Time period: 19-25 February 2022

Top news story. Undoubtedly, the main news of the week was the operation to demilitarize and denationalize Ukraine, initiated by Russia. Of course, the imposition of accompanying sanctions too. It will only be a few weeks before one realizes their real impact on both Russia and its allies, and for those who have imposed these sanctions, but certain points can be made. First, contrary to the traditions of recent years, European sanctions are much more severe than American sanctions.

Second, the sanctions of European countries proved to be more reckless: for example, the ban on “Aeroflot” to fly to London immediately resulted in a ban on British companies to fly through Russian airspace. This means, a priori, a sharp increase in the cost of routes from England to South-East Asia. Thus, the response to England was stronger than the main sanctions.

Thirdly, American sanctions in this sense have a very precisely directed impact, and mainly concern financial issues. In fact, they are not of particular importance to the Russian economy, but are of a demonstrative and propaganda nature. In terms of overall development, this is understandable: if US leaders are somehow responsible for the situation, the European Union politician is in principle not responsible for any action. In this regard, they have a very short life span and are aimed at at meeting momentary political problems. All the consequences in such a situation cannot be calculated, and problems are solved as the attack.

It is certain that no positive outcome in an economy with such an approach can be achieved, as will be evident in the next section of the Review.

Macroeconomics

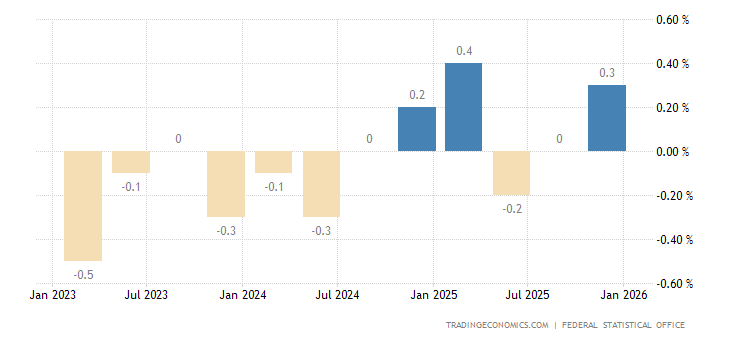

In the 4th quarter of 2021, Germany’s GDP is -0.3% per quarter:

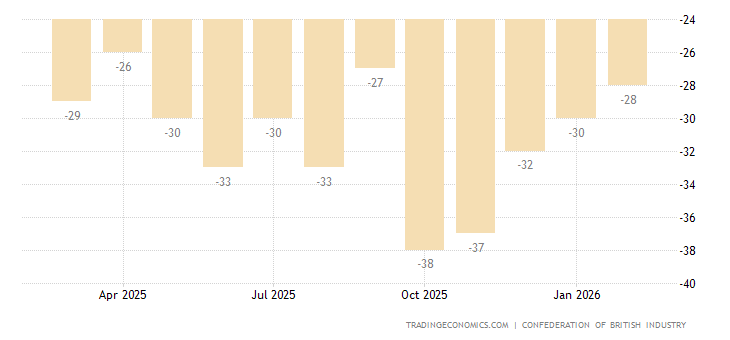

United Kingdom CBI Industrial Trends Orders had become somewhat worse, with 77% of businesses raising prices, which has peaked since 1976:

PMI (the Peer Review Index, which describes the conditions in the industry; its value below 50 signifies stagnation and decline) of Japan’s service sector at 42.7 points, at its lowest since May 2020:

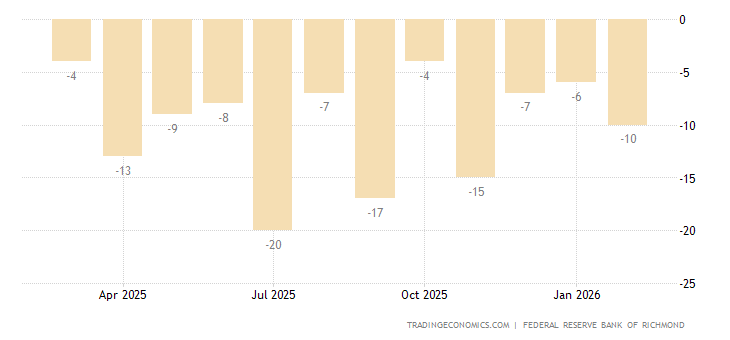

United States Richmond Fed Manufacturing Index is the weakest in 5 months:

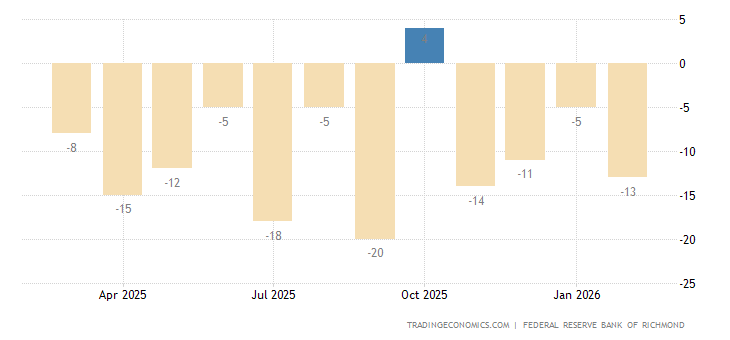

And United States Richmond Fed Manufacturing Shipments Index is the weakest in almost two years:

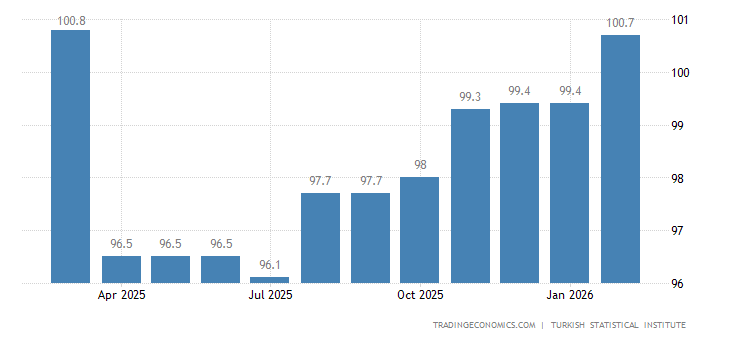

Turkey Economic Confidence Index is at a 9-month trough:

It is customary to note that if inflation rates are calculated objectively, then the indicators of industries are significantly degraded, which will worsen both indices and market sentiment. But inflation understatement is a habit of any authority, so it is useless to complain, whereas inflation rates are already accustomed to breaking records.

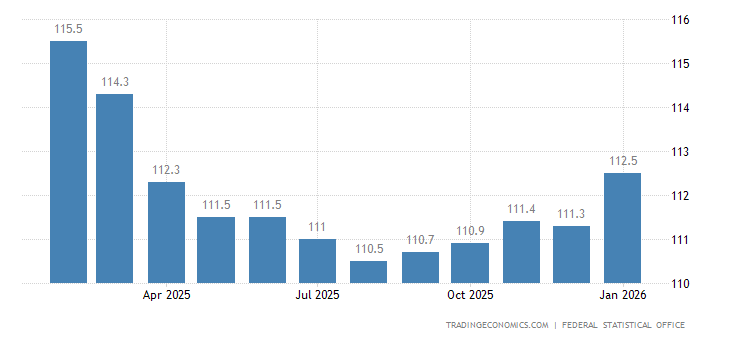

Import prices in Germany +26.9% per year, which is the highest since 1974:

PPI (Producer Price Index) of Germany is +25.0% per year, which was a record for 72 years of survey:

PPI of France is +22.2% per year, a record in 22 years of statistics:

PPI of Spain 35.7% per year, which is a record in 46 years of survey:

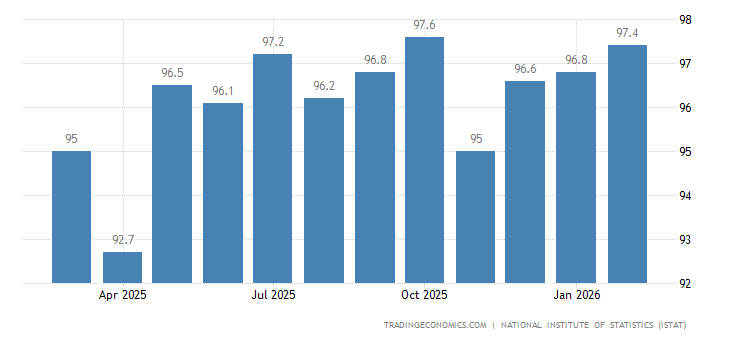

Italy’s CPI (Consumer Price Index) is +4.8% per year, and is the highest since 1996:

Monthly performance (+1.6%) is at its peak since 1982:

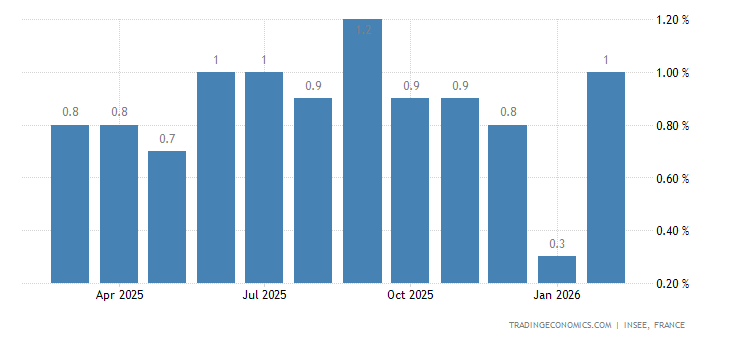

CPI of France 3.6% per year, at its height since 2008 and near its peak since 1991:

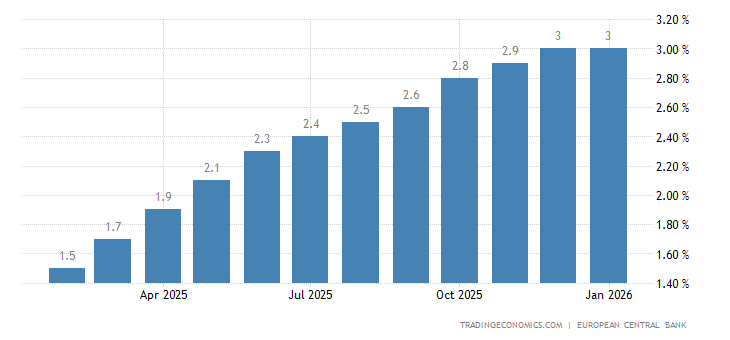

The Euro Area CPI +5.1% per year, which is a record for 31 years of survey:

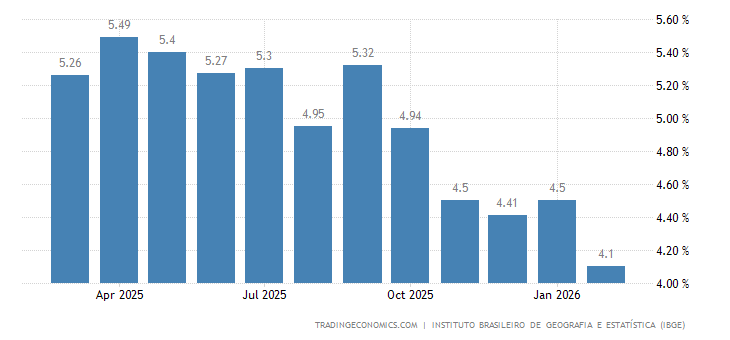

CPI of Brazil +10.8% per year, which is a return to the 19-year peak that took place in 2016:

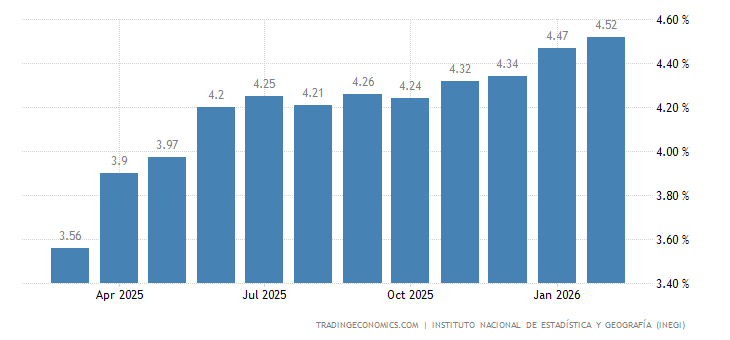

CPI less food and energy in Mexico is +6.5% – at its highest since 2001:

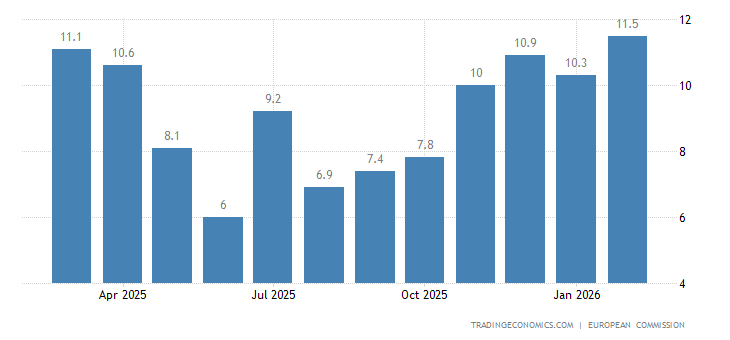

At the same time, expectations of growth in selling prices in the Euro Area are the highest in 37 years of observation:

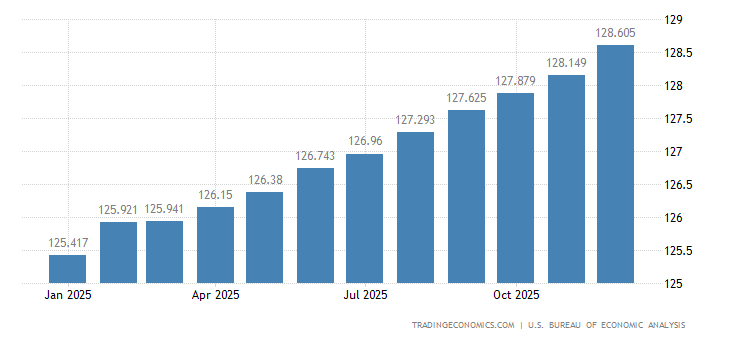

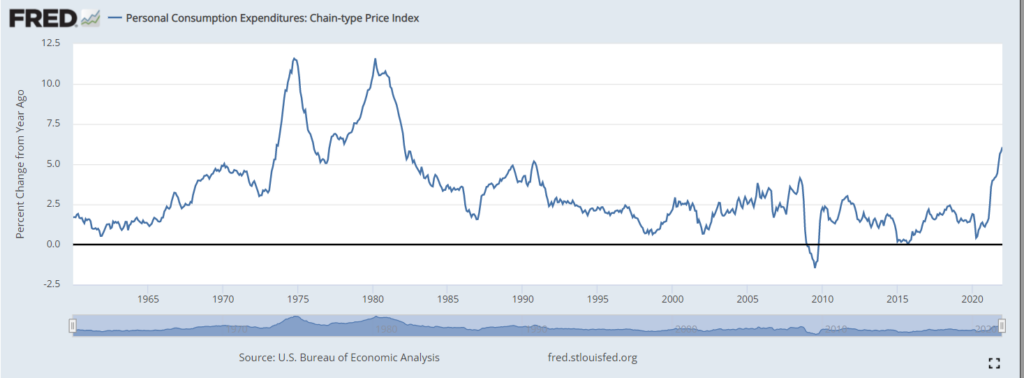

United States Personal Consumption Expenditure Price Index is +6.1% per year, which is the peak since 1982:

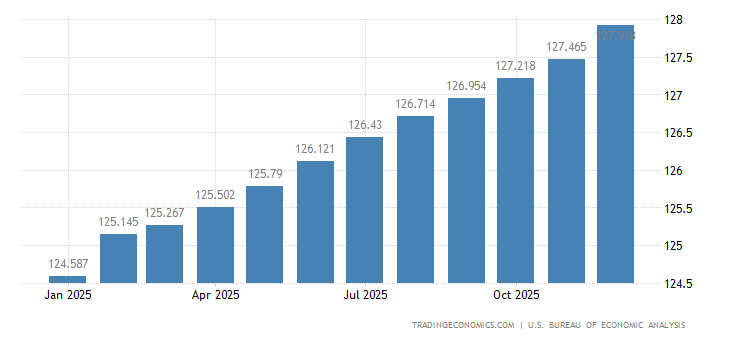

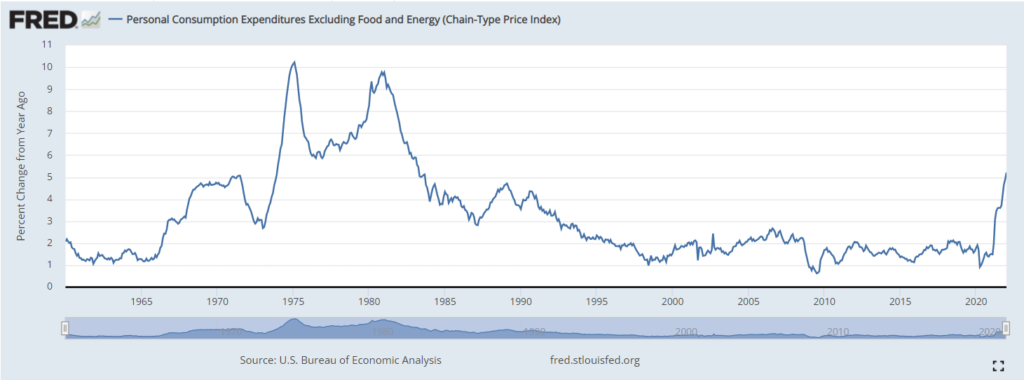

Excluding food and energy is +5.2% – this is the top since 1983:

U.S. home prices are picking up again:

New home sales in the US collapsed amid rising prices:

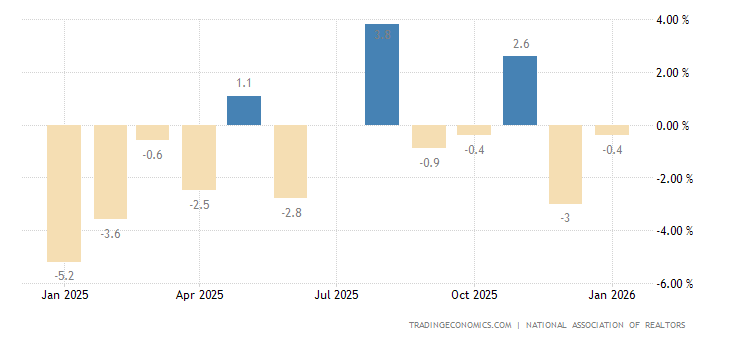

U.S. pending existing home sales -5.7% m/m – 3rd consecutive time in the red zone and 8th time in the last year:

And -9.5% per year, record low since April 2020:

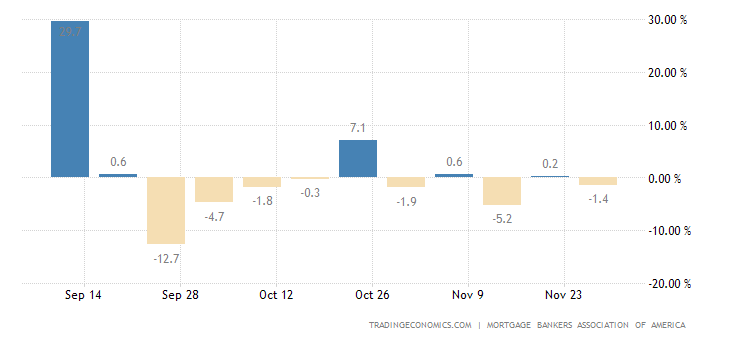

Mortgage applications in the US -13.1% per week, which is the worst performance in 2 years and the lowest number of applications since the end of 2019:

The same is true separately for refinancing, with both indices close to the worst levels of this century:

The reason is the mortgage interest rate, which has been at its highest since July 2019:

Credit to households in the Euro Area has the highest growth rate since 2008 (+4.3% per year):

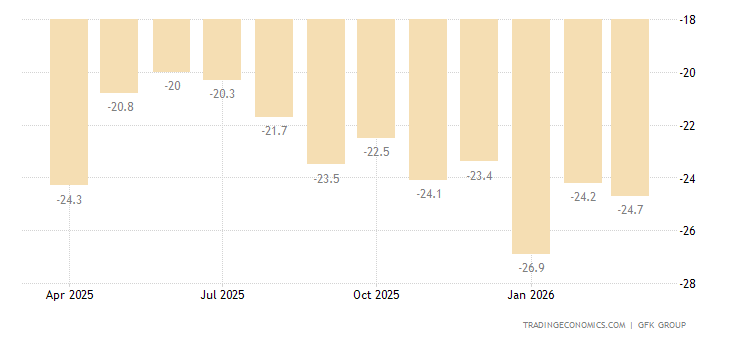

Consumers in Germany are in a grim mood, with the greatest pessimism in 10 months:

The same goes for Italy, in nine months:

Similarly, in the Euro Area – for 11 months:

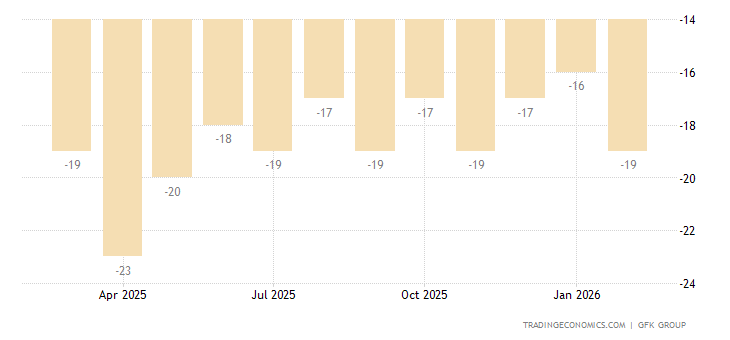

The same is true in Britain, in 13 months:

American consumer sentiment is worst in more than 10 years:

And their inflation expectations remain at their peak since 2008 (+4.9%):

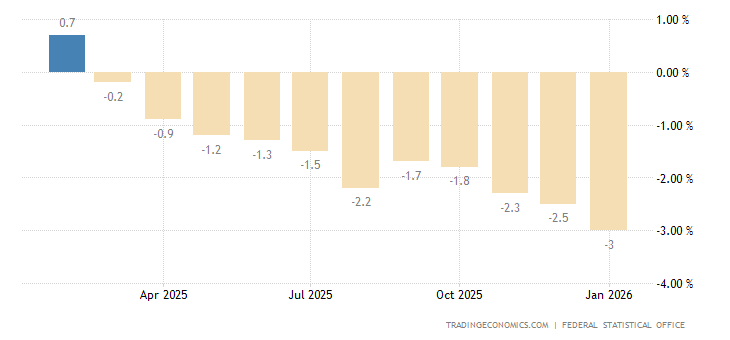

French spending -1.5% per month, which is a six-month low, for the last four months has been only one positive:

The Central Bank of China has not changed monetary policy, the Central Bank of South Korea has left everything the same.

The Central Bank of New Zealand raised the rate by 0.25% to 1.00%.

Summary. Inflationary pressures are increasing and are increasingly affecting household sentiments. More and more often people begin to view any other news (including Ukraine) as attempts by the authorities to evade the question of what and how to improve the situation. At the same time, the authorities themselves do not want to talk about the economy or at least give a minimal description of the future of the situation.

Readers of our reviews see the full picture of the future (though not very pleasant) and in this sense can hope that a better knowledge of the picture of developments will enable them at least to smooth out the consequences of the crisis. But at the very most, they could be among the few winners at its end. In the meantime, it is now almost certain that the structural crisis has entered full force and that its pace is more likely to be accelerated than slowed down.

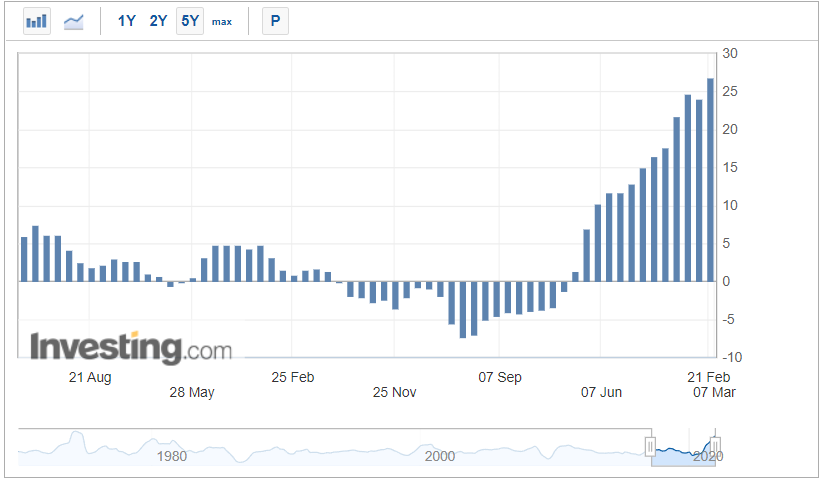

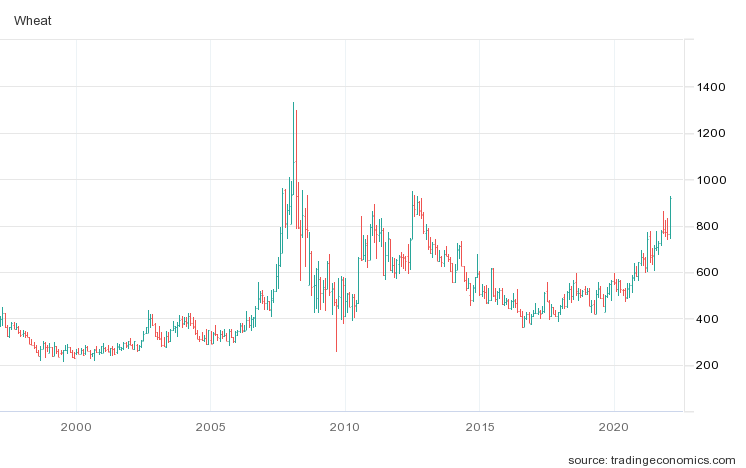

For example, there are two graphs: aluminium prices –

and wheat prices –

They are on the rise, and because of the importance of these products in the economy, one can certainly conclude that they will be visible in all sectors of the world economy in the coming months.

If the US monetary authorities start raising interest rates (which could happen soon enough, the end of February ), the structural inflation factor could become more significant in the coming weeks. Understanding this will take time, but it is likely that by mid-spring, the Fed leadership will realize that raising the stakes does not have the desired effect, and then very interesting events will start, as there is no theoretical justification for this effect in mainstream economic science at present.

We are far from thinking that US Treasury officials will read “Reminiscence about the Future”, most likely, they will initiate theoretical discussions and will imitate the vigorous activity in the field of monetary policy. But it will last until November, when the Democratic Party of the United States will be decisively defeated by the midterm election of the Republican Party, which will control both houses of Congress. After which for the long months everything will be left in the mind in politics, and the economy will fall according to the patterns of the early 30s of the last century, as it is written in Memories of the Future.

And as for Western Europe, they will attempt to repeat the Fed’s policy (with a similar result), in some variations that will depend on political scandals in particular countries. We believe that sanctions activity against Russia will gradually decline (as the EU and Britain deteriorate), but, given the problems of individual countries, the situation will be worse than in the US. Already, inflation in the EU, initially lagging behind the US, has begun to outpace it.

We plan to describe in one of the nearest reviews the approximate development of the situation in more detail and for the time being we wish our readers a successful working week.