November 11-17, 2023

Big news. Actually, there are two of them. The first appeared at the very end of the previous week, like the main news of last week. This is a message from the rating agency Moody’s about the revision of the US rating from stable to downgraded. This caused a mixed reaction in the American political establishment; even US President Biden expressed dissatisfaction.

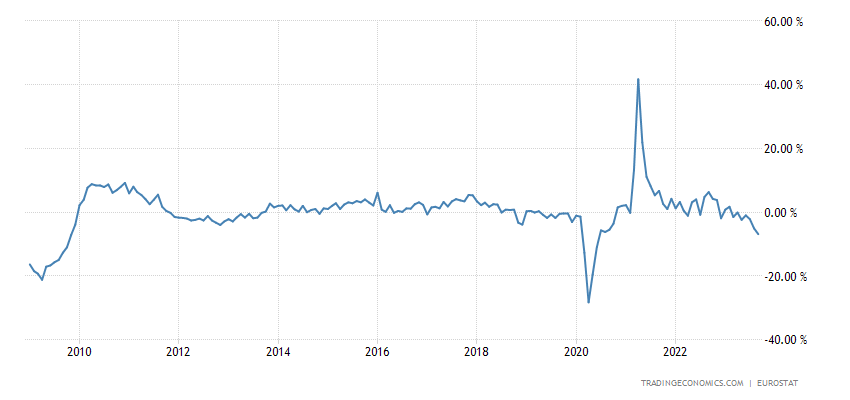

The second news is no less important, but is more specific. Inflation data for October has been released. The data on the PPI (industrial inflation) and CPI (consumer inflation) indices are practically the same, the decrease is purely symbolic. But the data on the entire volume of industrial goods turned out to be more interesting:

Or, in numbers, deflation at the end of October (that is, the change in prices for the year, from November 2022 to October 2023) amounted to 3.6%, despite the fact that the month before it was 3.4%. It would seem “that is nothing at all”, but, as can be seen in the graph, from the maximum in June 2022, industrial inflation has been falling all the time and this could be either a positive or a negative symptom, depending on the economic model.

But then deflation began and this is almost certainly a negative symptom. The minimum was -9.4% in June, and then deflation began to decrease, it seemed that a little more and the situation would calm down. But instead, the price decline intensified.

In fact, this is the same symptom as the reduction in workweek length that we discussed in the previous review. In the United States, a rather serious decline is clearly continuing and it is clearly manifested not even in one, but in a whole series of symptoms. And it is precisely from this that we must proceed when assessing the economic situation, and not from the optimistic desires of current politicians who are already clearly thinking about the upcoming elections.

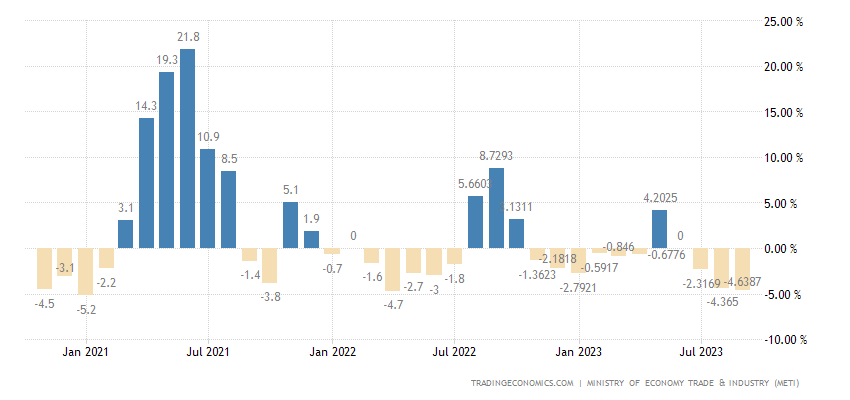

Macroeconomics. Chinese data for October is mixed:

investment in fixed assets slowed down to an anti-record (excluding covid) +2.9% per year:

Рис. 2

Including foreign direct investment -9.4% per year – not counting 2020, it was worse only in 2009:

Рис. 3

Industrial production changed little (+4.6% per year after the previous +4.5%):

Рис. 4

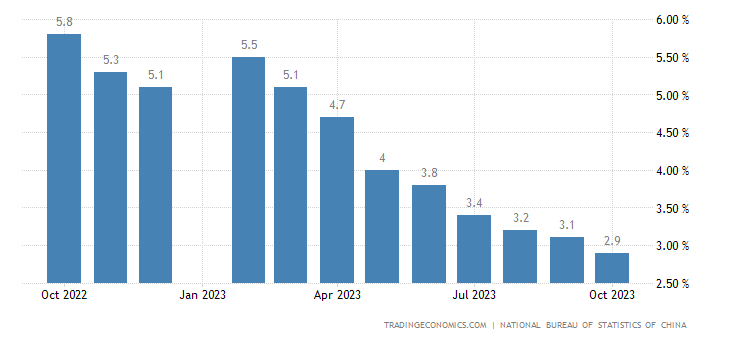

Unemployment is also unchanged (5.0%):

Рис. 5

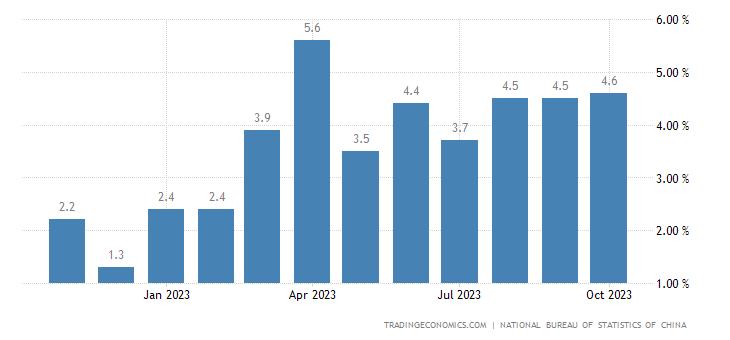

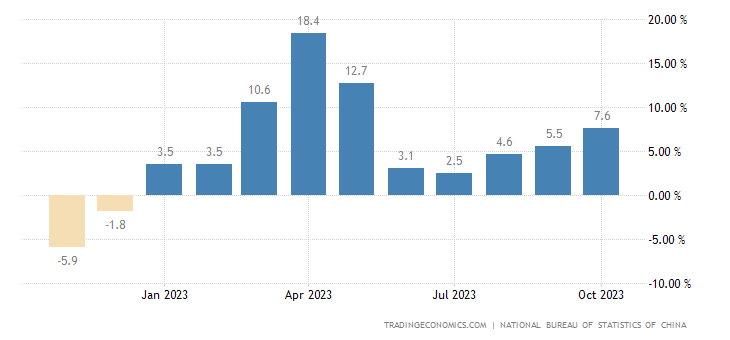

Retail accelerated to 5-month peak +7.6% annually:

Рис. 6

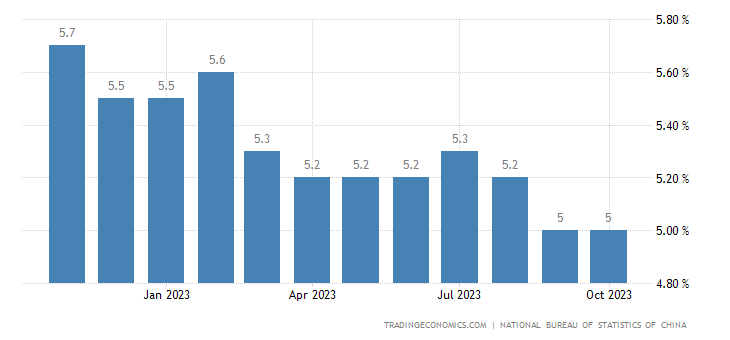

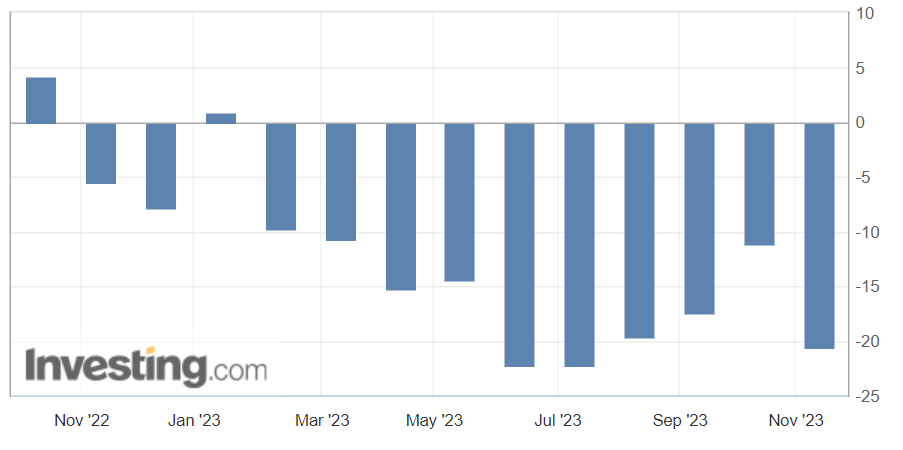

However, the positive data loses much of its credibility when you consider that the volume of loans in China +10.3% per year is the minimum for almost 22 years:

Рис. 7

And in response, China’s central bank injected 600 billion yuan into the banking system through medium-term loans and almost 500 billion through one-week reverse repos:

Рис. 8

That is, it is possible that the growth in retail sales is simply the result of the issue.

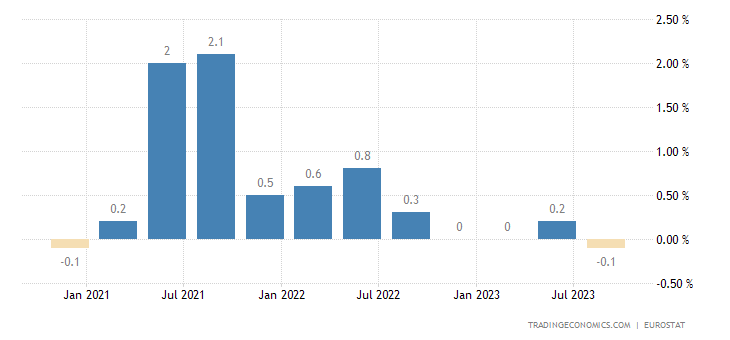

Eurozone GDP in April-June -0.1% per quarter:

Рис. 9

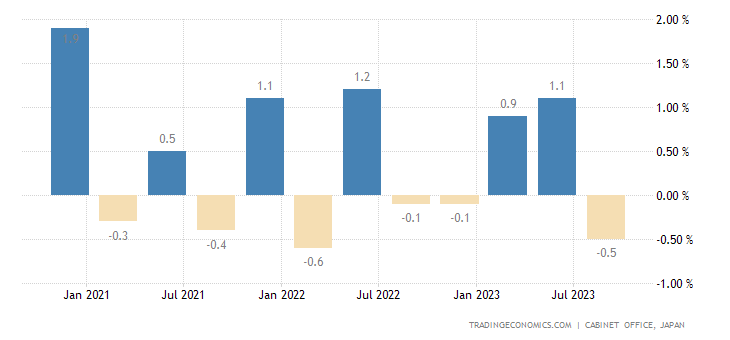

In Japan -0.5% per quarter:

Рис. 10

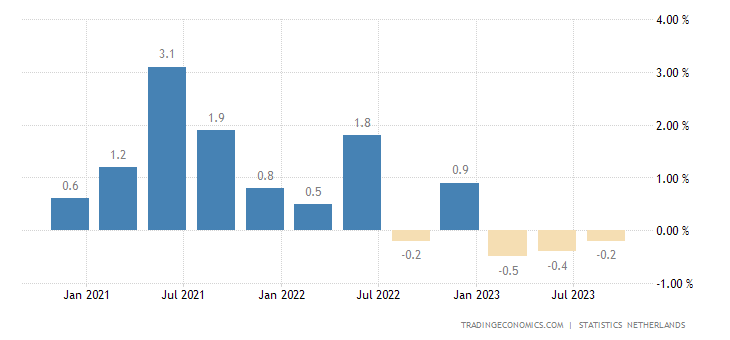

Dutch GDP in July-September -0.2% per quarter – 3rd negative in a row:

Рис. 11

And -0.6% per year is the worst dynamics in 2.5 years, and without taking into account the Covid failure – since the beginning of 2013:

Рис. 12

Orders for machines and equipment in Japan -20.6% per year – the 10th negative in a row:

Рис. 13

And the output of its industry is -4.4% per year – a 3-year minimum:

Рис. 14

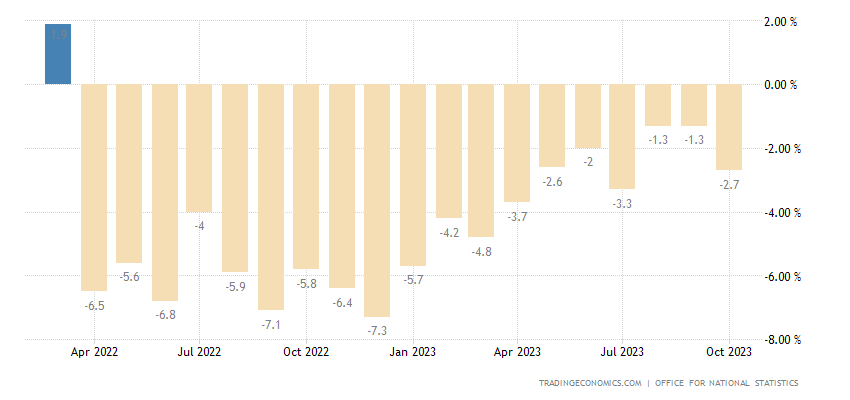

Industrial production in the eurozone -6.9% per year – the 7th minus in a row and the worst dynamics since 2009 (not counting the failure due to Covid in 2020):

Рис. 15

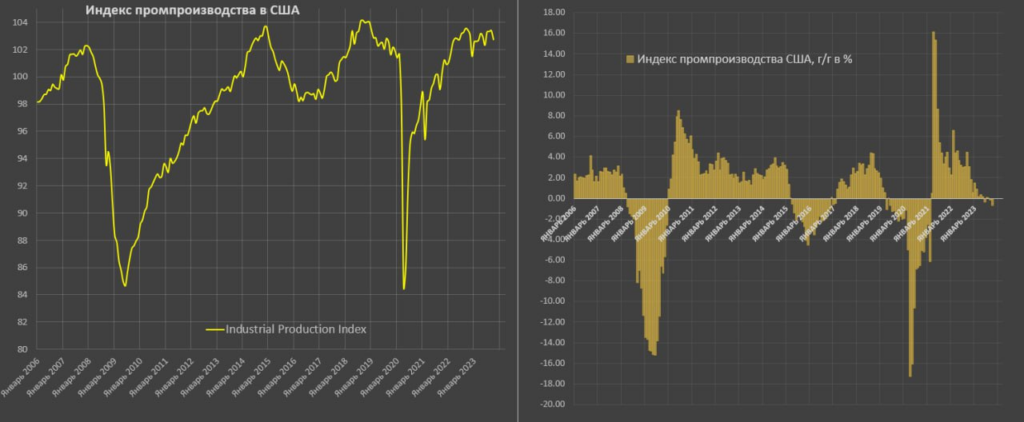

US industrial output -0.7% per year – the minimum for almost 3 years:

Рис. 16

Over the same period, the worst dynamics were observed in the manufacturing industries (-1.7% per year):

Рис. 17

Details of the situation in US industry are in the final section of the Review.

The assessment of the current situation in the German economy remains at 14 years (excluding the failure of 2020):

Рис. 18

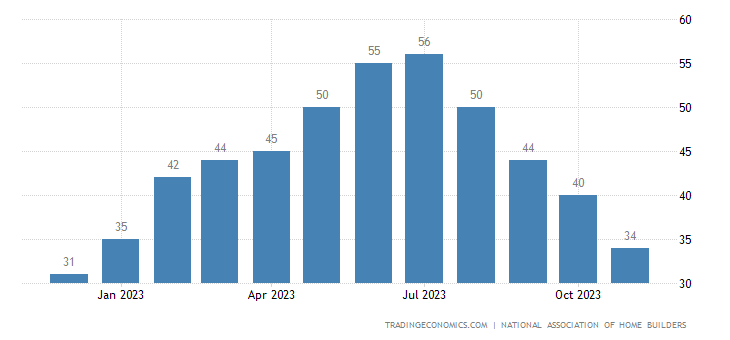

The US housing market index is the worst for the year and in the depression zone (34 points):

Рис. 19

House prices in Britain (Rightmove review) -1.3% per year – the worst dynamics since 2009:

Рис. 20

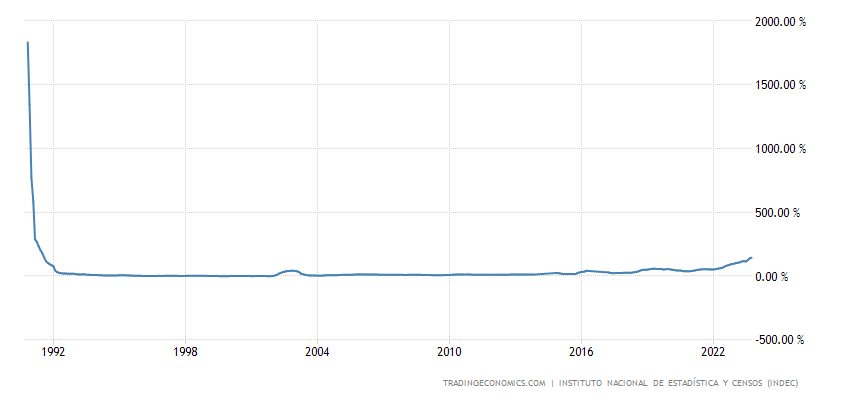

Argentina CPI +142.7% per year – new 32-year high:

Рис. 21

Wholesale prices in Germany -4.2% per year – at least for 3.5 years, and minus covid – for 14 years:

Рис. 22

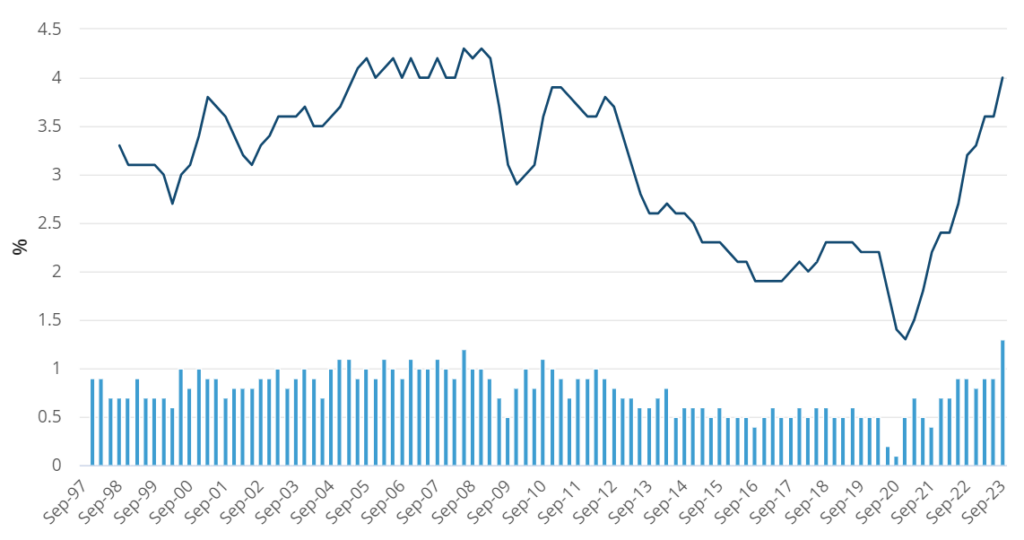

Salaries in Australia +1.3% per quarter (record for 26 years of data collection) and +4.0% per year (15-year peak):

Рис. 23

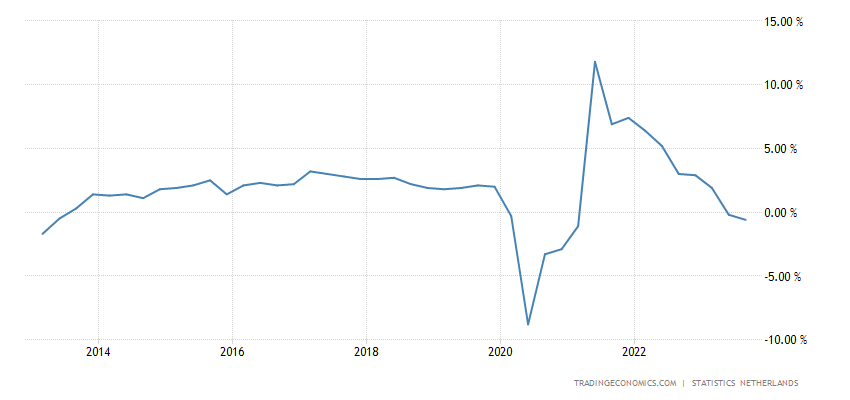

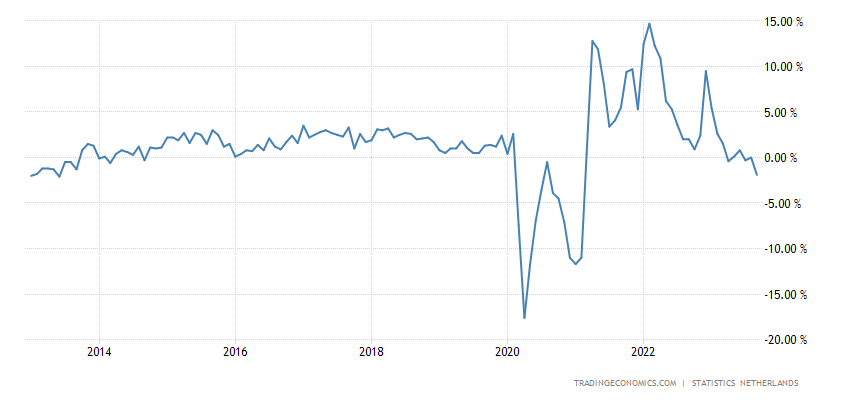

Household spending in the Netherlands -1.9% per year – minus Covid, this is the bottom since 2013:

Рис. 24

Retail sales in Britain -2.7% per year – the 19th monthly minus in a row:

Рис. 25

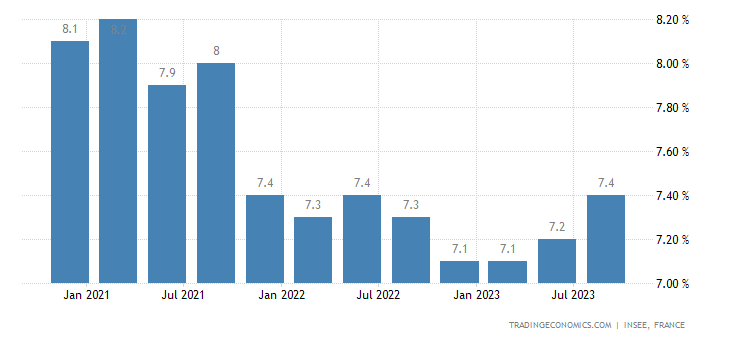

Unemployment in France (7.4%) is the highest in 2 years:

Рис. 26

The number of recipients of unemployment benefits in the United States is the highest in 2 years:

Рис. 27

Bank credit in India +20.4% per year – a record for 12 years of observation:

Рис. 28

Main conclusions. Structural crisis in all its glory. There are no glimmers of positivity, including in the United States, despite all attempts by the monetary authorities to show the opposite.

For this reason, we post materials from Pavel Ryabov (Spydell) about the state of US industry.

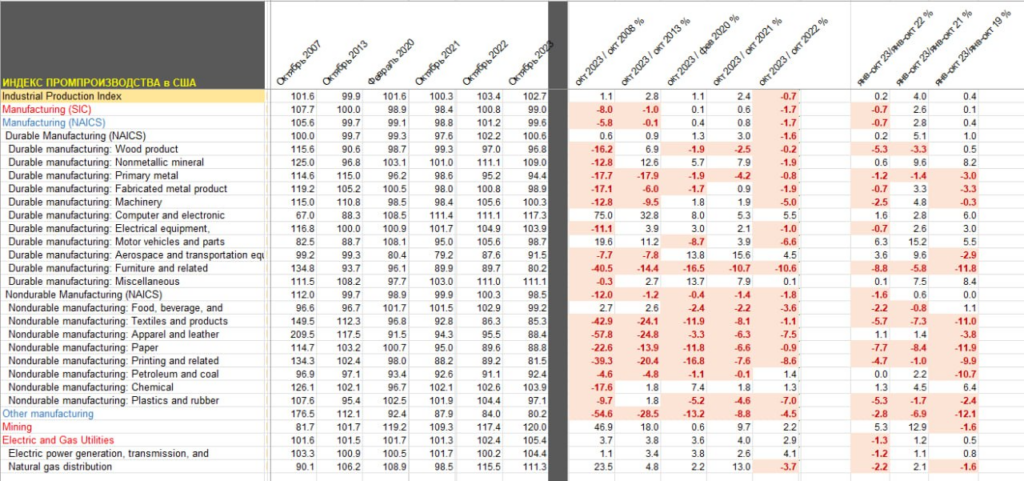

“US industrial production fell 0.7% y/y in October, which was the steepest decline since February 2021 – the post-Covid recovery period is over, which never translated into expansion of production.

For 15-16 years now, the industrial sector has been at the same level – since October 2007, growth has been only 1%. Unbreakable level.

This is the fifth time they have been hitting the industrial production ceiling: 4Q07, 4Q14, 4Q18, 3Q22, and finally the last attempt in August-September 2023. They couldn’t.

There has already been one similar episode in US history, when from 1922 to 1938 the industrial sector was at the same level – although within this period there were dramatic ups and downs, and from 1939 to 1945 the industrial sector grew 3.5 times due to state defense orders and comprehensive industrialization.

This time, such a scenario is not visible – the military-industrial complex has not launched in the United States. If we compare the high-tech segment of the defense sector, which is included in “Aerospace and transportation equipment” – for two years (Jan-Oct. 23/Jan-Oct. 21) there is a quite sensitive increase of 9.6%, but a decrease of 2.9% compared to 2019 for the first 10 months of the year.

Shells and cartridges are included in the “Fabricated metal product”, but here too there is a decrease of 3.3% by 2019. The two indicated sectors include the civilian sector, so it is difficult to assess the exact disposition of the military-industrial complex, but no expansion can be traced. In Russia, the corresponding sectors are growing by tens of percent, although the capacity is incomparably lower in Russia (low base effect).

The comparison goes to 2019, because… In 2021, there was a rather sticky post-Covid recovery with varying intensity and the data was unbalanced across sectors. A detailed comparison by sector and period is presented in the table.

Can’t or don’t want to? Most likely, the United States lacks political will and a developed concept of a modified world order. They believe that the existing forces are sufficient to maintain the existing balance, but have not yet proposed anything new. This is a direct implication of the defense budget plans, which do not anticipate significant expansion.”

In reality, this is a confirmation of Mikhail Khazin’s old thesis that restoring the US industrial sector to the levels of the 50-60s of the last century (“Make America Great Again”, D. Trump) using the resources of the US domestic market is impossible. So the logic of a fight with China for Southeast Asia arises again and again. Taking into account US political decisions and actions in the Philippines, Indonesia and Myanmar, this looks increasingly convincing.

However, let’s hope that this cup will pass for our readers, so we wish them to have a fun weekend and spend the working week without any unpleasant surprises!