November 18-24, 2023

Big news. The big news comes not from specific statistics, but from the appearance of an article by Ruchir Sharma (Ruchir Sharma is an investor, writer, fund manager and columnist for the Financial Times. He is the head of international business at Rockefeller Capital Management and was an emerging markets investor at Morgan Stanley Investment Management) in F.T.

“The Chinese economy’s decades-long period of enormous growth has finally come to an end,” wrote Ruchir Sharma in the Financial Times.

The world’s second-largest economy now accounts for a smaller share of global GDP.

“In a historic turn, China’s rise as an economic superpower is being reversed. The biggest global story of the last half century may be over,” said the chairman of Rockefeller International.

In nominal dollar terms – which Sharma believes is the most accurate measure of an economy’s relative strength – China’s share of global GDP began to decline in 2022 as strict zero-Covid measures remained in place for much of the year.

Despite expectations for a strong recovery, China’s share will continue to fall in 2023, reaching 17%. That puts China on track for a two-year decline of 1.4 percentage points, a decline not seen since the 1960s and 1970s, when Mao Zedong presided over a weak economy, he added.

… In 1990, China’s share of the global economy was less than 2%, but by 2021 it has skyrocketed to 18.4%. Sharma noted that such rapid growth has never been seen before.

But with the current downturn, China will not be responsible for the growth of global GDP over the past two years, a total increase of which is estimated at $113 trillion.

“The decline of China could change the order of the world,” Sharma said. “Since the 1990s, the country’s share of global GDP has grown mainly at the expense of Europe and Japan, whose shares have remained more or less stable over the past two years. The gap left by China has been filled mainly by the US and Japan and other developing countries.”

India, Indonesia, Mexico, Brazil and Poland will account for half of emerging market growth, he added later, calling it “a strong sign of a possible power shift in the future.”

For its part, Beijing has maintained its annual growth target at 5% and expects to achieve it this year. The forecast is supported by the International Monetary Fund, which forecasts economic growth of 5.4% in 2023.

But Sharma rejects the use of real GDP growth as a measure, saying it leaves room for Chinese authorities to adjust the figures to suit their forecasts and hide the possibility of a slowdown. In nominal dollar terms, the country’s GDP will fall this year.”

We have been monitoring the situation in the Chinese economy for many weeks and noted in one of our previous reviews that a serious economic crisis has begun in this country. Actually, it had to begin, since the United States and China, from an economic point of view, represent two sides of the same coin, and in the United States, an active structural crisis has been going on since the beginning of autumn 2021.

However, the fact that this topic was raised so loudly seems to be a very interesting circumstance. It is clearly of a political nature, since the economic argument does not stand up to criticism. Indeed, growth of 5% is a lot, given the recession in the US and EU. India, Indonesia, Poland and Brazil do not have such growth rates, and China in such a situation simply cannot help but increase its share in the world economy.

One can, of course, assume that in reality everything is not so good for China (which we wrote in previous reviews), but this means contradicting the data of the key Bretton Woods institutions. The author clearly did not have enough strength for this, so the distorted static information greatly limits him. Although he makes various hints to explain this.

But if we suppose that his real task is to convince speculators that China’s problems do not threaten world markets, since China is already falling significantly, even if this does not correspond to formal figures, then the article finds its explanation. In fact, it can be assumed that the United States is going to actively limit China’s economic influence in the world and is trying to convince financial market participants that this will not lead to critical consequences.

Well, forewarned is forearmed!

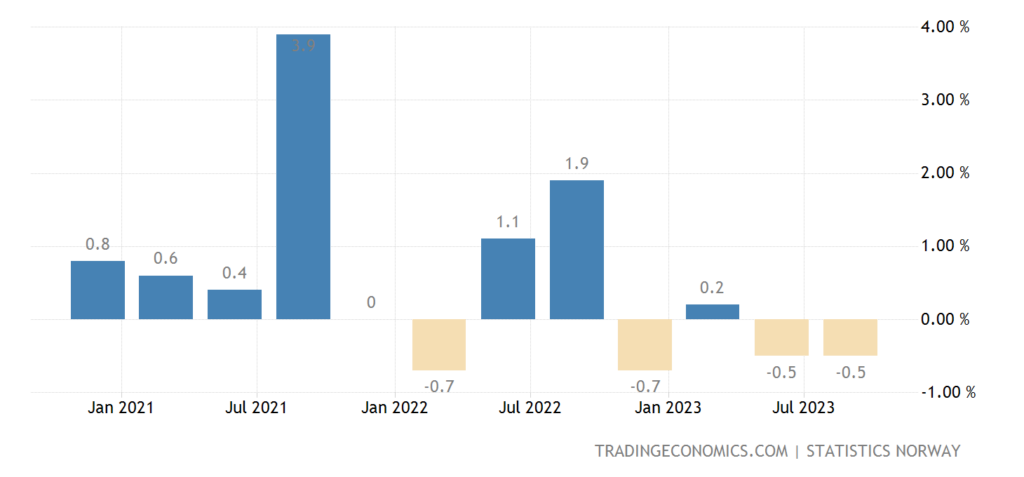

Macroeconomics. Norway’s GDP -0.5% quarterly after a similar decline in the previous quarter:

Рис. 1

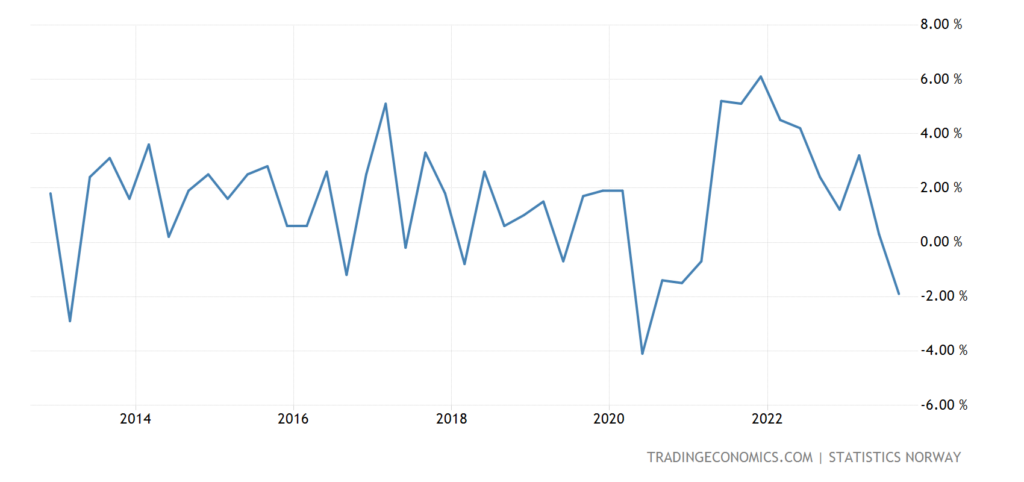

And -1.9% per year – not counting Covid, the worst dynamics in 11 years:

Рис. 2

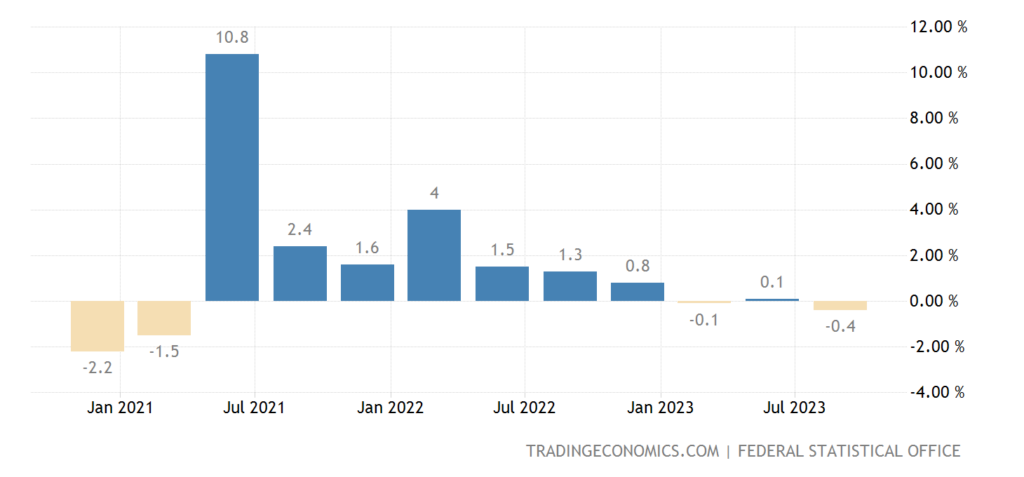

German GDP -0.4% per year – bottom for 2.5 years:

Рис. 3

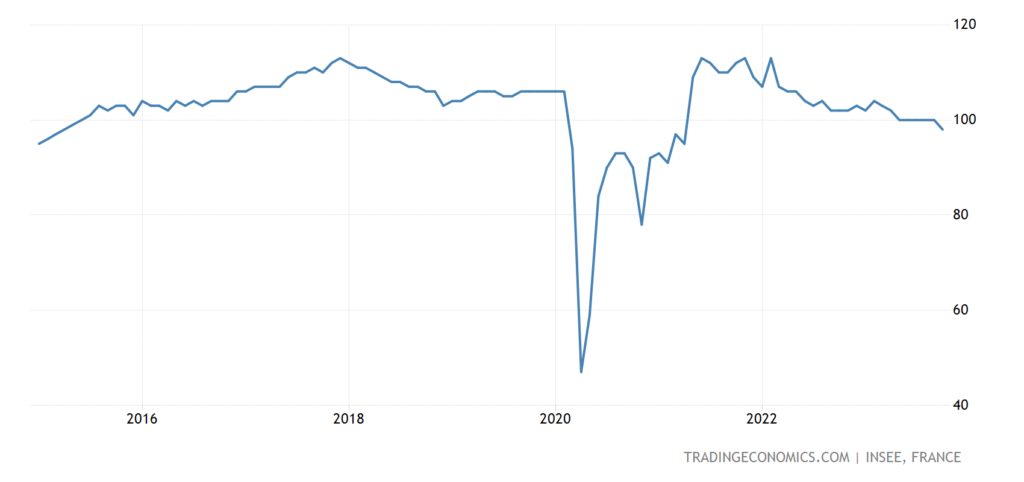

The business climate in France (excluding the failure of 2020) is the worst in 8 years:

Рис. 4

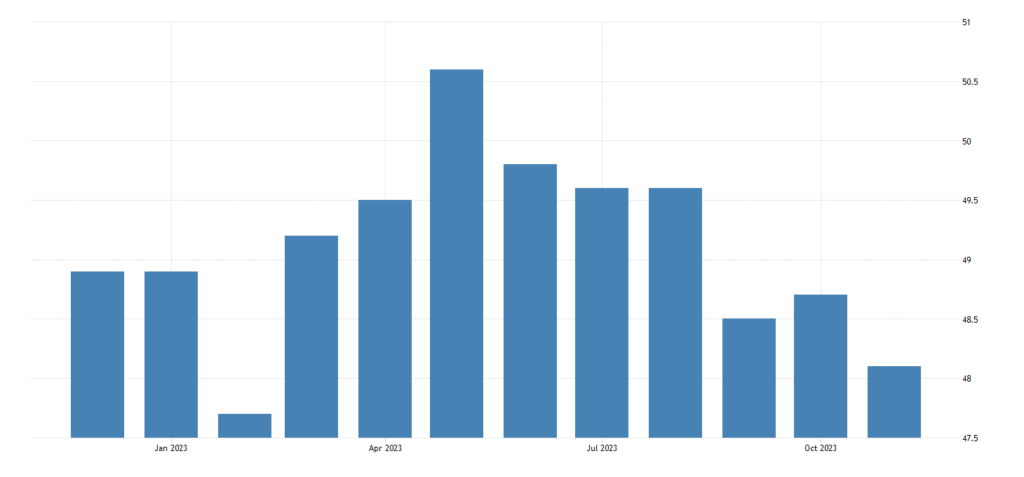

Its manufacturing PMI (an expert index reflecting the state of the industry; its value below 50 means stagnation and decline) (42.6) is the weakest since May 2020, and excluding Covid, it is a record low:

Рис. 5

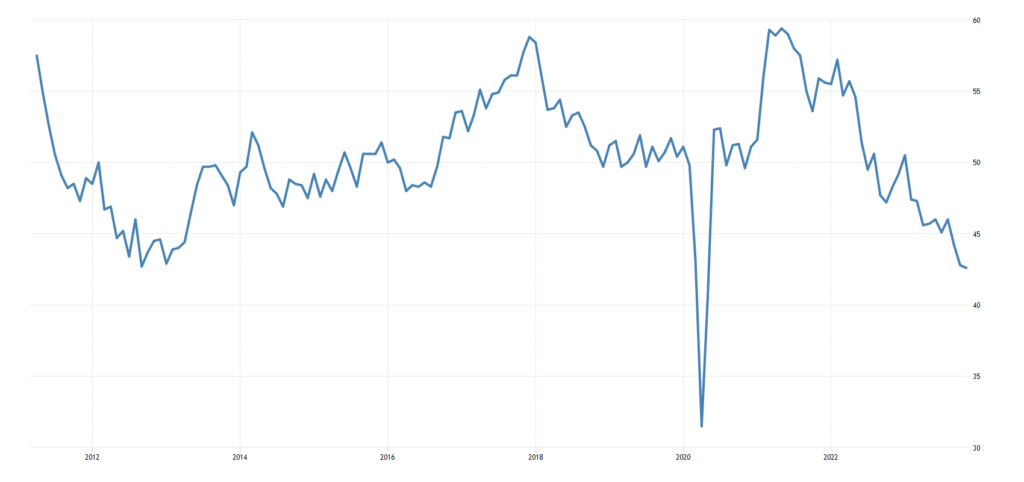

Japan’s PMI is at its 9-month low:

Рис. 6

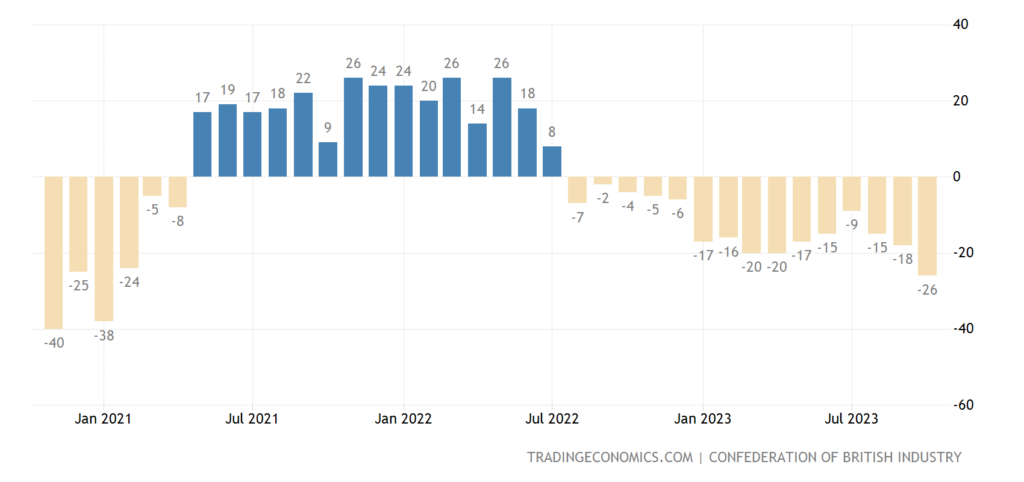

The balance of industrial orders in Britain has been negative for 16 months in a row, the worst in 3 years:

Рис. 7

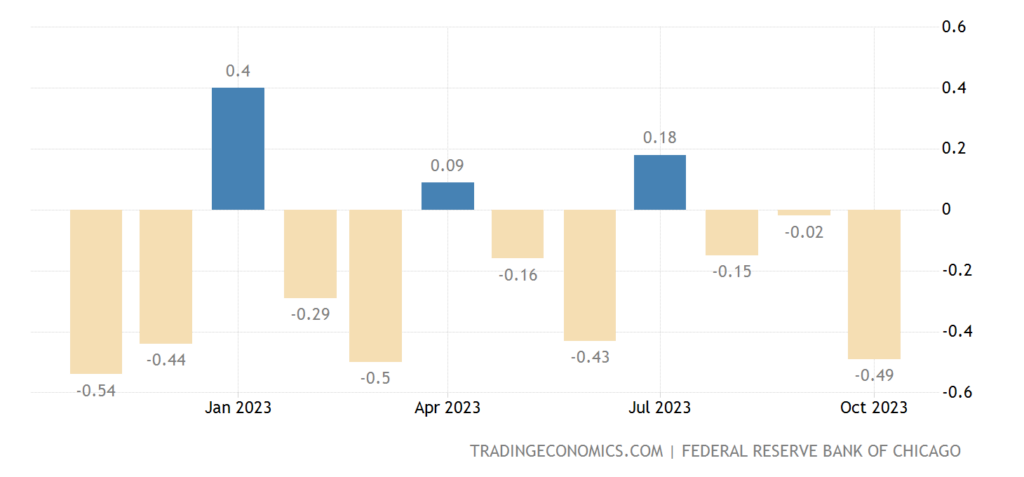

The US National Activity Index from the Chicago Fed is the weakest in 7 months, remaining in the negative for 3 months in a row:

Рис. 8

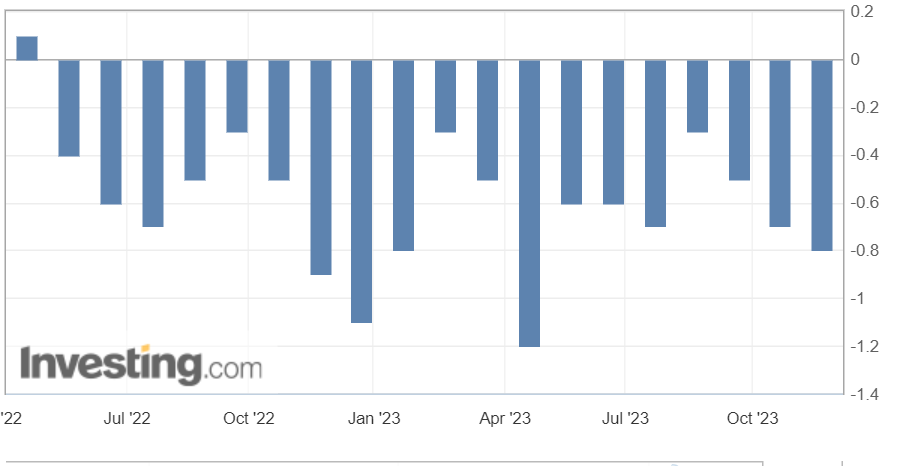

Leading indicators in the US -0.8% per month – 19th minus in a row:

Рис. 9

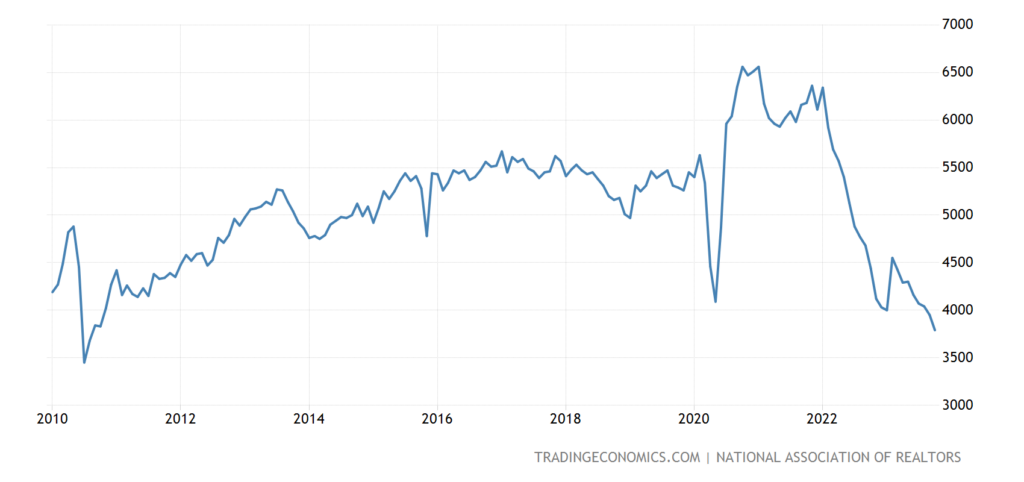

Existing home sales in the US are the lowest in 13 years:

Рис. 10

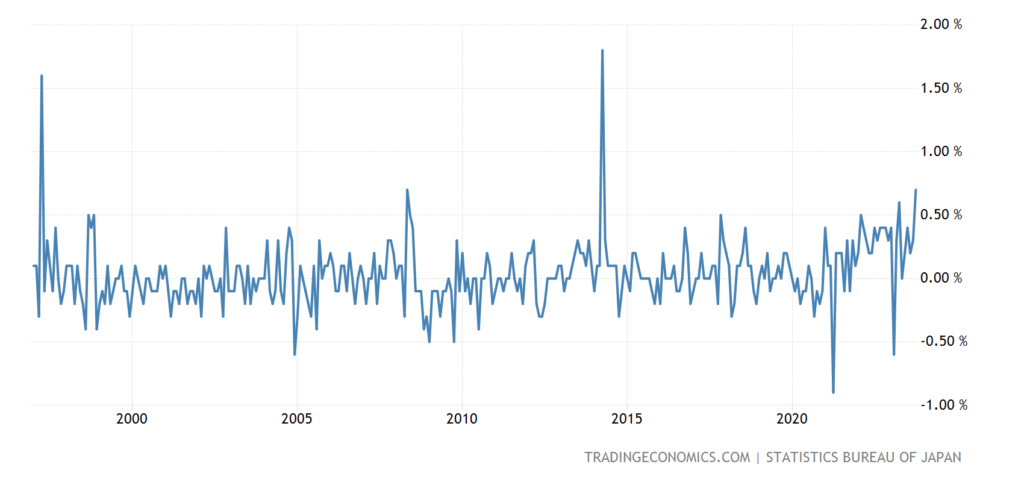

CPI (consumer inflation index) of Japan +0.7% per month – it was higher only in 2014, and before that – in 1997:

Рис. 11

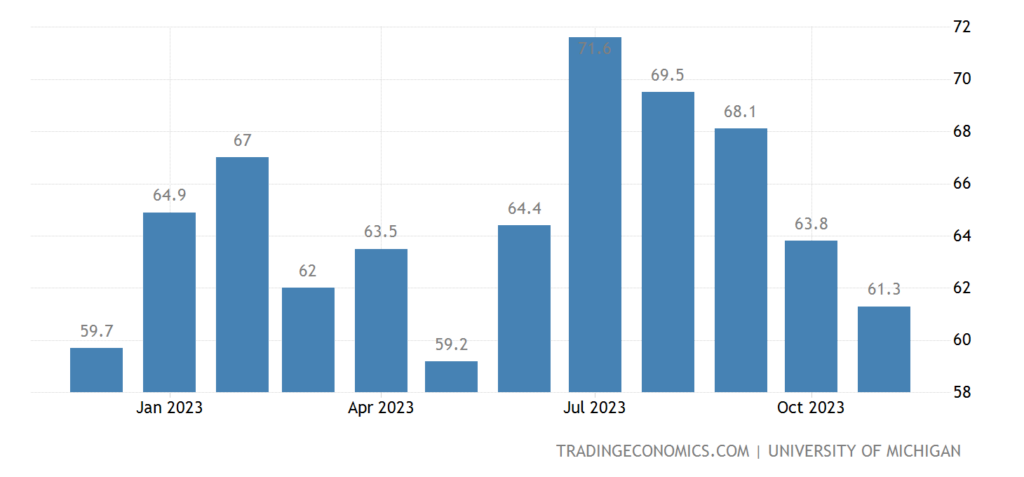

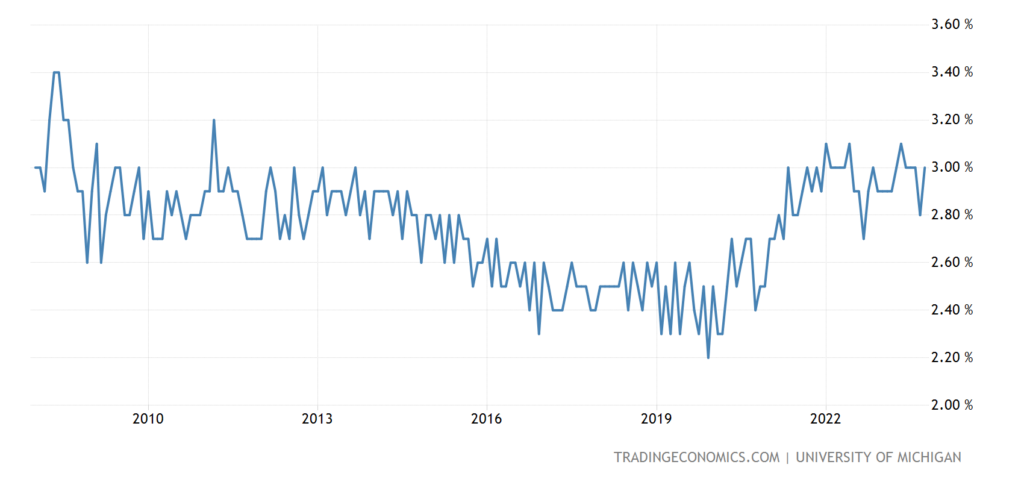

American consumers are the most pessimistic in six months:

Рис. 12

And their 5-year inflation expectations are the strongest in 15 years (+3.2%):

Рис. 13

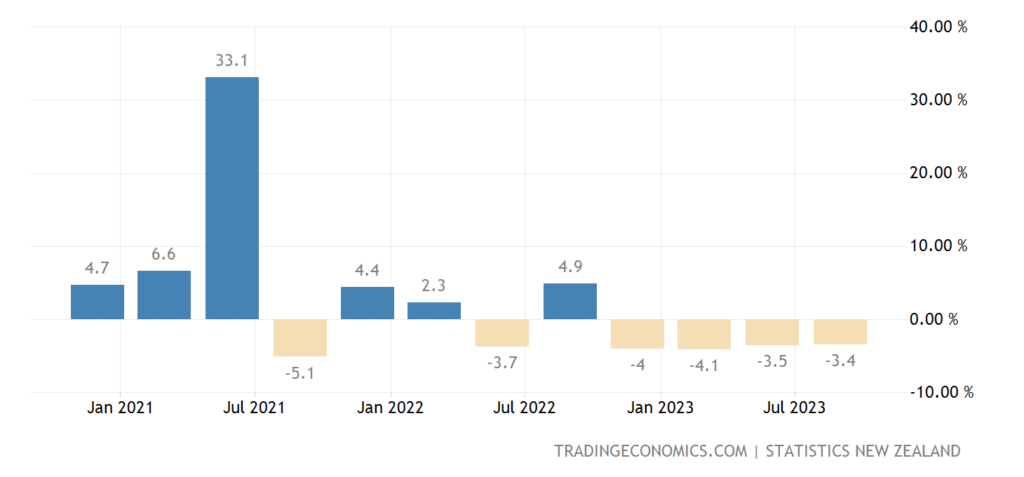

New Zealand retail sales -3.4% annually – 4th consecutive quarter of decline:

Рис. 14

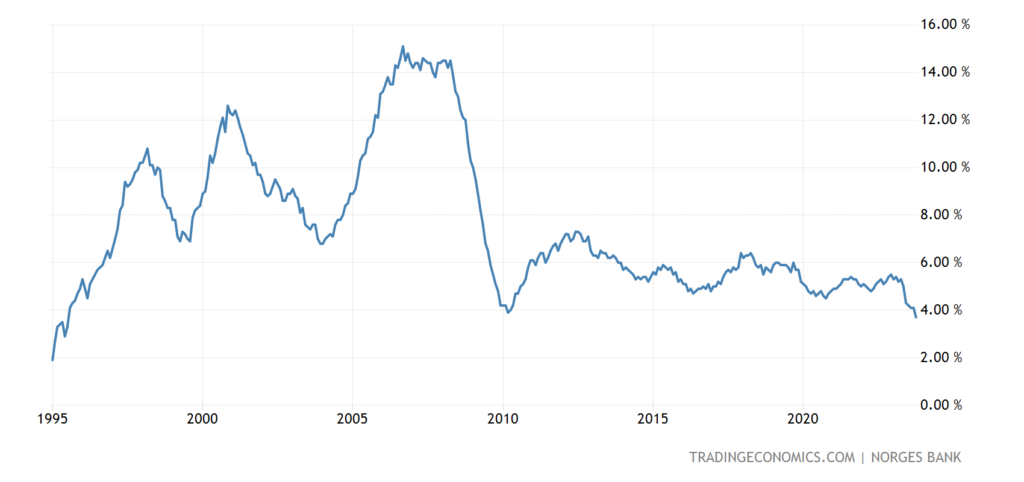

Loans in Norway +3.7% per annum – 28-year low:

Рис. 15

The Central Bank of China left its monetary policy unchanged, as did the Central Bank of Indonesia, the Central Bank of Sweden and the Central Bank of South Africa.

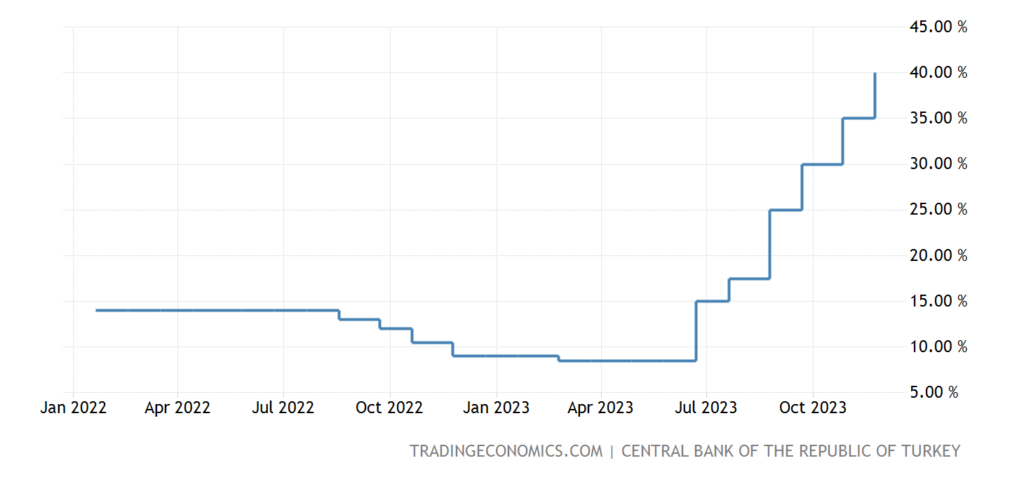

The Turkish Central Bank raised the rate by 5% to 40%:

Рис. 16

However, given the scale of inflation, this decision will clearly not lead to success.

Main conclusions. If we assume that the FT article is not an accident, then we can expect a sharp increase in trade wars, between the US and China in the first place. This is fully consistent with the strategic line that we outlined for the United States in previous reviews, but the question of the timing of its start was open. It is possible that the article mentioned in the first section of the Review is a symptom that this war will begin at the very beginning of 2024.

Everything else is pretty usual. The structural crisis continues and no signs of improvement are visible. So the US’s haste is understandable: the longer it waits, the worse the situation will be when it will have to start a fight for the markets of Southeast Asia.

In addition, as usual, Pavel Ryabov’s analysis of the US real estate market.

“The crisis in the US real estate market is growing – sales on the secondary market are reaching a 40-year low and an absolute minimum in terms of population.

As of September 2023, 3.79 million homes were sold in annual terms – the minimum since 2010, when tax breaks were canceled, which is 35-40% lower than average sales from 3Q20 to 4Q21 and 30% less than sales volume from 2017 to 2019.

If we adjust sales per capita, current activity in the secondary real estate market is 55% lower than the maximum in 2005-2006 and is the minimum for the entire period of statistics.

New home starts/primary real estate starts are 25% lower than construction at its peak in 2021 and 35% lower than the pre-crisis peak in 2006, although still 15% above the 2017-2019 average due to fairly low supply in the market , which smoothes out the effect of the crisis.

According to Zillow (the most rapid indicator of real estate prices), real estate values have been growing for the seventh month in a row, which made it possible to compensate for the fall in prices in the second half of 2022 and achieve positive annual dynamics (+1.8% y/y).

The weighted average price of residential real estate is almost $350 thousand (historical maximum), which is 40-42% higher than the level before the COVID crisis.

The situation is absurd – prices rise when sales fall, which is associated with inflation processes (real estate as an opportunity to save savings from depreciation), a shift in demand towards expensive real estate (increases the average price) due to the activity of wealthy buyers and a fairly low supply volume (cumulative effect low volume of construction over the past 15 years).

Taking into account inflation, current prices are only 2-3% above the 2006 bubble high, and at par they are 68% higher.

With a property value of $350 thousand, a 20% down payment and a 30-year mortgage at 7.8%, the average monthly loan payment was $2 thousand excluding taxes and insurance, and in 2019, with a property value of $245 thousand and rates of 3.6%, the payment was $890.”

In general, the specific market fully confirms the overall picture of the crisis. We do not rule out that, as happens with a structural downturn, the problems in the real estate sector will stop (even, perhaps, there will be a small compensation), but at the same time it will sharply intensify in other industries.

Another thing is that with a correct understanding of the ongoing processes, they can be used to benefit a specific business. Therefore, we are calm for our readers who understand the processes taking place in the global economy. And they, in turn, can relax on the weekend with pleasure and confidently start the work week!