Big news is not economic at all. More precisely, does not concern numbers. At the end of the week (after the failure of his mission in Jordan), the US President gave a keynote speech in which he made a fundamental thesis. Details of the speech, for information, are in the final section of the Review, and the thesis reads like this:

“America’s leadership is what unites the world.”

Since the profound inadequacy of this thesis is obvious to everyone, even to those who sincerely support the United States (for example, those leaders of Israel who want to preserve this country), its voicing cannot cause anything other than very serious suspicions that the United States does not have any positive ideas.

As you can see from the next section (and from all reviews of the previous two years), the economic situation in the United States is worsening. If our hypothesis about a structural crisis is correct (and so far there is not a single fact that would refute it), then the decline of the US economy will continue for several more years, and in the process there will inevitably be a collapse of financial markets. And this will inevitably entail a drop in the capitalization of fictitious assets, with an inevitable sharp decrease in GDP.

For all US partners, the most painful question is: what will happen to the accumulated assets that are denominated in dollars? Here we will reveal one important circumstance, due to which, in particular, in the previous review we recognized the Hamas attack on Israel as the main economic news. The fact is that, in our opinion, it was this attack that became the point after which the return of capital denominated in dollars would become impossible.

Of course, there will be exceptions: in particular, Iran will most likely get its money. But in general, the issue is already closed; no one will be able to use their capital.

Returning to Biden’s statement, let us recall that we have already raised the question of what political project the Democratic Party can offer, taking into account the fact that it must save the Breton Woods dollar system (and the Republican Party, accordingly, must restore American industry with the destruction of B-W systems). But then there was no answer. Biden’s speech suggests that even now there is no option. So the assumption of the previous paragraph seems quite natural.

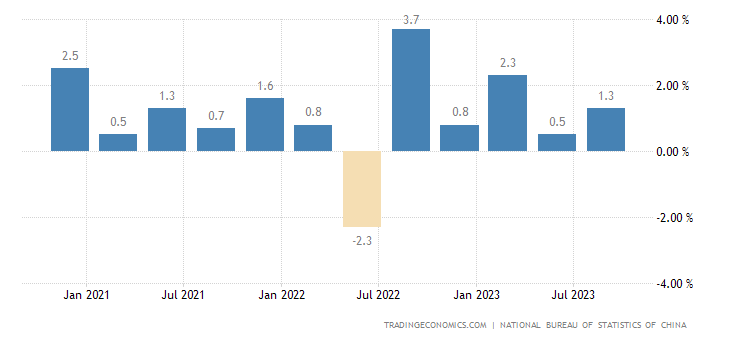

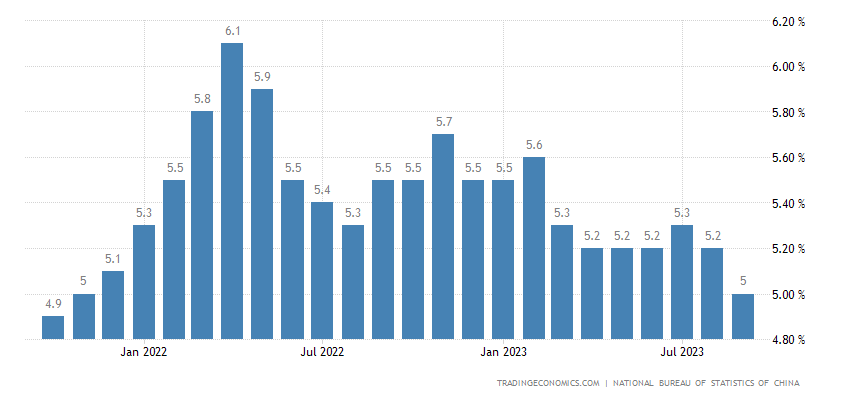

Macroeconomic. Chinese data this time came out mostly positive. GDP +1.3% per quarter – better than expected:

Pic. 1

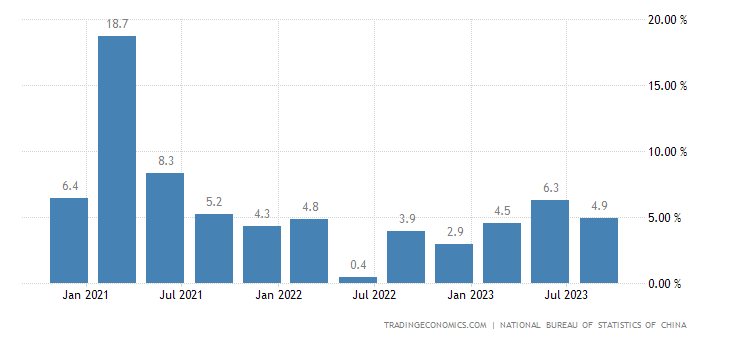

And +4.9% per year – also stronger than forecasts:

Pic. 2

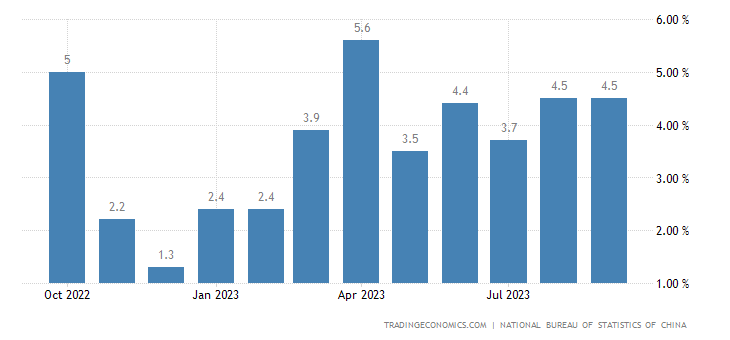

Industrial production, contrary to expectations, did not slow down (repeating the previous +4.5% per year):

Pic. 3

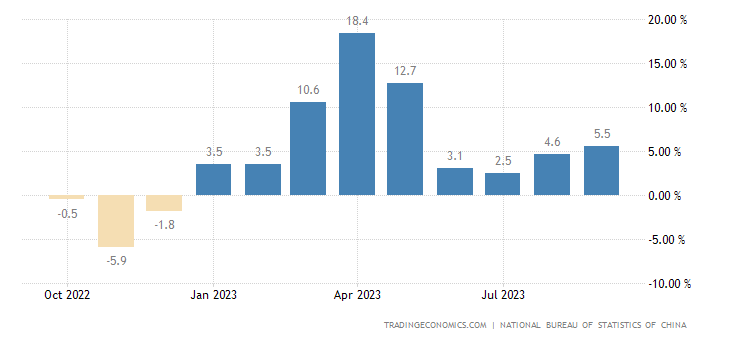

Retail sales rose to a 4-month high of +5.5% annually:

Pic. 4

Unemployment fell to a 2-year low of 5.0%:

Pic. 5

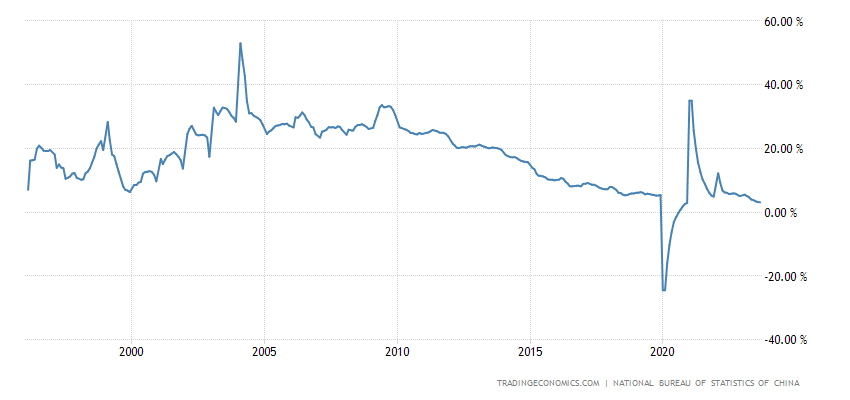

Only capital investment continues to slow down (+3.1% per year – excluding 2020, this is a record low):

Pic. 6

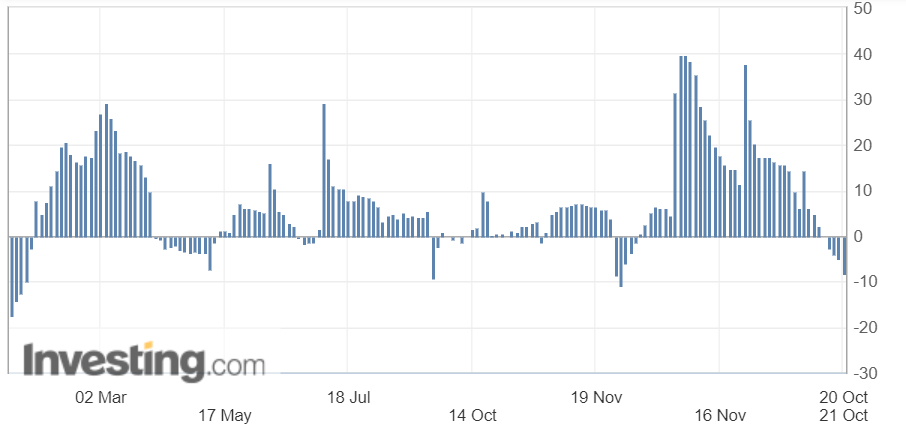

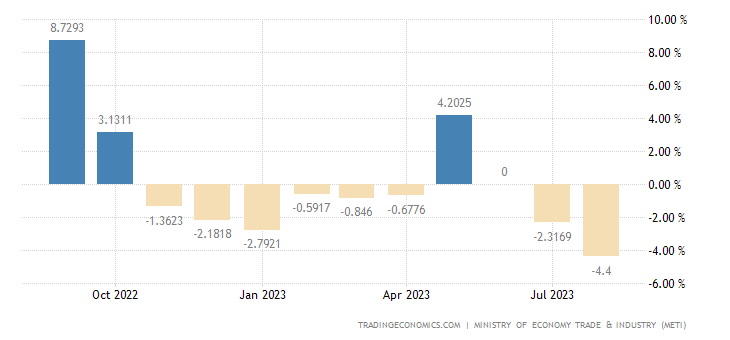

Foreign direct investment -8.4% per year – not counting Covid and calendar effects, bottom since 2009:

Pic. 7

However, if we take into account the fact that the Central Bank of China injected the maximum amount in 3 years into the banking system through medium-term loans, then this improvement can be explained.

Industrial production in Japan -4.4% per year – 9th minus over the last 10 months:

Pic. 8

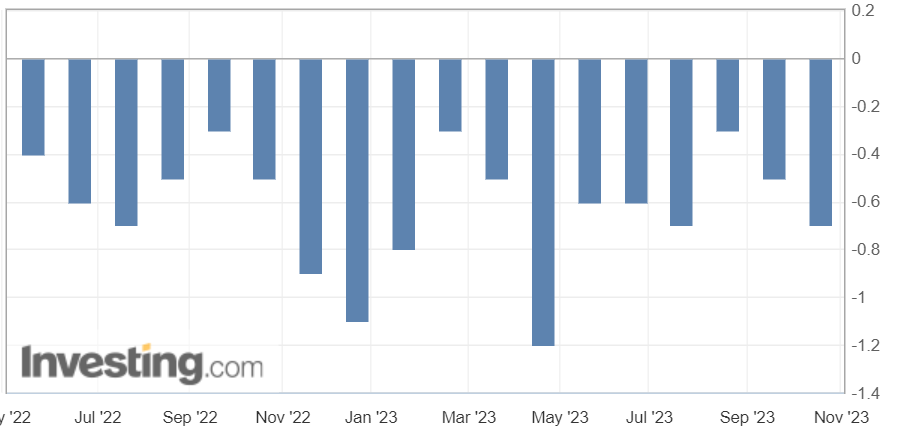

US manufacturing output -0.8% per year – 7th negative in a row:

Pic. 9

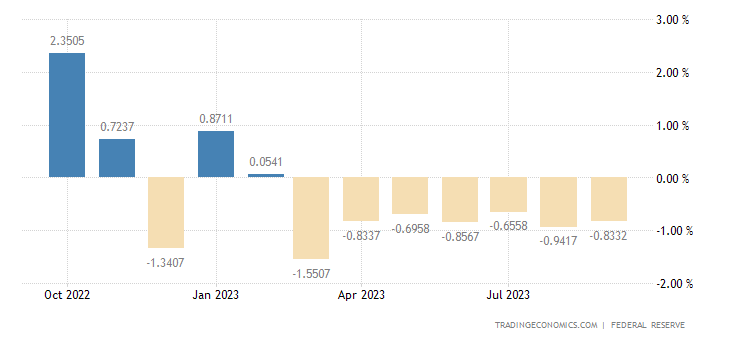

Leading indicators in the US -0.7% per month – the 17th minus in a row:

Pic. 10

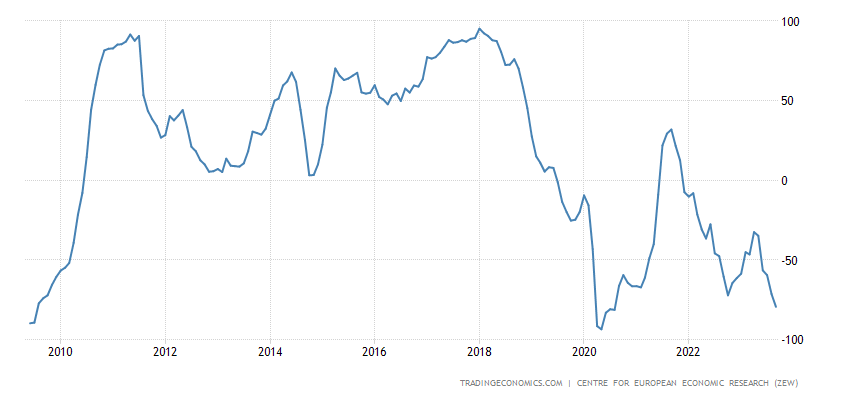

The assessment of the current state of the German economy (ZEW review) is the worst since 2020, and before that – since 2009:

Pic. 11

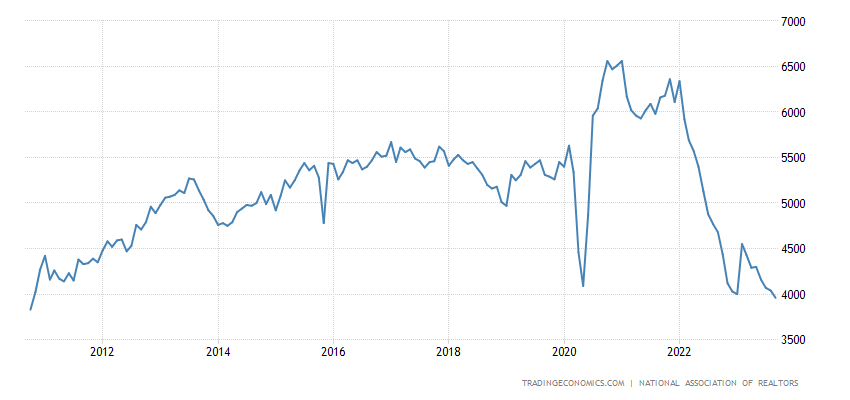

Existing home sales in the US are at their lowest in 13 years:

Pic. 12

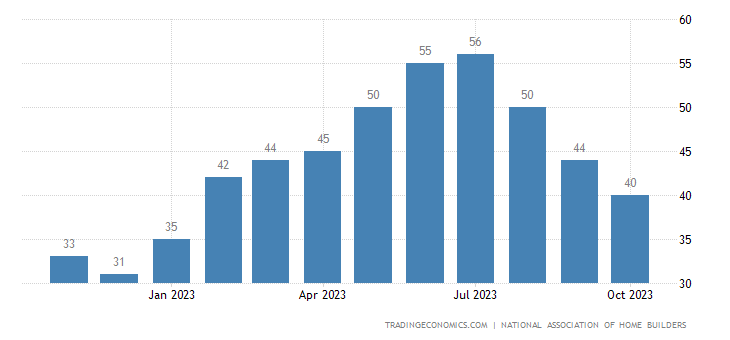

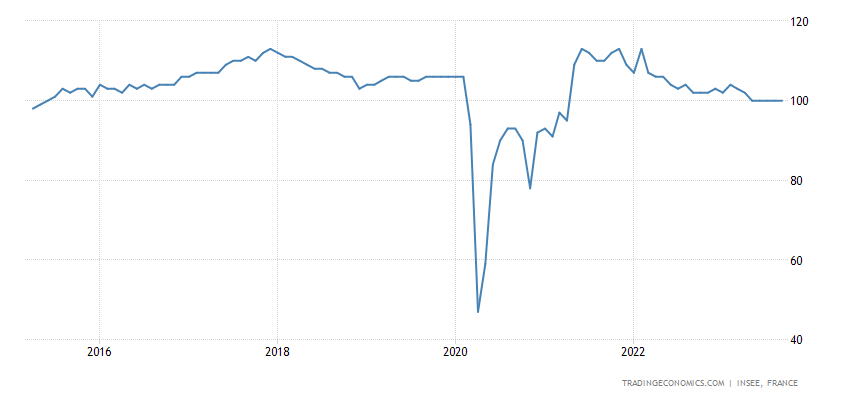

The US housing market index (from the Home Builders Association) is the worst in 9 months and in the depression zone:

Pic. 13

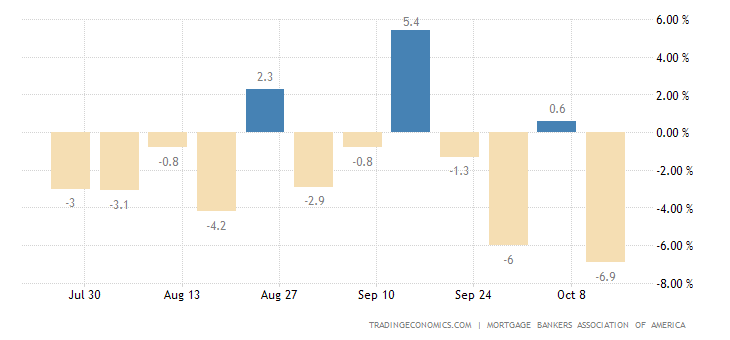

Mortgage applications in the US -6.9% per week – the weakest weekly dynamics in six months:

Pic. 14

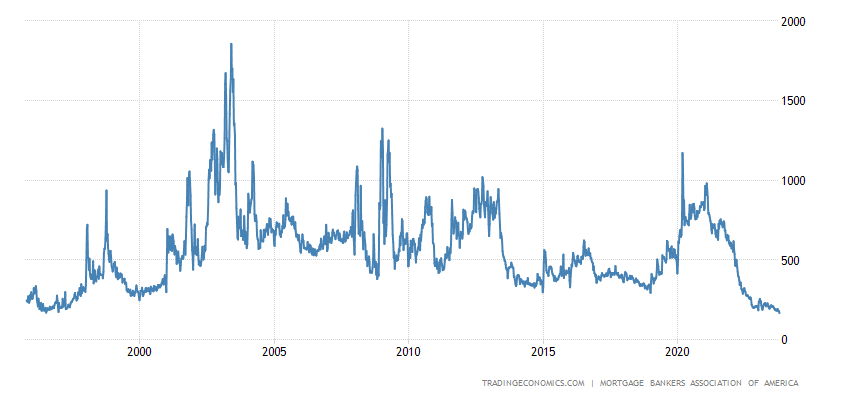

To a minimum since 1995:

Pic. 15

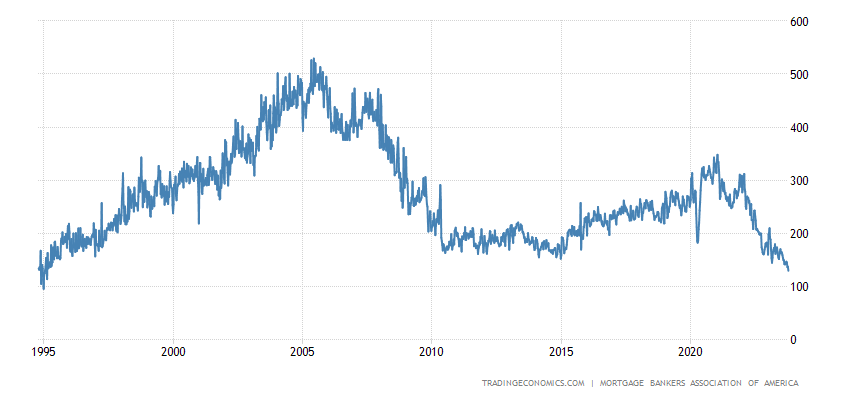

Separately, for loans for purchase (not refinancing) there is also a bottom for almost 29 years:

Pic. 16

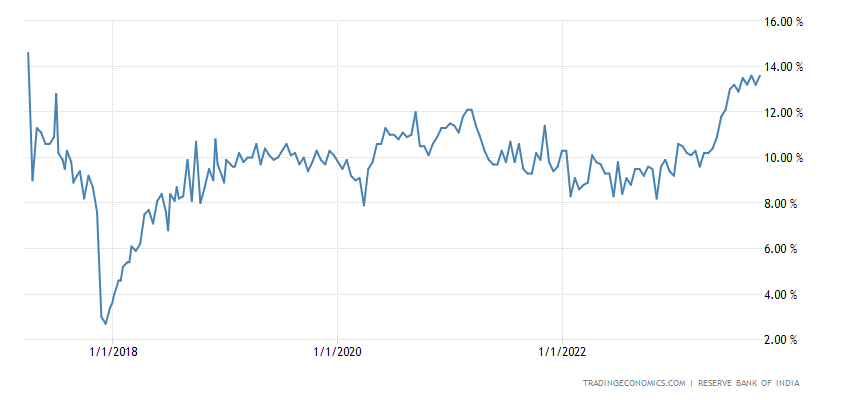

What is to blame for the loan rate, which has updated its 23-year high (7.70%):

Pic. 17

Leading indicators of Argentina -2.8% per month – the weakest dynamics in 3.5 years:

Pic. 18

The business climate in France has been at its lowest for 2.5 years; minus the Covid failure – in 8.5 years:

Pic. 19

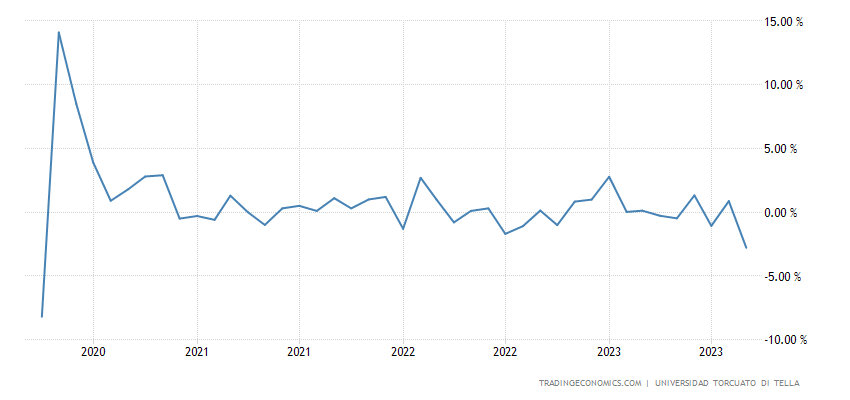

Deposits in Indian banks +13.6% per year – the largest increase since the spring of 2017:

Pic. 20

Wholesale prices in Germany -4.1% per year: the worst dynamics since May 2020, and before that since 2009:

Pic. 21

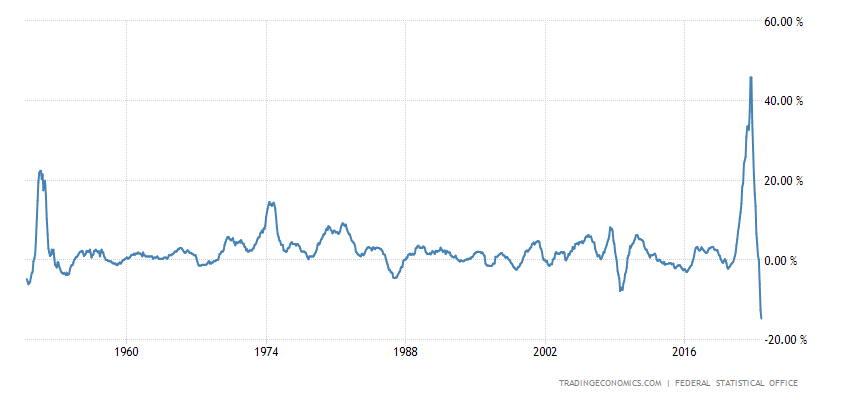

PPI (industrial inflation index) of Germany -14.7% per year – an anti-record for 74 years of observation:

Pic. 22

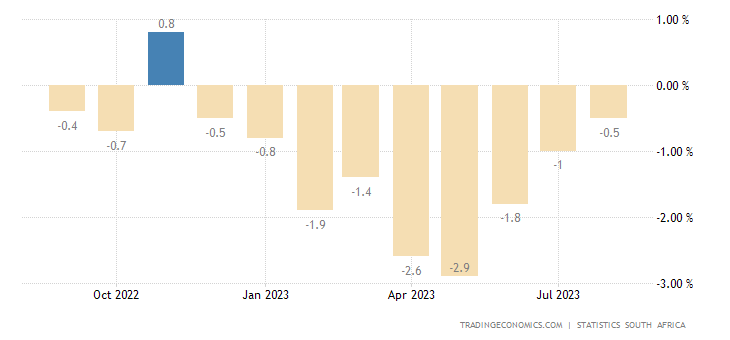

Retail South Africa -0.5% per year – 9th minus in a row:

Pic. 23

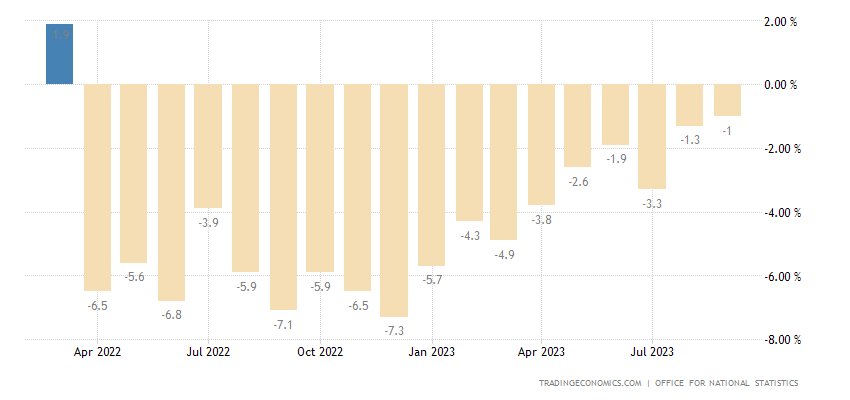

UK retail -1.0% per year – 18th minus in a row:

Pic. 24

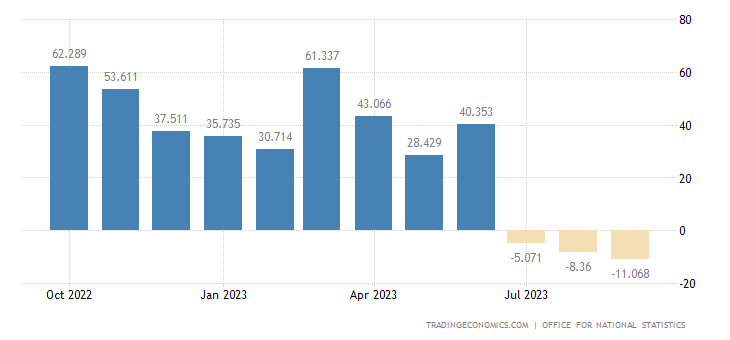

The number of employees in Britain has fallen for 3 months in a row:

Pic. 25

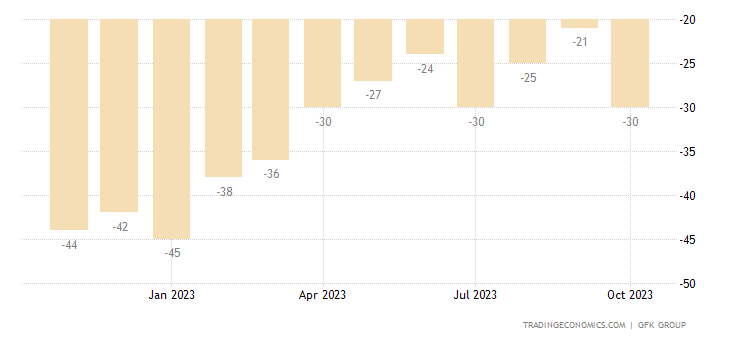

And the mood of consumers there is the worst in six months:

Pic. 26

The Indonesian Central Bank unexpectedly raised the rate by 0.25% to 6.00%. The Central Bank of South Korea did not change anything in its monetary policy.

Main conclusions. As promised, the main points of Biden’s speech – – without comment, this has nothing to do with economics:

- It is vital to America’s national security that Israel and Ukraine win;

- Washington does not want the US army to fight the Russian army;

- emergency budget request for funding for Israel and Ukraine will be sent on Friday;

- assistance to Ukraine is a “smart investment” that will bring dividends to future generations;

- The US and partners are working towards a better future for the Middle East that will benefit Washington itself;

- The task of a two-state solution to the Israel-Palestine conflict cannot be abandoned.

A week earlier than Biden, Powell spoke. Since he did not say anything new, in the same way, a brief retelling of theses:

- The Fed will tread carefully;

- financial conditions have tightened significantly in recent months, and long-term bond yields have been an important driver of this tightening;

- we continue to monitor these developments closely as ongoing changes in financial conditions may have implications for the direction of monetary policy;

- a range of uncertainties, both old and new, complicate our task of balancing the risk of tightening monetary policy too much with the risk of tightening too little;

- doing too little could cause inflation to persist above target and ultimately require larger rate hikes;

- too much may also cause unnecessary harm to the economy;

- The latest data shows that we are on track to meet our inflation and employment targets. I look at data that shows economic growth and workforce resilience;

- Low summer inflation figures are very positive, but September data is not so encouraging.

- We have repeatedly commented on all this in previous reviews, so there will be no new comments.

As usual, informal symptoms. Mortgage housing affordability index:

American sources say that real inflation in the United States since Biden became president is several times higher than the official figure of 16.4%. The relatively independent publication The Messenger writes about this. The closest thing to official statistics is butter – it has risen in price “only” by 23%. A pound of ground beef – plus 58%. Next comes a gallon of gasoline: plus 64%. Sugar packaging in the US has become 97% more expensive. Well, the leader of the rating is a pound of turkey: plus 114%.

The publication’s calculation method is more reliable than that of the US Department of Labor: journalists obtained Walmart receipts from 2020 and compared them with current ones. Moreover, we are talking about the largest retailer’s own brands – that is, in other stores everything is still more expensive.

New data from Pavel Ryabov (Spydell):

“Retail sales in the US are showing signs of growth, but the overall disposition remains unchanged – stagnation for 2.5 years.

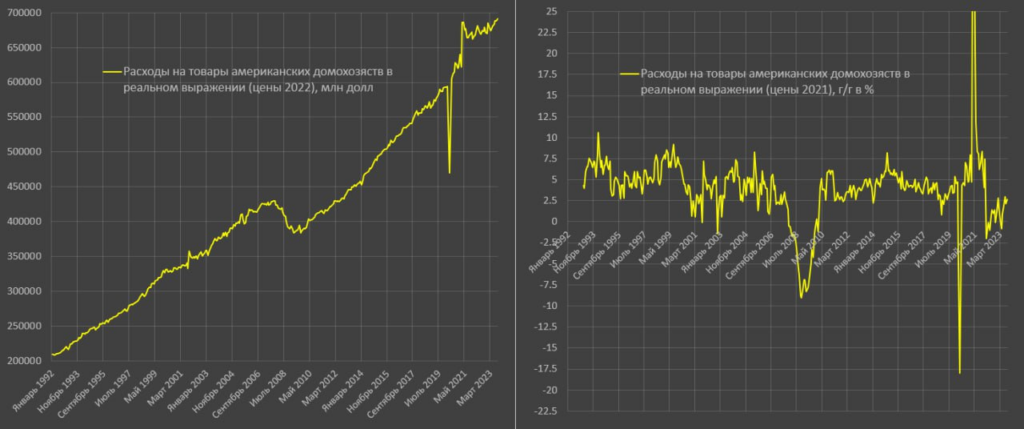

Retail sales in September increased by 2.7% y/y, compared to September 2021, an increase of 3.7%, but practically unchanged from March 2021. Compared to February 2020 (the last month of the pre-Covid era), an increase of 16.4%.

For January-September 2023, retail sales increased by 1.6% y/y, plus 2.8% over two years and a significant increase of 18.2% compared to 2019.

The methodology for calculating real retail sales has changed on my part (Census publishes nominal sales) and now matches the data that the BEA publishes in the GDP report under consumer demand for goods. That’s why the current data differs from my previous retail sales surveys, although the conclusions are unchanged.

How do current retail sales rates compare to historical rates? From January 2010 to January 2020, the average monthly growth rate was 0.35% in real terms or 4.3% per annum using the SAAR method.

What has happened since February 2020? By September 2023, growth will be 16.4%, which corresponds to 0.35% average monthly growth for the period, i.e. a return to the historical trend of 2010-2019.

Stagnation for 2.5 years is compensation for excess and unsecured growth from July 2020 to March 2021, provoked by fiscal and monetary incentives.”

And another study by Pavel Ryabov:

“Industrial production in the US is stagnating – a symbolic increase of 0.1% y/y in September, plus 0.3% y/y for January-September and the same for four years.

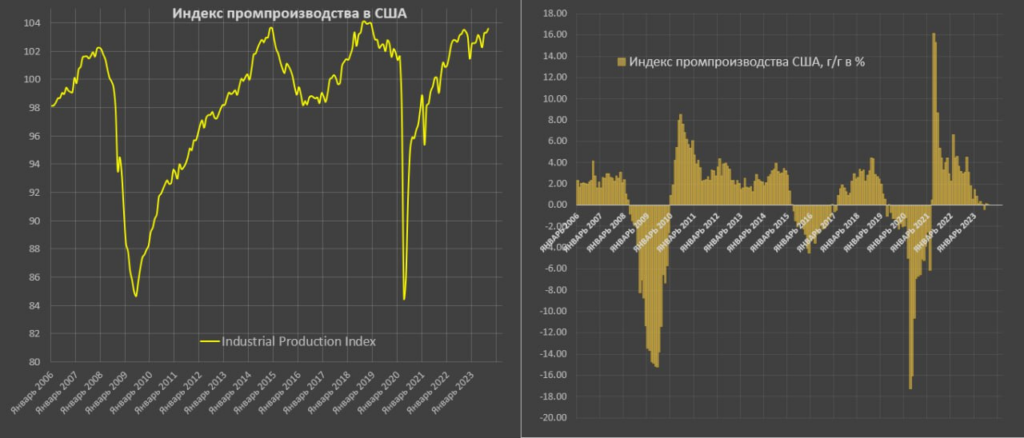

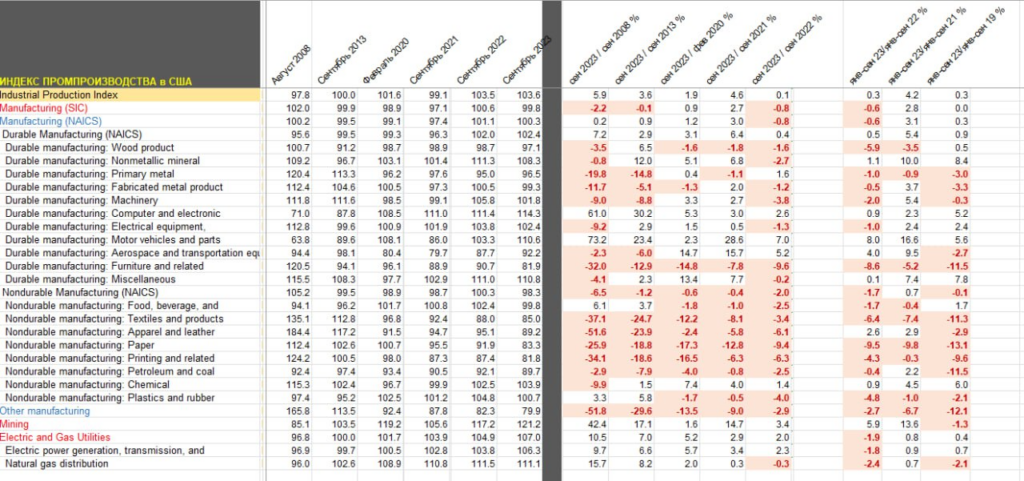

Taking into account the statistical error and regular revision of data within plus or minus 0.5%, we can assume that there is no growth either in a year or in four years (pre-Covid 2019).

Manufacturing production decreases by 0.8% y/y, minus 0.6% y/y for 9 months and at zero compared to 2019.

Mining production is growing by 3.4% y/y, plus 5.9% y/y over 9 months, but minus 1.3% by 2019. Oil and gas production in the US is reaching an all-time high.

Electricity production and utilities are growing by 2% y/y, although in the negative 1.9% y/y for 9 months of 2023, and compared to 2019, an increase of 0.4%.

The production of furniture, fittings and related goods is under the greatest pressure, with a decline of 9.6% y/y and minus 8.6% over nine months, which is associated with a drop in demand for residential real estate. There is a serious decline in the production of paper products (minus 9.4% y/y), publishing and printing activities (minus 6.3% y/y), although in the modern world this production is practically unimportant.

The production of plastic, rubber and related products was in the red by 4% y/y, and there was a negative trend (minus 3.8%) in mechanical engineering for industrial and commercial purposes.

The knowledge-intensive segment of the manufacturing industry is growing in the United States. Automotive and component manufacturing is in a better position than any other industry – plus 7% y/y in September, plus 8% y/y for January-September 2023, growth of 16.6% over two years and quite significant growth (vs. other industries) by 5.6% over 4 years.

Aerospace, military-industrial complex and other types of transport equipment are in a phase of steady growth of 5.2% y/y and 4% y/y for 9 months, although lower by 2.7% than 4 years ago.

The production of computers and electronics is growing by 2.6% y/y and plus 0.9% y/y over 9 months, by 2019 an increase of 5.2%.

The dynamics of production are multidirectional and there is a clear bias towards knowledge-intensive production.”

Let us point out that it is no coincidence that this data is not included in the main part of the Review. These are not macroeconomic data; they are even more susceptible to dependence on methods and subjective aspects. In addition, all these data are also price data, which, taking into account the systemic underestimation of inflation (and prices for final products are rising), gives a much less positive result. Well, let’s remember the results of China, it is quite possible that this is simply the result of increased investments in the industry, the effectiveness of which will become clear only in a few years.

But for those of our readers who work in certain industries, this is quite interesting information. And we constantly describe its real adequacy from the point of view of general economic processes.

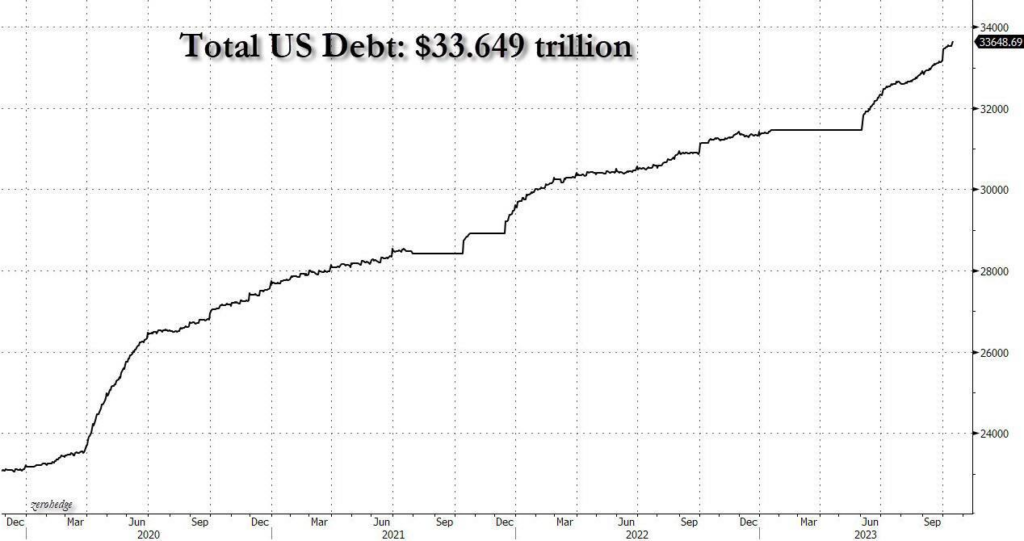

And finally, here’s a picture of the US federal debt:

In general, we can only confirm the statement given above: the crisis continues and is not going to stop. Nevertheless, we wish our readers a good weekend and minimal dependence of their business on various disturbances that began two weeks ago…