Period: 11 – 17 July 2020

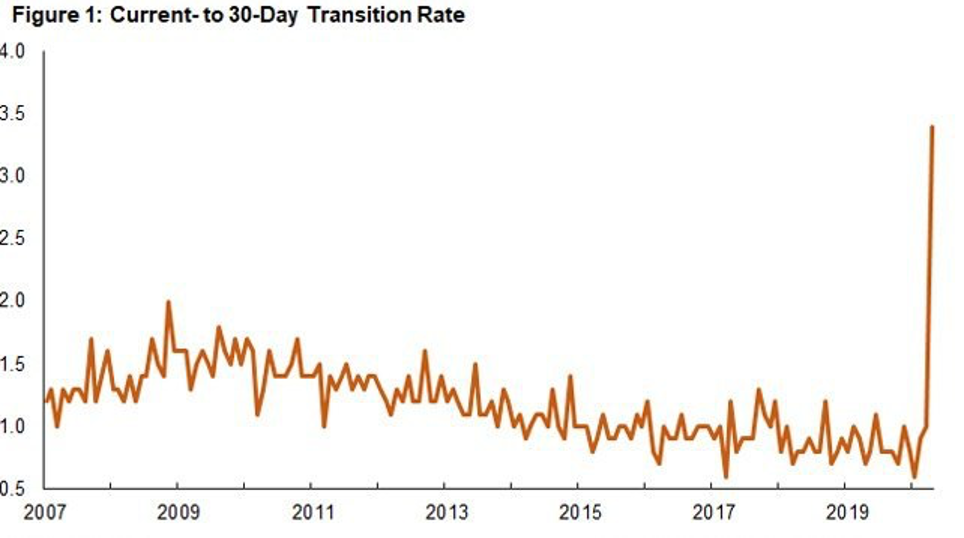

Top news story: «Loan Performance Insights Report» report on overdue mortgage payments in the U.S. for April is published. The share of mortgage loans with «less than 30 days» overdue reached 3,4% in April, the highest level in the whole period of statistics (since 1999), significantly above the previous November 2008 record of 2%. The share of mortgage loans overdue «30-59 days» in April reached 4,2%, which is also a record for the entire period of statistics. The share of mortgage loans overdue «60-89 days» and «over 90 days» remained relatively low in April (0,7% and 1,2%, respectively). The overall delinquency rate surged from 3,6% a year ago to 6,1%.

Macroeconomics

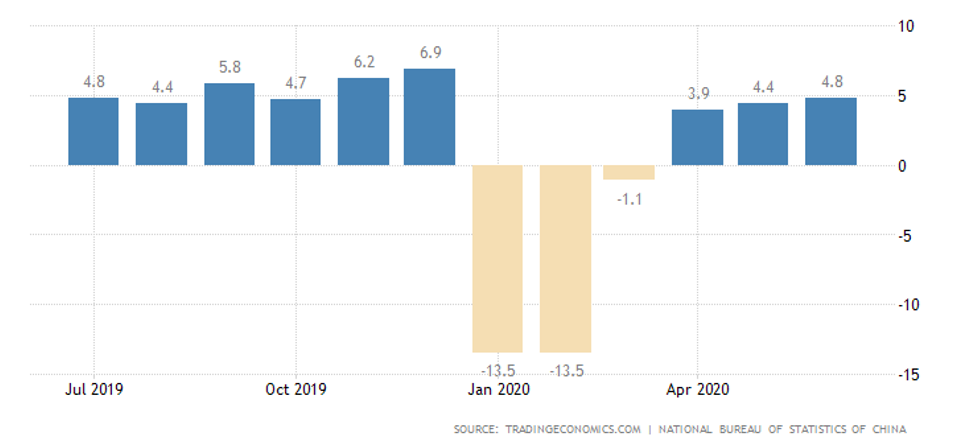

China’s GDP in Q2 surged 11,5% QOQ and 3,2% YOY. Industrial production in China is also growing, but at a slower pace:

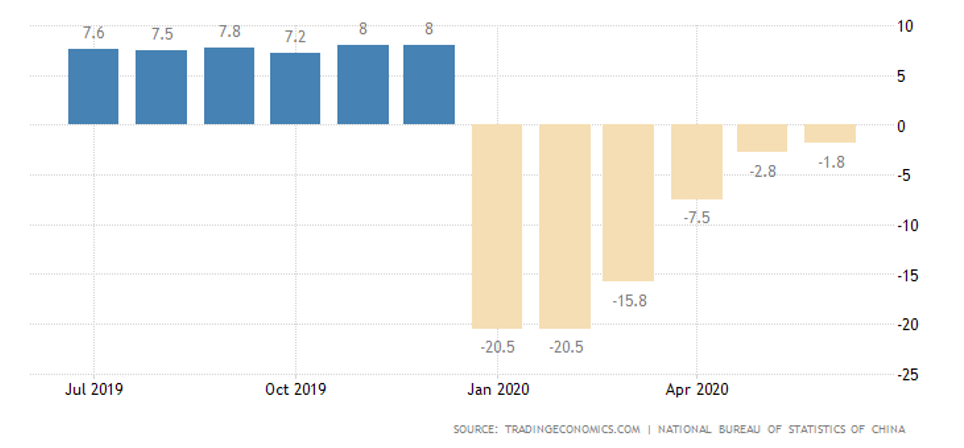

Retail sales are still down:

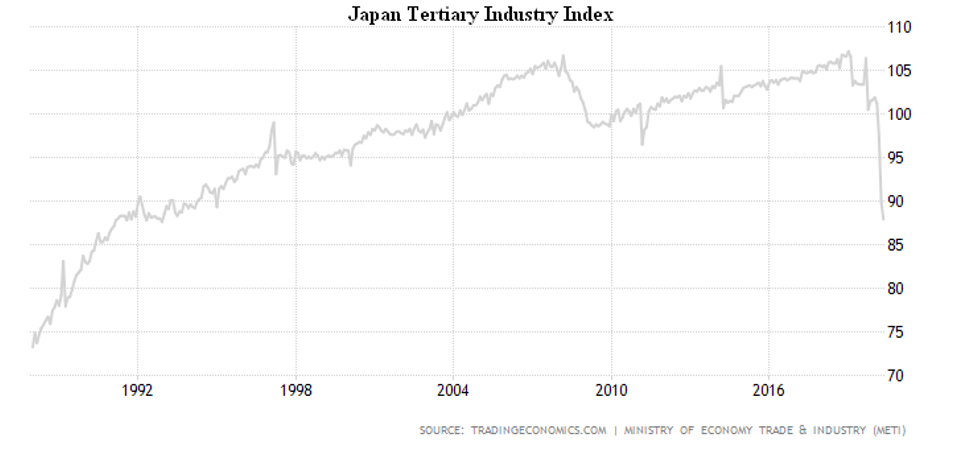

Japan’s services activity in May fell to the levels of the early 1990s:

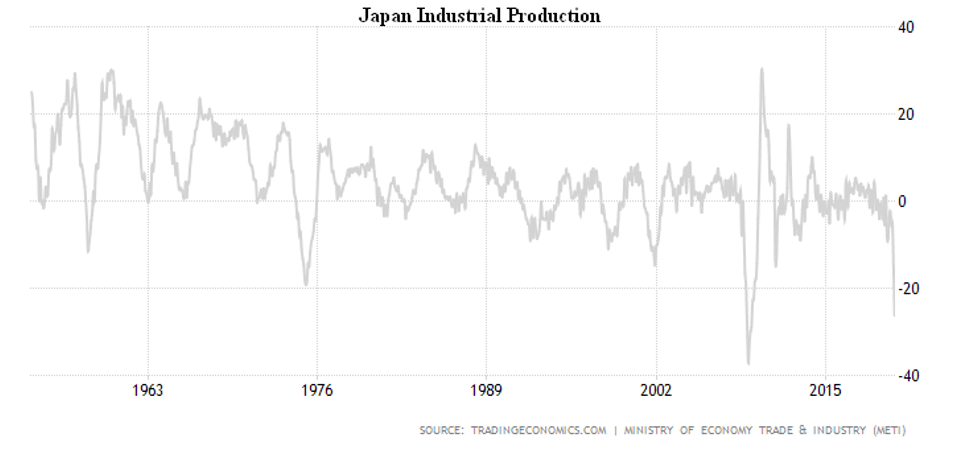

Industrial production in Japan declined 8,9% m/m in May (4th consecutive) and 26,3% Y/Y (11-year trough):

Capacity utilization (70.6%) is also the worst since 2009. The Reuters Tankan Activity Index even in July has only slightly moved from the 11-year minimum, with the rate turning negative a year ago, i.e. before the epidemic.

In the eurozone, output in the industry soared by 12,4% in May (in contrast to the expected 15%) and fell by 20,9% per year.

In Britain, industrial production grew by 6% a month in May, but was down 20% a year. This is also the case for the manufacturing industry (8,4% per month and 22,8% per year). The construction industry was very poor, at 39,7% per year.

For GDP in May, the pattern was the same: 1,8% per month (against the expected 5,5%) after -20,3% in April; -24,0% per year after -25,3%. The 3-month average (March-May) fell to an unprecedented -19,1% per year. British weekly wages dropped by 0,3% a year between March and May – the lowest since 2009.

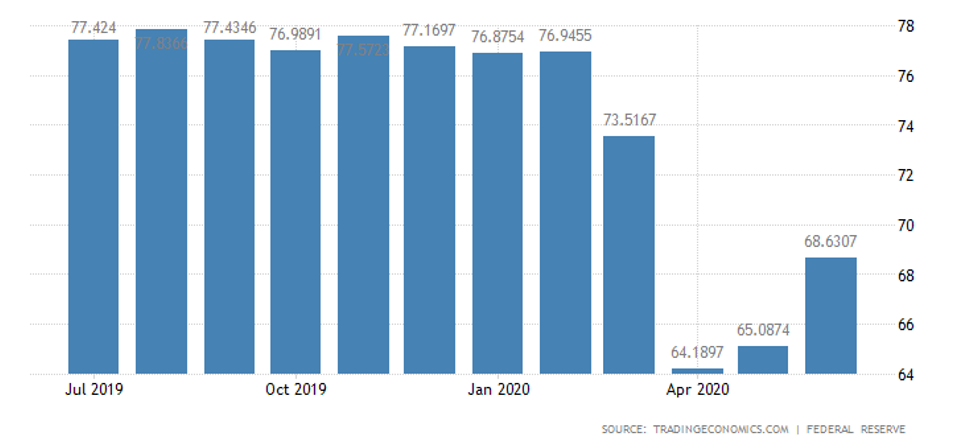

In the US in June, industrial production surged by 5,4% per month (a 60-year peak), but remained in the red by 10,8% per year and 11,1% per February 2020; for a total of Q2. The drop in output was 10,65% (-42,6% annualized), unseen since 1946/47. A similar picture of capacity utilization:

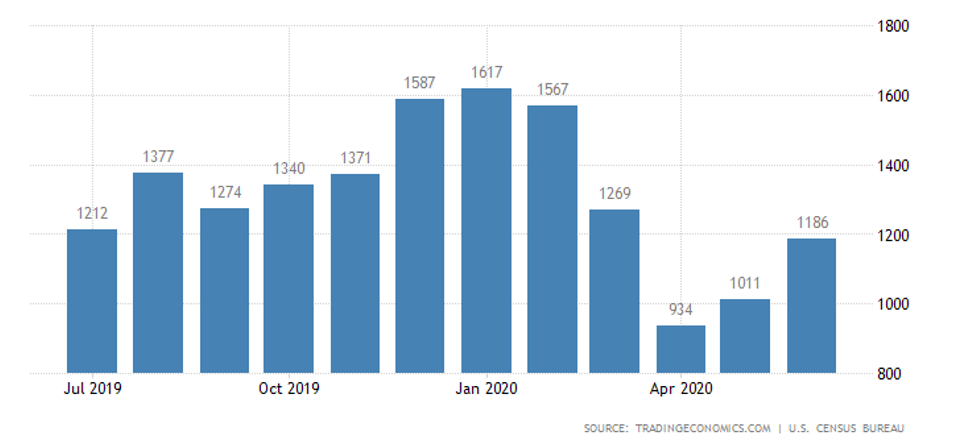

Construction performance in the US continues to improve, but slowly, to winter peaks far away:

The US CPI surged by an 11-year record 0,6% per month in June, and by the same amount per year due to the rise in gasoline prices by 12,3% per month. Food prices are also soaring – an average of 4,5% per year, the highest since 2011. Without food and gasoline, the situation is stable: 1,2% per year (9-year low).

Retail prices in the United States in June increased by a further 7,5% m/m and went into an annual plus (by 1,1%, excluding inflation).

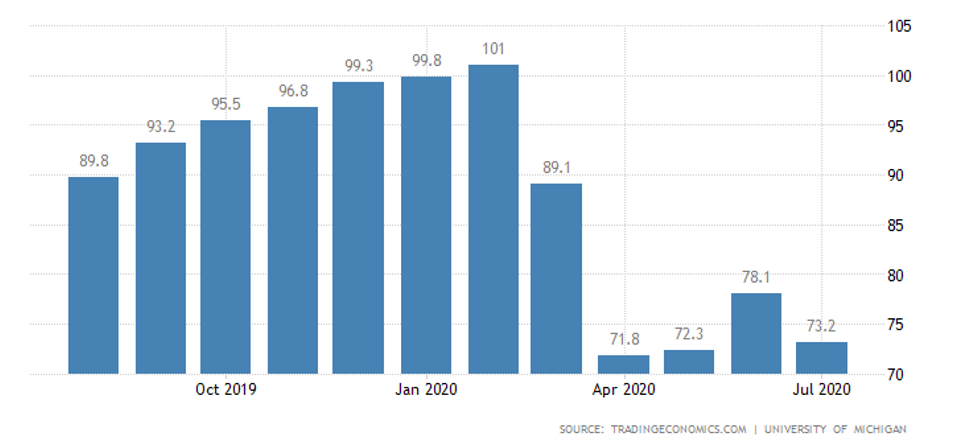

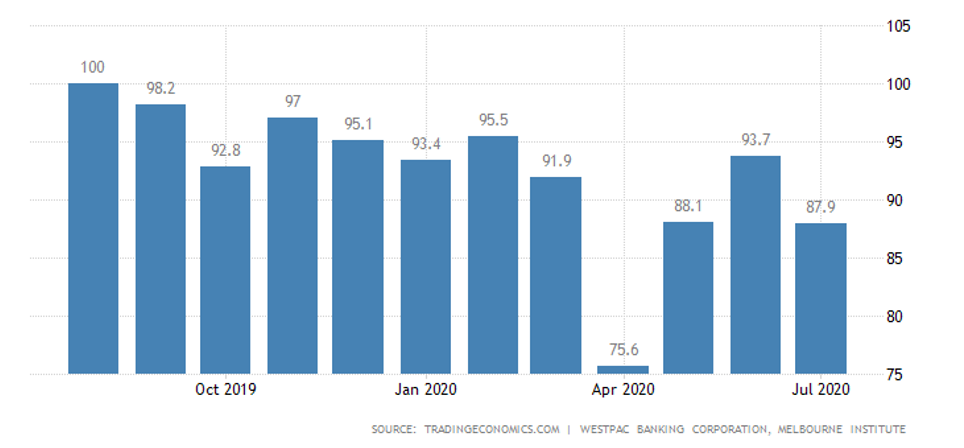

American sentiment suddenly deteriorated significantly in July:

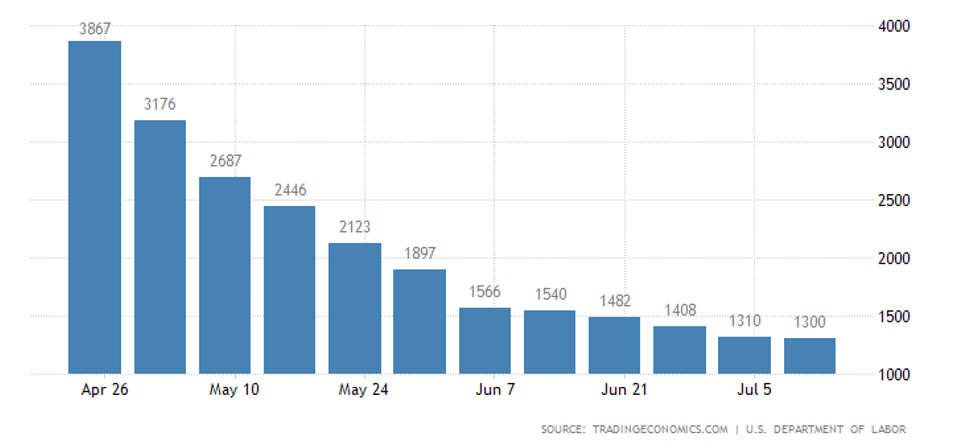

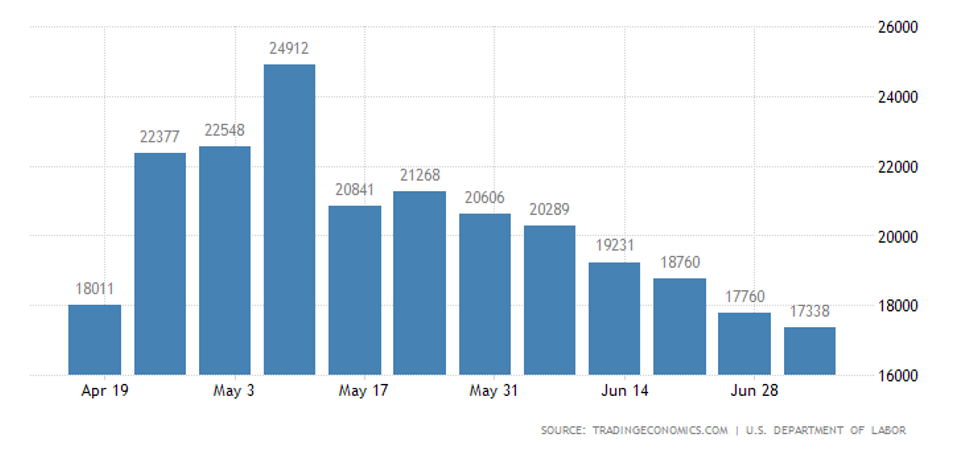

In the US, the number of primary and secondary applications for unemployment benefits continues to decline:

According to a press release issued by the Ministry of Labour, the total number of recipients of unemployment benefits is twice as high as the regular number due to emergency programmes.

Australian unemployment rose to its highest since 1998 in June, and a new deterioration in Australian sentiment in July reversed all June improvements:

Indonesia’s CB cut the interest rate by 0,25% to a record low of 4,00% and expanded bond purchases

The ECB, anticipating the course of events, has made no difference.

The Bank of Japan expects GDP to fall by 4.5-5.7% in 2020, its monetary policy has remained the same.

The same for the Central Bank of Canada, only a 7.8% drop in GDP is expected.

Same thing at the South Korean Central Bank.

Summary: The global economy continues to recover, but is too slow to reverse the spring recession by autumn. This is also natural: many data, particularly from the US, suggest that a structural recession is beginning. It will, of course, proceed at a slower pace than the collapse caused by quarantine activities, but will be more protracted.

In general, the following analogy can be found today: if an epidemic had started in the United States in February 1930 and quarantined, then the recession of 1930-31 would have taken place within a few months. After that there would have been a local recovery (as now), but then the recession would have continued. The economy would have bottomed out not by the end of 1932, but by the end of 1931. The epidemic has precipitated the recession associated with the structural crisis, but its full scale is still greater. For this reason, the global recession is likely to continue in the fall of 2020, requiring all stakeholders to seriously consider a new strategy for behavior.