September 16-22, 2023

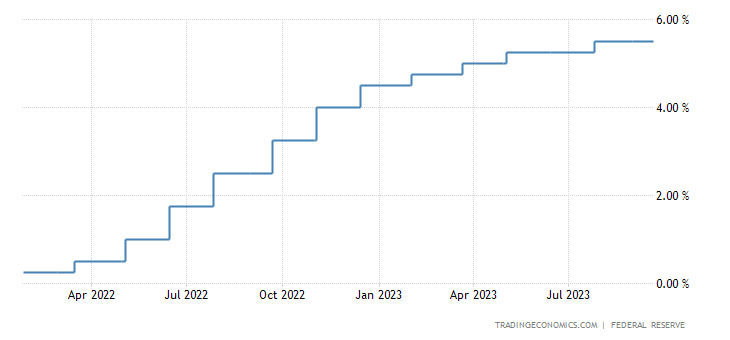

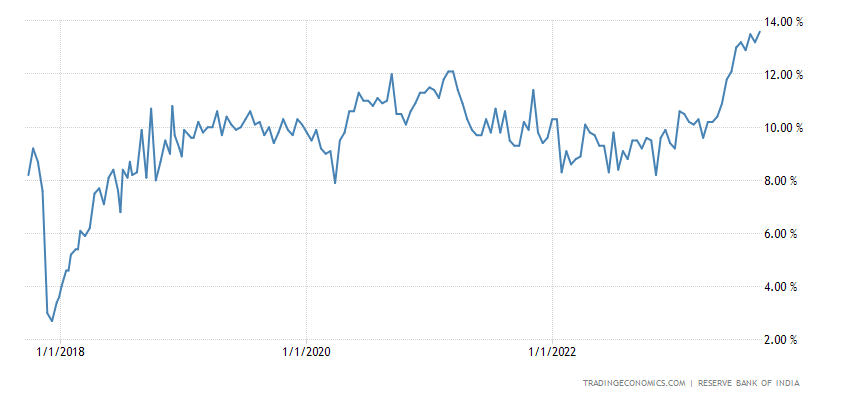

Big news. The Federal Reserve at the Federal Open Market Committee (FOMC) meeting did not change rates, but hinted at another rate hike before the end of the year; in 2024, the percentage is expected to decrease by 0.5% (instead of previous estimates of a reduction of 1.0%):

Pic. 1

This decision could raise questions, especially with inflation slight increase. More precisely, the consumer price index amounted to 3.7% year-on-year as of September 13 (that’s why we have noted this in the previous review, but the FOMC meeting took place this week) with the previous value (as of mid-August) 3.2% and the forecast of 3.6%. However, the main event occurred at the press conference.

In fact, Fed Chairman Powell has thrown a tantrum there, repeating several times the same theses that the maximum rate point was close but unknown for the Fed and that the processes taking place in the Fed economy were not clear. Details are in the last section of the review, but the overall picture looks rather strange.

We can only make an assumption: the fact is that this week UN Secretary-General Gutierres said that the Bretton Woods system (like the UN) needs reform. Taking into account the fact that official liberal propaganda believes that B.-W. the system ceased to operate in 1971, this statement seems quite unexpected, but at the same time, not new, since the first time he said this was in May of this year. Considering the fact that the fate of B.-W. systems are in no way included in the mandate of the UN Secretary-General, the combination of these factors allows us to make a (relatively) plausible assumption.

Its essence is that the Fed’s helplessness in determining the causes of the crisis (for readers of these reviews of the Khazin Foundation there are no questions at all; the theory of the current crisis was described in rough form 20 years ago, but outside the framework of liberal economic theory) causes natural irritation among the elite of the “Western” global project and the US political elites. And it is possible that in May of this year Powell was given a strict condition to correct the situation (conditionally, by the end of the year). And so that this warning did not look like an empty threat, Gutierres was used.

Otherwise, the dollar system will face reform, since the rate of accumulation of debts clearly exceeds all reasonable limits. Well, something needs to be done. At the same time, by the way, there is a serious question whether dollar debts will be preserved (or to what extent they will be preserved). And thus, the current leadership of the Fed and other Bretton Woods institutions (IMF, World Bank, WTO, etc.) are facing serious problems.

And if you consider that with the arrival of fundamentally new people, a thorough audit is possible, Powell’s nervous reaction becomes understandable. And his words, in fact, are addressed to all potential victims of this reform and are an offer to do something real. From system support to suggestions on how to fix the situation.

Of course, this is just a hypothesis. However, the head of the Khazin’s Foundation, in the process of both his work in public service and writing books about the theory of Power, has encountered similar situations more than once. And from the point of view of this experience, the situation looks quite transparent and natural. However, the Foundation team will be grateful for expressing alternative reasons for Powell’s behavior.

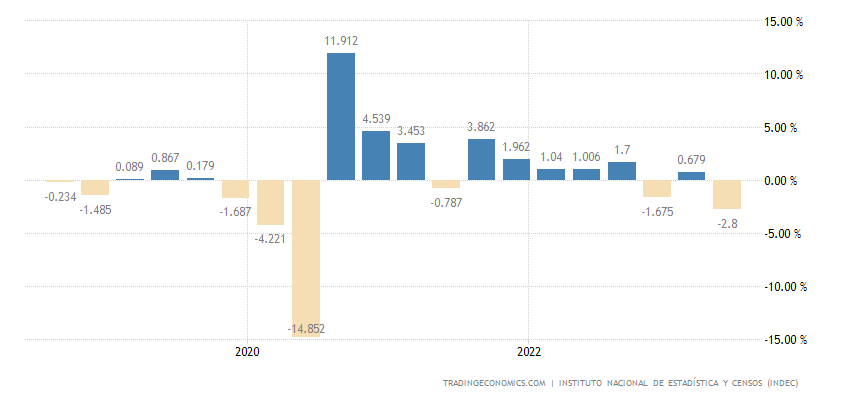

Macroeconomics. Argentina’s GDP -2.8% per quarter – without taking into account Covid, this is the bottom for 5 years:

Pic. 2

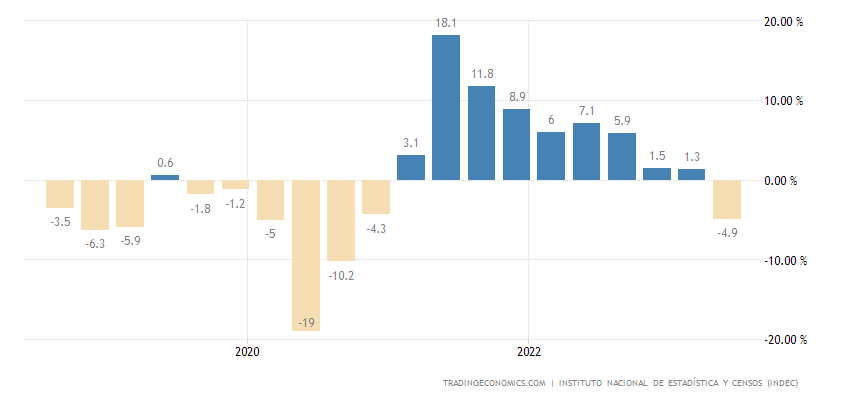

And -4.9% per year is also a 5-year minimum (minus the failure of 2020):

Pic. 3

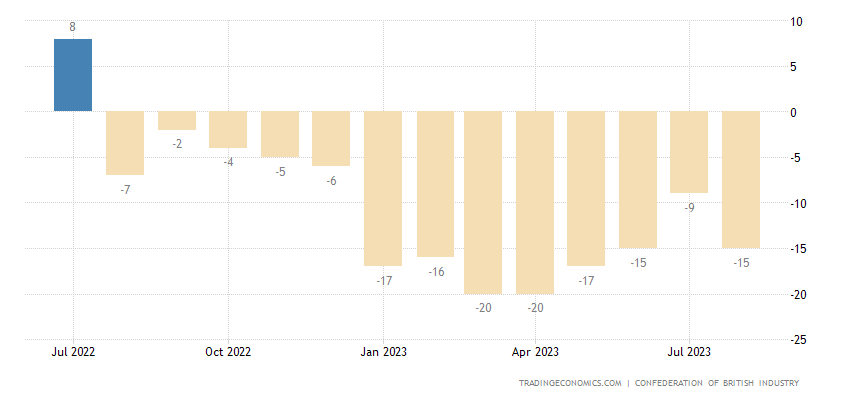

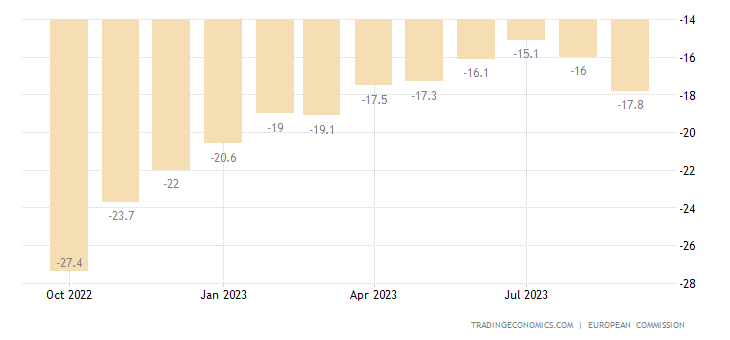

The balance of orders in British industry has been in the red for 14 months in a row:

Pic. 4

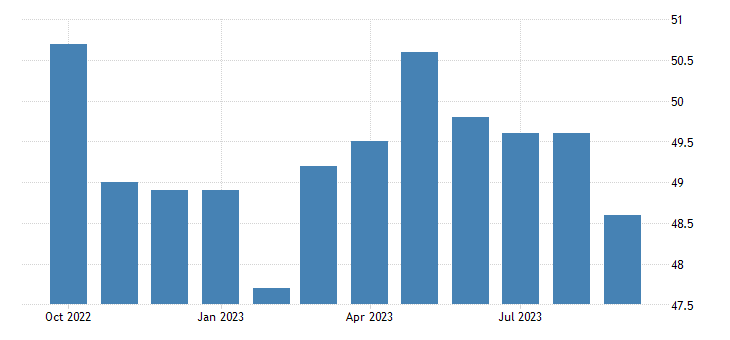

PMI (expert index of industry condition; its value below 50 means stagnation and decline) of the Japanese industry is the weakest in 7 months and in the recession zone (48.6):

Pic. 5

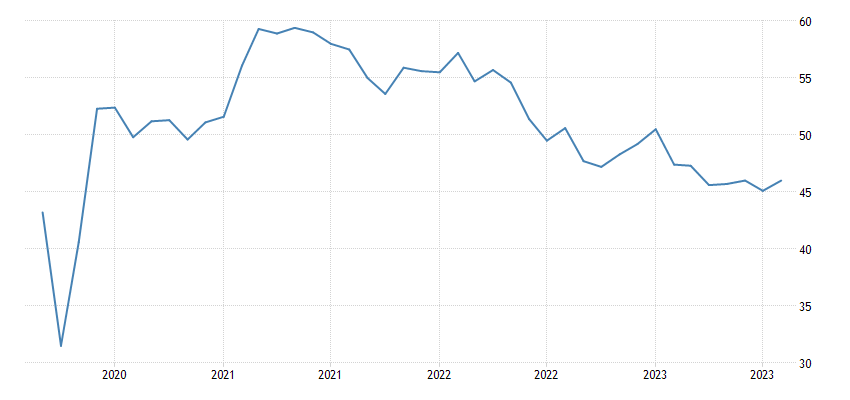

In France, the bottom for 3.5 years (43.6), the bottom of 2012 is under threat:

Pic. 6

In Germany it is even worse (39.8), but it was even lower; output index at the bottom since May 2020:

Pic. 7

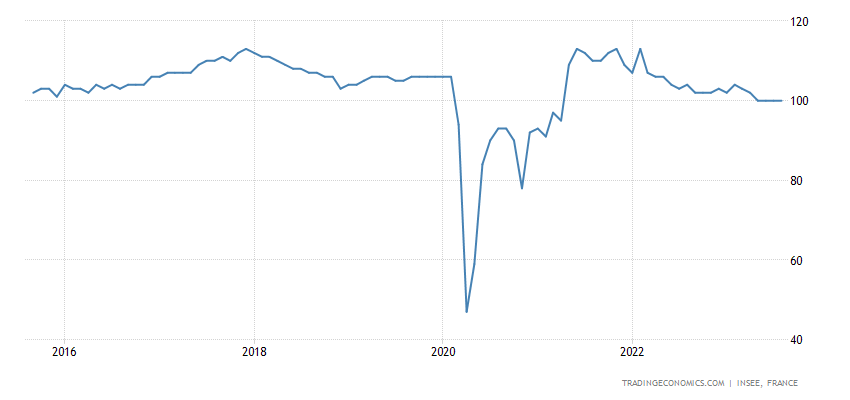

The business climate index in France has been at its lowest since 2020, and without taking into account Covid – for 8 years:

Pic. 8

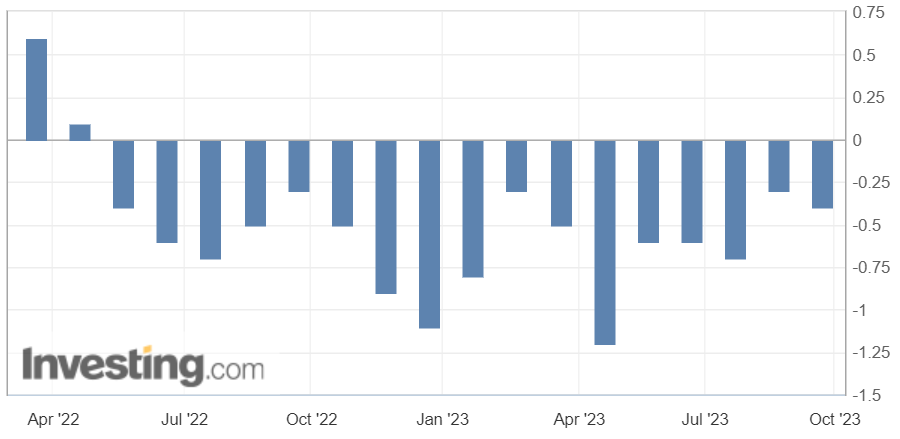

Index of leading indicators in the US -0.4% per month – 17th minus in a row:

Pic. 9

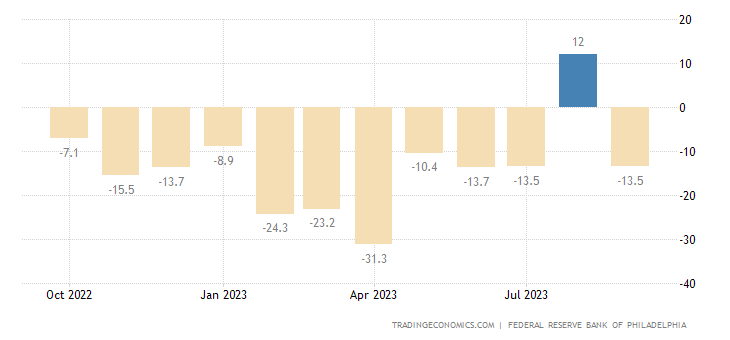

The Philadelphia Fed index returned to negative territory after its only positive gain over the past year:

Pic. 10

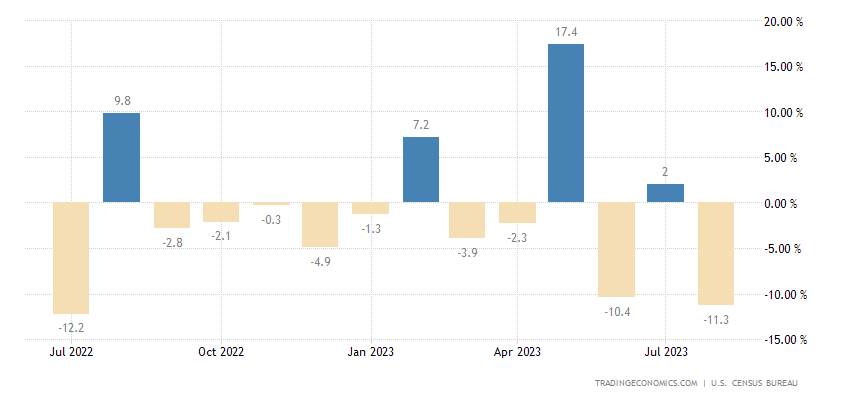

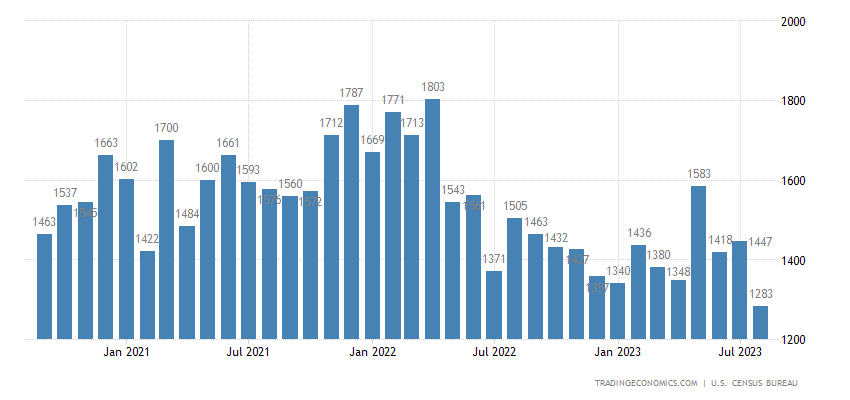

The number of new buildings in the US -11.3% per month – the weakest dynamics in 13 months:

Pic. 11

and much lower than the forecast of -2.5% and the previous value of 2%.

And reached a more than 3-year low:

Pic. 12

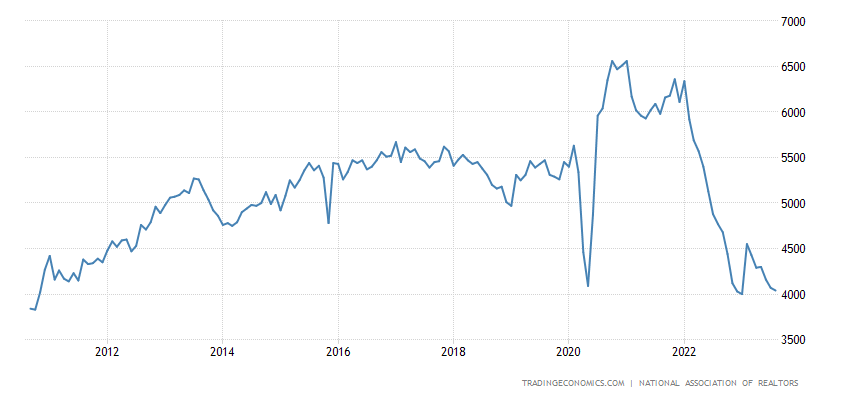

US existing home sales are only 1% above their 13-year low:

Pic. 13

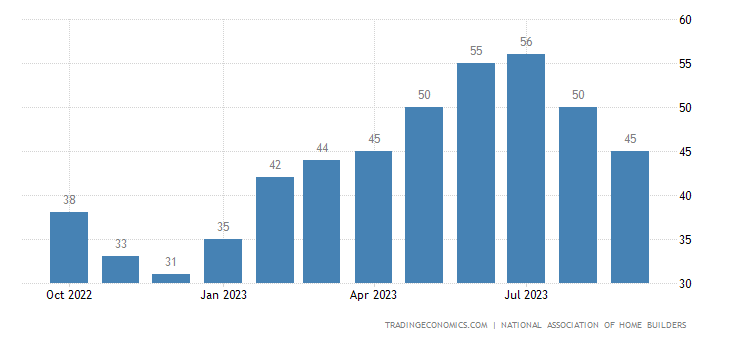

The US housing market index is the weakest in six months and is again in the recession zone:

Pic. 14

Which is not surprising, since the 30-year mortgage rate repeated its recent 23-year peak (7.31%):

Pic. 15

And the 10-year Treasury yield has broken through last year’s high and is now at its highest since 2007:

Pic. 16

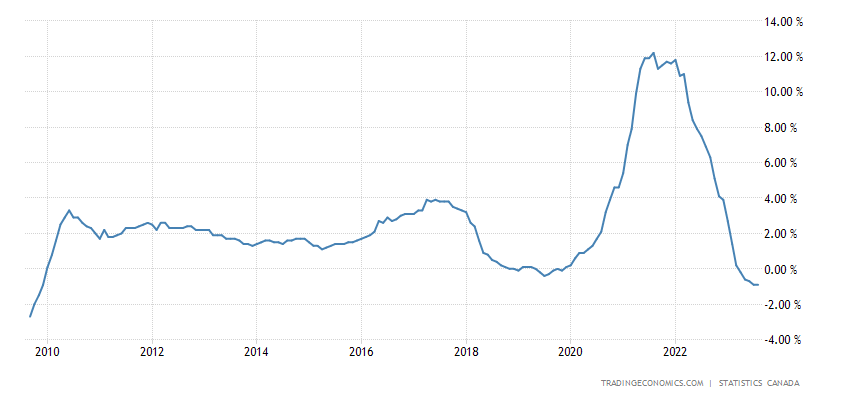

Prices of new buildings in Canada -0.9% per year – 14-year minimum:

Pic. 17

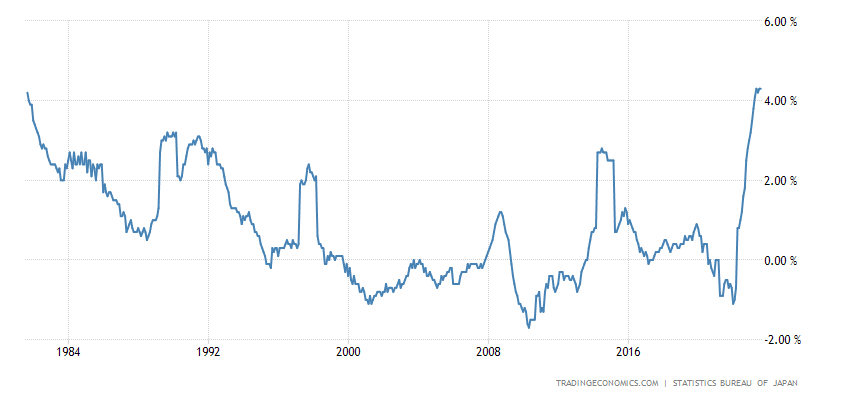

CPI (Consumer Inflation Index) excluding food and fuel in Japan remains at a 42-year high of +4.3% per year:

Pic. 18

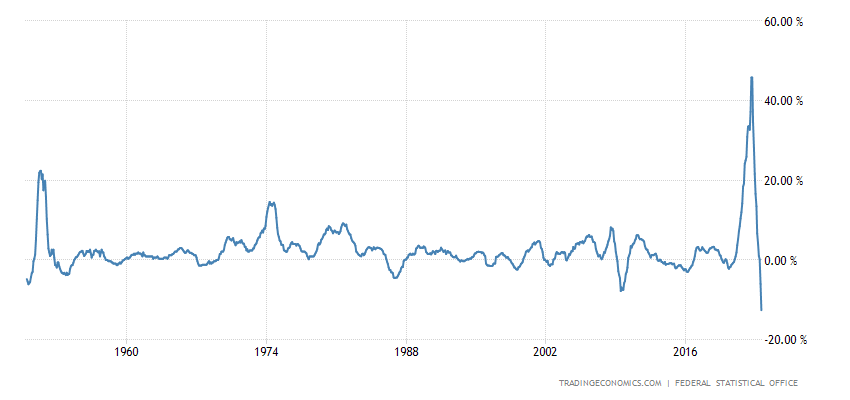

PPI (industrial inflation index) of Germany -12.6% per year – an anti-record for 74 years of statistics:

Pic. 19

In fact, there is severe depression. However, this is the norm during a structural crisis.

The growth of deposits in Indian banks (+13.2% per year) is the highest since 2017:

Pic. 20

Eurozone consumers are the most pessimistic in six months:

Pic. 21

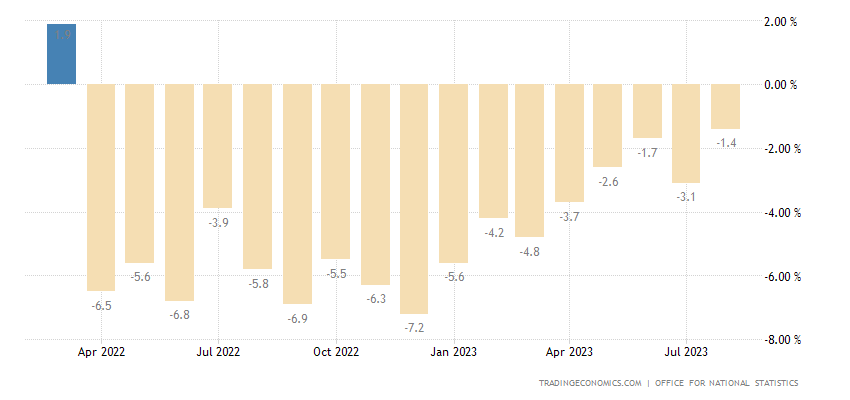

Retail sales in Britain -1.4% per year – the 17th negative in a row:

Pic. 22

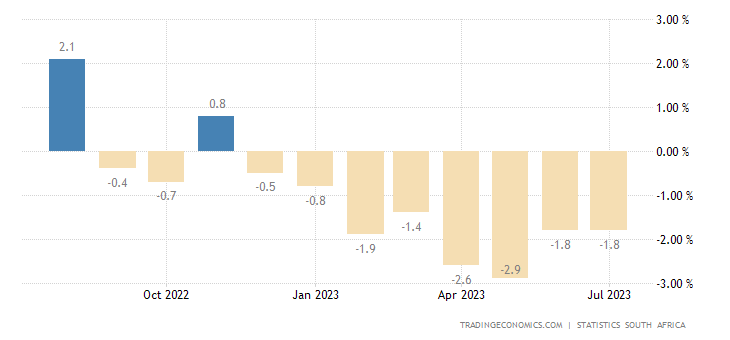

Retail in South Africa -1.8% per year – 8th negative in a row:

Pic. 23

The Bank of England unexpectedly did not raise rates (by a majority vote of 5 to 4). The Bank of Japan left everything as it was, despite rumors of possible signals of future tightening

The Chinese Central Bank predictably left its monetary policy unchanged. As do the Central Bank of Indonesia and the Central Bank of South Africa.

The Central Bank of Brazil lowered the rate by 0.50% to 12.75%.

The Turkish Central Bank increased the percentage by 5% to 30%.

Main conclusions. First, a little information about the rate.

The decision was expected; this forecast was given by 94 out of 97 economists surveyed by Reuters. The next meeting on the rate will take place on October 31 – November 1. The market considers the most likely scenario that the rate will remain unchanged, according to data from the FedWatch tool, which is calculated by the CME exchange based on rate futures. As of September 20, the probability of such a decision was estimated at 72.8%. However, almost every fifth expert surveyed by Reuters (17 out of 97) expects at least one rate hike before the end of the year.

In fact, this means that the Fed is following the market and is not trying to somehow “steer” the situation.

Powell press conference, preliminary statement:

“Now we can act CAREFULLY!

our decisions will be based on data and risk assessments;

The Fed is focused on a “dual mandate” (dollar stability and low unemployment, note FH);

without price stability there will be no strong labor market;

real GDP growth exceeded expectations;

the US economy has not yet felt the past tightening of monetary policy;

the unemployment rate is still low, inflation is still high;

There is a long way to go to get to 2% inflation;

we will adhere to sufficiently tight policies to achieve our inflation target;

the current state of monetary policy is restrictive.

Answers to journalists’ questions:

“The forecasts of the Fed members are not a plan;

Fed policy depends on data;

more progress is needed to begin to claim that everything is OK;

decisions will be made from meeting to meeting;

we are obliged to maintain a sufficiently restrictive policy;

economic activity in the US is higher than expected;

maintaining the interest rate here does not mean that we have achieved or have not achieved the desired political position;

I would not attach great importance to another rate increase;

we are close to the peak in the rate;

strong economic activity has forced us to pay more attention to interest rates;

the labor market still needs some easing;

it’s good that we see a significant restoration of balance in the labor market without a significant increase in unemployment.

a “soft landing” of the US economy is not a baseline scenario;

the question now is to find a rate level that we will leave constant;

a “soft landing” is a very likely result, but there are factors beyond our control;

we will discuss all the data at the last two meetings that we will hold this year;

when I answer questions about rate reductions, I am not going to announce any deadlines!

US GDP is not the goal of our mandate!

we only evaluate economic strength to achieve our goals;

a soft landing of the US economy is the main task;

we are still looking for the peak rate level;

rising energy prices are a significant factor for inflationary surges;

the government shutdown will not have a broad impact on the economy;

the worst thing we can do is not restore price stability in the country;

forecasts are very uncertain;

the risk of excessive tightening is equal to the risk of insufficient tightening of the monetary policy;

the latest inflation reports were good, but we need more data like this. There is no need to rush to conclusions;

a government shutdown could lead to a shortage of economic data. You will have to come to terms with this;

any future decision to reduce rates will be determined only by economic requirements (if necessary);

growth in government profitability bonds is not associated with an increase in inflation, but with an increase in the supply of these securities on the market.”

Statements about GDP look quite specific in the current situation; in reality, the US economy has been falling for quite some time (since the fall of 2021). But the art of statisticians cannot be ignored and the result is obvious. Well, the information about deflation in the industrial sector mentioned in the previous review confirms this assumption.

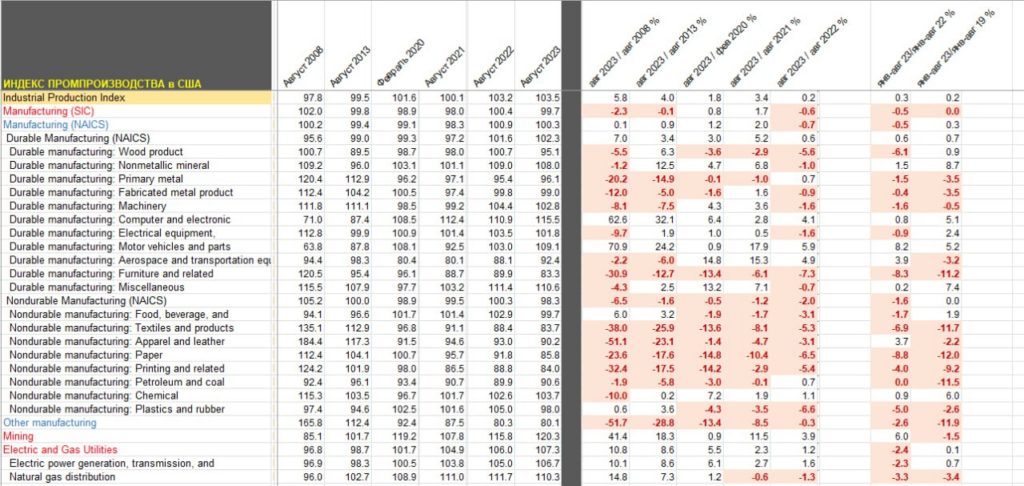

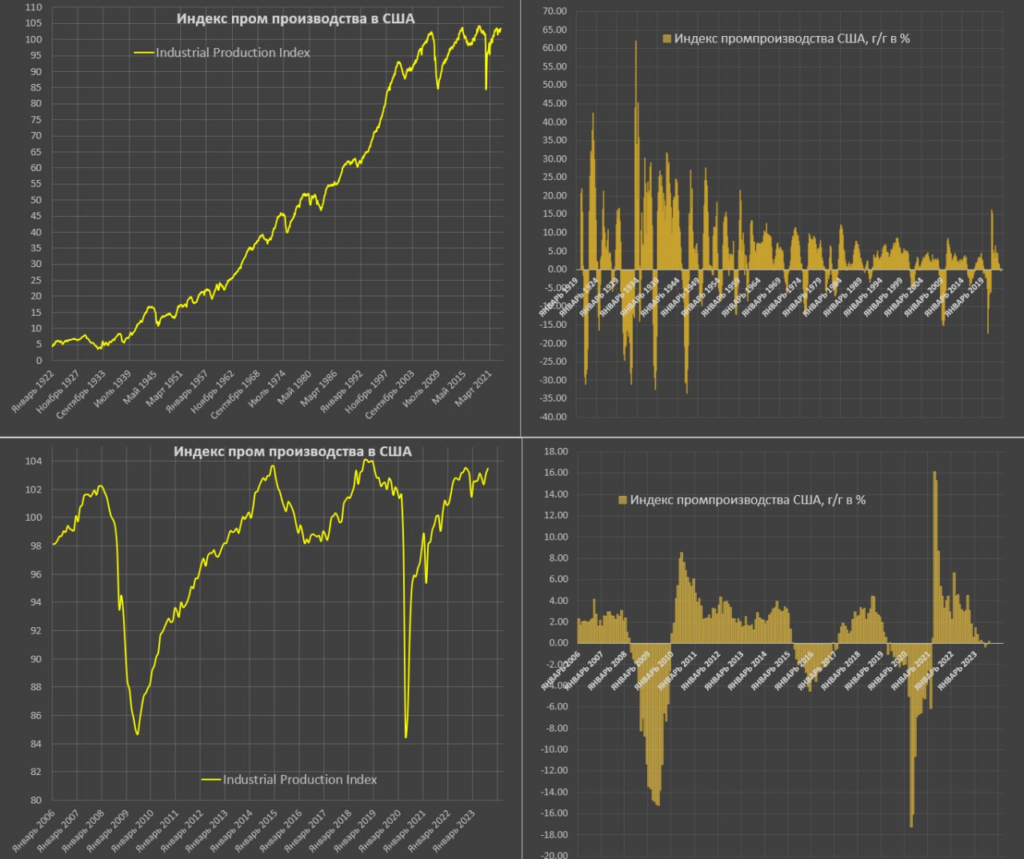

Information on the state of US industry (from Pavel Ryabov, Spydell):

- “Industry in the United States is not decisive in terms of shaping economic dynamics. Industry forms less than 13% of the US economy directly, and taking into account industries related to industry. sector, industry directly or indirectly affects at least ¼ of GDP.

- However, industry is a leading indicator of business cycles and structural changes in the economy. The latest data for August indicate continued stagnation without sudden disruptions – growth relative to last year is within the accuracy of the calculation (0.25% y/y) and approximately comparable growth of about 0.3% y/y for January-August 2023.

- In the first eight months of 2023, the growth of industrial production (mining + processing + electricity and utilities) amounted to 0.2% compared to the same period in 2019 – prolonged stagnation. The details are presented in the table below, but several significant points can be highlighted.

- There are no signs of significant activation of the military-industrial complex, because the production of ammunition is included in the “Fabricated metal product”, but a decrease of 0.4% y/y and minus 3.5% by 2019 is recorded here, and the production of high-tech products, including armored vehicles, is included in the category “Aerospace and transportation equipment”, but nothing here either outstanding – growth by 3.9% y/y, but a decrease by 3.2% by 2019.

- The trends are similar to European industry (reduction in low- and medium-process production and low-profit production), but with the difference that energy-intensive production and electricity production are practically unaffected, but the production of petroleum products is in a vulnerable position.

- Yes, in the USA there is an emphasis on knowledge-intensive and high-tech production, but the trend is less pronounced than in Europe, where there is a pronounced concentration of resources on high-tech. In general, it is fair to talk about a growing trend in the high-value production segment in the United States.

- Industry is near highs but stagnating – 4% growth over 10 years is not a reason to be proud.”

Note that this assessment by Pavel Ryabov was made basing on official industry figures. Our assessment (a serious decline is already underway) is based on a general assessment of the situation.

But the 10-year US Treasury note is on track to fall for the third year in a row (after -3.9% in ’21, -17.0% in ’22 and -0.3% in ’23). And this has never happened in the entire 250-year history of the United States, starting in 1787.

Which, however, is not surprising given the record-tight monetary policy:

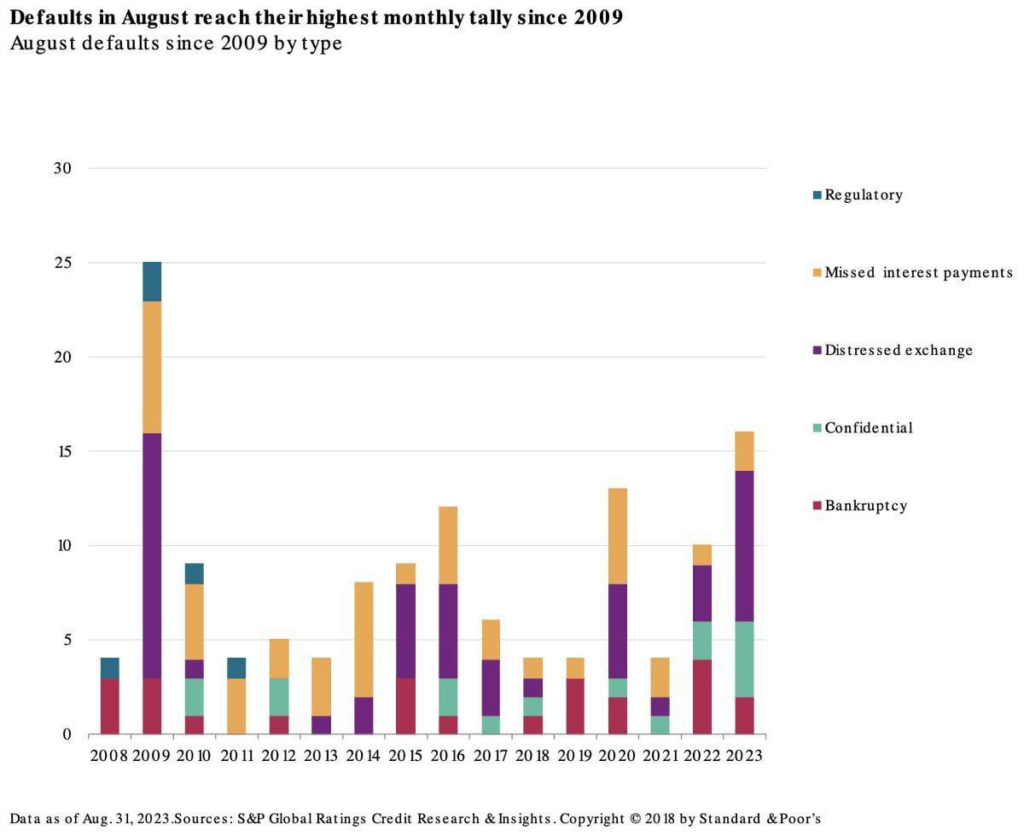

Things are not very good with bankruptcies:

In general, in conclusion, it can be noted that the official figures, of course, do not look very good, but still, they leave hope. But any realistic assessment of the general situation significantly reduces this optimism! However, we hope that this will not prevent our readers from relaxing on the weekend and working calmly the following week!