September 10-16, 2023

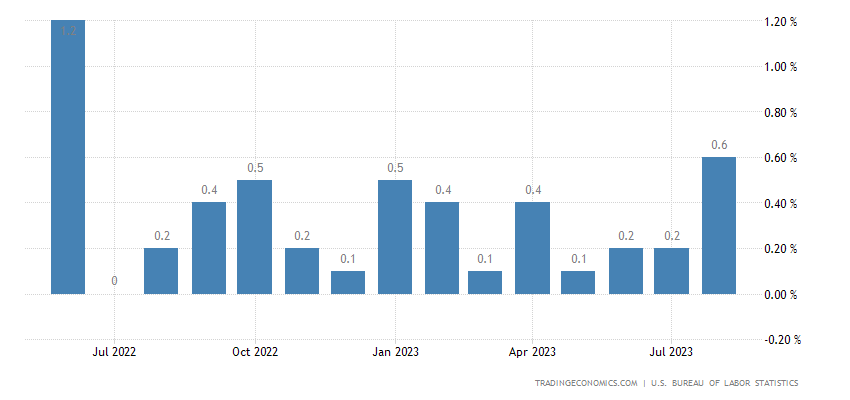

Big news. Inflation growth in the USA. НPowell has been nervous for a reason in recent weeks – the situation is gaining momentum. CPI (consumer inflation index, which is simply called “inflation” in the media) USA +0.6% per month (for August) – 14-month top:

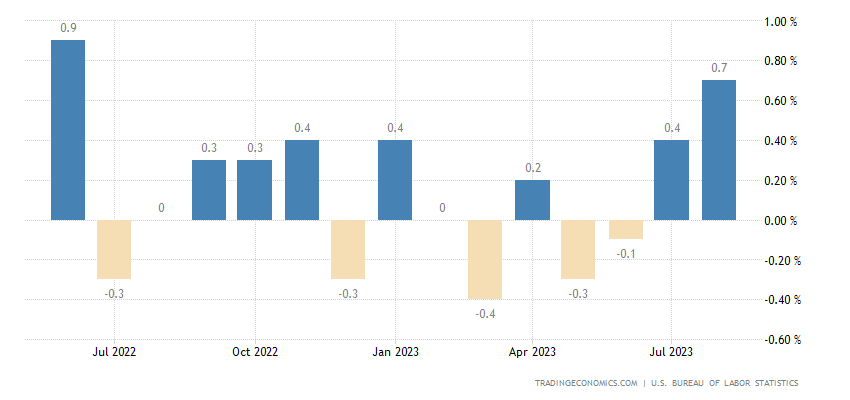

US PPI (industrial inflation index) +0.7% per month – also a 14-month peak:

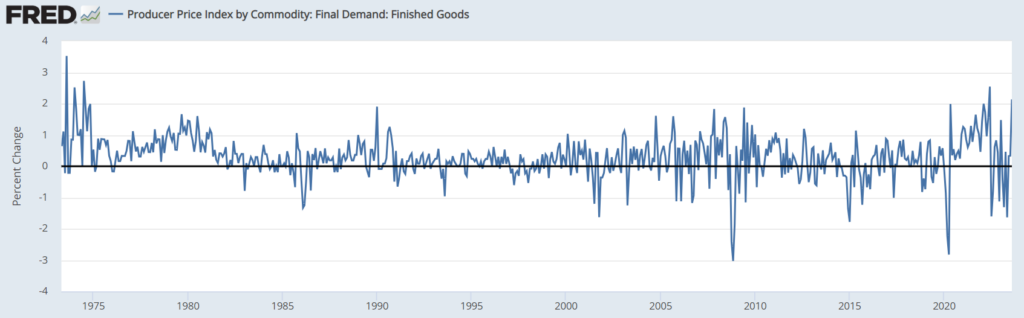

PPI of final goods +2.1% per month – over the past 49 years it was higher only once, in June 2022 (+2.5%):

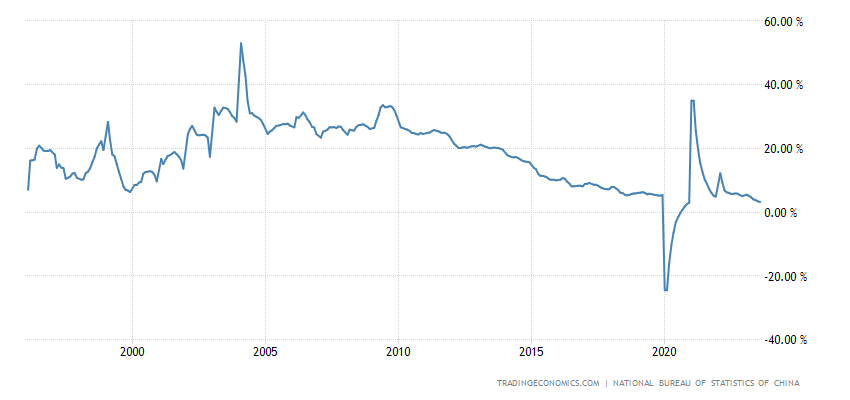

And finally, the price index for the entire list of industrial goods:

Indexes for August – -4.4%. Yes, this is deflation, but less than in July and especially June (it was -9.5%). The fact that deflation continues indicates that there is no growth in industry, and the general economic decline continues (and indirect data confirms this, see the next section). Thus, the rise in prices is not associated with the beginning of growth and is of a different nature.

What are the options? There are two of them. The first is an increase in costs, that is, there is not monetary inflation, but cost inflation. The second option – raising import prices, which allows trade to raise domestic prices. This needs to deal with, but in any case, this does not affect the overall picture in the US economy; rather, it worsens the situation from the point of view of the Fed’s logic. Which we discussed in detail in previous reviews.

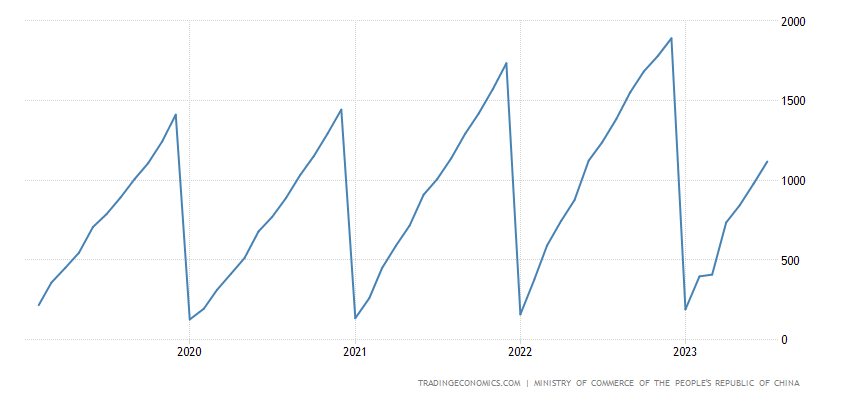

Macroeconomics. Chinese indexes for August differ.

Investments in fixed assets +3.2% per year – not counting the failure of 2020, this is a record low:

Pic. 5

And foreign direct investment -5.1% per year is the weakest dynamics in 3.5 years:

Pic. 6

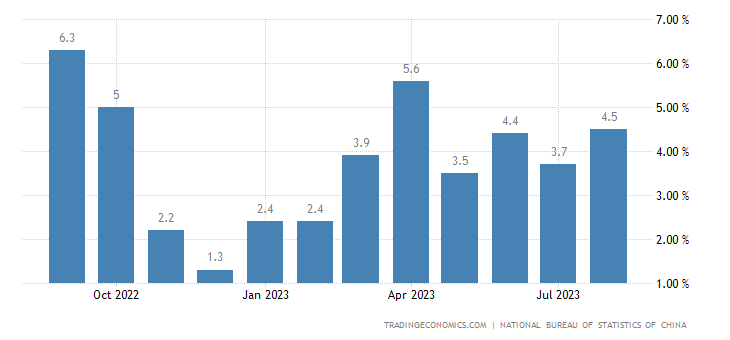

At the same time, industrial production accelerated to +4.5% per year –

Pic. 7

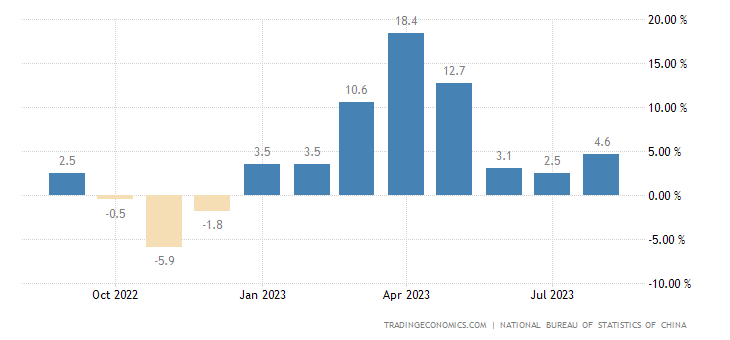

And retail – up to +4.6% per year:

Pic. 8

And the question immediately arises: maybe this positive is simply the result of underestimating inflation?

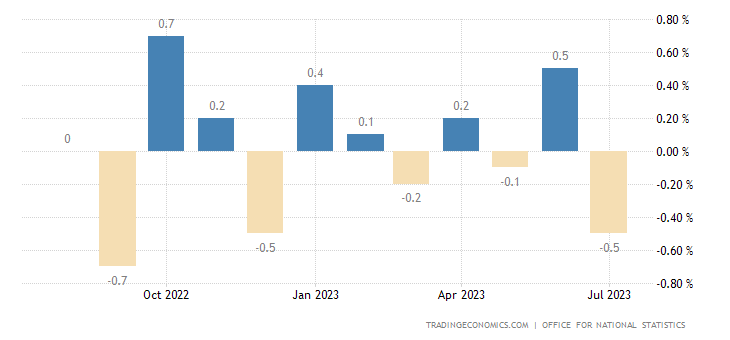

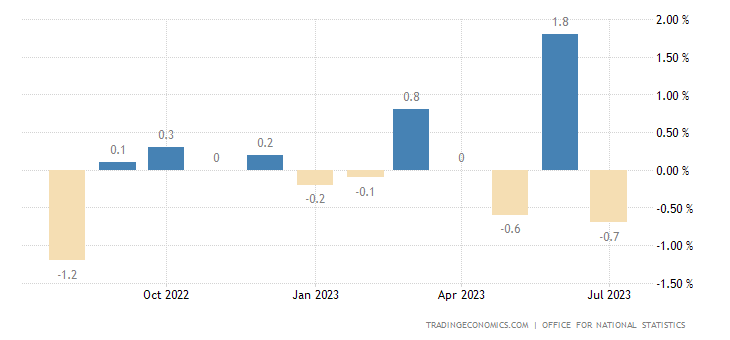

In July, UK GDP was -0.5% per month – the worst dynamics in 10 months:

Pic. 9

And output in its industry is -0.7% per month – an 11-month minimum:

Pic. 10

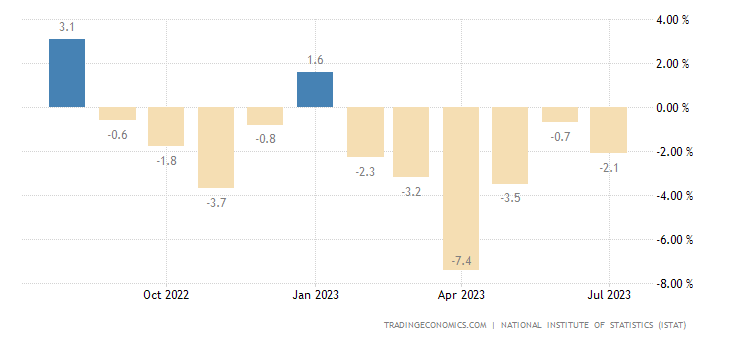

Industrial production in Italy -2.1% per year – the 6th minus in a row and the 10th in the last 11 months:

Pic. 11

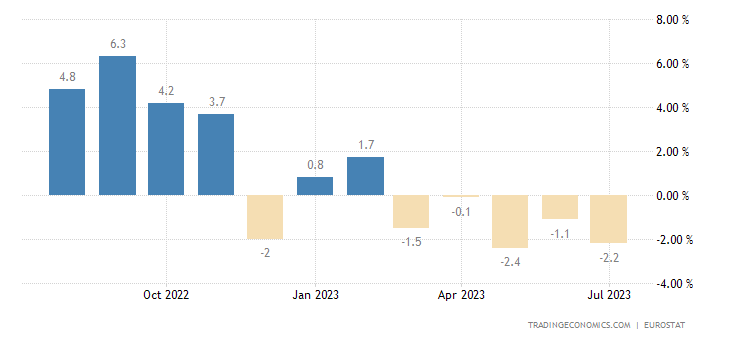

In the eurozone as a whole, -2.2% per year – the 5th minus in a row:

Pic. 12

Very correlated with data on German industrial orders from the previous review. So an industrial collapse has fully formed in the European Union.

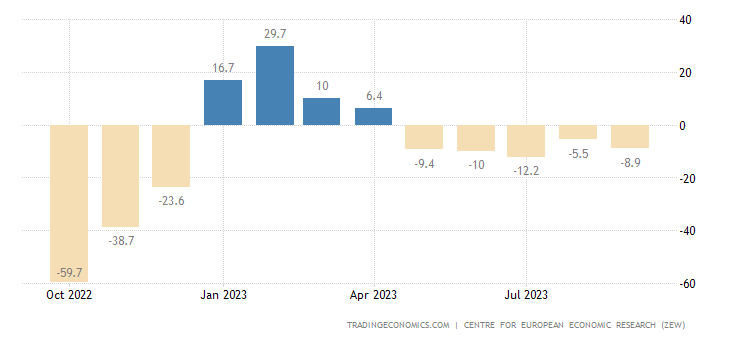

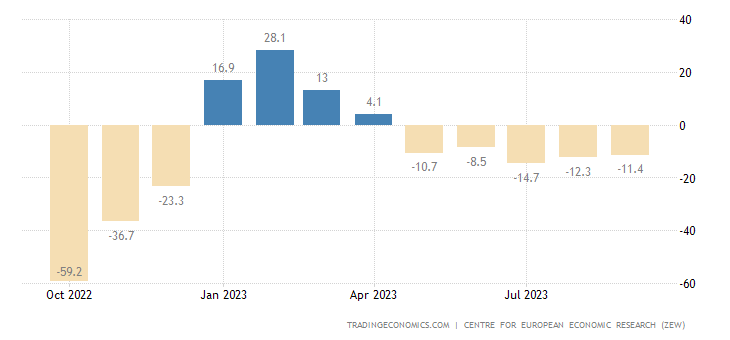

Accordingly, the index of economic sentiment in the eurozone (ZEW survey) has been in the negative for 5 months in a row:

Pic. 13

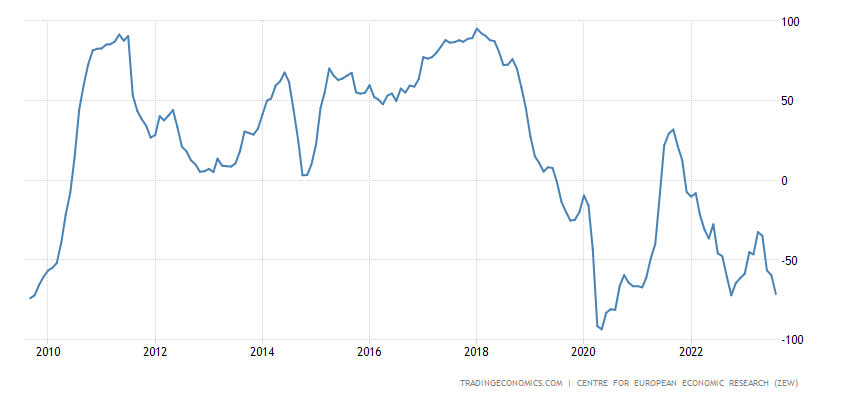

As well as separately in Germany:

Pic. 14

The latter has a very poor assessment of its current state – without taking into account 2020, it has been at the bottom since 2009:

Pic. 15

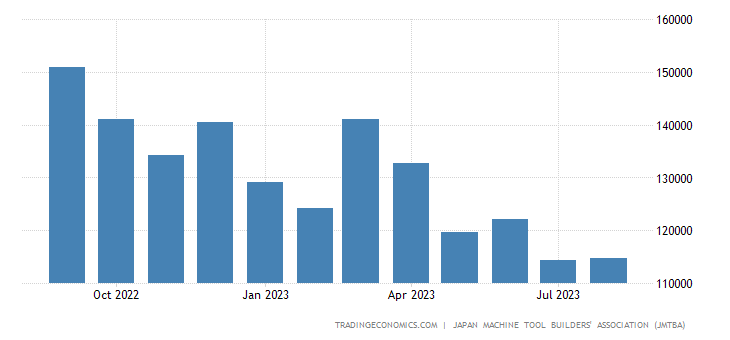

Orders for machines and equipment in Japan -17.6% per year:

Pic. 16

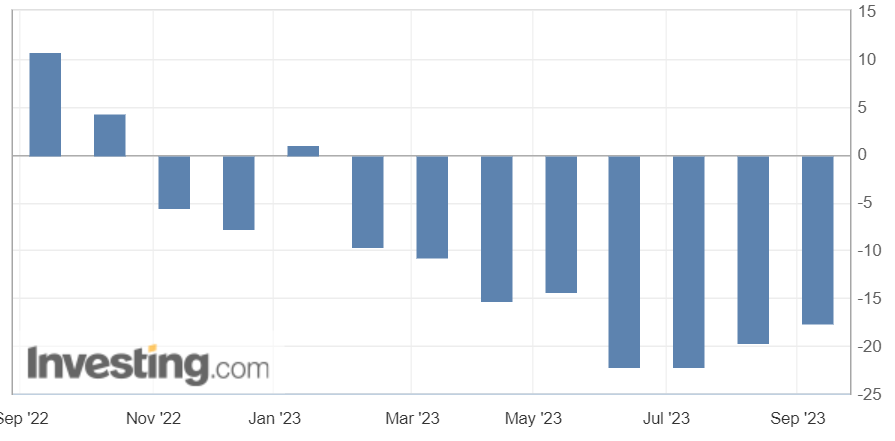

8th minus in a row and 10th in the last 11 months:

Pic. 17

Net engineering orders in Japan -13.0% per year – 3-year minimum:

Pic. 18

And here the situation is similar to the EU.

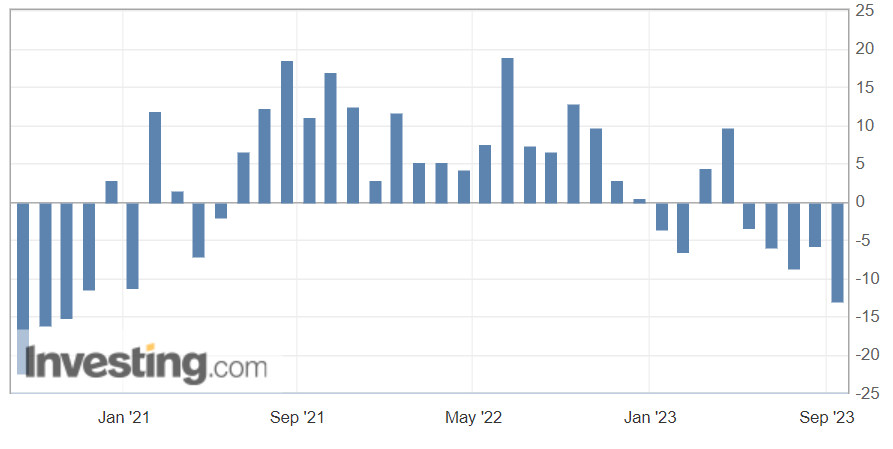

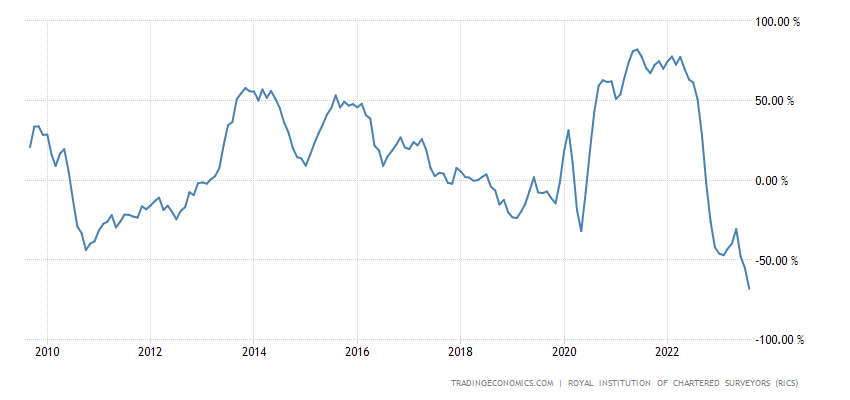

The balance of house prices in Britain -68% is the minimum since 2009:

Pic. 19

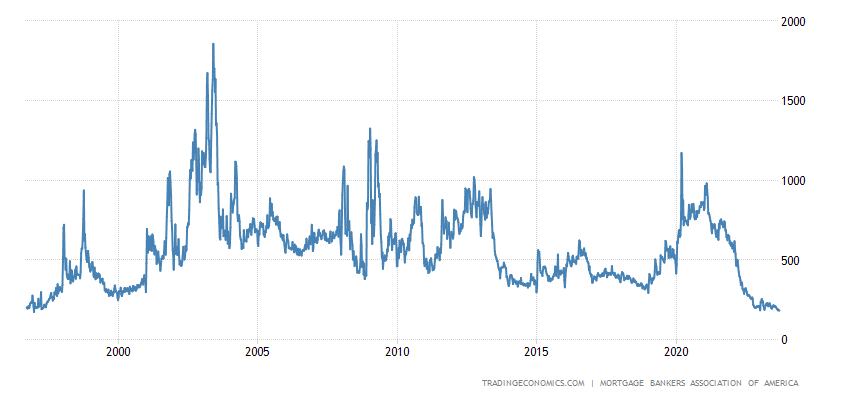

US mortgage rates hover near 23-year high:

Pic. 20

Why lending hit a 27-year low:

Pic. 21

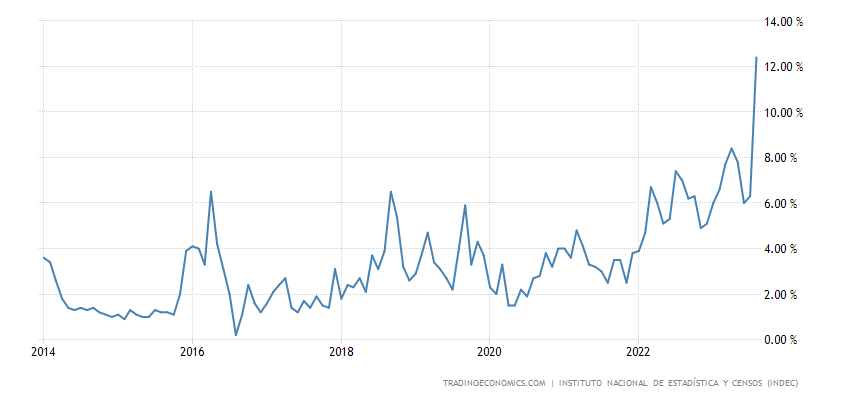

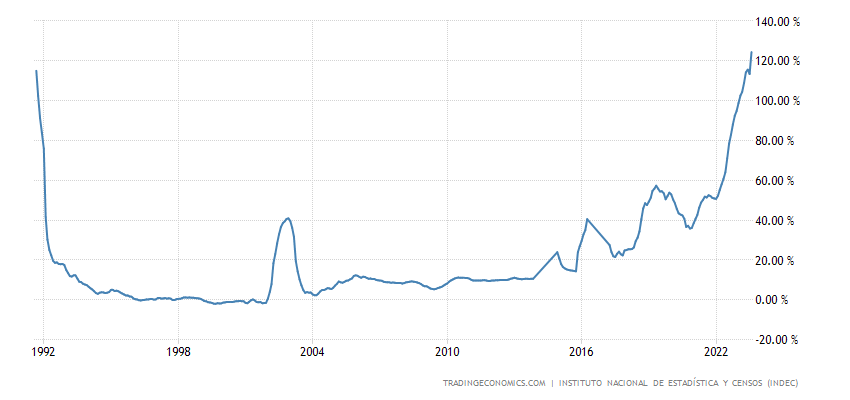

Argentina CPI +12.4% per month – a record high:

Pic. 22

And +124.4% per year – 32-year top:

Pic. 23

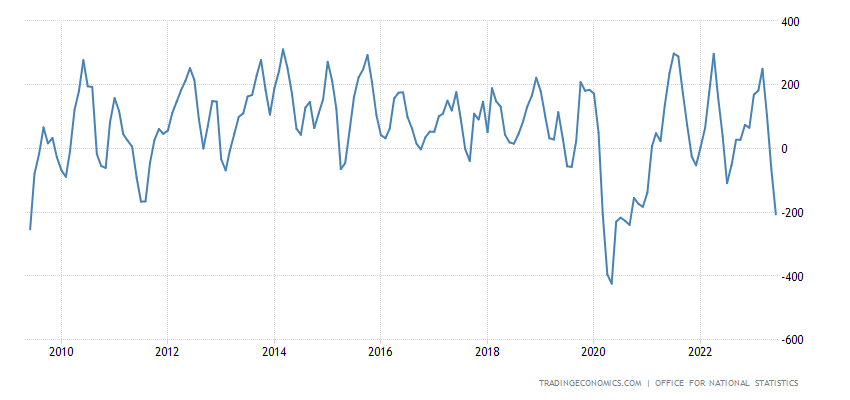

Employment in Britain in May-July -207 thousand – not counting the failure of 2020, the worst figure since 2009:

Pic. 24

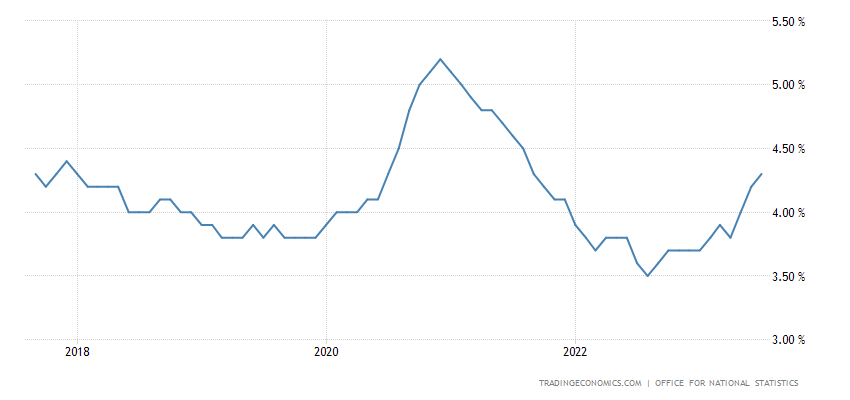

Why the unemployment rate rose to its highest level since 2017 (again, excluding 2020):

Pic. 25

The ECB raised rates by 0.25% to a 22-year high of 4.50%. At the same time, the interest rate on deposits reached a record high of 4.00%.

China’s central bank cut the reserve ratio for large banks by 0.25% to a 16-year low of 10.50%. This, of course, is not a rate, but also a completely effective method of easing monetary policy. Which is indirect evidence that problems in the Chinese economy continue.

Main conclusions. Apparently, it will not be possible to find a clear reason for the increase in costs in the US economy. This is, in general, a normal situation during a structural crisis, when during a decrease in demand and a simplification of the structure of the economy (and the second automatically follows from the first), various types of costs begin to rise. And this process will continue as long as the structural crisis continues.

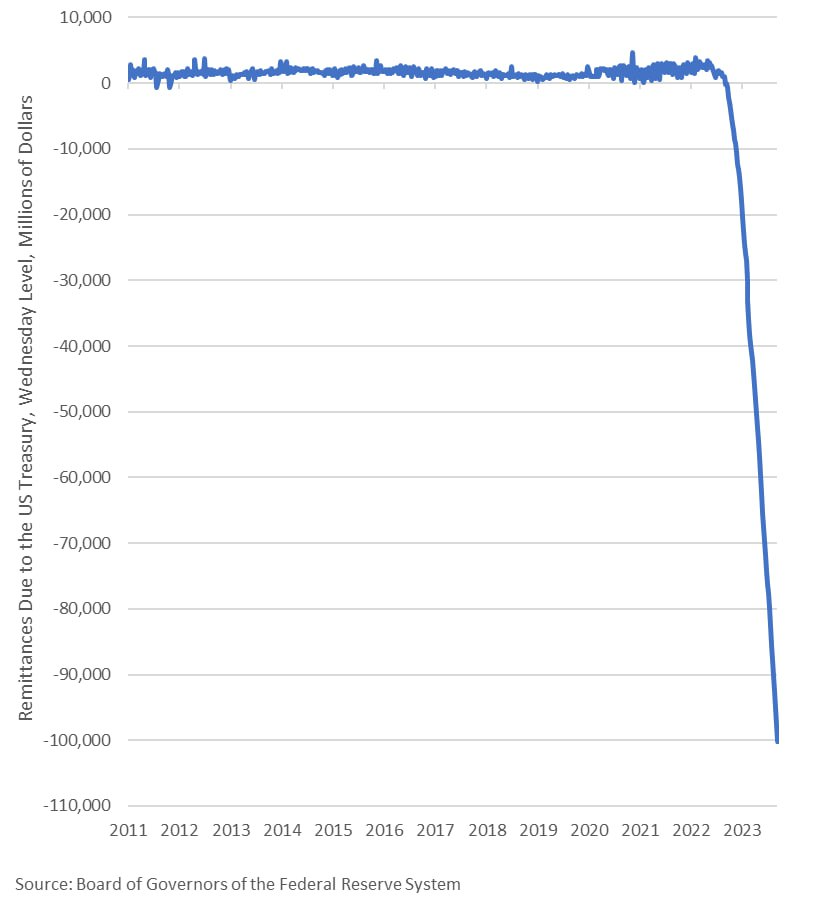

Indirect indicators clearly show a change in the structure of the economy. They, of course, say nothing about how it changes, but, for example, you can consider this indicator:

This is what the Fed loses by paying interest to commercial banks on reverse repos and interest on reserves. Losses just reached $100 billion, or $758 million per day.

Before all these crazy games with interest and money pumping began, the Fed sent its profits to the US Treasury every year. But now the Fed has huge paper losses on its bond portfolio and huge daily losses on the money it must pay to commercial banks to keep the system from collapsing.

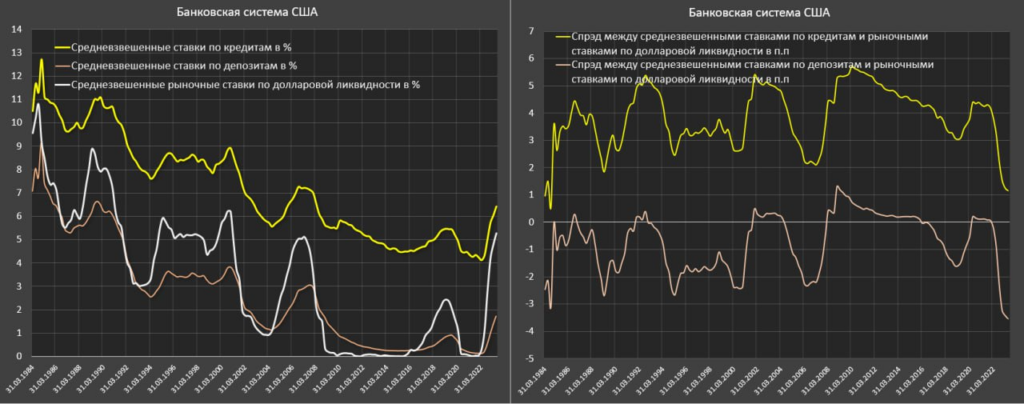

Another picture, the weighted average cost of funding for the US banking system:

As you can see, it is growing. Before the cycle of tightening monetary policy from the Federal Reserve in March 2022, the weighted average rates on attracted deposits were only 0.12% per annum, in the Q2 of 2022 – 0.19%, then 0.52%, 0.95%, 1.36% at the beginning of 2023 and 1.72% in the 2nd quarter 2023, which is the highest funding cost since Q3 2008!

These are not rates on new/opened deposits, but the weighted average yield for the entire volume of deposits of any maturity, including interest-free. As deposits are refinanced on new terms, profitability gradually increases.

The weighted average rates on loans are 6.43% for all types and types of loans to legal entities and individuals (including mortgage loans), and a year earlier the rates were 4.33%.

As can be seen, weighted average loan rates grew faster than deposit rates, which led to a significant increase in banks’ interest margins from 4-4.2%, which was observed before the monetary policy tightening cycle, to 4.7-4.8% in mid-2023 (maximum margin since Q3 2012). But this is a temporary effect. Record outflows of deposits from the banking system and the depletion of cash positions relative to risk-weighted assets have intensified competition among banks for a deposit base that is still significantly cheaper than market funding, costing over 5.2%.

Weighted average rates on the deposit base will continue to grow actively at a rate of 0.35-0.4 percentage points per quarter, i.e. may rise to 2.5% in Q4 2023. The spread between weighted average deposit rates and market rates on dollar liquidity is a record negative (3.55 p.p.), which is 1 p.p. higher than the norm in the phase of rapid tightening of monetary policy.

Loan rates, on the contrary, will slow down due to a decrease in demand for loans, which intensifies competition between banks for borrowers, so the net margin of banks will begin to decline rapidly from 3Q 2023.

At the same time, overdue loans will begin to accelerate, as a natural reaction of the system to the extreme cost of borrowing, which will lead to the accumulation of costs for loan write-offs. This, in fact, is a description of one of the mechanisms for increasing costs for the real sector of the economy.

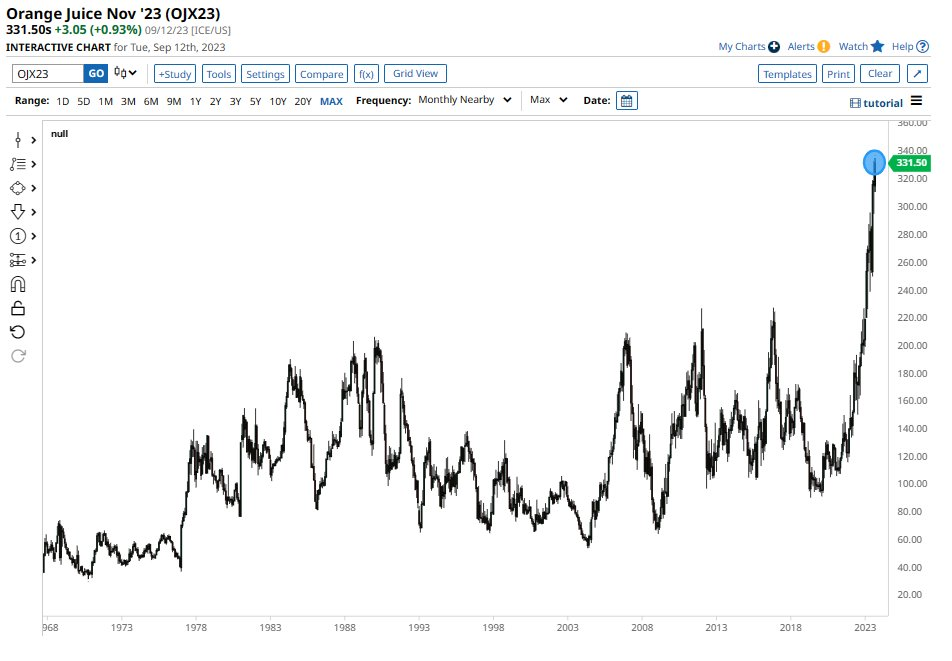

Of course, in such situations it is a very convenient time for speculators, as shown, for example, by the prices of orange juice:

To sum up, general anxiety in the global economy is growing, but I hope that our readers are doing well, so we can wish them a pleasant weekend and a relaxing work week!