Time period: 11-17 December 2021

Top news story. The key news of the week was a press conference by United States Federal Reserve Chief Executive D. Powell following up on the Open Markets Committee meeting. We will give details in the next section of the Review, and here we will highlight the most important point: despite the fact that inflation rates have reached record levels (see below), the Fed head has never explained what to do and what he will do personally. More specifically, Powell made the following points:

- The increase in the number of COVID-19 cases in recent weeks, as well as the Omicron strain, is a future threat;

- We are still witnessing rapid economic growth;

- As a result of the pandemic, some people who might otherwise have sought employment are still unemployed;

- We believe that the labor market will continue to strengthen;

- The supply reduction and supply constraints were stronger and longer than expected;

- The narrowing of the scope of the proposal and its limitations proved to be stronger and longer than expected;

- The inflation rate will continue to rise and will exceed our target of 2% throughout the next year;

- Salaries increases have so far not been a significant factor in inflation;

- We are using all instruments in our hands to maintain the labor market and prevent higher inflation from taking root;

- We believe that full employment will be achieved next year.

Some of these propositions seem highly controversial – we discussed the US labor market in the last Review and their very questionable economic growth – some of them (lowering inflation) have a vague rationale. However, there are strong reasons to believe that no positive trends in inflation expectations can be expected, and this is largely the fault of D. Powell himself.

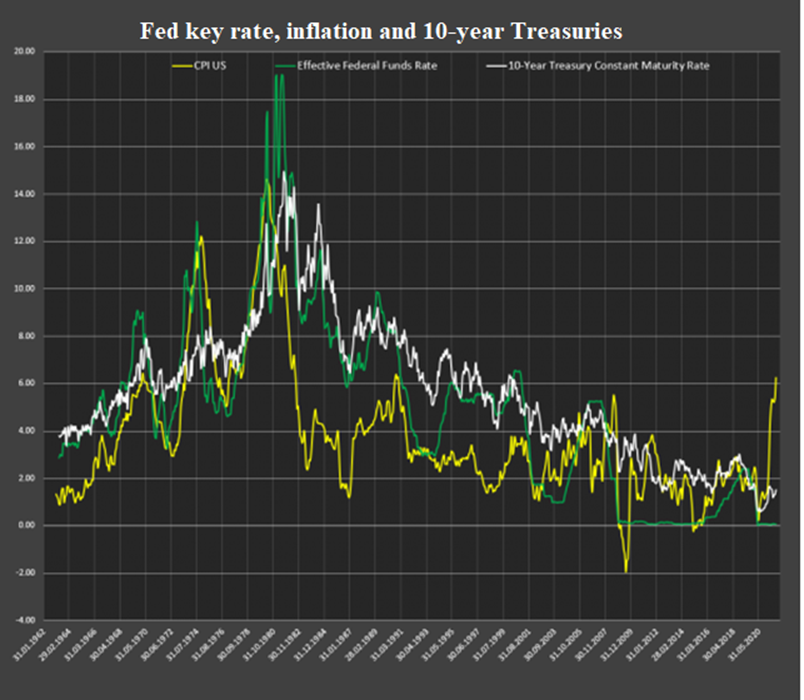

As an argument, we propose the following chart:

This chart shows that the Fed’s key rate has always been rising ahead of consumer inflation. In our reviews, we showed that industrial inflation was expected to rise as early as spring, and in August we claimed that consumer inflation would rise – that is, the gap between CPI and PPI would be reduced by a rise in the former rather than a fall in the latter, as Powell thought. Today, however, inflation has soared, and the Fed has taken no action.

In fact, this means that the leadership of this institute has been engaged not in the strategic forecasting and shaping of the debt market, but solely in the immediate reaction to the situation. Moreover, it is not entirely rational, since there is a far cry from talking about reducing inflation to 2% to the corresponding results. In fact, the Fed washed its hands, which makes the prospects for next year very and very sad.

Macroeconomics

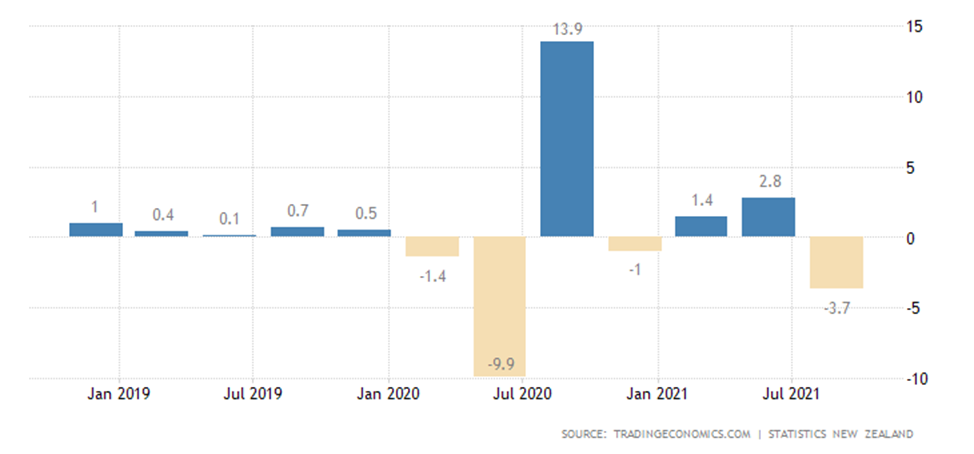

New Zealand’s GDP growth rate is -3.7% QoQ:

And -0.3% per annum:

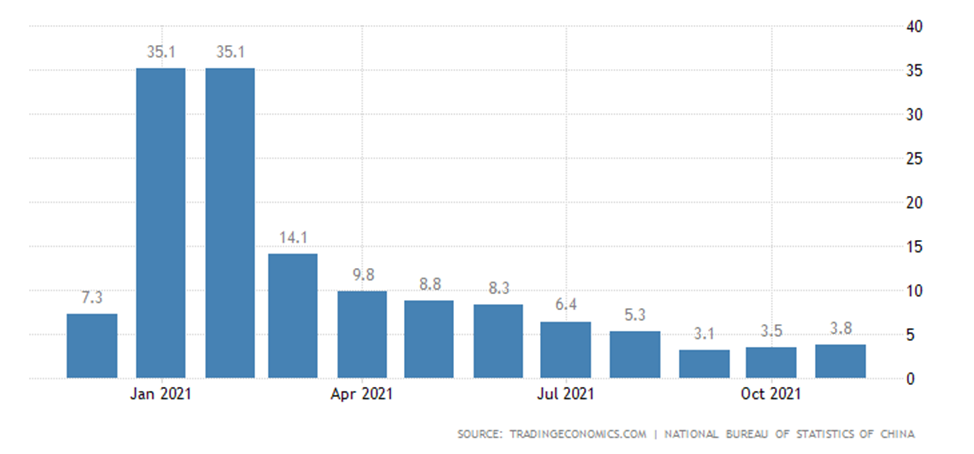

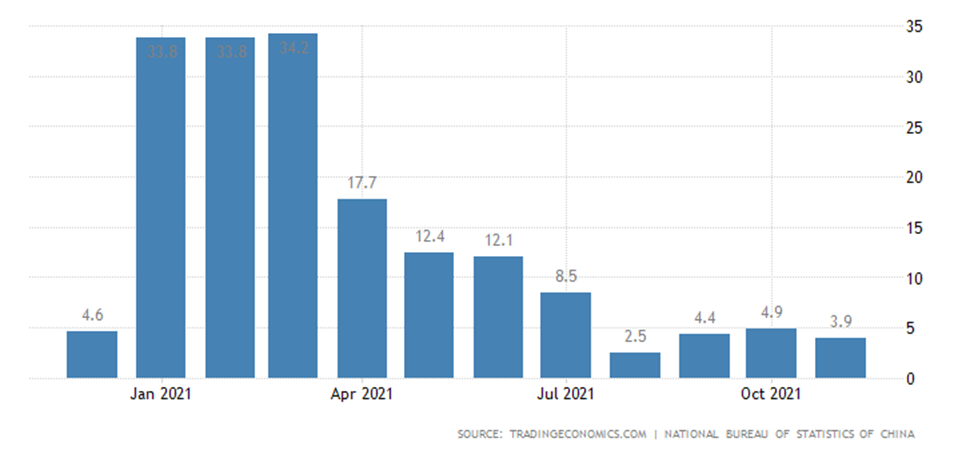

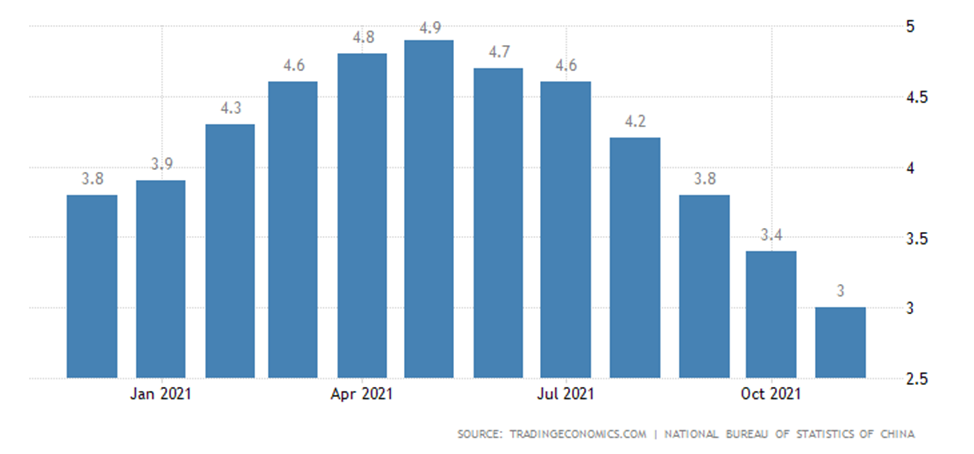

Chinese data are again contradictory: industrial production has accelerated slightly (+3.8% per year), but at a slower pace than before the pandemic:

Retail sales decreased (+3.9% YoY):

Fixed assets investments continue to slow down:

The rate of increase in house prices was the lowest in 6 years:

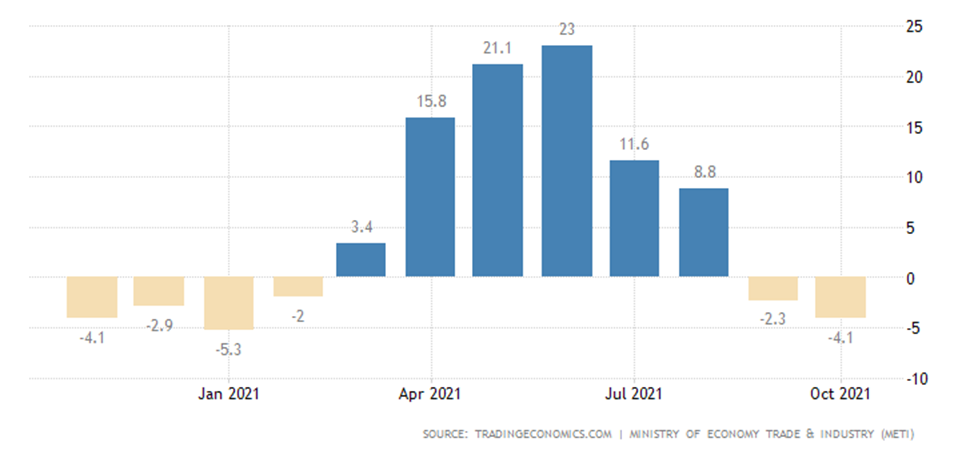

Industrial production in Japan -4.1% per year – the worst performance since January:

The Business Climate Index in Germany (IFO survey) is the lowest in 10 months:

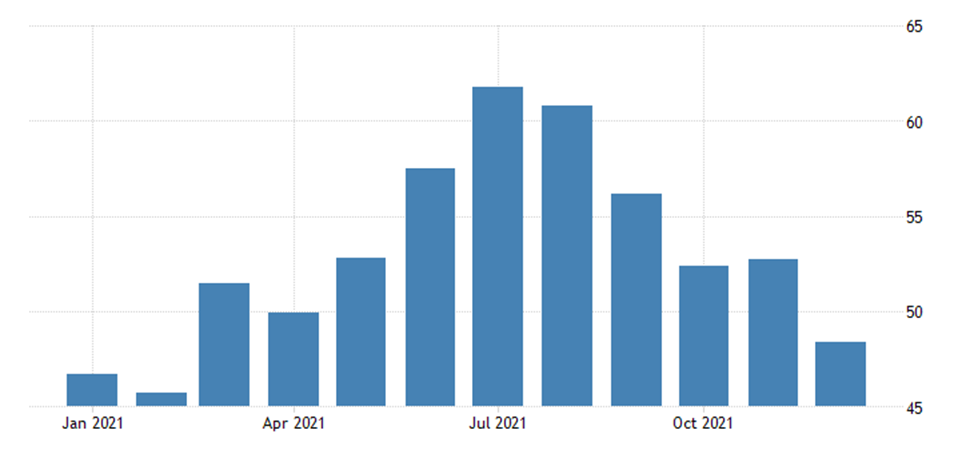

PMI (expert evaluation of the state of the industry; a value below 50 means stagnation and decline) of the German service sector at its’ lowest in 10 months and is located in the red zone (48.4 points):

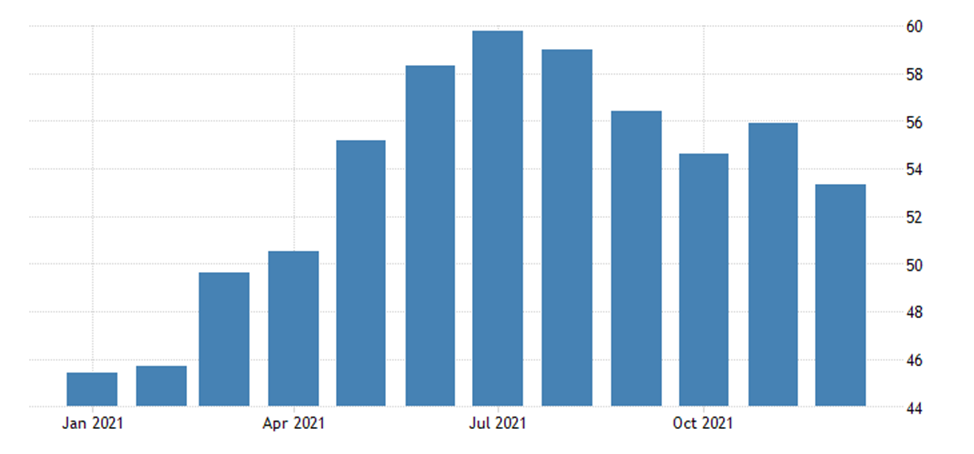

Therefore, and for the Euro Area as a whole, the PMI is the weakest in eight months, but remains in the growth zone (53.3):

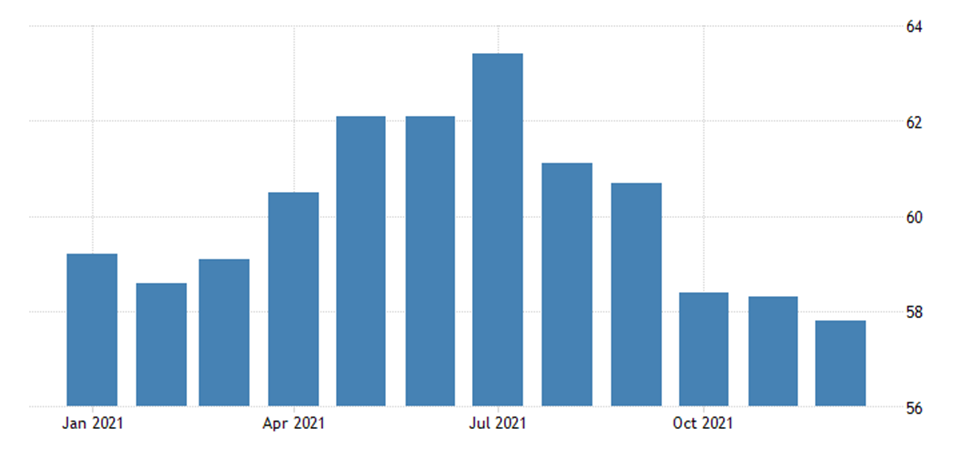

The same picture is in Britain, where the 10-month low (53.2) takes place:

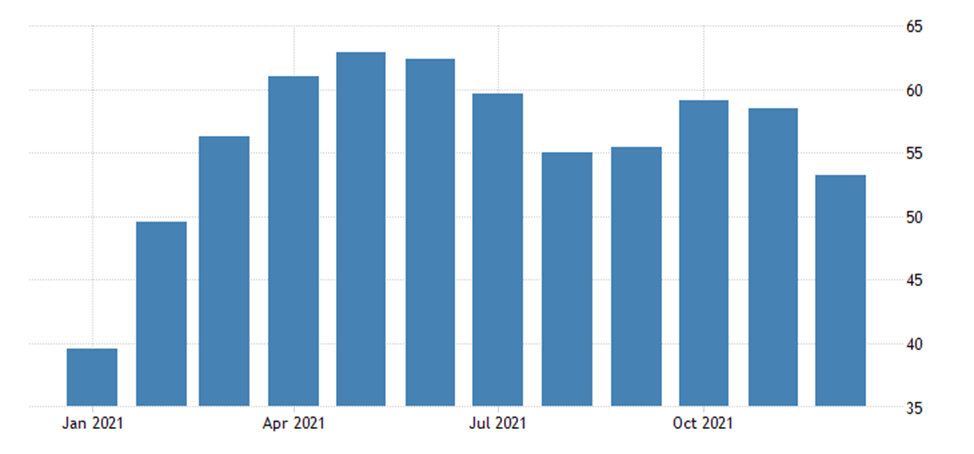

The PMI of the US industry is on an annual trough, but clearly in a growth zone (57.8 points):

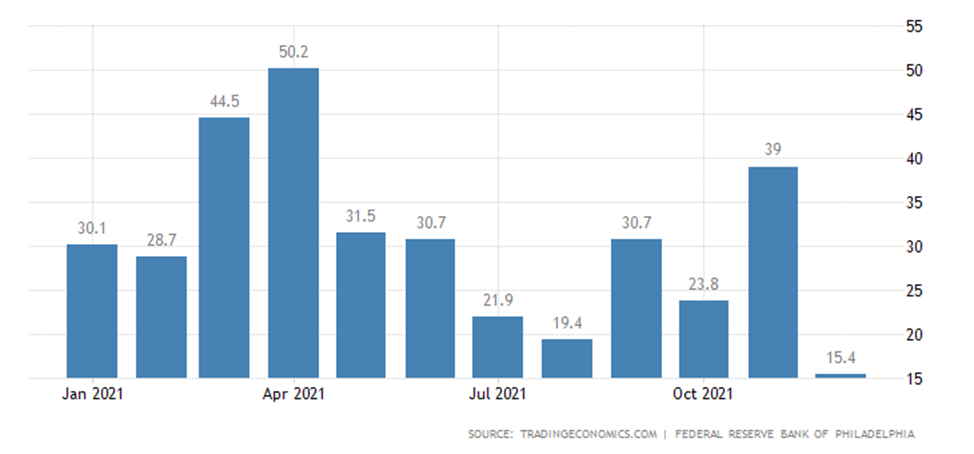

United States Philadelphia Fed Manufacturing Index is the worst in a year:

The optimism of small businesses in the United States remains below the average of many years:

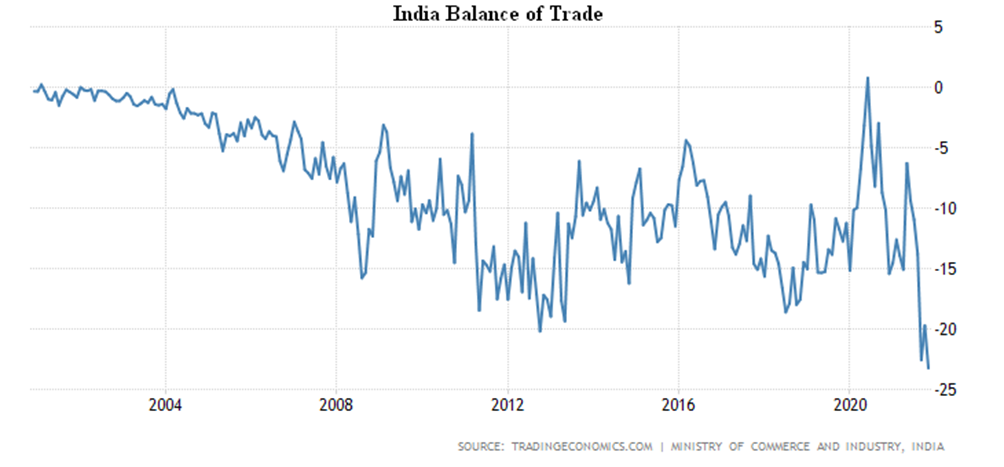

India’s trade deficit hit a record in 65 years of survey:

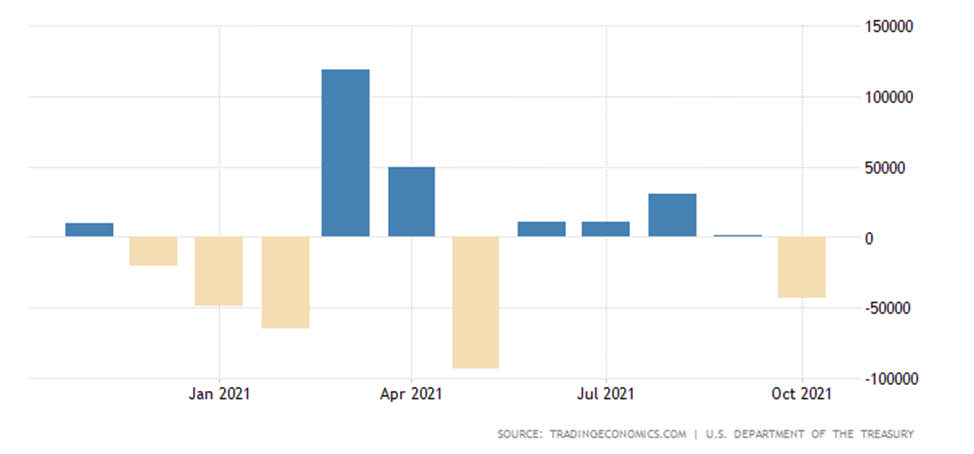

Foreign purchases of US government bonds fell far into the red zone:

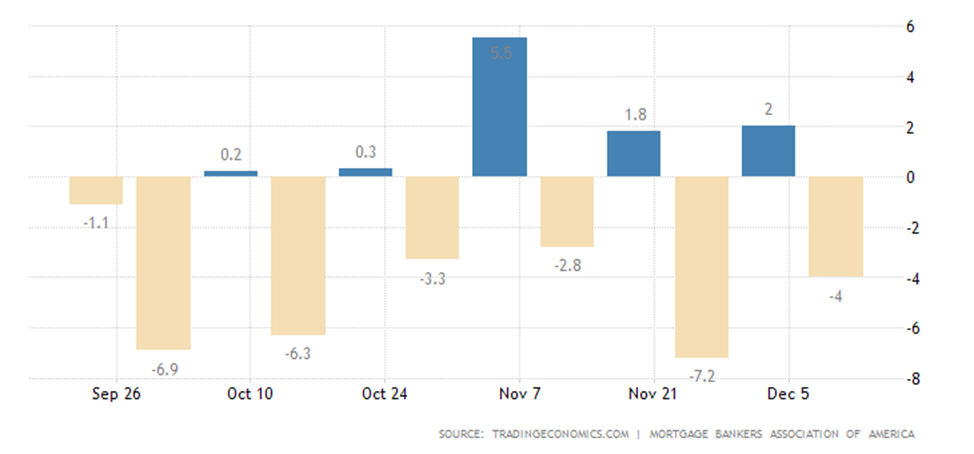

Mortgage applications -4% per week, even though loan rates remained the same:

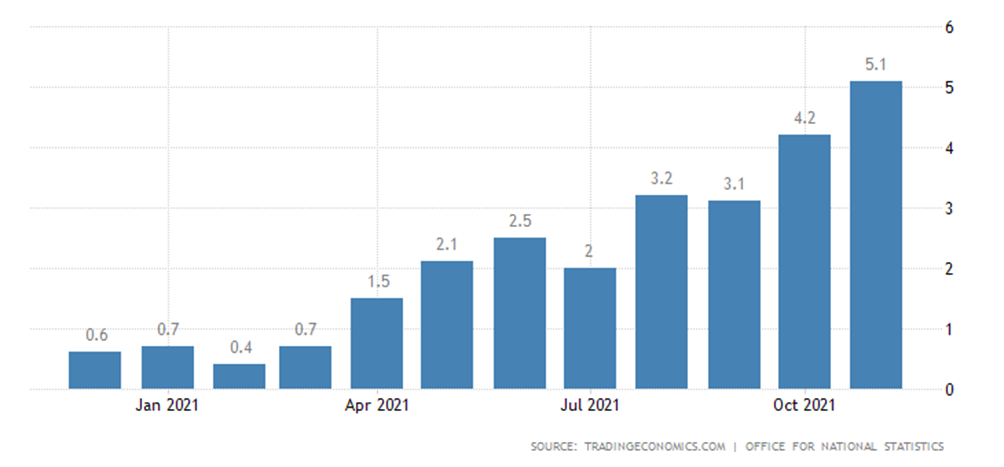

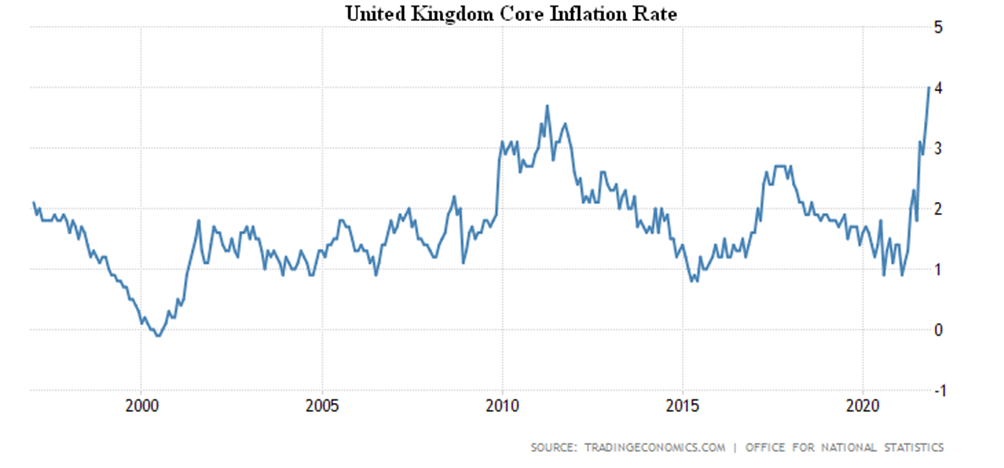

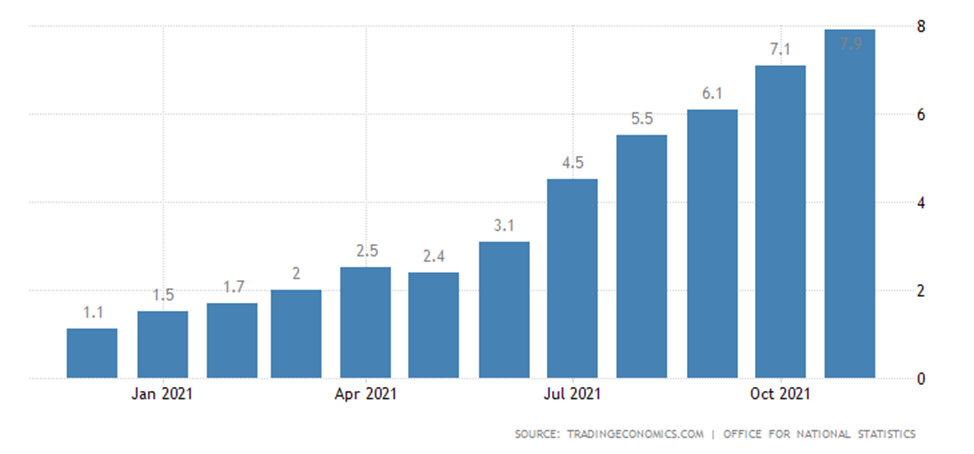

As usual lately, inflation data are breaking records. CPI (Consumer Price Index) in Britain +5.1% per year, this is the maximum in 10 years:

Less food, energy, alcohol and tobacco +4.0%, which is a record for 25 years of survey:

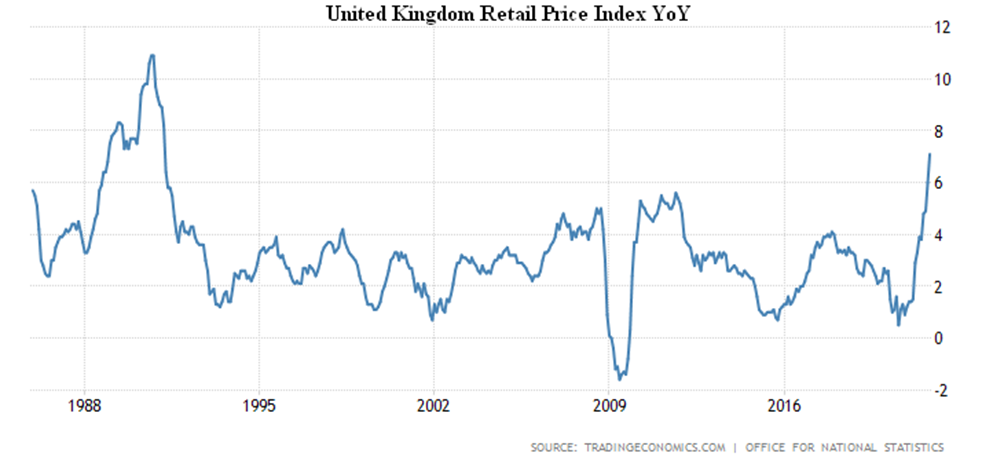

Retail price index (outdated inflation measure) +7.1% per year, the highest since 1991:

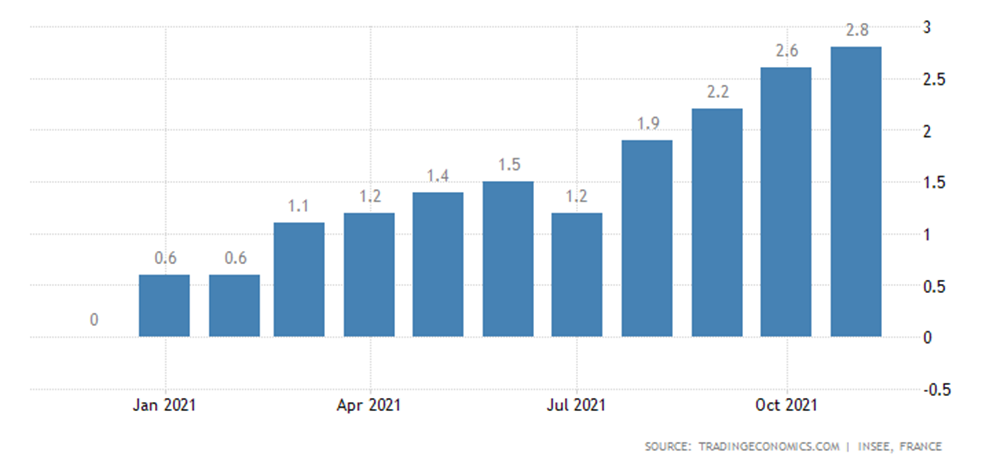

CPI of France +2.8% per year, this is the peak since 2008:

CPI of Italy +3.7% per year, this is also a peak since 2008:

Spanish CPI + 5.5% p.a., top since 1992:

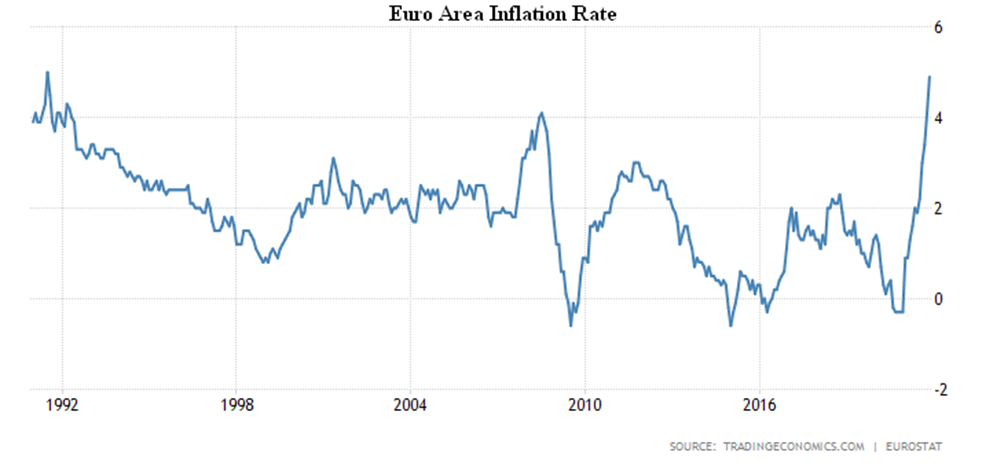

The Euro Area CPI +4.9% per year – a record since 1991:

CPI Canada +4.7% per year, repeating the highest value since 1991:

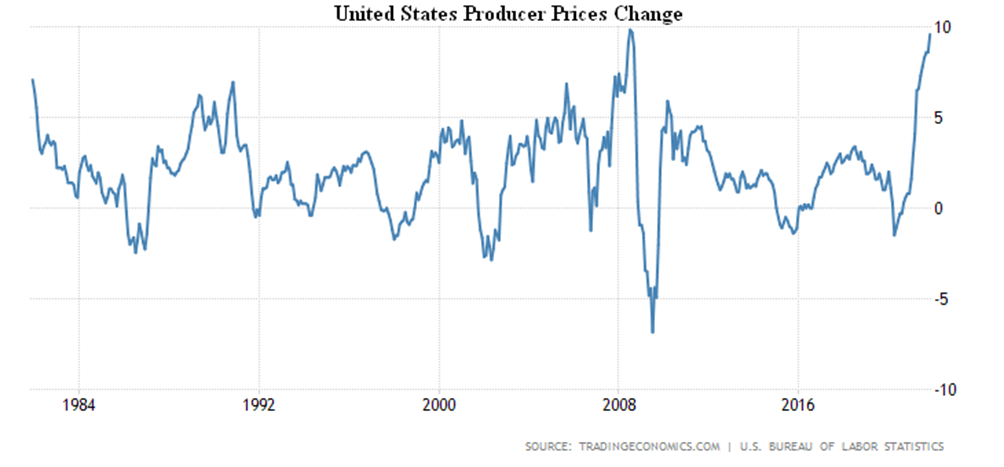

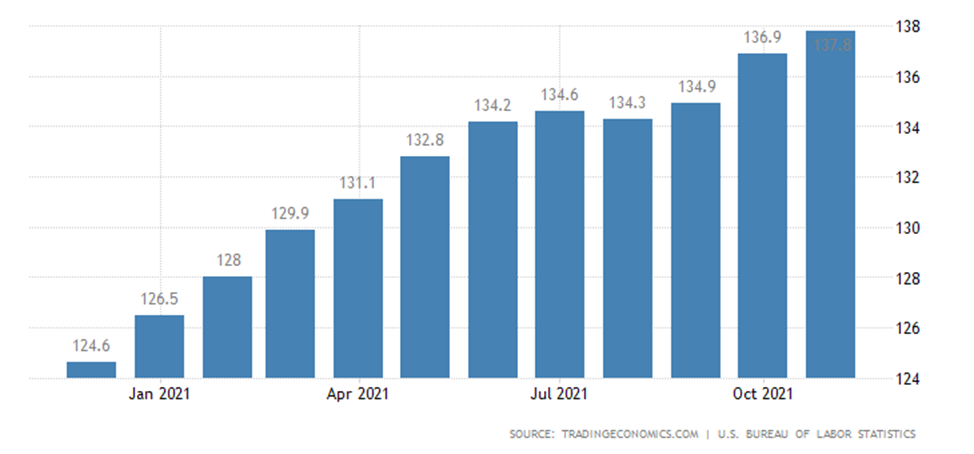

In the USA, PPI (Producer Price Index) +9.6% per year, this is the most intense growth since 2008:

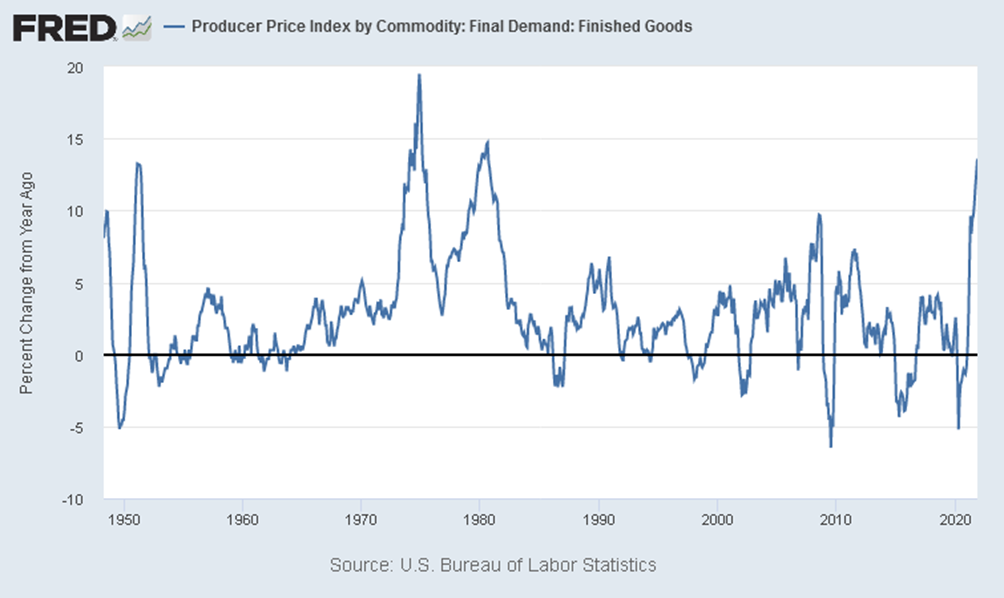

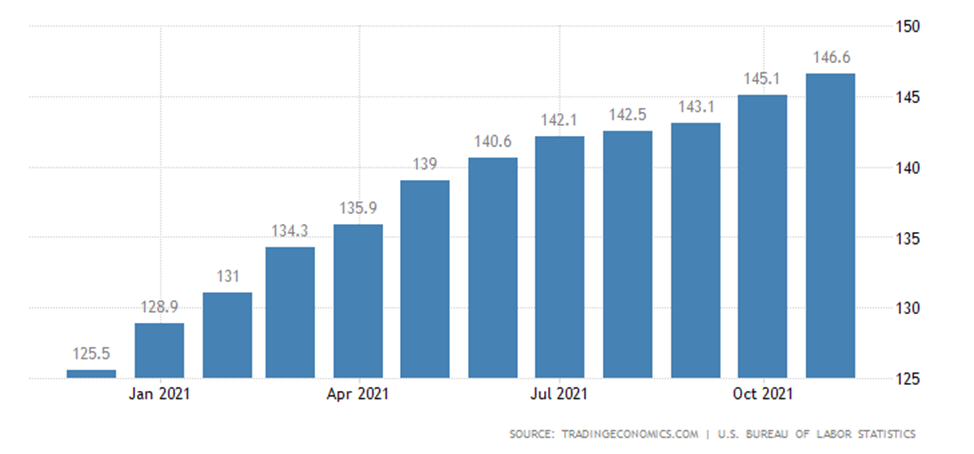

Finished goods +5.6% per year, are at their highest since 1980:

Final goods excluding food and energy +5.6% per year, peak since 1982:

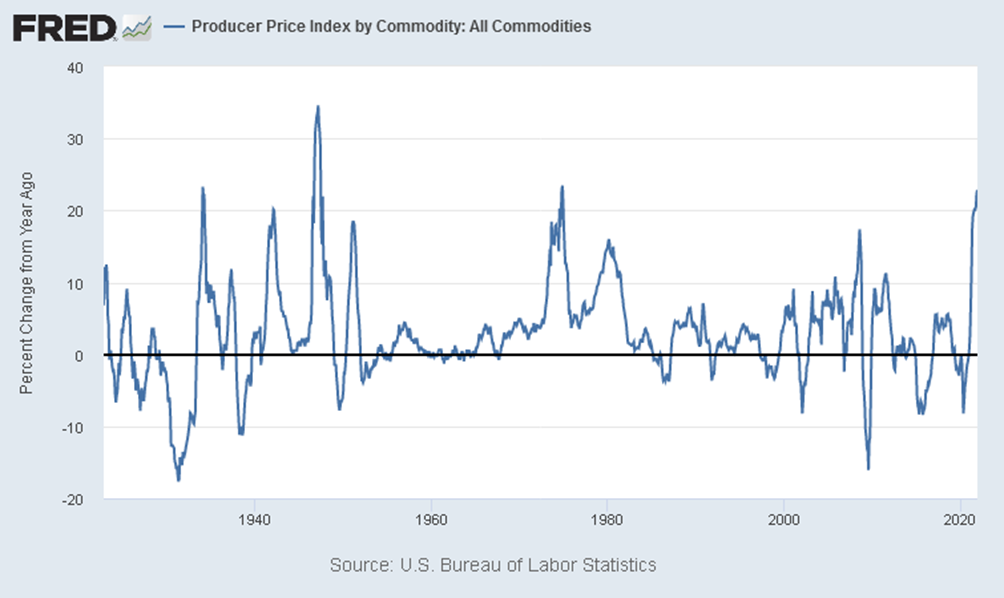

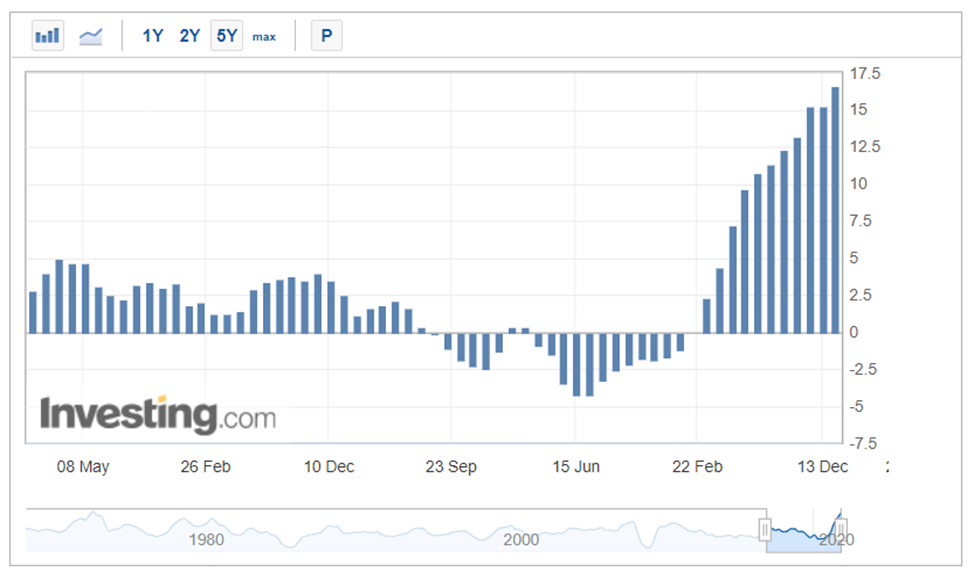

All commodities are 22.8% a year, peaking since 1974 (then 23.4%), previously such figures were only in 1947:

UK PPI + 9.1% p.a., is in the peak since 2008:

Core prices +7.9% per year, a record for 25 years of observation:

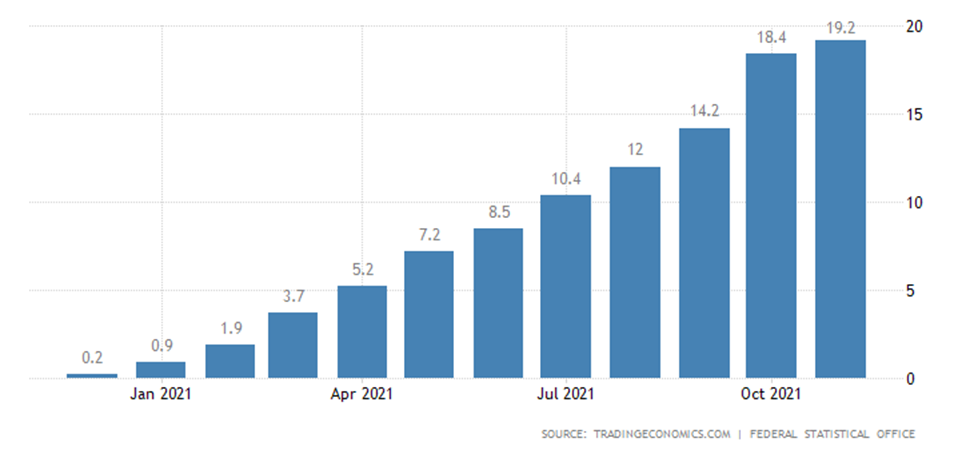

PPI of Germany +19.2% per year, the maximum in exactly 70 years (since November 1951):

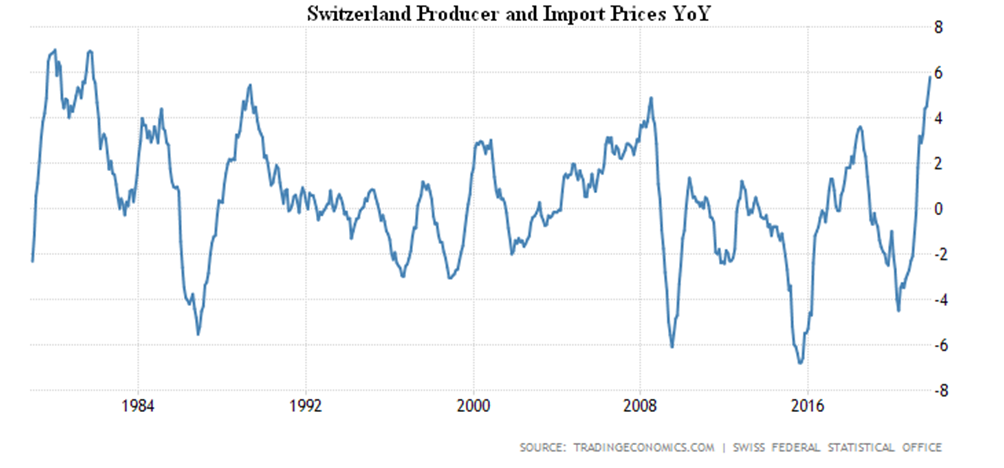

Producer and importer prices in Switzerland +5.8% per year, at the top since 1981:

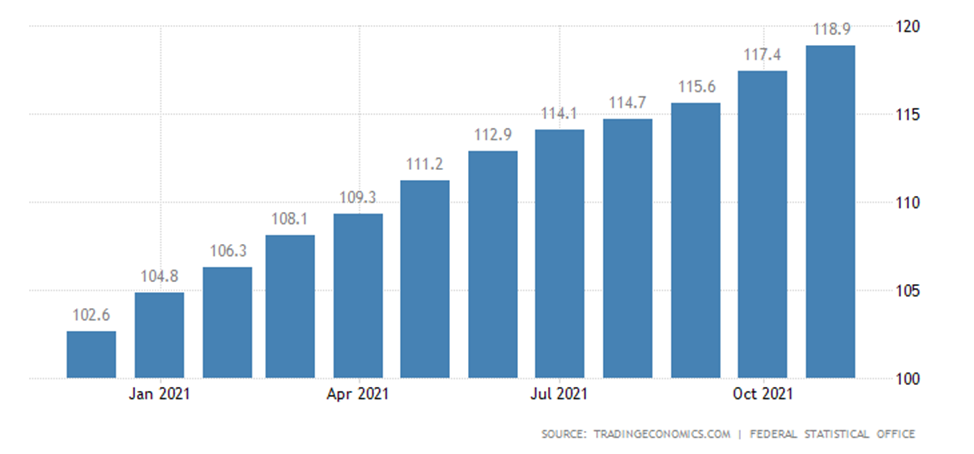

Wholesale prices in Germany +16.6% per year, a record for 52 years of observation:

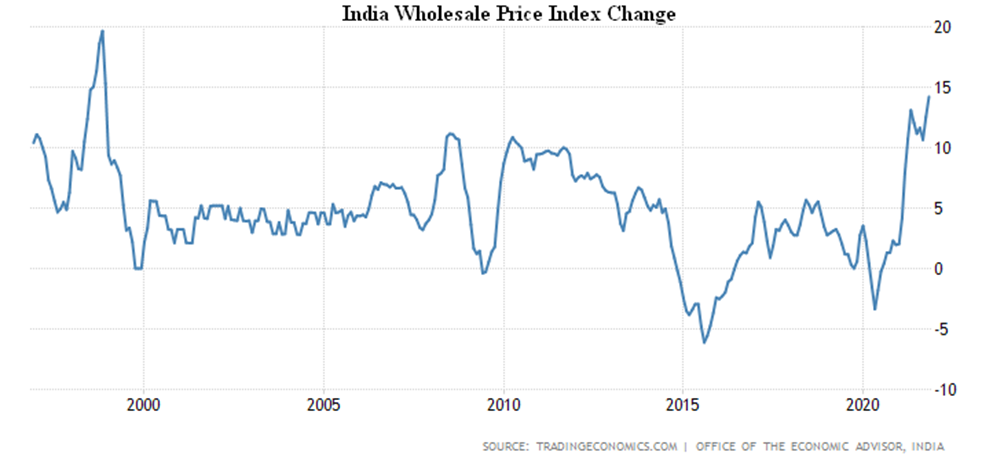

Wholesale prices in India +14.2% per year, the highest since 1998:

Import prices in the USA +11.7% per year, peak since 2011:

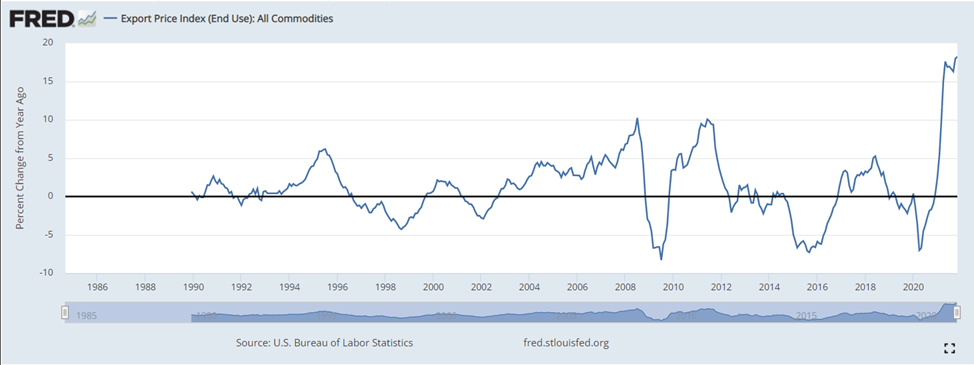

Export prices +18.2% per year, a record for 33 years of survey:

The U.S. Federal Reserve has doubled the scope of decline in bond purchases ($30 billion a month), so the entire program will end in March; inflation is no longer called “temporary” and forecasts have been revised upwards; board members expect, on average, that in 2022 and 2023 they will raise the interest rate three times, and in 2024 they will double.

The ECB is also cutting back on purchases of bonds and will wind them down in March, but keeps them under a different program, which is more tighten; in Europe, the inflationary surge is still considered a temporary phenomenon.

The Bank of Japan is also scaling down purchases to pre-pandemic levels, although it retains emergency assistance. But the Bank of UK did not want to wait and raised the rate from 0.10% to 0.25% surprisingly for the markets.

Mexico’s central bank also surpassed expectations, raising the rate by 0.5% to 5.5%.

The Bank of Russia raised the rate by an additional 1.0% to 8.5%, as expected, although the rationale for this action is far from clear, as inflation in Russia doesn’t have a monetary nature and the cost inflation from raising the rate is only growing. The Central Bank of Indonesia did not change anything, nor did the Swiss Central Bank.

And the Central Bank of Turkey continues to cut rates by an additional 1.0% to 14.0%, as a result of which the lira continued its free fall vertically, and problems began on the Turkish stock exchange:

Summary. The monetary authorities of all countries of the world (specifically about the US we have already written above) have no idea what to do. The traditional recipe is to raise the rate, but this cannot be done with accumulated debt by households and corporations. Nor can it be tolerated: the US has a midterm election in November 2022, and with such inflation there is absolutely nothing to do. In theory, it can be reduced in part, and the Fed has already begun to do large-scale, about $1.5 trillion, and reverse repo operations – short-term sales of the paper on its balance sheet for cash. The problem is that, on the one hand, inflation has a structural component that such operations do not affect, and, on the other hand, budgetary programs to support the economy need to be launched. Naturally, it will increase the amount of money in the economy.

The situation needs to be resolved before May – after which there is nothing new to explain to voters – which requires very drastic and decisive action. Powell’s words don’t make sense, and neither can his actions. And these actions, by and large, don’t exist, except for the emissions. Dropping everything before an election is a bold decision, and for that reason we see only one course of action: if we continue sterilizing the money supply, we need to sharply cut back on spending (for example, stop financing many US allies) and start cutting imports, at the same time increasing subsidies to the real US sector. That is, in other words, very quickly to break up the world dollar system and begin to move to economic autarky.

Whether it will help is a big question, because we need to act very quickly. But these are, nevertheless, actions that could potentially be “sold” to the electors. Ultimately, the Democratic Party of the United States does not need a victory, but just a minor defeat in the elections. Now, let’s hope for the best.

We wish our readers a productive working week!