Period: 30 August – 4 September 2020

Main events. Two major events this week.

The first is the dramatic deterioration of the political situation in the world and in the United States: the announcement by Angela Merkel of the poisoning of the leading opposition in Russia, Alexei Navalny, and the announcement by US Secretary of State Pompeo of sanctions against the prosecutor of the International Criminal Court, Fatou Bensouda, increasing civil strife in the US, and much more.

This may be due to Donald Trump’s increased popularity during the campaign, but it is bound to raise savings amid rising public anxiety (i.e., lower spending, and thus GDP). It will also increase the need for law and order, which is the main message of the Trump campaign.

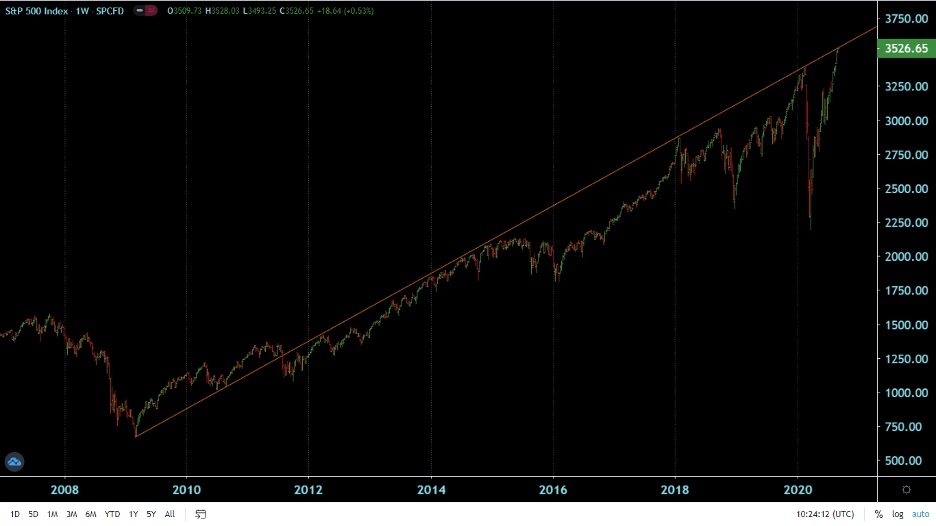

Second, global trends in the stock market and the United States dollar have changed. The S&P index at the beginning of the week reached its key line that has been seen since 2009, the crisis year. According to technical analysis (which rarely gives the wrong result in such situations), this means that over time the market should come to the same values that were at the beginning of the trend.

That is, to the level below 800.

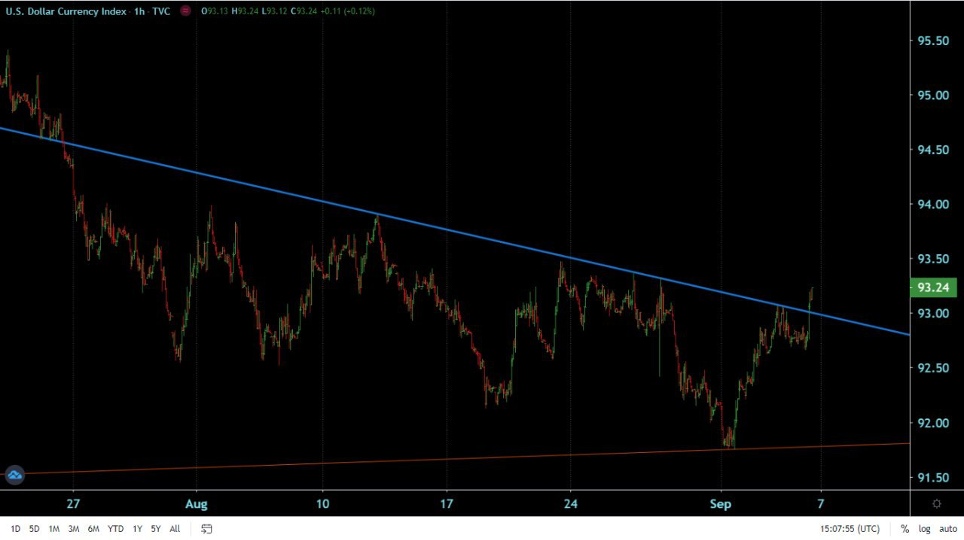

The dollar index broke up the long-term trend line and began to rise. This is consistent with the fundamental principle that the most liquid assets are maximized in times of crisis.

The excess of dollars in this situation does not matter, inflationary processes will manifest themselves later, already after the stock collapse. In addition, a significant part of the dollars printed by the Fed is still in the accounts of the US Treasury (initially – about 6 trillion), that is, in the hands of Donald Trump, and will be released during the election campaign.

Here we can additionally cite another index, the so-called «Buffet indicator». It counts as the ratio of US stock market capitalization (the Wilshire-5000 index) to GDP. It’s a record high, and it’s going to stay that way, even if it brings GDP back to the end of 2019.

Macroeconomics

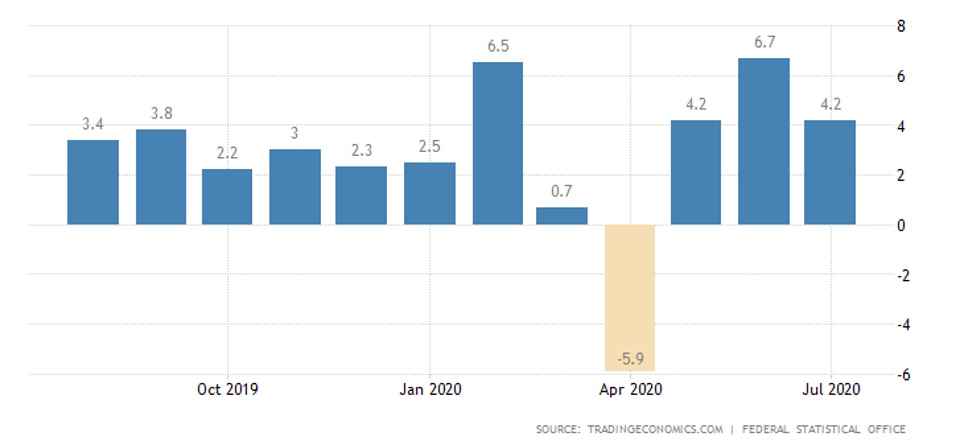

The publication of GDP figures for the second quarter of this year is continuing. Turkey’s GDP in Q2 fell by 11,0% per quarter (historical minimum) and 9,8% per year (trough since 2009); exports -35,3% per year.

Italy’s GDP -12,8% per quarter and -17,7% per year – both the worst in 60 years of observation. India’s GDP plummeted 23,9% y/y, unprecedented in 70 years of observation – well below expectations

Anti-records in Brazil, – 9,7% per quarter and -11,4% per year.

And Australia has the lowest values for 60 years of observation, -7.0% per quarter and -6.3% per year.

Industrial production in Japan surged by a record 8,0% per month in July, but the year-on-year decline has barely subsided (-16,1% after -18,2%).

Industrial orders in Germany in July grew by 2,8% per month after 28,8% in June, but the annual decline remained significant, -7,3%. In fact, this means that the rate of recovery is no longer sufficient to restore the economy to pre-quarantine levels.

The decline in Japanese building orders in July accelerated to -22,9% per year, and the number of new housing developments is also firmly in the negative -11,4% per year.

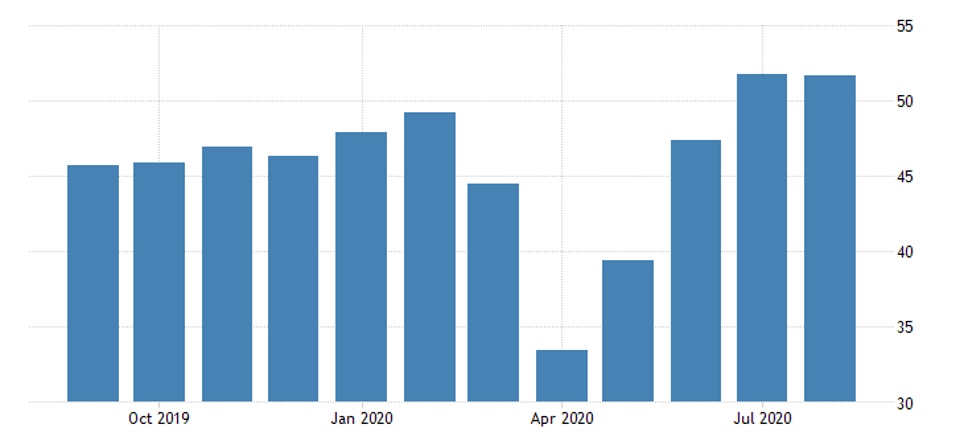

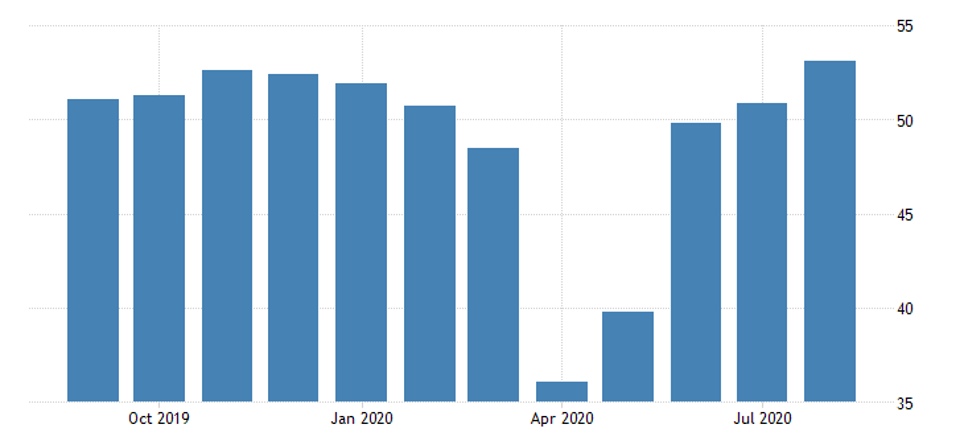

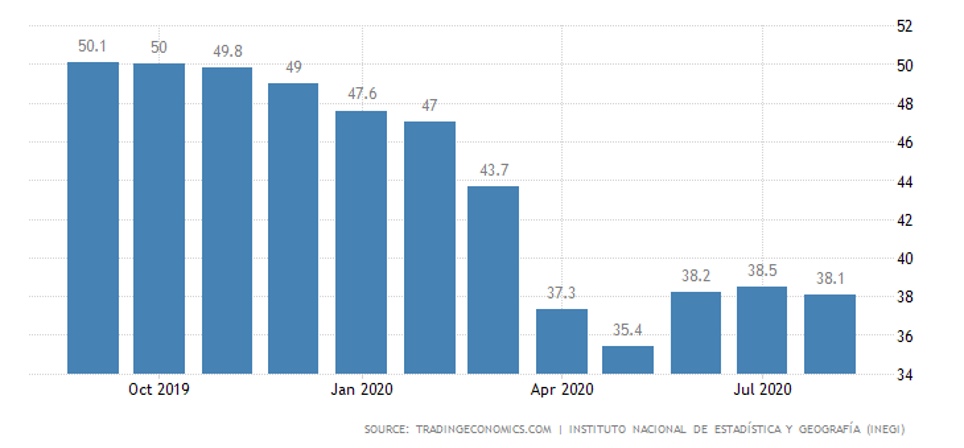

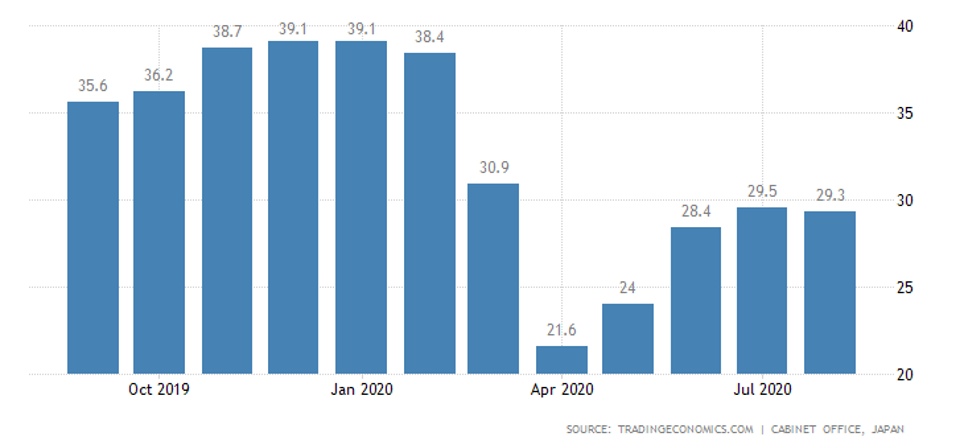

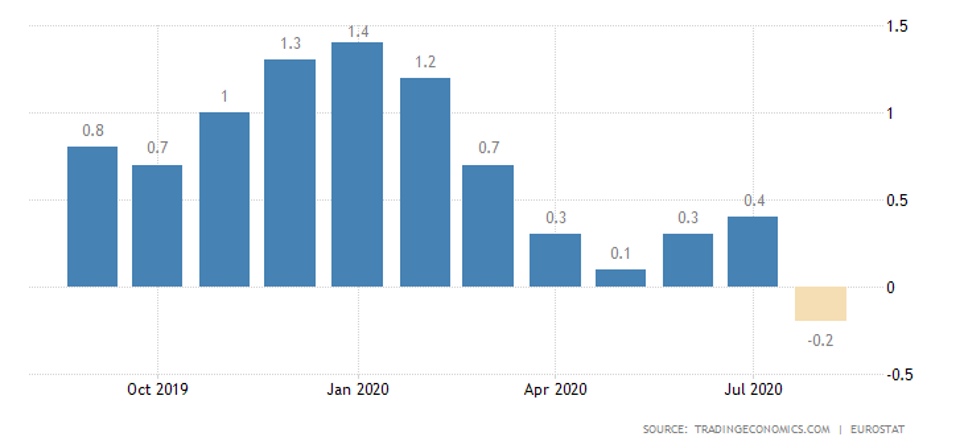

Manufacturing PMIs in most of the world either deteriorated or remained in recession in Australia, Japan, the Euro Area:

On the contrary, the improvement continues in Britain:

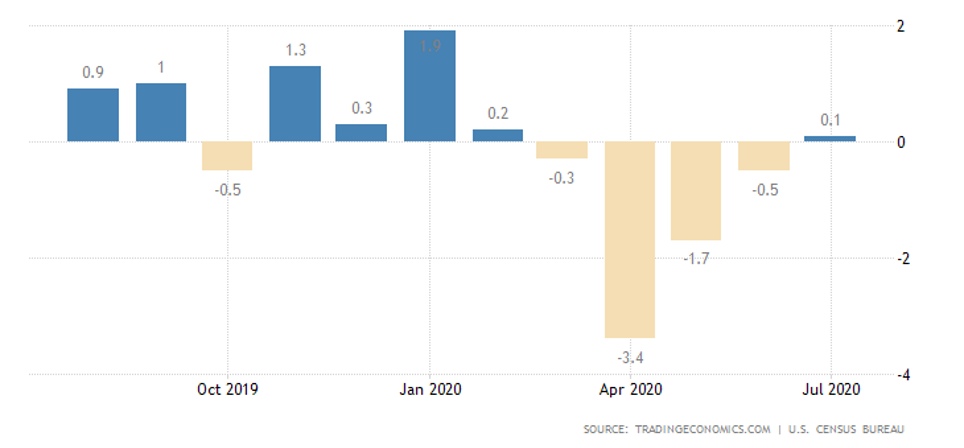

and the US:

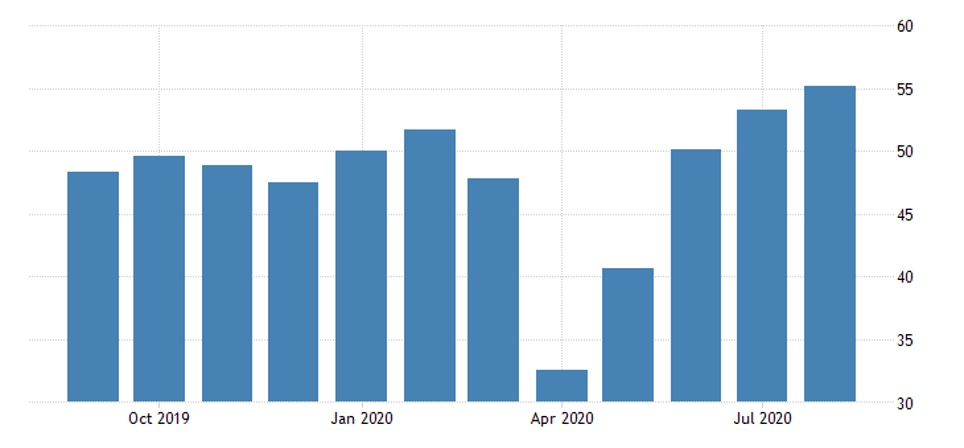

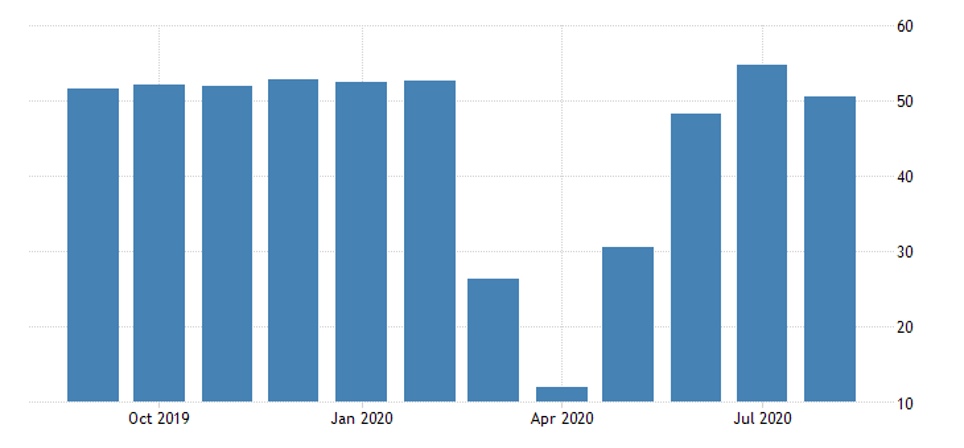

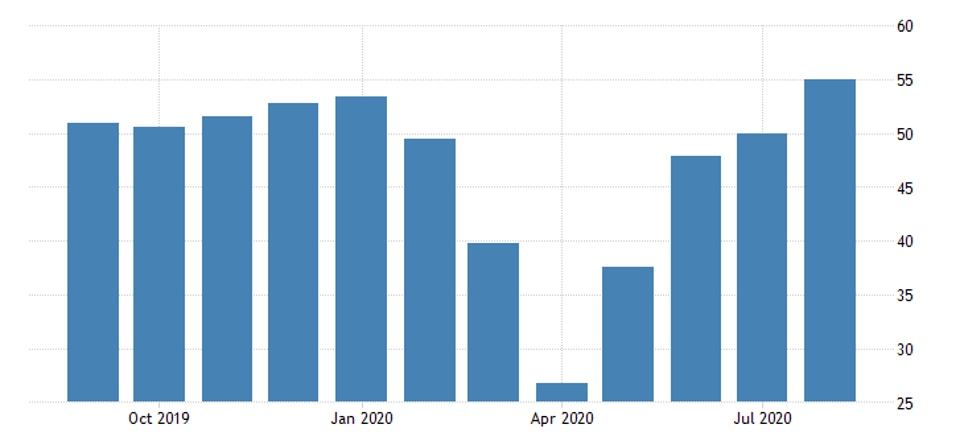

In the service sector, the picture is similar. Australia, Japan and the Euro Area are worse off than they were the previous month. Spain and Italy are in recession, while growth in France and Germany has slowed sharply:

But as with industry, the improvement continues in Britain and in the USA:

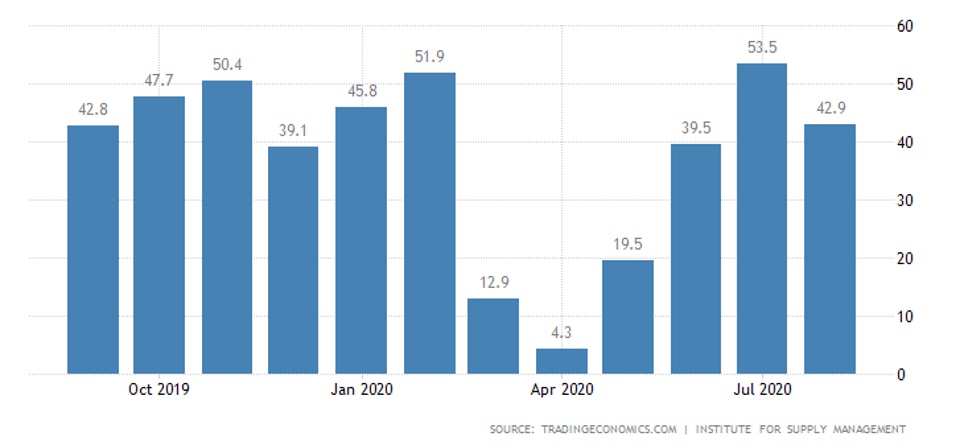

But New York’s PMI suddenly returned to a recession:

Business confidence in New Zealand fell to its lowest levels in mid-spring in August and Mexico’s also deteriorating:

Japanese consumer sentiments began to deteriorate again in August:

Italy’s CPI recession picked up to 0.5% per year in August – only 0.1% higher than the historical lows of 58 years, a similar picture for the Euro Area as a whole:

Construction spending in the US is slowly recovering – especially in the non-residential sector:

The South Korean retail market slumped by 6,0% per month in July, which made the annual growth shrink from 6,3% to 0,5%. A similar picture in Japan – but there has already returned to the annual decline (-3,3% per month and -2,8% per year).

In Germany, monthly negative values in June and July, annual growth is decreasing:

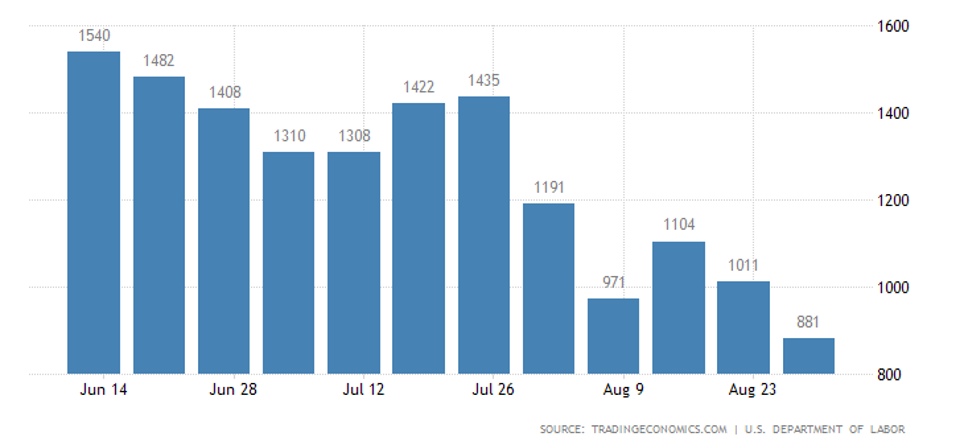

The weekly number of applications for unemployment benefits in the United States declined only because of the new methodology by the Department of Labor, which dramatically increased the seasonal clearance rates:

From the report of the Ministry of Labor it follows that without seasonal clearance, the number of applications increased and the total number of beneficiaries jumped by 2,2 million. up to 29,2 million.

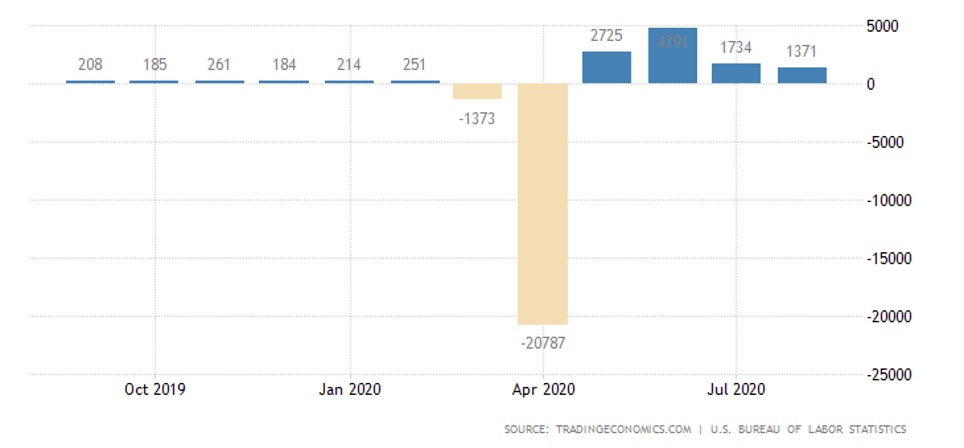

According to ADP, jobs in the private sector were 2,3 times less than expected in August, but the Ministry of Labour claims that the actual figure is 2,5 times higher. Overall, according to data from the Ministry of Labour on the economy, there are many new jobs:

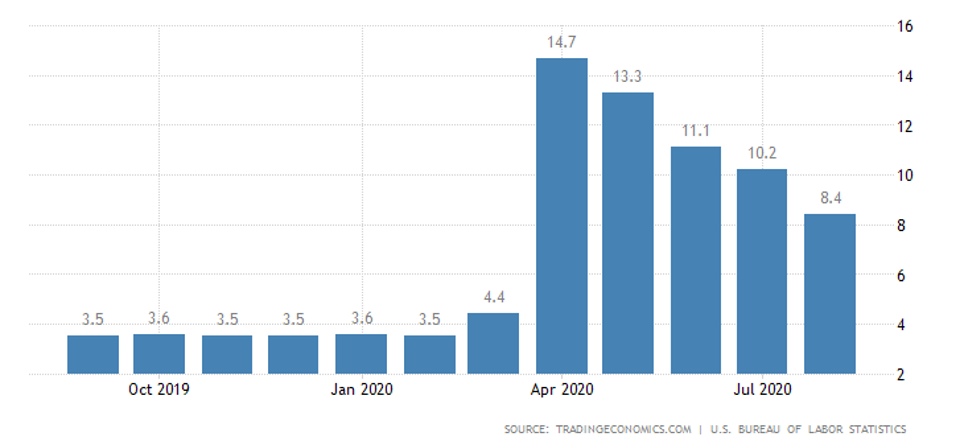

And unemployment is supposedly falling:

All this is not confirmed – just innovative statistical technologies conquer reality.

The Central Bank of Australia did not change rates, but extended the bank lending program until the summer of 2021.

Summary. Autumn has come into its rightful place, but the summer figures do not give the slightest reason to draw optimistic conclusions about the beginning of economic growth.

Compensatory growth is stalling (and in some cases stagnant), and current trends in the stock market, if they continue, suggest an inevitable return to recession. Let us recall that this is precisely the increase in the value of collateralized assets, which strongly supports the investment process.

It should be noted that we mean exactly objective macroeconomic data, since economic theory says that a structural crisis has begun, which will prevent economic growth from starting until the structural imbalances in the world economy are corrected.

At the same time, data from labour statistics in the United States show that the authorities (in reality – of all countries of the world, including Russia) are more than concealing the real picture from citizens who cannot independently carry out an objective analysis of current trends. It is for this reason that adequate reviews of current developments are beginning to play such an important role.