October 7-13, 2023

Big news. Of course – Hamas attack on Israel with subsequent consequences, since both the reasons for this operation and its implications, of course, have a pronounced economic meaning.

There were a lot of comments on this topic, as well as the reasons for the events. But there is no doubt that the financial, logistical, and geopolitical consequences will be colossal. It became clear, in particular, that there was no hope for restoring stability in the global economy. This is obvious to our readers, but they still constitute a minority of the citizens of the whole world. Plus, hope dies last; it seems to us that many of our readers hoped that we were sometimes mistaken in long-term forecasts.

Today it is obvious that confrontation in the world is only intensifying. The key question is where the US strike will be directed. There are several options, the main one being China’s interests in Southeast Asia. But there are many who want to redirect American armed forces, including to Iran. But the events of the last week have shown that the United States understands the real state of affairs and attempts to direct them towards Iran are not working.

Another very important topic is the conflicting interests of the United States and Great Britain in the Middle East. Roughly speaking, the USA wants to preserve Israel and weaken Turkey, Great Britain – on the contrary. And this contradiction has come to the surface and it is no longer possible to reconcile the opposing positions. It is possible for events to develop one way or another, and even together (the destruction of both Israel and Turkey), but restoring the situation of recent years – no.

We will not continue to talk about this topic, it clearly does not relate to macroeconomics, but since it has a colossal impact on the development of the economic situation, it was impossible to remain silent. We’ll talk about more or less clear consequences only in two weeks, and certainly after the start of Israel’s ground operation in Gaza and the actions of other potential participants in the conflict. In the meantime, we move on to macroeconomics.

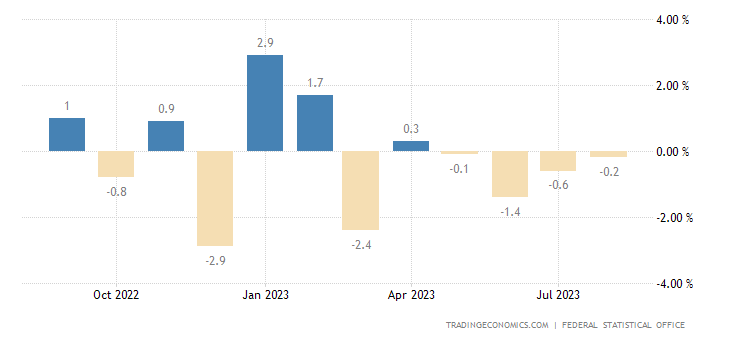

Macroeconomics. Industrial production in Germany -0.2% per month – 4th minus in a row:

Pic. 1

And -2.0% per year – the 3rd minus in a row:

Pic. 2

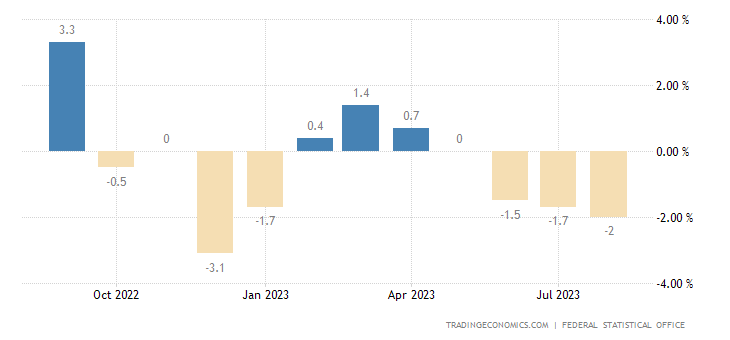

In Belgium -2.2% per year – the 9th minus in a row:

Pic. 3

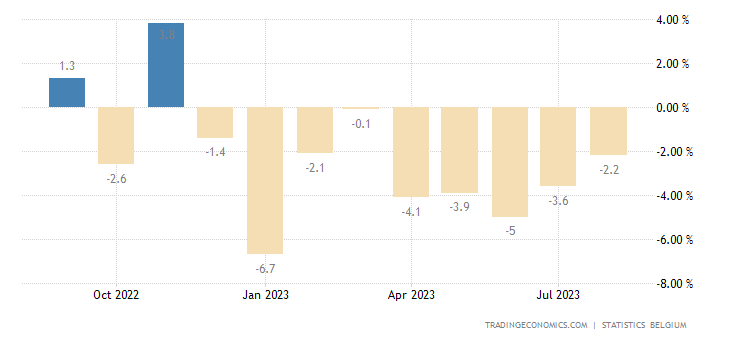

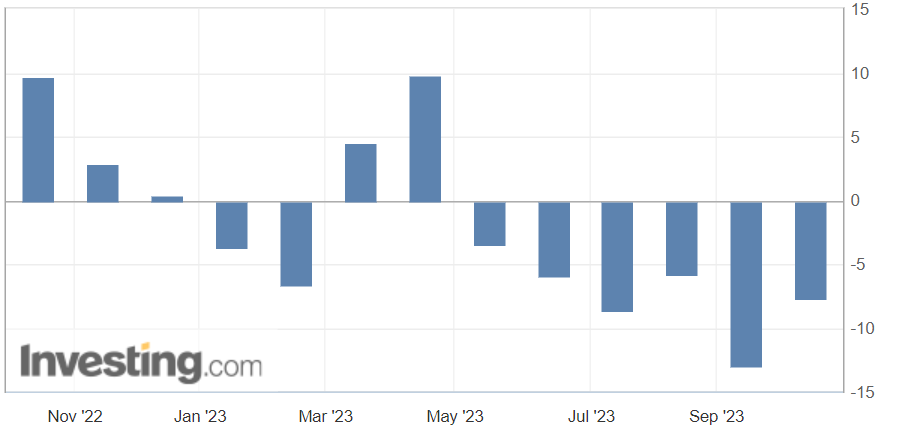

In Italy -4.2% per year – the 7th minus in a row and the 11th in the last 12 months:

Pic. 4

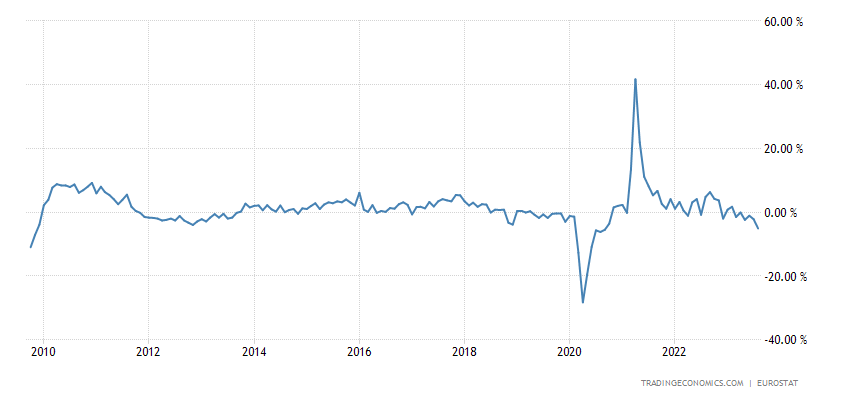

In the eurozone as a whole -5.1% per year – excluding 2020, this is the worst dynamics since 2009:

Pic. 5

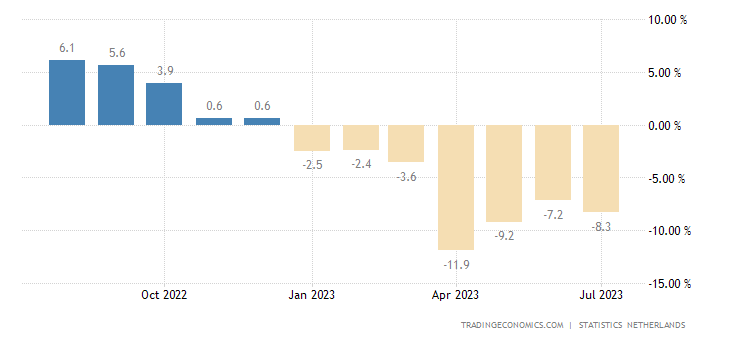

Dutch manufacturing output -8.0% per year – 8th negative in a row:

Pic. 6

There is a full-fledged structural decline in the European Union.

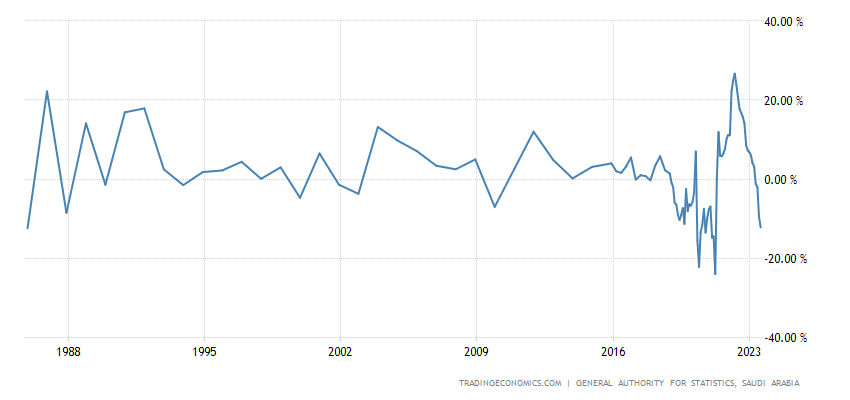

In Saudi Arabia, industrial production is -12.2% per year – not counting the failures of 2020/21. This is the bottom since 1986:

Pic. 7

Net engineering orders in Japan -7.7% per year – 6th negative in a row:

Pic. 8

The index of economic observers in Japan has entered the stagnation zone and is the worst in 8 months:

Pic. 9

As expected from the same review:

Pic. 10

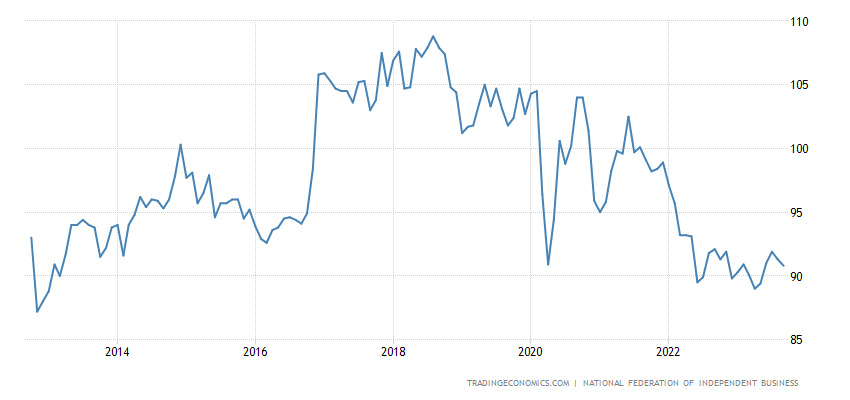

US small business confidence is the worst in 4 months, well below long-term averages and near more than 10-year lows:

Pic. 11

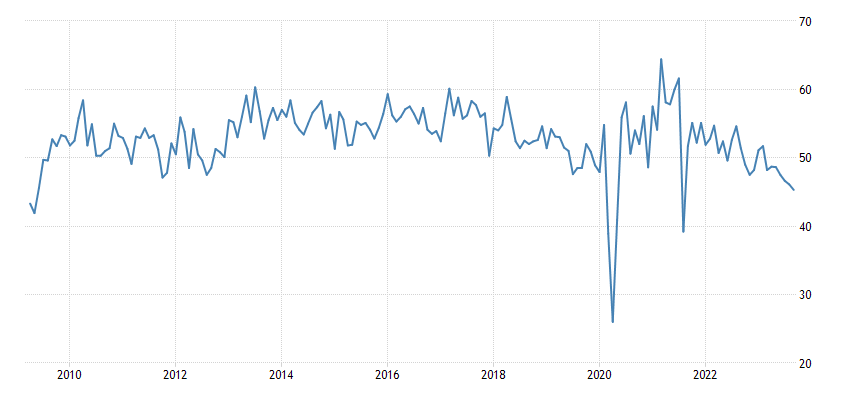

Manufacturing PMI (expert index of the state of the industry; its value below 50 means stagnation and decline) of New Zealand 45.3 – not counting Covid failures, this is the minimum since 2009:

Pic. 12

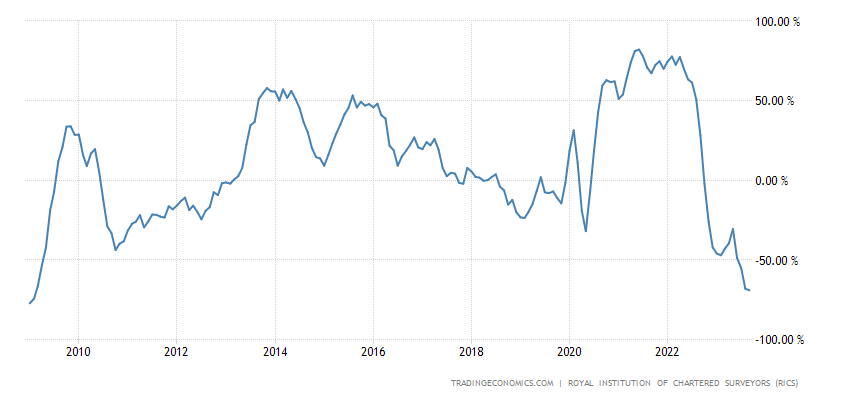

The balance of house prices in Britain (-69%) is the weakest in 14 years:

Pic. 13

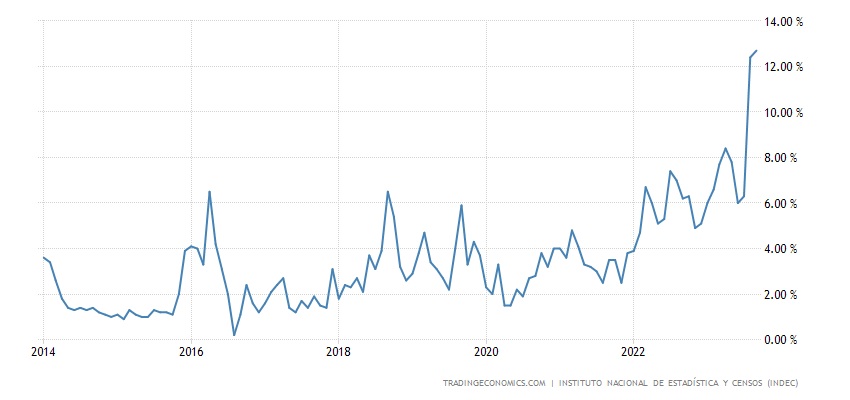

CPI (consumer inflation index) of Argentina +12.7% per month – a record for 10 years of observation:

Pic. 14

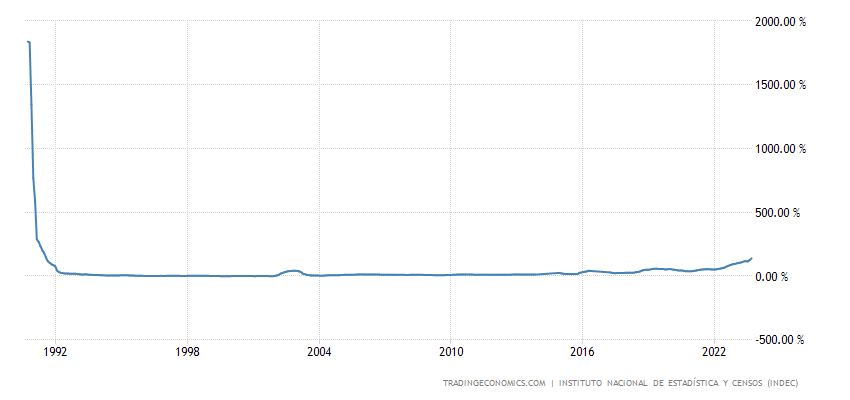

And 138.3% per year – 33-year top:

Pic. 15

The 30-year mortgage rate in the US reached a 23-year high (7.67%):

Pic. 16

Freddie Mac has similar data (7.57%, peak since 2000):

Pic. 17

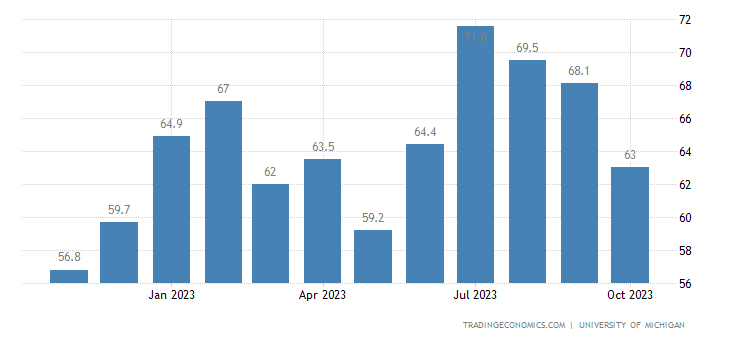

Americans are the most pessimistic in the last 5 months:

Pic. 18

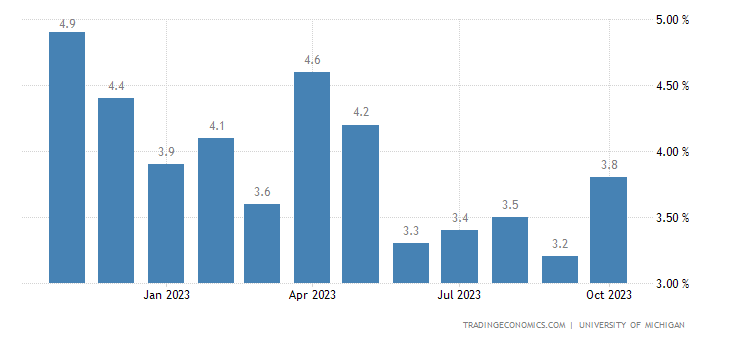

And their inflation expectations are at their peak over the same 5 months (+3.8% per year):

Pic. 19

Loans in China +10.9% per year – repeating the minimum since 2002:

Pic. 20

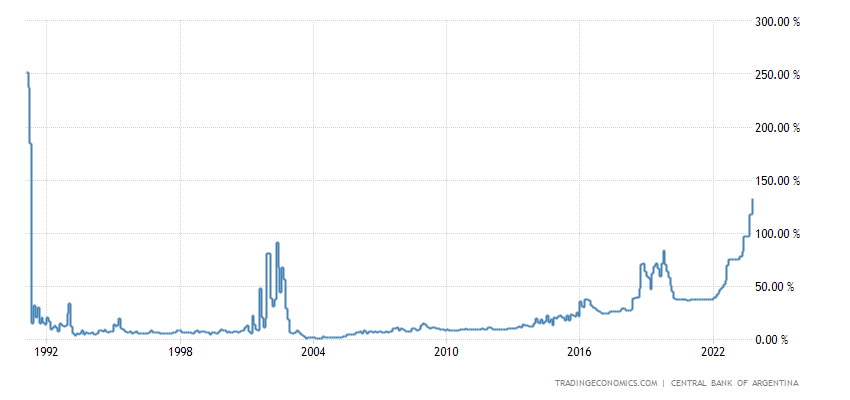

The Argentine Central Bank raised the rate by another 15 percentage points. up to 133%, a record since 1991:

Pic. 21

Main conclusions. The structural decline of the global economy continues. There are no grounds for optimism. The most interesting thing that could happen this week was inflation data in the US. Our favorite indicator, inflation for the full volume of industrial goods in annual terms (September to September) is -3.3%.

Deflation continues, although it is decreasing. The question arises: is this a general effect of rising prices or is industrial growth beginning? So far there are no signs of the latter, but who knows… We will monitor the situation.

As for the data on the CPI and PPI indices, they did not provide any real information. The level of core inflation for the month was, as in the month before, 0.3%, annual consumer inflation remained at 3.7%, core (minus highly volatile components) 4.1%. It seems not very much, but let’s not forget the systematic underestimation of this indicator using statistical methods.

The PPI index in September amounted to 2.2%, with a forecast of 1.6% and the previous value (August to August) of 2.0%. That is, there is a slight increase.

This data is not relevant enough, it does not provide information about what is happening in the economy. In addition, with a colossal increase in public debt (we wrote about this in the previous review), unexpected “outbursts” of money with a sharp increase in inflation are possible. And so here we agree with Powell: inflation data does not provide information about future developments. We disagree with him on another point: we believe that the structural crisis in the United States began in the fall of 2021 and is still ongoing. And it will continue.

Well, we wish our readers a pleasant weekend and a relaxing work week!