August 19-25, 2023

Big news. There are two main stories in the week, with one explaining the importance of the second. The first was the BRICS summit in Johannesburg (South Africa). Why has he become so important? But the fact is that before the summit there were numerous rumors that a new BRICS currency would be introduced at it.

Of course, it is impossible to introduce a new currency just like that, and Mikhail Khazin has repeatedly explained that the BRICS countries are not ready for this. Because today they do not have single markets that have pricing in domestic currencies. But the discussion of this topic at the summit was unconditional and, taking into account the increase in the number of participants, there is no doubt that in the fairly near future the issue, at least with the settlement system, will arise again. And this, of course, will be a very serious blow to the Bretton Woods system.

Of course, but why, in fact, a strong blow? Maybe it’s an illusion? And the fact is that at the end of the week there was a second event – the speech of the head of the Fed, Jerome Powell, at a conference in Jackson Hole. The details of his speech in the final section of the Review, for the time being, we note that Powell did not say any intelligible explanations of what and how will happen in the dollar world, which cannot but cause alarm among all economic entities.

Roughly speaking, since the situation is clearly deteriorating and everyone can already see it, despite attempts to inject optimism on the part of the US monetary authorities, the latter should say something. And their avoidance of an answer creates high nervousness, on which the activity of the BRICS countries (of which there are already more than ten) falls. And although these countries cannot have a single economic policy (we remind you that for the first time these countries were united by A. Kobyakov and M. Khazin in the book “The Decline of the Dollar Empire and the End of Pax Americana” as potential leaders of various currency zones into which the modern dollar system), but a single settlement system based on an alternative currency may well be.

Moreover, as problems with the dollar increase, including due to the destruction of the Bretton Woods rules through the imposition of sanctions against Russia, the desire to create such a system is growing all the time. And a year later, at the summit in Kazan, this issue may be raised in an absolutely constructive way. Which, as is clear, the stability of the dollar system will significantly shake.

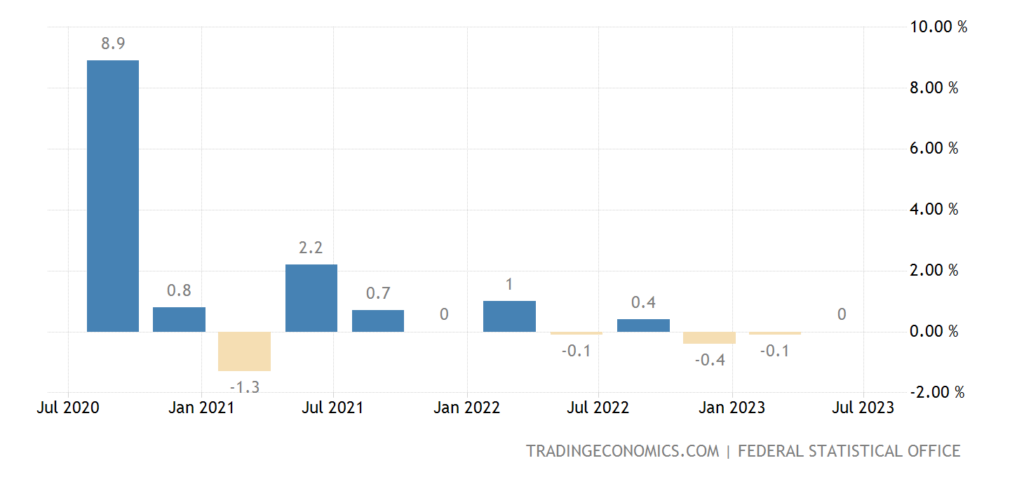

Macroeconomics. German GDP 0.0% qoq after -0.1% qoq and -0.4% in Q4 2022:

Pic. 1

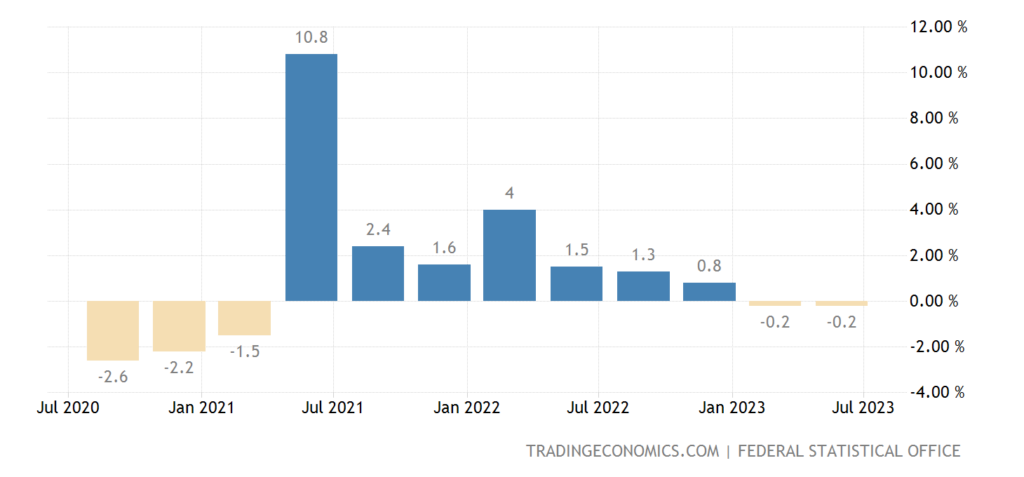

And -0.2% per year – the same as it was in the previous quarter:

Pic. 2

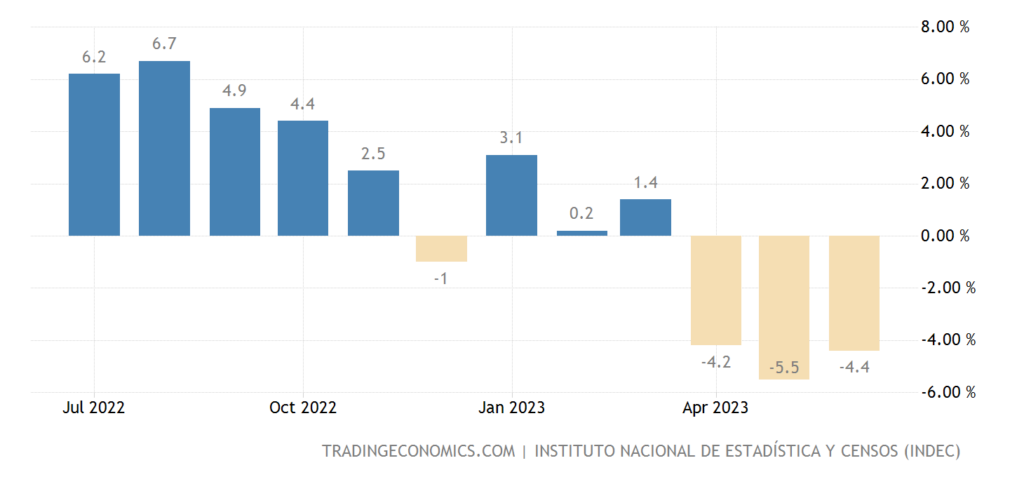

The indicator of economic activity (some analogue of GDP) of Argentina -4.4% per year – the 3rd minus in a row:

Pic. 3

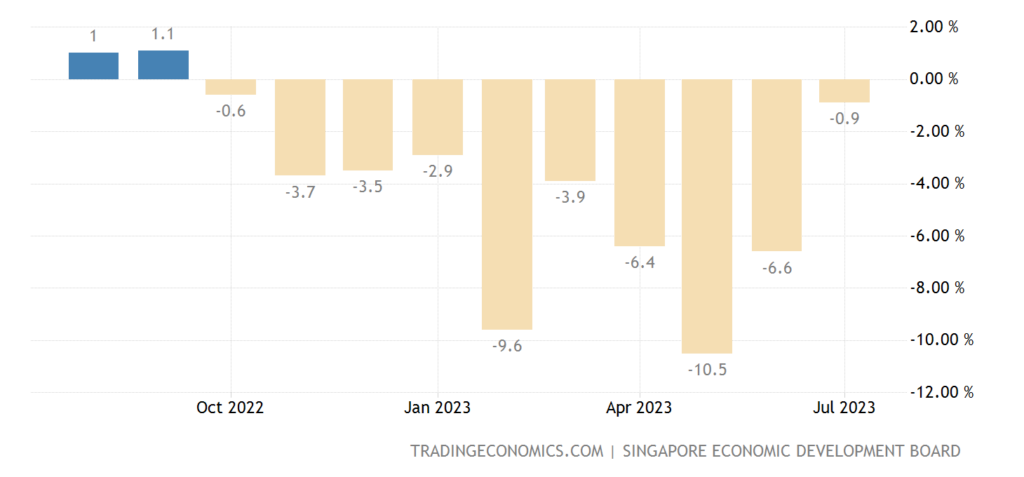

Industrial production in Singapore -0.9% per year – the 10th consecutive minus:

Pic. 4

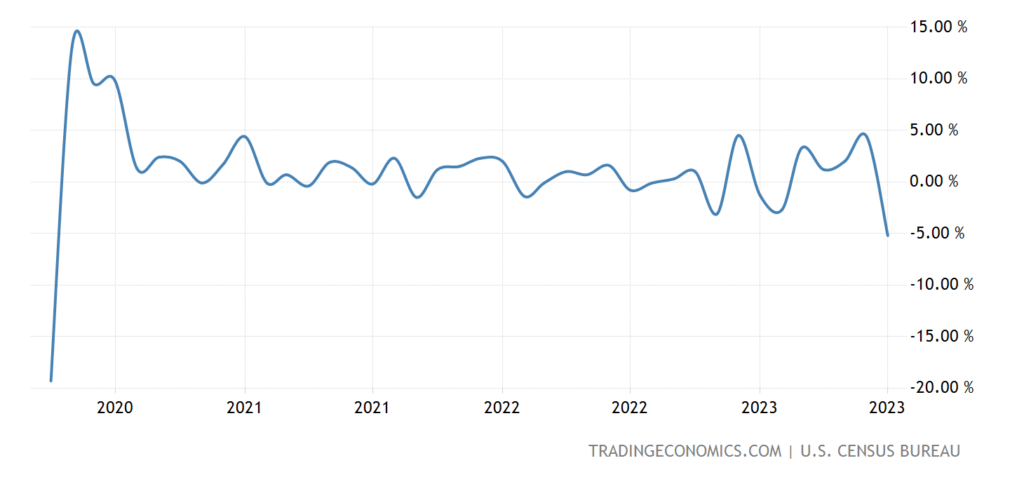

US durable goods orders -5.2% per month – minimum since April 2020:

Pic. 5

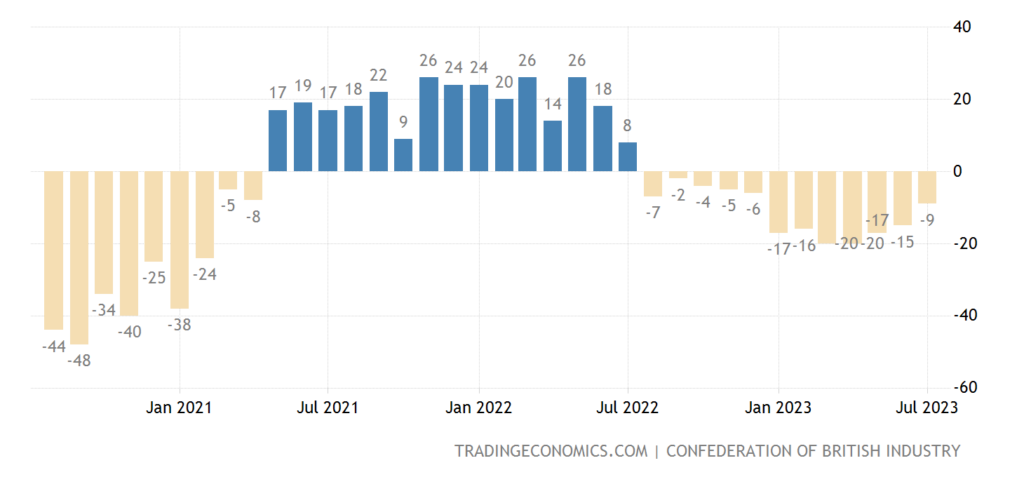

UK industrial order balance negative for 13 consecutive months, worst output since 2020:

Pic. 6

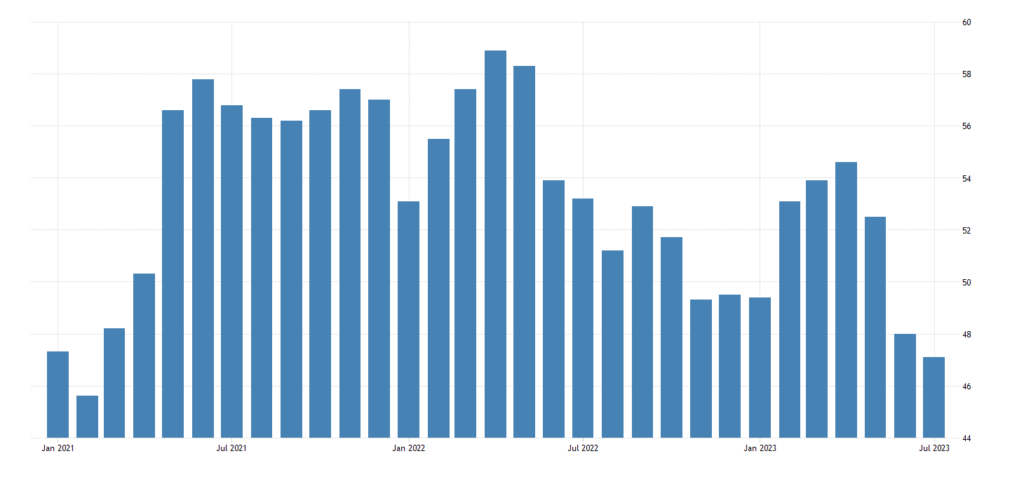

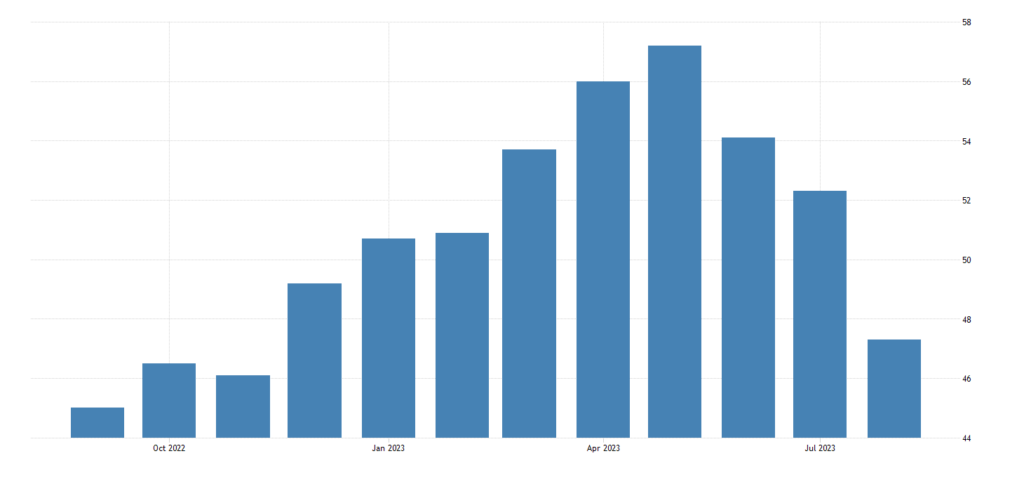

PMI (an expert index showing the state of the industry; its value below 50 means stagnation and recession) of industries have stabilized in the recession zone everywhere. As expected in a structural crisis, activity should move to another area of the economy. So in the European Union, indicators of the service sector flew down:

In France, 46.7 is the bottom in 2.5 years:

Pic. 7

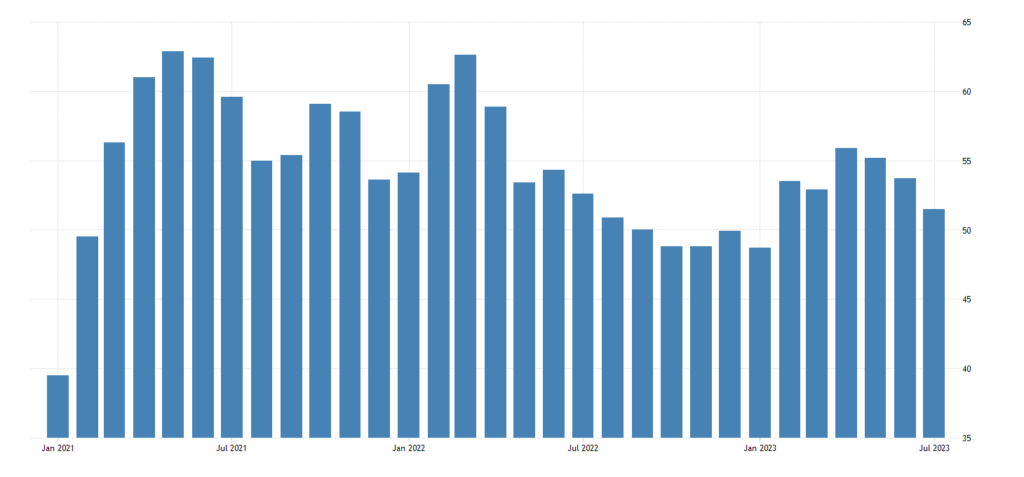

In Britain, 48.7 is also the weakest value in 2.5 years:

Pic. 8

In Germany, 47.3 is a sharp deterioration (it was 52.3) and at least for 9 months:

Pic. 9

In the eurozone as a whole 48.3 – excluding cataclysms of covid quarantine 10-year bottom:

Pic. 10

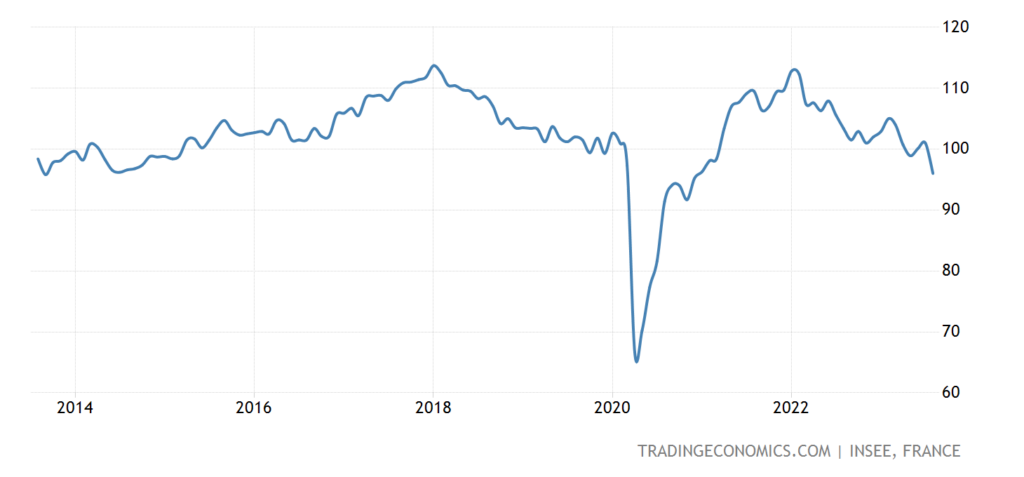

Business confidence in France is the worst in 2.5 years, and minus the covid collapse – in 10 years:

Pic. 11

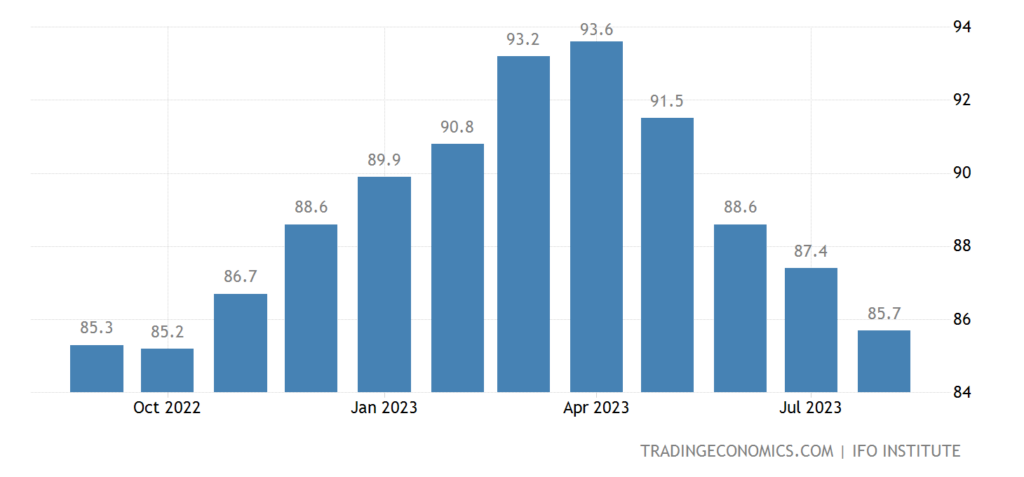

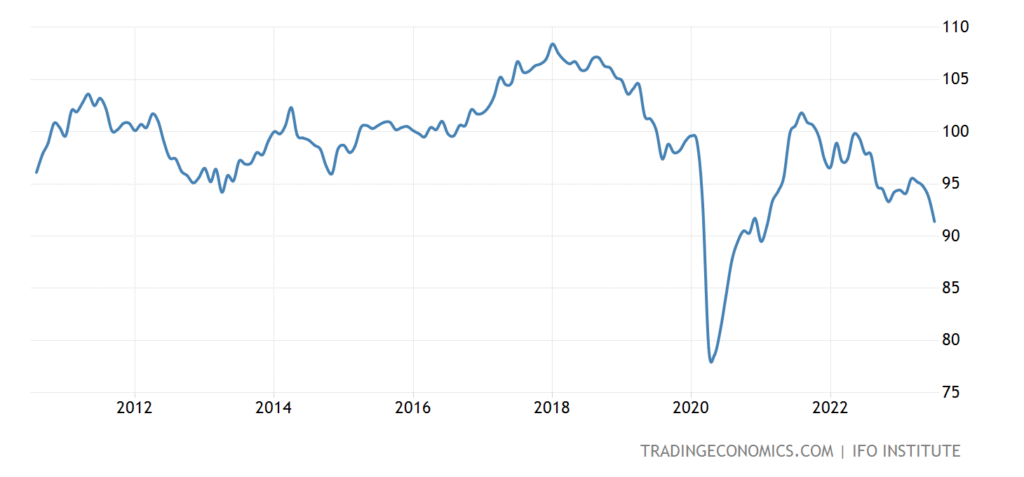

The business climate in Germany (IFO survey) continues to deteriorate:

Pic. 12

Moreover, the assessment of current conditions is the weakest in 3 years, and without taking into account the covid failure – since 2010:

Pic. 13

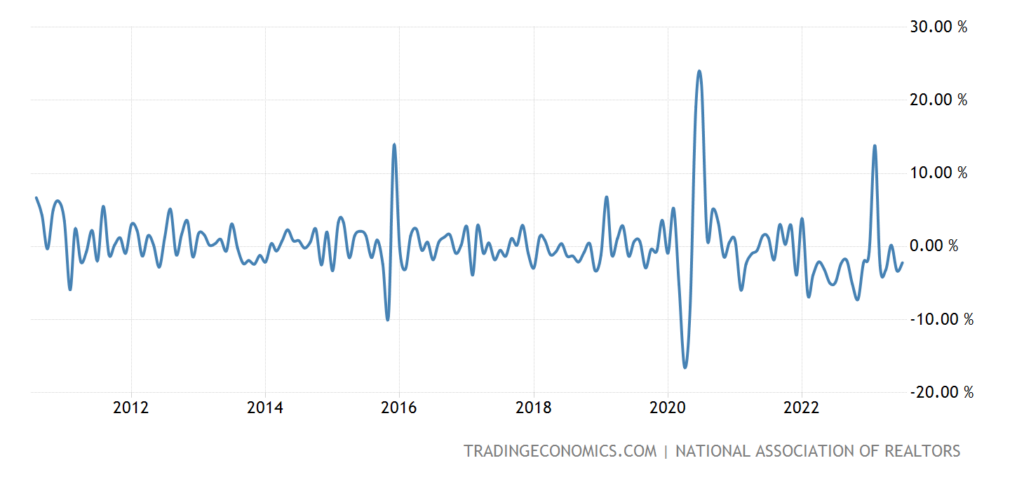

US existing home sales -2.2% m/m – 4th minus in 5 months and 16th in 18 months; sales volume is close to the worst values in 13 years:

Pic. 14

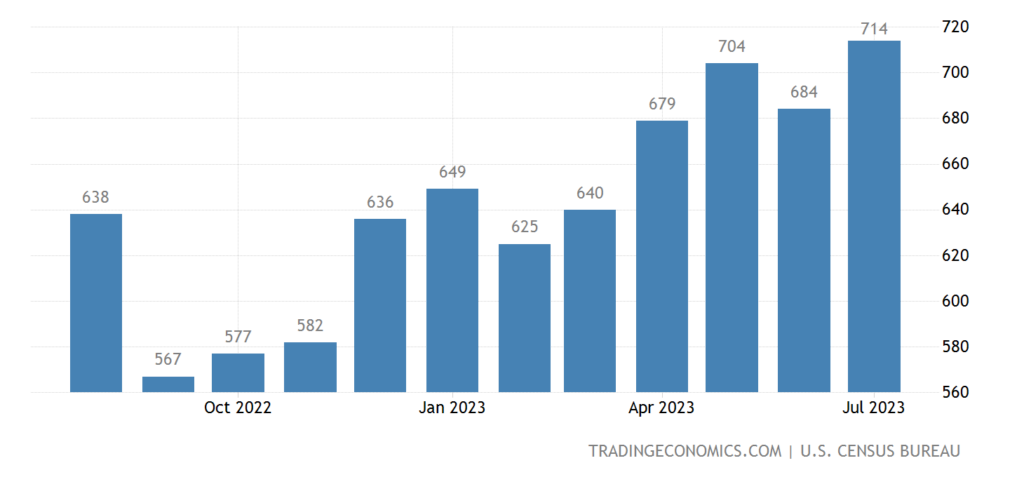

But sales of new buildings are growing – since their prices have fallen by 10% over the past year:

Pic. 15

We leave the question of what and how they sell for now outside the brackets, this is not quite macroeconomics.

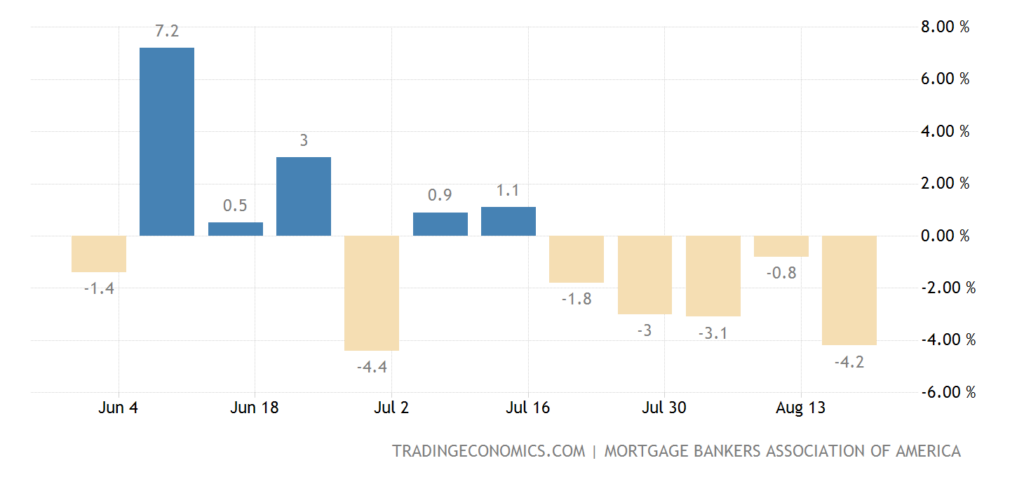

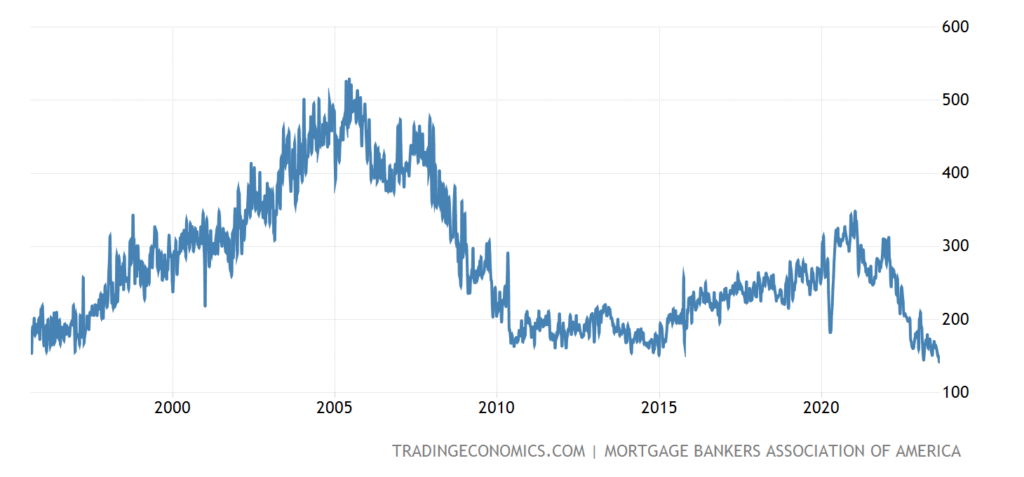

Mortgage applications in the US -4.2% per week – 5th negative in a row:

Pic. 16

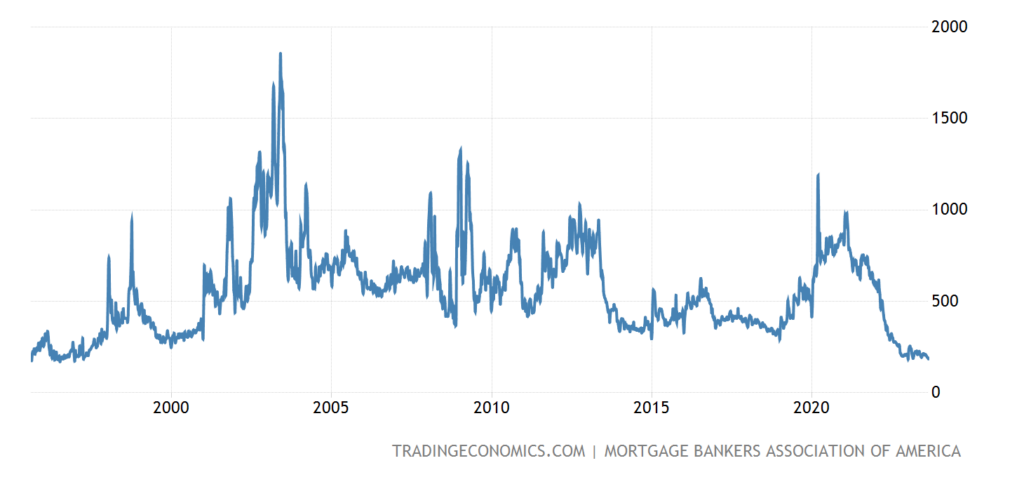

To the worst level since April 1995:

Pic. 17

The same 28-year minimum and separately for loans for the purchase of housing (not refinancing):

Pic. 18

The loan rate is to blame – it has been at its peak since 2000 (up to 7.31% on 30-year loans):

Pic. 19

The same picture for Freddie Mac mortgages (7.23%, top since 2001):

Pic. 20

In reality, this means a decline in the standard of living of the population. While not very significant, but the trend is evident.

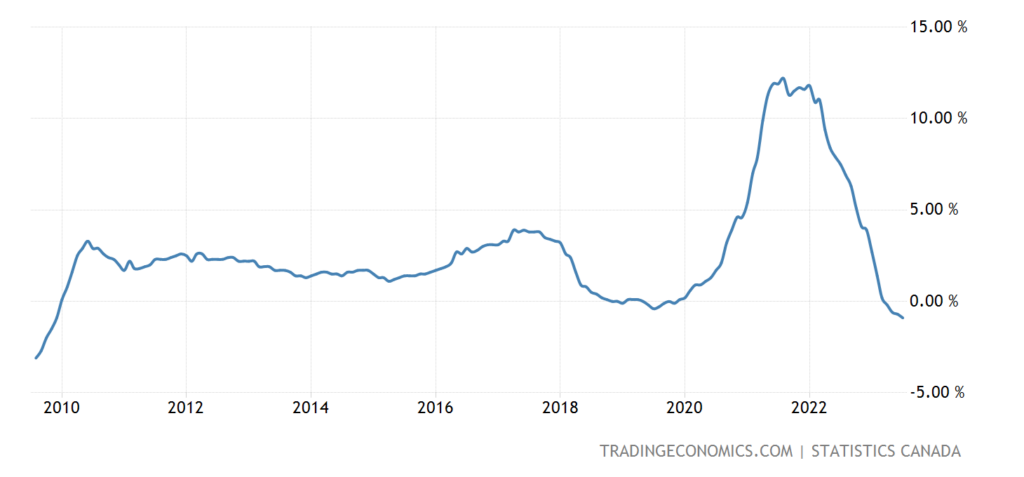

New home prices in Canada -0.9% per year – bottom since 2009:

Pic. 21

CPI (Consumer Inflation Index) without food and fuel in Tokyo Prefecture +2.6% per year – 30-year high:

Pic. 22

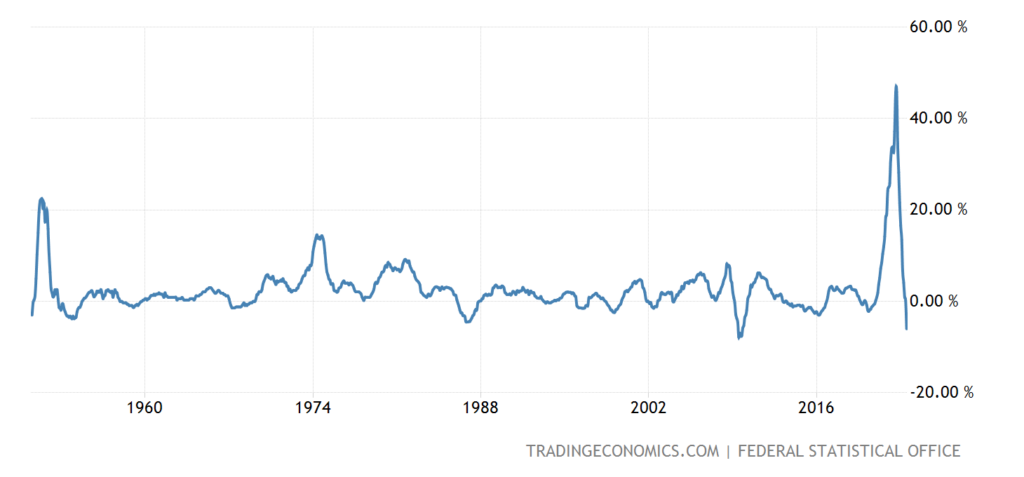

PPI (industrial inflation index) Germany -6.0% per year – not counting the failure of 2020, this is the minimum since March 1950 (and then it was only -6.1%):

Pic. 23

PPI Spain -8.4% per year – over 58 years of observation, it was lower only once, in May 2020 (-8.8%):

Pic. 24

Severe deflation, a sign of industrial decline.

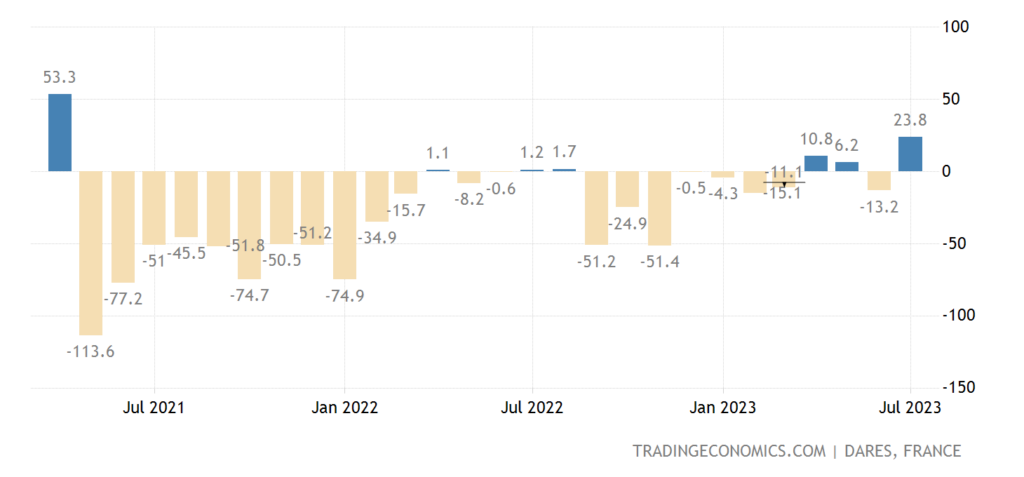

The number of registered unemployed in France grew at the fastest pace in 27 months:

Pic. 25

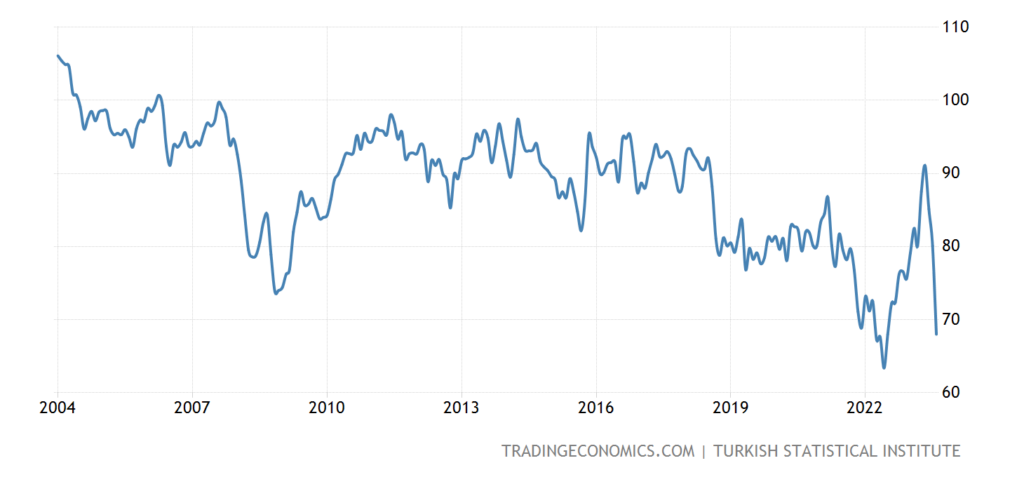

Consumer sentiment in Turkey is the worst in a year and is near record pessimism:

Pic. 26

Given the increase in rates (see below), a completely natural phenomenon.

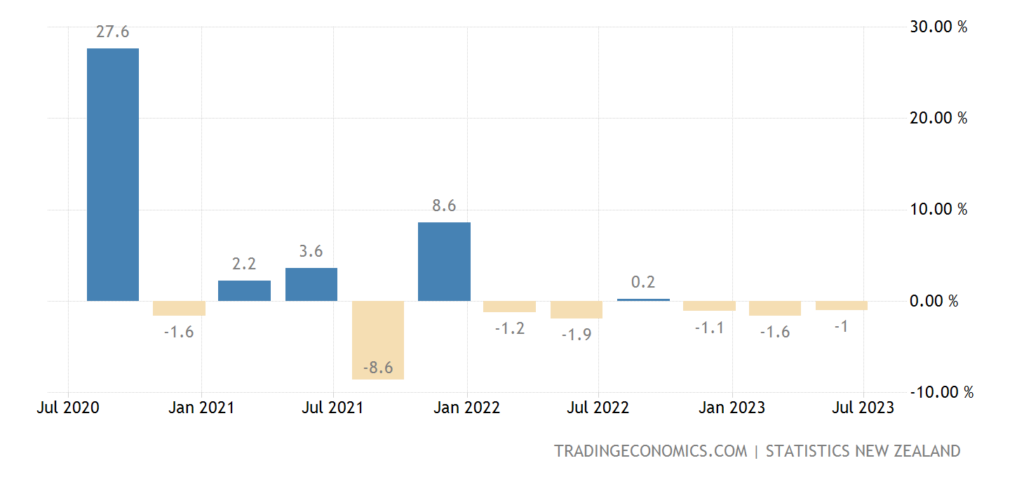

New Zealand Retail Sales -1.1% QoQ – 3rd straight loss:

Pic. 27

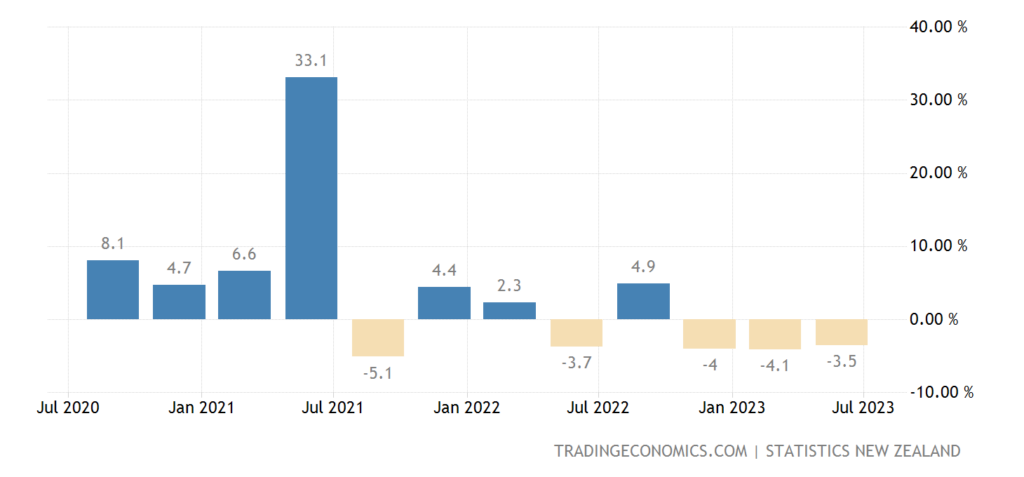

And -3.5% per year – also the 3rd consecutive quarter in the red:

Pic. 28

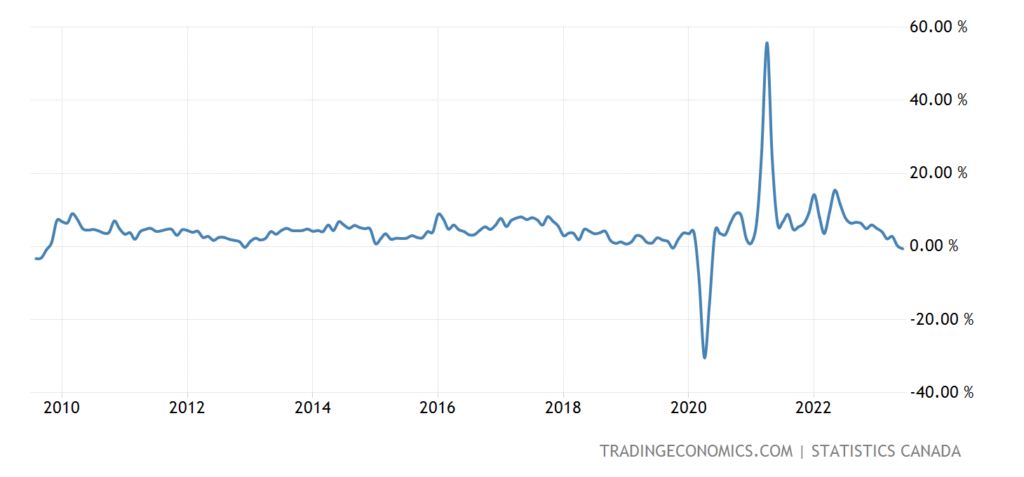

Canadian retail -0.6% per year – 1st minus since May 2020, and before that – since 2009:

Pic. 29

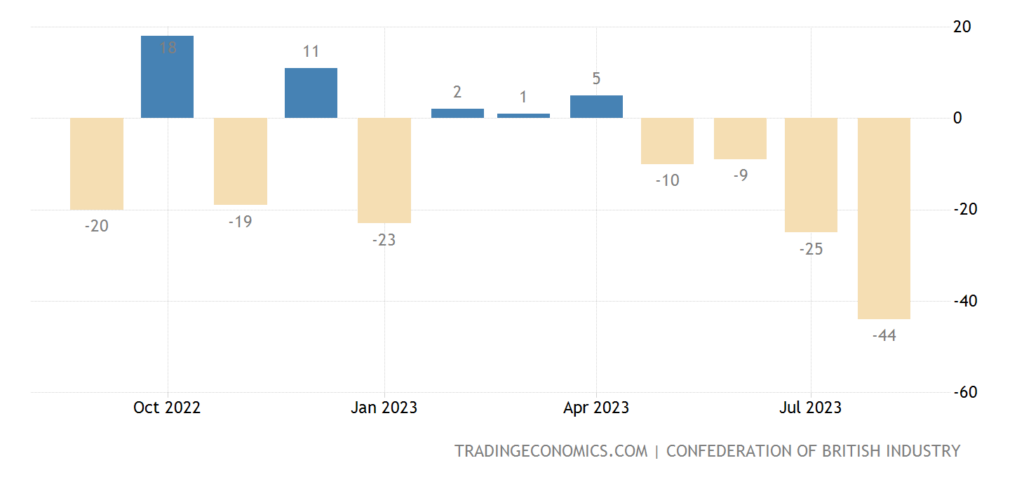

UK retail balance (-44%) (calculated by the Confederation of British Manufacturers based on a survey of employees of retail and wholesale companies; a level above 0 indicates an increase in sales, below 0 – a decrease.) near record weak values:

Pic. 30

The Central Bank of China predictably cut the rate on annual loans by 0.10% to 3.45% – but unexpectedly left it unchanged for 5-year loans (to which mortgages are tied).

The Central Bank of South Korea did not change its monetary policy, as did the Central Bank of Indonesia.

The Turkish Central Bank raised the rate by 7.5% to 25.0%, the highest in almost 20 years.

Main conclusions. Theses from Powell’s speech at Jackson Hole:

- we are ready to further raise rates, if necessary;

- we will act “cautiously” in tightening monetary policy;

- 2 months of good macro data is only the beginning to start seeing clear signs of a steady decline in inflation;

- The Fed will not change the inflation target of 2%;

- economic growth above the trend may lead to a further increase in the rate;

- some progress in service sector inflation is needed;

- rates will remain restrictive until we see a steady decline in inflation towards the target;

- The Fed is not sure about the understanding of the neutral rate indicator;

- labor market resistance may force the Fed to move on;

- Rent in the housing market indicates a slowdown in inflation. Watching;

- we will act cautiously in the context of “raising the rate further” or “leaving the rate at the current level”;

- to reduce inflation requires a period of economic growth in the US below the trend;

- it is possible that the US economy has not yet fully taken into account the increase in rates in the past (that is, the time lag of the impact of the rate on inflation is unknown).

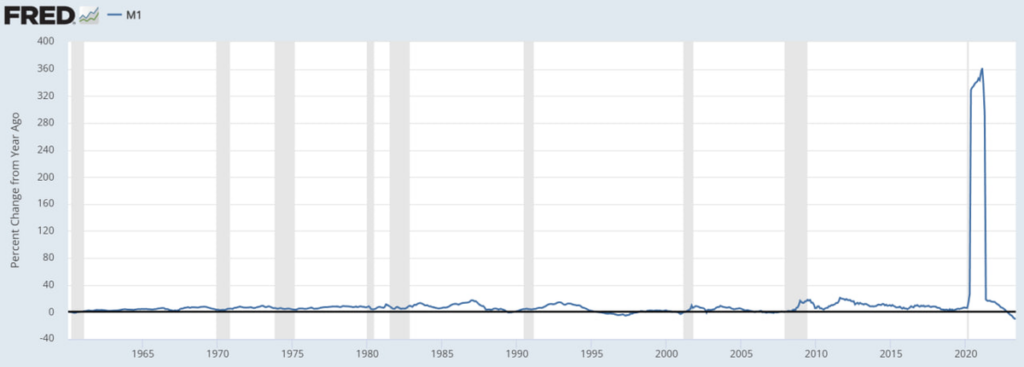

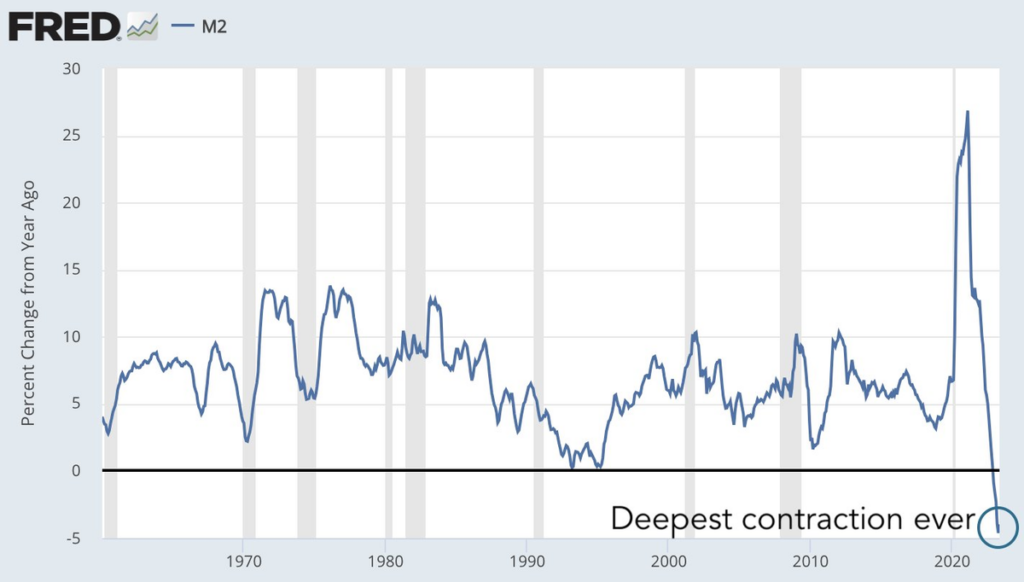

What is Powell so afraid of? But the fact is that he very actively reduced the money supply, both cash and extended:

The decline in consumer inflation is evident, although it is higher than the levels desired by the Fed management. But another misfortune came out, the industrial recession, which we have been describing for several months now. And a natural question arises: if even now consumer inflation is above the norm, then what will happen to it if actions are taken to stimulate production?

But if the industry falls, then the general level of wages, that is, the standard of living, also falls (I remind you that elections are just around the corner!). And we see the results, including real estate sales and demand for mortgages. What to do here? And if the BRICS countries (GDP which is already significantly higher than the G7 countries) start real actions to create an alternative monetary system, what should be done?

It should be noted that all this is happening against the backdrop of a structural recession, which has clearly manifested itself in recent weeks in the European Union. So it’s understandable why Powell is nervous. But our readers do not need to be nervous at all, they can calmly go on vacation and continue their work, since the picture of the world is clear to them!