Big news – Elections in the US of course. But the main essence of these elections from an economic point of view is the choice of an economic development strategy (or, alternatively, degradation) for the United States and the rest of the world. Insofar as this world is still holding on to the Bretton Woods dollar system.

The “Biden team” has no positive scenario. This can be seen in the extremely nervous behavior of Powell (we discussed this issue in detail in the previous Review), and in the turmoil in the monetary system, and in the general trend in the movement of the American economy (see the next section of this Review). And the absence of a positive scenario (and, as a result, a political project for the Democratic Party as a whole; however, this is not entirely true for its individual representatives) means that the victory of the Democrats in the midterm elections only strengthens the US movement, both economic and socio-political into a deep and extremely viscous swamp.

As for the Republican Party, we have restored its economic program based on fragments of information and individual statements of various political figures. At the same time, we suspect that part of the Democratic establishment has joined this program. The essence of this program is that two fundamental changes have been made to the logic of Trump (“Make America great again”) about restoring the real sector of the US economy. The first is that the real sector of the economy needs to be raised not within the framework of the United States, but within the framework of AUKUS (meaning that the dollar currency area in terms of the book by A. Kobyakov and M. Khazin “The Decline of the Dollar Empire and the End of Pax Americana” will include the United States, Canada, UK, Australia and New Zealand).

The second is that in order for investments to go to the real sector, it will be necessary to “throw off” the financial liberal superstructure over the economy. Actually, this point was obvious both in 2016 and in 2020, but then Trump did not have the courage to voice this topic. By the way, even today it has not been publicly announced, but, judging by some leaks, it is being discussed among the American establishment.

Accordingly, the arrival of Republicans in the leadership of both houses of Congress would lead not only to political, but also to acute economic consequences. With the caveat that we may be wrong in reconstructing the thought of the national American establishment. And, of course, you may simply not have the courage.

From the point of view of such an analysis, the midterm elections simply do not have results. One House of Representatives is not enough to change economic policy, and the Republicans do not have a majority in the Senate. Since they have 50 senators so far, and the Georgia issue has been postponed to December, the Republican Party still has the opportunity to implement its maximum program (take both houses of Congress). But on the other hand, they already have the opportunity to do harm to any Biden programs, which only increases the viscosity and depth of the swamp mentioned above.

Accordingly, the crisis will continue as gradually and viscous as before. That is, the situation will worsen, but slowly and sadly.

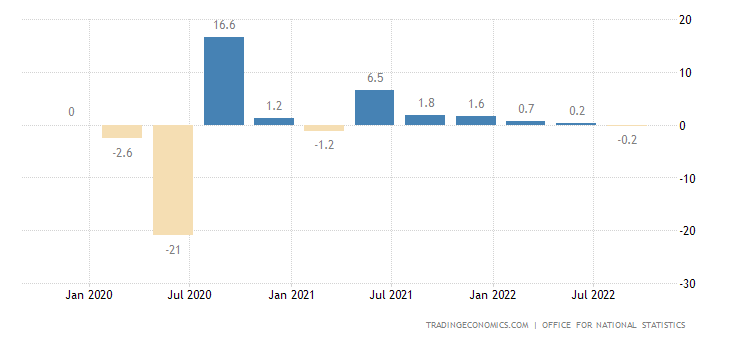

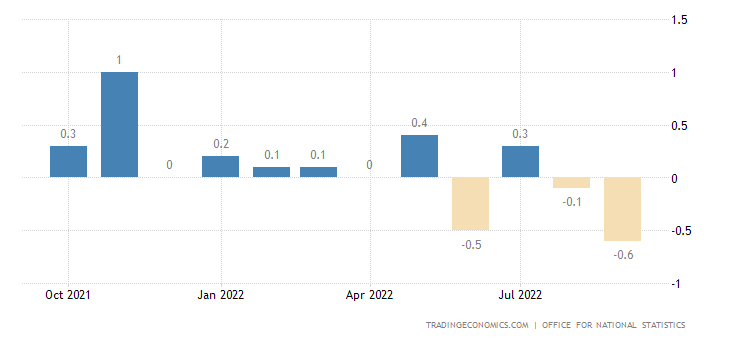

Macroeconnomics. UK GDP in Q3 went into the red (-0.2% qoq):

Separately for September -0.6% per month:

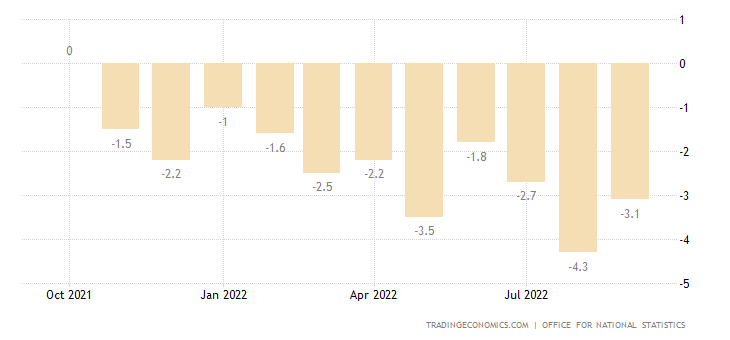

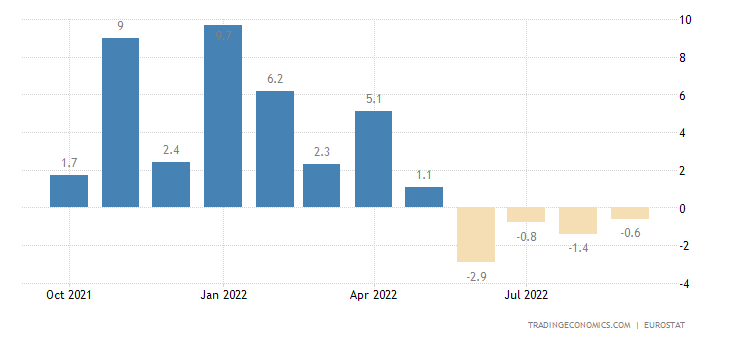

The annual dynamics of industrial output in Britain cannot show a single plus for a whole year:

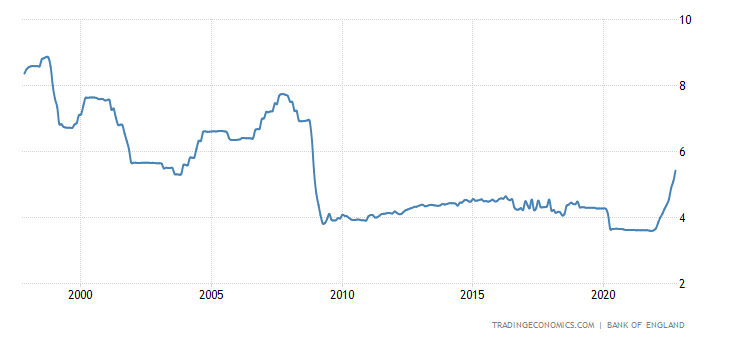

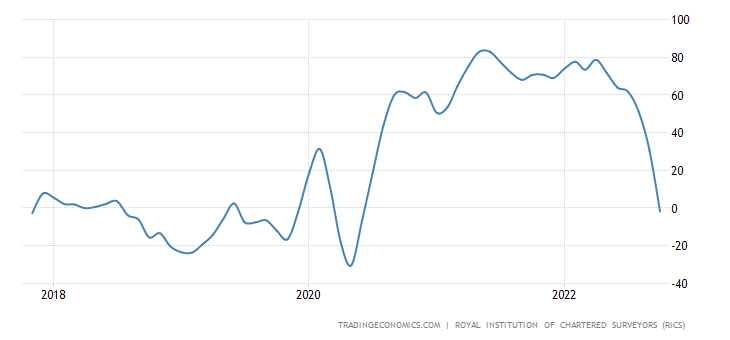

The average mortgage rate in Britain has reached a 14-year peak (5.42%):

Because of this, the balance of housing prices in Britain has sharply gone negative for the first time since the summer of 2020:

In Mexico, industrial production -0.2% per month for the 2nd month in a row:

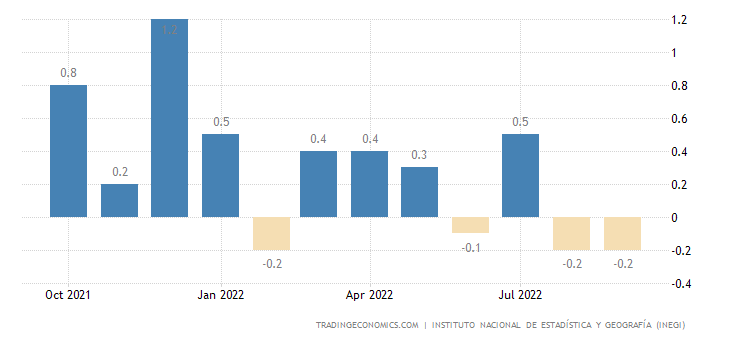

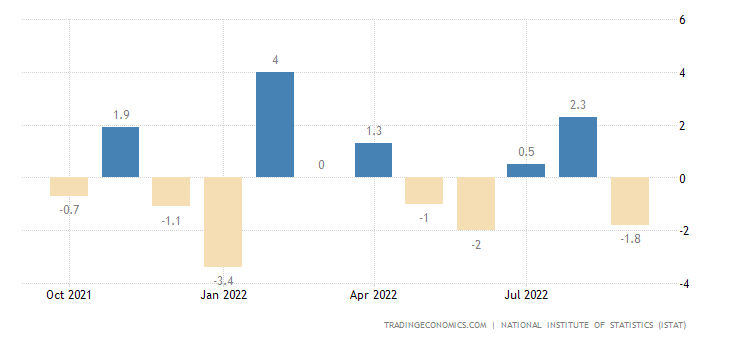

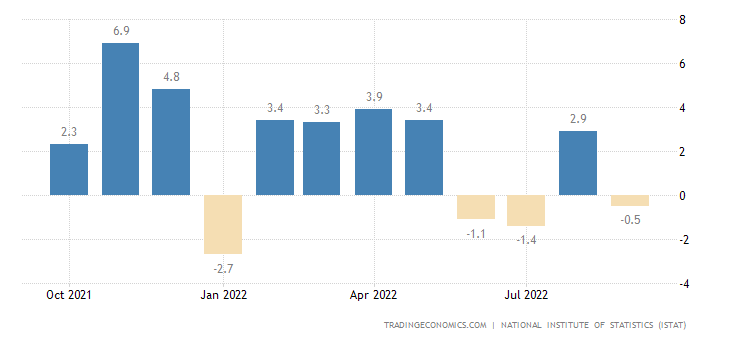

Industrial production in Italy -1.8% per month:

And -0.5% per year (3rd minus in the last 4 months):

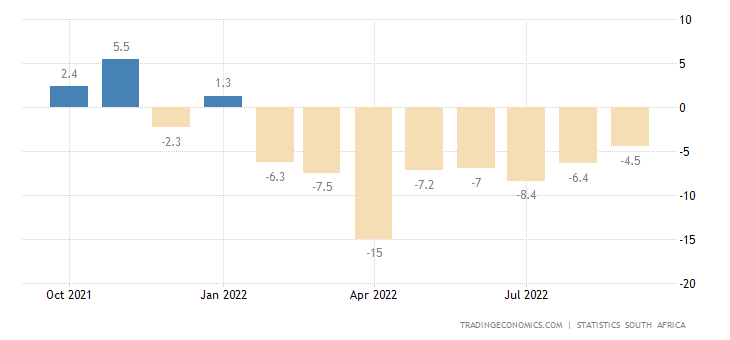

Mining industry in South Africa keeps in the red for 8 months in a row:

Business confidence in Australia worst in 10 months:

Construction PMI (expert index of the state of the industry; its value below 50 means stagnation and recession) of the eurozone in the depression zone (44.9), housing sector at the bottom for 2.5 years:

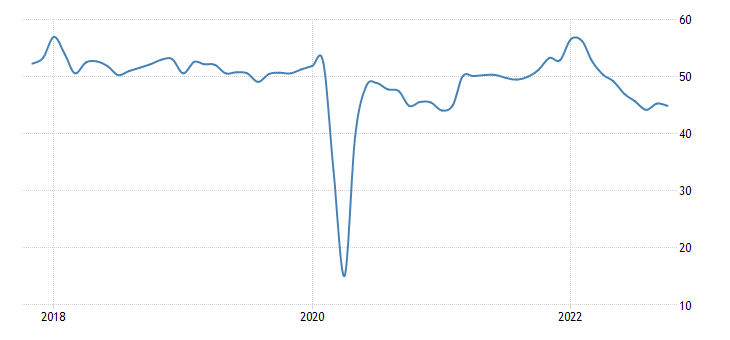

Japanese manufacturers sentiment weakest in 22 months:

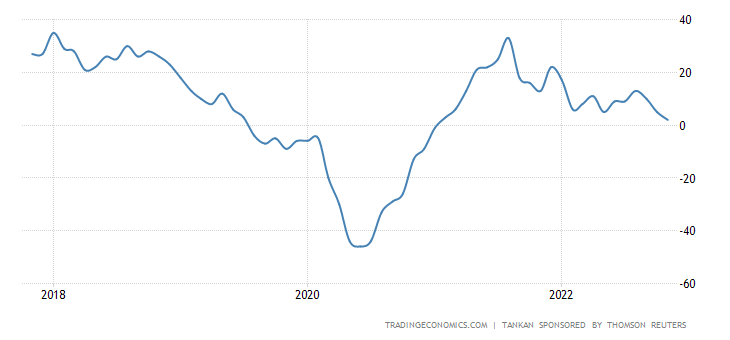

And the leading indicators in Japan are for 21 months:

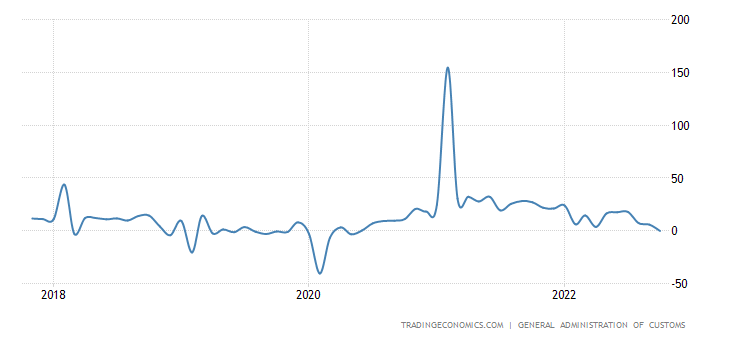

Annual dynamics of Chinese exports went negative for the first time in 2.5 years due to weak external demand:

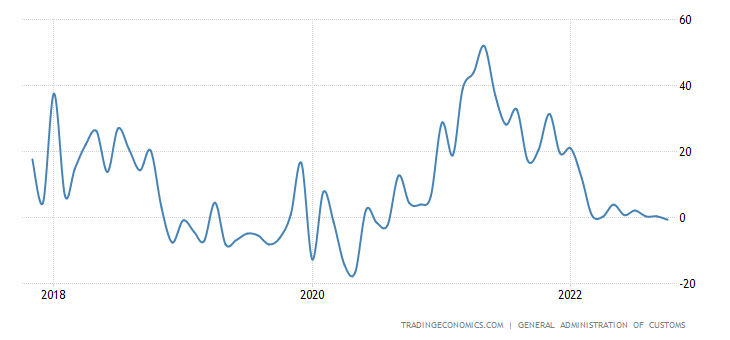

The dynamics of imports is also in the red – and also for the first time since 2020:

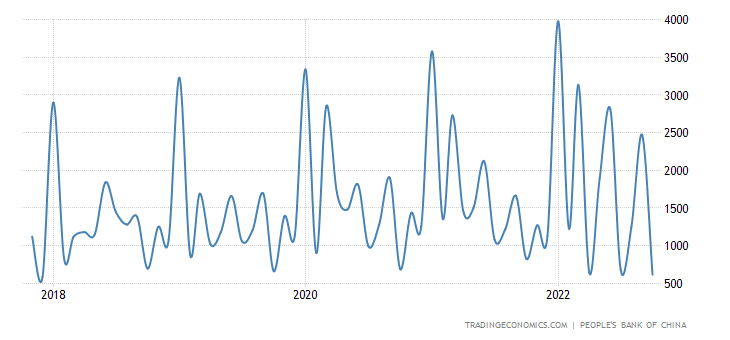

New lending in China weakest in 5 years:

France’s trade deficit is a record 53 years of observation:

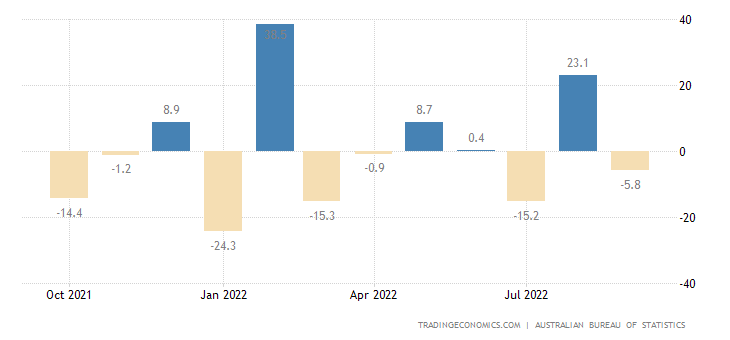

Building permits in Australia -5.8% per month and -13.0% per year:

In the US, mortgage rates (7.14%) are almost back to the top since 2001 (was 2 weeks ago: 7.16%):

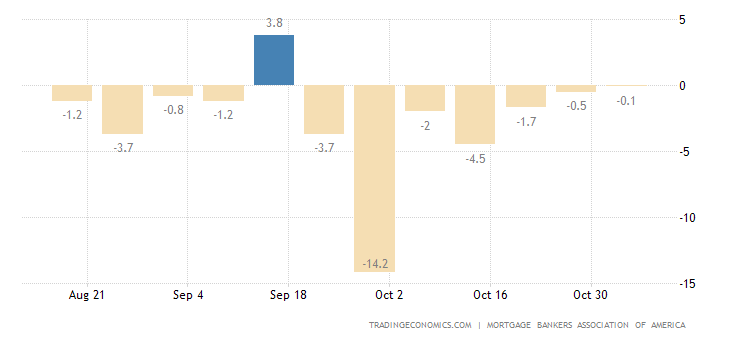

Why loan applications are down 7 weeks in a row (demand for refinancing fell 8 times in a year):

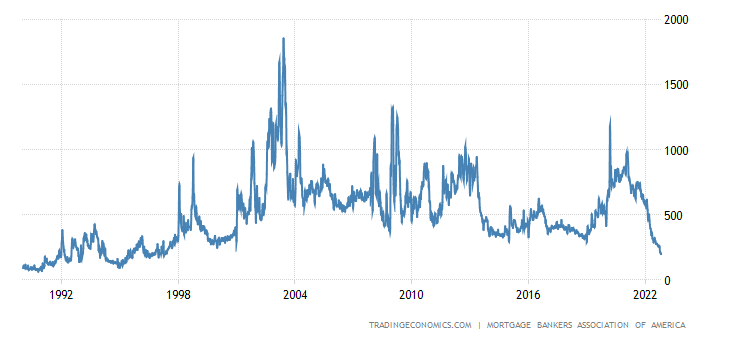

By updating the 25-year low:

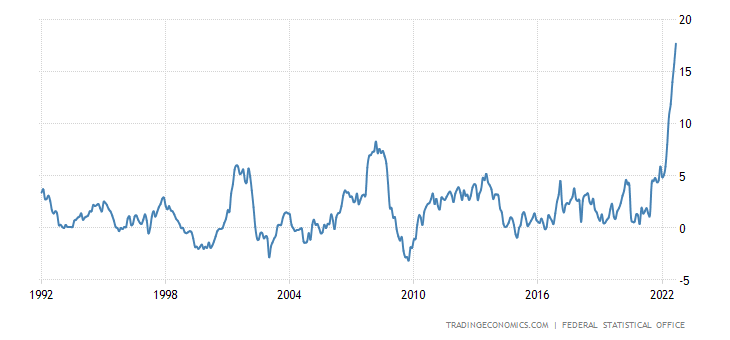

CPI (Consumer Price Index) Germany +10.4% per year – the highest in more than 70 years:

Including food prices +20.3% per year – a record peak in 31 years of data collection:

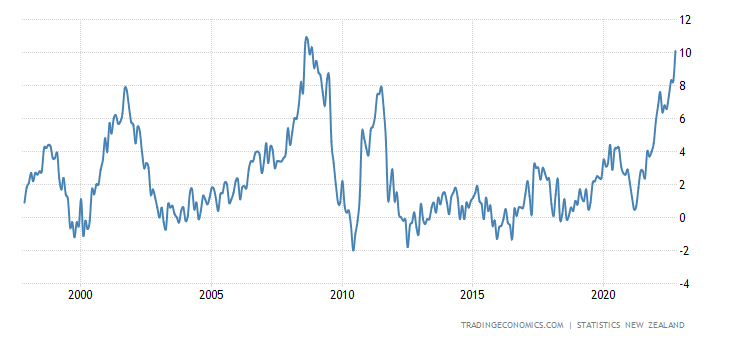

Food prices are also actively rising in New Zealand, + 10.1% per year – at the peak of 2008:

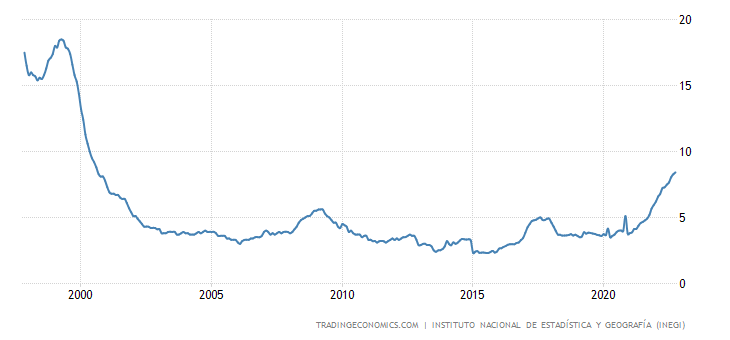

“Net” (minus prices for highly volatile components of food and fuel) Mexico’s CPI (+8.4% per year) is the highest since 2000:

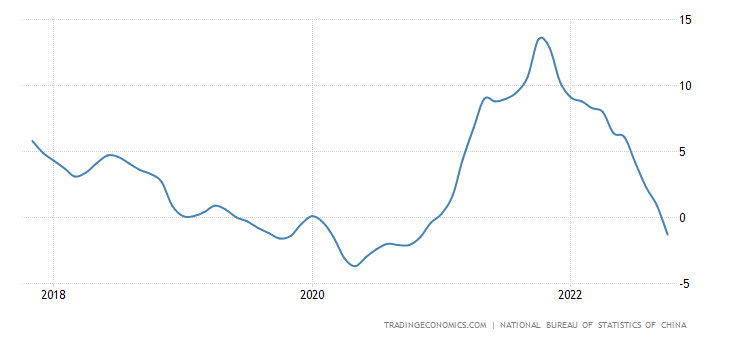

PPI (industrial inflation index) China -1.3% per year – 2-year bottom:

The volume of retail sales in the Eurozone keeps in the red for 4 months in a row:

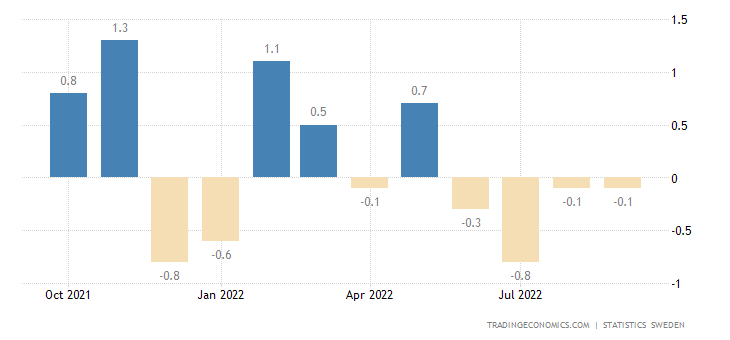

Household consumption in Sweden (-0.1% per month) has been declining for 4 consecutive months:

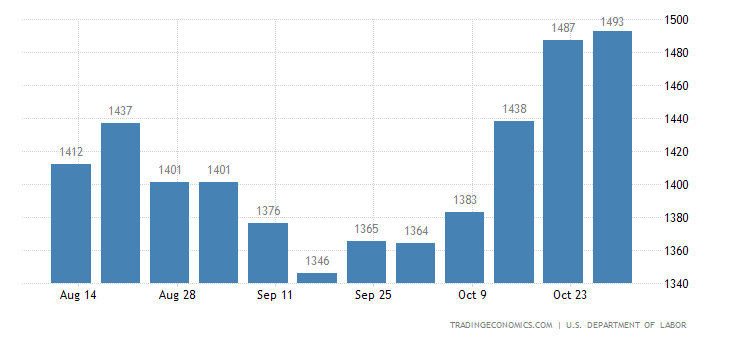

Number of U.S. Unemployment Claims in 7 Months Maximum:

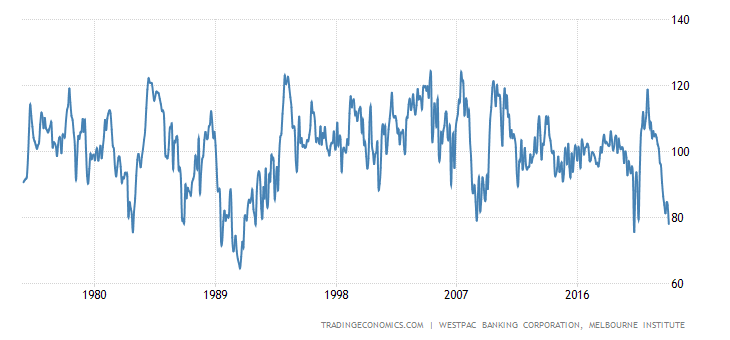

Australians are pessimistic for the most in 30 years (not counting the covid failure of 2020):

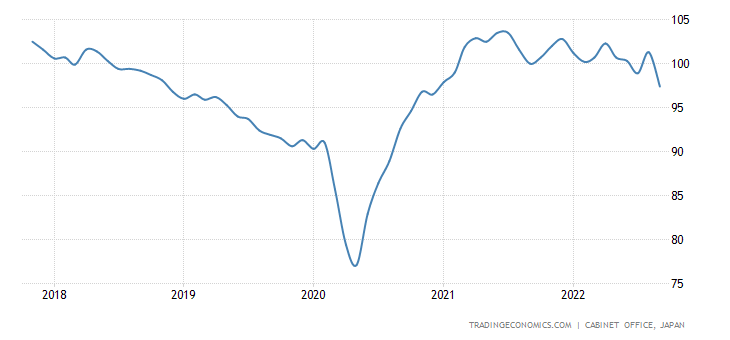

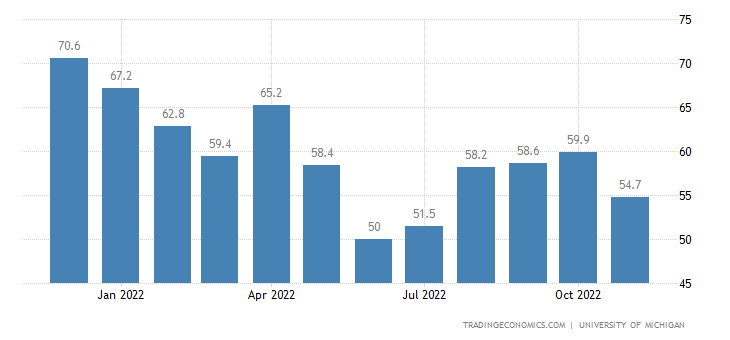

American sentiment began to deteriorate again (4-month low):

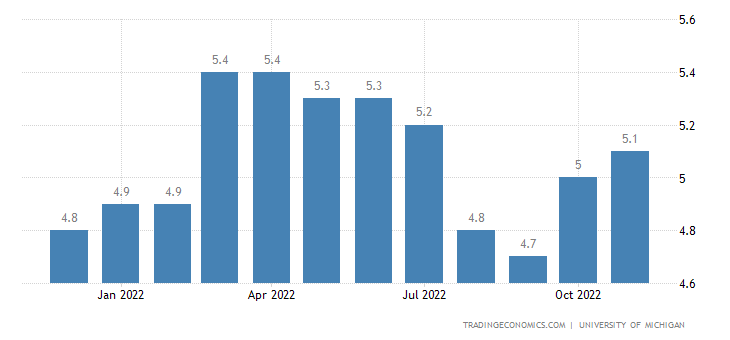

Against the backdrop of rising inflation expectations:

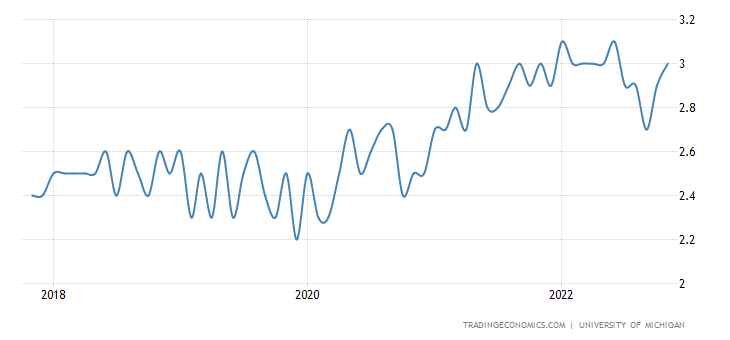

Including long-term:

The Central Bank of Mexico raised the rate by 0.75% to 10.00%.

Main conclusions. In general, as you can see, the economic picture of the world practically ignored the US elections. Of course, if the Republicans had won, the effect could have manifested itself (for example, in a collapse of the markets), but this hardly affected macroeconomic indicators. Incidentally, this is a typical pattern for structural crises, they react very weakly to political events.

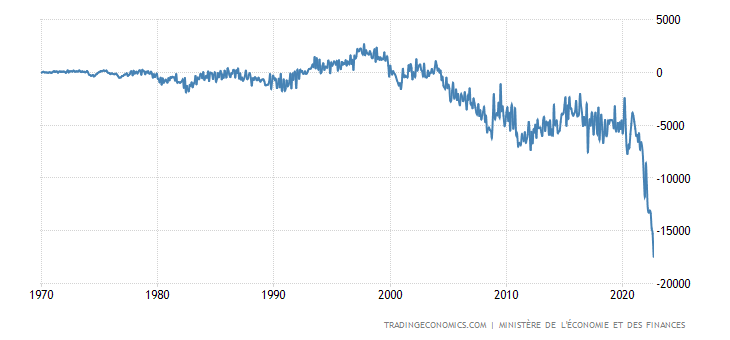

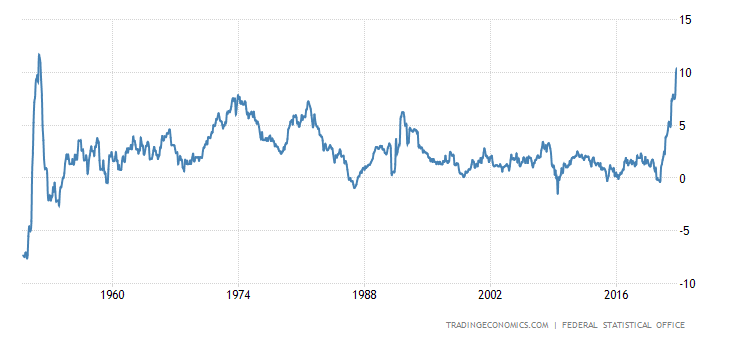

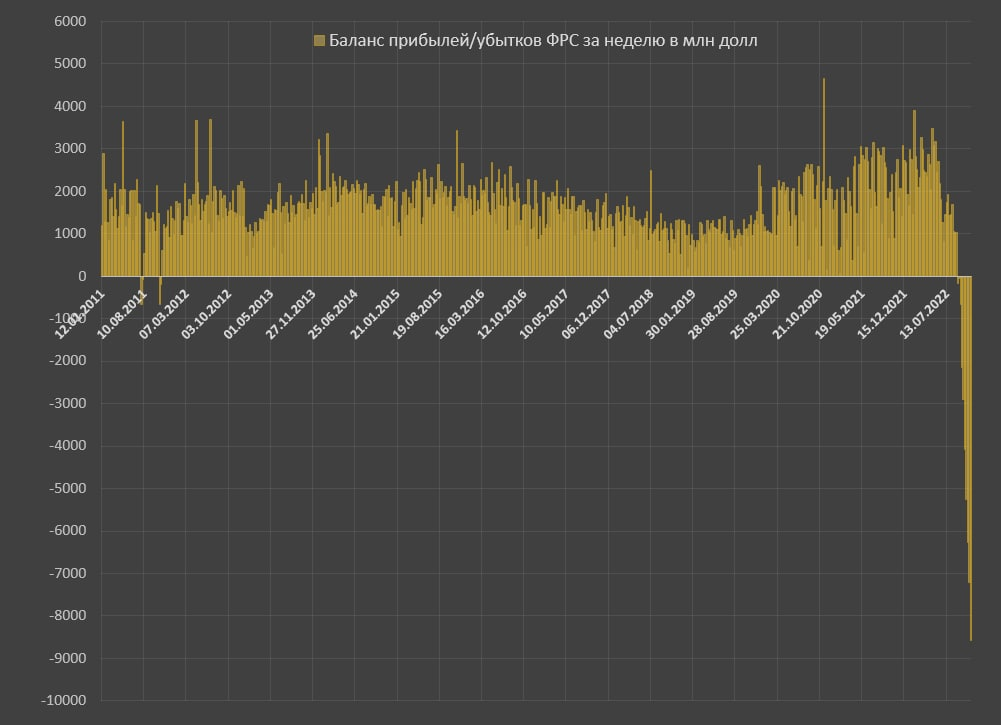

However, one event happened, we are talking about the profitability of the Fed as a market entity. As you can see from the picture below (for which we thank Pavel Ryabov, Spydell, it is taken from his telegram channel), the Fed has gone into deep loss:

This situation is understandable: the Fed’s income comes from securities sold at zero rates, and bank deposits placed with the Fed must be paid at the current rate. Recall that the discount rate is just the interest rate on such deposits.

Not that it was such a big money, but such a picture shows that banks do not want to give loans (the risks are too high, and the real commercial interest rate is frankly negative), so they at least reduced the risks of default to zero. And such a picture, by the way, shows why investments in the real sector are impossible without a “reset” of the financial system – banks in the current situation will not lend to the real sector.

We do not think that the picture of the crisis will fundamentally change. Yes, depending on the week, certain countries and/or industries can take the lead, new negative trends may appear. But there will be no quick collapse (which many experts already expect) in the current situation, at least until it becomes clear that the Republican Party will control both houses of Congress (which will become clear in December, and will be implemented by the end of January next year) and that she would risk going to the maximum program. Which is also not obvious.

In the meantime, we believe that our readers can safely continue their work, since we exhaustively explain the general picture of the world in our reviews. And we wish them a cloudless weekend and a productive working week!