October 28 – Novenber 3, 2023

Big news. The Federal Open Market Committee (FOMC) of the US Federal Reserve decided not to raise the discount rate. We have repeatedly noted in previous reviews the difficulties of this point, so we will confine ourselves to only the basic problems. If you need, details of the official FOMC press release and the press conference of Fed Chairman Powell will be in the final section of the Review.

The essence of the Fed’s problems is that the rate level has become too high. Both for the US budget (we have described this in previous reviews) and for the American economy. This can be seen in all reviews for the last two years, with the most recent figures in the next section. Theoretically, the rate should be lowered in order to reduce the burden on budget refinancing and give an impetus to industry, but… But inflation has not dropped to 2% and, apparently, is ready to got up again.

At the same time, there is deflation in industry (a sign of recession). We will find out the figure for October next week (or in two, haven’t checked what they promise), but in the world, as can be seen from the next section, industrial deflation is raging with all its might. And in this situation, it would be necessary to soften monetary policy, especially since the election campaign requires supporting the living standards of the population. But it’s very scary…

In general, the hesitation of the Fed leadership suggests that it is not able to offer a more or less clear strategy of action. Even if it’s a crisis. Powell can’t even acknowledge the two-year economic downturn (which is masked by understating inflation and increasing monetization of fictitious assets) because of the election. And then it’s easy to say, “the economy will fall by 3%,” but what if it continues to fall? And she continued…

And if we also take into account at least two impending wars, with Iran and/or China, not counting the support of Ukraine… Ukraine, however, cannot be left, since the question of testimony against Biden regarding corruption charges will immediately arise. However, this question has already arisen and how it will affect the financial markets is a big question. In general, the leadership of the Fed has complex problems, a more or less clear solution to which is simply not in sight.

Macroeconomics. Sweden’s GDP -1.2% per year is a 3-year minimum, and without taking into account Covid – an 11-year minimum:

Рис. 1

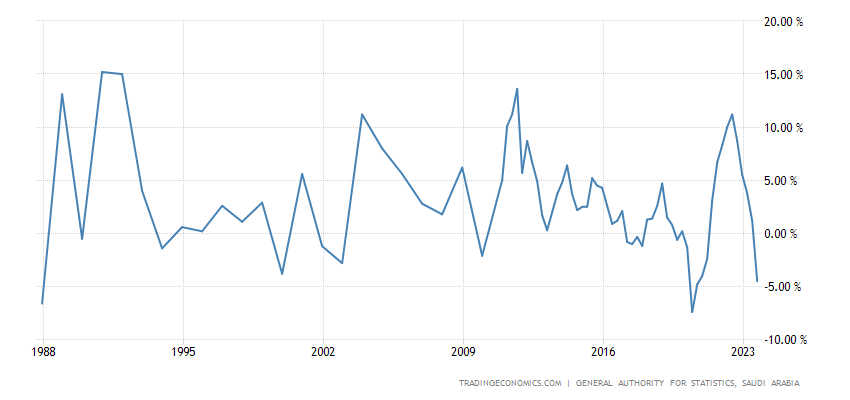

Saudi Arabia’s GDP is -4.5% per year – the last time it was even worse was only in 1988:

Рис. 2

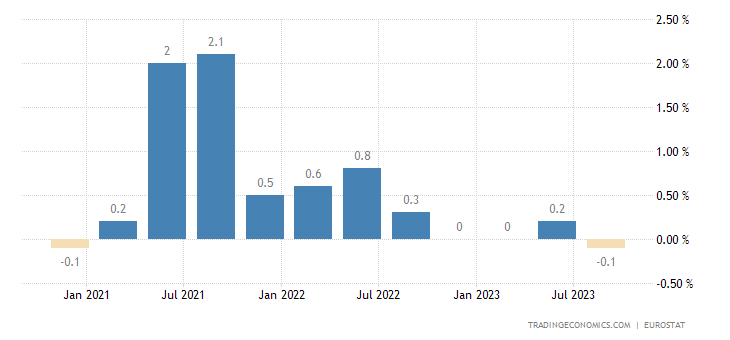

The eurozone economy is stagnating again: -0.1% per quarter:

Рис. 3

And +0.1% per year

Рис. 4

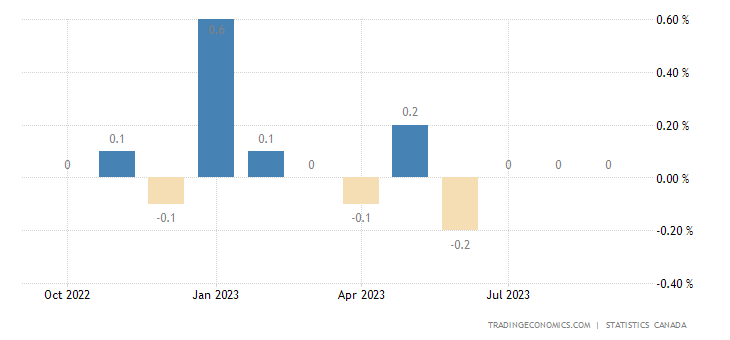

Canada is also stagnating, the economy shows zero change for 3 months in a row:

Рис. 5

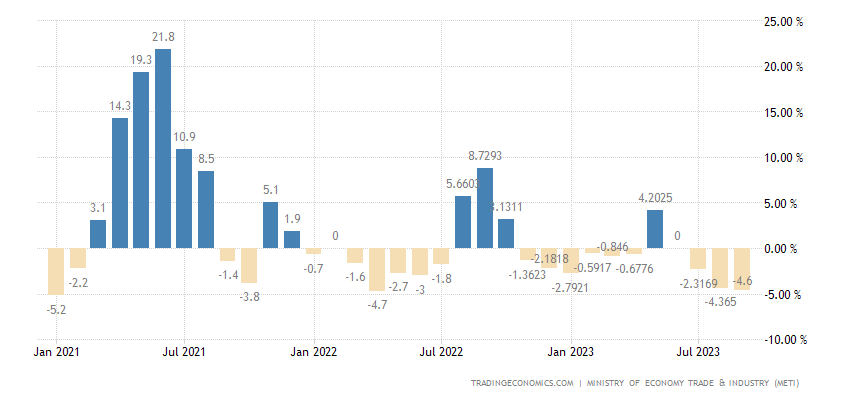

Industrial production in Japan -4.6% per year – a year and a half minimum:

Рис. 6

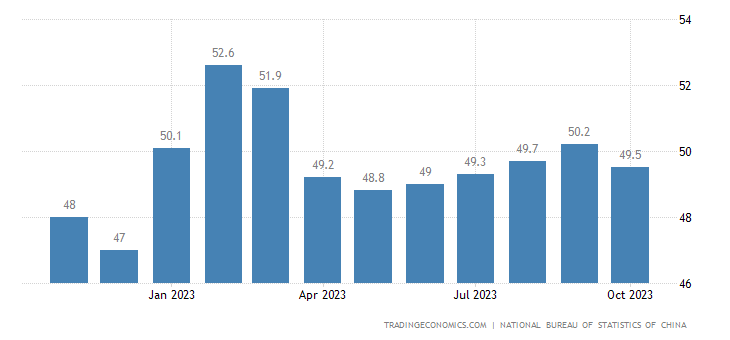

The official PMI (expert industry performance index; its value below 50 means stagnation and decline) of China’s industry returned to the recession zone (49.5):

Рис. 7

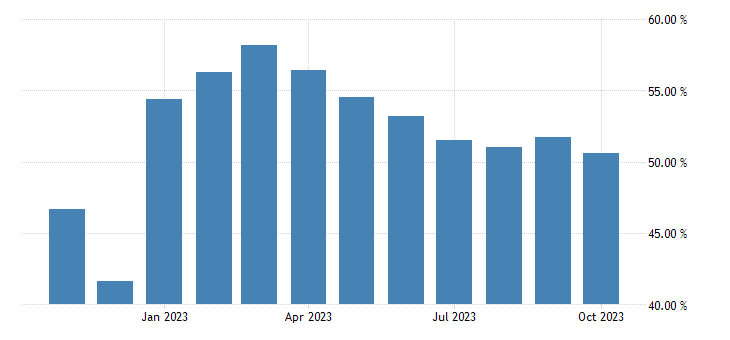

Other sectors are still in the area of mini-growth (50.6), but this is already the weakest in 10 months:

Рис. 8

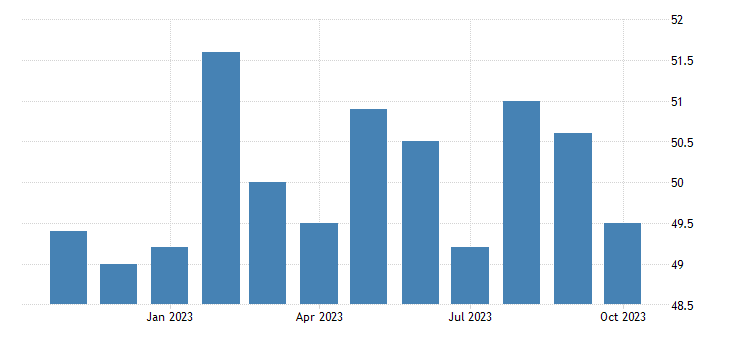

Independent researchers paint approximately the same picture:

Рис. 9

And this is in a situation where the real indicators of price growth are unknown, most likely, here too inflation is significantly underestimated.

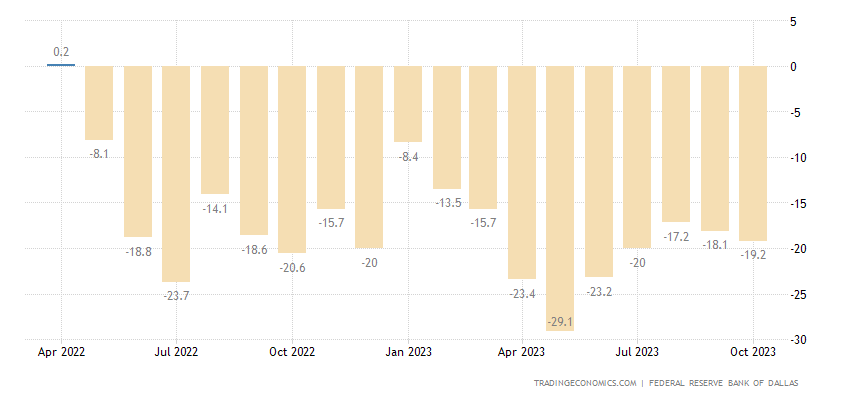

Manufacturing activity in the Texas Fed zone in the US has been in the red for 18 months in a row:

Рис. 10

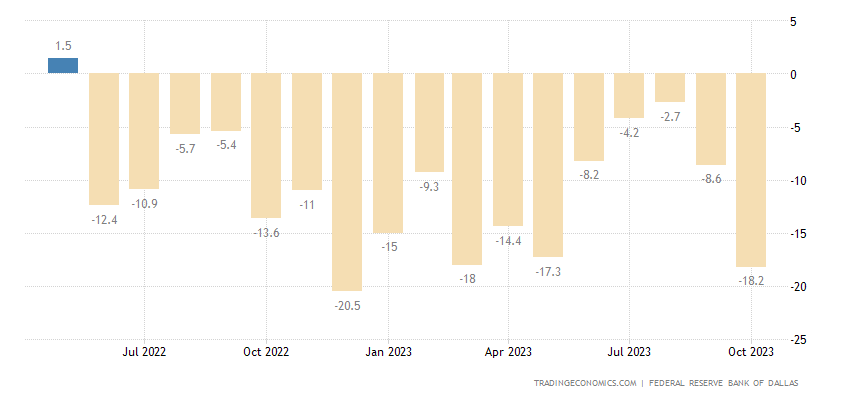

In the service sector of the same region, the 17th minus in a row:

Рис. 11

Taking into account the active relocation of companies from Silicon Valley to Austin (the capital of Texas), Katina looks depressing.

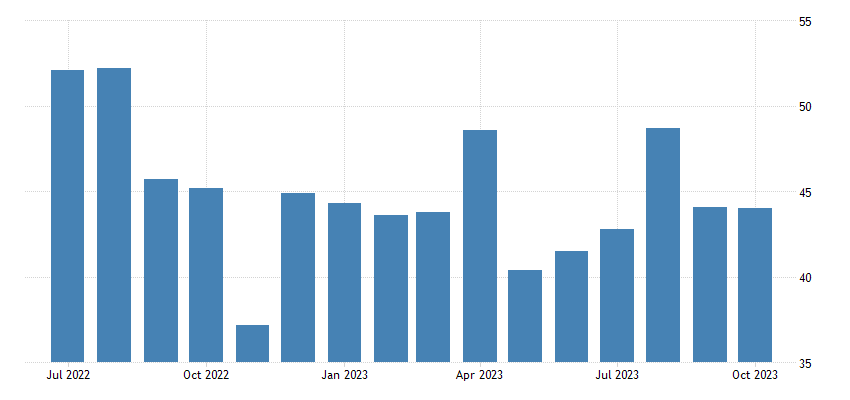

Chicago’s PMI has been in decline for 14 straight months:

Рис. 12

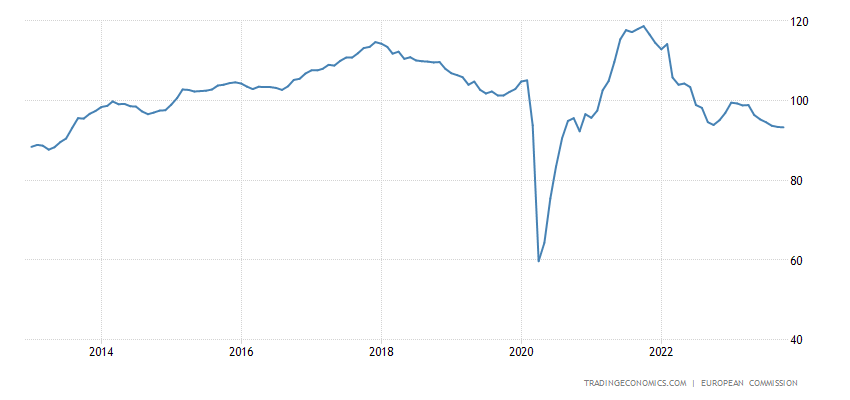

Economic sentiment in the eurozone is the worst in 10 years (excluding 2020):

Рис. 13

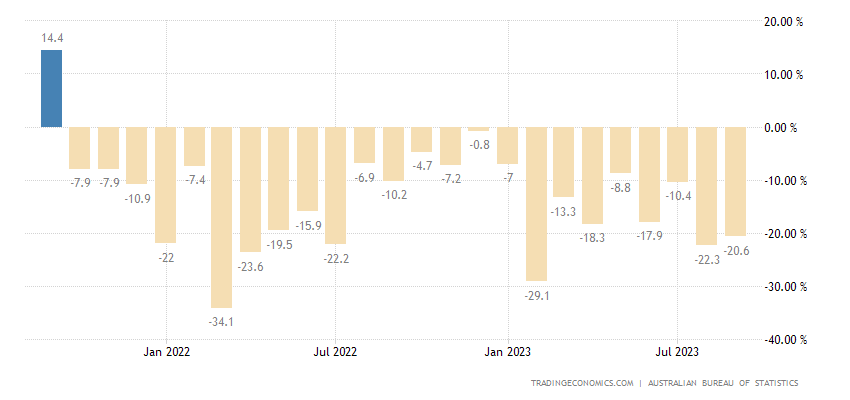

Building permits in Australia fell 20.6% annually – the 24th consecutive monthly decline:

Рис. 14

To 2008/12 levels:

Рис. 15

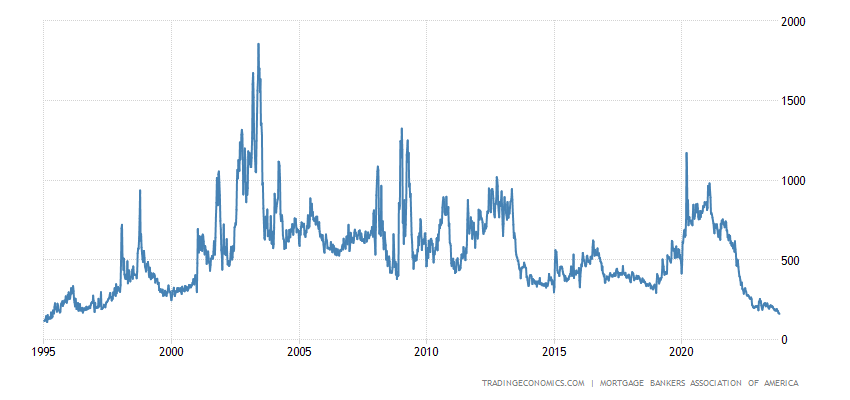

US mortgage applications hit 28-year low:

Рис. 16

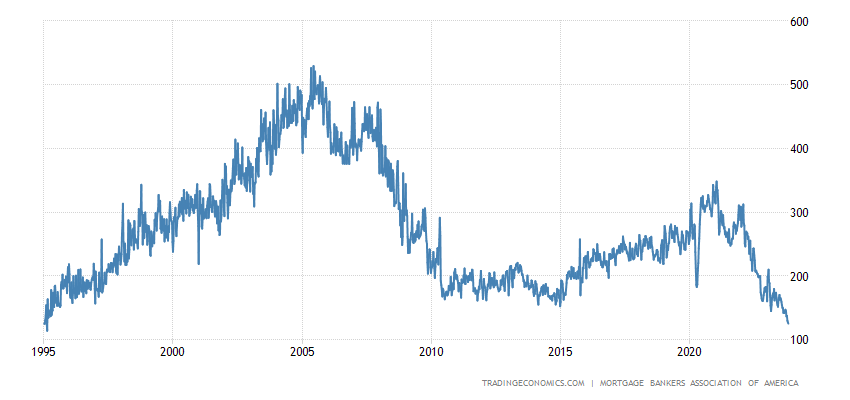

Same as purchase loans (i.e. minus refinancing of existing loans):

Рис. 17

Despite the stabilization of mortgage rates (however, at very high levels):

Рис. 18

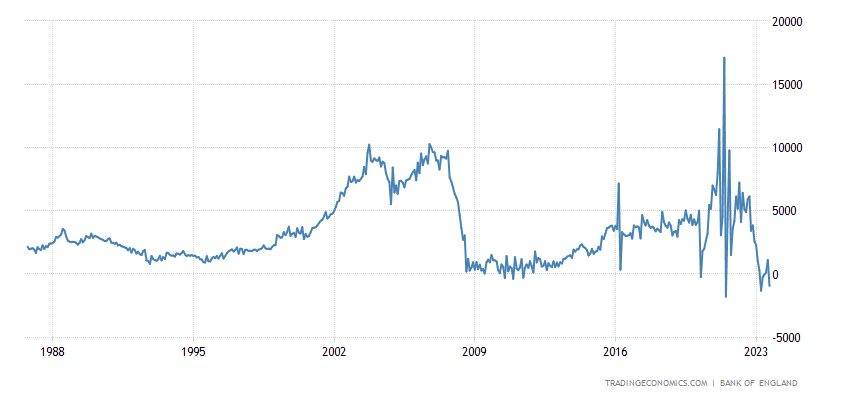

Net mortgage credit in Britain went negative and showed one of the worst values in history:

Рис. 19

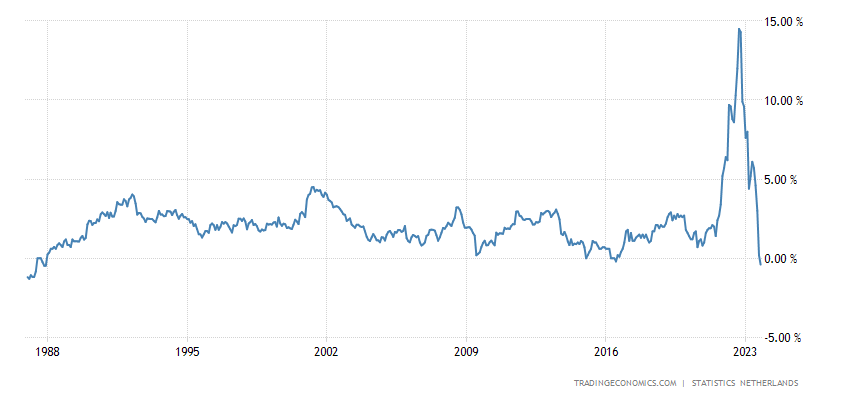

CPI (Consumer Inflation Index) of the Netherlands -0.4% per year – 36-year low:

Рис. 20

This is already very bad, a sharp drop in the standard of living of the population.

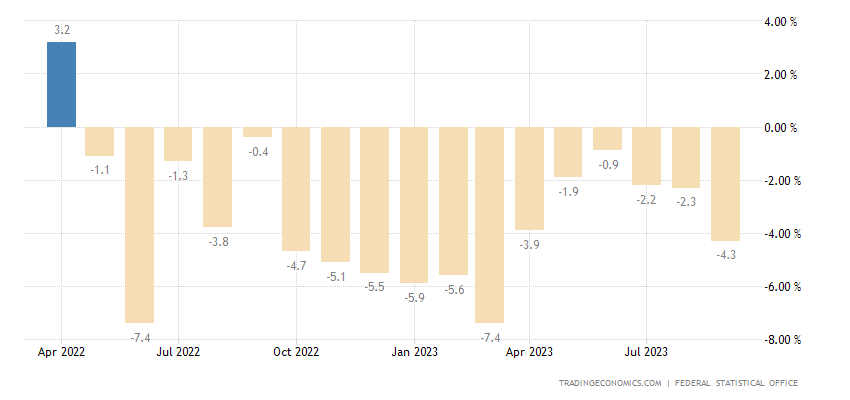

PPI (industrial inflation index) of Italy -14.1% per year – a record decline in 32 years of data collection:

Рис. 21

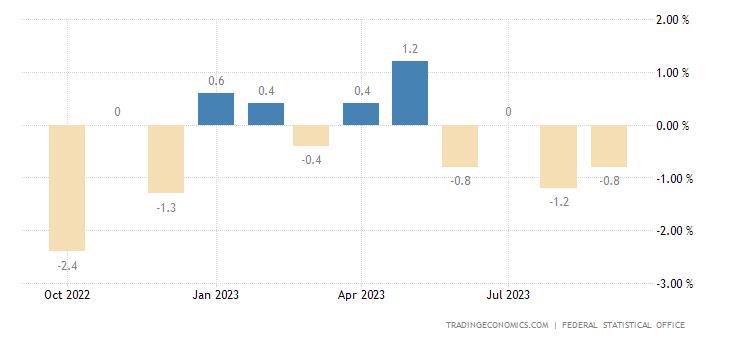

Retail sales in Germany -0.8% per month – 4th negative in a row:

Рис. 22

And -4.3% per year – the 17th minus in a row:

Рис. 23

If inflation is underestimated, we remind you!

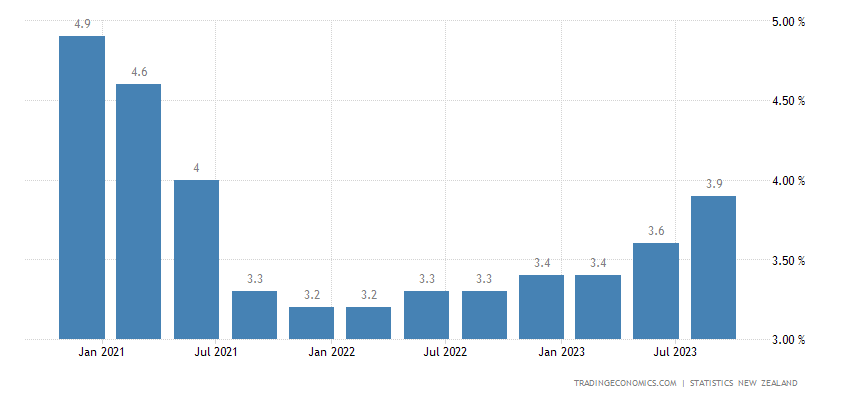

Unemployment in New Zealand is the highest in more than 2 years:

Рис. 24

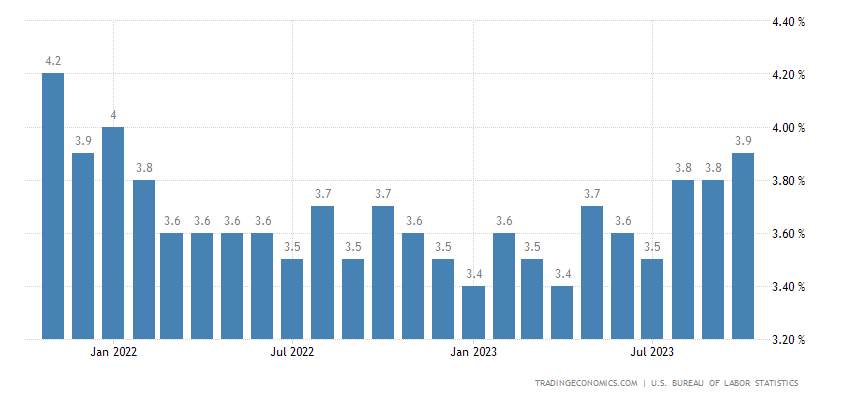

In the USA – in almost 2 years:

Рис. 25

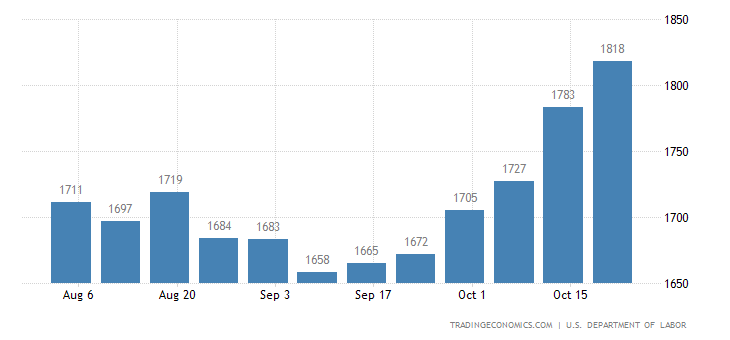

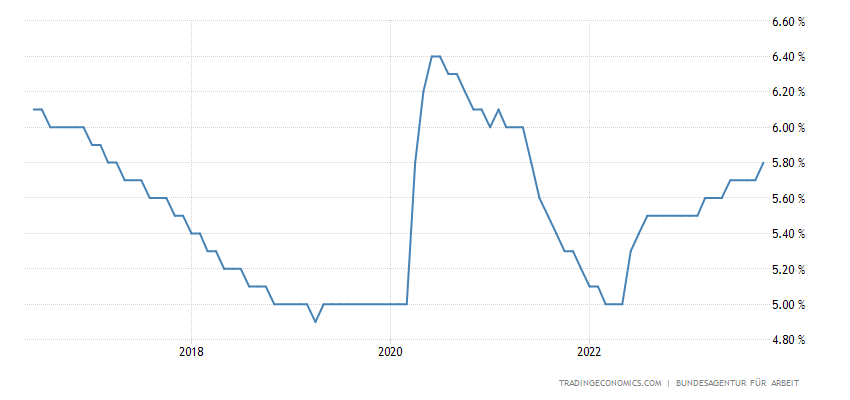

The number of recipients of unemployment benefits in the United States is the highest in six months:

Рис. 26

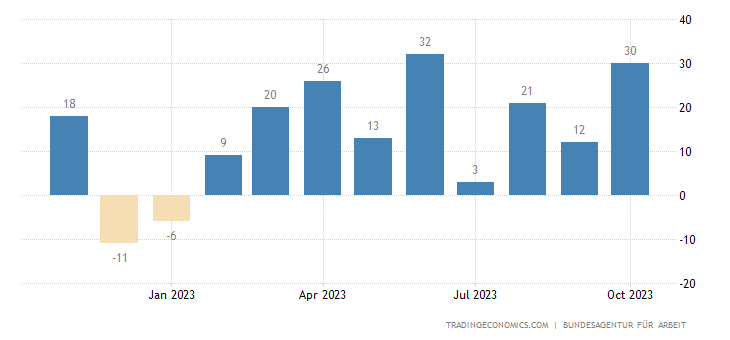

The number of unemployed in Germany has been growing for 9 months in a row:

Рис. 27

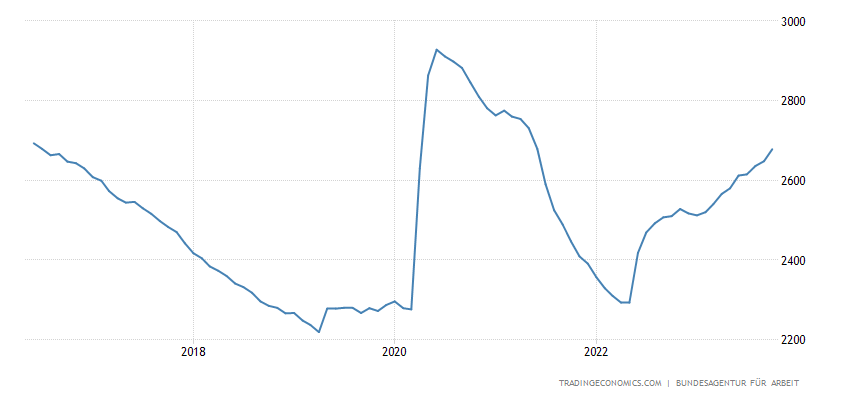

And it has already reached the levels of summer 2016:

Рис. 28

There is also the unemployment rate:

Рис. 29

In Norway, the Central Bank left the rate the same, but they continue to hint at further tightening. The same thing happened in Britain. But the Central Bank of Japan still refuses any tightening of monetary policy.

The Central Bank of Brazil cut the rate for the third time in a row by 0.50%, to 12.25%.

Main conclusions. A significant part of Powell’s press conference about the results of the rate announcement was devoted to the main pain point of the market – the extreme increase in the yield of medium-term and mainly long-term bonds, both government and corporate.

The official marginal fixing rate of the US Treasury was 4.95% for 10-year Treasuries on October 25, 2023, while within the trading day on October 23 the 5% limit was broken, albeit for a short period. The emphasis on bond yields and assurances from the Fed that it is in control of the situation led to a release of tension and a decrease in 10-year yields to 4.7-4.75% (mid-October levels).

It was the nightmare in the debt market that led to the collapse of the stock market last week, and the stabilization of Treasuries instantly restored the capitalization of the S&P500. It would seem that everything is fine. But not quite, as Powell’s behavior shows.

Powell repeated himself a lot this time, so it’s becoming increasingly difficult to highlight what’s important. The first question about the rapid increase in yields on long-term securities (0.6-0.7 percentage points since the last meeting) was left unanswered. Apparently, it was decided that the situation would normalize and the head of the Fed did not want to get into details. Since the topic is, after all, important, Powell still said: “… From the content, we can highlight that we expect an increase in long-term rates from the Fed in the context of high short-term rates.”

It was further said that the Fed is considering a set of financial indicators that allow one to assess the level of stress and imbalance in the system, but the Fed will not say what these indicators are (God forbid, someone starts checking their effectiveness. Note from the Khazin Foundation). The Fed does not look at any one indicator in isolation outside the context of a more balanced financial and macroeconomic picture. High long-term rates alone, regardless of integral financial conditions, are not a sufficient argument for the Fed to take any action.

A decrease in the value of bonds should not affect the stability of the system this time as it did in March 2023, because Over the past six months, the Fed and the banks have done some work.

The window of opportunity for a rate increase has been preserved, but the likelihood of implementation, as always, is uncertain: “we haven’t made a decision yet, we don’t know what we will do, we will continue to monitor the data.” There is no set of factors that will trigger a possible rate increase, that is, there is no benchmark that will determine that this is the level where the Fed will raise the rate. The Fed will consider a complex of factors and their relationships in the context of the situation.

The Fed is not considering a rate cut in the near future; this issue is not even on the current agenda. The only thing that matters is the length of time that contractionary policy will continue until the Fed is confident that its inflation target has been achieved.

We are close to the end of the monetary tightening cycle, but this is not a promise or a plan for the future, because The Fed makes decisions based on current incoming data and risks in the system. We are reviewing incoming data and proceeding with caution. PrEP is quite restrictive at the moment.

The Fed does not view QT as having enough of an impact on the excess supply of securities that could affect long-term rates. The Fed is not considering the possibility of reducing QT in the face of high rates on medium- and long-term bonds. 1 trillion balance sheet reduction, given previously accumulated assets, is not something that can cause imbalances in the debt market.

The Fed does not consider a recession as a hypothetical scenario and believes that the economy is strong (No comments here. Notes from the Khazin Foundation). The way the economy responded to the current rate increase rate is a historically unusual result and does not fit into standard economic models/theories and forecasts (Liberal models and theories. We have appropriate models, we also have a theory, and they show adequate results. Note from the Khazin Foundation).

Well, as usual: “We have to achieve a slowdown in the economy below the trend, stabilize imbalances in the labor market and reduce inflation to the Fed target. There is a lag in the transmission of strict monetary policy to the real economy, but the timing and strength of the conversion are unknown.” The question arises, what is known then?.. However, it is purely rhetorical in nature.

In general, those who believe Powell find it difficult to sleep peacefully, since reality constantly contradicts their picture of the world. The same cannot be said about our readers, to whom we wish a good weekend and a productive work week!