June, 17-26 июня 2023

Big news. A sharp increase in the rate by the central bank of Turkey, by 6.5% percent, to 15.0%. Moreover, he tends to raise it further. The reaction of the Turkish lira is corresponding:

Why is it so important? But the fact is that in the late 70s, when there was high inflation in the United States, the then head of the Fed, the recently deceased Paul Volcker, raised the rate right up to 20% – because he understood that it was impossible to cope with inflation otherwise. As we can see, the reaction of the current leadership of the Fed is completely different.

Yes, debt has accumulated since then, primarily households. The average household debt in the US has roughly doubled relative to real disposable income, from 60% to over 100% (at its peak, in 2008, it was over 130%). And this, in the conditions of the growth of the rate, has an extremely negative effect on aggregate demand. Namely, it basically forms the FFP of the country.

But if you want to stimulate demand, then in order for this to have an effect, demand must be supported for domestic products. Then, in the 70s, the question did not arise at all, there were practically no non-American products on the US markets. But today, the actual US monetary authorities are stimulating demand for Chinese products … There is no economic sense in this at all.

In other words, the leadership of the US monetary authorities needs to decide. Or spit on inflation, lower the rate and start supporting demand by sharply raising import tariffs and stimulating domestic production. Or – forget about GDP and incomes of the population, recognize the inevitability of a sharp decline in living standards, raise the rate to 12-15% and put pressure on inflation. True, this will have to be done in an election year …

The importance of the decision of the Central Bank of Turkey is that before that the major economies of the world followed the decisions of the US Federal Reserve. Accordingly, no one raised the stakes especially (Argentina does not count, its monetary policy has been nothing but surprise to anyone for many decades). And then a decision was made that had nothing to do with American politics. This can be an example for everyone, even for the leadership of the Fed. In general, this is a serious event.

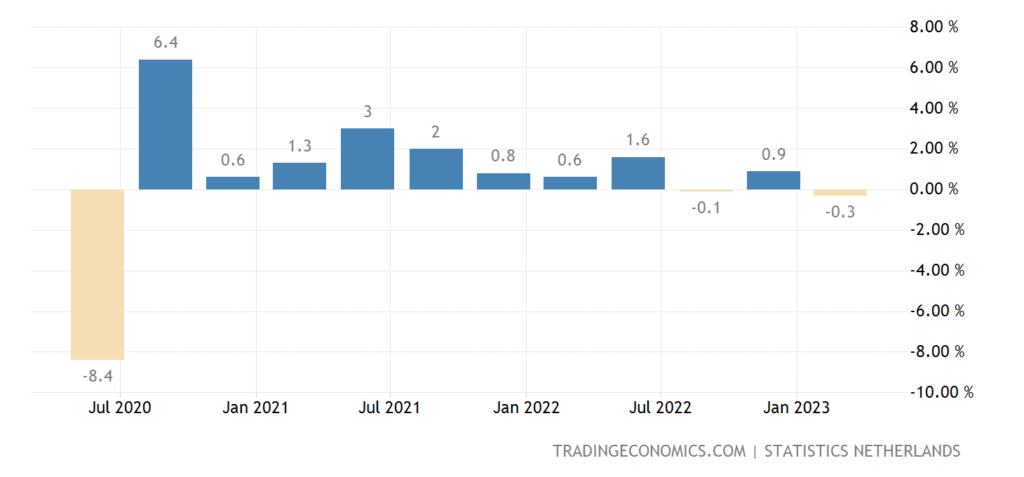

Macroeconomics. Dutch GDP -0.3% per quarter:

Pic. 2

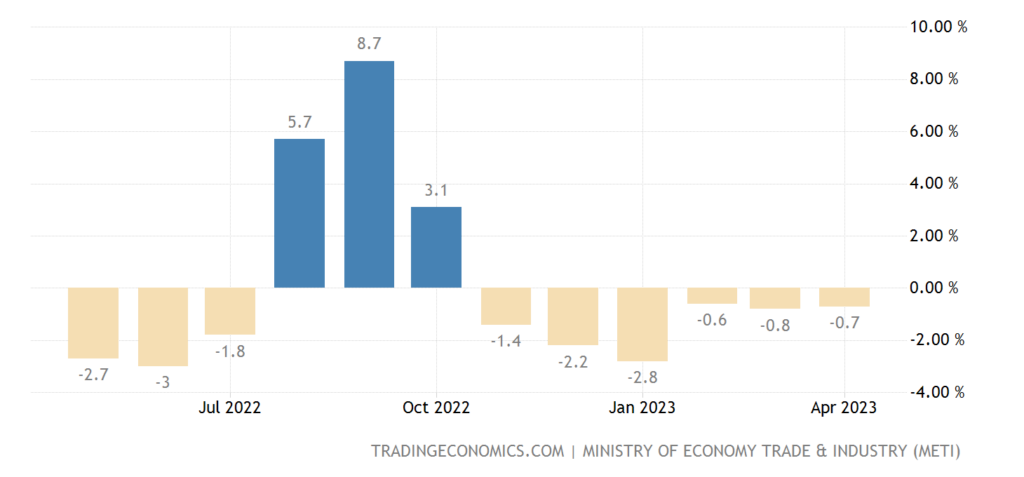

Industrial production in Japan -0.7% per year – 6th monthly loss in a row:

Pic. 3

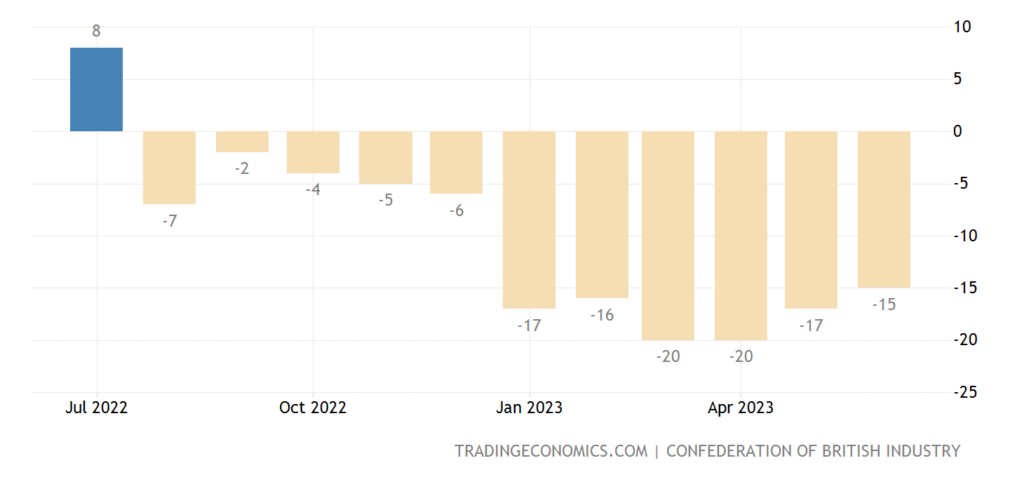

The balance of industrial orders in Britain keeps in the red for 11 months in a row:

Pic. 4

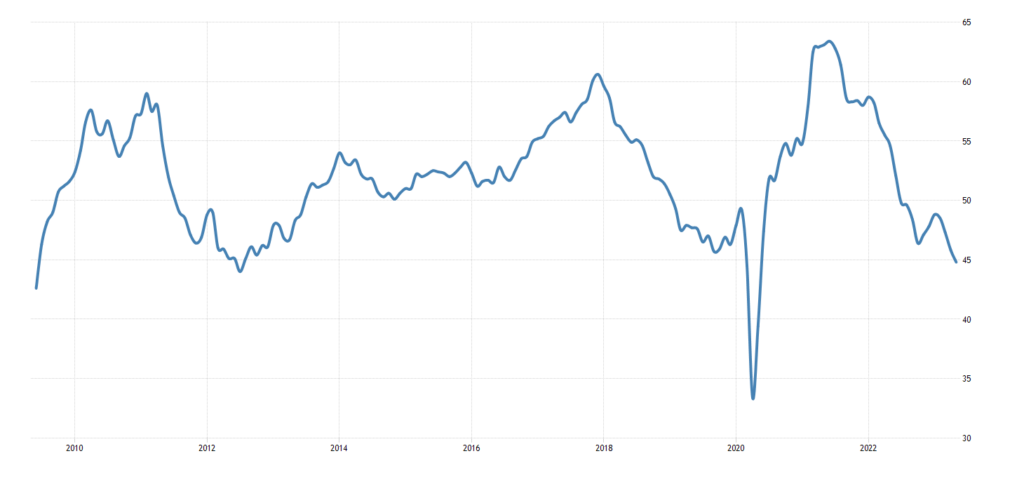

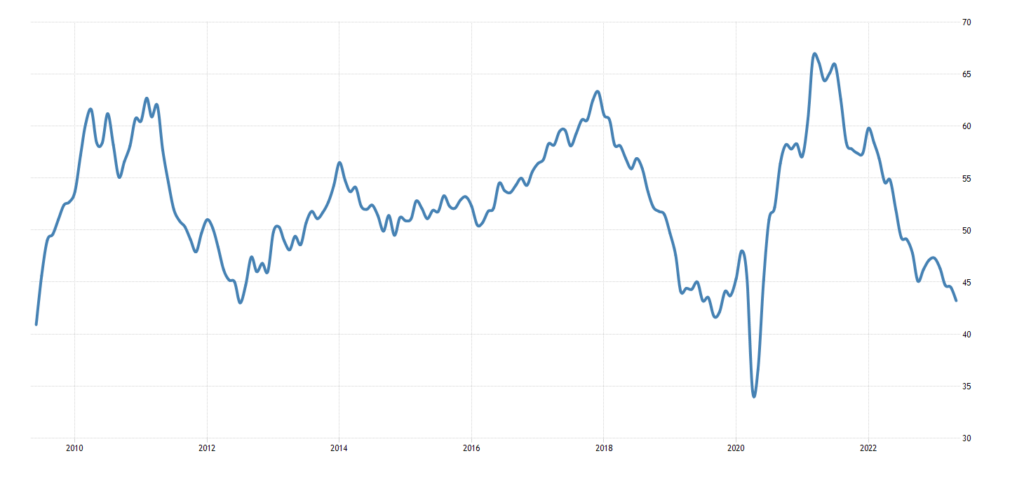

PMI (expert index of the state of the industry; its value below 50 means stagnation and recession) of the eurozone industry of 43.6 is a 3-year low, and without taking into account the failure of 2020, even a 14-year one:

Pic. 5

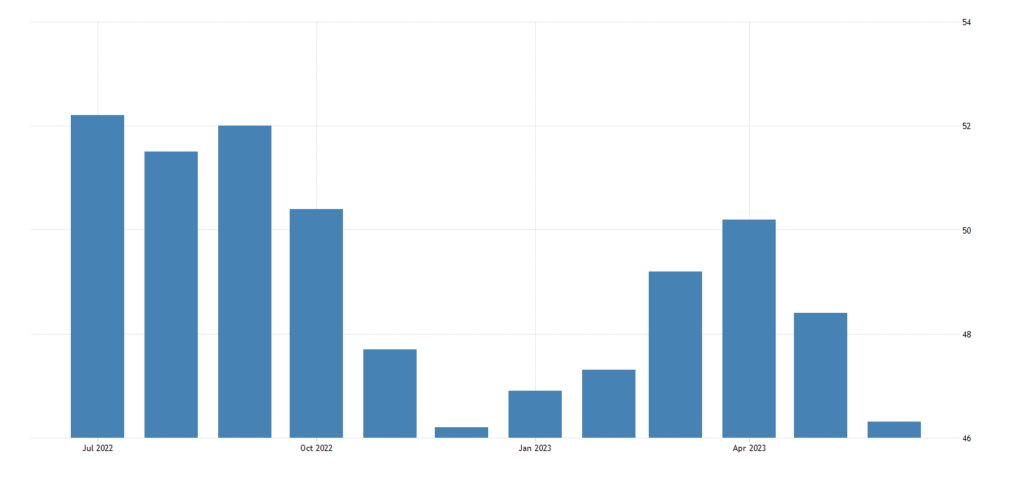

Mainly thanks to Germany, where the picture is the same, but the value is even worse (41.0):

Pic. 6

A similar situation is in the US, where PMI (46.3) just 0.1 did not reach the December low:

Pic. 7

Against the background of these indicators, the legends that “something is being restored there” cause nothing but sincere surprise.

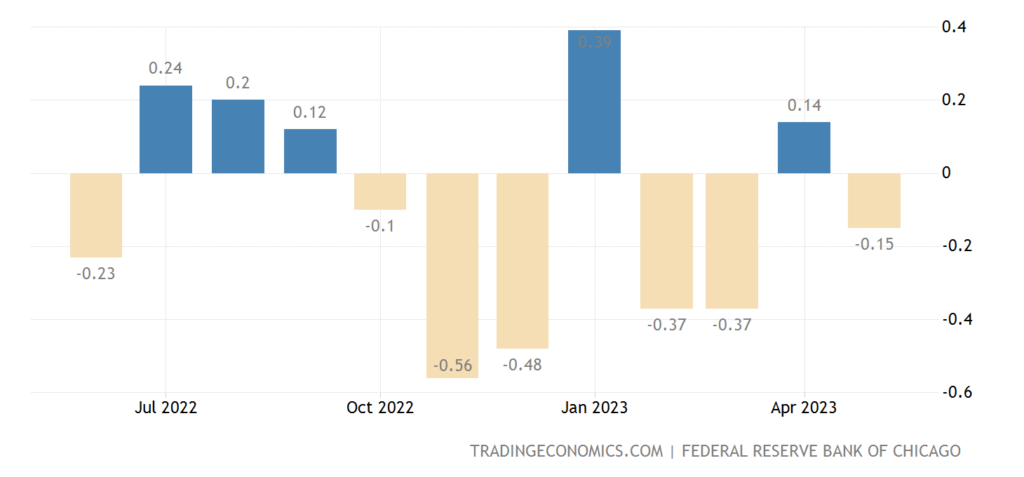

The National Activity Index in the US from the Chicago Fed is back in the red:

Pic. 8

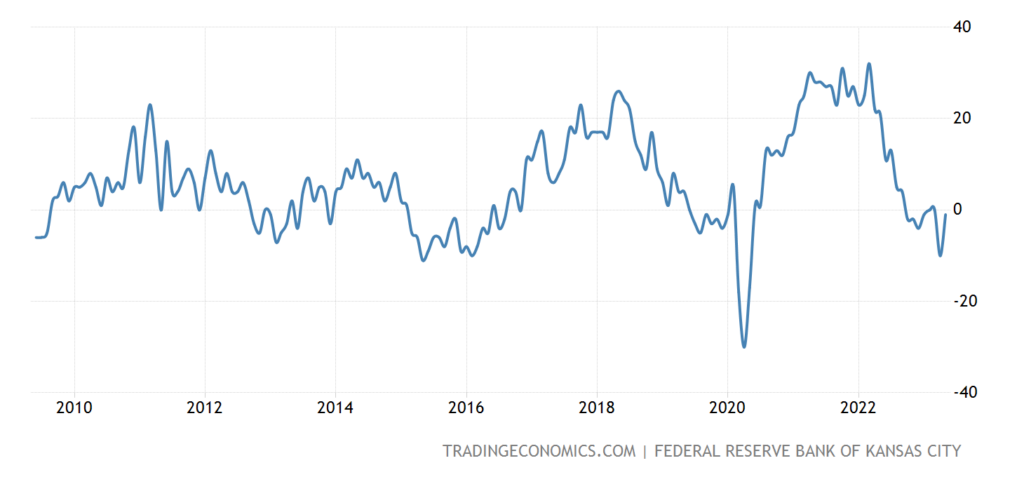

The composite (across all industries) index of the Kansas Fed, with the exception of the failure of 2020, is at the bottom since 2009:

Pic. 9

Leading indicators in the US fall on a monthly basis for 14 months in a row:

Pic. 10

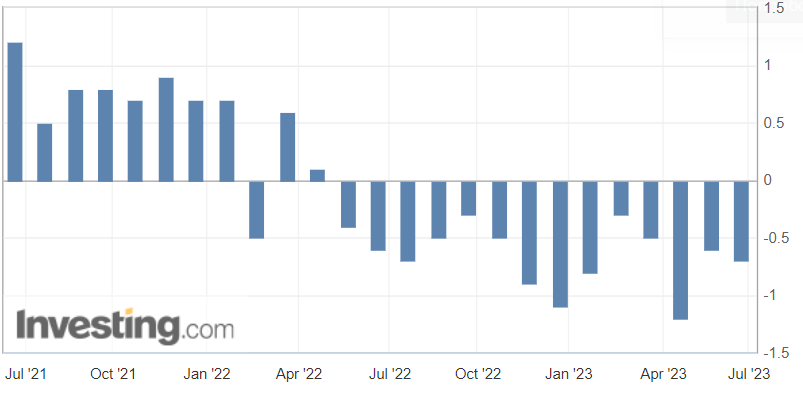

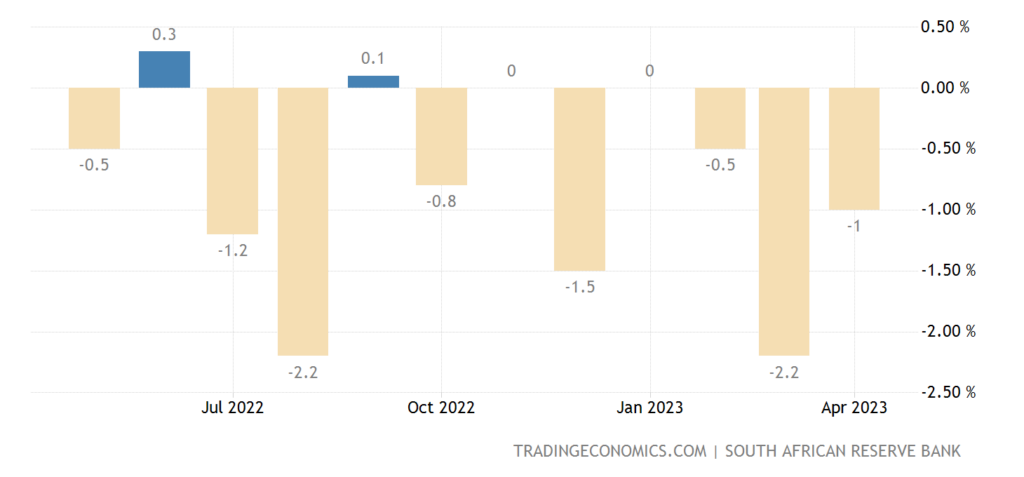

Leading indicators of the business cycle in South Africa -1.0% m/m – 5th negative in a row:

Pic. 11

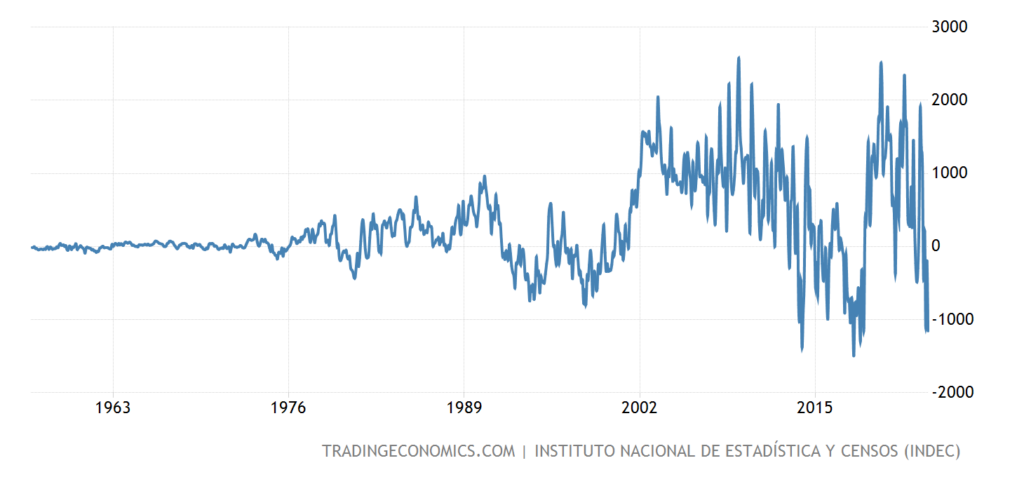

Argentina’s trade deficit is at its highest in 5 years and close to a record:

Pic. 12

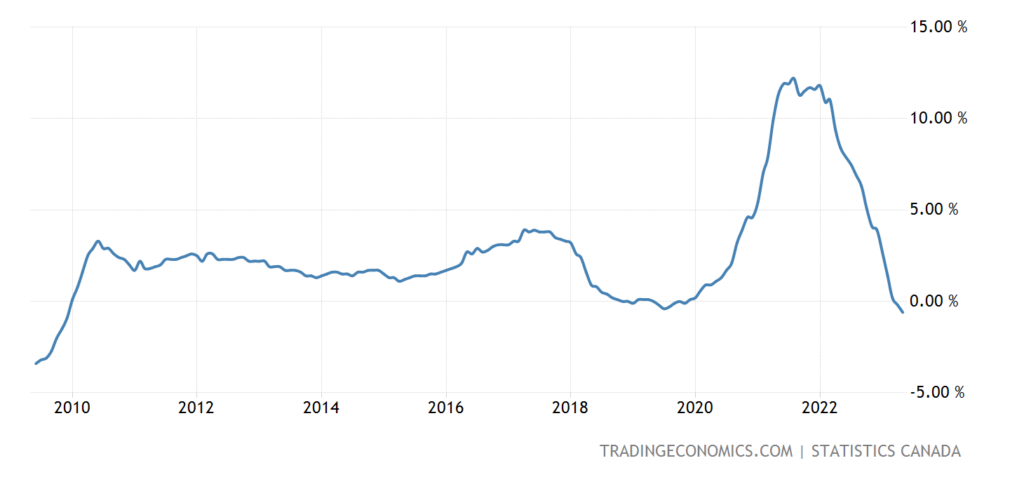

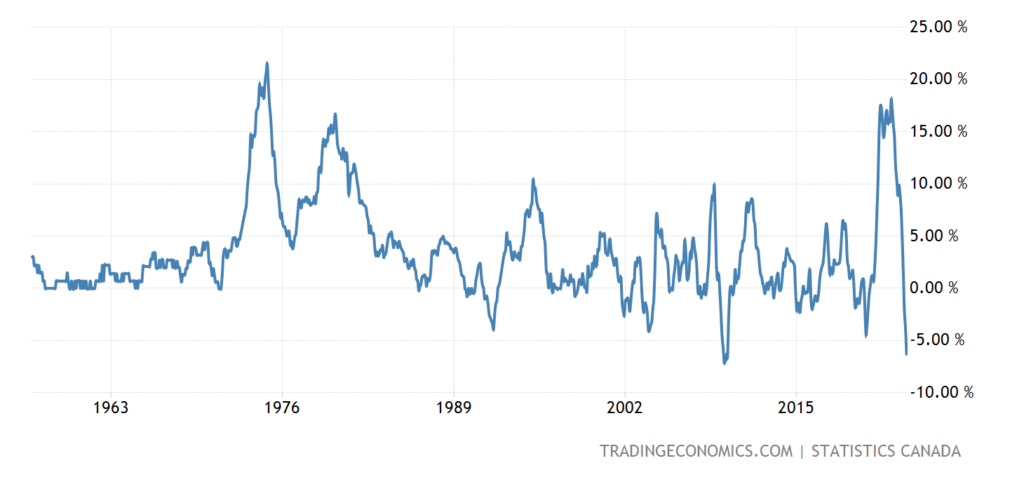

Prices of new buildings in Canada -0.6% per year – at least since 2009:

Pic. 13

Britain’s net (excluding highly volatile food and fuel components) CPI (Consumer Inflation Index) suddenly accelerated to a record high:

Pic. 14

As in Japan – CPI without food and fuel + 4.3% per year – the top since 1981:

Pic. 15

PPI (Industrial Inflation Index) Canada -6.3% per year – for 66.5 years of observations, it was lower only during a few months of 2009:

Pic. 16

Classical deflation, a typical indicator of a serious recession.

U.S. Initial Jobless Claims Highest in 20 Months:

Pic. 17

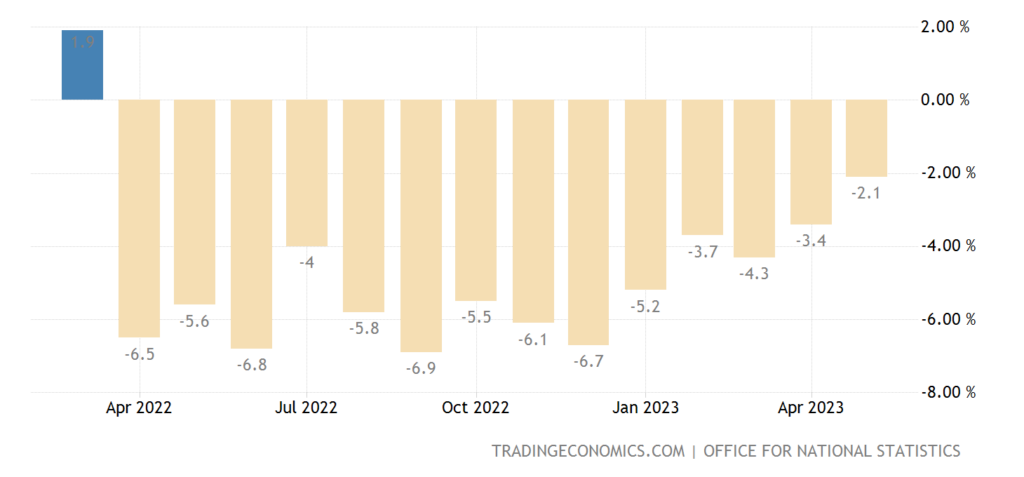

Retail sales in the UK -2.1% per year – the 14th consecutive minus:

Pic. 18

The Central Bank of China lowered key rates by 0.10%: on annual loans – up to 3.55%, on 5-year loans – up to 4.20%; both are record lows.

The Central Bank of Brazil left rates in place. So did the Central Bank of Mexico and the Central Bank of Indonesia.

The Central Bank of Switzerland raised the rate by 0.25% to 1.75%, ready for further tightening.

The Bank of England raised the rate by 0.5% to 5.0% – a more modest increase was expected. Fed chief Powell made it clear that further rate hikes are likely.

Main conclusions.

Powell spoke again this week, but he did not say anything new, except for assurances that he was ready to raise the rate. In the first section, we explained why, in reality, his policies are a palliative that cannot have an effect. We have expressed our opinion on this issue many times and it is that a serious decline in GDP and the standard of living of the population in the United States cannot be avoided, and therefore we need to think about how to make the reindustrialization process profitable. Whether the leaders of the US monetary authorities will reach this idea, we do not know, but there are doubts that this is possible with their current composition.

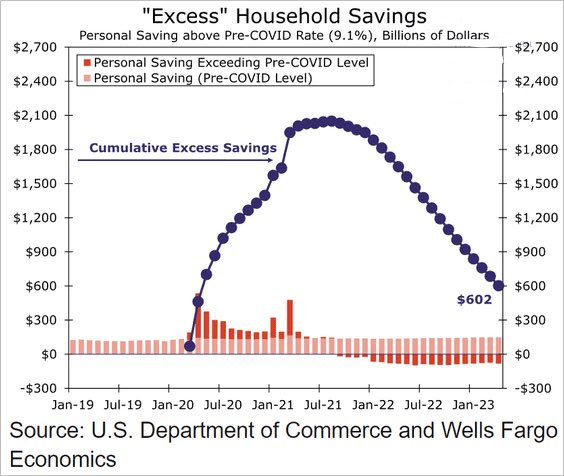

At the same time, what Powell is afraid of can be understood. Well, for example, the excess (created in 2020) savings of the population are melting and will soon come to an end:

However, they play an important role in the current demand:

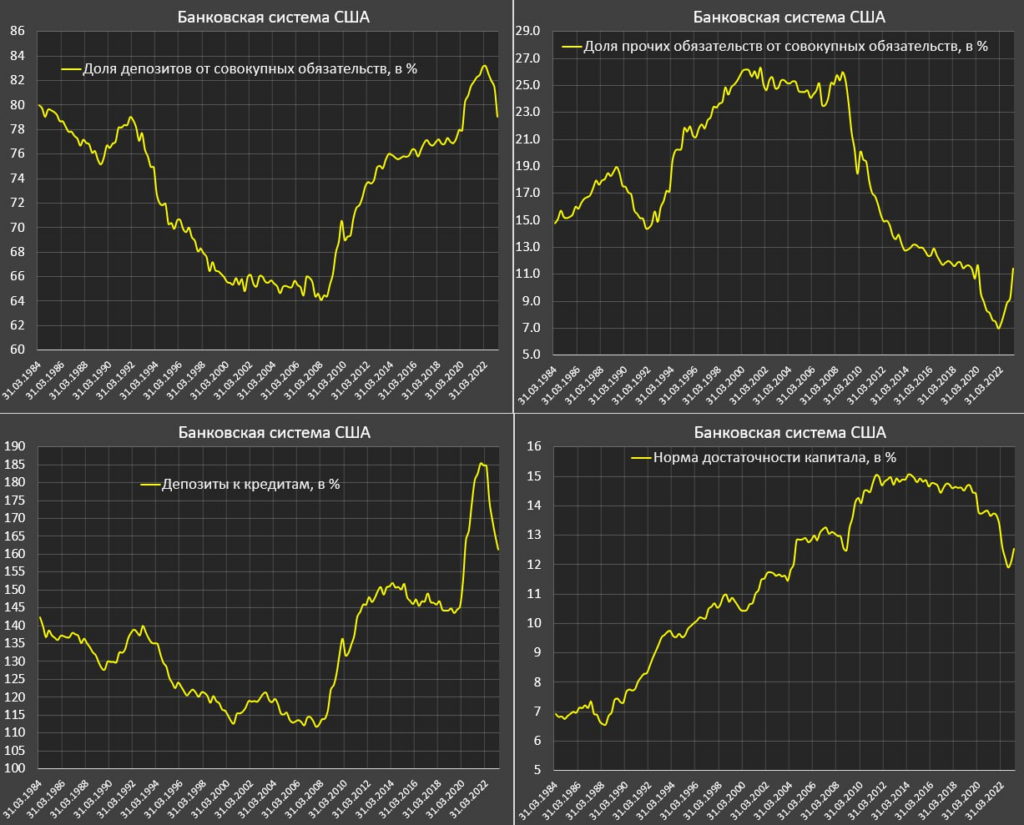

Serious problems in the banking sector:

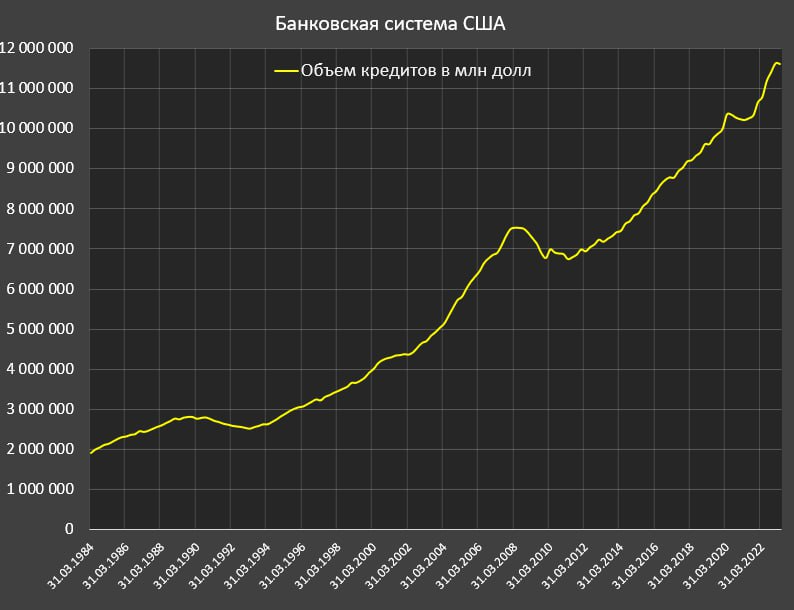

At the same time, banks continue to increase the volume of loans:

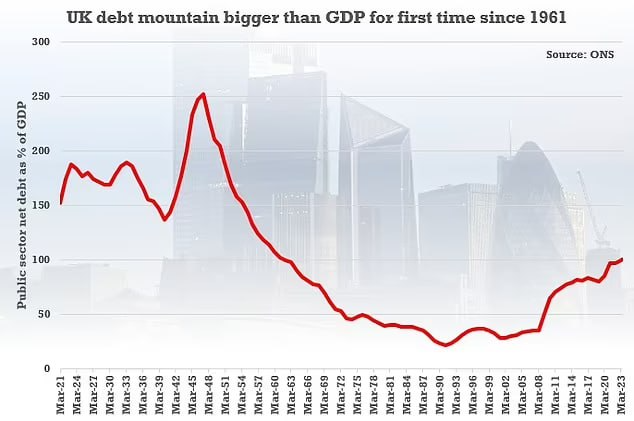

Debts are growing not only in the US, in the UK they have exceeded 100% of GDP for the first time in peacetime:

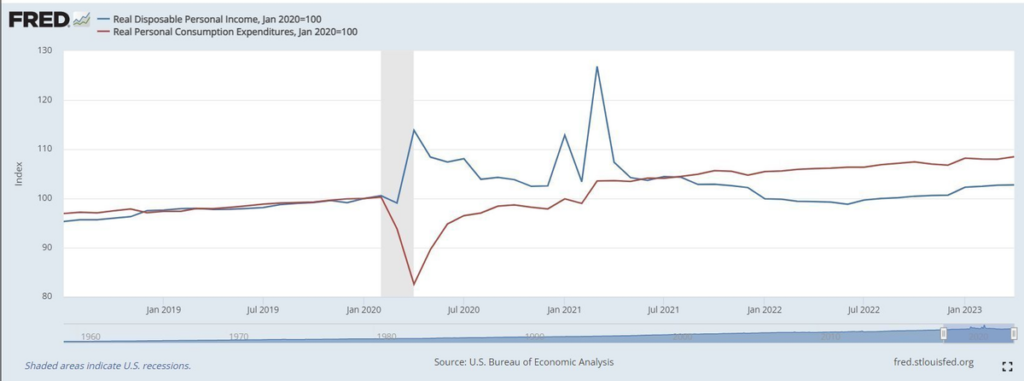

I specifically do not comment on the graphs – in this case they simply illustrate the processes, their complex internal explanation does not make much sense.

In general, it can be noted that against the background of the ongoing structural crisis, which is not even interesting to comment on, the macroeconomic picture has not changed for many months, the only tool to maintain the situation is emission. Either monetary (from the side of central banks), or credit. Which makes it increasingly dangerous to tighten monetary policy, as it could cause a collapse in defaults, both private and corporate.

With the corresponding collapse of the financial markets. Of course, it is quite difficult to determine this moment based on macroeconomic data alone (although in 2008 it almost succeeded, the collapse occurred three months before the US completely zeroed the rate), but the general trend, apparently, can no longer change. It remains to develop compensatory measures and not to panic, for which it is good to relax on weekends and work calmly on weekdays!