Period: 6 – 12 June 2020

Key takeaway: This review brings 2 key takeaways. First one – oil price recovery and pessimistic statement of FRS Chairman Powell which led to stock market collapse on Thursday, 11 June. This collapse, which happened despite the end of riots/disorder in USA, tells us that stock market recovery is temporary and influenced by FED’s continuous stimulus and it seems highly unlikely that current level of stock market can be sustained after U. S. Presidential election.

Macroeconomy

Eurozone’s 1Q GDP dropped 3,6% compared to previous quarter (record minimum) and dropped 3,1% compared to previous year (minimum since 2009). Germany’s quarterly drop is worst since 2009; for France, Italy, Spain – worst fall since GDP measurements started.

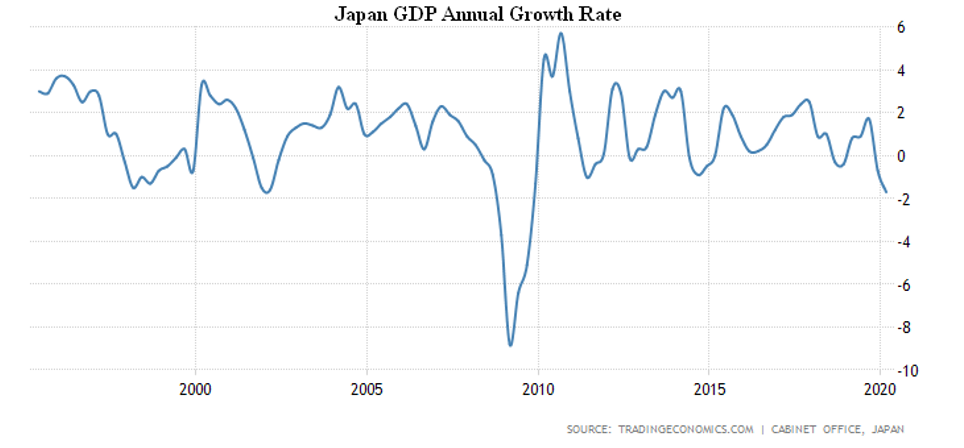

Japan’s 1Q GDP fell again 0,6% compared to previous quarter after a fall of 1,9% at the end of 2019 (due to sales tax increase):

This is first recession (2 consecutive quarters of GDP drop) since 2015 with year on year drop of 1,7% which is worst result since 2017.

UK’s GDP collapsed 20,4% against previous month and 24,5% against previous year (record minimum):

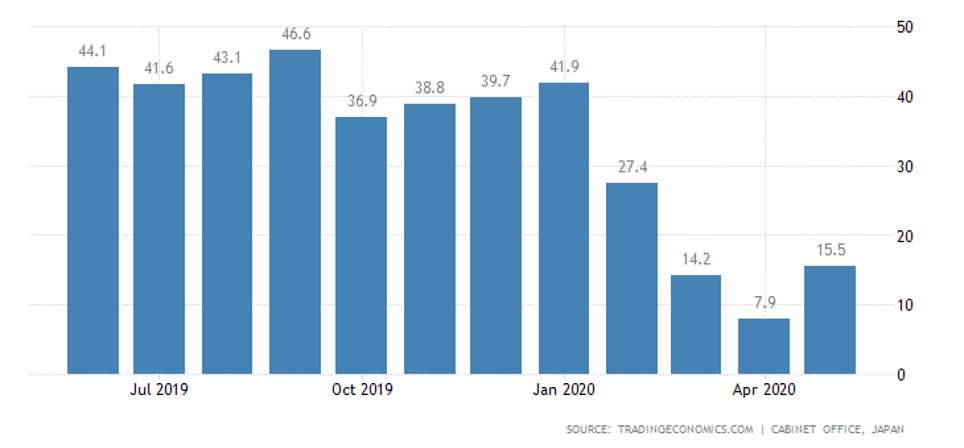

Japan’s economic observer index in May rose slightly from April’s record lows but still remains low.

Heavy equipment/machinery building orders in Japan collapsed 52,8% against last year to record lows since 2010. Japan’s PPI yearly decline in May (-2,7%) is strongest since September, 2016.

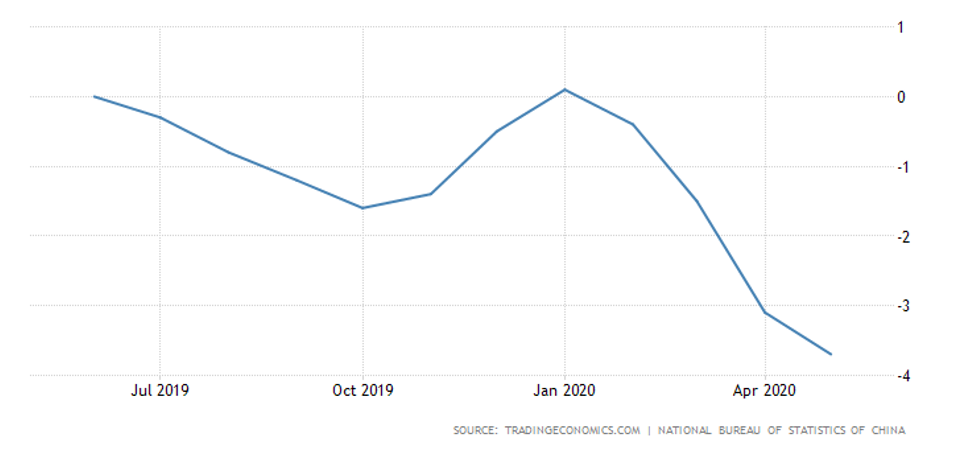

Chinese PPI drop is strongest since March, 2016:

Brazil’s CPI is lowest since January, 1999 (+1,88% YoY). USA’s CPI lowest since September, 2015 (+0,1% YoY or +1,2% with food and fuel excluded – lowest since March, 2011).

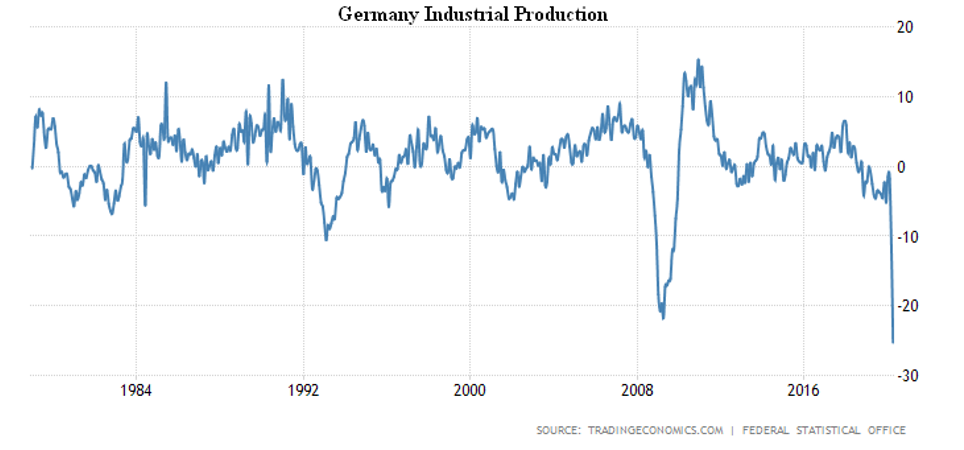

Germany’s monthly industrial production dropped 17,9% (lowest in 29 years), yearly industrial production dropped 25,3% (lowest in 41 years):

Processing industries drop of 31,2% is absolute record.

France fell 20,1% month-over-month (31 year minimum) and 34,2% year-over-year (39 year minimum). Processing industries drop of 37,1% YoY is strongest in 64 years.

Italy fell 19,1% MoM and 42,5% YoY (record minimum). Processing industries dropped 45,6%.

EU fell 17,1% MoM and 28,0% YoY – both are record minimums over 29 years of observations.

UK fell 20,3% MoM and 24,4% YoY (both record lows). Processing industries dropped 28,5% which is 51 year record.

Japan fell 9,8% MoM (record fall since 2011 earthquakes) and 15,0% YoY (record since 2009).

Mexico closed -25,1% MoM and -29,3% YoY (both record lows). Processing industries output closed -35,3% YoY (record low).

Turkey closed -30,4% MoM and -31,4 YoY (34 year lows).

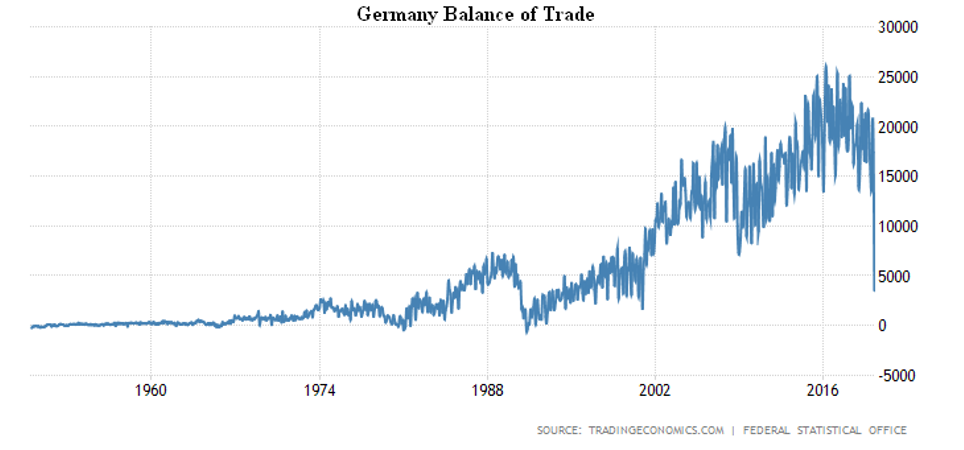

Germany’s trade surplus is lowest since December, 2000 and is equal to average of 1980/90’s.

This happened due to exports fall of 31,1% YoY and imports fall of 21,6% YoY.

Retail sales in Turkey in April dropped 21,0% MoM and 19,3% YoY – historical lows.

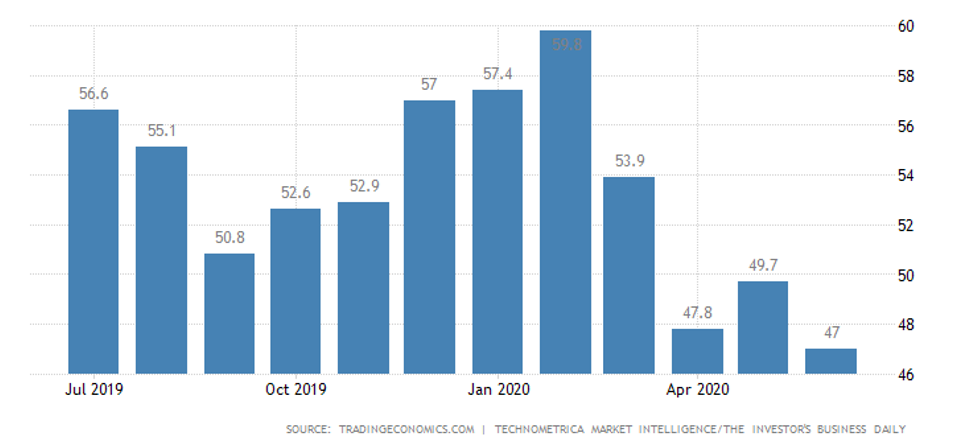

USA’s IBD/TIPP economic optimism index is at 4 year minimum. Pessimism is strongest amongst people with lower wages who took the main job cut’s blow due to coronavirus shutdown.

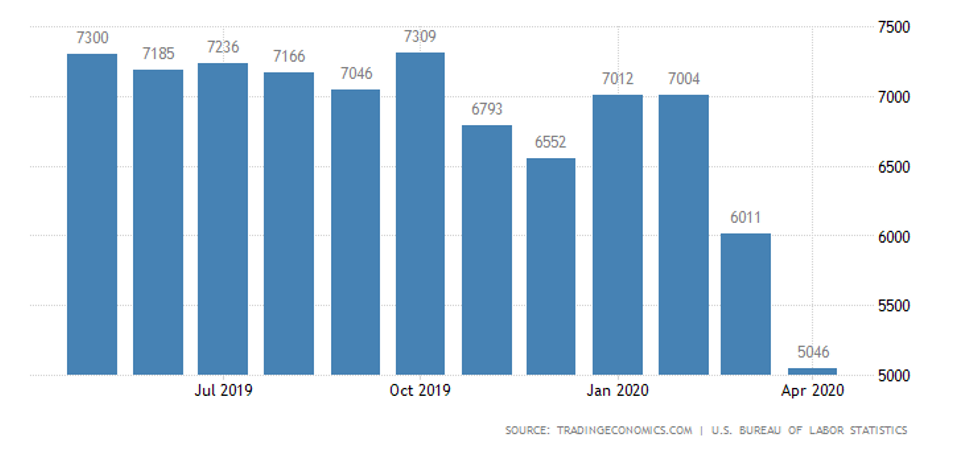

Number of new vacancies in USA in April (JOLTS review) was lowest since 2014.

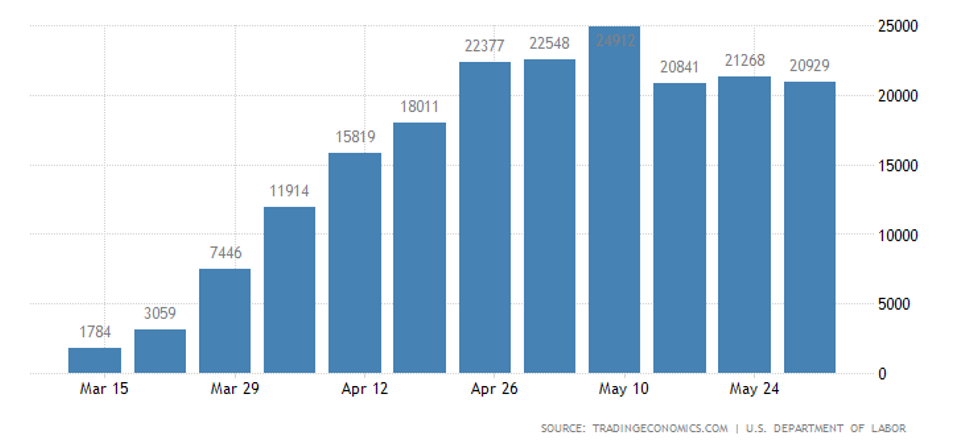

US department of labor May’s optimistic report isn’t confirmed by huge number of people – recipients of unemployment benefits:

Unemployment numbers in South Korea are highest since January, 2010.

May’s job vacancies in Australia grew only by 0,5% MoM after -53,4% in April. YoY decline is 59,8% which is close to rock bottom over 21 years of observations.

USA’s Federal Reserve policy remains unchanged with a promise that rates will remain at today’s levels until the end of 2022. Treasuries purchases will remain at 120 billion dollars per month. Small and mid-sized business support has been expanded as a result of very pessimistic economic forecasts (-6,5% GDP in 2020 and +5,0% in 2021 with unemployment levels at 9,3% and 6,5% respectively).

Key conclusions: As we assumed earlier in our reviews, official US unemployment numbers are not supported by facts. In current crisis situation it is critically important to understand the underlying economic fundamentals rather than drawing conclusions from official statistics. Such disturbances come from the fact that small data samples from which conclusions are drawn aren’t representative of the whole population in crisis scenarios.

We (Mikhail Khazin’s Economic Research Fund and researchers who work with us) have been studying crisis processes for more than 20 years and have mathematical and statistical models which are fine tuned to suit crisis situations. Looking at our data we can conclude that main crisis trigger lies in structural disproportions between how much is consumed and how much is earned by households (latter being much less that the former). Thus, economic decline can only be stopped when consumption and income will be balanced. For USA (and many other countries) this parity is still far ahead, so, even when we see short term economic recoveries due to FED’s active stimulus, the overall trend for economic decline will continue.