Period: 13 – 19 February 2021

Top news story: As a matter of fact, there are two news items this week that are closely related. The first, to put it mildly, is a strong disillusionment with the concept of «Green energy», related to events in the southern United States, in particular in Texas. Thus, the cost of maintaining this model may be significantly higher than expected.

The second news is a strong rise in the prices of multiple asset groups. Oil can still be justified by localized cooling, especially given speculative bursts:

However, it should be borne in mind that this increase generally began before the cold in the United States, which is linked to the large decline in production in that country.

Whereas this circumstance does not at all explain the price of copper, which has reached an eight-year peak. Admittedly, China’s demand has been growing, but it has been growing for almost a year. China is simply returning to its pre-pandemic performance, so there is nothing unexpected about this demand.

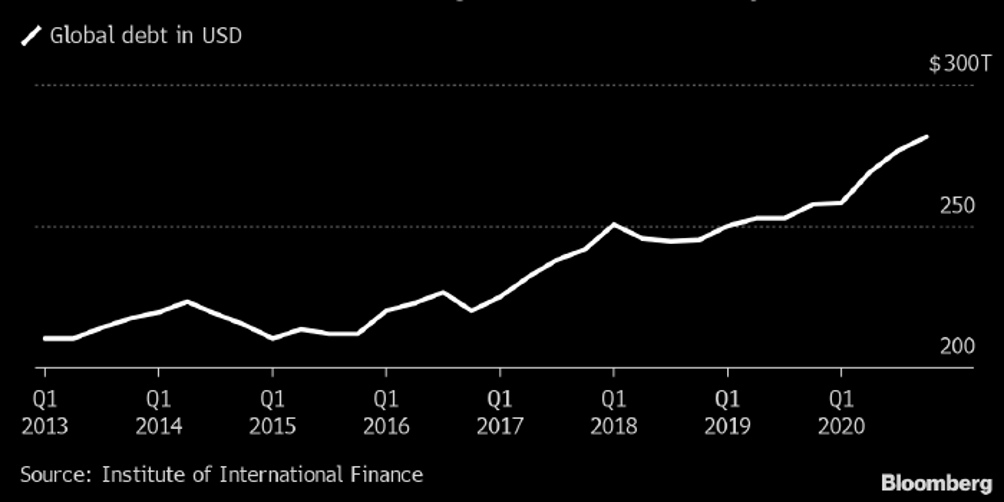

To this should be added the steady increase in total debt:

Macroeconomics

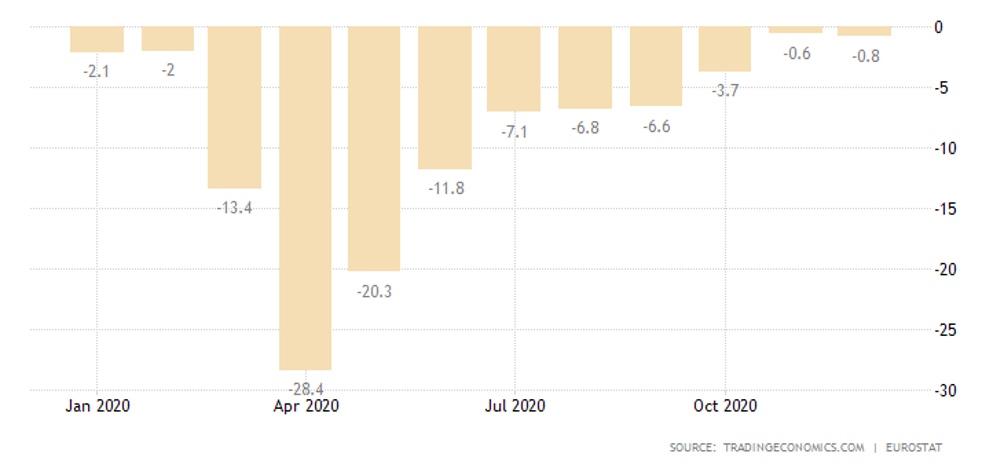

The Euro Area GDP slumped by 0,6% per quarter in the fourth quarter, causing the annual decline to worsen from -4,3% to -5,0%.

Britain’s GDP, on the other hand, grew by 1,0% per quarter in the fourth quarter, bringing the annual recession down to -7,8%.

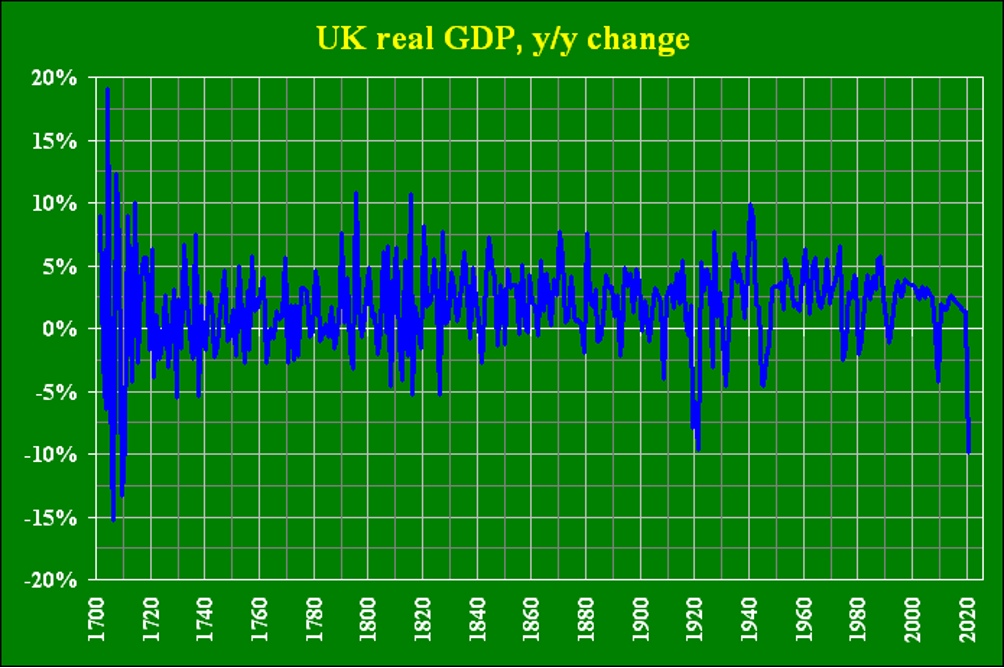

Overall, the economy fell by 9,9% in 2020 – weaker than in 1921 (-9,7%) and the worst performance with the «Great Frost» of 1709:

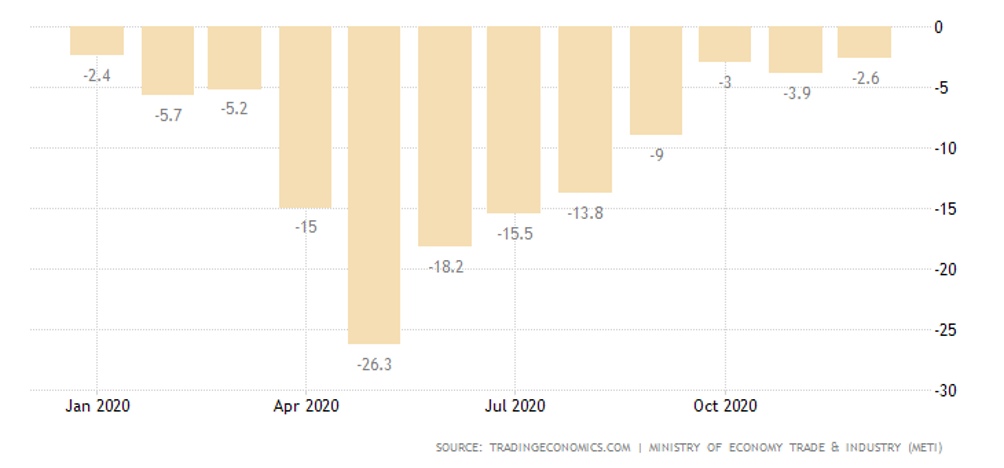

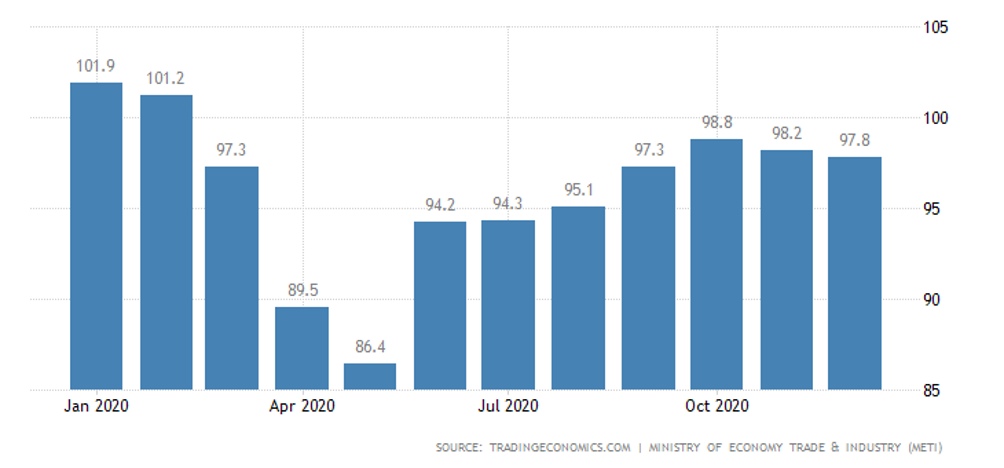

Industrial production in Japan fell by 1,0% per month in December (second consecutive loss), and the annual decline continues (-2,6%):

A similar situation in the Euro Area:

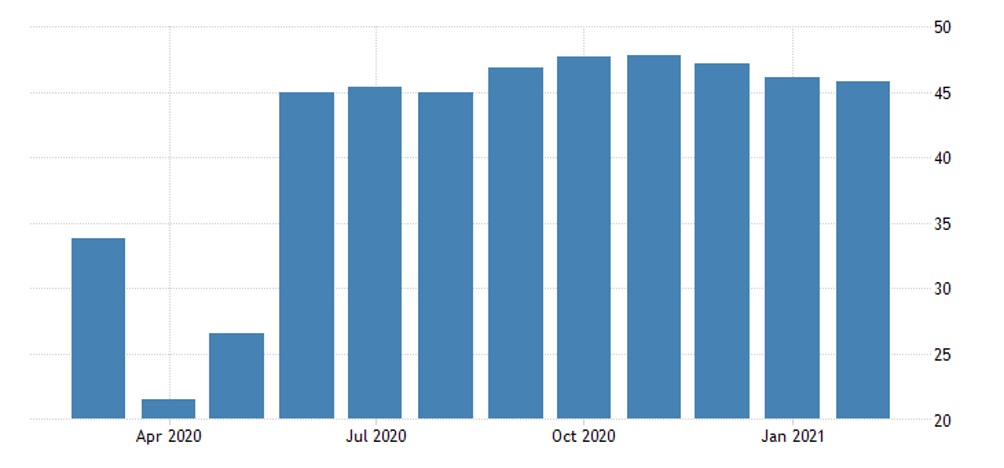

Services activity in Japan declined again:

This is confirmed by the industry PMI:

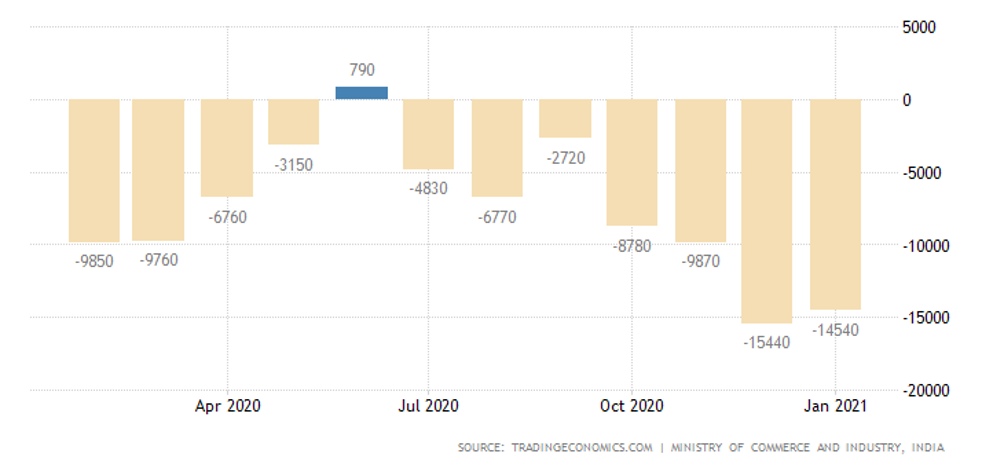

India’s trade deficit is near its worst:

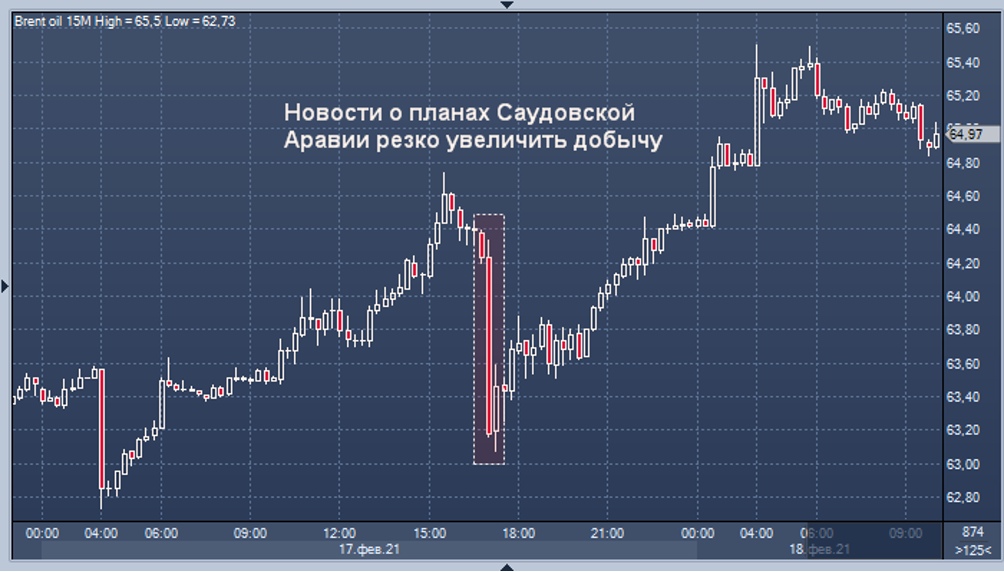

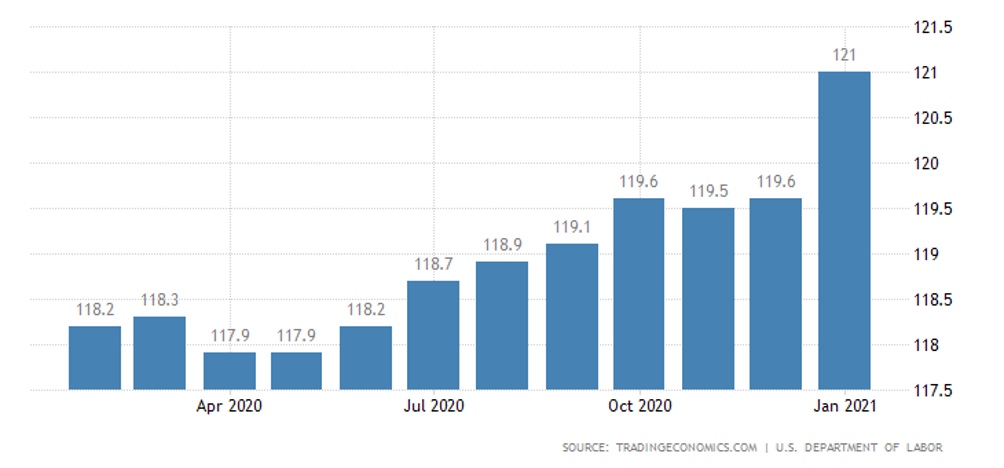

Oil reserves in the United States continue to be severely depleted and oil prices have returned to annual peaks (see fig. 1).

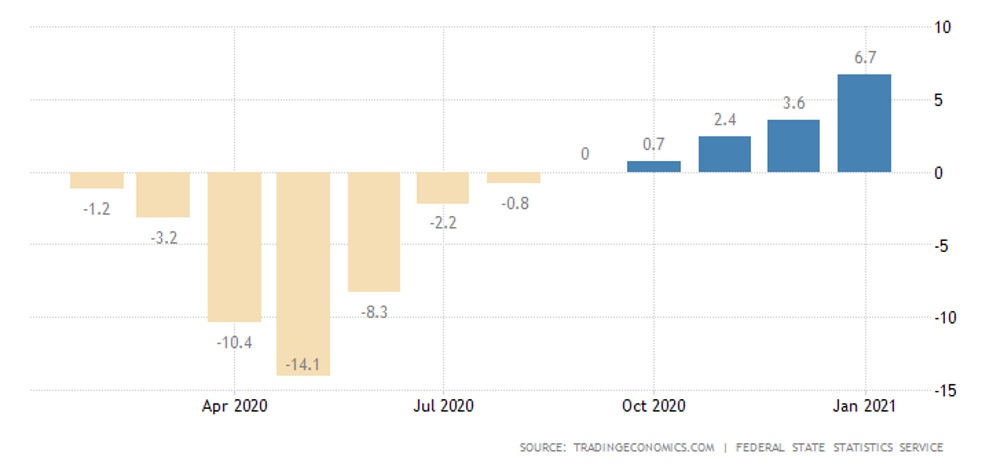

Russia’s PPI (industrial inflation) has been maximal since May 2019 (+6,7% per year):

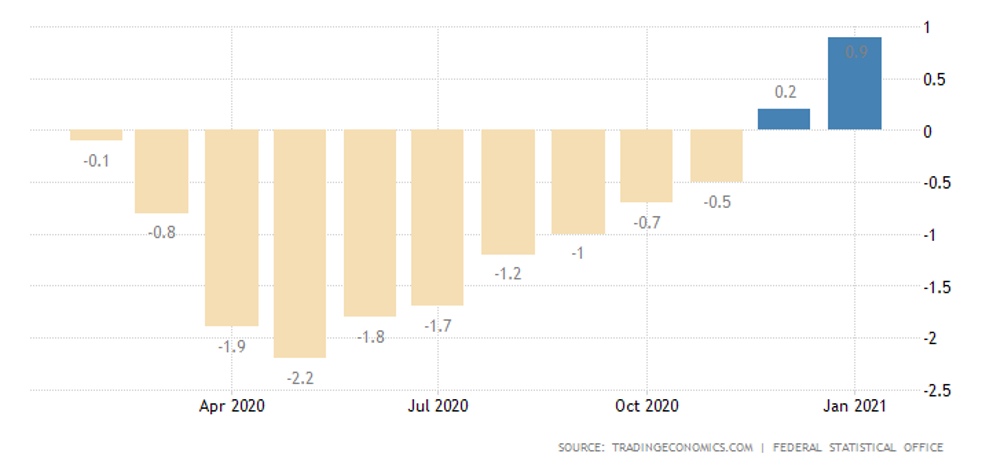

In Germany – since July 2019:

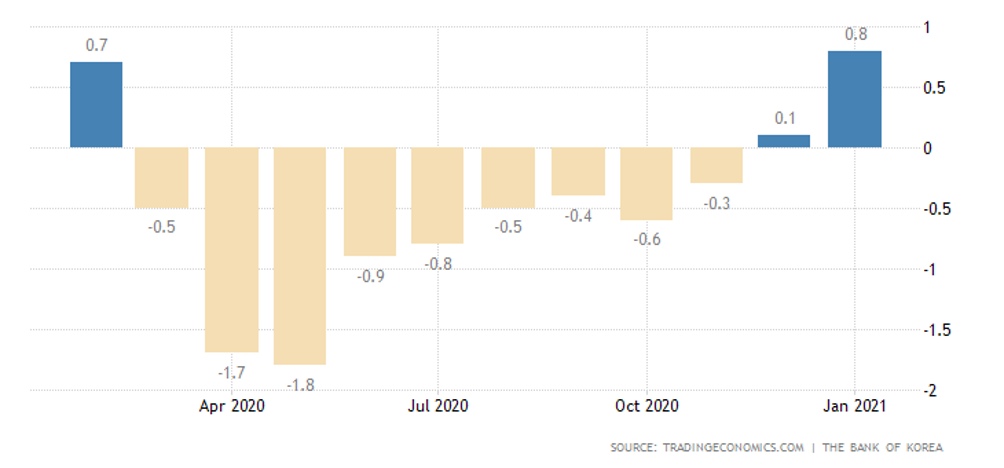

In South Korea – from January 2020:

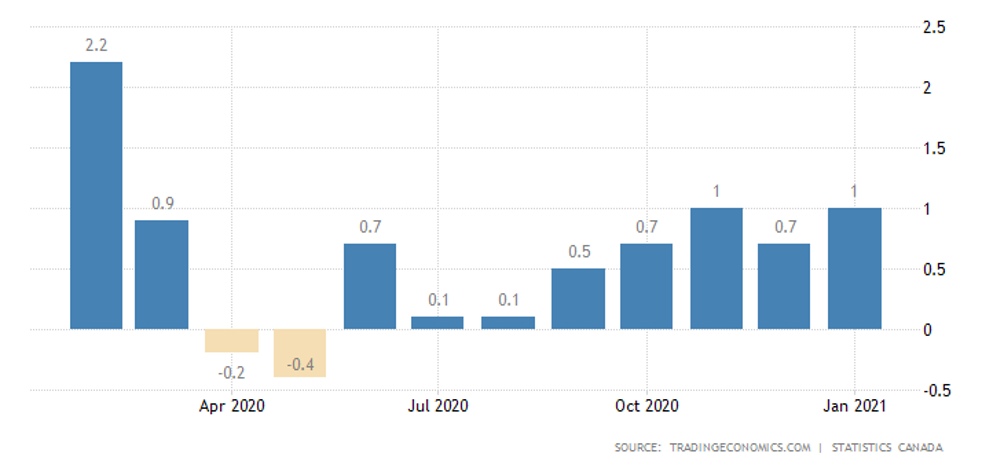

Canada has the largest price increase in a year:

The US PPI surged 1,3% per month – the highest in all 11 years of observation. The highest annual growth since the end of 2019 (+ 1,7%). Without food and fuel + 1,2% per month and + 2,0% per year:

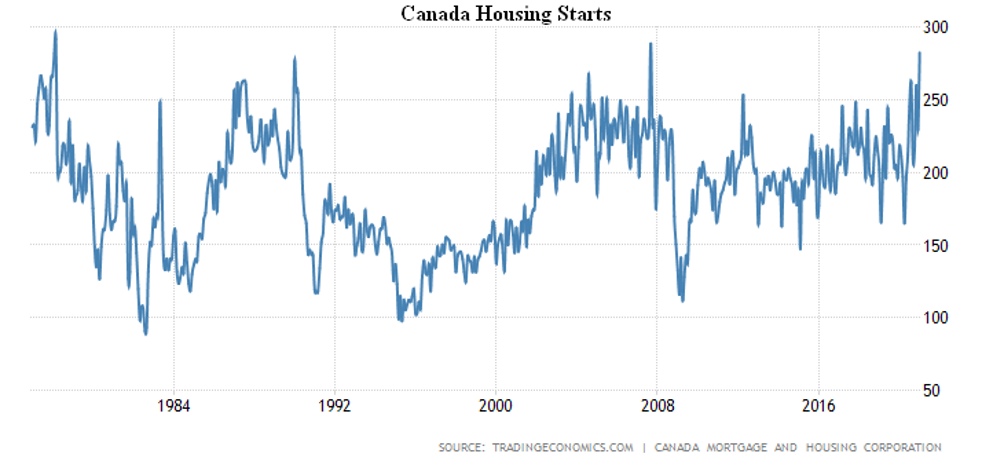

In January, the Canadian New Builds came close to a record: the housing bubble in this country too:

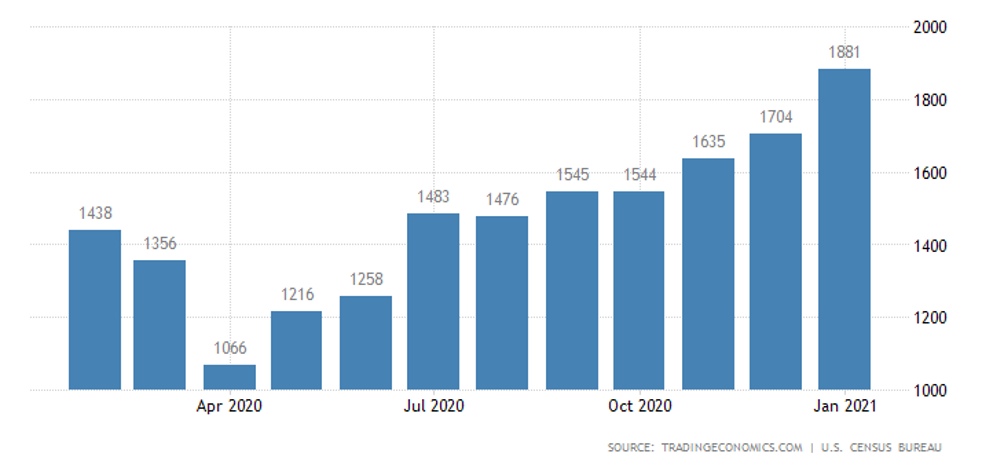

Building permits in the United States are the highest in 15 years:

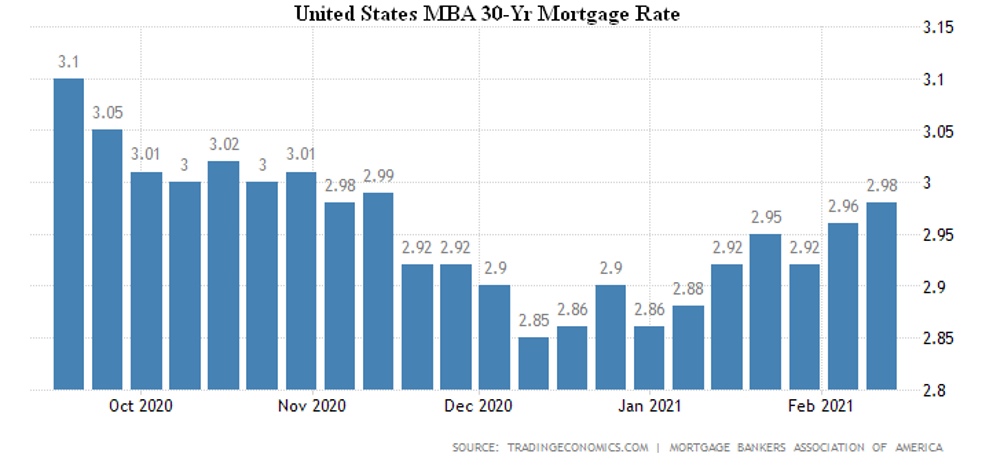

Mortgage applications in the US drop two weeks in a row, because the 30-year mortgage rate peaks in three months:

And the yield on 10-year US government bonds at their highest annual peak:

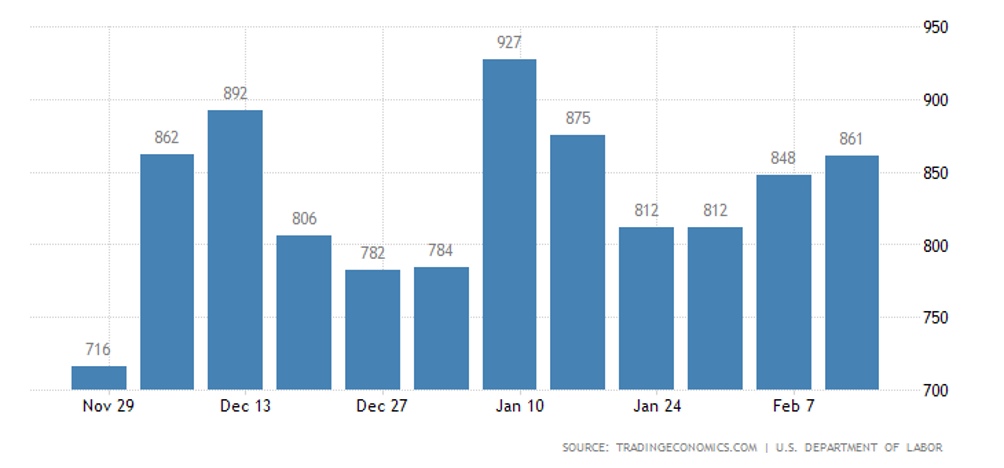

US Initial Jobless Claims Peak in 4 Weeks:

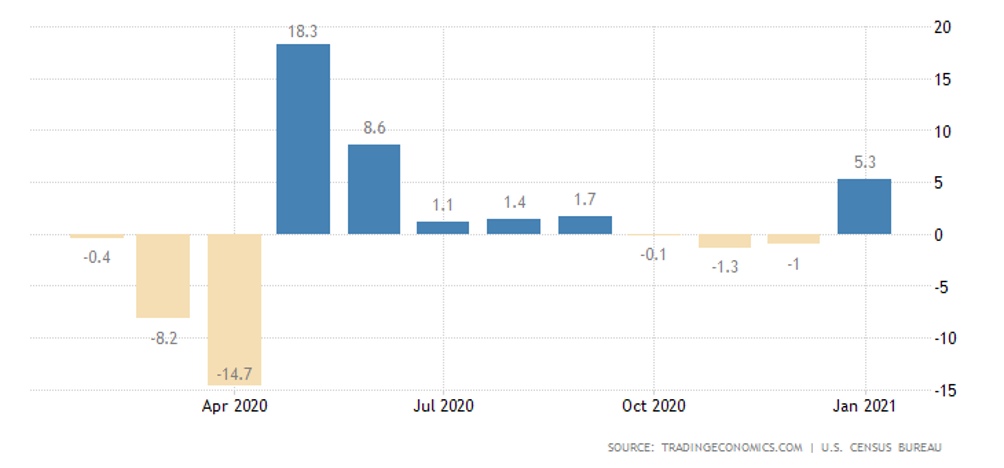

The new stimulus skyrocketed the US retail market in January by 5,3% per month, annual growth (+7,4%) peaked since September 2011:

But in Britain, the opposite is true: -8.2% per month – the worst since April 2020 and more than three times worse than expectations. Accordingly, -5,9% per year – minimum from May 2020 and first minus from June.

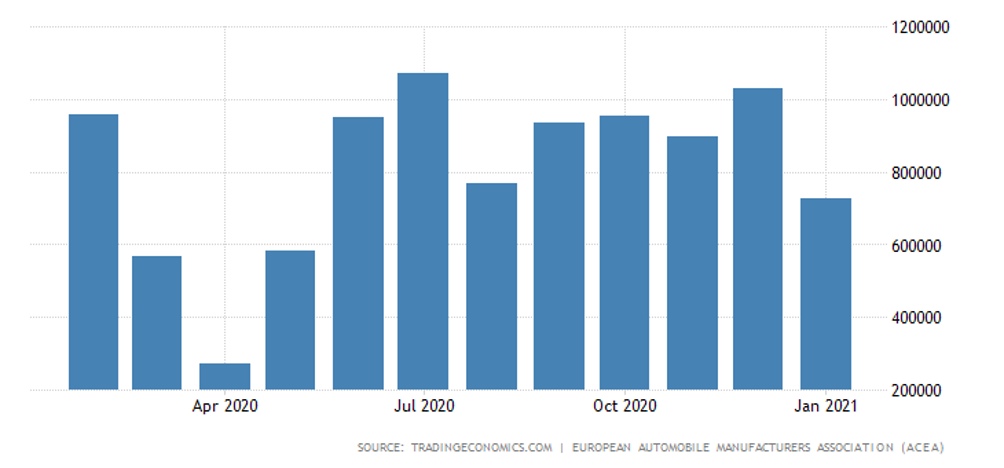

The Euro Area car sales in January are the worst since May 2020:

The Central Bank of Indonesia cut the rate by 0,25% to 3,50% and lowered its GDP forecasts.

The Central Bank of Turkey has left the rates unchanged, contrary to expectations of a reduction. The Fed’s protocol confirmed its willingness to continue the money pump.

Summary. We talked about the onset of the structural crisis in the global and American economies back in the summer. In accordance with the theory set forth in the book «Reminiscences about the Future. Ideas of a New Economy», this crisis should have a decline rate of about 1% per month, as in 1930-32. However, the above indicators are obviously lower in all countries. Why?

This is due to the incentives already mentioned. Statistical and accounting institutions have learned to convert the issuing dollars (euros and other currencies) into nominal value added growth. This raises the formal GDP figures even though the decline is strong. This fictitious share of GDP is extremely difficult to single out, and we estimate it to be around $7 trillion for the US today. That is, real GDP in the US is not $21-22 trillion, but 14-15 trillion (slightly less than China’s).

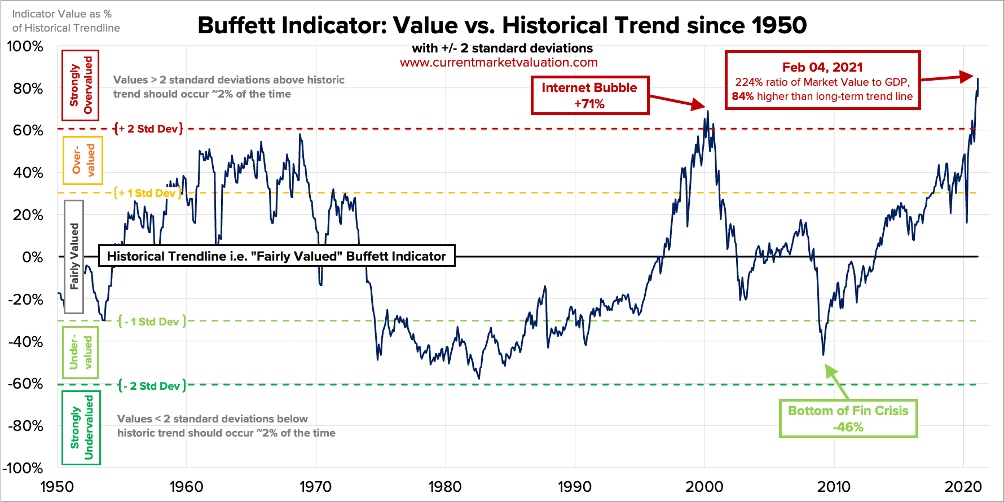

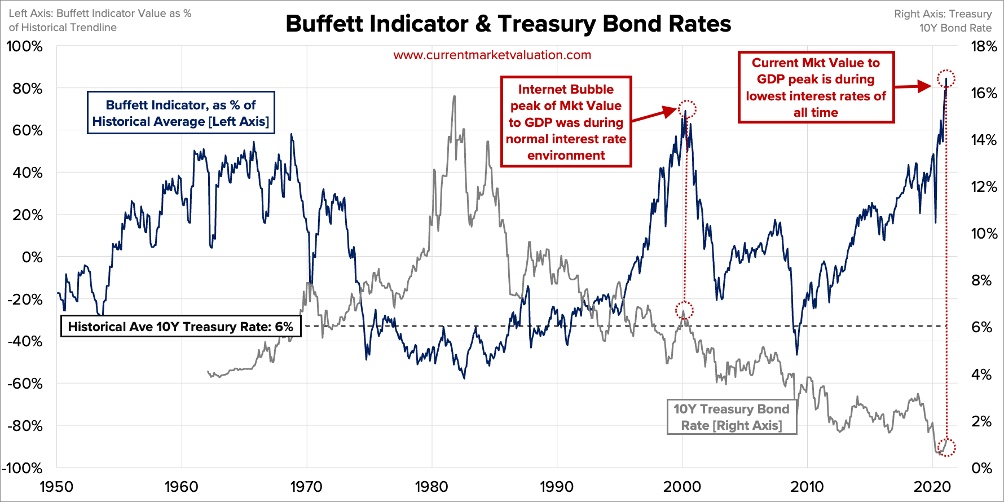

The scale of the bubble in the stock market can be estimated by the so-called «Buffett indicator» (the ratio of market capitalization to GDP), which is at a record high; this is partly reasonable at current rates – but as they rise, this reason will disappear:

We note that the increase in house prices, the decrease in car sales (against the background of an increase in consumer activity), the increase in the prices of other assets mentioned in the first section of our Survey indicate that the equilibrium rates should be significantly higher than the current rates. Of course, their formal rise will immediately formally record an accelerated economic downturn, which is unacceptable from the point of view of politicians, especially before the elections.

But since financial bubbles are not eternal, it will be necessary to return to natural indicators. And the longer the economy remains structurally distorted, the stronger the subsequent recession will be.