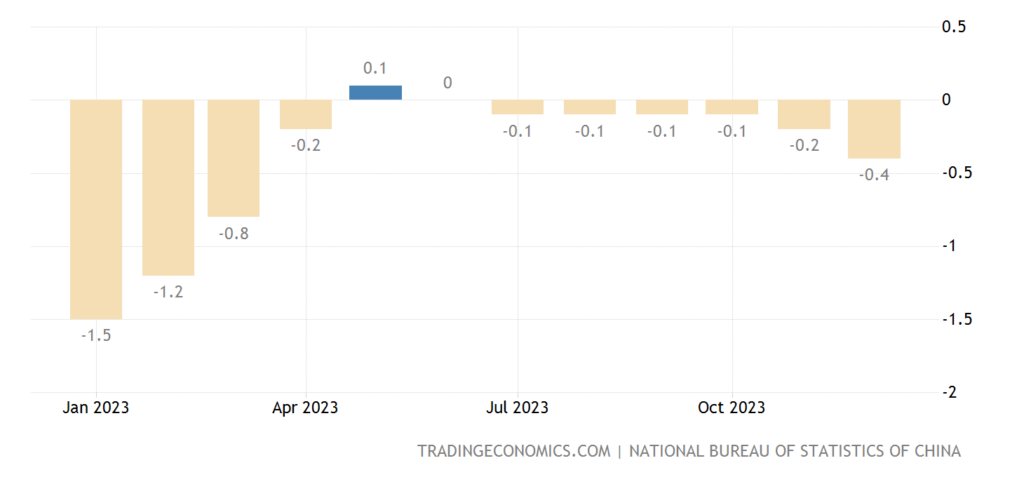

The fall in housing prices accelerated (-0.4% per year):

Pic. 9

In general, it can be noted that the data does not show a collapse. But it is important to take into account that they are official (that is, precisely adjusted for the better) and, most importantly, that imports from China to the United States are not yet limited. Neither by the income of American households, nor by political restrictions. Elections in Taiwan have been remarkably quiet, but that could change as the crisis in the US unfolds. According to Pavel Ryabov, the free money pumped into the financial system during Covid will run out in April, and it is by this time that the US monetary authorities will have to make serious decisions. Which will inevitably have a negative impact on the Chinese economy.

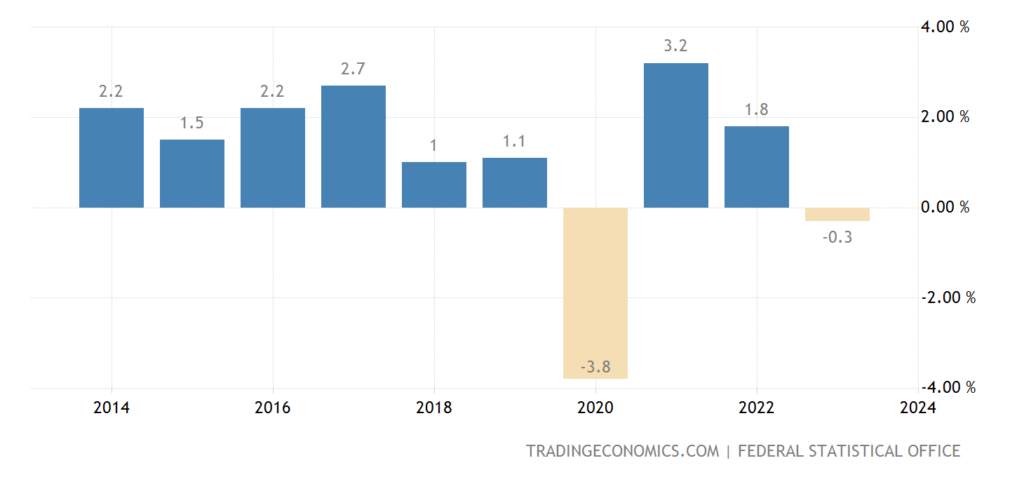

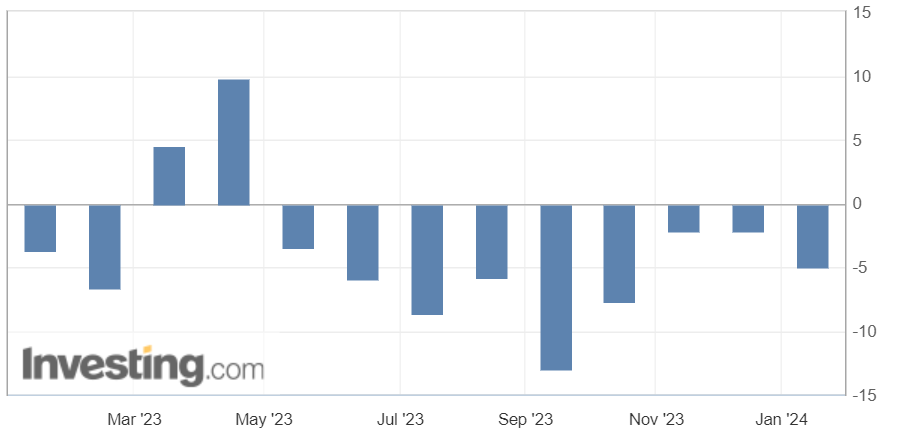

German GDP -0.3% for the entire 2023 year as a whole:

Pic. 10

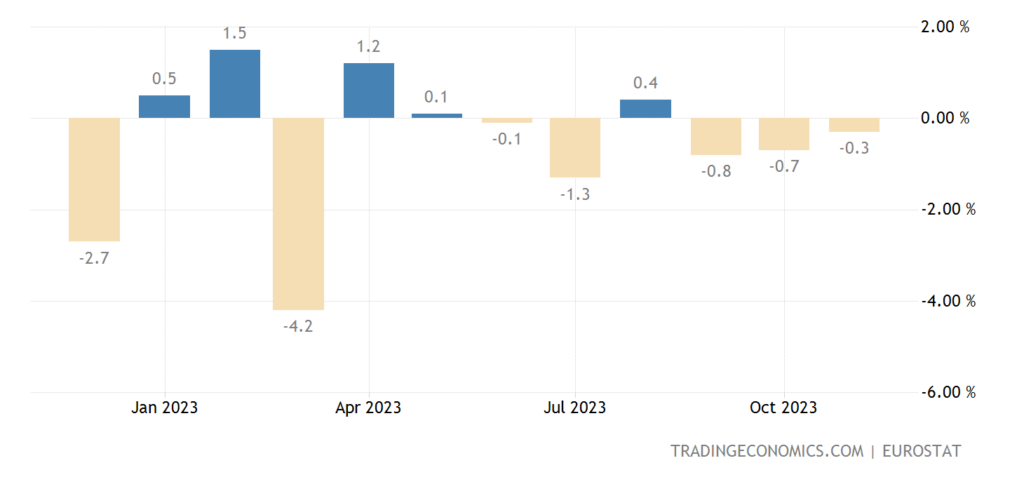

Industrial production in the eurozone -0.3% per month, the 3rd negative in a row and the 5th in the last 6 months:

Pic. 11

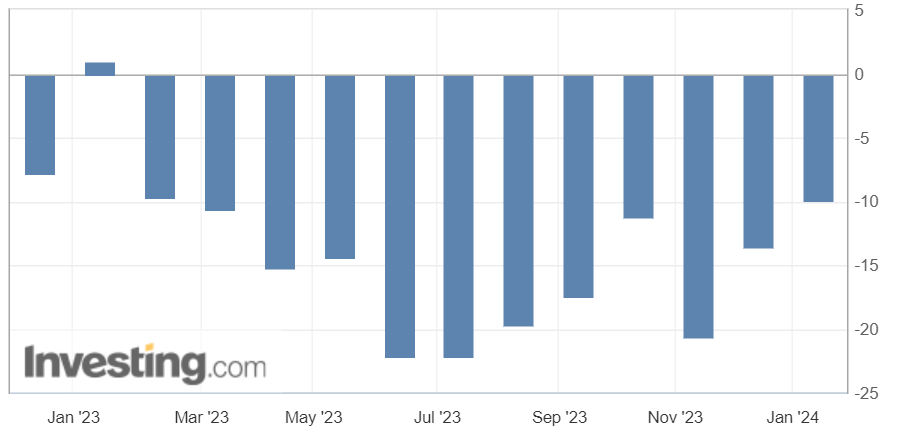

And -6.8% per year, the 9th minus in a row and the worst dynamics since 2009 (not counting the Covid failure):

Pic. 12

Orders for machine tools and similar equipment in Japan -9.9% per year, 12th monthly minus in a row:

Pic.13

In general, in mechanical engineering, orders are -5.0% per year, the 9th minus in a row:

Pic.14

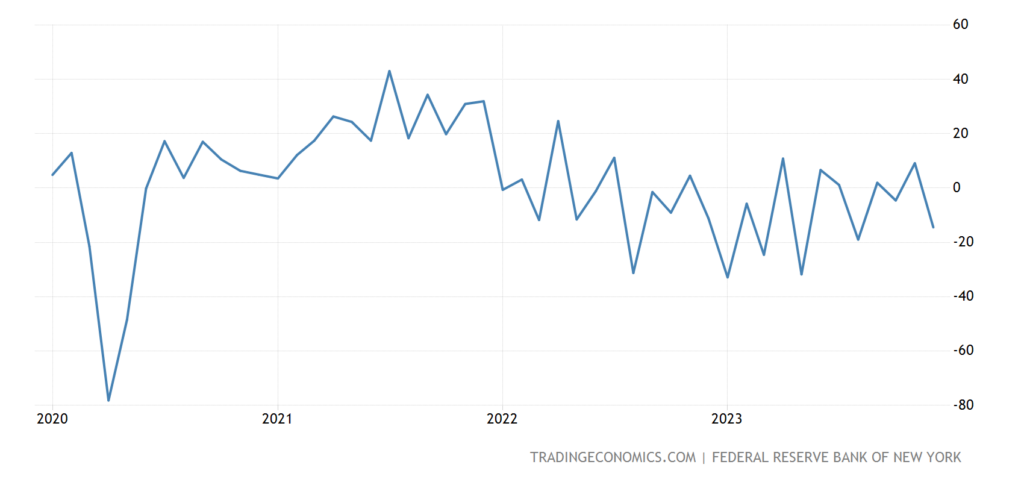

The New York Fed index is at its lowest in 23 years of data collection, not counting the Covid dip in 2020:

Pic. 15

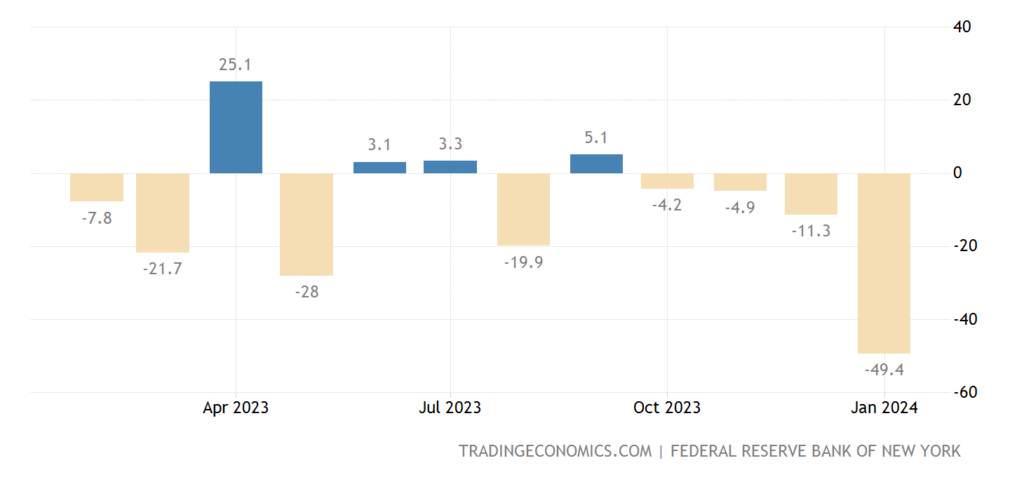

The same minimums apply to the new orders component:

Pic. 16

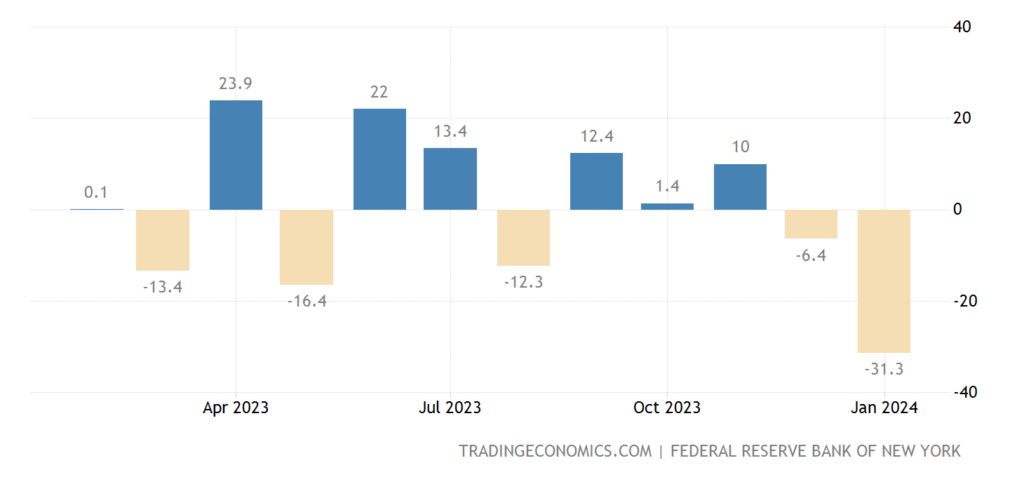

And shipments:

Pic. 17

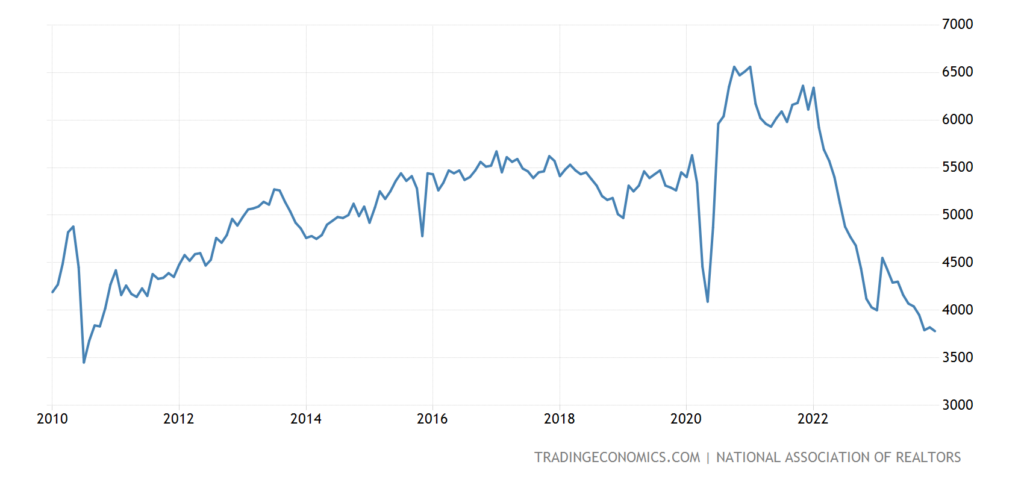

Existing home sales in the US have been at their lowest since 2010:

Pic. 18

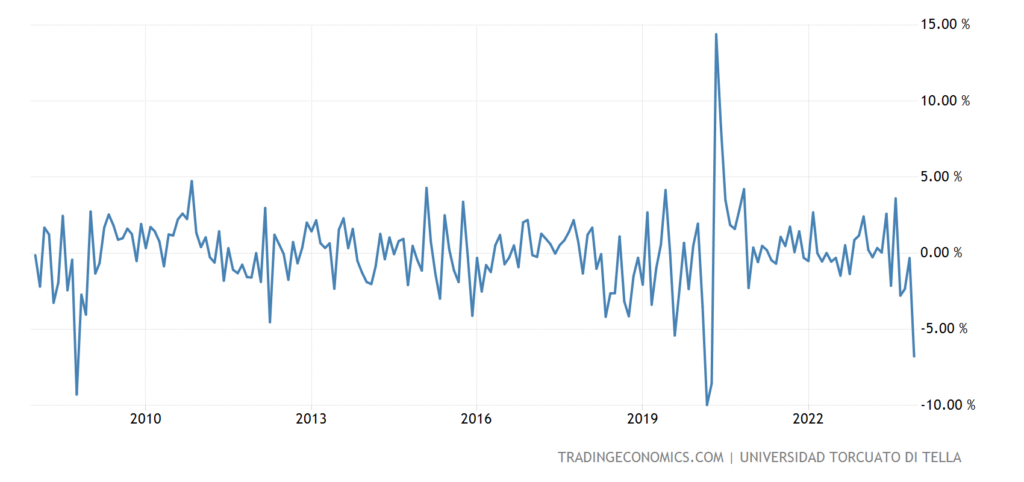

Argentina’s leading indicators are -6.8% per month, not counting Covid, this was only in 2008:

Pic. 19

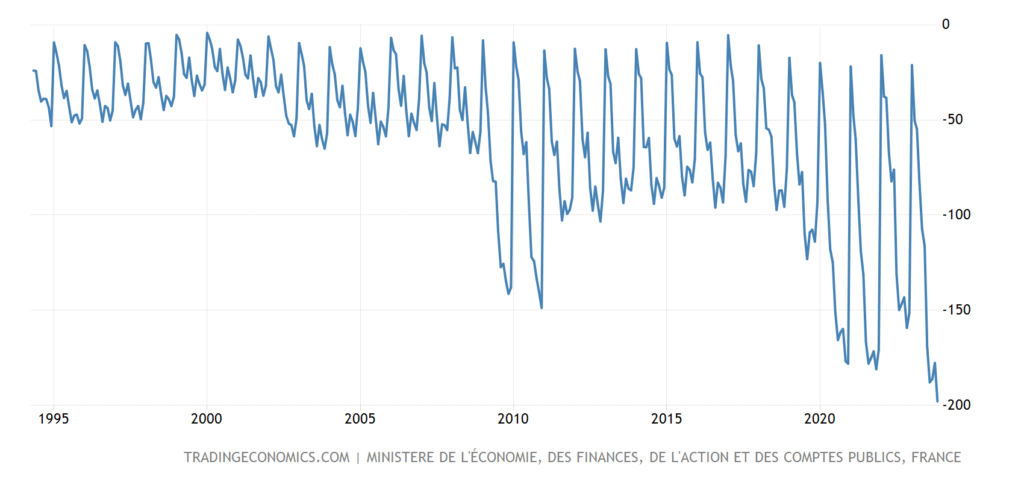

France has a record budget deficit:

Pic. 20

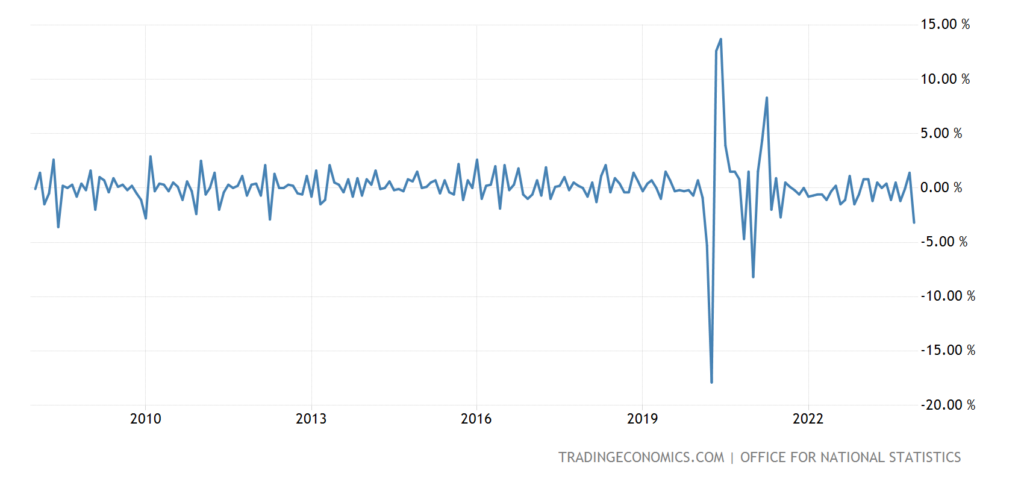

UK retail sales volume -3.2% per month, the weakest dynamics in 3 years, and without taking into account Covid – since 2008:

Pic. 21

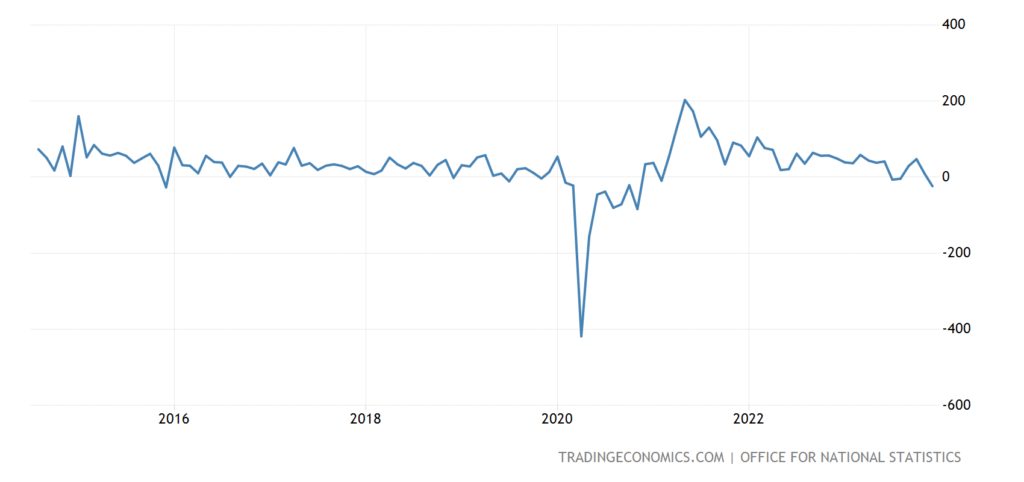

The number of registered unemployed in Britain has been growing for 4 months in a row and 8 of the last 10 months:

Pic. 22

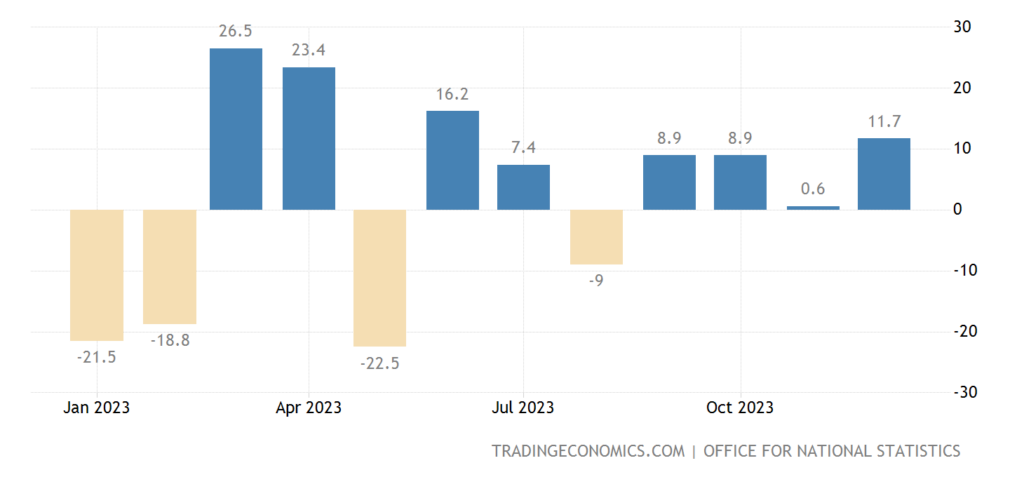

The total number of paid employees is 24 thousand per month, not counting Covid, an anti-record for 10 years of observation:

Pic. 23

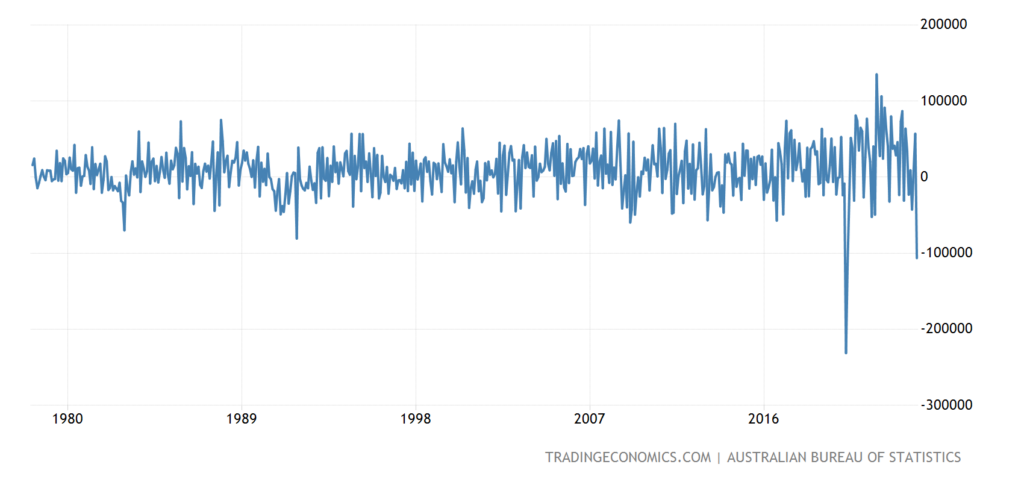

Permanent (full-time) employment in Australia is -106.6 thousand per month, not counting the Covid crisis, this is the worst monthly dynamics of the indicator in all 46 years of statistics:

Pic. 24

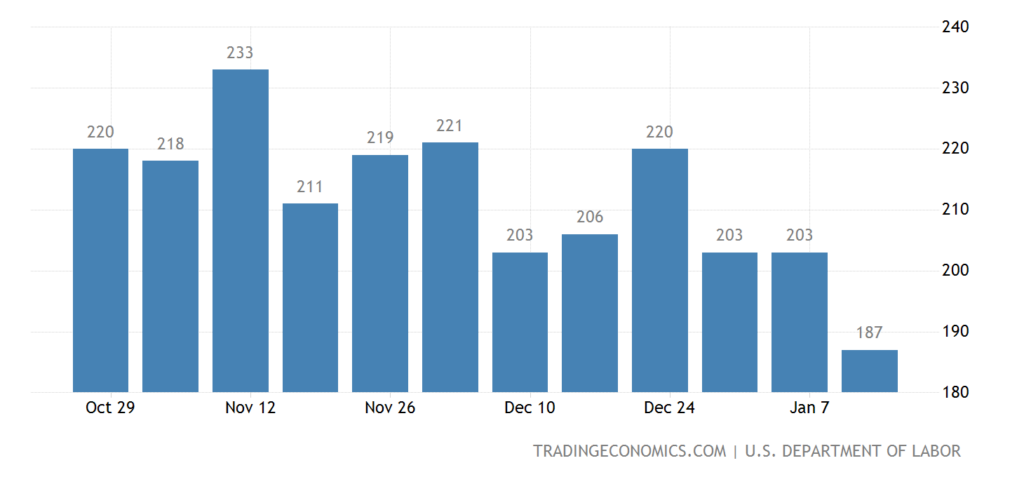

In the US, the number of initial unemployment claims has improved slightly:

Pic. 25

But at the same time, it is necessary to take into account that an increasing share of the employed population is occupied by people who are forced to work with restrictions, including part-time work. As we have noted many times, labor statistics in the United States are particularly skewed.

The Indonesian Central Bank has not changed its monetary policy.

Main conclusions. US inflation data in December 2023 (see previous review) appears to have finally convinced the US monetary authorities and the main managers of the Bretton Woods system that there will be no return to the old principles (see the first section of this Review ). This means that the largest institutions of the system, both purely financial and managerial (IMF, World Bank, WTO, Federal Reserve System) have already begun work to protect the interests of their beneficiaries.

At the expense of all other participants in the economic process, both entrepreneurs, countries, and other institutions. The problem here is that all these institutions and their managers are trained to work within the framework of the B.W. systems and therefore are not protected from its systemic abuses. Not to mention the fact that their activities are absolutely transparent, both through the system of dollar payments, and through the system of global ratings and consulting.

Therefore, the salvation of all other companies and institutions that do not belong to the B.W. elite. systems is only possible through a change in system strategy. Such a new strategy can, to a large extent, be implemented by the current management. But to develop such a strategy, we need specialists who see and understand all the crisis processes in the modern economy, and there are very few of them.

And here we can only note that for our readers, finding such experts does not pose any problem, and therefore they can calmly relax on the weekend and go to work with optimism after it’s over!