Period: 5 – 11 September 2020

Top news story: This week’s headline is the lack of breaking news. In fact, all the changes in the economy have naturally continued the processes that began long before today. There is no reason to invoke force majeure. All the more interesting to see what the world economy looks like in such a calm, orderly life.

Despite this stability, political tensions are mounting for understandable reasons: there are no signs of economic growth. To put it another way, the world economy is likely to be in a stable state of permanent recession. This state of affairs is fully in line with the concept of structural crisis developed by the Mikhail Khazin Foundation for Economic Research, although of course it is difficult to call it optimistic.

Macroeconomics

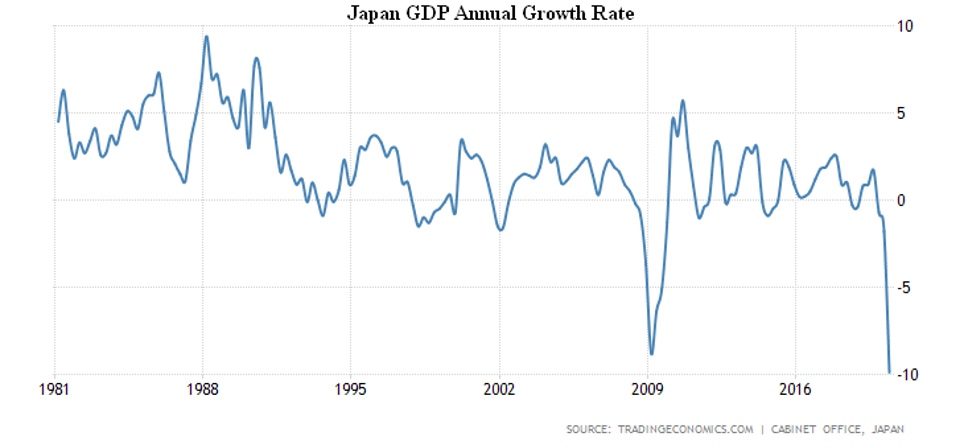

Japan’s GDP in April-June collapsed at its worst in 40 years of observation 7,9% per quarter and 9,9% per year: private demand -7,9% per quarter to 2001 levels, investment -4,7%, exports -18,5%:

Euro Area GDP in Q2 fell by a record 11,8% per quarter and 14,7% per year: private demand -12,4% and -15,9%, investments -17,0% and -21,1%, exports -18,8% and -21,5%, imports -18,0% and -20,7%:

But the most spectacular collapse in South Africa: as much as -51% per quarter. Recalling that South Africa is one of the BRICS countries.

The recovery of industrial production in Germany in July (recalling that July was the first month of the third quarter still under way) slowed sharply to -1,2% per month. The annual decline is still strong, at 10,0%:

The same is true for France (3,8% per month and -8,6% per year), Italy (7,4% per month and -8,0% per year) and Britain (5,2% per month and -7,8% per year).

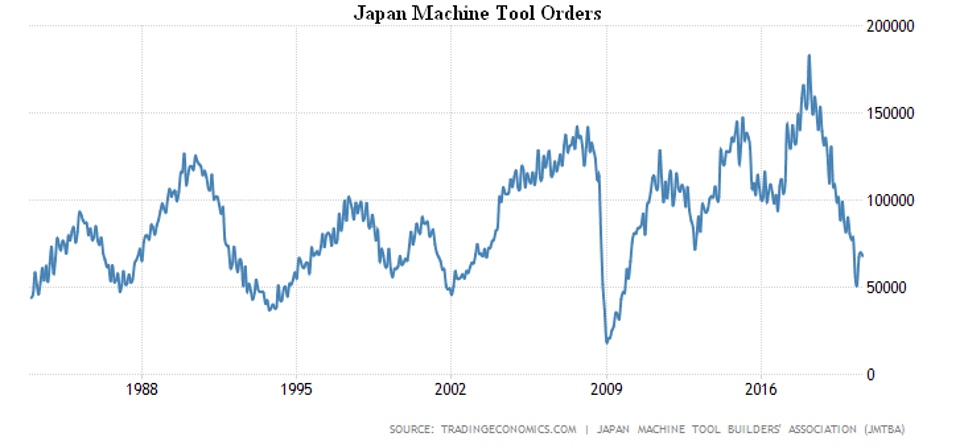

Orders for machinery and equipment in Japan slumped 2,7% per month and 23,3% per year, remaining at 1980/1990 levels:

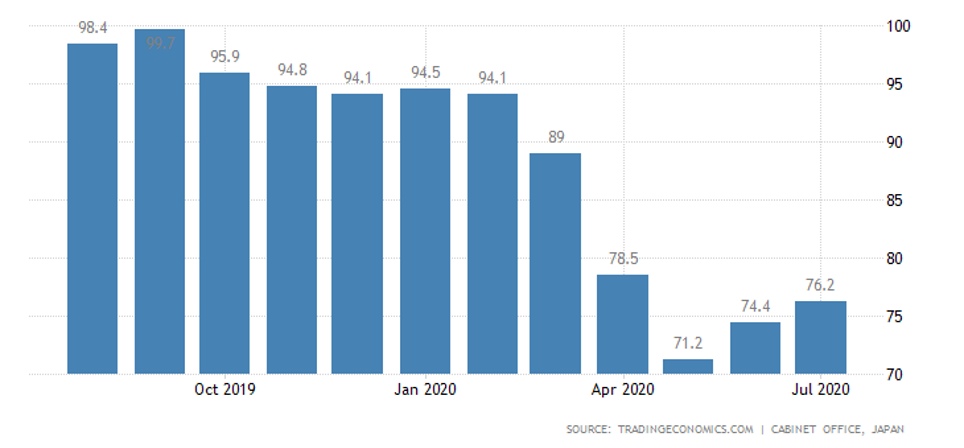

Leading indicators in Japan continue to recover, but very slowly, even worse are coincident indicators:

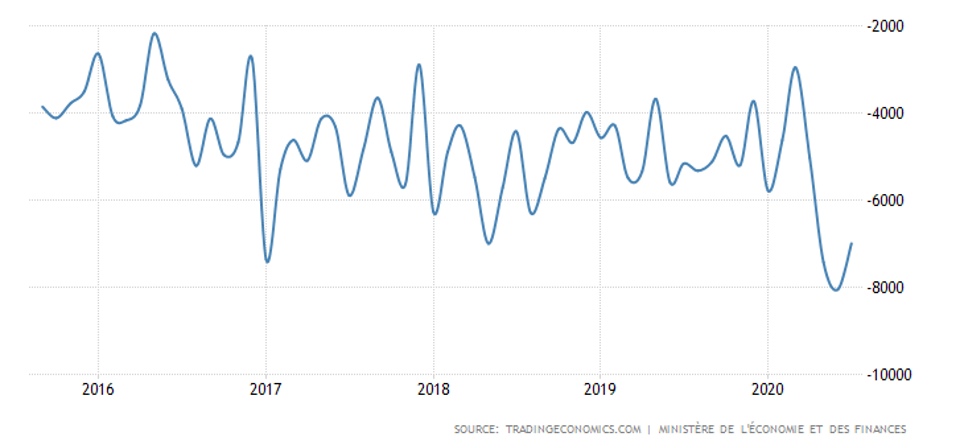

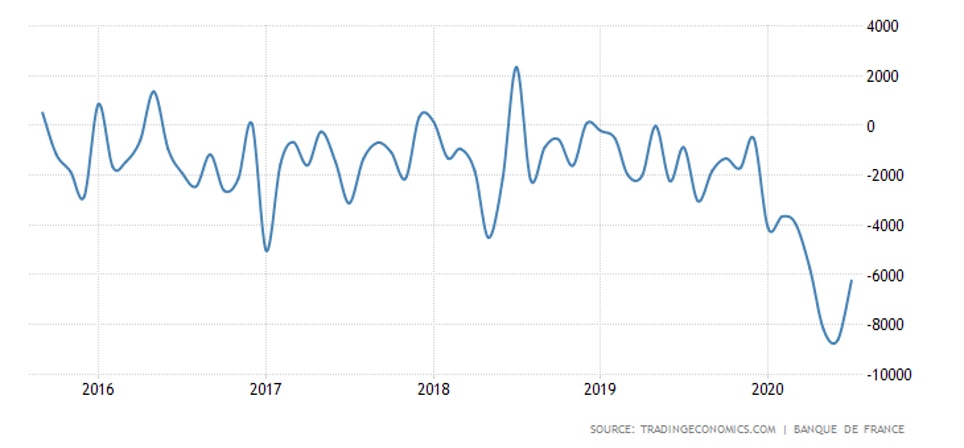

France’s trade and balance-of-payments deficit is close to record highs:

Inflation in China has declined to a minimum since March 2019 (2,4% per year), but the PPI is emerging from recession, though it is still present (-2,0% per year).

In Mexico, the CPI has peaked since May 2019 (4,05% per year).

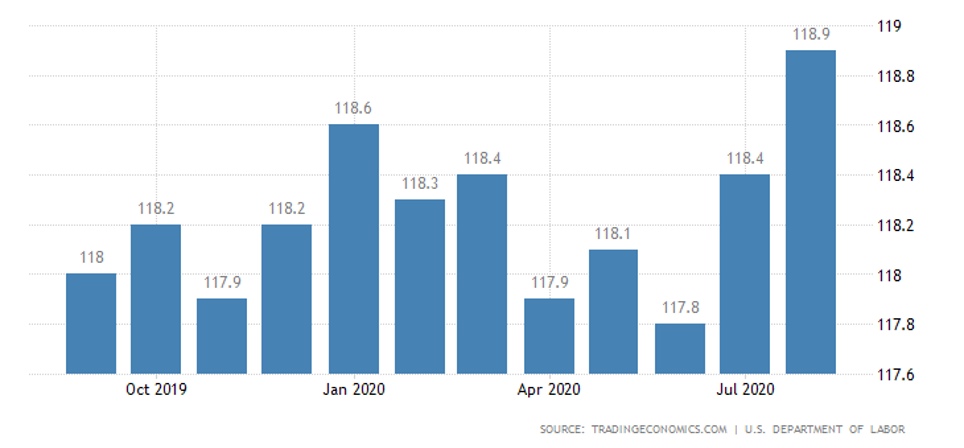

In the US, the PPI grew by 0,3% per month in August, and reduced the annual decline to 0,2%. Excluding food and fuel, prices rose by 0,4% per month and 0,6% per year, breaking the January peak. US CPI 0,4% per month and 1,3% per year – five months maximum and markedly higher than expected; second-hand car sales surged by 5,4% per month, the highest since 1969.

The US Economic Optimism Index (IBD/TIPP Survey) deteriorated again in September, because the incentives were tightening:

Australian job postings in August slowed growth to 1,6% per month, vacancies remain at -30% per year. The number of vacancies in the US clearly increased beyond expectations, but with real recruitment of personnel falling sharply:

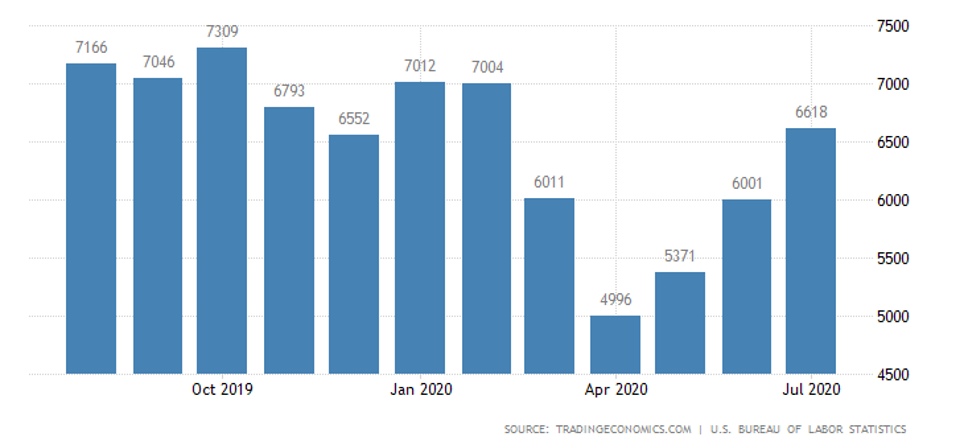

In the United States, a recent change in seasonal clearance (which we detailed in the previous issue) has resulted in relatively small weekly unemployment benefits. Without this methodology, the situation is worse – the number of applicants grows 4 weeks in a row, the number of recipients also grows, the total number of beneficiaries in all programmes has almost returned to 30 million (now 29,6 million).

Employment in France in Q2 dropped to levels at the end of 2016.

Japanese nominal incomes fell 1,3% per year in July, while real wages fell 1,6%. Real Japanese spending plummeted 6,5% a month in July, increasing the annual decline to 7,6%. The same situation with retail in Italy – in July -2,2% per month and -7,2% per year. The surge in postponed demand was short-lived.

The ECB has left monetary policy unchanged, the GDP forecast for 2020 is up from -8,7% to -8,0%, the euro growth is not alarming.

Summary: The main problems in estimating macroeconomic indicators are delays in the availability of data, with delays of different time periods. At the beginning of the survey, it appears that GDP data are now available for the second quarter. These data show that our summer estimates that recovery has been significantly weaker than desired have been correct.

At present, it makes sense to look at the unemployment situation as it reflects the current picture. The main interest is not so much its growth as the inconsistency with conventional economic models. The US situation shows that there is both an increase in supply and an increase in unemployment. In general, this discrepancy is a typical sign of a structural crisis (i.e., a change in the structure of demand and the sectoral structure of the economy). But in this case, it is possible to clarify this circumstance.

The fact is that people who lost their jobs at the beginning of the COVID-19 epidemic imagine themselves a request from employers in the «old» format. Whereas entrepreneurs see a significant change in demand, including due to a large increase in household savings, followed by a reduction in optional demand. Alternatively, aggregate demand has moved substantially closer to current needs, and purchases of new gadgets and/or unnecessary clothing are postponed for a long time.

Production, procurement, sales and related jobs of these goods (and services) are thus reduced. But current consumption is even increasing as quarantine activities are gradually completed. Accordingly, the structure of new jobs is less attractive (both in terms of working conditions and wages) than those closed at the beginning of spring. So, the parameters of the labor market are also fundamentally changing.

Note that as budget stimulus activities are reduced (which is almost inevitable after 3 November), these processes will accelerate. This will be compounded by changes in the structure of basic industries. More information about this can be found in general theoretical sources.