Time Period: 31 July – 6 August 2021

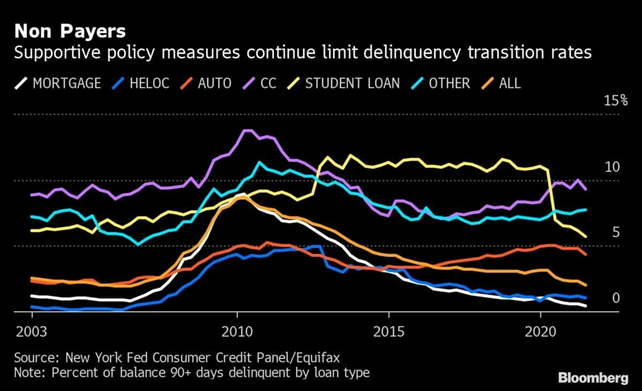

Top news story. Mortgage “boom” has led to the biggest increase of household debt since 2013. Household liabilities rose by 313 billion to 14.96 trillion in the second quarter. According to the Federal Reserve Bank of New York, that’s 2.1% more than in the second quarter. Mortgages contributed most to the increase in debt.

It should be noted that since 2008 total household debt has declined on average, although it is well above historical values, which before the start of «Reaganomics» did not exceed 60% of real disposable income. By the autumn of 2008, it was over 130%, falling just below 100% by 2020.

A return to debt growth means that tightening credit policy (i.e. increasing borrowing costs) inevitably means massive bankruptcies of households. This means that, in a debt economy, aggregate demand in the US economy will fall sharply.

Macroeconomics

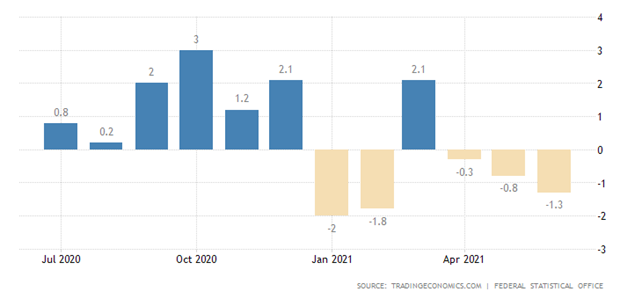

Industrial production in Germany has fallen for 3 consecutive months and 5 months out of the last 6:

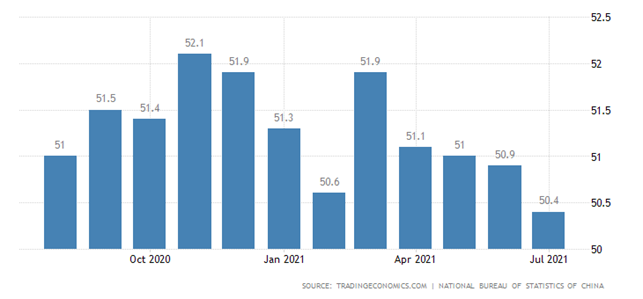

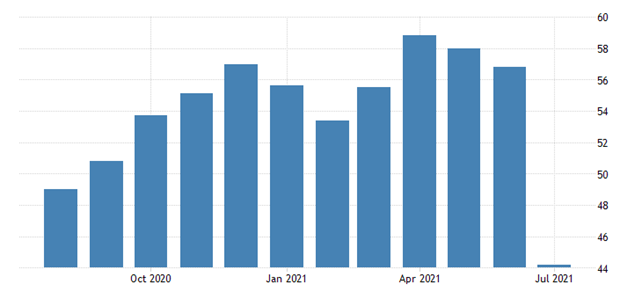

The production PMI (Purchasing Managers’ Index is describing the expert assessment of a particular industry; the view below 50 denotes stagnation and decline) of China, according to a private survey, has been at its lowest since April 2020 (50.3 points):

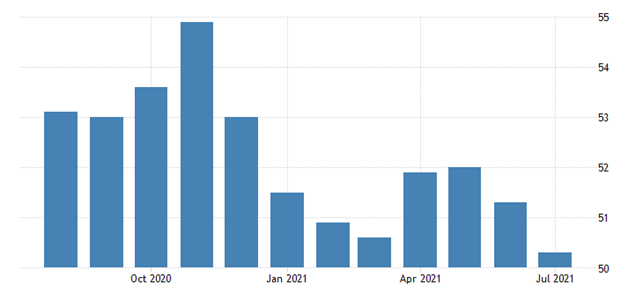

Official statistics confirm that Chinese industry is on the verge of halting growth:

PMI industry of Indonesia worst since June 2020 (40.1), components on the trough since May 2020, rising incoming prices record since 2014:

The same is true in South Africa, where the index is 43.5. In Russia, the 8-month low (47.5), i.e., industry is already in decline.

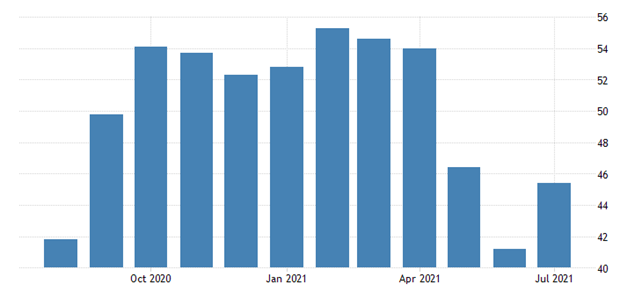

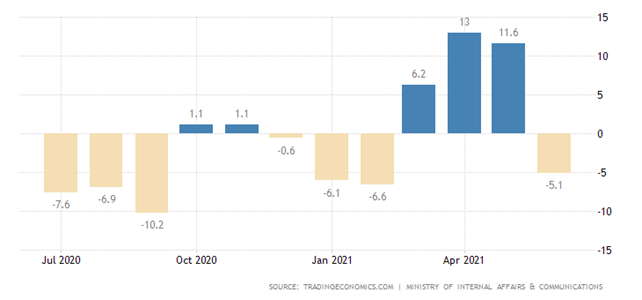

The decline in the Australian services PMI index can literally be called a collapse:

In India, it has improved, but it is still firmly in the recession zone:

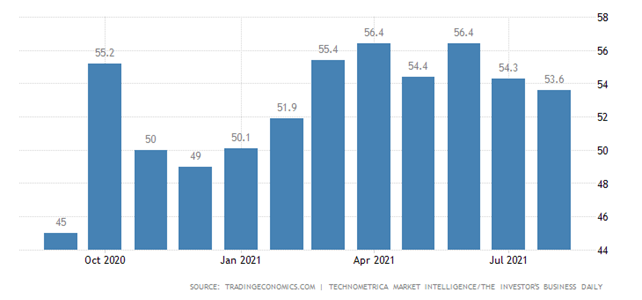

On the other hand, the PMI of the US services sector is the highest in 24 years of observation. The trouble is, as we have written in previous Reviews, inflation is now being actively understated in the US. Accordingly, price increases are depicted in statistics as increases in the real performance of the industry. All this is very little true:

Thus, economic optimism in the US, which is determined by the actual state of the economy rather than the nominal state of the economy, the weakest gap in investor and consumer sentiment in six months is the highest in the survey’s history (20 years):

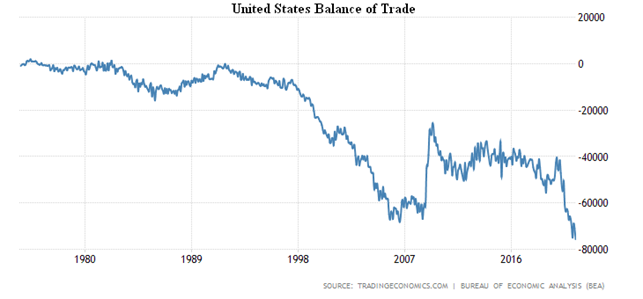

The US trade deficit is the largest in history:

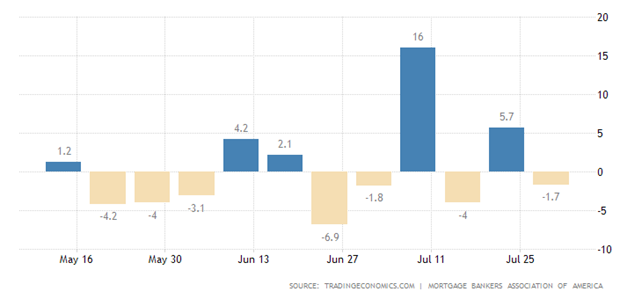

Mortgage applications in the US -1.7% per week, refinancing is lively, loans for purchases are falling non-stop:

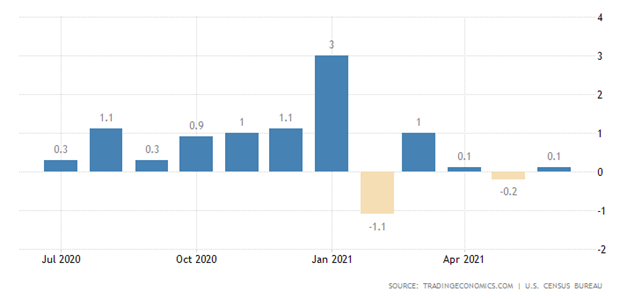

Construction costs in the United States have not increased since February:

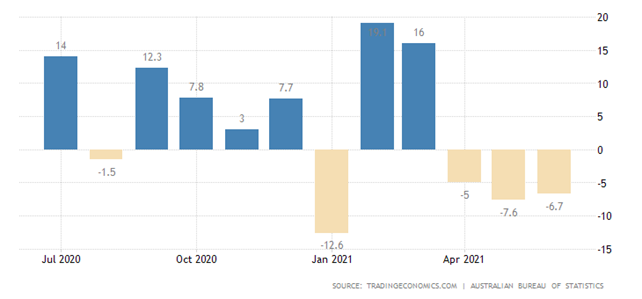

In Australia, building permits have not increased since the beginning of the year, and the last three months have been deeply negative:

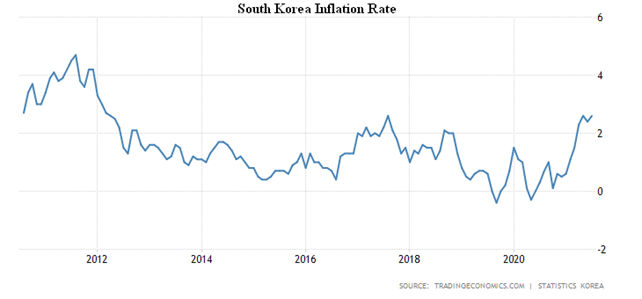

CPI (Consumer Price Index) of South Korea + 2.6% per year, the highest since 2012:

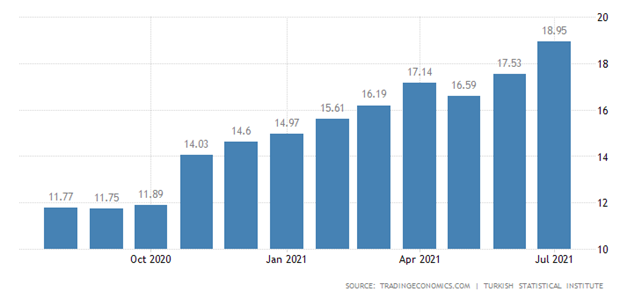

Turkey’s CPI + 19% per year, this is the peak since 2019:

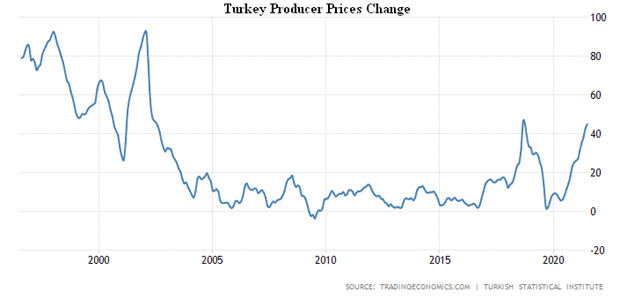

Turkey’s PPI (industrial inflation index) (+ 44.9% per year) is very close to the top of 2018, next in line is the highs of 2002:

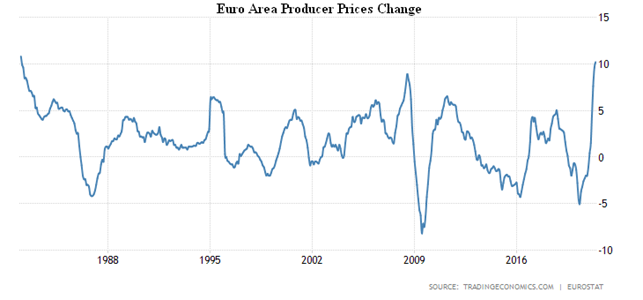

The Euro Area PPI 10.2% per year, maximum since 1982:

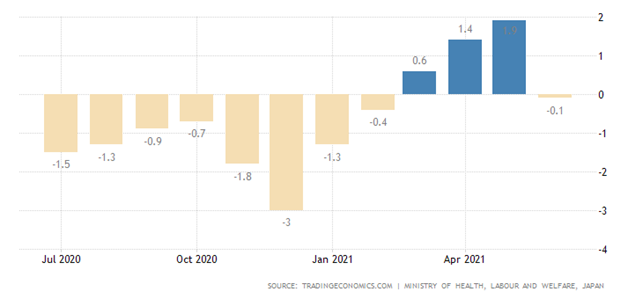

Total Cash Earnings in Japan have gone negative:

Japanese spending also fell, but on a much larger scale (-3.2% per month and -5.1% per year):

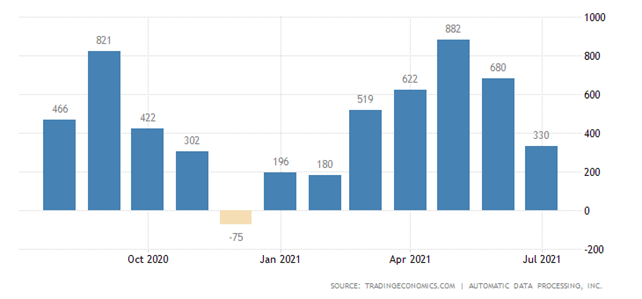

Employment in the United States private sector (ADP survey) has increased minimally since February and is half that expected:

The initial jobless claims in the US were not encouraging either, 400,000 per week against the forecast of 385,000; a week ago it was 424,000 (revised from 419,000).

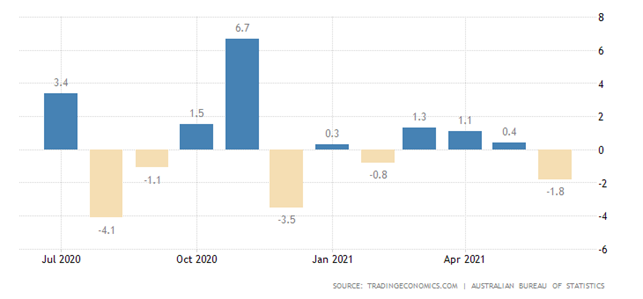

Retail sales in Australia are -1.8% per month, generally not up since the beginning of the year:

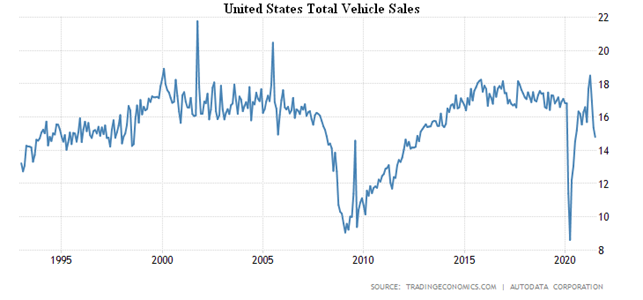

Total vehicle sales in the United States are minimal for a year due to the lack of spare parts:

The Central Bank of Australia has kept monetary policy unchanged, with moderately strong comments, and the Bank of England has done the same, however, with an overall plan for future policy tightening.

Brazil’s central bank charged 1.00% to 5.25%, unlike India’s central bank, which left the situation unchanged.

Summary. The conflicts with debt described in the first section of this Review and, in general, the less-than-optimistic sentiments indicate that the demand for loans by economic entities (both households and business entities) should decline. An additional factor is the huge subsidies.

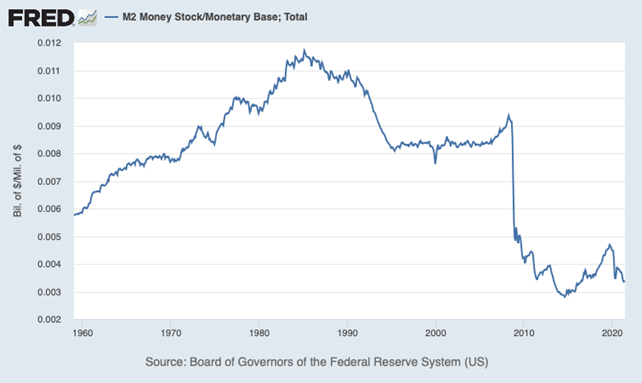

As a result, the credit multiplier decreases. The exact multiplier value (the ratio of M3 to the monetary base) for the United States can only be determined by estimation (Fed has not provided M3 data for a long time). But the scale of the phenomenon can be estimated using the M2 unit:

This chart clearly shows the collapse of 2008-2014 (which allowed the US without inflation to expand the monetary base fourfold without inflation), as well as the collapse of the last year. The real value of the credit multiplier today is about 2, which is significantly lower than the norm (which is 4 to 6; the value above 17, which was at the onset of the crisis in 2008 indicates an enormous bubble in the financial sector). De facto, today’s US banking system is inoperative, it was replaced by a printing press.

In this situation, it is not entirely clear what resource could trigger real (rather than nominal) growth in the US (and therefore in the world, certainly in China). In fact, without a healthier US financial system, the recession will continue, which is impossible without dismantling the financial pyramids. In other words, it is clear from the simplest of fiscal charts that without a collapse that corrects structural imbalances, there is no chance of recovery.

We wish all our subscribers a great vacation!