Time period: 4 – 10 December 2021

Top news story. The key news this week is strangely political, not economic. Jake Sullivan, National Security Adviser to the President of the United States, made a very important statement following a conversation between V. Putin and J. Biden.

“We, I believe, have entered an era of foreign policy and international affairs in which we are no longer talking about a formal huge structure, the Parthenon – the United Nations, the International Monetary Fund (IMF), the World Bank (WB) and so on. We now have a more complex hybrid of structures,” said statesman.

We will not elaborate on the political details of this statement – they don’t relate directly to macroeconomics. But the IMF and the WB are the major Bretton Woods institutions, and referring to them in this context can only mean that the current US leadership does not see the world dollar (Bretton Woods) system as a priori and unchanging part of reality. And that means that the global financial and economic system – with a global division of labor in mind – is about to undergo fundamental changes.

Of course, the crisis theory is based on the book A. Kobyakov and M. Khazin “Sunset Dollar Empire and the End of the Pax Americana” (2003), but this work was created already 18 years ago, and many of our critics have already exhausted themselves, laughing at the prediction of the collapse of the Bretton Woods system. However, the mills of history grind slowly, but they grind exceeding small, and the time has come. And we ask all our readers to consider this statement by J. Sullivan very carefully. It is much more important than any specific statistics describing the crisis.

It is impossible to assume that Sullivan misspelled or erred: this is the key phrase on which the Adviser’s entire logic is built. This logic is political in nature, but the reference to the key Bretton Woods institutions suggests that Sullivan has thought about them long and carefully. No doubt, Sullivan realizes that these economic institutions have long become systemically important in terms of building a global system of US superiority. And abandoning them as political will inevitably destroy their economic function, because these two functions have been inseparable for decades.

Macroeconomics

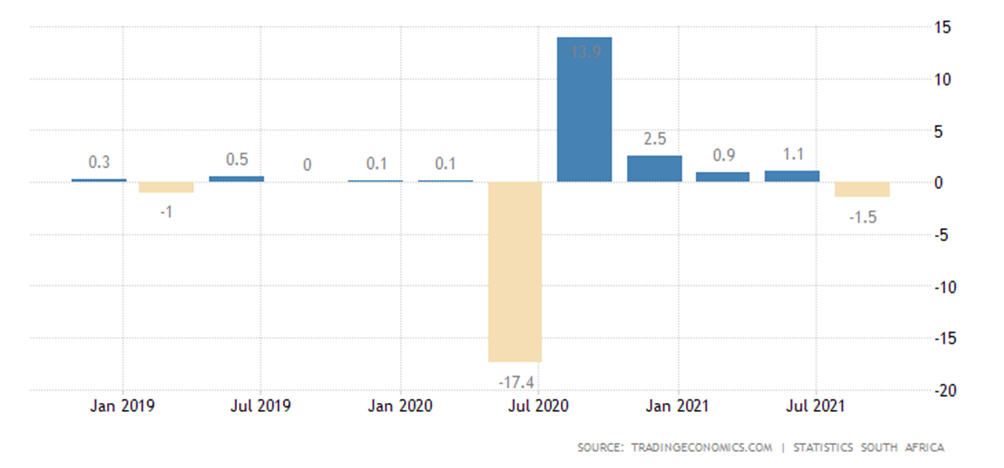

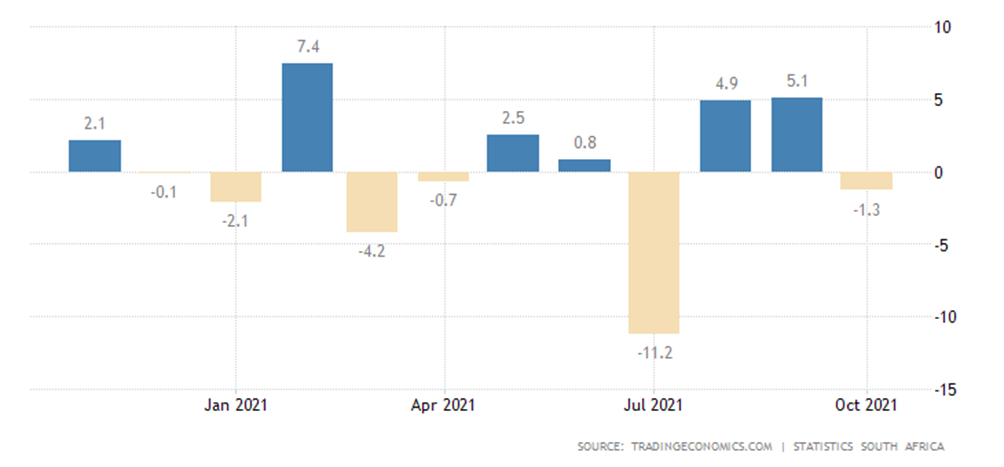

South African GDP -1.5% QoQ, this is the first negative after a break in a year:

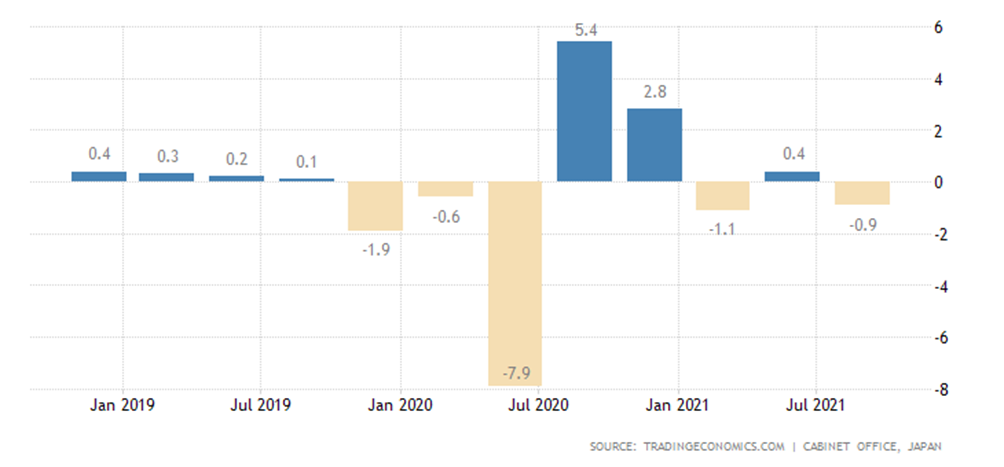

Japan’s GDP -0.9% QoQ, this is the 5th negative in the last 8 quarters:

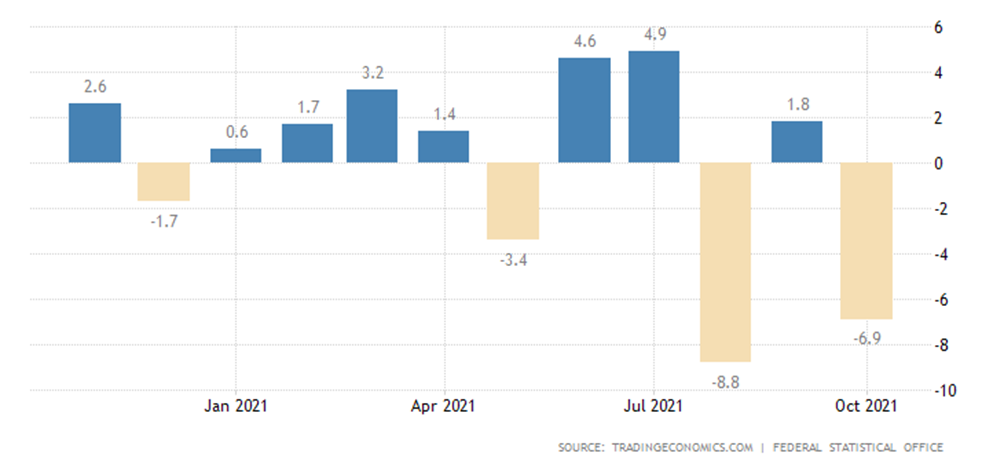

Factory orders in Germany -6.9% per month and -1.0% per year (the first downturn in over a year):

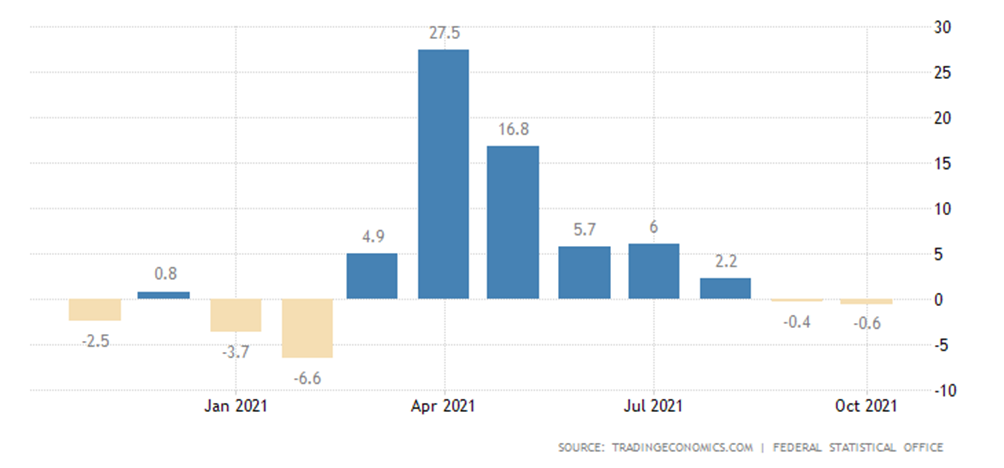

German industrial output went into the annual red for the first time in the last 7 months:

The last graph describes the “recovery” pattern very well: after a fairly long recession, a sharp rise begins. Looking at it separately from the previous recession, it seems that a very favorable period has begun, but the reality is that this peak is very short-lived and rapidly disappearing. In our case, annual growth of more than a quarter has gone into a steady decline in less than half a year.

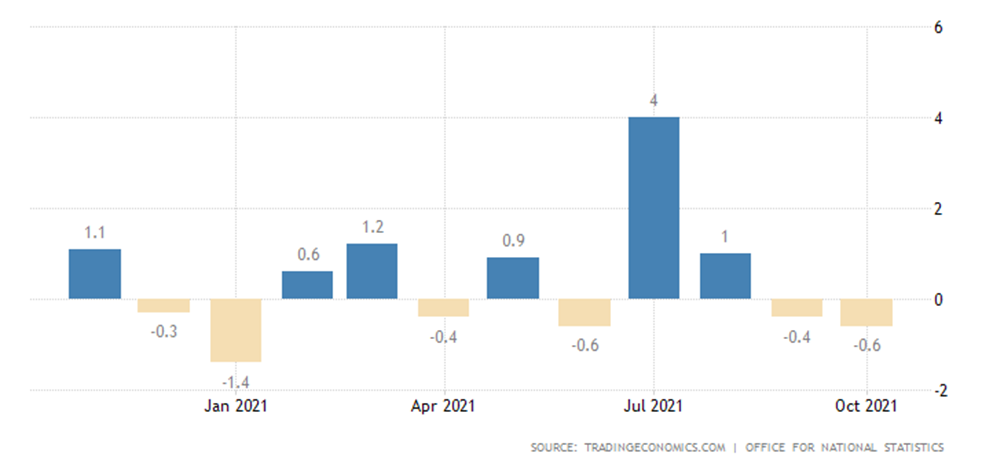

Industrial production in Britain is -0.6% per month, the second negative value in a row:

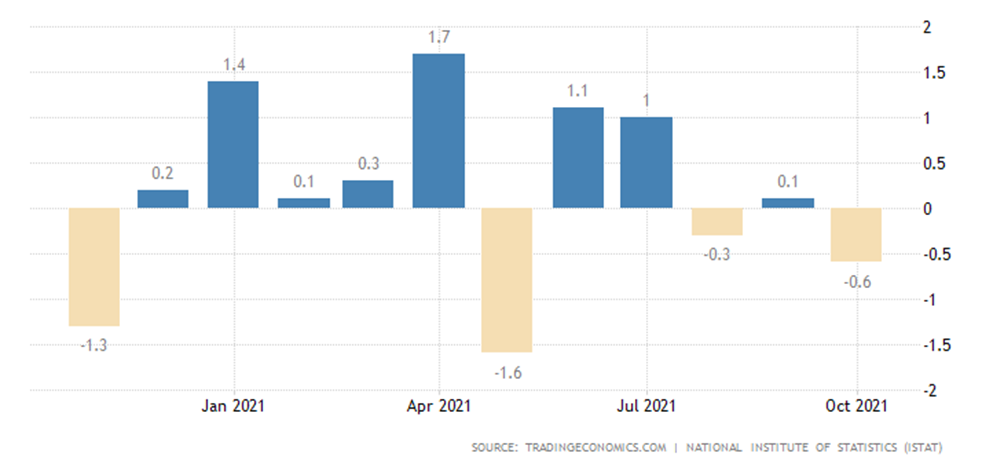

In Italy, too, -0.6% per month, this is the second negative in the last 3 months:

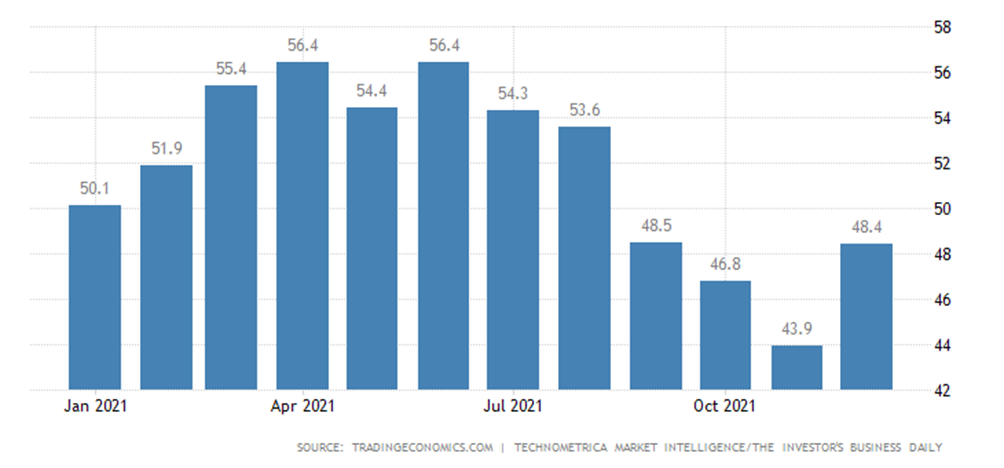

Economic optimism in the US (IBD/TIPP Survey) improved, but remained in recession:

Not surprising, with such inflation (see below)!

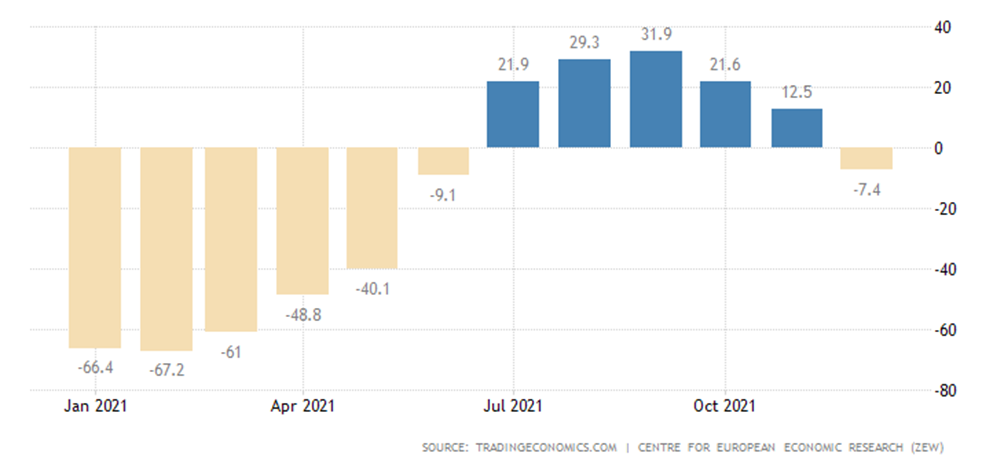

The current score in the ZEW survey of German economic sentiment went negative for the first time in six months:

In the Euro Area, conditions are no better, here the Sentix’s investor confidence is the weakest in the last eight months:

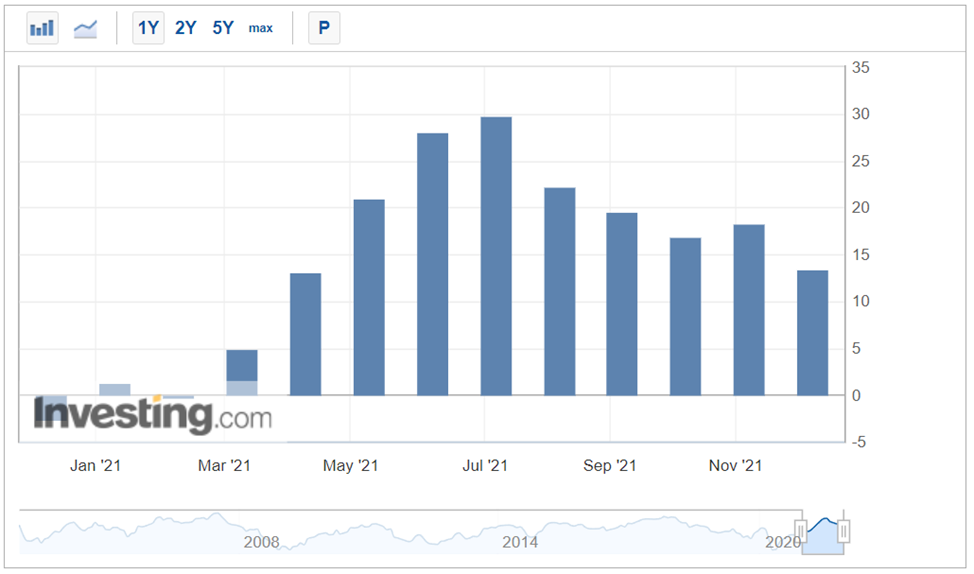

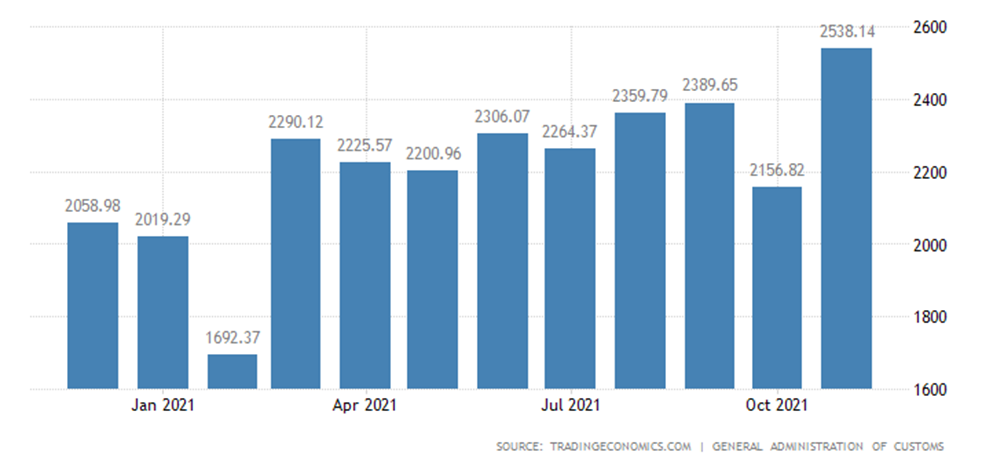

China’s exports and imports once again broke record highs:

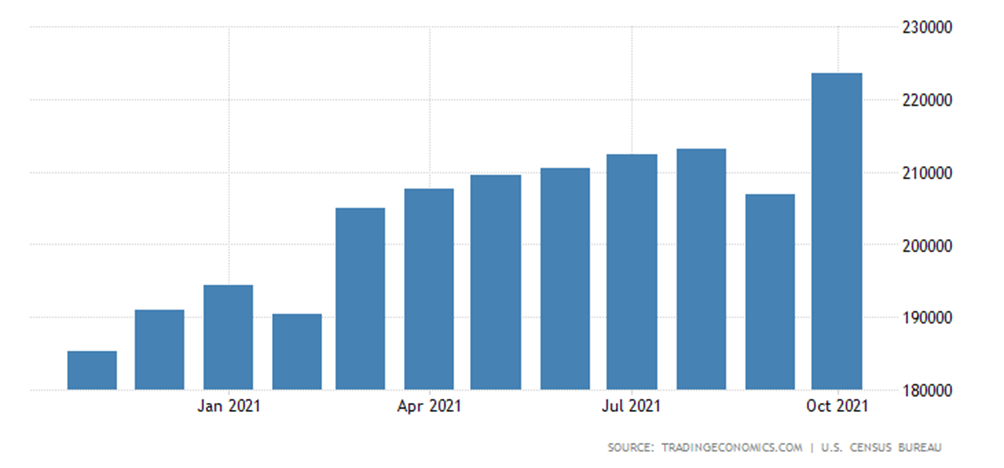

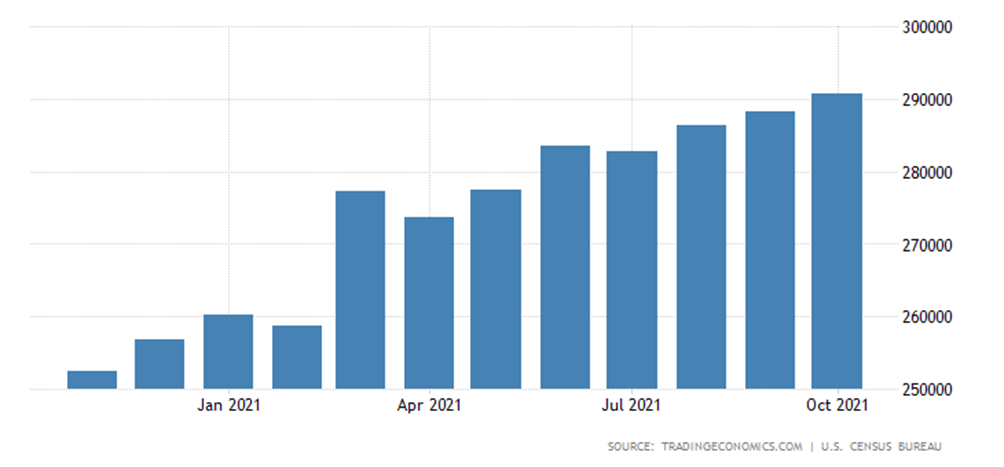

The same in the USA:

With the price increase, nothing else was expected. But it is not yet possible to assess systemic trends, as structural changes affect both supply and commodity prices in different ways. Analysts are finding it increasingly difficult to solve problems.

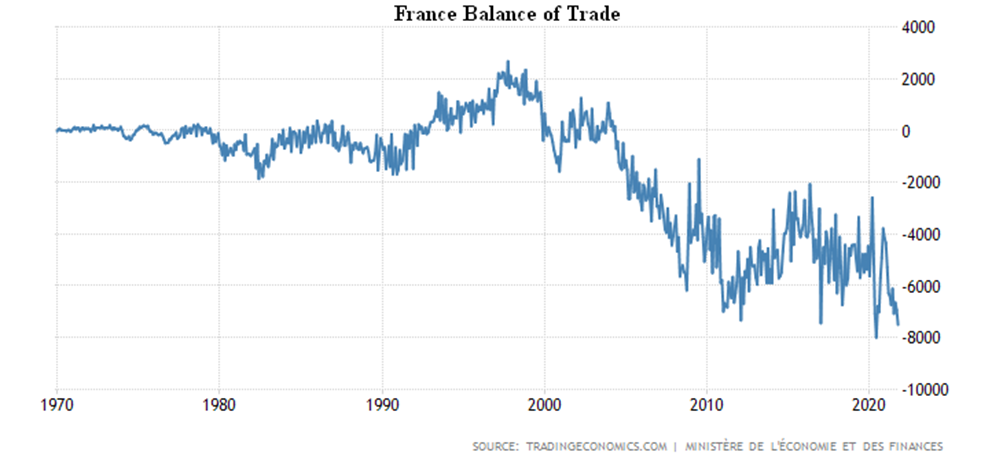

France’s balance of trade nearly matched a record high:

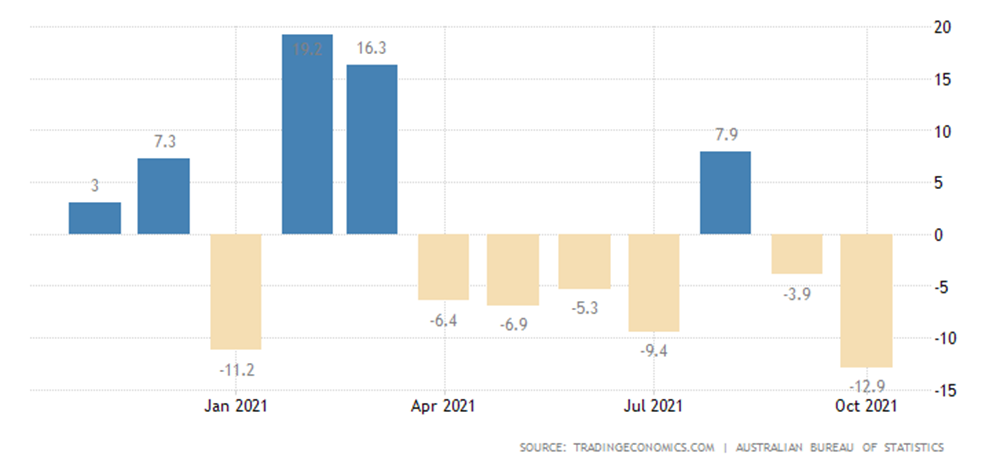

Dwelling approvals in Australia -12.9% per month, this is the worst performance in 1.5 years:

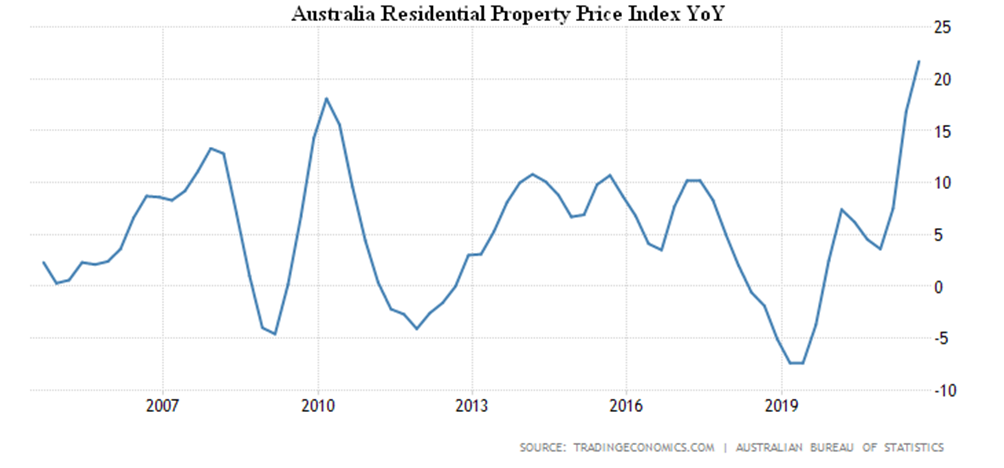

And house prices in Australia +21.7% per year, a record high in 18 years of observation:

Inflation figures have been a familiar pattern in recent weeks, breaking records.

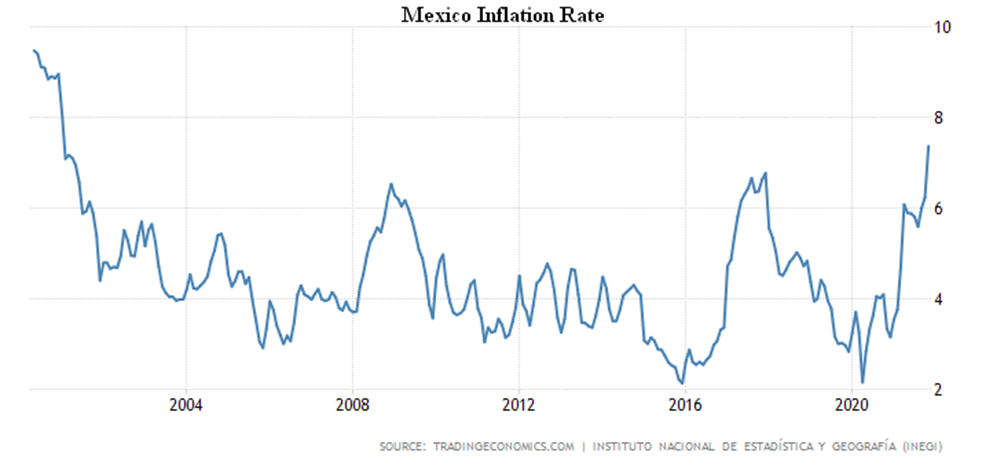

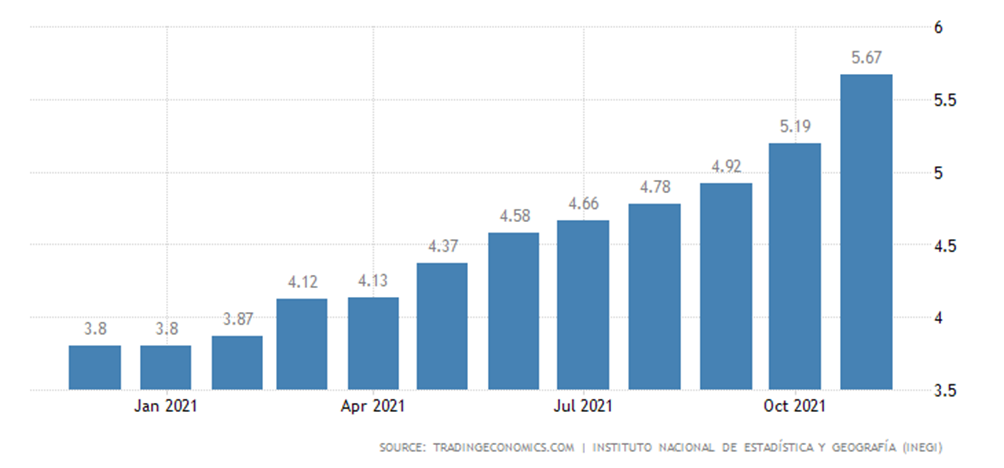

CPI (Consumer Price Index) of Mexico +7.4% per year, is at its highest since January 2001:

Similar situation with regard to prices without food and energy: +5.7%, peak since 2001 –

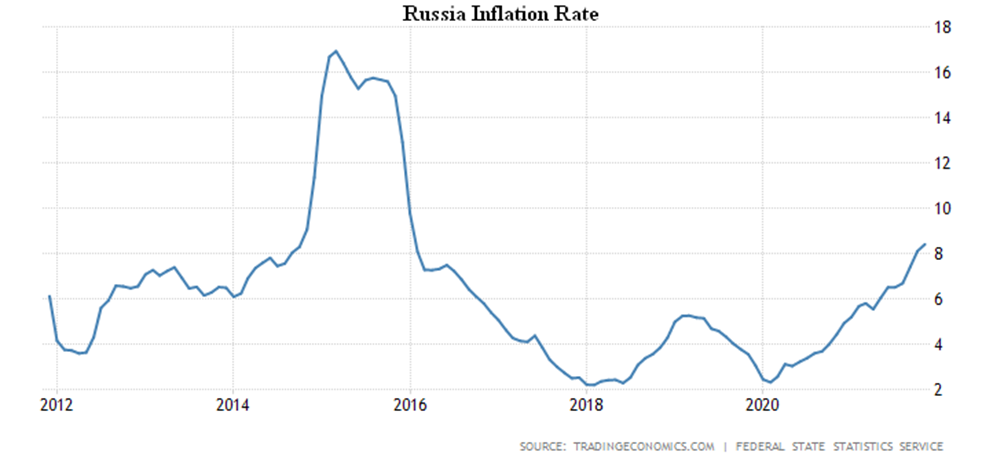

CPI of Russia +8.4% per year, the maximum since January 2016. Food +10.8%:

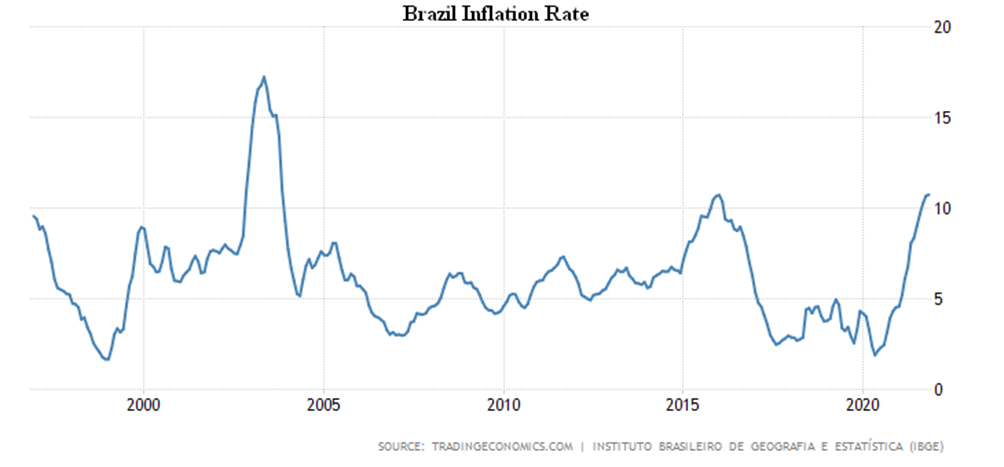

CPI Brazil + 10.7% per annum, the top since 2003:

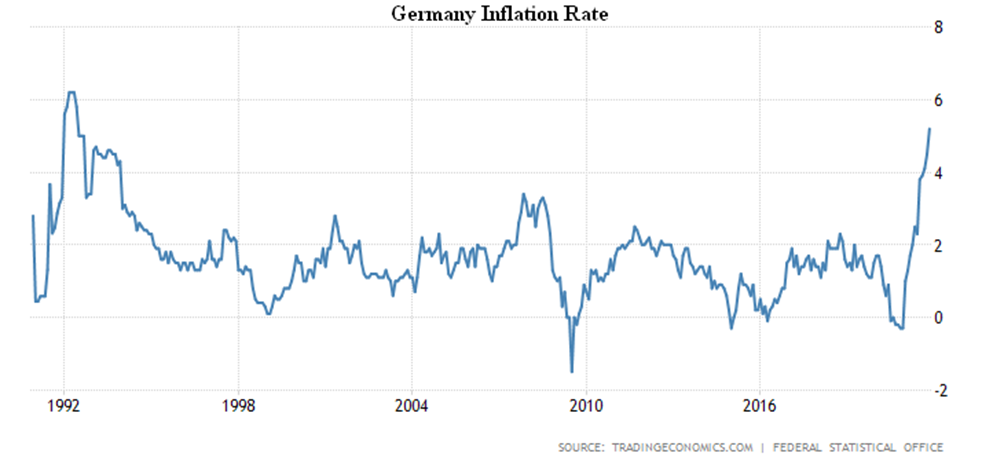

CPI in Germany + 5.2% per year, the highest since 1992:

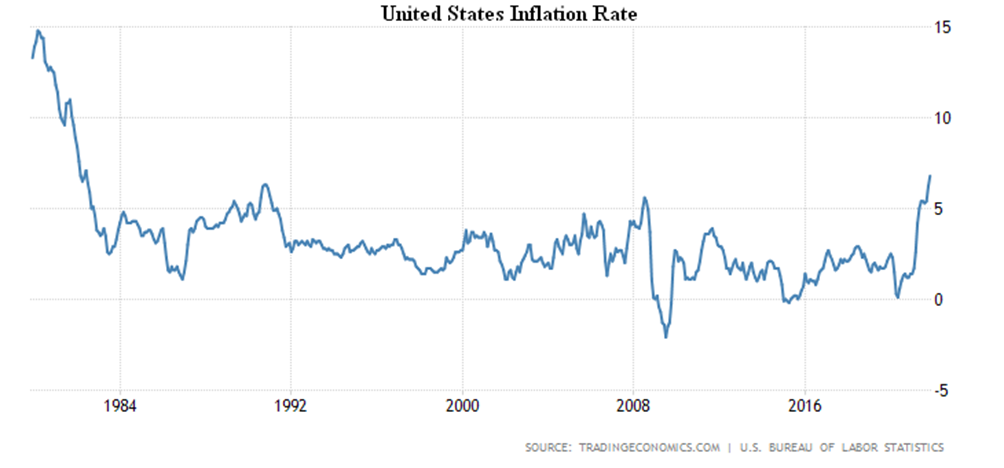

US CPI +6.8% per year, which is a record since 1982:

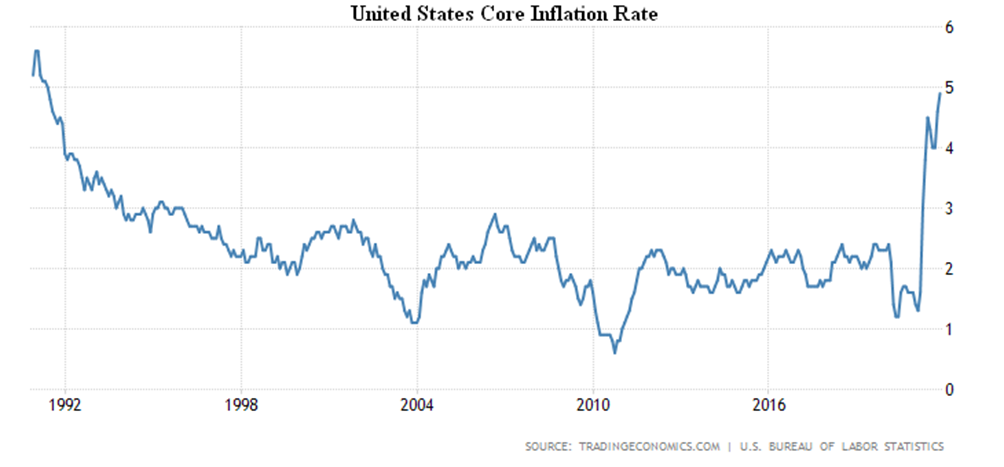

Less food and energy +4.9%, the maximum since 1991:

CPI China +2.3% per year, which was a 15-month peak, but below the expected value (+2.5%):

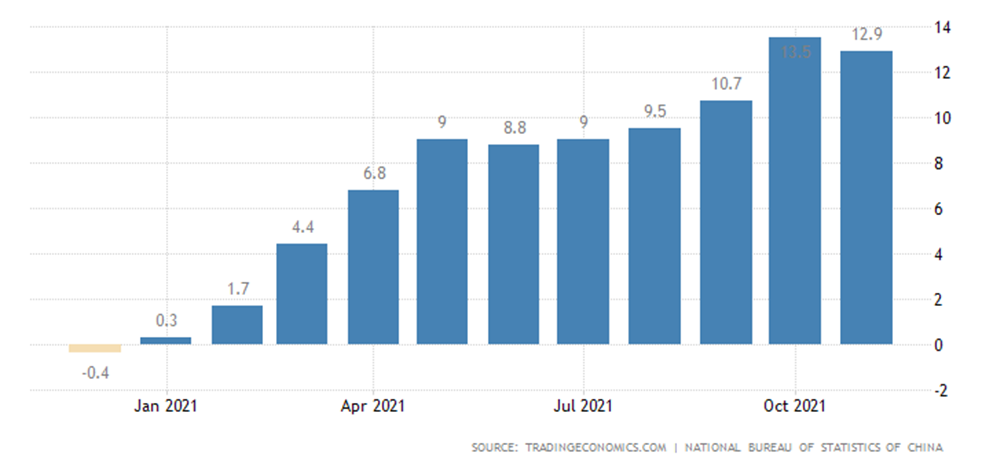

PPI (Producer Price Index) of China +12.9% per year, below the 26-year-high of last month (+13.5%), but higher than projected (+12.4%):

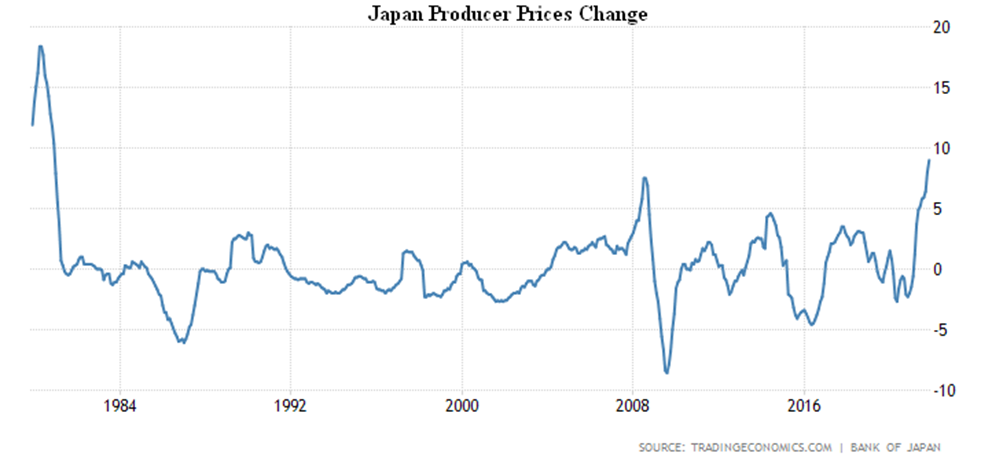

PPI Japan +9.0% per year, a record since 1980:

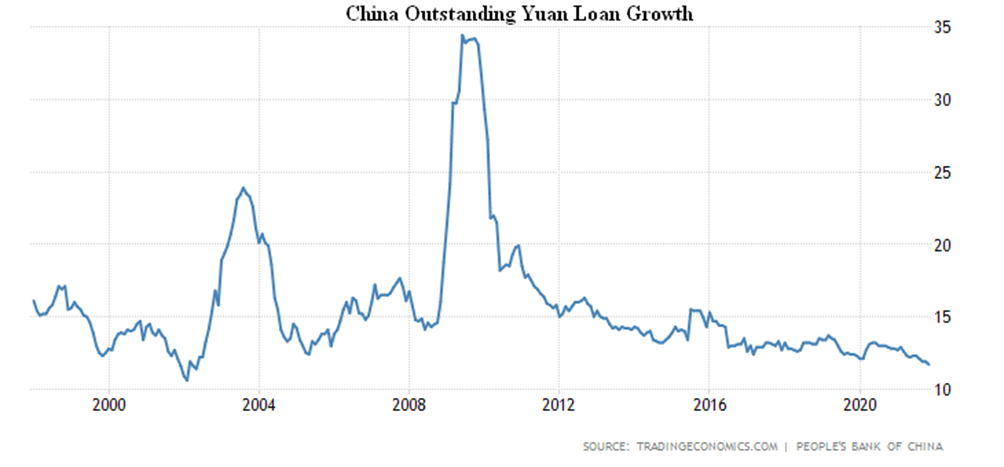

Outstanding Yuan loan growth in China +11.7% per year, the lowest since May 2002:

In Spain, consumer sentiment is darkest in seven months:

Retail sales in South Africa -1.3% per month:

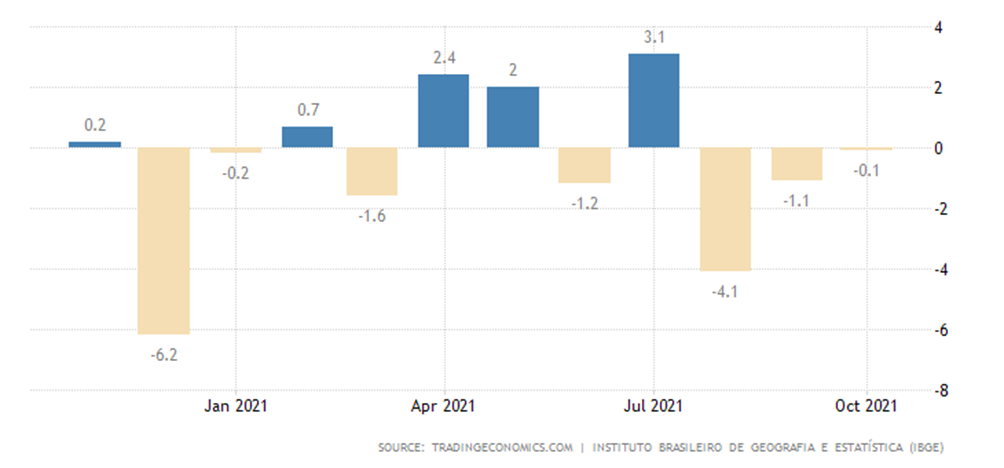

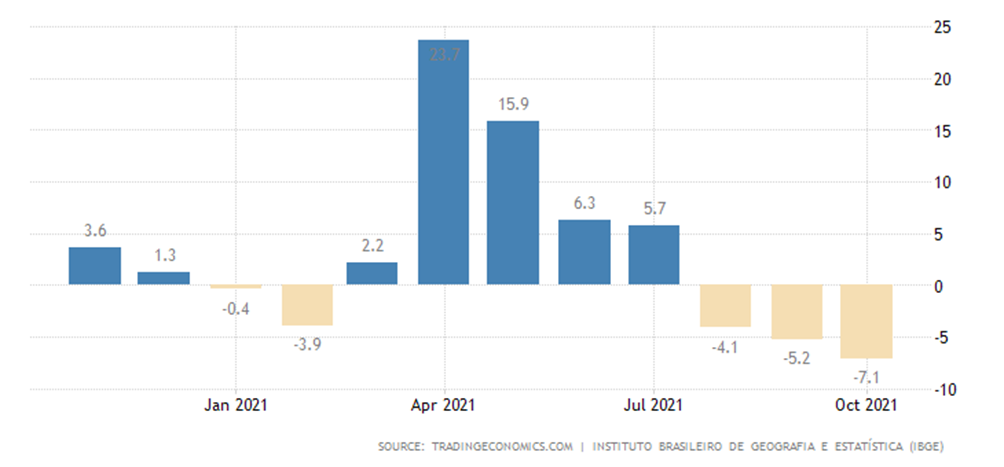

Retail in Brazil -0.1% per month, this is the third consecutive negative:

And already -7.1% per year, since May 2020 it’s the worst performance:

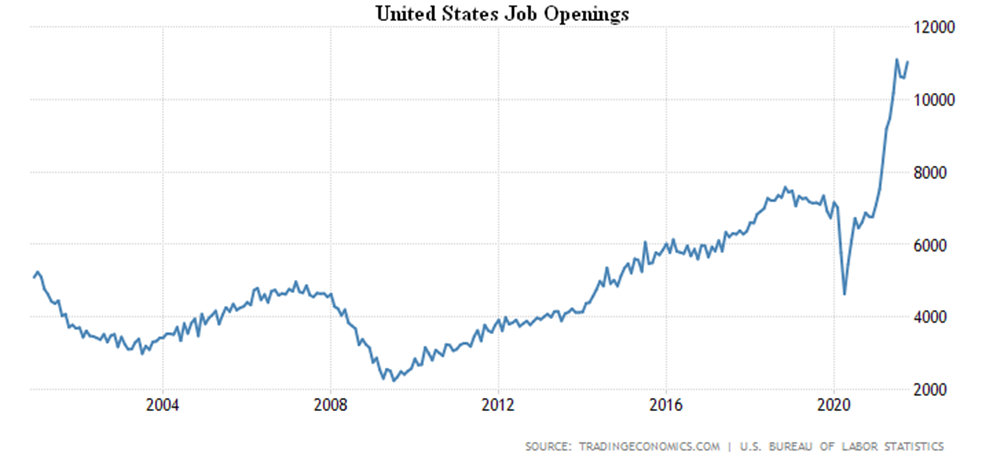

The number of vacancies in the United States is near record, as many firms are unable to hire the necessary staff:

It should be noted that, against this background, the rest of the labor statistics give rise to doubts. For example, the unemployment rate U-6 in November amounted to 7.8% against the October figures of 8.8%;

the level of participation of the population in the total labor force in November showed 61.8%, and in October it was already 61.6%;

the average working week (in hours) was 34.8 in November vs. 34.7 in October;

the unemployment rate in November is 4.2% and it was 4.6% in October.

Finally, the number of initial jobless claims in the last week was 222 000, with an estimated 240 000 (199 000 a week ago).

What remains to be seen here is that the statistical models used by the United States Department of Labor in the context of a structural crisis and strong budget support show completely untrue results. The Central Bank of Australia left its policy unchanged, as did the Central Bank of India and the Central Bank of Canada. While the Central Bank of Brazil hiked up the rate for the seventh consecutive time, by 1.50% to 9.25%, it promises to do the same at the next meeting.

Summary. According to US labor statistics, general statistical models in this country (and, given the specificities of the IMF’s work, they are used by almost the entire world) can no longer provide any objective data. It may be possible to correct the new models, but it will not be possible quickly to check whether they are adequate. And taking into account the strong structural changes, that’s not going to happen. The economic picture – the ratio of industries, prices, exports, imports, stocks and expenditures – has become very volatile.

In such a situation, only complex non-linear feedback models (at least cross-industry models) can work, which, for example, are used for their projections by the Mikhail Khazin Foundation for Economic Research. Unfortunately, almost none of the analysts and experts use such models anymore, which makes forecasting an undecidable problem for market participants. And with a high division of labor, it’s almost impossible to work without a forecast.

The structural crisis – the logistical component of which we have seen – is coming to the next level that we will face in the near future. It will be reflected primarily in the sharp increase in insurance premiums, and insurance companies will be in trouble as they increasingly have to pay for certain insurance cases. Or, on the contrary, we will see a sharp increase in the rejection of insurance payments, and perhaps both.

In any case, we can say with great confidence that the structural crisis is entering a new phase that will emerge in the coming months. The only good thing is that the recession is unlikely to pick up a strong pace.

We wish all readers a good luck and a fruity work week!