Period: May 9-15, 2020

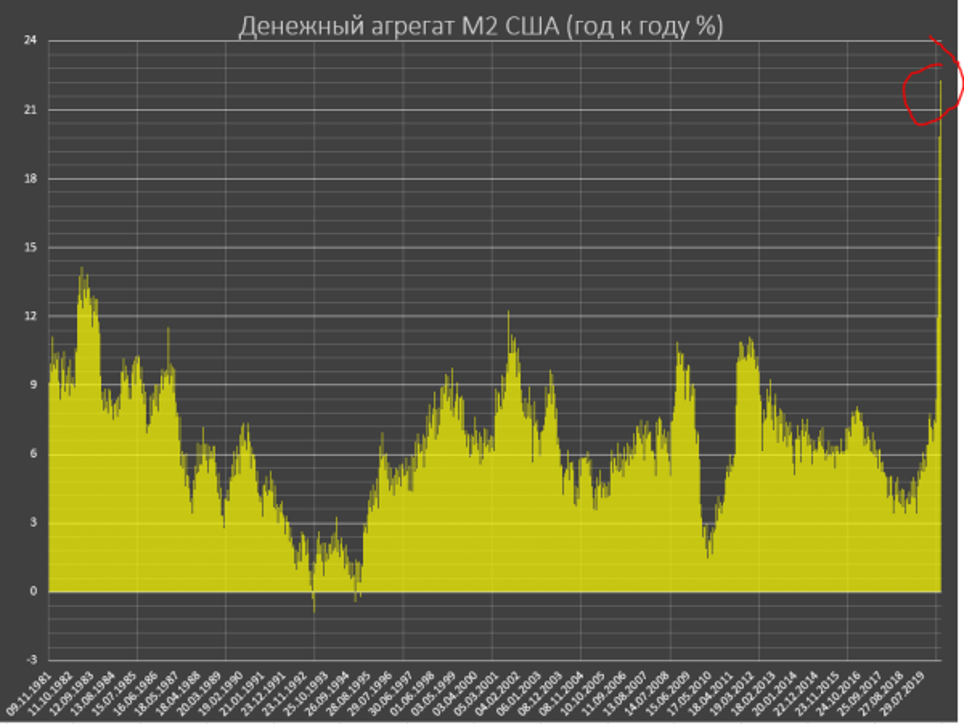

Main topic: Acute deflationary trends in the United States combined with a unique scale of money injection.

This combination of factors indicates a fundamental change in both consumer behavior and the basic patterns of entrepreneurial behavior.

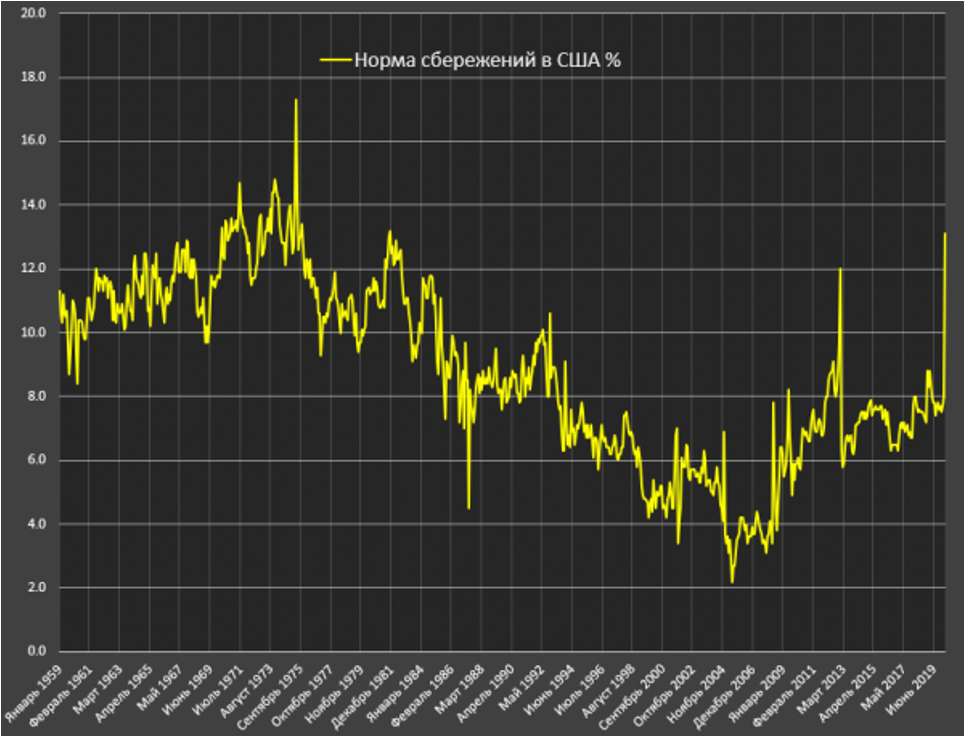

In particular, savings rose sharply, although due to the closure of stores, this figure is too early to evaluate.

Macroeconomics

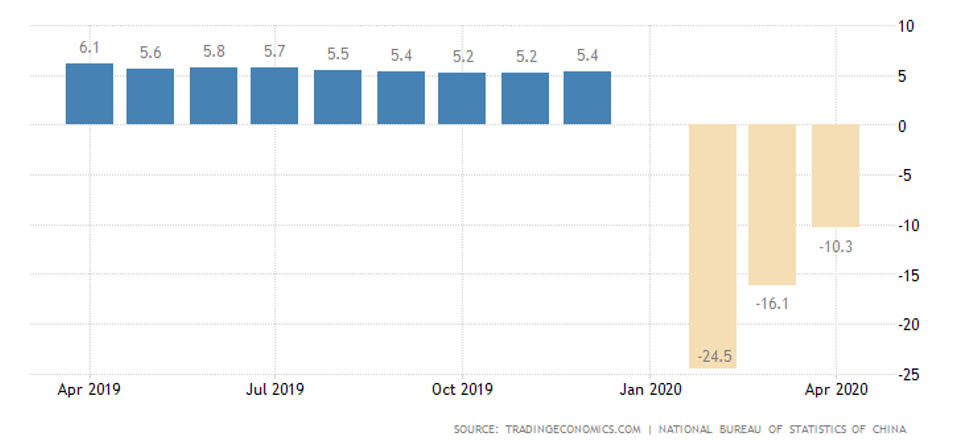

China’s investment and industrial production are recovering – but retail remains deeply in the red:

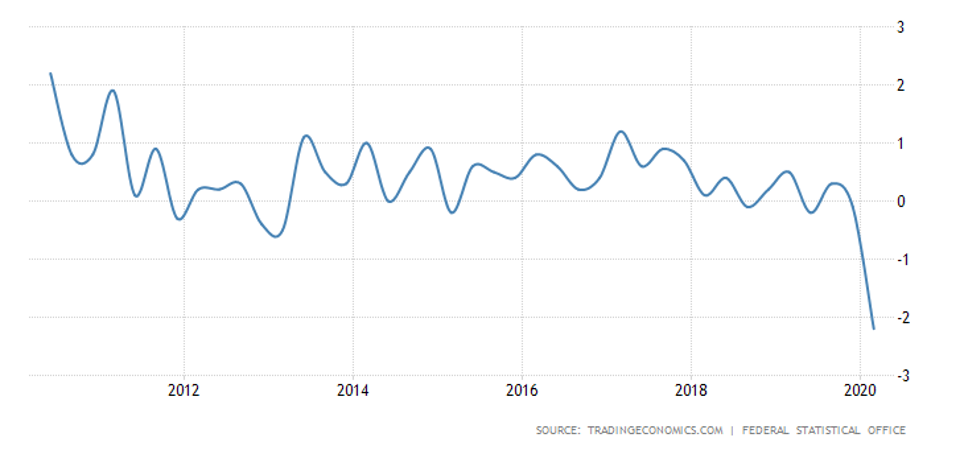

Germany’s GDP has fallen at the worst rate since 2009:

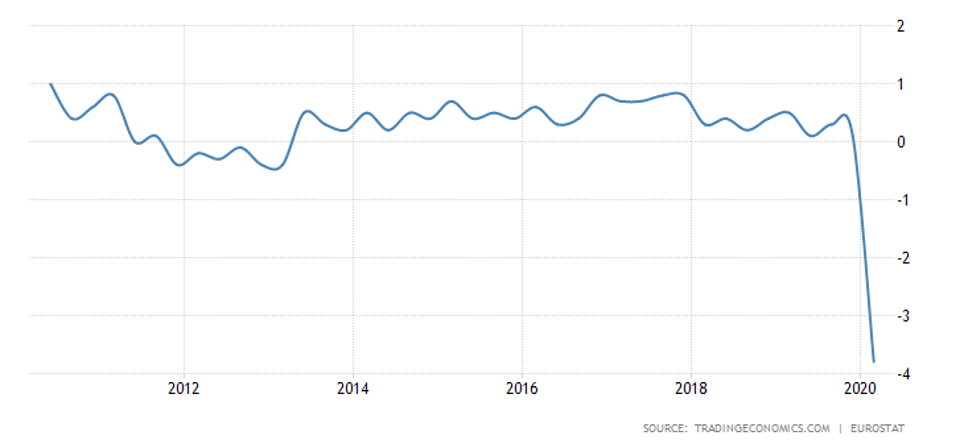

And Eurozone GDP as a whole even surpassed the 2009 collapse:

Britain’s GDP has the worst dynamics since the end of 2008, the annual change is the weakest since the end of 2009. In March, industrial output in Britain fell by 4.2% per month – the bottom since the late 1970s, the annual dynamics are the weakest since August 2009 (-8.2%). A similar situation is in manufacturing industries (-9.7%).

Industrial production in Italy in March collapsed by 28.4% per month – a minimum in 60 years of observation. Annual dynamics (-29.3%) are the worst in the history of the review since 1991.

In general, in the Eurozone it is -11.3% per month (anti-record for 30 years of observations) and 12.9% per year (minimum since August 2009).

Mexico’s industrial production in March fell 5% per year – a 10-year low. In India, -16.7% is a historical anti-record since 1994.

In the USA, industrial production collapsed by 11.2% per month (minimum since 1946) and 15.0% per year (since 2009). The same picture is in the manufacturing sectors (-13.7% and -18.0%). Capacity utilization is the worst in 53 years of observation (64.9%).

Sales in Canadian manufacturing fell 9.2% per month in March – a repeat of the record in 39 years of observation.

Orders for machine tools and equipment in Japan at a 10-year bottom; the annual decline is almost twofold.

Leading indicators of Japan at the bottom since June 2009, coinciding indicators are minimal since June 2011.

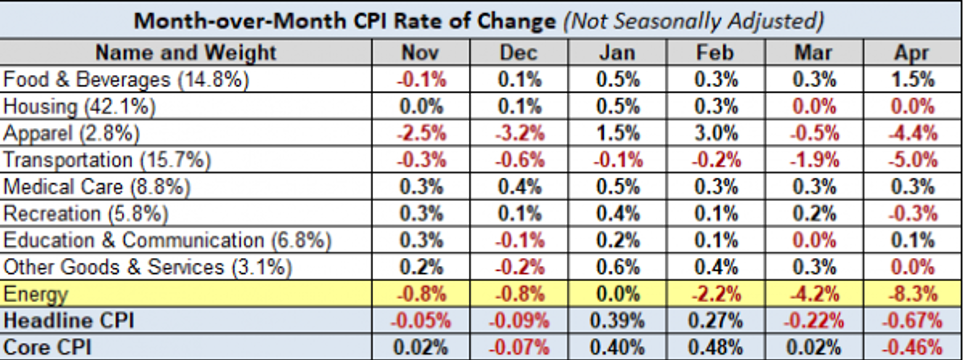

US CPI in April fell by 0.8% per month – a minimum since December 2008; gasoline fell by 20.6%, as expected, prices for insurance, tourism, airline tickets and clothing also collapsed. On the other hand, home food prices rose by 4.1%, the highest since February 1974. Excluding fuel and food, prices fell 0.4% per month – an anti-record in the history of the review since 1957. US PPI collapsed at a record 1.3% per month. The mood of small business in the United States is the most pessimistic since March 2013.

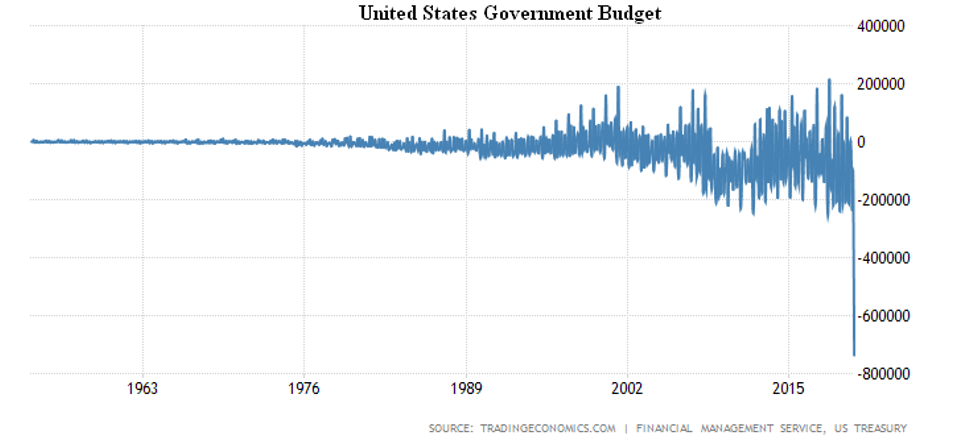

The US federal budget deficit in April reached $ 738 billion – a historic peak, 2.5 times greater than the previous record.

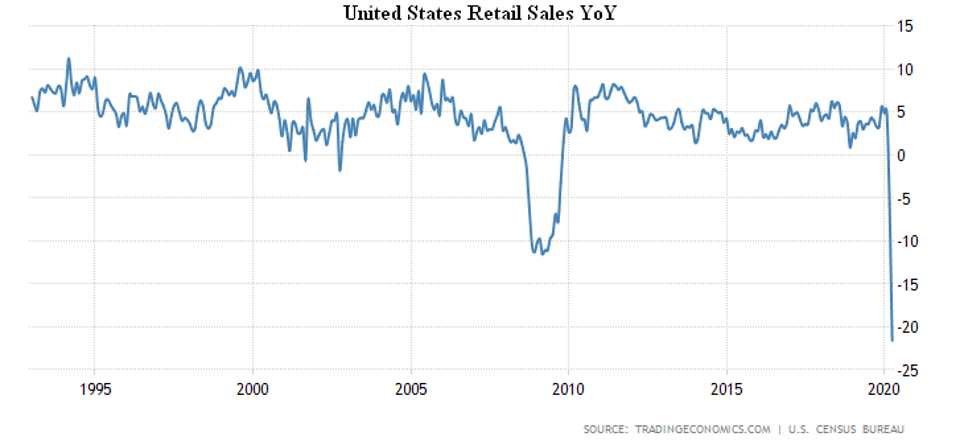

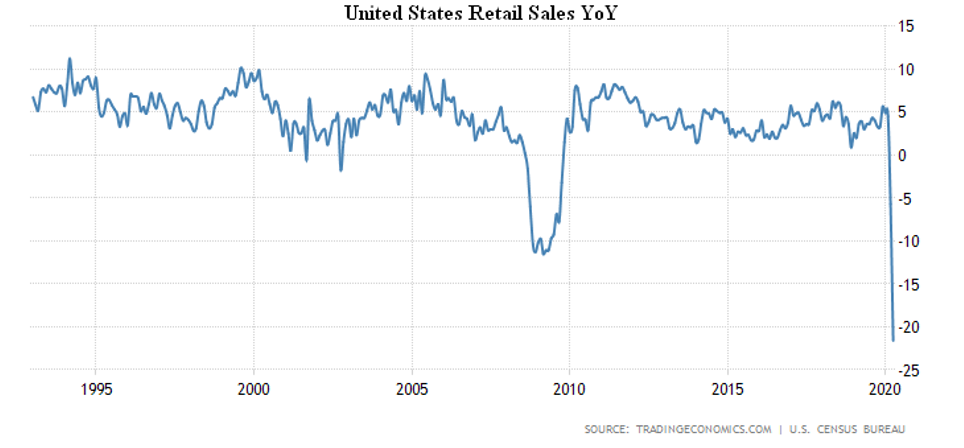

US retail sales fell 16.4% per month and 21.6% per year – both of which are the worst in history:

The Australian economy lost nearly 600 thousand jobs in April – a historical record with a 7-fold margin.

In the United States in early May, nearly 23 million people received unemployment benefits.

The Central Bank of Mexico cut the rate by 0.5% to 5.5%.

Conclusions

The colossal amount of cash thrown by the US Federal Reserve into the economy will inevitably show itself in inflationary processes. It is already clear that the enterprises that received support are not inclined to just pay salaries and support jobs, and their propensity to save has grown sharply (typical situation in a crisis period). As a result, on the one hand, there will be a significant increase in prices for some sectors, and for others, deflationary trends will manifest themselves. Prices will rise over time there (cost inflation will play a role), but it will be extremely difficult to predict the dynamics of these processes.

In fact, it can be stated that the economy has entered a period of high turbulence, characterized by rapid fluctuations in prices and rates, demand and tariffs. In addition, strong currency fluctuations are possible. For established businesses, even if there is a steady demand, the main problem will be the forecast of financial flows and resources.

In addition, the renewed discussion between Trump and Fed head Powell about lowering rates in the negative area, in fact, means, if Trump wins, the final destruction of the world dollar (Bretton Woods) system. Of course, its destruction is already inevitable, but if rates become negative this process will significantly accelerate.